Fructo-Oligosaccharides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

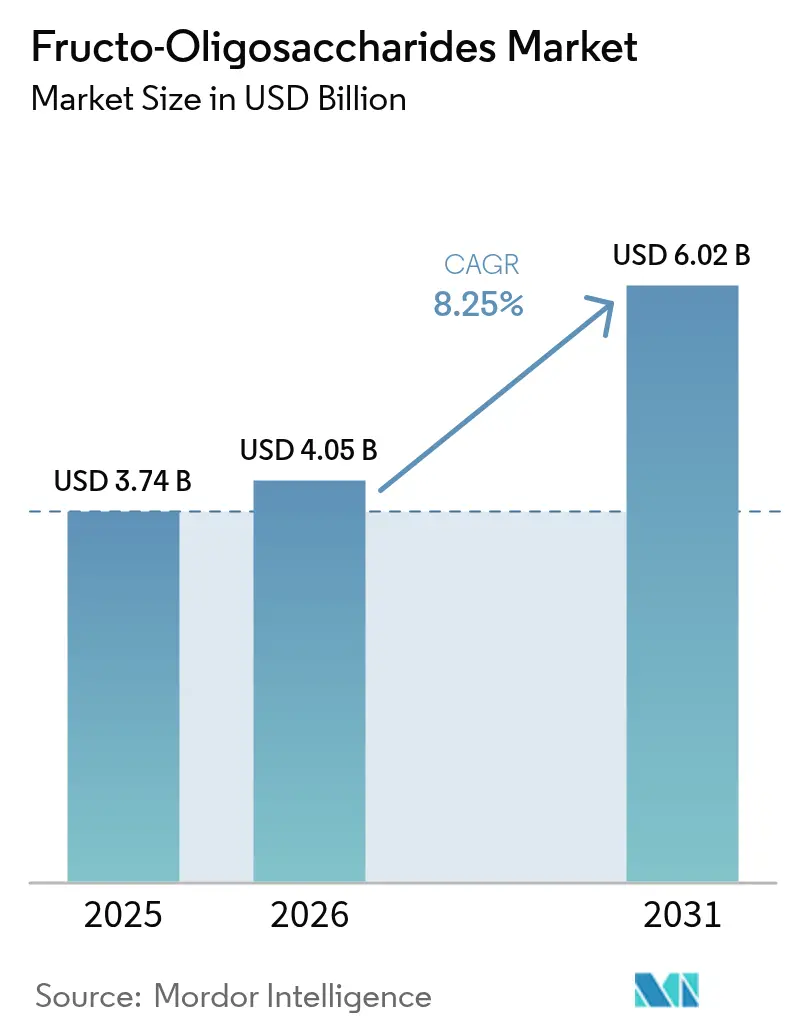

| Market Size (2026) | USD 4.05 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 8.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fructo-Oligosaccharides Market Analysis by Mordor Intelligence

The Fructo-Oligosaccharides Market size was valued at USD 3.74 billion in 2025 and is estimated to grow from USD 4.05 billion in 2026 to reach USD 6.02 billion by 2031, at a CAGR of 8.25% during the forecast period (2026-2031). This growth is primarily fueled by regulatory approvals that enable manufacturers to promote gut-health benefits. Furthermore, accelerated infant-formula standards now require specific oligosaccharide blends, while the pharmaceutical industry is actively exploring their use as microbiome-friendly excipients. Powder formats dominate the market due to their long shelf life across extended supply chains, while liquid and syrup formats are gaining popularity in ready-to-drink beverages for their instant solubility. Europe holds the largest revenue share, driven by strict clean-label regulations favoring naturally derived fibers. Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market, supported by a rising middle class opting for premium infant nutrition. Additionally, drug developers are becoming a significant buyer group, leveraging fructo-oligosaccharides as functional excipients to address antibiotic-associated dysbiosis and improve bioavailability.

Key Report Takeaways

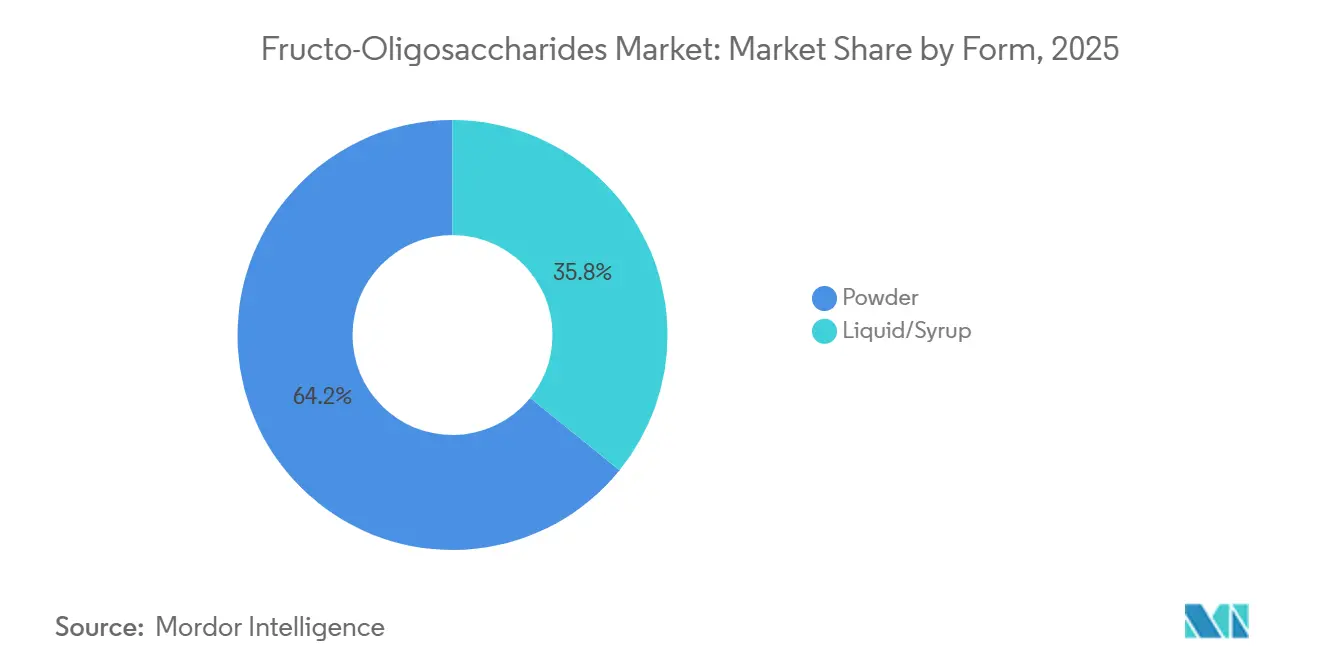

- By form, powder captured 64.17% of 2025 revenue, and liquid grades are forecast to expand at an 8.69% CAGR through 2031.

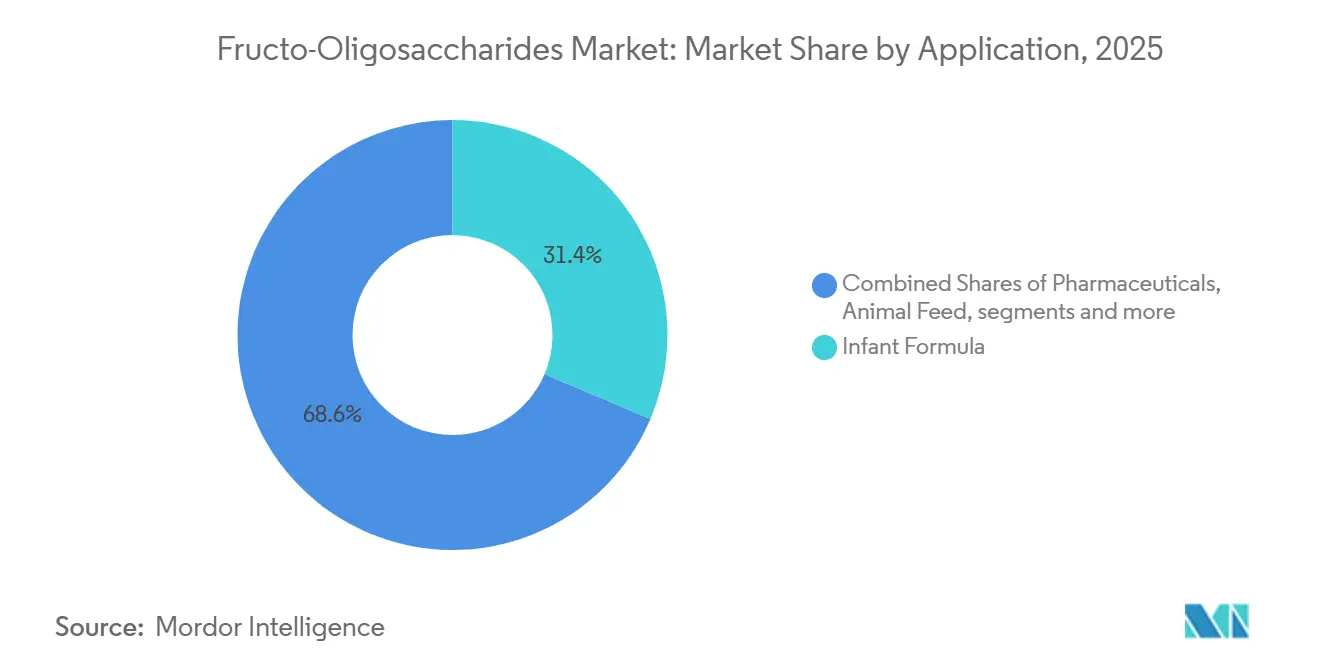

- By application, infant formula led with 31.38% share in 2025, while pharmaceuticals exhibit the fastest 9.57% CAGR for 2026-2031.

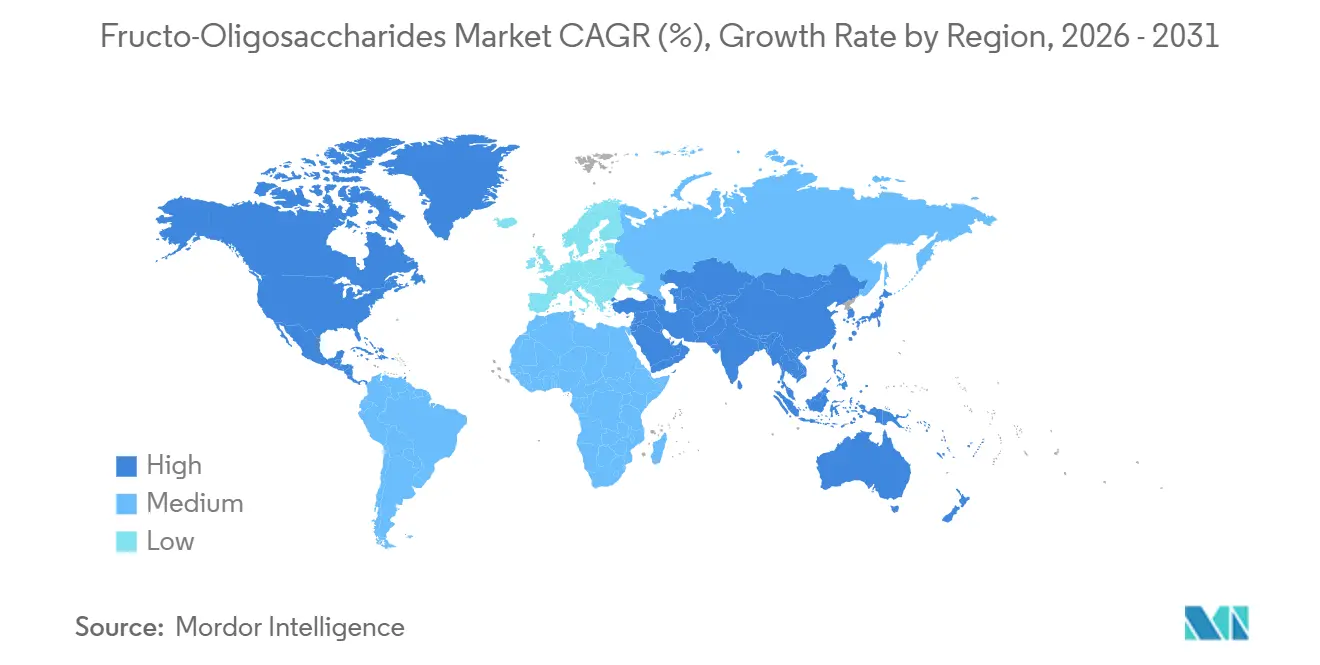

- By geography, Europe accounted for 34.97% of sales in 2025, and Asia-Pacific is advancing at a 10.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fructo-Oligosaccharides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for functional foods and dietary supplements | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing incorporation of FOS in infant nutrition formulas | +2.1% | Global, led by Asia-Pacific (China, Southeast Asia) and Europe | Short term (≤ 2 years) |

| Rising prevalence of lifestyle diseases | +1.5% | Global, acute in North America, Europe, and emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Rising gut-health and prebiotic awareness | +1.3% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Strategic collaborations and supply agreements | +0.9% | Global, with focal points in Europe and North America | Short term (≤ 2 years) |

| Industry investment in R and D to develop innovative synbiotic products | +0.7% | Global, concentrated in North America, Europe, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional foods and dietary supplements

Consumer spending on functional foods and dietary supplements is shifting from reactive sick-care to proactive wellness management, with prebiotics playing a crucial role in modulating gut microbiota composition. The International Food Information Council's Food and Health Survey 2024 indicates that nearly 67% of Americans consider healthfulness a key factor in their food and beverage purchasing decisions[1]Source: The International Food Information Council, "2024 IFIC Food & Health Survey,"ific.org. Regular Fructooligosaccharides (FOS) consumption is associated with improved mineral absorption, enhanced immune function, and better lipid profiles, benefits that appeal to aging populations in developed markets and health-conscious millennials in emerging economies. The European Food Safety Authority has approved health claims for oligosaccharides, enabling brands to highlight prebiotic benefits on product labels without regulatory challenges. This regulatory clarity is driving product innovation: dietary supplement manufacturers are incorporating 3 to 5 grams of FOS per serving into gut-health formulations, while functional beverage brands are adding liquid FOS syrups to ready-to-drink products, ensuring prebiotic fiber is delivered without affecting taste or mouthfeel. However, a major challenge persists in educating consumers about the difference between prebiotics and probiotics. This lack of awareness slows conversion rates despite strong clinical evidence supporting prebiotic benefits.

Increasing incorporation of FOS in infant nutrition formulas

Pediatric nutritionists have consistently worked to replicate the oligosaccharide profile of human breast milk, which contains over 200 structurally unique oligosaccharides that selectively support beneficial gut bacteria in infants. EU Regulation 2016/127 permits the use of fructo-oligosaccharide and galacto-oligosaccharide blends in infant formulas, with a maximum limit of 0.8 grams per 100 milliliters. These blends must adhere to a 90:10 GOS-to-FOS ratio, designed to mimic the prebiotic activity of human milk oligosaccharides. In 2024, China's National Health Commission updated its infant-formula standards to align with Codex Alimentarius guidelines. The National Bureau of Statistics of China reported 7.92 million births in China in 2025, creating a market opportunity for FOS-fortified products[2]Source: The National Bureau of Statistics of China, "Number of births per year in China", stat.gov.cn. Formulators prefer short-chain FOS over inulin-type fructans because shorter molecules dissolve more easily in reconstituted formula and generate less gas in immature digestive systems. This shift highlights that infant-formula demand is becoming less price-sensitive and more focused on specific formulations, benefiting suppliers capable of delivering pharmaceutical-grade FOS with low endotoxin levels and consistent batch quality.

Rising prevalence of lifestyle diseases

In 2024, the International Diabetes Federation estimated that approximately 589 million adults aged 20 to 79 were living with diabetes[3]Source: International Diabetes Federation, "Facts and figures", idf.org. With rising trends in obesity and non-alcoholic fatty liver disease, healthcare systems are shifting focus toward dietary interventions that address underlying metabolic dysfunctions rather than solely managing symptoms pharmacologically. Recent research indicates that short-chain fatty acids, produced through the microbial fermentation of FOS, improve insulin sensitivity by activating G-protein-coupled receptors in pancreatic beta cells and reducing systemic inflammation through histone deacetylase inhibition. This understanding has led endocrinologists and gastroenterologists to recommend 5 to 10 grams of daily prebiotic fiber as an adjunct therapy for patients with prediabetes and metabolic syndrome. The commercial potential lies in medical-nutrition products positioned at the intersection of food and pharmaceuticals. While this category commands premium pricing, it requires clinical validation and healthcare-professional endorsement to gain widespread acceptance.

Rising gut-health and prebiotic awareness

Public discourse has transitioned from academic journals to mainstream media, bringing attention to the microbiome-gut-brain axis. This transition is primarily driven by notable research linking gut dysbiosis to conditions such as depression, anxiety, and cognitive decline. In 2025, clinical trials demonstrated that an 8-week prebiotic supplementation with FOS significantly increased fecal bifidobacteria counts by 2 to 3 log units and reduced circulating inflammatory markers. These results were linked to improved mood scores and enhanced sleep quality. Surveys conducted in North America and Western Europe indicate that while adults are increasingly familiar with the term "prebiotic," many cannot differentiate it from probiotics or explain its mechanisms. This lack of awareness presents both challenges and opportunities: brands that focus on consumer education can foster loyalty and justify premium pricing, while those relying on vague "gut health" claims risk regulatory scrutiny and consumer skepticism. The strategic approach is to clearly communicate prebiotic benefits, such as “feeds good bacteria”, while grounding claims in peer-reviewed research and approvals from regulatory bodies like the FDA and EFSA.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and extraction costs | -0.8% | Global, acute in regions with high energy costs (Europe, Japan) | Medium term (2-4 years) |

| Consumer sensitivity related to low-FODMAP diets | -0.6% | North America, Europe, Australia (markets with high IBS diagnosis rates) | Short term (≤ 2 years) |

| Gastrointestinal tolerance issues at high dosages | -0.5% | Global, more pronounced in markets with high single-dose supplement consumption | Medium term (2-4 years) |

| Price sensitivity among end-users and manufacturers | -0.7% | Global, particularly acute in price-competitive emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High production and extraction costs

While the enzymatic synthesis of fructo-oligosaccharides (FOS) from sucrose using β-fructofuranosidase stands as the primary industrial method, it comes with notable cost challenges. These include the expenses of enzyme procurement or in-house production, energy-heavy purification processes like chromatography or membrane filtration, and a sucrose feedstock whose prices are tethered to global sugar market fluctuations. On the other hand, hydrolyzing chicory inulin presents a viable alternative, producing FOS with a purity of around 81%, compared to just 55% from the enzymatic method. However, this method's reliance on chicory root supplies introduces an added layer of risk tied to agricultural commodity prices. Furthermore, energy expenses for processes like spray drying and the cold-chain logistics needed for liquid syrups further strain profit margins. This is especially pronounced in regions like Europe and Japan, where industrial electricity rates surpass USD 0.15 per kilowatt-hour. In response, major producers are strategically positioning FOS plants in proximity to either sucrose refineries or chicory-processing sites, aiming to cut down on feedstock transport costs and secure volume discounts.

Consumer sensitivity related to low-FODMAP diets

Globally, 5% to 10% of adults are affected by irritable bowel syndrome (IBS). Randomized controlled trials conducted by Monash University and published in leading gastroenterology journals revealed that low-FODMAP dietary protocols—designed to limit fermentable oligosaccharides, disaccharides, monosaccharides, and polyols—alleviated symptoms in 50% to 80% of IBS patients. Fructo-oligosaccharides, categorized as high-FODMAP, create challenges for individuals on elimination diets, as they must avoid FOS-fortified foods and supplements during the initial restriction phase, which typically lasts 4 to 6 weeks. This dietary limitation generates a structural demand challenge in regions such as North America, Western Europe, and Australia, where IBS diagnosis rates are high, and dietitians frequently recommend low-FODMAP protocols as the primary treatment. As a result, brands must either develop FODMAP-free product lines or clearly disclose FOS content to retain the IBS patient segment. In response, some manufacturers are introducing tiered product offerings, standard formulations containing 5 grams of FOS per serving for general wellness consumers and FODMAP-compliant alternatives made with resistant starches or soluble corn fiber for sensitive individuals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Retains Leadership as Liquids Accelerate

In 2025, powder grades emerged as the leading segment in the Fructo-Oligosaccharides market, accounting for 64.17% of the total revenue. Their widespread adoption is attributed to their stability and compatibility with dry-blend infant formulas and solid-dose pharmaceuticals. These powders, characterized by their free-flowing and agglomerated properties, can withstand prolonged shipping durations without caking, making them highly reliable. This resilience and functionality have enabled powder grades to secure the largest market share. Looking forward to the period from 2026 to 2031, powder sales are anticipated to align closely with the overall market growth. This steady demand is primarily driven by the increasing popularity of sachet-based supplements, particularly across the Asia-Pacific region, where consumer preferences and health awareness are on the rise.

On the other hand, liquid and syrup grades are projected to achieve a robust compound annual growth rate (CAGR) of 8.69%, surpassing the overall market growth rate. This growth is fueled by the increasing demand from beverage and pediatric-syrup formulators who prioritize instant solubility in their products. Suppliers capable of offering both powder and liquid formats from a single facility gain a strategic advantage, as multinational food companies continue to streamline their vendor lists to enhance operational efficiency. High-solids syrups, which typically contain 70-75% solids, offer an optimal balance between viscosity and sweetness, making them a preferred choice in various applications. However, the production of these syrups requires energy-intensive concentration equipment, which poses significant capital investment challenges for new entrants attempting to penetrate the market.

By Application: Infant Formula Mature, Pharmaceuticals Surge

In 2025, infant formula accounted for 31.38% of total revenue, firmly establishing itself as the foundational segment of the Fructo-Oligosaccharides market. Although growth in volume terms is slowing due to declining birth rates, the increasing trend toward premium human-milk-oligosaccharide blends is driving value expansion within the segment. This segment continues to sustain a stable market size for Fructo-Oligosaccharides, primarily due to the near-universal adoption of 0.8 g/100 mL blends across key regions such as Europe, China, and several ASEAN countries.

Pharmaceutical applications are projected to witness the fastest growth among all tracked applications, with an anticipated CAGR of 9.57% during the forecast period from 2026 to 2031. The FDA’s GRAS Notice 717 has provided formulators with greater confidence to incorporate short-chain FOS as excipients in the production of antibiotic and probiotic capsules. Furthermore, clinical research linking FOS to a reduced risk of C. difficile infections strengthens the potential of this application. While dietary supplements, functional snacks, and animal feed represent smaller market segments, their collective contribution plays a crucial role in diversifying demand and mitigating over-reliance on the infant nutrition segment.

Geography Analysis

In 2025, Europe commanded a 34.97% share of the market, bolstered by its mature functional-food channels, stringent clean-label regulations favoring naturally derived prebiotics, and a well-entrenched infant-formula market where prebiotic fortification is the norm. The European Food Safety Authority's endorsement of oligosaccharide health claims has empowered brands to prominently feature prebiotic benefits on their labels. This regulatory clarity not only accelerates product launches but also boosts consumer acceptance. Leading the regional consumption are Germany, France, and the United Kingdom, thanks to their high per-capita spending on dietary supplements and functional foods. Meanwhile, Eastern European nations like Poland and Russia are emerging growth hotspots, buoyed by rising disposable incomes and the encroachment of Western retail formats. However, Europe grapples with market saturation: prebiotic use in infant formulas has surpassed 80%, and growth in dietary supplements is slowing as the market matures. In response, suppliers are pivoting towards pharmaceutical applications and premium synbiotic formulations, which offer higher margins compared to standard prebiotic powders.

From 2026 to 2031, the Asia-Pacific region is set to grow at a robust 10.03% CAGR, driven by a burgeoning middle class in China demanding premium infant nutrition. Japan's Foods for Specified Health Uses (FOSHU) framework is expediting prebiotic approvals, while India's Food Safety and Standards Authority is liberalizing fortification norms. In China, as parents increasingly seek infant formulas that mimic the oligosaccharide profile of human breast milk, there's a pronounced shift towards high-purity FOS, especially when blended with 2'-fucosyllactose and other human milk oligosaccharides. Japan's FOSHU system streamlines the process for manufacturers, allowing them to make health claims on prebiotic products post clinical evidence submission to the Consumer Affairs Agency. This has paved the way for swift market entry of FOS-fortified functional foods and beverages. In India, heightened health awareness and the rise of e-commerce are propelling the dietary supplement market, spurring demand for budget-friendly prebiotic powders and sachets. However, price sensitivity poses challenges, particularly in rural and semi-urban locales. Southeast Asian nations, notably Thailand, Indonesia, and Vietnam, are witnessing a surge in infant-formula sales and a swift embrace of functional foods among urban millennials.

In 2025, North America, South America, and the Middle East and Africa together made up the rest of the market share, with North America leading the pack. This dominance is attributed to its high consumption of dietary supplements and a robust functional-food retail landscape. In South America, countries like Brazil, Argentina, and Chile are slowly warming up to prebiotic-fortified products, thanks to rising disposable incomes and the spread of Western dietary habits. However, challenges like regulatory fragmentation and import tariffs hinder cross-border trade. Meanwhile, in the Middle East and Africa, demand for FOS is still in its infancy. Yet, urban hubs like Dubai, Riyadh, and Johannesburg, bolstered by their expatriate communities and affluent locals, are driving the consumption of imported functional foods and dietary supplements.

Regulatory Landscape

In the United States, fructo-oligosaccharides market access is commonly supported through the FDA voluntary GRAS notice pathway (21 CFR 170.35), where the agency issues a no-questions response rather than affirming GRAS status. Recent filings reinforce momentum in both mainstream foods and more tightly scrutinized infant nutrition: BENEO received an FDA no-questions letter for GRAS Notice GRN 001242 in July 2025, covering use of short-chain FOS across multiple food categories, and Tate & Lyle received an FDA no-questions letter for GRN 001271 in March 2026 for short-chain FOS use in cow-milk based, non-exempt infant formula for term infants.

In Europe, claims and labeling are governed by the EU framework for nutrition and health claims under Regulation (EC) No 1924/2006. This requires EFSA scientific evaluation before European Commission authorization and inclusion on the Union list. For infant formula specifically, EU Regulation 2016/127 permits blends of fructo-oligosaccharides and galacto-oligosaccharides with defined compositional limits (including a 0.8 g/100 mL maximum and a 90:10 GOS-to-FOS ratio), keeping supplier quality systems and documentation aligned with infant-nutrition compliance expectations.

Value Chain Analysis

The FOS value chain starts with feedstock sourcing and enzyme inputs, then moves through synthesis or hydrolysis, purification, finishing, and downstream distribution into food, beverage, dietary supplement, infant formula, and pharmaceutical channels. On the input side, manufacturers either convert sucrose via enzymatic biotransformation (using enzymes such as fructosyltransferase or beta-fructofuranosidase) to produce short-chain FOS, or hydrolyze inulin derived from crops such as chicory (Cichorium intybus) and Jerusalem artichoke (Helianthus tuberosus) to target longer-chain fractions.

Processing economics and quality are shaped by purification and drying requirements. Activated carbon, ion-exchange resins, adsorption media, and membrane filtration are used to remove mono-saccharides and by-products and to reach higher purities demanded by infant formula and pharmaceutical applications. Distribution typically runs through direct sales to multinational food and nutrition manufacturers and through ingredient distributors for smaller formulators; powder grades tend to be favored for long-distance logistics, while liquid or syrup formats require tighter handling and storage discipline. Agricultural variability in chicory or inulin supply and the technical challenge of separating reaction by-products remain recurring bottlenecks, sustaining investment in more efficient membrane and adsorption systems and reinforcing the advantage of larger, vertically integrated ingredient producers (such as Ingredion, Cargill, and BENEO) with scale, QA infrastructure, and regulatory-dossier capabilities.

Competitive Landscape

The Fructo-Oligosaccharides market is moderately fragmented, with approximately a dozen vertically integrated producers controlling the majority of enzymatic and chicory-root capacities. These market players distinguish themselves through three primary strategies: achieving cost leadership by situating feedstock production facilities in close proximity, enhancing product purity to meet pharmaceutical-grade standards, and pursuing rapid expansion in the Asia-Pacific region to capitalize on growing demand. Galam's upcoming plant, scheduled to commence operations in January 2026, is expected to increase global capacity by 15%. This development underscores the significant capital expenditure required to maintain competitiveness in the market. Additionally, the collaboration between BENEO and WACKER on 2′-FL reflects a strategic pivot toward higher-margin human-milk oligosaccharides, which serve as a complementary product line to their core FOS volumes.

Chinese manufacturers, such as Quantum Hi-Tech, are aggressively scaling their operations by leveraging lower production costs, thereby exerting downward pressure on commodity-grade pricing. In response, European companies are adopting a value-added approach by bundling services such as regulatory dossier preparation, co-development partnerships, and ISO 22000 accreditation. These efforts enable them to command a price premium of 20-30% over their competitors. Meanwhile, biotech start-ups are innovating by engineering microbes capable of fermenting FOS directly from cellulosic biomass. If successfully commercialized, this technology could reduce production costs by 30-40%, potentially disrupting the market in the long term. Furthermore, compliance with GMP and infant-formula standards has become a critical requirement, significantly raising entry barriers for smaller regional processors and new entrants.

Merger and acquisition activity in the market is centered around consolidating chicory-inulin assets and acquiring specialized enzyme technologies that can shorten synthesis cycles. Established suppliers face a strategic decision: whether to focus on defending their existing powder product volumes or to shift toward higher-value segments such as liquid syrups and synbiotics. While these segments offer the potential for higher EBITDA margins, they also require the development of new processing capabilities, presenting both opportunities and challenges for market participants.

Fructo-Oligosaccharides Industry Leaders

-

Cargill Inc.

-

Ingredion Incorporated

-

Tereos Group

-

Südzucker AG (BENEO)

-

Baolingbao Biological Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

High-purity FOS (95%+ content) remains a practical whitespace area for premium infant nutrition blends and for pharmaceutical excipient use cases where batch-to-batch consistency and impurity control are critical. This view is supported by tightening scrutiny in sensitive applications, including the US FDA no-questions letter issued to Tate & Lyle in March 2026 for GRAS Notice GRN 001271 covering short-chain FOS use in non-exempt infant formula for term infants, alongside broader food-category support such as BENEO's GRAS Notice GRN 001242 (July 2025). These pathways tend to favor suppliers that can pair application-specific specifications with documentation packages, allergen and contaminant controls, and validated analytical methods.

Technology and process intensification offer a second opportunity lane for cost and yield improvement, particularly for syrup grades used in beverages and pediatric formats. In January 2026, an EFSA safety evaluation for beta-fructofuranosidase (EC 3.2.1.26) from non-GM Aspergillus sp. ATCC 20611 supports expanded use of this enzyme class in FOS syrup production, and 2026 academic work reported high-content, high-concentration outputs in scaled systems (for example, a co-immobilized multi-enzyme approach reported 95.1% FOS content and 288.1 g/L concentration in a 200 L fermenter). Parallel demonstrations using lower-cost substrates, such as sugarcane molasses, point to a pathway to reduce dependence on refined sucrose and improve sustainability positioning, aligning with clean-label and sugar-reduction formulation programs in functional foods and beverages.

Recent Industry Developments

- June 2026: Ingredion announced the acquisition of Benicaros, expanding its prebiotic fiber portfolio alongside its sugar-reduction and texture offerings. While Benicaros is not a fructo-oligosaccharide, the move strengthens Ingredion's ability to supply broader prebiotic-fiber systems to beverage, dairy, and nutrition customers that also buy FOS. It increases competitive pressure on standalone FOS suppliers by shifting demand toward multi-fiber solution selling.

- July 2025: BENEO received an FDA no-questions letter for GRAS Notice GRN 001242 covering the use of short-chain fructo-oligosaccharides across a range of food categories, including beverages and dairy products, at specified inclusion levels. The clearance supports wider formulation latitude for brands that want to label prebiotic fiber benefits within US compliance norms. It also raises the importance of regulatory documentation and standardized specifications in supplier selection.

- January 2024: The EU infant-formula framework under Regulation (EU) 2016/127 continued to anchor global formulation practices for prebiotic blends by permitting fructo-oligosaccharide and galacto-oligosaccharide combinations with defined limits (including a 0.8 g/100 mL maximum and a 90:10 GOS-to-FOS ratio). This keeps demand concentrated among suppliers capable of delivering consistent, high-purity FOS suited to infant-nutrition QA requirements. The rule structure also shapes product development toward blend-ready grades rather than commodity fiber powders.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the fructo-oligosaccharides (FOS) market is defined as revenues generated from selling FOS ingredients used for prebiotic and functional benefits across food, nutrition, feed, and related uses, counted at the point of ingredient sale.

Scope exclusions: We exclude downstream finished-product retail value, in-house transfers not priced at market terms, and non-FOS prebiotic fibers that are not sold as FOS.

Segmentation Overview

-

Form

- Liquid/Syrup

- Powder

-

Application

- Infant Formula

- Fortified Food and Beverage

- Dietary Supplements

- Animal Feed

- Pharmaceuticals

- Other Applications (Cosmetics and personal care, Processed Meat)

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Poland

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Thailand

- Singapore

- Indonesia

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- South Africa

- Saudi Arabia

- Egypt

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean view of the demand pool and supply capacity, then aligning that view with what is realistically traded and consumed by end use. For sugar and chicory context, we rely on public and official references such as USDA and other national agriculture agencies. To map ingredient flows into and out of regions, we use UN Comtrade for trade flows of relevant carbohydrate inputs. For consumption and availability indicators, we reference FAO food balance style datasets. On the food and infant nutrition side, we cross-check positioning using Codex Alimentarius and FDA and EFSA pages for claim and use context. We also use scientific literature indexed on PubMed and similar peer-reviewed sources to validate common dosage ranges and recurring application patterns in foods and supplements.

On the company and pricing side, we review annual reports, investor presentations, press releases, and plant expansion updates to understand capacity additions and the commercial emphasis by form (powder versus syrup). For market signals that are not consistently published, we also use paid subscriptions that provide company financials and commercial intelligence, news and financials tracking, patent lookups, and shipment-level import or export views where available for the ingredient category. The desk sources listed here are illustrative only, and we use additional public and subscription references for cross-checks and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the model assumptions that desk sources cannot settle, especially price ranges by grade and form, typical contract structures, and how demand is split across infant nutrition, fortified foods, supplements, feed, and pharmaceuticals. We speak with ingredient manufacturers, distributors, and application-facing experts, and we also validate with formulators and procurement roles who see real usage rates and substitution behavior. For a global market, inputs were checked across APAC, EMEA, and the Americas so regional pricing and adoption differences were not averaged out.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 46% |

| Mid tier: 52% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 15% | Managers: 45% | Americas: 23% |

Market-Sizing & Forecasting

Sizing begins with a top-down build where production and trade indicators are used to reconstruct the available FOS ingredient pool by region, which is then allocated to major applications based on validated usage patterns. Once the demand pool is shaped, we corroborate it with selective bottom-up approximations, including sampled supplier revenue bands, distributor channel checks, and volume multiplied by realistic average selling prices (ASPs) for powder and syrup formats.

Key inputs that move the model include the mix shift between powder and liquid or syrup, the share of demand coming from infant formula and fortified foods, typical inclusion rates in formulations, and regional adoption of digestive health products. We also track the raw material context for sucrose and chicory-linked supply, since it can influence cost and pricing discussions. In parallel, we check trade direction changes to avoid overstating local consumption when a region is mainly re-exporting.

For forecasting, scenario analysis is used so the outlook can reflect different adoption speeds in functional foods and supplements, plus more cautious cases where pricing softens with capacity additions. The final path is selected after interviewing market participants on expected demand growth, form-factor preferences, and the pace of new product launches. Where bottom-up snapshots have gaps, for example private suppliers without clear revenue disclosure, those gaps are handled through conservative sampling and then normalized back to the top-down demand pool.

Data Validation & Update Cycle

Validation is handled through triangulation across independent signals, followed by variance checks at region and application level so one strong assumption does not distort the whole picture. We compare implied per-capita or per-industry consumption against trade patterns and capacity news, then review any outliers in ASPs or volume growth before sign-off.

A second analyst review is completed to re-check calculations, unit conversions, and currency handling. If the model shows unusual jumps, key assumptions are re-confirmed. Reports are refreshed annually, and interim updates are made when material events occur, such as large capacity expansions or notable regulatory changes affecting claims and labeling. Right before delivery, a fresh pass is completed so clients receive the latest updated view we can support.

Mordor Intelligence's Fructo Oligosaccharides Fos Market Sizing Compared With Other Published Estimates

Published market values for FOS can look far apart, even when they all sound like they cover the same ingredient category. The differences usually come from where the boundary is drawn, which applications are counted, and how pricing and volume are carried forward from the base year into the forecast.

By tracking form-level pricing and application-level inclusion rates, Mordor Intelligence keeps the total tied to an ingredient demand pool (not finished-product value), which helps explain why some estimates land higher when they include broader prebiotic fibers or retail sales proxies.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.74 B (2025) | |

| Industry Publisher A | USD 3.10 B (2024) | Uses a base-year view that can understate the 2025 demand lift, and its scope language often blends FOS with adjacent prebiotic ingredients across applications, which can shift what is counted. |

| Industry Publisher B | USD 3.07 B (2025) | Leans on broader forward assumptions with a longer forecast window and limited visibility on how ASPs by form are updated, which can keep the 2025 value lower when price progression is not refreshed with recent contract ranges. |

The table shows that most of the spread can be traced to scope boundaries and the year used for anchoring prices and volumes. When the model is built from clear application demand drivers and then cross-checked with practical supplier and channel signals, the resulting market size stays easier to reconcile and repeat from one update to the next.

Key Questions Answered in the Report

What is the projected value of the Fructo-Oligosaccharides market in 2031?

The sector is forecast to reach USD 6.02 billion by 2031 at an 8.25% CAGR from 2026.

Which format currently leads sales of fructo-oligosaccharides?

Powder grades held 64.17% of 2025 revenue thanks to superior shelf stability and ease of formulation.

Why are liquid FOS syrups gaining popularity?

Beverage and pediatric-syrup brands prefer liquids for instant solubility, driving an 8.69% CAGR in this sub-segment.

Which region will record the fastest growth through 2031?

Asia-Pacific is projected to expand at a 10.03% CAGR powered by premium infant-formula demand.

Page last updated on: