Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

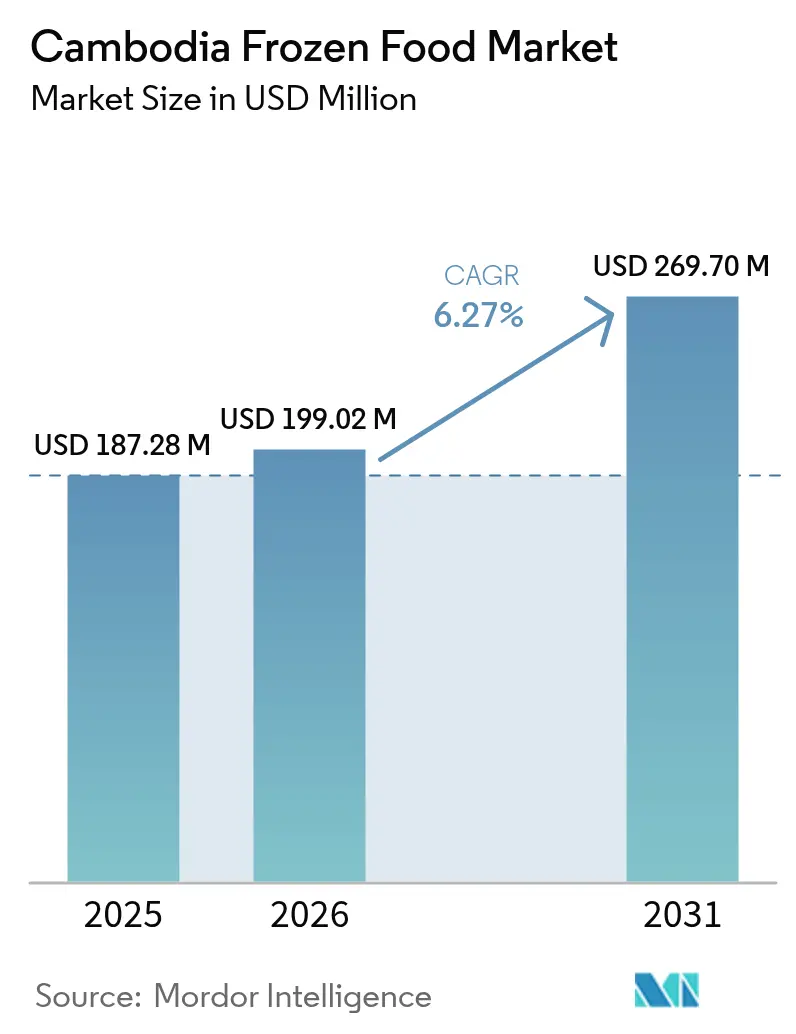

| Base Year Market Size (2025) | USD 187.28 Million |

| Market Size (2026) | USD 199.02 Million |

| Market Size (2031) | USD 269.7 Million |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

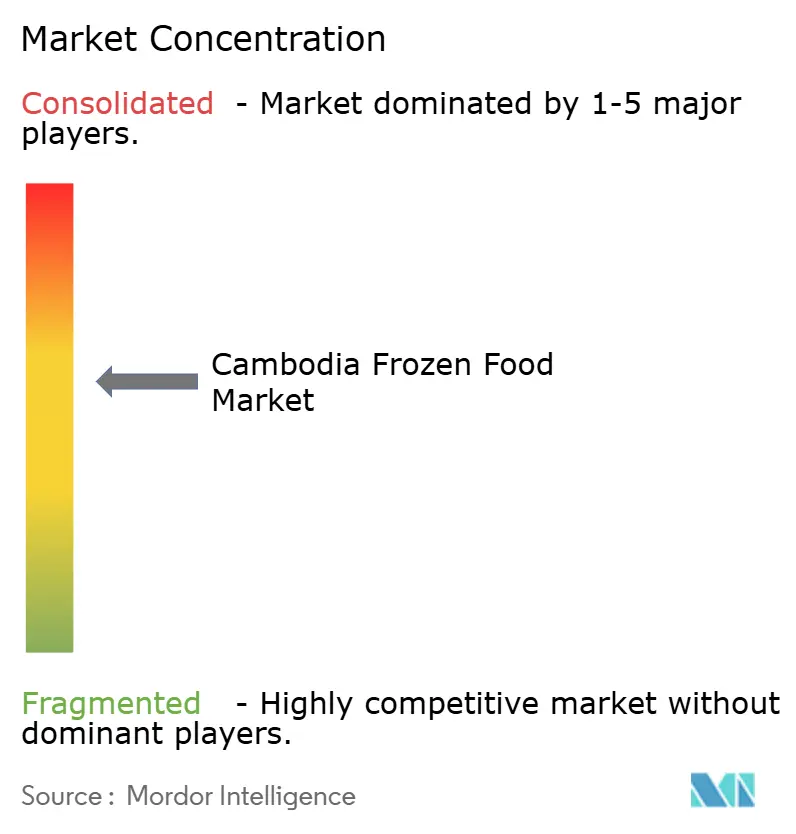

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cambodia Frozen Food Market Analysis by Mordor Intelligence

The Cambodia frozen food market size was valued at USD 187.28 million in 2025 and estimated to grow from USD 199.02 million in 2026 to reach USD 269.7 million by 2031, at a CAGR of 6.27% during the forecast period (2026-2031). Rising urbanization, a 79.5% female labor-force participation rate, and a 4.5% annual increase in the working-age population are driving demand for convenient frozen meals. Phnom Penh’s modern grocery space now exceeds 600,000 square meters, while tourist arrivals have recovered to 94.8% of pre-pandemic levels, boosting on-trade consumption of frozen seafood and desserts. Cold-chain developments, such as the 36,205-cubic-meter Kandal facility and the Fangchenggang–Koh Kong shipping lane launched in March 2025, have cut transit times by 30%, reducing spoilage risks. However, high electricity tariffs (USD 0.15 per kWh) and fragmented food-safety oversight pose challenges, manageable only by operators with strong capital or integrated supply chains.

Key Report Takeaways

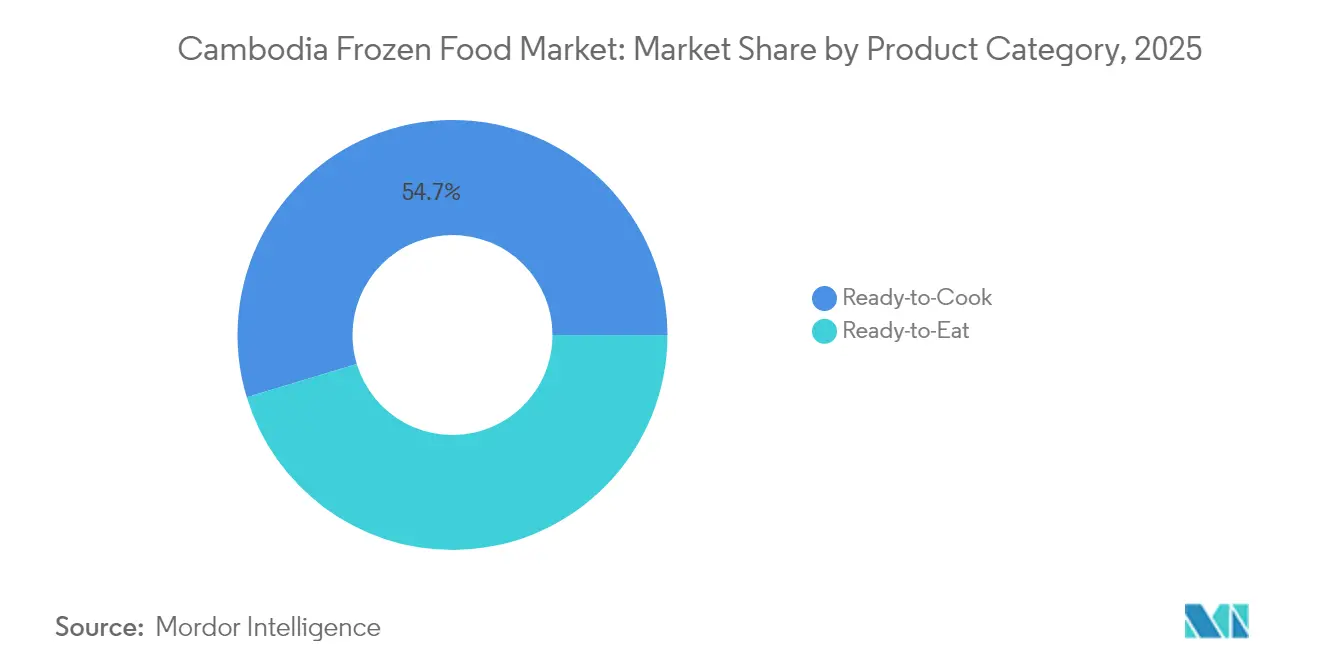

- By product category, ready-to-cook lines held 54.68% of the Cambodia frozen food market share in 2025, whereas ready-to-eat meals are set to outpace the total market at a 7.11% CAGR through 2031.

- By product type, frozen meat and seafood commanded 35.20% share of the Cambodia frozen food market size in 2025, while frozen fruits and vegetables are forecast to expand at a 6.86% CAGR over 2026-2031.

- By distribution channel, off-trade formats accounted for 69.34% of 2025 value, yet on-trade venues are projected to record the fastest 7.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Cambodia Frozen Food Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising urbanization and working population fueling convenience-food demand | +1.8% | Phnom Penh, Siem Reap, Sihanoukville | Medium term (2-4 years) |

| Expansion of cold-chain logistics infrastructure | +1.5% | National, with early gains in Phnom Penh and border provinces | Long term (≥4 years) |

| Proliferation of modern retail formats | +1.2% | Urban centers, expanding to secondary cities | Medium term (2-4 years) |

| Tourism growth boosting frozen seafood and meal demand in hospitality | +0.9% | Phnom Penh, Siem Reap, coastal provinces | Short term (≤2 years) |

| Government incentives for refrigeration investments | +0.6% | Special Economic Zones nationwide | Long term (≥4 years) |

| On-demand delivery apps driving home delivery of frozen foods | +0.4% | Phnom Penh, Siem Reap | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Urbanization and Working Population Fueling Convenience-Food Demand

In 2023, Cambodia had a female labor force participation rate of 79.5%, ranking among the highest in Asia[1]World Bank. "Cambodia Economic Update." World Bank Group, worldbank.org. However, 68% of working women reported not having enough time to prepare meals, driving demand for ready-to-consume frozen food options. Urban households have been spending more on convenience foods, with their share of the food budget increasing from 12% in 2020 to 18% in 2024. Additionally, the consumption of ready-to-eat meals among urban households grew by 25% between 2023 and 2024. The garment sector, a key part of Cambodia's economy, employs over 750,000 workers, most of whom are women. These workers, often working 48-hour weeks, increasingly rely on frozen meals to save time. Cambodia's population, which stood at 17.09 million in 2023, is expected to grow by 9.1% by 2033. Over the same period, the per capita GDP is projected to increase by 67%, expanding the middle-class consumer base for premium frozen products. In 2024, Thailand's ready-to-eat food exports to Cambodia accounted for 9.3% of Thailand's total RTE shipments. At the same time, Cambodia absorbed 20.3% of Thailand's instant noodle exports, reflecting strong cross-border supply chains that cater to the needs of time-constrained urban households.

Expansion of Cold-Chain Logistics Infrastructure

In 2024, PIDG launched its first cross-docking and cold-storage facility in Cambodia, marking a significant step in improving the country's logistics capabilities. To address the growing demand for cold storage, Kandal Cold Storage began constructing a 36,205-cubic-meter facility in 2022, aiming to close the gap toward the projected requirement of 140,000 cubic meters by 2030. The China-Cambodia cold-chain shipping route, scheduled to begin operations in March 2025, will connect Fangchenggang port to Koh Kong. This new route is expected to cut transit times for frozen seafood and vegetables from southern China by 30% compared to overland routes, enhancing efficiency in the supply chain. AEON secured a three-hectare lease at Sihanoukville Port to set up a logistics center, which will streamline imports and distribute frozen goods to its three malls in Phnom Penh. These malls collectively offer over 98,000 square meters of gross leasable area, supporting AEON's growing retail operations. Furthermore, in 2022, USAID pledged USD 2 million to collaborate with the Kampot Chamber of Commerce and Amru Rice on cold-chain pilot projects for agricultural exports. This initiative not only supports agricultural exports but also strengthens infrastructure for inbound frozen food distribution, showcasing the importance of donor-backed investments in Cambodia's cold-chain sector.

Proliferation of Modern Retail Formats

In December 2022, AEON MALL 3 debuted in Phnom Penh, backed by a USD 289.6 million investment. This expansion pushed the city's total retail space beyond 600,000 square meters. Notably, AEON MALL 3 introduced dedicated frozen-food sections, equipped with walk-in freezers, setting a new standard that traditional wet markets struggle to match. By 2024, modern retail's share of grocery sales climbed to 15%, a significant jump from 8% in 2020. This growth was fueled by supermarkets and hypermarkets venturing into secondary cities, extending their reach beyond just Phnom Penh and Siem Reap. Data from 2024 reveals a stark urban-rural divide in retail access: 29% of urban households now shop at mini-marts, a stark contrast to just 4% in rural areas. Betagro, with its branded Betagro Shop outlets in Phnom Penh and Siem Reap, is directly catering to consumers. By offering frozen, ready-to-cook chicken and pork products, Betagro is sidestepping traditional wet-market intermediaries. As of 2024, retail occupancy in Phnom Penh was at 70.7%. This statistic underscores the potential for further growth, especially as developers set their sights on middle-income neighborhoods. Here, they're introducing smaller-format convenience stores, with a focus on stocking frozen snacks and desserts.

Tourism Growth Boosting Frozen Seafood and Meal Demand in Hospitality

Tourist arrivals in the first half of 2024 rose by 22.7% year-over-year, reaching 94.8% of pre-pandemic levels, as reported by the Asian Development Bank[2]Asian Development Bank. "Asian Development Outlook 2024: Cambodia." adb.org . This growth was largely driven by the recovery in tourism and the expansion of the manufacturing sector. The CAMFOOD & CAMHOTEL 2024 expo, held in November, attracted over 150 exhibitors and 12,000 visitors. The event showcased frozen seafood and ready-meal products tailored to meet the needs of hotel and restaurant buyers. Cambodia's hospitality sector primarily sources frozen shrimp, squid, and white fish from Thailand and Vietnam. In 2022, 44% of globally traded aquatic products were frozen, ensuring a steady supply for hotels in both coastal and urban areas throughout the year. The Ministry of Tourism forecasts that international arrivals will exceed pre-pandemic levels by late 2025, driving sustained demand for frozen seafood platters and pre-portioned meal components, which help reduce kitchen labor costs. Siem Reap's hotel occupancy rates recovered to 75% in 2024, while frozen dessert consumption in hospitality channels increased as operators focused on ensuring consistent quality and extended shelf life compared to fresh alternatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented food-safety enforcement across the supply chain | -0.7% | National, with acute gaps in rural provinces | Long term (≥4 years) |

| Consumer perception of frozen food as less fresh/healthy | -0.5% | Rural areas and traditional urban neighborhoods | Medium term (2-4 years) |

| High electricity tariffs increasing operating costs | -0.9% | National, especially Phnom Penh and industrial zones | Short term (≤2 years) |

| Limited cold-storage capacity | -0.6% | National, with bottlenecks at border crossings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Food-Safety Enforcement Across the Supply Chain

Cambodia introduced its Law on Food Safety in June 2022, appointing the Ministry of Commerce as the primary authority. However, enforcement responsibilities are divided among the Ministry of Agriculture, Forestry and Fisheries, the Ministry of Health, and the Ministry of Industry, Science, Technology and Innovation. This division has led to overlapping roles and challenges in ensuring compliance. In 2022, only 25.8% of the population had access to safely managed drinking water, increasing the risk of contamination throughout the cold chain. Cambodia reported just two notifications to the International Food Safety Authorities Network (INFOSAN) in both 2020 and 2021, suggesting potential underreporting of foodborne disease outbreaks. A 2024 WHO case study documented over 7,000 cases of foodborne illnesses between 2014 and 2023, emphasizing that fragmented surveillance systems hinder effective traceability, especially for frozen products. Furthermore, the USDA's 2024 Food and Agricultural Import Regulations report highlighted that high-risk frozen fish and meat are subject to 100% inspection at ports. However, delays caused by limited laboratory capacity increase the risk of spoilage during the clearance process.

High Electricity Tariffs Increasing Operating Costs

Cambodia introduced its Law on Food Safety in June 2022, appointing the Ministry of Commerce as the primary authority. However, enforcement responsibilities are divided among the Ministry of Agriculture, Forestry and Fisheries, the Ministry of Health, and the Ministry of Industry, Science, Technology and Innovation. This division has led to overlapping roles and challenges in ensuring compliance. In 2022, only 25.8% of the population had access to safely managed drinking water, increasing the risk of contamination throughout the cold chain. Cambodia reported just two notifications to the International Food Safety Authorities Network (INFOSAN) in both 2020 and 2021, suggesting potential underreporting of foodborne disease outbreaks. A 2024 WHO case study documented over 7,000 cases of foodborne illnesses between 2014 and 2023, emphasizing that fragmented surveillance systems hinder effective traceability, especially for frozen products. Furthermore, the USDA's 2024 Food and Agricultural Import Regulations report highlighted that high-risk frozen fish and meat are subject to 100% inspection at ports. However, delays caused by limited laboratory capacity increase the risk of spoilage during the clearance process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Dual-Income Households Accelerate Ready-to-Eat Adoption

In 2025, Ready-to-Cook products accounted for 54.68% of the Cambodia Frozen Food Market. This dominance is driven by consumers' familiarity with frozen chicken, pork, and seafood, which require minimal effort beyond thawing and cooking. As shoppers shift from traditional wet markets to modern retail, they tend to prefer frozen raw proteins that align with their usual purchasing habits. Additionally, middle-income households, being price-conscious, often choose bulk-pack frozen meats over higher-priced ready-to-eat meals. CP Cambodia is expanding its ready-to-cook poultry and pork production with three new food processing plants, building on its Kampot facility established in May 2022. This expansion leverages the parent company's vertically integrated feed-to-retail model, which generated THB 4,539 million in revenue from Cambodia in 2024. Similarly, Betagro opened a feed mill in Phnom Penh in November 2024, with an annual capacity of 216,000 tons. This facility strengthens Betagro's ability to supply contract farmers producing frozen ready-to-cook chicken for both domestic and export markets.

From 2026 to 2031, Ready-to-Eat products are projected to grow at a 7.11% CAGR, outpacing the overall market. This growth is fueled by the increasing number of dual-income households, which now make up 62% of urban families, prioritizing convenience over cost. With 79.5% of women participating in the labor force in 2023 and 68% of working women reporting limited time for meal preparation, there is a growing demand for frozen meals that only require microwave reheating. Urban spending on convenience foods rose from 12% of household food budgets in 2020 to 18% in 2024, while ready-to-eat meal consumption increased by 25% between 2023 and 2024. In 2024, Cambodia accounted for 9.3% of Thailand's ready-to-eat exports. Thai processors are efficiently using cold-chain corridors along the border to supply Phnom Penh's AEON malls and modern supermarkets. Ajinomoto, with its strong manufacturing presence across ASEAN and a history of acquiring frozen-food companies like France's Labeyrie Traiteur Surgelés, is well-positioned to capitalize on this growing demand.

By Product Type: Seafood Dominance Meets Vegetable Velocity

In 2025, Frozen Meat and Seafood accounted for 35.20% of the market share in Cambodia. This strong performance is due to Cambodia's location between Thailand and Vietnam, two major aquaculture producers. These countries supply frozen shrimp, pangasius, and squid through well-established cross-border trade routes. A new cold-chain shipping route, launched in March 2025, connects Fangchenggang in China to Koh Kong, Cambodia. This route reduces transit times for frozen seafood by 30% compared to overland routes, minimizing spoilage risks and allowing Cambodian distributors to access Chinese tilapia and shellfish at competitive prices. Vinh Hoan Corporation, Vietnam's largest pangasius producer, reported revenue of VND 10,700 billion (approximately USD 421 million) in 2024. The company exports to 140 countries and includes Cambodia in its regional distribution network, leveraging its proximity to supply Phnom Penh's modern retail chains.

Frozen Fruits and Vegetables are expected to grow at a 6.86% CAGR from 2026 to 2031, the fastest growth rate among all product types. This growth is driven by increasing health awareness and the expansion of modern retail stores, which now allocate freezer space for imported berries, mixed vegetables, and pre-cut tropical fruits. Cambodia imports most of its frozen vegetables from China (45%), followed by Thailand (30%) and Vietnam (15%). In 2024, frozen vegetable exports from China to Cambodia grew by 18% year-over-year as Chinese processors focused on ASEAN markets. Thailand's frozen fruit exports to Cambodia reached USD 8.2 million in 2023, a 15% increase from 2022, while Vietnamese frozen vegetable exports totaled USD 5.6 million in 2023. This reflects rising demand from hotels, restaurants, and catering businesses that require year-round ingredient availability. AEON MALL, with three locations in Phnom Penh, stocks premium imported frozen items such as broccoli, cauliflower, and berry mixes. These products, while priced higher, appeal to health-conscious consumers and expatriates.

By Distribution Channel: Off-Trade Dominance Yields to On-Trade Momentum

In 2025, Off-Trade channels dominated the Cambodia Frozen Food Market with a 69.34% share. These include supermarkets, hypermarkets, convenience stores, online platforms, and traditional retail formats catering to households. AEON’s three malls in Phnom Penh, with over 98,000 square meters of leasable space, feature frozen-food sections with walk-in freezers. Its logistics center at Sihanoukville Port streamlines imports and distribution. Modern retail penetration in grocery retail rose to 15% in 2024, up from 8% in 2020, driven by supermarket expansions and more convenience stores in urban areas. Online food delivery also grew significantly, with Foodpanda leading the market, followed by NHAM24. Consumers preferred frozen snacks and single-serve meals over bulk purchases. Grab’s acquisition of a stake in Nham24 in December 2024, approved by Cambodia's Competition Commission, signals sector consolidation and potential growth in frozen-food offerings.

On-Trade channels, including hotels, restaurants, and catering services, are projected to grow at a 7.73% CAGR from 2026 to 2031, the fastest among distribution channels. Tourism recovery and new hotel projects are driving demand for frozen seafood, pre-portioned proteins, and desserts. Tourist arrivals in the first half of 2024 rose 22.7% year-over-year, reaching 94.8% of pre-pandemic levels. The CAMFOOD & CAMHOTEL 2024 expo in November attracted over 150 exhibitors and 12,000 visitors, with suppliers showcasing frozen products tailored for hotels and restaurants. Siem Reap’s hotel occupancy recovered to 75% in 2024, boosting frozen dessert consumption due to their longer shelf life. Siam Canadian Group, a Thailand-based frozen seafood processor, reported THB 15 billion (USD 430 million) in 2024 revenue and invested THB 800 million in cold-storage expansion during 2023-2024 to support regional hospitality clients, including Cambodian hotels and resorts.

Geography Analysis

In 2025, Cambodia's pivotal role in ASEAN's frozen-food trade saw imports led by China at 34.60%, followed by Vietnam at 13.10% and Thailand at 12.65%. A new cold-chain shipping route, inaugurated in March 2025, connects Fangchenggang in China to Koh Kong in Cambodia. This route, reducing transit times by 30% compared to land corridors, allows Cambodian distributors to source frozen seafood, vegetables, and processed meats from southern China, benefiting from decreased logistics costs. In 2024, U.S. agricultural exports to Cambodia reached USD 105.73 million, securing a 4.6% market share. Notably, after a year-long ban, imports of frozen pork offal from the U.S. resumed in March 2025, presenting fresh opportunities for American suppliers in the hospitality and food-service sectors.

Phnom Penh and Siem Reap lead domestic consumption trends. Phnom Penh boasts all three AEON malls and over 600,000 square meters of retail space. Meanwhile, Siem Reap's hospitality sector, driven by tourism, sources frozen seafood and desserts for its hotels and restaurants. Coastal provinces like Sihanoukville and Koh Kong act as gateways for imported frozen goods. AEON's three-hectare logistics center at Sihanoukville Port streamlines these inbound shipments for distribution nationwide. While urban areas see 11% of households purchasing frozen foods online, rural provinces lag, with only 2% online adoption and 82% relying on mobile vendors. Border provinces near Thailand and Vietnam leverage cross-border cold-chain infrastructure. A notable initiative is the USAID-backed USD 2 million pilot project, in collaboration with Kampot Chamber of Commerce and Amru Rice, enhancing refrigerated logistics for both agricultural exports and incoming frozen foods.

In regional trade dynamics, Thailand stands out as the primary supplier of ready-to-eat meals and instant noodles to Cambodia. In 2024, Cambodia imported 20.3% of Thailand's instant noodle exports and 9.3% of its ready-to-eat shipments. However, border tensions between 2024 and 2025 intermittently disrupted these supply chains, nudging Cambodian importers to seek alternatives in Vietnam and China. Despite a 28% dip in Vietnam's pangasius exports from January to September 2023, Vinh Hoan Corporation, boasting a 2024 revenue of VND 10,700 billion (around USD 421 million), continues to view Cambodia as a strategic node in its regional distribution, capitalizing on its proximity to supply Phnom Penh's modern retail chains.

Competitive Landscape

The Cambodia frozen food market is moderately consolidated, shaped by the presence of a few established regional manufacturers and strong import-driven brands that collectively command a significant share of retail and foodservice channels. Key players include CP Cambodia Co., Ltd., Betagro Co., Ltd., Ajinomoto Co., Ltd., Tyson Foods, Inc., and Khmer Angkor Food Co., Ltd. These players benefit from well-developed supply chains, cold-storage capabilities, and partnerships with modern retail formats such as supermarkets, hypermarkets, and convenience stores, giving them a competitive edge in nationwide reach. Their ability to maintain consistent product availability and quality further strengthens brand recognition among urban consumers who increasingly seek convenience-oriented food options.

At the same time, mid-sized local processors are gradually expanding their presence by offering competitively priced frozen meats, seafood, and ready-to-cook items tailored to Cambodian taste preferences. However, the high cost of cold-chain infrastructure, regulatory compliance, and reliance on imported raw materials create barriers for smaller businesses aiming to scale. These constraints limit market fragmentation and reinforce the dominance of brands with financial resources and operational maturity. Importers, particularly those supplying frozen poultry, seafood, and vegetables from Thailand, Vietnam, and China, also play an important role in shaping category availability.

Overall, competition in the market revolves around pricing efficiency, supply reliability, and the ability to cater to rising demand in the hotel, restaurant, and café (HoReCa) sector. As Cambodia’s urbanization accelerates and modern retail expands, established players are focusing on improving storage capacities, diversifying product portfolios, and strengthening distributor partnerships. This dynamic sustains a moderately consolidated structure, where a handful of well-positioned companies continue to shape growth and category development across the country.

Cambodia Frozen Food Industry Leaders

-

Betagro Co., Ltd.

-

Ajinomoto Co., Ltd.

-

Tyson Foods, Inc.

-

Khmer Angkor Food Co., Ltd.

-

Charoen Pokphand Foods Public Company Limited (CPF)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Phnom Penh Foodies has launched Cambodia’s first non‑powdered organic frozen yoghurt store in Phnom Penh, positioned as a low‑sugar, low‑fat “healthy dessert” option. It indicates a move away from powdered mixes toward fresher, more natural frozen yoghurt formats in the local market.

- July 2024: Yolé, one of the leading frozen dessert brands, opened its third store in Cambodia, known for its vibrant culture and natural beauty. The brand claims that it is committed to delivering Premium taste with its high-quality, zero-dairy, zero-sugar-added desserts, ensuring a healthy treat for everyone.

Cambodia Frozen Food Market Report Scope

The Cambodia frozen food market is segmented by product type and distribution channel. By product type, the scope includes frozen meat and seafood, frozen dessert, frozen fruit and vegetable, frozen ready meal, and other product types. By distribution channel, the market studied is segmented into hypermarket/supermarket, traditional grocery store, online channel, and other distribution channels.

By Product Category

| Ready-to-Eat |

| Ready-to-Cook |

By Product Type

| Frozen Fruits and Vegetables |

| Frozen Meat and Seafood |

| Frozen Ready Meals |

| Frozen Snacks and Bakery |

| Frozen Desserts |

| Other Product Types |

By Distribution Channel

| On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Online Stores | |

| Other Retail Formats |

| By Product Category | Ready-to-Eat | |

| Ready-to-Cook | ||

| By Product Type | Frozen Fruits and Vegetables | |

| Frozen Meat and Seafood | ||

| Frozen Ready Meals | ||

| Frozen Snacks and Bakery | ||

| Frozen Desserts | ||

| Other Product Types | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Online Stores | ||

| Other Retail Formats | ||

Key Questions Answered in the Report

How fast is the Cambodia frozen food market expected to grow to 2031?

It is projected to post a 6.27% CAGR, taking value from USD 199.02 million in 2026 to USD 269.7 million by 2031.

Which product category leads current sales?

Ready-to-cook items account for 54.68% of 2025 value, reflecting consumer familiarity with frozen raw proteins.

What segment will expand the quickest?

Ready-to-eat meals are forecast to register the highest 7.11% CAGR through 2031, driven by dual-income urban households.

How is e-commerce affecting distribution?

Platforms such as Nham24 and Grab now reach 11% of urban grocery spend, enabling rapid home delivery of frozen snacks and meals.

Page last updated on: