Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

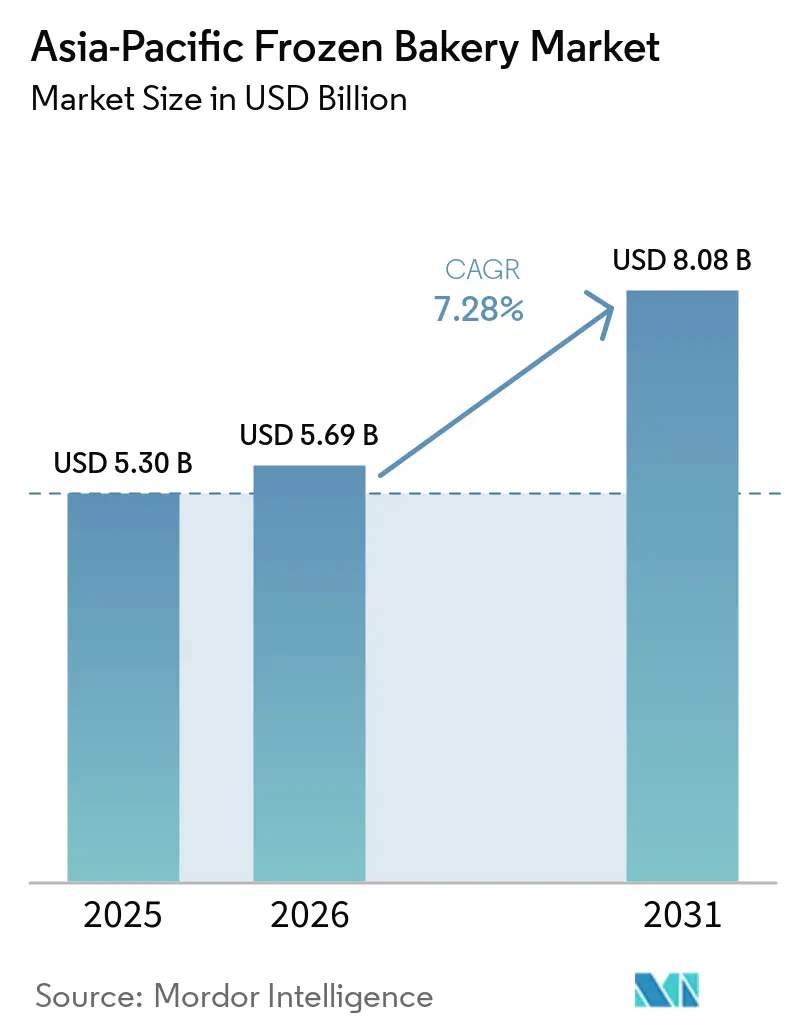

| Base Year Market Size (2025) | USD 5.30 Billion |

| Market Size (2026) | USD 5.69 Billion |

| Market Size (2031) | USD 8.08 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

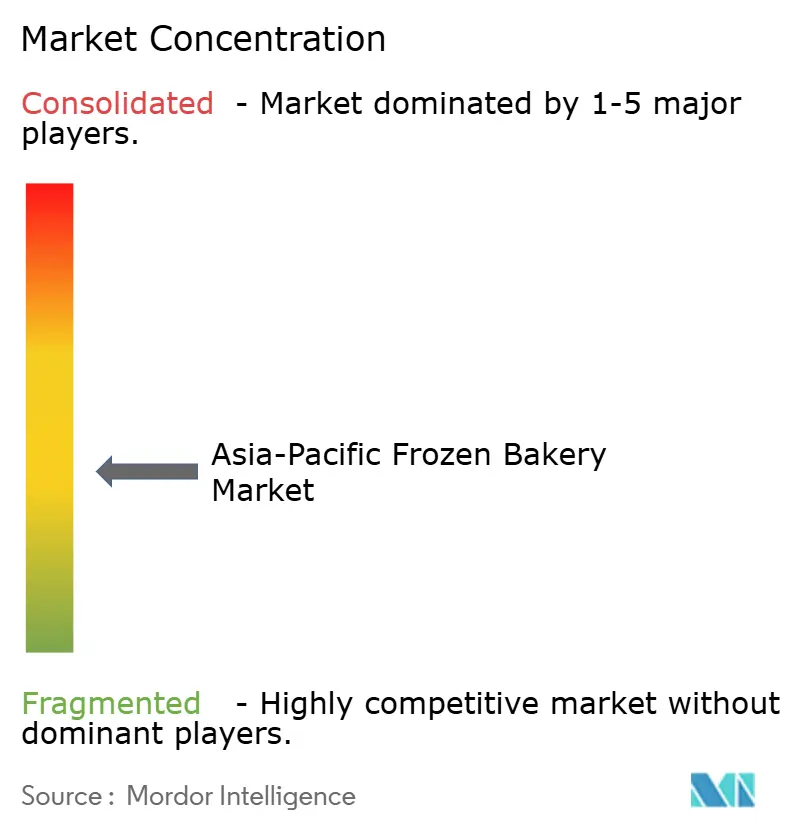

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Frozen Bakery Market Analysis by Mordor Intelligence

The APAC frozen bakery market size is expected to grow from USD 5.3 billion in 2025 to USD 5.69 billion in 2026 and is forecast to reach USD 8.08 billion by 2031 at 7.28% CAGR over 2026-2031. The APAC frozen bakery market benefits from rapid urbanization, expanding cold-chain networks, and premiumization trends that shift consumer demand toward artisanal, health-focused products. Growing convenience store penetration supports on-the-go breakfast habits, while bake-off technologies enable retailers to combine operational efficiency with a “fresh-baked” shopping experience. Multinational manufacturers leverage scale to roll out ready-to-bake formats, whereas regional specialists capture local-flavor niches. E-commerce and home-cooking habits that linger post-pandemic further fuel retail channel uptake of frozen baked goods[1]U.S. Department of Commerce, “Indonesia Cold Chain Industry,” trade.gov. Collectively, these dynamics underpin sustained momentum for the APAC frozen bakery market through the forecast period.

Key Report Takeaways

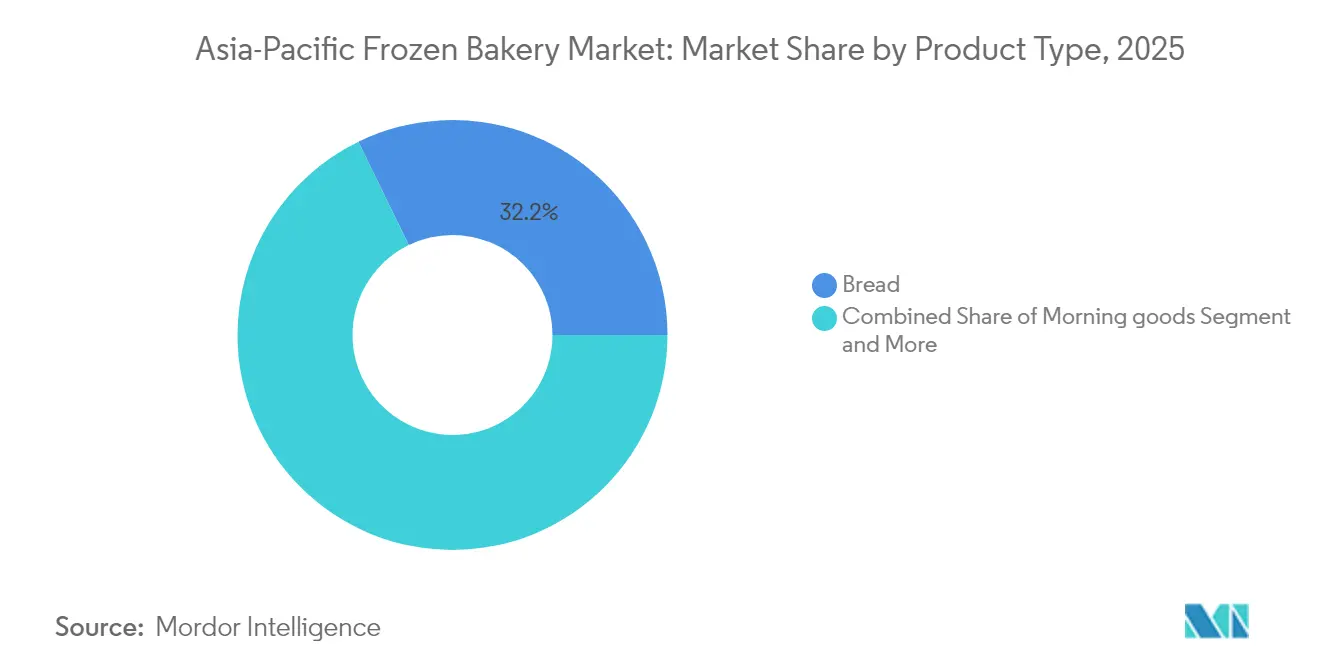

- By product type, bread retained 32.21% of the APAC frozen bakery market share in 2025, while morning goods are forecast to expand at a 9.52% CAGR through 2031.

- By form, ready-to-cook commanded 37.28% share of the APAC frozen bakery market size in 2025; ready-to-bake is projected to accelerate at 8.84% CAGR between 2026 and 2031.

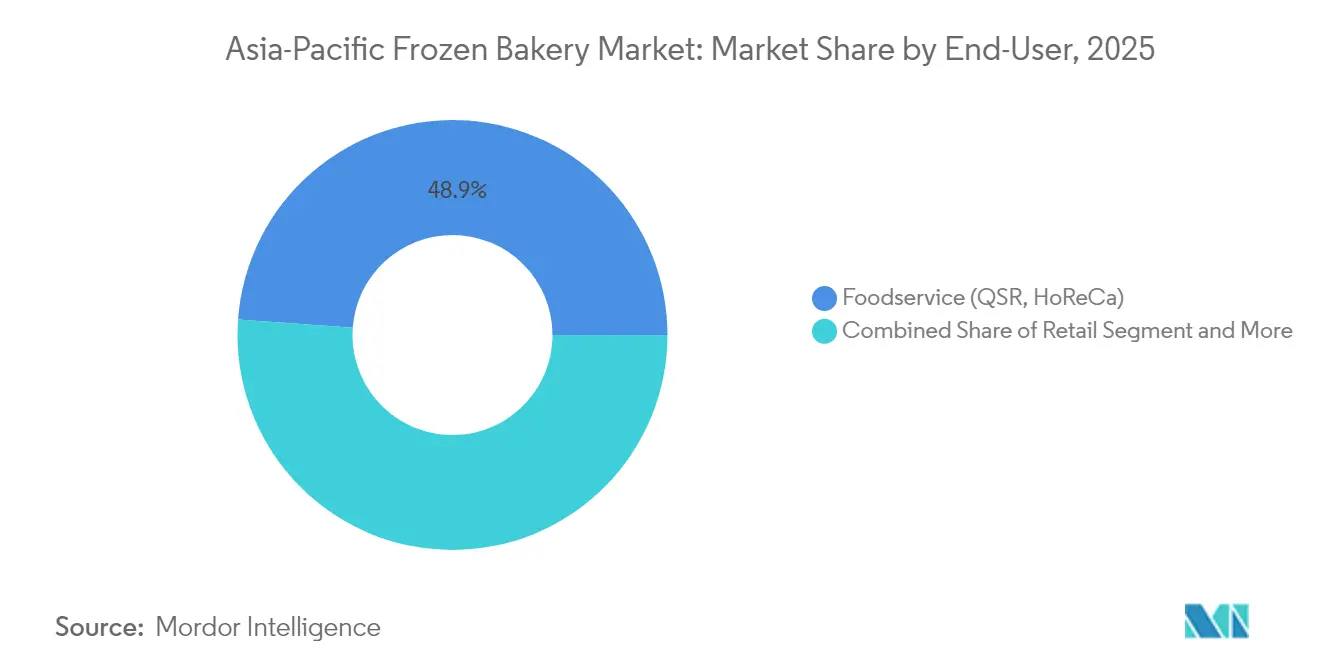

- By end use, foodservice accounted for 48.86% of the APAC frozen bakery market size in 2025, while retail/household leads growth at 9.01% CAGR.

- By geography, China held 37.22% revenue share in 2025; Indonesia is advancing at a 10.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Frozen Bakery Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient breakfast and snacking options | + 2.1% | Urban China, Indonesia, Philippines | Short term (≤ 2 years) |

| Expansion of cold-chain logistics and bake-off equipment penetration | + 1.8% | Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| Premiumization and health-driven NPD | + 1.5% | Japan, Australia, Singapore, urban China, South Korea | Medium term (2-4 years) |

| Retail adoption of in-store thaw-and-serve programs | + 1.2% | Core APAC convenience chains | Short term (≤ 2 years) |

| Local-flavor hybrids gain acceptance | + 0.9% | Malaysia, Thailand, Philippines | Long term (≥ 4 years) |

| Enhanced customization for product formats | + 0.4% | Japan, Australia, urban China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Convenient Breakfast and Snacking Options

Urban migration fuels single-person households and time-pressed routines, making portable, thaw-and-serve bakery items a staple of daily consumption. Convenience-store majors are scaling aggressively; Seven & i Holdings alone targets 100,000 stores worldwide by 2030[2]Convenience Store Association, “Seven & i Eyes New Regions,” convenience.org, creating an extensive last-mile grid for frozen pastries. South Korean chains such as GS25 have validated premium frozen dessert collaborations, revealing shoppers’ willingness to pay for indulgent formats. Indonesia's middle class, heading toward 135 million consumers by 2030, magnifies regional volume potential for Southeast Asia bakery products as expanding incomes meet better refrigeration coverage. Producers equipped with flexible cold-chain networks and portion-controlled SKUs gain a durable edge as breakfast behaviors evolve from fresh-baked daily purchases to stock-and-serve freezer staples.

Expansion of Cold-Chain Logistics and Bake-Off Equipment Penetration

Cold-chain infrastructure development represents a critical enabler for frozen bakery market expansion, particularly in emerging APAC economies where inadequate refrigeration historically constrained market penetration. Indonesia exemplifies this transformation, with government and private sector investments addressing cold-chain inefficiencies that previously caused up to 31% post-harvest losses for temperature-sensitive products. Lotte Global Logistics' USD 55 million investment in a cold-chain distribution center in Vietnam's Dong Nai Province, scheduled for full operation by May 2026[3]MK News, “Global Bakery Goods in Convenience Stores,” mk.co.kr, demonstrates the scale of infrastructure investments required to support frozen product distribution across Southeast Asia. The integration of advanced monitoring technologies, including real-time temperature sensors and blockchain-based traceability systems, addresses quality assurance concerns that previously limited consumer acceptance of frozen bakery products. Bake-off equipment penetration in retail environments enables the "fresh-baked" positioning that bridges the quality perception gap between frozen and fresh products, with retailers adopting ready-to-bake formats that require minimal skilled labor while maintaining artisanal appearance. The Philippines Cold Chain Project, supported by USDA funding from 2013-2018, provides a template for public-private partnerships that accelerate infrastructure development in markets where private investment alone proves insufficient.

Premiumisation & Health-Driven New Product Development

Health consciousness among APAC consumers drives demand for functional bakery products incorporating protein fortification, gluten-free formulations, and clean-label ingredients. South Korean food conglomerates exemplify this trend, with Shinsegae Food launching probiotic rice bread using domestically milled rice flour and patented gluten-degrading probiotics, achieving 12% month-over-month sales growth and cumulative sales exceeding 600,000 units. SPC Group's collaboration with the University of Helsinki to develop Nordic-style whole-grain fermentation processes for its premium health-bakery brand 'Paran Label' demonstrates the technical sophistication required to address texture and taste challenges in healthier formulations. Protein fortification emerges as a particularly compelling opportunity, with General Mills expanding its protein product lineup through launches like Cheerios Protein, delivering 8 grams of protein per serving to address rising consumer demand for protein-enhanced foods. Ajinomoto's partnership with Shiru to develop sweet proteins up to 5,000 times sweeter than sugar represents next-generation ingredient innovation that could enable significant sugar reduction without compromising taste profiles. The integration of functional ingredients requires sophisticated supply chain management and regulatory compliance across diverse APAC jurisdictions, creating competitive advantages for manufacturers with established ingredient sourcing networks and technical capabiliti

Retail Adoption of In-Store Thaw-and-Serve Programmes

Retailers increasingly adopt thaw-and-serve frozen bakery programs that eliminate traditional barriers to offering fresh-baked products while reducing labor costs and operational complexity. Baker Boy's launch of The Donut Hole® Thaw & Serve donut line, featuring fully finished products requiring only thawing, demonstrates the commercial viability of zero-preparation frozen bakery solutions for convenience stores. The company's USD 11 million investment in donut-line modernization, increasing capacity from 5,000 to 22,000 donuts per hour, reflects the scale advantages achievable through centralized production and frozen distribution. CraftMark Bakery's 345,000 square foot highly automated facility with seven production lines and 500 million pounds annual capacity illustrates the industrial infrastructure supporting thaw-and-sell cookie programs and ready-to-eat flatbreads for foodservice and in-store bakery markets. Puratos' development of specialized ingredient systems for Pre-Fermented Frozen and Par-Baked Frozen applications addresses technical challenges related to gluten protection during frozen storage and color development during final baking. The adoption of bake-off technologies represents approximately 20% of baked goods production in Europe, with 3% annual growth projected in stable markets, suggesting significant expansion potential in developing APAC markets where modern retail penetration continues to accelerate.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fresh-versus-frozen quality perception gap | -1.4% | Global, particularly pronounced in traditional markets like Japan, rural China | Medium term (2-4 years) |

| Rising energy & refrigeration costs in emerging markets | -0.8% | Indonesia, Philippines, Vietnam, Thailand | Short term (≤ 2 years) |

| Tariff and regulatory risk on imported butter/dairy inputs | -0.6% | China, Indonesia, Malaysia, with spillover to regional supply chains | Short term (≤ 2 years) |

| Carbon-footprint rules targeting high-energy frozen supply chains | -0.4% | Australia, Japan, Singapore, with expanding influence across APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fresh-versus-Frozen Quality Perception Gap

Consumer perception challenges regarding frozen bakery quality relative to fresh alternatives constrain market penetration despite technological advances in freezing and preservation techniques. Traditional bakery cultures in markets like Japan and rural China maintain strong preferences for daily-fresh products, creating resistance to frozen alternatives even when nutritional and taste profiles prove comparable. The Real Bread Campaign's distinction between "real bread" and industrial bread made through processes like Chorleywood, which affects approximately 80% of UK breads, illustrates how processing methods influence consumer perception and acceptance. Gardenia Philippines' implementation of G-Lock color-coded packaging systems that indicate baking dates represents industry efforts to bridge freshness perception gaps through transparency and visual cues. The challenge extends beyond consumer education to encompass operational execution, as temperature fluctuations during distribution and inadequate in-store handling can compromise product quality and reinforce negative perceptions. Overcoming these barriers requires sustained investment in consumer education, supply chain optimization, and product innovation that demonstrably matches or exceeds fresh product attributes while maintaining the convenience advantages that justify frozen formats.

Rising Energy & Refrigeration Costs in Emerging Markets

Escalating energy costs and refrigeration infrastructure expenses create significant operational headwinds for frozen bakery distribution, particularly in emerging APAC markets where electricity reliability and pricing remain challenging. Commercial refrigeration equipment markets face high initial costs, with walk-in cooler installations ranging from USD 3,000 to USD 9,000 and average repair costs between USD 100 and USD 325, creating barriers for smaller retailers and distributors. Indonesia's cold-chain industry confronts energy availability challenges outside Java, Bali, and Sumatra, despite solar energy options, while adoption of energy-efficient and low-GWP refrigerants remains limited due to low awareness and delayed regulatory guidance. The Move to -15°C Coalition's advocacy for resetting frozen food temperature standards from -18°C to -15°C demonstrates industry efforts to reduce energy consumption, with research indicating potential energy savings of 25 TWh annually and supply-chain cost reductions of 5-12%. However, regulatory approval and consumer acceptance of modified temperature standards require extensive validation and coordination across supply chain participants. Rising energy costs particularly impact smaller market participants who lack economies of scale in refrigeration infrastructure, potentially accelerating market consolidation toward larger players with more efficient cold-chain operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Morning Goods Drive Premium Positioning

Bread maintained a 32.21% share in 2025, cementing its status as a staple across diverse dietary cultures. The APAC frozen bakery market size for bread reflects efficient large-scale production and broad retail reach. Yet morning goods such as muffins, pancakes, and sweet buns are forecast for a 9.52% CAGR, outpacing all other categories. Morning goods satisfy an experiential breakfast trend tied to café culture in metropolitan centers from Shanghai to Sydney. Lotus Bakeries’ forthcoming Biscoff facility in Thailand demonstrates capital commitment to satisfy demand for premium coffee-paired treats. Partnerships between Lotus Bakeries and Mondelēz in India envision co-branded chocolate applications that can migrate into frozen pastry shells, illustrating cross-category growth synergies.

Morning goods also carry functional upgrades, including high-protein waffles and reduced-sugar Danish pastries enabled by sweet protein technology. As portion-controlled indulgence gains traction among health-conscious millennials, the APAC frozen bakery market keeps bread as its volume bedrock yet leans on morning goods for value elasticity and brand storytelling. The blend of indulgence and health credentials positions this sub-segment as a profit driver through 2031.

By Form: Ready-to-Bake Gains Retail Traction

Ready-to-cook formats held 37.28% share in 2025, anchored in foodservice routines where consistency and speed trump retail theater. The APAC frozen bakery market share for ready-to-cook remains solid, but ready-to-bake is set for a 8.84% CAGR as modern grocery chains install ventless ovens that deliver fresh aromas onsite. Ingredient houses such as Puratos supply dough matrices engineered for freeze-thaw stability, allowing even small stores to guarantee oven spring and golden crust every time.

European precedence shows bake-off already accounts for 20% of bakery output, offering a learning curve for APAC adopters. Dawn Foods’ strategic divestment of its AMEAP frozen pastry lines signals a pivot toward higher-margin components that support in-store baking programs. The combination of elevated shopper experience and reduced skilled-labor dependency reshapes the competitive map within the APAC frozen bakery market.

By End Use: Retail Channels Accelerate Growth

Foodservice operators—QSR, hotels, and catering—controlled 48.86% of value in 2025. Scale procurement and standardized SKUs keep this channel central to volume throughput. However, retail/household demand will expand at 9.01% CAGR, narrowing the gap as consumers stock freezers for flexible meal planning. Convenience-store momentum is pivotal: Indomaret and Alfamart exceed 35,000 Indonesian outlets combined, offering shelf access to impulse freezer snacks.

Innovations in moisture-retaining films and portion-controlled packaging lengthen shelf life and enable at-home microwave or air-fryer preparation without compromising crust quality. As households seek restaurant-style pastry experiences at lower cost, the APAC frozen bakery market channels more SKUs into retail multipacks. Compliance hurdles, such as Indonesia’s halal-certification deadline in October 2024, segment suppliers by regulatory readiness but ultimately strengthen consumer trust in certified brands.

Geography Analysis

China leads the APAC frozen bakery market with a 37.22% share in 2025. Rising disposable incomes, Western breakfast adoption, and nationwide cold-chain grids keep demand robust. Bakery sales at warehouse clubs such as Sam’s Club surpassed CNY 2.75 billion in 2023, while frozen equivalents cost 30-80% of fresh options, cementing value appeal. However, China’s stringent customs checks elevate compliance costs and favor multinationals with robust QA.

Indonesia is the fastest-growing territory at 10.31% CAGR. Middle-class expansion to 135 million people by 2030, plus targeted cold-chain incentives, turns the archipelago into a high-priority battleground. Convenience chains add roughly 1,000 stores yearly, widening freezer reach. Ingredient supply gaps—Indonesia imports 65% of processed-food inputs—create open lanes for exporters of butter, cheese, and pre-fermented dough.

Japan and Australia exhibit mature, premium orientation where freshness expectations test frozen propositions. Success rests on high-tech freeze processes and sensory parity to artisan bread. Meanwhile, Vietnam, Thailand, and the Philippines remain infrastructure-limited yet investment-rich. Lotte’s Vietnamese hub will improve regional frozen logistics by 2026. Thailand’s attraction of Biscoff manufacturing highlights policy consistency and skilled labor supply.

Competitive Landscape

The APAC frozen bakery market features moderate fragmentation. Global leaders such as Lantmännen Unibake, Grupo Bimbo, General Mills, Yamazaki Baking, and Aryzta AG compete with regional champions like BreadTalk and Goodman Fielder. Aryzta’s Food Rest of World division posted CHF 2.19 billion in revenue in 2024 with a 19.3% EBITDA margin, showcasing profitability in diverse Asian footprints.

Investment in production upgrades remains a core tactic. McCain Foods has committed USD 30 million to expand its Nebraska plant with energy-efficient lines, underscoring its capacity for APAC exports. Lotus Bakeries’ Thai facility exemplifies “produce-in-Asia, sell-to-Asia” localization to cut freight costs and align flavors. Ingredient innovation partnerships, including Ajinomoto-Shiru sweet proteins, grant early-mover rights in reduced-sugar formulations.

Consolidation persists. Flowers Foods acquired Simple Mills for USD 795 million to expand its health-centric offerings, while Conagra bought Pinnacle Foods for $10.9 billion to strengthen its frozen brand portfolio. Such deals illustrate capital deployment to secure premium portfolios that align with sustainability and wellness priorities shaping the APAC frozen bakery market.

Asia-Pacific Frozen Bakery Industry Leaders

Lantmännen Unibake

Grupo Bimbo

General Mills

Yamazaki Baking

Aryzta AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Japan’s PanforYou has launched its frozen bread ‘PANSUKU Box Kyoto’ in Singapore, marking the company’s first international venture. The product features a selection of breads from a Kyoto bakery and leverages Singapore’s established frozen delivery services and robust café culture.

- April 2024: Yamazaki has announced the expansion of its bakery production facility at the Kizuna Serviced Factory in Vietnam, doubling its production scale after four years of successful local operation.

Asia-Pacific Frozen Bakery Market Report Scope

Freezing is a procedure that assists in preserving food items from the time it has been cooked to when it is consumed. The Asia-Pacific frozen bakery market offers frozen bakery products in various forms, including bread, cakes and pastries, pizza crust, and morning goods. Each product type is retailed through supermarkets/hypermarkets, convenience stores, departmental stores, online retailing, and other distribution channels. The report offers market size and forecast for processed meat in value (USD million) for all the above segments.

By Product Type

| Bread |

| Cakes and Pastries |

| Pizza Crust |

| Morning Goods |

| Viennoiserie and Danish |

| Other Product Types |

By Form

| Ready to Cook |

| Ready to Bake |

| Ready to Proof |

| Ready to Eat |

By End Use

| Foodservice (QSR, Bakeries, HoReCa, Catering) | |

| Retail/ Househod | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Specialty Bakery Stores | |

| Online Retail / E-commerce | |

| Others |

By Geography

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Indonesia |

| Thailand |

| Malaysia |

| Vietnam |

| Philippines |

| Singapore |

| New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Bread | |

| Cakes and Pastries | ||

| Pizza Crust | ||

| Morning Goods | ||

| Viennoiserie and Danish | ||

| Other Product Types | ||

| By Form | Ready to Cook | |

| Ready to Bake | ||

| Ready to Proof | ||

| Ready to Eat | ||

| By End Use | Foodservice (QSR, Bakeries, HoReCa, Catering) | |

| Retail/ Househod | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Specialty Bakery Stores | ||

| Online Retail / E-commerce | ||

| Others | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Vietnam | ||

| Philippines | ||

| Singapore | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the APAC frozen bakery market in 2026?

The APAC frozen bakery market size is valued at USD 5.69 billion in 2026.

What is the forecast CAGR for frozen bakery products across APAC?

The APAC frozen bakery market is projected to grow at a 7.28% CAGR from 2026 to 2031.

Which product category grows fastest within frozen bakery?

Morning goods, including muffins and sweet buns, are expected to expand at 9.52% CAGR through 2031.

Which sales channel outpaces others in growth?

Retail and household consumption is set to rise at 9.01% CAGR as convenience stores proliferate across the region.

Which APAC country offers the highest growth potential for frozen bakery?

Indonesia leads with a projected 10.31% CAGR, driven by middle-class expansion and cold-chain investment.

Page last updated on: