Brazil Sugar Confectionery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.61 Billion |

| Market Size (2026) | USD 1.72 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Brazil Sugar Confectionery Market Analysis by Mordor Intelligence

The Brazil sugar confectionery market was valued at USD 1.61 billion in 2025 and estimated at USD 1.72 billion in 2026, and is projected to reach USD 2.34 billion by 2031, expanding at a CAGR of 6.33% during 2026–2031. Market growth is driven by Brazil's strong cultural affinity for confectionery, continuous product innovation, and increasing demand for premium and functional products. The country's robust domestic sugar production supports a competitive manufacturing base, enabling manufacturers to expand product portfolios, improve production efficiency, and introduce innovative confectionery offerings. Growing urbanization and evolving consumer lifestyles are further reinforcing demand for convenient confectionery products, while digital engagement and premiumization continue to stimulate new product adoption.

Key Report Takeaways

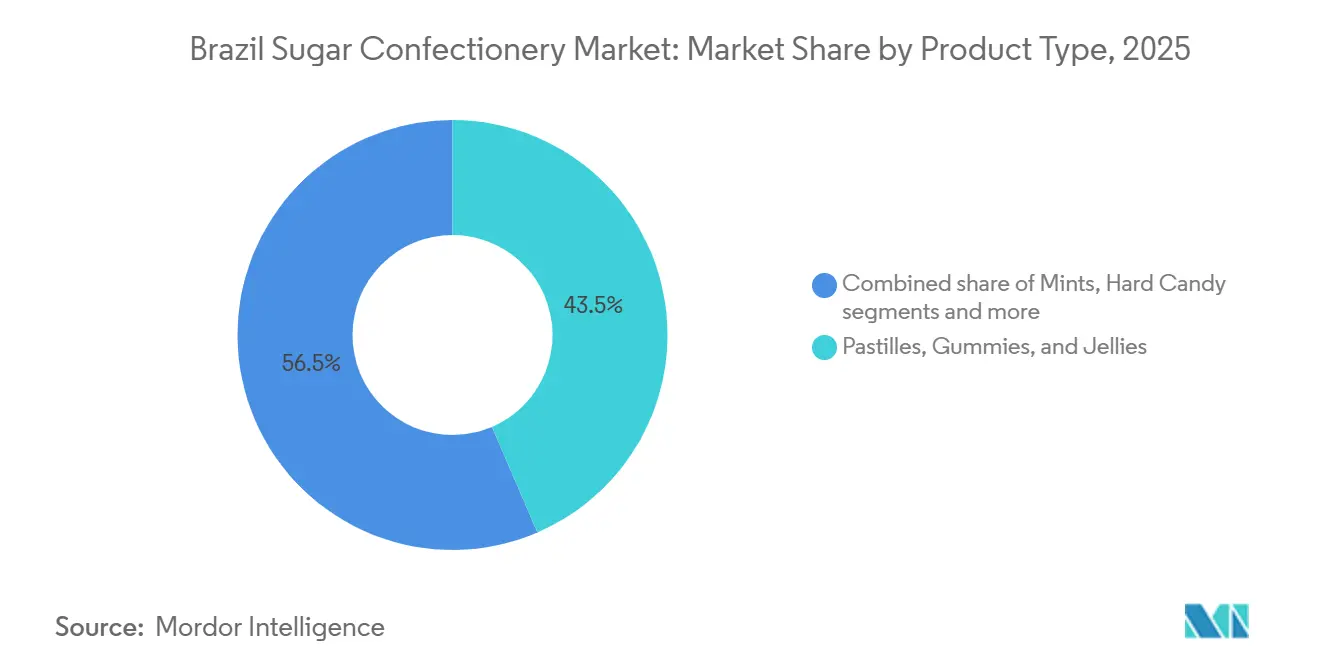

- By product type, Pastilles, Gummies, and Jellies led with a 43.54% share in 2025, while Mints are projected to grow at a 6.81% CAGR through 2031.

- By functional benefit, Novelty held a 53.32% share in 2025, while Fortified confectionery is projected to expand at a 7.23% CAGR through 2031.

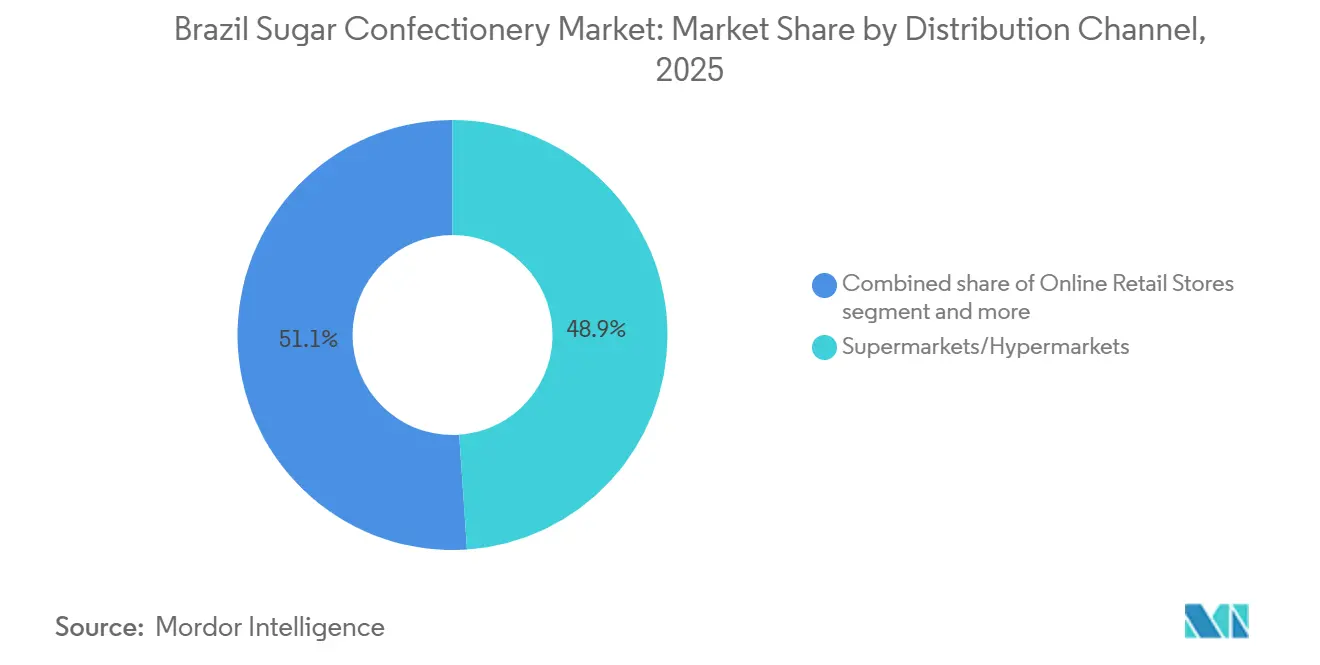

- By distribution channel, Supermarkets and Hypermarkets accounted for 48.92% of sales in 2025, while Online Retail Stores are forecast to grow at an 8.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Brazil Sugar Confectionery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cultural preference for sweet treats and traditional confectionery | +1.3% | National, with strongest intensity in Northeast and Southeast Brazil | Long term (≥ 4 years) |

| Growing urbanization and on-the-go consumption | +1.1% | National; concentrated impact in São Paulo, Rio de Janeiro, Belo Horizonte, Recife metropolitan areas | Medium term (2-4 years) |

| Domestic sugar availability and local manufacturing cost advantage | +0.8% | National; cost advantage concentrated in Center-South producing states (São Paulo, Minas Gerais, Paraná) | Short term (≤ 2 years) |

| Product innovation in flavors, textures, and formats | +1.0% | National, with premium innovation skewed toward Southeast and South urban centers | Medium term (2-4 years) |

| Demand for functional and better-for-you confectionery | +0.9% | National, with early adoption concentrated in São Paulo, Curitiba, Porto Alegre | Medium term (2-4 years) |

| Rising demand for premium and artisanal confectionery | +0.7% | Southeast and South Brazil; spill-over emerging in urban Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cultural preference for sweet treats and traditional confectionery

Brazil's cultural affinity for sweet treats and traditional confectionery is a fundamental driver of the sugar confectionery market. Candies, hard sweets, gummies, caramels, and regional sugar-based products are deeply embedded in everyday consumption habits, family gatherings, festive celebrations, and gifting traditions, supporting consistent year-round demand. This cultural attachment encourages repeat purchases across all age groups while sustaining demand for both traditional recipes and contemporary confectionery products. Manufacturers continue to build on these preferences by introducing nostalgic flavors, locally inspired formulations, seasonal collections, and premium variants that align with evolving consumer tastes. The role of confectionery in Brazil's social and cultural occasions, combined with continuous product innovation, supports sustained market growth and brand loyalty.

Growing urbanization and on-the-go consumption

Growing urbanization is transforming consumer lifestyles and driving demand for sugar confectionery in Brazil. According to the World Bank, 87.9% of Brazil's population lived in urban areas in 2024, reflecting a continued shift toward metropolitan living and faster-paced daily routines [1]Source: World Bank, "Share of urban population in Brazil", worldbank.org. Urban lifestyles have increased preference for convenient, portable food products that require no preparation, making sugar confectionery a natural fit for everyday consumption. Manufacturers are responding by developing compact packaging, portion-controlled formats, longer-lasting flavor profiles, and innovative product designs that align with evolving consumer habits. Urbanization is also increasing exposure to new product innovations, premium confectionery, and seasonal launches, encouraging higher product trial, greater brand engagement, and more frequent consumption. These structural lifestyle changes continue to support the long-term growth of Brazil's sugar confectionery market.

Domestic sugar availability and local manufacturing cost advantage

Domestic sugar availability is a key driver of the Brazil sugar confectionery market, providing manufacturers with a reliable and abundant supply of their primary raw material while supporting production efficiency and supply chain stability. According to the United States Department of Agriculture (USDA), Brazil's sugar production reached approximately 44.7 million metric tons in MY 2025/26, maintaining the country's position as the world's largest sugar producer [2]Source: United States Department of Agriculture (USDA), "Sugar production in Brazil", usda.gov. This domestic production enables confectionery manufacturers to secure consistent raw material availability, reduce reliance on imported sugar, support large-scale manufacturing, and facilitate product innovation. The strong local sugar supply also improves manufacturing competitiveness, supports operational resilience against global supply disruptions, and enables producers to meet both domestic consumption and export demand.

Product innovation in flavors, textures, and formats

Continuous product innovation in flavors, textures, and formats is a key driver of the Brazil sugar confectionery market, enabling manufacturers to sustain consumer interest and encourage repeat purchases. Companies are introducing diverse fruit-inspired flavors, sour and sweet combinations, layered and dual-texture candies, filled confectionery, chewy gummies, and novel shapes to cater to evolving taste preferences across different age groups. Innovation also extends to premium formulations, limited-edition collections, seasonal offerings, and regionally inspired flavor profiles that differentiate products in a competitive market. Advances in manufacturing technologies further enable the development of improved textures, longer-lasting flavor release, and visually appealing confectionery, helping brands strengthen consumer engagement, expand product portfolios, and drive category growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing concerns over sugar-related health issues | -0.9% | National; consumer awareness highest in Southeast urban centers (São Paulo, Curitiba) | Long term (≥ 4 years) |

| Stringent front-of-pack nutrition labeling regulations | -0.6% | National; compliance burden heaviest for mid-sized domestic manufacturers | Medium term (2-4 years) |

| Competition from healthier confectionery and sugar-free products | -0.8% | National, with greatest substitution risk in premium retail channels | Medium term (2-4 years) |

| Stringent food safety and labeling compliance requirements | -0.5% | National; INMETRO and ANVISA compliance concentrated in industrial production centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing concerns over sugar-related health issues

Growing concerns over sugar-related health issues are restraining the growth of Brazil's sugar confectionery market. Consumers are increasingly aware of the long-term health effects associated with excessive sugar consumption, including obesity, diabetes, dental health problems, and other lifestyle-related conditions. This awareness is encouraging many consumers to reduce their intake of conventional sugar confectionery and seek healthier snack alternatives or reduced-sugar products. According to the World Obesity Federation, 48% of Brazilian adults are projected to be living with obesity by 2044, while a further 27% are expected to be overweight, highlighting the scale of the public health challenge. This trend is prompting greater scrutiny of sugar content, encouraging product reformulation by manufacturers, and moderating demand for traditional high-sugar confectionery products.

Stringent front-of-pack nutrition labeling regulations

Stringent front-of-pack (FOP) nutrition labeling regulations are also restraining market growth by increasing regulatory compliance requirements and influencing consumer purchasing behavior. Brazil's mandatory front-of-pack warning labels for products high in added sugar, saturated fat, or sodium have increased transparency regarding nutritional content, prompting consumers to scrutinize product labels more closely before making purchase decisions. These regulations are compelling confectionery manufacturers to invest in product reformulation, packaging redesign, nutritional testing, and regulatory compliance, which increases development costs and extends product launch timelines. As a result, companies face greater pressure to reduce sugar content while maintaining the taste, texture, and sensory appeal expected by consumers, creating additional challenges for traditional sugar confectionery manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gummies Lead; Mints Challenge Category Convention

Pastilles, gummies, and jellies held a 43.54% share of the Brazil sugar confectionery market in 2025, making it the dominant product category. The segment's position is supported by strong consumer preference for chewy, fruit-flavored, and soft-textured confectionery suitable for both children and adults. Continuous innovation in flavor combinations, dual-texture formats, fruit juice-infused recipes, and limited-edition offerings has sustained repeat purchases. Manufacturers are also expanding vegan, gelatin-free, and reduced-sugar gummy formulations to align with evolving dietary preferences while maintaining indulgent appeal. Resealable packaging and portion-controlled packs further encourage frequent snacking and impulse purchases, reinforcing the segment's dominant market position.

Mints are the fastest-growing product segment within the Brazil sugar confectionery market, projected to expand at a 6.81% CAGR through 2031. Growth is driven by rising consumer demand for confectionery that offers both refreshment and functional benefits, including breath freshening and oral care support. Increasing adoption of sugar-free formulations, natural mint extracts, xylitol-based products, and herbal ingredients is broadening consumer acceptance among health-conscious buyers. Compact, portable packaging makes mints well suited for on-the-go consumption, while premium flavors such as spearmint, peppermint, eucalyptus, and mixed botanical blends continue to support product differentiation and category expansion.

By Functional Benefit: Novelty Anchors Volume; Fortified Captures Health Trade-Up

The Novelty segment accounted for 53.32% of the Brazil sugar confectionery market by functional benefit in 2025, making it the dominant category. This position is driven by continuous innovation in interactive confectionery formats, including shape-changing candies, surprise-filled products, themed collections, and limited-edition launches that generate consumer interest beyond taste alone. Strong demand for visually appealing confectionery, attractive packaging, and products tied to entertainment, holidays, and seasonal occasions further supports repeat purchases. The segment also benefits from its gifting appeal and ability to drive impulse buying through unique product experiences.

Fortified confectionery is projected to be the fastest-growing functional benefit segment, expanding at a CAGR of 7.23% through 2031. Growth is driven by the convergence of indulgence and wellness, as consumers increasingly seek confectionery that offers added nutritional value without compromising taste. Manufacturers are incorporating vitamins, minerals, botanicals, probiotics, collagen, and immune-supporting ingredients into candies and gummies to differentiate their products. The segment is further supported by advances in ingredient technologies that enable functional additions while maintaining desirable texture, flavor, and shelf stability, encouraging broader adoption among health-conscious consumers.

By Distribution Channel: Supermarkets Dominate Volume; Online Rewrites Impulse Logic

Supermarkets and hypermarkets accounted for 48.92% of the Brazil sugar confectionery market in 2025, making them the dominant distribution channel. Their position is supported by high impulse purchases driven by strategically positioned checkout displays, promotional end-cap merchandising, and large confectionery aisles with extensive product assortments. Consumers benefit from the convenience of purchasing confectionery alongside routine grocery shopping, while retailers stimulate demand through seasonal campaigns, bundle offers, loyalty programs, and exclusive product launches. The channel also provides manufacturers with greater shelf visibility for new product introductions, premium variants, and family-sized packs, supporting strong sales volumes and consistent consumer engagement.

Online retail stores are projected to expand at the fastest CAGR of 8.11% through 2031. Growth is supported by Brazil's expanding digital ecosystem, with 83.8% of the population using the internet in 2024, according to the International Telecommunication Union (ITU). Increasing smartphone penetration and the adoption of digital payment solutions are making online confectionery purchases more accessible [3]Source: International Telecommunication Union (ITU), "Individuals using the Internet", itu.int. E-commerce platforms are driving demand through personalized product recommendations, targeted promotional campaigns, subscription purchasing models, and quick-commerce delivery services that address immediate consumption needs. The channel also enables broader access to premium, imported, limited-edition, and specialty confectionery products that are often unavailable in traditional retail outlets, while consumer reviews and social media-driven product discovery continue to encourage trial and repeat purchases.

Geography Analysis

Southeast Brazil remains the largest regional market for sugar confectionery, led by São Paulo, Rio de Janeiro, Minas Gerais, and Espírito Santo. The region has the highest concentration of confectionery manufacturing facilities in the country, along with well-developed supermarket and hypermarket networks and extensive convenience retail infrastructure that ensures broad product availability. It also serves as the primary launch market for premium, imported, and innovative confectionery products, supported by strong modern trade penetration, advanced logistics networks, and widespread adoption of omnichannel retail, making it the country's key consumption and distribution hub.

Northeast Brazil, encompassing Bahia, Pernambuco, Ceará, Maranhão, and Piauí, represents the second-largest regional market. Growth is driven by strong demand for affordable confectionery, traditional sweets, and impulse purchases through neighborhood grocery stores, wholesalers, and convenience outlets. The region continues to attract manufacturers through expanding organized retail, increasing product availability in secondary cities, and growing penetration of regional distributors. Seasonal festivals, cultural celebrations, and tourism further stimulate confectionery sales, encouraging manufacturers to introduce localized flavors, value packs, and promotional product assortments tailored to regional preferences.

Southern Brazil, comprising Rio Grande do Sul, Santa Catarina, and Paraná, represents a mature confectionery market characterized by strong demand for premium, sugar-free, and functional confectionery products. The region benefits from high retail sophistication, efficient cold-chain and logistics infrastructure, and rapid adoption of new product launches through supermarkets, specialty stores, and online channels. The Central-West and North regions remain comparatively underpenetrated but present significant long-term growth opportunities as modern retail networks expand, e-commerce penetration improves, and manufacturers strengthen distribution into underserved cities, enabling broader access to branded confectionery products.

Competitive Landscape

The Brazil sugar confectionery market features competition between established global manufacturers and strong regional brands, creating a moderately consolidated landscape driven by product innovation and brand expansion. Key companies, including Mondelez International, Inc., Nestlé S.A., Perfetti Van Melle Group B.V., Arcor S.A.I.C., and Fini Company, S.A., compete through broad product portfolios spanning gummies, hard candies, jellies, mints, chewing candies, and seasonal confectionery. Competitive advantage is built on extensive retail penetration, manufacturing scale, rapid product launches, and the ability to serve both value-oriented and premium consumer segments.

A notable feature of the Brazilian market is the growing use of brand collaborations, licensed characters, entertainment partnerships, and franchise retail concepts to strengthen consumer engagement and brand visibility. Companies regularly introduce limited-edition collections, movie- and cartoon-themed confectionery, exclusive retail launches, and experiential store formats to attract younger consumers and drive impulse purchases. Digital marketing, influencer partnerships, and social media campaigns have also become important competitive tools, enabling manufacturers to build product awareness and accelerate the adoption of new confectionery formats.

Competition is increasingly shifting toward premiumization and product differentiation, with manufacturers expanding beyond traditional mass-market confectionery into premium artisanal hard candies, gourmet gifting collections, natural ingredient formulations, and functional confectionery. Companies are investing in sophisticated packaging, premium flavor combinations, seasonal gift assortments, and cleaner-label products to capture higher-value sales and strengthen brand loyalty. Continuous investments in manufacturing modernization, sustainable packaging, omnichannel distribution, and innovation pipelines are enabling leading players to reinforce their competitive positions in Brazil's evolving sugar confectionery market.

Brazil Sugar Confectionery Industry Leaders

-

Mondelez International, Inc.

-

Nestlé S.A.

-

Perfetti Van Melle Group B.V.

-

Arcor S.A.I.C.

-

Fini Company, S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Nanchang Xol Food Co., Ltd. announced its participation as an exhibitor at ANUGA SELECT BRAZIL 2026 in São Paulo, where it showcased its portfolio of cotton candy products to strengthen its presence in the Brazilian and broader Latin American confectionery market.

- June 2025: Nestlé announced a USD 1.27 billion investment in Brazil for 2025–2028, covering factory modernization, production capacity expansion, and sustainability infrastructure, with a key focus on its Vila Velha, Espírito Santo confectionery plant.

Brazil Sugar Confectionery Market Report Scope

Sugar confectionery refers to a class of confectionery products that are primarily made from sugar and encompass a variety of items. The Brazil sugar confectionery market is segmented by product type, functional benefit, and distribution channel. Based on product type, the market is segmented into hard candy, mints, pastilles, gummies and jellies, toffees and nougats, lollipops, and others. The mints segment is further categorized into power mints and standard mints. Based on functional benefit, the market is segmented into novelty, fortified, digestive/botanicals, and others. Based on distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels. The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

| Hard Candy | |

| Mints | Power Mints |

| Standard Mints | |

| Pastilles, Gummies, and Jellies | |

| Toffees and Nougats | |

| Lollipops | |

| Others |

| Novelty |

| Fortified |

| Digestive/Botanicals |

| Others |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Convenience Stores |

| Other Distribution Channels |

| By Product Type | Hard Candy | |

| Mints | Power Mints | |

| Standard Mints | ||

| Pastilles, Gummies, and Jellies | ||

| Toffees and Nougats | ||

| Lollipops | ||

| Others | ||

| By Functional Benefit | Novelty | |

| Fortified | ||

| Digestive/Botanicals | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Online Retail Stores | ||

| Convenience Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How large is the Brazil sugar confectionery market in 2026?

The Brazil sugar confectionery market stands at USD 1.72 billion in 2026 and is projected to reach USD 2.34 billion by 2031 at a 6.33% CAGR.

Which product category leads confectionery sales in Brazil?

Pastilles, Gummies, and Jellies lead the category with a 43.54% share in 2025, supported by strong demand for chewy and visually engaging formats.

Which sales channel is growing the fastest in Brazil’s confectionery space?

Online Retail Stores are forecast to grow the fastest at an 8.11% CAGR through 2031 as quick-commerce expands impulse buying beyond physical stores.

Why are mints gaining ground faster than other candy formats in Brazil?

Mints are projected to grow at a 6.81% CAGR through 2031 because they serve both refreshment and snacking occasions, which broadens demand.

Page last updated on: