Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.43 Billion |

| Market Size (2026) | USD 2.5 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 2.93% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Sugar Substitute Market Analysis by Mordor Intelligence

The Europe sugar substitutes market size was valued at USD 2.43 billion in 2025 and estimated to grow from USD 2.5 billion in 2026 to reach USD 2.89 billion by 2031, at a CAGR of 2.93% during the forecast period (2026-2031). This growth is driven by a well-established regulatory framework, continuous product reformulations within the food and beverage industries, and a gradual consumer preference for healthier alternatives. Germany's regulatory leadership, along with anti-dumping measures on erythritol, has ensured stable domestic production, mitigated price volatility, and strengthened manufacturers' confidence in supply reliability. The adoption of fermentation-derived stevia and monk fruit has increased significantly, with clean-label claims commanding retail price premiums. Although high-intensity sweeteners continue to dominate in terms of volume, polyols, and plant-derived alternatives are capturing higher consumer spending, particularly as their applications in pharmaceuticals and sports nutrition expand. To reduce the carbon footprint of sweetening solutions, companies are leveraging strategies such as precision fermentation, vertical integration, and enhanced life-cycle transparency, which have become critical competitive differentiators.

Key Report Takeaways

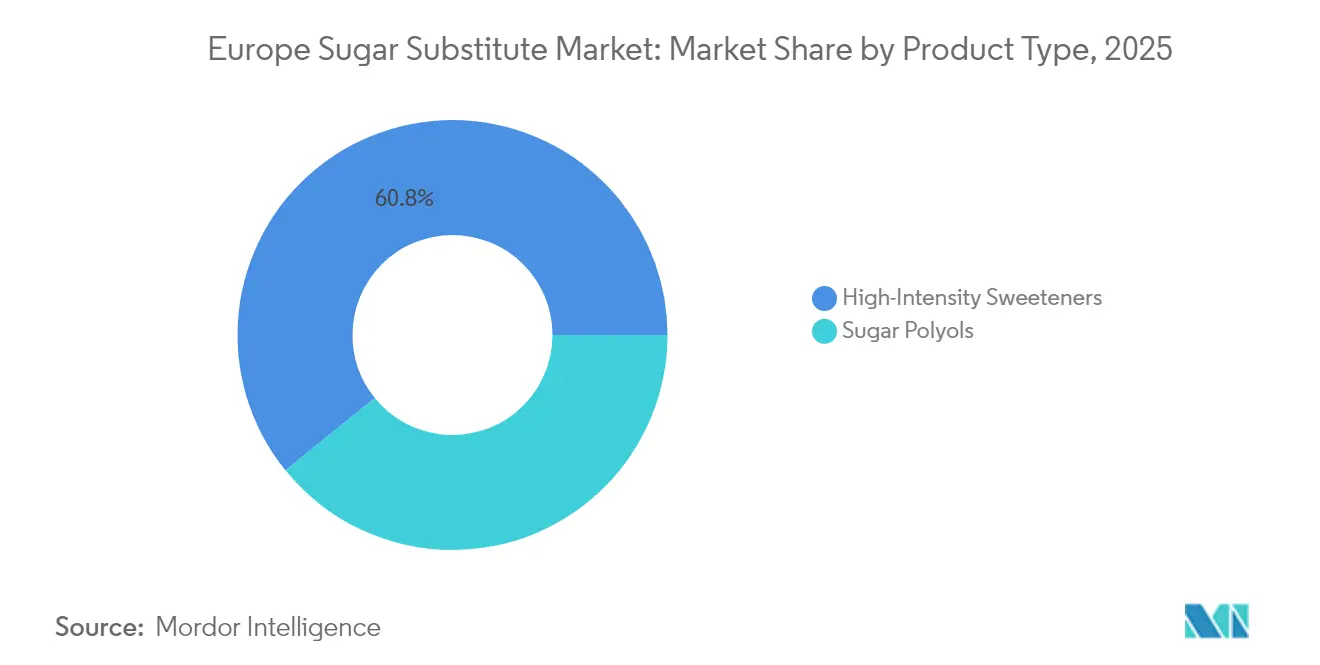

- By sweetener type, high-intensity sweeteners led with 60.84% revenue share in 2025, whereas sugar polyols are projected to expand at an 7.92% CAGR through 2031.

- By origin, synthetic variants held 56.40% of the European sugar substitutes market share in 2025, while plant-derived alternatives are forecast to grow at a 8.78% CAGR to 2031.

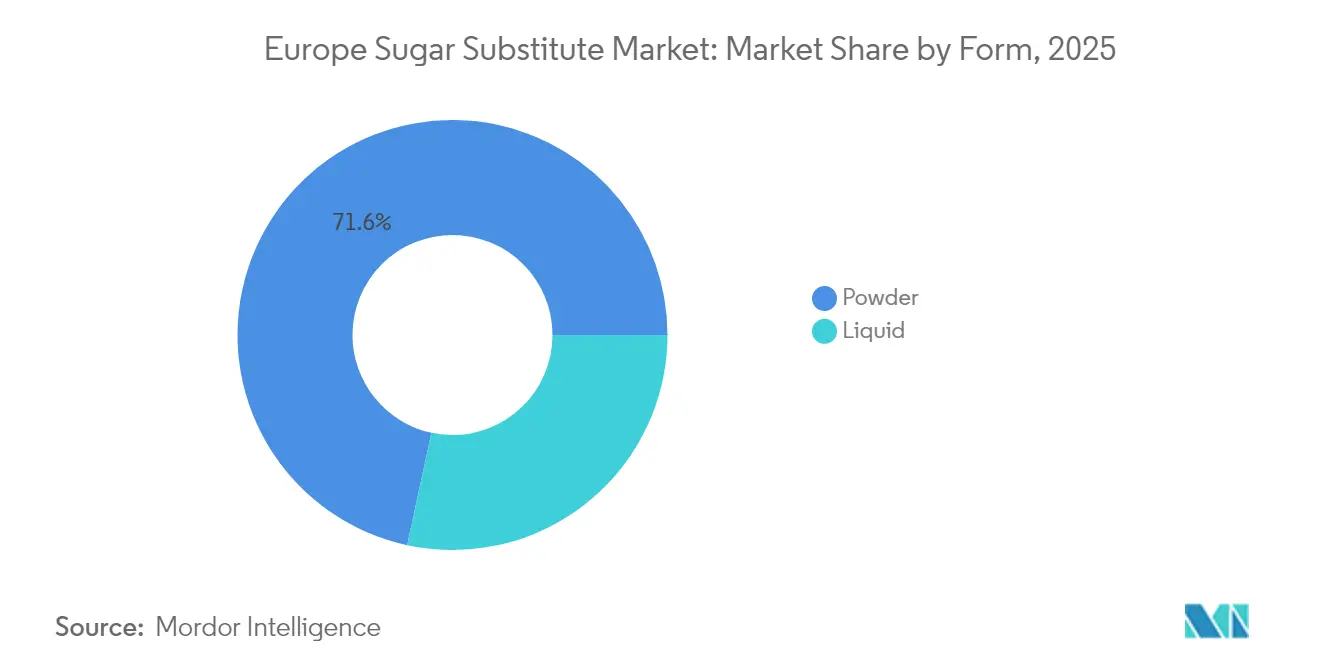

- By form, powder products commanded 71.62% of the European sugar substitutes market size in 2025; liquid formats are advancing at a 7.45% CAGR to 2031.

- By application, beverages accounted for 44.20% of the European sugar substitutes market size in 2025; pharmaceuticals exhibit the fastest expansion at an 8.63% CAGR to 2031.

- By country, Germany captured 19.00% of 2025 revenue and also posts the highest national CAGR at 4.12% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Sugar Substitute Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in clean-label preference for natural sweeteners | +0.8% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Expansion of low/no-sugar products fueling market growth | +0.7% | Europe | Long term (≥ 4 years) |

| Soaring diabetes and obesity rates fueling demand for low-calorie sweetenres | +0.6% | Germany, United Kingdom, Italy | Long term (≥ 4 years) |

| EU sugar-reduction legislation accelerating reformulationa | +0.5% | Europe | Short term (≤ 2 years) |

| Rising shift to lower-carbon footprint ingredients | +0.3% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Increasing consumer awareness of health and wellness drives market expansion | +0.4% | Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in clean-label preference for natural sweeteners

European consumers are placing greater emphasis on scrutinizing ingredient lists, driving a significant increase in demand for plant-derived sweeteners that align with transparency and clean-label expectations. This evolving consumer preference is compelling food manufacturers to reevaluate their procurement strategies, prioritizing natural alternatives such as stevia, monk fruit, and other botanical sweeteners over synthetic compounds to meet these requirements. Regulatory advancements, including the approval of fermentation-derived stevia variants like DSM-Firmenich and Cargill's EverSweet by EFSA and FSA, are expanding the range of formulation possibilities while ensuring compliance with clean-label standards. Additionally, the willingness of consumers to pay a premium for natural alternatives creates lucrative margin opportunities, as they increasingly favor products featuring botanical sweeteners over those containing artificial ingredients.

Expansion of low/no-sugar products fueling market growth

The European beverage sector is undergoing a significant transformation, with an increasing focus on low and no-calorie options. This shift is not only redefining the beverage market but also creating substantial growth opportunities for sugar substitute suppliers. Furthermore, this trend extends beyond beverages, influencing the confectionery, dairy, and bakery markets, where manufacturers are actively reformulating their flagship products to align with evolving consumer preferences while maintaining the original taste profiles. Addressing this demand, Kerry's Tastesense Advanced range offers a solution capable of achieving up to a 100% reduction in sugar content without compromising the sensory qualities that consumers expect. The energy drink category, in particular, is driving innovation within the sector. Brands are introducing products fortified with BCAAs and vitamins, alongside sugar-free formulations, to cater to the growing health-conscious demographic. Supporting this industry-wide shift, regulatory initiatives such as the Union of European Beverage Associations' target of a 10% sugar reduction by 2025 are providing a strong framework that sustains and accelerates long-term growth trajectories across the sector.

Soaring diabetes and obesity rates fueling demand for low-calorie sweeteners

Europe grapples with a mounting public health crisis, as obesity and type 2 diabetes rates climb, particularly in the UK, Germany, and Italy. In response, health-conscious consumers are actively seeking to cut sugar intake without compromising on flavor. Those managing diabetes or weight are turning to products featuring both natural and artificial sugar substitutes. The rise of the clean label trendsfavoring natural, non-GMO, and plant-based ingredients, has bolstered the popularity of natural sweeteners like stevia and monk fruit. Concurrently, the growing adoption of GLP-1 therapies is steering formulators towards crafting sugar-free meal replacements that resonate with weight-management protocols. According to WHO's European Health Report, 2024 sees nearly 1 in 3 school-aged children in Europe classified as overweight, with 1 in 8 grappling with obesity[1]Source: World Health Organization, “European Health Report 2025,” who.int. These alarming figures are largely linked to poor dietary choices, heavily swayed by aggressive marketing of high-sugar products. Beyond the food and beverage realm, sugar substitutes are making their mark in diabetic medications, oral supplements, and nutraceuticals, all aimed at weight loss and blood sugar control, underscoring a robust industrial demand.

EU sugar-reduction legislation accelerating reformulation

Starting November 2024, the European Union's Regulation (EU) No 1308/2013 mandates uniform marketing and labeling standards, pushing manufacturers to reformulate products to stay competitive in the evolving market. This regulation aims to ensure transparency and consistency in product information, benefiting both consumers and businesses. Italy's sugar tax, introduced amidst the EU's regulatory landscape, underscores the intensifying push for compliance among food and beverage producers, encouraging them to innovate and adapt to changing consumer preferences and regulatory demands. Furthermore, the European Food Safety Authority (EFSA) has revisited its stance on key sweeteners, notably upping saccharin's acceptable daily intake from 5 mg/kg to 9 mg/kg body weight, thus broadening formulation avenues for producers and enabling them to explore new product offerings. The UK's sugar tax, which has notably curtailed sugar levels in soft drinks, not only serves as a blueprint for similar initiatives across Europe but also sets the stage for wider adoption, demonstrating the potential for regulatory measures to drive significant changes in public health and industry practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent EU novel-food approval delays for new sweeteners | -0.4% | Europe | Medium term (2-4 years) |

| Consumer safety perception issues around artificial sweeteners | -0.3% | Germany, France, United Kingdom | Long term (≥ 4 years) |

| Limited domestic stevia cultivation causing supply-chain volatility | -0.2% | Europe | Short term (≤ 2 years) |

| High production costs of sugar substitutes impact market growth | -0.3% | Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent EU novel-food approval delays for new sweeteners

EFSA's stringent assessment process for novel foods ensures consumer safety but also imposes significant barriers to market entry. This approach restricts innovation and alters the competitive dynamics within the European sugar substitutes market. For instance, D-allulose remains unapproved in Europe, despite receiving authorizations in other regions, due to incomplete evaluations resulting from insufficient hazard characterization data. Similarly, monk fruit extract faces regulatory inconsistencies, with aqueous extracts approved while concentrated extracts remain prohibited due to gaps in safety data. These inconsistencies limit manufacturers' ability to develop optimal sweetening solutions. The updated EFSA guidance, effective February 2025, seeks to enhance clarity but continues to mandate comprehensive dossiers. These include detailed production processes, composition data, and extensive toxicological information, often extending approval timelines beyond 18 months for complex applications. Such delays particularly impact biotechnology companies developing precision fermentation sweeteners, where regulatory uncertainty constrains investment decisions and market entry strategies.

High production costs of sugar substitutes impact market growth

Production costs for advanced sweeteners remain considerably higher than those of traditional sugar, creating significant adoption barriers, particularly in price-sensitive market segments where achieving cost parity remains challenging despite technological advancements. For instance, even with a 51% yield improvement in fermentation, erythritol's unit costs are still substantially higher than refined sugar. Anti-dumping duties of up to 233.3% on Chinese erythritol further exacerbate this cost disparity. Stevia agronomy projects necessitate investments in drip irrigation, greenhouse nurseries, and farmer training, which significantly increase capital expenditures (CAPEX). Although bioconversion offers scalability benefits, the requirement for stainless-steel fermenters and downstream purification processes demands substantial capital, posing challenges for smaller market players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: A resilient Core With Polyol Tailwinds

In 2025, acesulfame K, aspartame, and sucralose, high-intensity molecules, dominate the European sugar substitutes market, making up 60.84% of total revenue. Their widespread use in key applications like soft drinks, tabletop sachets, and chewing gum solidifies their market leadership. These molecules benefit from economies of scale, ensuring cost efficiency and consistent supply, which further strengthens their position in the market. Meanwhile, polyols are carving out a significant growth segment, with projections showing a robust CAGR of 7.92% through 2031. This surge is largely attributed to sorbitol's essential role in pediatric syrups, where it acts as a sweetener and stabilizer, xylitol's recognized dental care advantages, including its ability to reduce cavity-causing bacteria, and erythritol's distinctive cooling mouthfeel, which enhances its use in confectionery and beverages. Collectively, these factors are driving the increasing adoption of polyols across diverse industries.

Stevia Rebaudioside M, crafted through precision fermentation, is overcoming traditional taste hurdles, such as bitterness and aftertaste, prompting reformulations in baked goods and broadening its food industry adoption. This innovation is particularly significant as it allows manufacturers to create products with improved taste profiles while maintaining natural and clean-label claims. Moreover, the raised Acceptable Daily Intake (ADI) of acesulfame K to 15 mg/kg has expanded its application range, paving the way for zero-sugar Cola launches and other low-calorie beverages. The European sugar substitutes sector is also aligning more closely with pharmaceutical industry regulations, spurring the dual-use adoption of polyols in both food and pharmaceutical formulations. This regulatory alignment is fostering innovation, enabling manufacturers to develop multifunctional products, and driving overall market growth.

By Origin: Plant-based Surge Reshapes Portfolios

In 2025, synthetic variants accounted for 56.40% of the market revenue but grappled with challenges tied to consumer perception, particularly concerns about artificial ingredients and potential health risks. In contrast, plant-derived alternatives surged ahead, boasting a robust CAGR of 8.78%, driven by increasing consumer demand for natural and clean-label products. Initiatives in Greece and Spain, such as tobacco-to-stevia conversion projects, are bolstering carbon sustainability by reducing reliance on traditional agricultural practices and promoting eco-friendly production methods. Synthetic variants, known for their high sweetness intensity, with sucralose being 600 times sweeter than sugar, find extensive use in processed foods, diet soft drinks, and pharmaceuticals due to their cost-effectiveness and stability in various formulations. Dominating the beverages and dessert segments are sucralose and Acesulfame-K, which continue to be preferred for their ability to maintain taste profiles without adding calories.

Consumers, especially those diabetic or weight-conscious, increasingly view plant-derived sweeteners as healthier and safer options, aligning with the growing trend toward health-conscious eating habits. Stevia, at the forefront of this segment, sees its applications spanning yogurts, beverages, and baked goods, supported by its natural origin and minimal impact on blood sugar levels. Biotechnological fermentation is carving a niche, merging natural claims with industrial efficiency by enabling the production of high-purity sweeteners at scale. After receiving EFSA clearance, Cargill’s EverSweet steviol glycosides and DSM-Firmenich’s Rebaudioside M have made their way to European soda fountains, offering manufacturers a reliable supply of high-quality sweeteners. Moreover, there's a rising consumer acceptance of precision-fermented products, with many viewing them as nature-identical, alleviating previous skepticism and paving the way for broader adoption in the food and beverage industry.

By Form: Liquids Gain When Speed Matters

From 2026 to 2031, liquid sweeteners are projected to witness a CAGR of 7.45%. This growth is largely attributed to the beverage industry's push for enhanced processing efficiency. The industry's preference for liquid sweeteners stems from their superior solubility, which streamlines manufacturing processes by enabling faster and more uniform mixing. Additionally, liquid sweeteners reduce the need for extensive mechanical processing, thereby lowering energy consumption and operational costs. Meanwhile, in 2025, powdered sweeteners are set to dominate the market, holding a substantial 71.62% share. Their prominence is especially evident in the bakery, confectionery, and pharmaceutical sectors, where their bulk properties and stability provide distinct advantages, such as ease of storage, extended shelf life, and consistent performance in various formulations.

The beverage industry's shift towards liquid sweeteners is not merely a trend but a calculated move. The operational benefits are clear: liquid sweeteners offer reduced mixing times, quicker dissolution, and better flavor integration, which are critical for maintaining product consistency and meeting consumer expectations. Such advantages not only elevate product quality but also justify a premium pricing strategy for these solutions, making them an attractive option for manufacturers aiming to differentiate their offerings. On the other hand, the pharmaceutical industry is leaning towards powdered forms, especially in tablet production, where their compressibility and stability ensure precise dosage and efficacy in medicinal applications.

By Application: Pharma Eclipses Beverages On Growth

Pharmaceuticals demonstrate the fastest-growing application with an 8.63% CAGR during 2026-2031. This growth stems from the pharmaceutical industry's increasing utilization of sugar alcohols as excipients in drug formulations and the expanding demand for sugar-free medications. Sugar alcohols serve as crucial ingredients in pharmaceutical products, offering both sweetening properties and functional benefits such as improved tablet binding and extended shelf life. The beverages segment maintains a dominant 44.20% market share in 2025, bolstered by the Union of European Beverage Associations' commitment to reduce sugar content by 10% by 2025. This initiative responds to consumer health concerns and regulatory pressures. In 2023, soft drink consumption in the European Union (EU) reached 51,905.7 million liters, according to UNESDA - the Union of European Soft Drinks Associations.

Food applications, encompassing bakery, confectionery, and dairy categories, are witnessing a substantial transformation toward sugar substitutes. This shift is driven by stringent regulatory requirements for nutritional labeling and increasing consumer awareness of the health implications associated with excessive sugar consumption. The pharmaceutical sector's robust growth highlights the expanding role of sugar alcohols in both excipient applications and sugar-free medication development. These formulations enhance patient compliance, particularly benefiting diabetic individuals who manage multiple daily prescriptions while monitoring their sugar intake.

Geography Analysis

In 2025, Germany represented 19.00% of the turnover in Europe's sugar substitutes market, with a projected CAGR of 4.12% through 2031. According to Statistisches Bundesamt, there were 226 active milk processing businesses in Germany as of 2023, with the increasing incorporation of sugar substitutes in dairy products driving market growth. Collaborative efforts among food manufacturers, academic institutions, and the government have effectively normalized the use of stevia and erythritol through well-funded consumer education initiatives. A notable reduction in sugar consumption among children underscores successful behavioral changes, ensuring consistent demand. Additionally, Germany hosts several fermentation campuses where major players like Cargill and ADM, along with numerous biotech startups, are advancing the production of novel glycosides.

France, Spain, Italy, and the United Kingdom collectively contribute to nearly half of the region's revenue. In France, reformulations in pastry and dairy products are driving demand for high-purity stevia imports. Italy's soft drink excise tax has heightened the urgency for reformulation, despite stringent oversight by EFSA. Meanwhile, the United Kingdom, operating its own novel food approval framework post-Brexit, occasionally approves certain molecules ahead of the European Union, providing a competitive advantage to early registrants.

Central and Eastern Europe have been slower to adopt sweetener alternatives due to income sensitivity. However, rising obesity rates and EU-wide labeling regulations are expected to accelerate adoption. In Scandinavia, the high penetration of organic products aligns with a preference for plant-derived sweeteners, encouraging retailers to stock sugar-free seasonal confections. Furthermore, the Rest of Europe segment is benefiting from increased local production investments, particularly in Benelux and the Balkans, driven by freight cost reductions and the impact of anti-dumping levies.

Competitive Landscape

The European sugar substitutes market is moderately fragmented, with numerous global food ingredient companies competing for market share. Prominent players include Cargill, Incorporated, The Archer-Daniels-Midland Company, Tate & Lyle PLC, Ingredion Inc., and Kerry Group plc leverage integrated portfolios of starches, sweeteners, and texturants to provide comprehensive reformulation solutions. The Avansya joint venture between Cargill and DSM-Firmenich has launched a 10,000 metric-ton Rebaudioside M production line, serving European beverage clients.

Emerging players are making strides in the market by scaling up the production of enzymatic tagatose and upcycled fructose, respectively. These innovations emphasize metabolic health benefits and align with the principles of a circular economy, addressing both consumer preferences and sustainability goals. Additionally, Ingredion’s life-cycle assessment highlights that farm-sourced stevia achieves a 56% reduction in greenhouse gas emissions compared to traditional cane sugar, providing buyers with a compelling Scope-3 sustainability proposition.

Market participants are increasingly adopting advanced competitive strategies, including the development of proprietary taste modulation technologies, the implementation of carbon labeling initiatives, and fostering strong relationships with grower communities to ensure sustainable sourcing. Efforts to mitigate supply-side risks are evident through initiatives such as the establishment of Greek stevia cooperatives and Spanish monk fruit pilot projects, which aim to minimize transportation distances and enhance supply chain efficiency. Furthermore, leading companies are expediting regulatory filings with the European Food Safety Authority (EFSA) and the United Kingdom Food Standards Agency to secure exclusivity periods, thereby strengthening their competitive positioning in the market.

Europe Sugar Substitute Industry Leaders

Cargill, Incorporated

The Archer-Daniels-Midland Company

Tate & Lyle PLC

Ingredion Inc.

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Tate and Lyle has completed its USD 1.8 billion acquisition of CP Kelco, positioning itself as a leading global provider of specialty food and beverage solutions with enhanced expertise in sweetening, mouthfeel, and fortification technologies.

- July 2024: Roquette has partnered with Bonumose to enhance the scalability of tagatose production. This collaboration combines Roquette's expertise in starch-based sweeteners with Bonumose's advanced enzymatic technology to address the increasing demand for low-glycemic sugar alternatives in confectionery applications.

- June 2024: Fooditive Group has introduced Keto-Fructose, a sweetener derived from apple and pear waste, aligning with circular economy principles. This sustainable sugar alternative is currently undergoing FDA GRAS assessment.

- July 2023: Tate and Lyle PLC, launched a new addition to its sweetener portfolio TASTEVA SOL Stevia Sweetener. An internationally patent-protected breakthrough in stevia technology, this addition expands Tate and Lyle’s ability to help customers solve stevia solubility issues in food and beverages and helps deliver on consumer demand for healthier and tastier, sugar and calorie-reduced products.

Europe Sugar Substitute Market Report Scope

The European sugar substitute market has segmented by origin, which includes natural and artificial/synthetic. Based on type, the market is segmented into high-intensity, low-intensity, and high fructose syrup. Based on the application, the market is segmented into food, beverage, and pharmaceutical. The report further analyses the regional scenario of the market, which includes a detailed analysis of the United Kingdom, France, Germany, Italy, Spain, Russia, and Rest of Europe.

By Product Type

| High-Intensity Sweeteners | Acesulfame Potassium |

| Advantame | |

| Aspartame | |

| Neotame | |

| Saccharin | |

| Sucralose | |

| Stevia | |

| Monk Fruit | |

| Other High-Intensity Sweeteners | |

| Sugar Polyols | Sorbitol |

| Xylitol | |

| Maltitol | |

| Erythritol | |

| Other Sugar Polyols |

By Origin

| Plant-Derived |

| Synthetic |

| Biotechnologically Fermented |

By Form

| Powder |

| Liquid |

By Application

| Food | Bakery and Cereals |

| Confectionery | |

| Dairy and Dairy Alternatives | |

| Sauces, Condiments and Dressings | |

| Other Food Applications | |

| Beverage | Carbonated Soft Drinks |

| RTD Tea and Coffee | |

| Sports and Energy Drinks | |

| Other Beverages | |

| Pharmaceuticals | |

| Other Applications |

By Country

| United Kingdom |

| Germany |

| Spain |

| France |

| Italy |

| Russia |

| Rest of Europe |

| By Product Type | High-Intensity Sweeteners | Acesulfame Potassium |

| Advantame | ||

| Aspartame | ||

| Neotame | ||

| Saccharin | ||

| Sucralose | ||

| Stevia | ||

| Monk Fruit | ||

| Other High-Intensity Sweeteners | ||

| Sugar Polyols | Sorbitol | |

| Xylitol | ||

| Maltitol | ||

| Erythritol | ||

| Other Sugar Polyols | ||

| By Origin | Plant-Derived | |

| Synthetic | ||

| Biotechnologically Fermented | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Food | Bakery and Cereals |

| Confectionery | ||

| Dairy and Dairy Alternatives | ||

| Sauces, Condiments and Dressings | ||

| Other Food Applications | ||

| Beverage | Carbonated Soft Drinks | |

| RTD Tea and Coffee | ||

| Sports and Energy Drinks | ||

| Other Beverages | ||

| Pharmaceuticals | ||

| Other Applications | ||

| By Country | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe sugar substitutes market?

The market is valued at USD 2.5 billion in 2026 and is expected to reach USD 2.89 billion by 2031.

Which country leads the market in both size and growth?

Germany holds 19.00% of revenue in 2025 and records the fastest national CAGR at 4.12% through 2031.

Which sweetener type is growing the quickest?

Sugar polyols are forecast to expand at an 7.92% CAGR from 2026 to 2031, driven by pharmaceutical and clean-label uses.

How does EU regulation influence market demand?

Sugar-reduction directives and higher excise taxes incentivise reformulation, directly boosting uptake of approved alternative sweeteners.

Page last updated on: