Sodium Starch Glycolate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

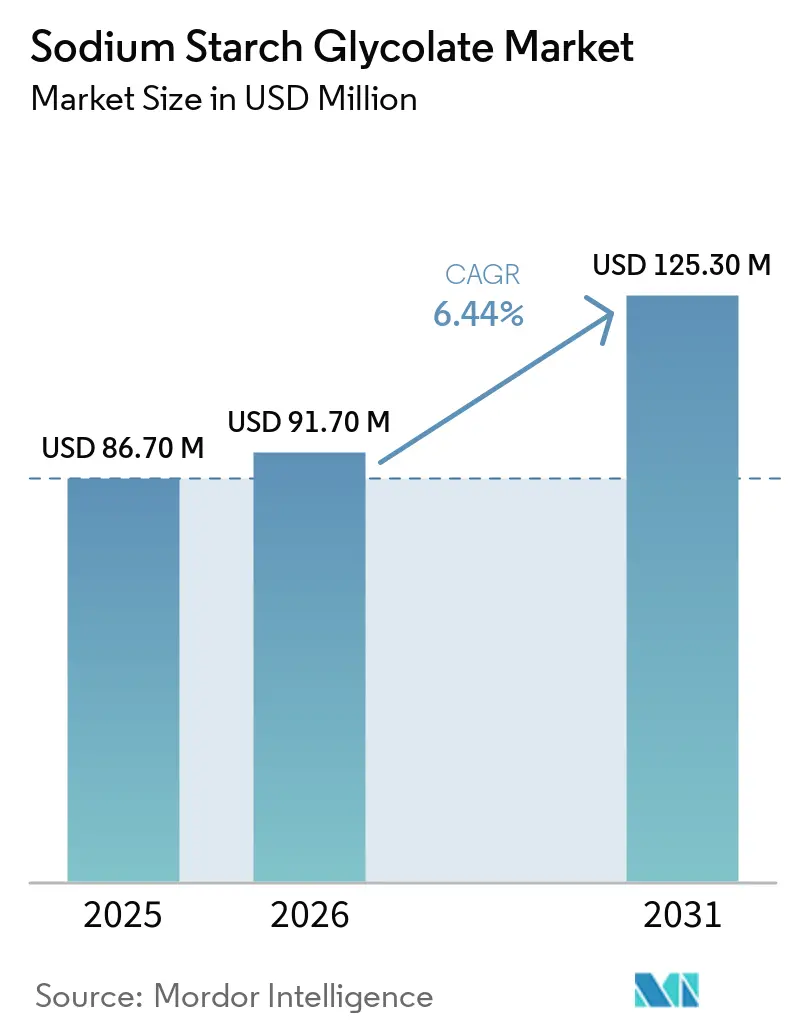

| Market Size (2026) | USD 91.70 Million |

| Market Size (2031) | USD 125.30 Million |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

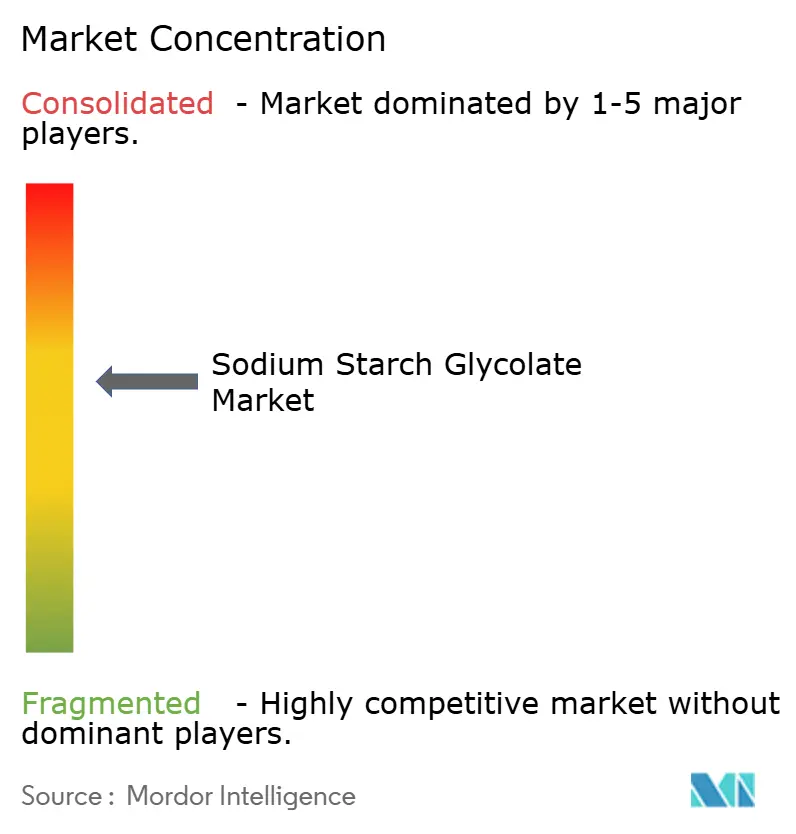

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium Starch Glycolate Market Analysis by Mordor Intelligence

The sodium starch glycolate market size is expected to grow from USD 86.70 million in 2025 to USD 91.70 million in 2026 and is forecast to reach USD 125.30 million by 2031 at 6.44% CAGR over 2026-2031. Sodium starch glycolate remains a benchmark superdisintegrant in solid oral dosage manufacturing, and pharmaceutical use still anchors demand with a 72% revenue contribution in the current structure. Faster generic drug launches continue to support the sodium starch glycolate market because regulatory clearance for abbreviated products keeps adding validated demand for compendial excipients across major tablet programs. Asia-Pacific stayed the largest production base for the sodium starch glycolate market, while North America is set to post the fastest regional expansion as nutraceutical tablets, formulation modernization, and regulated quality upgrades gain weight in procurement decisions. The sodium starch glycolate market is also broadening beyond its core pharmaceutical base as clean-label positioning, food processing use, and dual-use sourcing strategies strengthen demand for plant-derived excipients from qualified suppliers. Competitive conditions in the sodium starch glycolate market are being shaped by raw material swings, substitution pressure from synthetic disintegrants, and supplier efforts to widen their technical and geographic reach through portfolio moves and formulation support investments

Key Report Takeaways

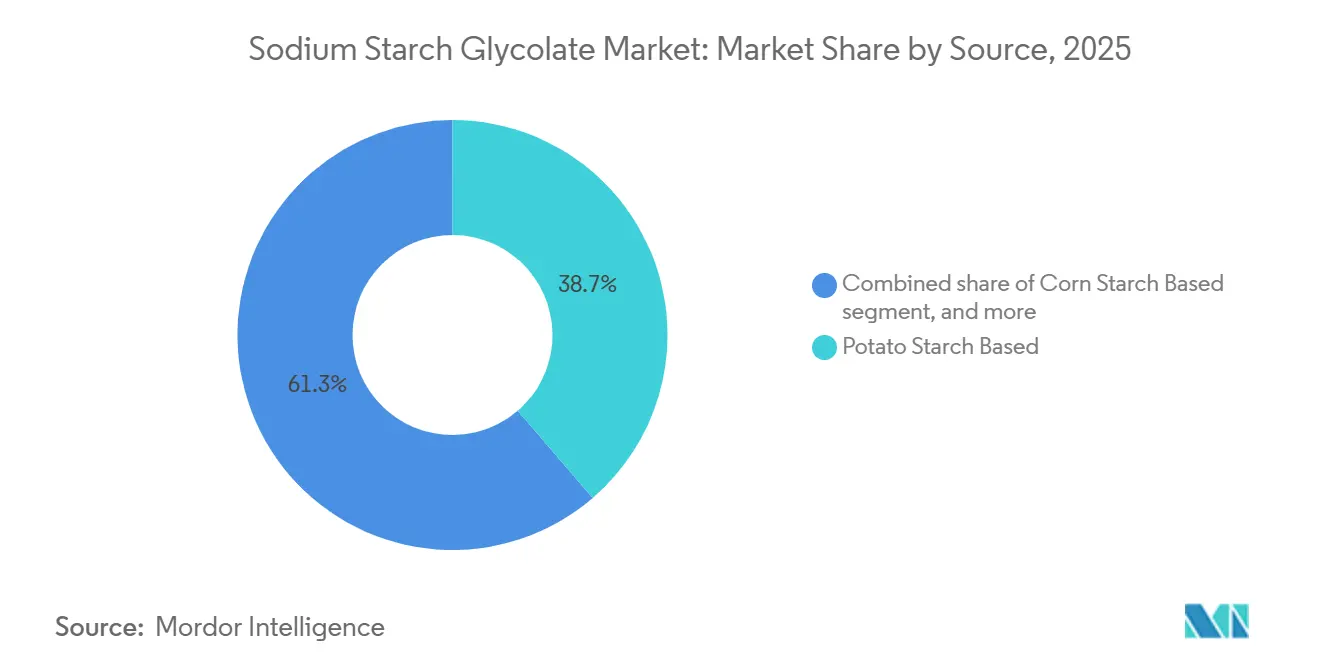

- By source, the potato starch-based sodium starch glycolate market held 38.7% of revenue in 2025, while the corn starch-based is forecasted to expand at a 6.32% CAGR through 2031.

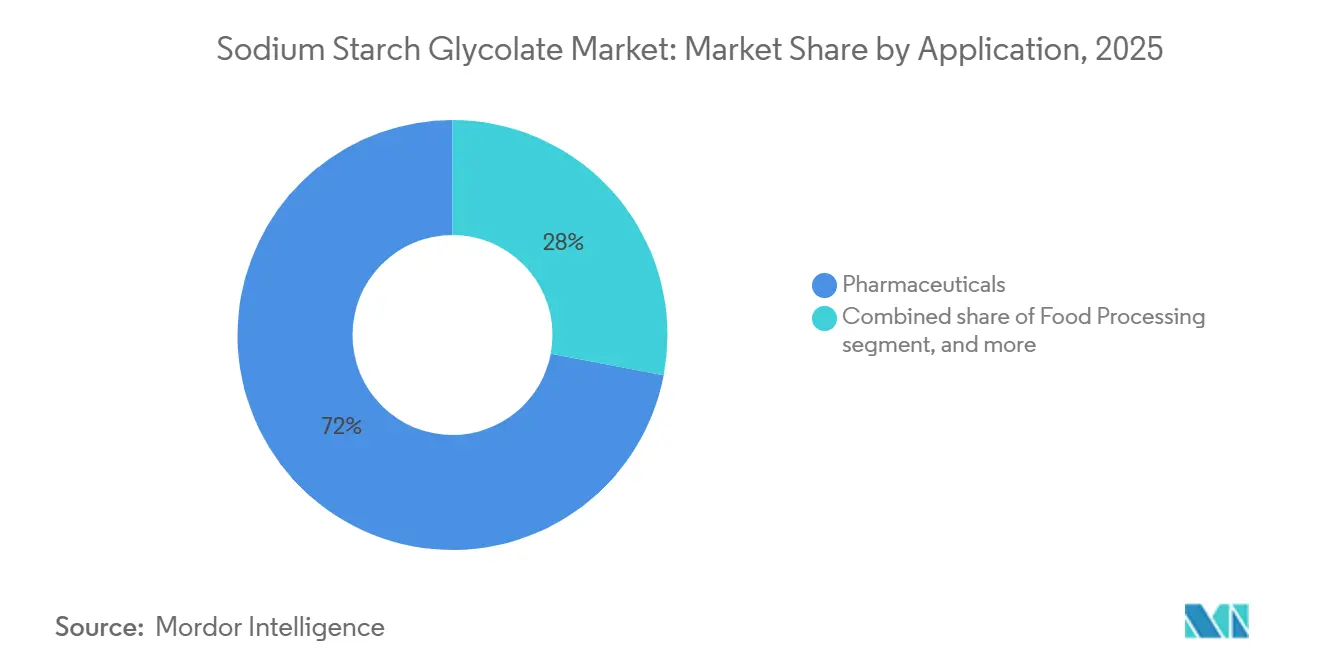

- By application, pharmaceuticals accounted for 72% of total revenue in 2025, while food processing is projected to grow at a 5.33% CAGR through 2031.

- By geography, Asia-Pacific held 34.8% of revenue in 2025, while North America is projected to advance at a 5.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sodium Starch Glycolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global generic drug production | +1.8% | Global, with concentrated gains in India, China, and the United States | Short term (≤ 2 years) |

| Growing nutraceutical tablet and capsule demand | +1.2% | North America, Asia-Pacific, and Western Europe | Medium term (2-4 years) |

| Clean label and plant-based excipient preference | +0.7% | North America, EU, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Innovation in Novel Drug Delivery Systems (NDDS) | +0.6% | Global, with primary research and vevelopment in the United States, Germany, Japan, and India | Long term (≥ 4 years) |

| Increasing use of convenience and instant food products | +0.5% | Asia-Pacific and North America | Medium term (2-4 years) |

| Price volatility of competing disintegrants is strengthening SSG's cost position | +0.4% | Global, most pronounced in price-sensitive Asia-Pacific and Latin American markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising global generic drug production

The sodium starch glycolate market continues to benefit directly from rising generic pharmaceutical output across regulated and emerging markets. The United States Food and Drug Administration approved 76 first-generic drugs in 2024, and that flow of approvals keeps creating new formulation demand for compendial excipients used in tablet manufacturing [1]Source: U.S. Food and Drug Administration, “FDA Drug Competition Action Plan,” U.S. Food and Drug Administration, fda.gov. A key advantage for sodium starch glycolate market suppliers is that broad pharmacopeial alignment reduces documentation friction for companies that want to serve both the United States and European product pipelines. Prequalification pathways also widen the addressable demand base because manufacturers that qualify products for public health procurement need excipients that fit recognized quality frameworks. As more multisource products enter large tablet categories, manufacturers that already standardize on sodium starch glycolate tend to keep it in place because requalification work on core excipients adds time and cost.

Growing nutraceutical tablet and capsule demand

The sodium starch glycolate market is gaining added support from the steady expansion of nutraceutical tablets and capsules. This format mix matters because tablets remain attractive for producers that want precise dosing, scalable output, and stable shelf life across a wide product range. Sodium starch glycolate fits this setting well because its low use level helps formulators manage cost while still supporting fast breakup in compressed products. Suppliers and customers are also narrowing the gap between supplement-grade and drug-grade specifications as retailers and brand owners place more attention on consistency, documentation, and quality claims. The result is a broader demand pool for the sodium starch glycolate market that is no longer tied only to prescription and generic drug production.

Clean label and plant-based excipient preference

The sodium starch glycolate market is also being influenced by a stronger preference for plant-derived and recognizable excipient inputs. Sodium starch glycolate is made from starch sources such as potato, corn, and wheat, which gives it a clear positioning advantage over petrochemical-derived alternatives in clean-label discussions[2]Source: DFE Pharma, “Primojel , Sodium Starch Glycolate,” DFE Pharma, dfepharma.com. That advantage is becoming more relevant in pharmaceutical and nutraceutical programs that emphasize Genetically Modified Organism (GMO)- free, allergen-aware, or plant-origin sourcing language. DFE Pharma's continued focus on Primojel and its dedicated production base in the Netherlands shows that suppliers are responding to this demand with targeted capacity and documentation support. The sodium starch glycolate market is therefore seeing sourcing decisions shaped not only by functionality and price, but also by traceability and positioning value.

Innovation in Novel Drug Delivery Systems (NDDS)

The sodium starch glycolate market is moving into more advanced formulation settings as oral delivery platforms become more specialized. Sodium starch glycolate is already used in standard tablets, but its role is widening in orally disintegrating tablets, bilayer formats, pediatric mini-tablets, and other systems where disintegration behavior must be tightly controlled. Suppliers are now pairing excipient grades with technical support so customers can evaluate performance under newer manufacturing approaches. DFE Pharma's continuous manufacturing platform with Gericke reflects this shift because it places CM-ready Primojel grades inside an ICH Q13-aligned development setting. This raises the strategic value of the sodium starch glycolate market in programs where formulation reliability and process compatibility matter as much as the excipient's basic disintegrant role.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility in starch feedstocks | -1.1% | Europe (potato starch), North America and Asia-Pacific (corn starch), EU (wheat starch) | Short term (≤ 2 years) |

| Regulatory burden across pharmacopeial grades | -0.7% | Global, most acute for exporters targeting United States, EU, and Japan simultaneously | Long term (≥ 4 years) |

| Moisture sensitivity and packaging complexity | -0.5% | Tropical and subtropical markets, South and Southeast Asia, Midde East and Africa | Medium term (2-4 years) |

| Substitution pressure from crospovidone and croscarmellose sodium | -0.9% | Global, most pronounced in high-speed tableting and orally dissolving tablet applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility in starch feedstocks

The sodium starch glycolate market faces a clear restraint from raw material volatility because starch feedstocks remain exposed to agricultural cycles, fertilizer costs, and energy pass-through. Roquette's March 2026 market update for Europe noted pressure across the cereal complex and linked the environment to weather uncertainty and wider energy and fertilizer stress[3]Source: Roquette Frères, “March 2026 Update on the European Industry Market,” Roquette, roquette.com. This matters more in potato-based grades because the feedstock base is concentrated in Northern Europe, which makes procurement more sensitive to regional crop conditions and cost swings. Producers that supply pharmaceutical customers under fixed or slower-moving contracts cannot always pass higher input costs through immediately, so margin pressure builds quickly. The sodium starch glycolate market also shows a split between commodity grades and higher-value pharmaceutical grades, which means not every supplier has the same pricing power when raw materials move against them.

Regulatory burden across pharmacopeial grades

The sodium starch glycolate market also faces substitution pressure from crospovidone and croscarmellose sodium in more demanding oral dosage settings. These materials can offer performance advantages in specific uses, especially where wicking behavior, neutral pH compatibility, mouthfeel, or very fast onset are critical to product design. Competitor investment is still active, and JRS Pharma opened a new cotton-based croscarmellose sodium plant in Mehsana, India, in July 2024 to deepen its position in the excipient base serving generic drug manufacturing. Sodium starch glycolate still defends its place through lower commodity-grade cost and wider pharmacopeial acceptance across the United States Pharmacopeia, European Pharmacopoeia, and Japanese Pharmacopoeia. Even so, the sodium starch glycolate market can lose share in premium or high-speed formulations when those alternative materials solve a more specific technical problem for the customer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Potato Starch Maintains Lead as Corn Starch Accelerates Globally

Potato Starch-based SSG held 38.7% of the sodium starch glycolate market share in 2025, and that led to formulation preference more than simple feedstock availability. Potato-derived grades are associated with phosphorous cross-link chemistry, and that profile supports chemical stability that is especially valued in moisture-sensitive formulations. The source has also benefited from long-standing pharmacopeial familiarity, which helps manufacturers working across regulated tablet programs. European producers and users have stayed loyal to this source because regional supply access, Drug Master File support, and a long qualification history reduce the need to revisit core excipient choices.

Corn Starch-based SSG is projected to deliver the fastest sodium starch glycolate market size growth at a 6.32% CAGR from 2026 to 2031. Its growth case is tied to broader agricultural availability across North America and East Asia, which gives suppliers a more diversified feedstock base than the more regionally concentrated potato chain. That broader base supports sourcing resilience for the sodium starch glycolate industry, especially in markets that want lower import dependence and more predictable year-round availability.

By Application: Pharmaceutical Dominance Anchors Demand, Food Processing Gains Momentum

Pharmaceuticals accounted for 72% of the sodium starch glycolate market size in 2025, which confirms that tablet and capsule manufacturing remains the core demand center. Sodium starch glycolate keeps its strong position in immediate-release formulations because its swelling action supports rapid breakup under standard dissolution conditions. That role extends across both branded and generic portfolios, and it is reinforced by procurement systems that specify pharmacopeially acceptable excipient grades for hospital and tender channels. Pharmaceutical dominance, therefore, remains durable because the excipient is embedded in large-volume oral dosage workflows that reward consistency and regulatory familiarity.

Food Processing is projected to post the fastest application growth in the sodium starch glycolate market at a 5.33% CAGR from 2026 to 2031. Demand is building in instant soups, dry beverage mixes, and gluten-free baked products where moisture control, stabilization, and texture support are relevant to product performance. DFE Pharma's Primojel, Type B positioning shows how suppliers are using one qualified platform to serve both food and pharmaceutical customers, which reduces complexity for buyers working across multiple end uses.

Geography Analysis

Asia-Pacific accounted for 34.8% of the sodium starch glycolate market share in 2025, making it the largest regional base for current demand. India and China anchor this position because their tablet and capsule manufacturing scale feeds directly into high-volume excipient procurement for generic medicines. Export-oriented Indian manufacturers increasingly need harmonized grades with strong documentation support, while a part of the Chinese domestic base still works with more price-led commodity supply. China's excipient Good Manufacturing Practice (GMP) annex, effective from January 1, 2026, is raising the local compliance floor and narrowing gaps with international expectations. Supplier investment in regional technical support is reinforcing the sodium starch glycolate market in Asia-Pacific, and DFE Pharma's Hyderabad center reflects the push to shorten formulation development cycles close to customer demand.

North America is expected to record the fastest sodium starch glycolate market size growth at a 5.8% CAGR through 2031. The regional outlook is supported by a strong pipeline of generic drug launches and by a nutraceutical sector that continues to favor tablet and capsule delivery formats. Demand is also benefiting from formulation upgrades and wider attention to natural-origin excipient options across regulated and adjacent health products. Ashland's 2026 tablet coatings investment in India still matters to North American strategy because it reflects a broader supply chain model built around dual sourcing and closer links with Asia-Pacific manufacturing nodes.

Europe remains an important but more mature part of the sodium starch glycolate market. The region houses advanced excipient producers such as DFE Pharma and Roquette, and their operations continue to influence quality expectations across global pharmacopeial supply. Roquette's portfolio expansion through the International Flavors and Fragrances Pharma Solutions deal widened its presence across oral dosage excipients and strengthened Europe's role in higher-value formulation support. South America and the Middle East and Africa remain smaller in size, but local pharmaceutical manufacturing and formulation capability investments are still creating incremental demand for the sodium starch glycolate market in those regions.

Competitive Landscape

The sodium starch glycolate market is led by a small group of established excipient specialists that hold strong positions in pharmacopeial registration, technical documentation, and formulation support. DFE Pharma, Roquette Frères, and JRS Pharma have influence that goes beyond volume because customers in regulated applications often stay with suppliers that already support approved grades and validation files. This creates a layered structure in the sodium starch glycolate market, with global branded suppliers at the upper end and a broad set of Indian and Chinese producers competing more aggressively on price in less demanding or domestic programs. The practical result is that buyers do not switch easily in highly regulated products, even when a lower-cost supply exists. That pattern keeps competition active, but it also preserves a premium for suppliers that can combine product performance with technical and regulatory support.

A major strategic move came from DFE Pharma, which launched a continuous manufacturing platform with Gericke to position Primojel® more directly inside modern tablet development workflows. Roquette reshaped the broader excipient field by completing its acquisition of IFF Pharma Solutions in May 2025 for EUR 2,403 million (USD 2,595.2 million), giving it a wider mix of starch, cellulose, alginate, and polymer technologies under one platform. That scale matters to the sodium starch glycolate market because customers increasingly value suppliers that can solve multiple oral dosage needs through one commercial relationship. The sodium starch glycolate market is therefore seeing competition shift from product availability alone toward platform breadth and formulation partnership depth.

Pricing and regional expansion are also shaping the next phase of the sodium starch glycolate market. BASF Pharma Solutions announced a global price increase of up to 20% for pharmaceutical excipients and selected APIs in March 2026, signaling broader input pressure across the category. Ashland expanded its partnership with WACKER in 2026 and continued investing in tablet-coatings capacity, which shows how adjacent excipient players are widening their offering and strengthening channel reach. Smaller Asian suppliers are still gaining space in price-sensitive accounts, but rising Good Manufacturing Practices, audit, and certification expectations mean that compliance readiness is becoming a more decisive competitive filter across the sodium starch glycolate market

Sodium Starch Glycolate Industry Leaders

DFE Pharma

Roquette Frères SA

JRS Pharma

Colorcon

Ashland

- *Disclaimer: Major Players sorted in no particular order

Global Sodium Starch Glycolate Market Report Scope

The starch glycolate market refers to the global industry involved in the production, distribution, and use of starch glycolate compounds for industrial applications. It serves sectors such as pharmaceuticals, food processing, and, where manufacturers value starch glycolate for its disintegration, thickening, binding, and stabilizing properties. The sodium starch glycolate market report is segmented by source into potato starch-based, corn starch-based, wheat starch-based, and other starch sources. By application, the market is segmented into pharmaceuticals, food processing, personal care and cosmetics, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Potato Starch Based |

| Corn Starch Based |

| Wheat Starch Based |

| Other Starch Sources |

| Pharmaceuticals |

| Food Processing |

| Personal Care and Cosmetics |

| Other Applications |

| North America |

| Europe |

| Asia-Pacific |

| South America |

| Middle East and Africa |

| By Source | Potato Starch Based |

| Corn Starch Based | |

| Wheat Starch Based | |

| Other Starch Sources | |

| By Application | Pharmaceuticals |

| Food Processing | |

| Personal Care and Cosmetics | |

| Other Applications | |

| By Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle East and Africa |

Key Questions Answered in the Report

What is driving sodium starch glycolate demand through 2031?

Growth is being supported by generic drug production, rising nutraceutical tablet demand, and expanding food processing use, which together are expected to lift value from USD 91.7 million in 2026 to USD 125.3 million by 2031.

Which application generates the most revenue for sodium starch glycolate?

Pharmaceuticals lead by a wide margin, accounting for 72% of total revenue in 2025 because sodium starch glycolate remains deeply embedded in tablet and capsule manufacturing.

How concentrated is competition among suppliers?

Crospovidone and croscarmellose sodium can outperform sodium starch glycolate in selected applications where very fast disintegration, wicking, or mouthfeel characteristics are more important.

What limits wider use in advanced oral formulations?

Crospovidone and croscarmellose sodium can outperform sodium starch glycolate in selected applications where very fast disintegration, wicking, or mouthfeel characteristics are more important.

Page last updated on: