Frozen Bakery Additives Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 2.22 Billion |

| Market Size (2030) | USD 2.99 Billion |

| Growth Rate (2025 - 2030) | 6.14% CAGR |

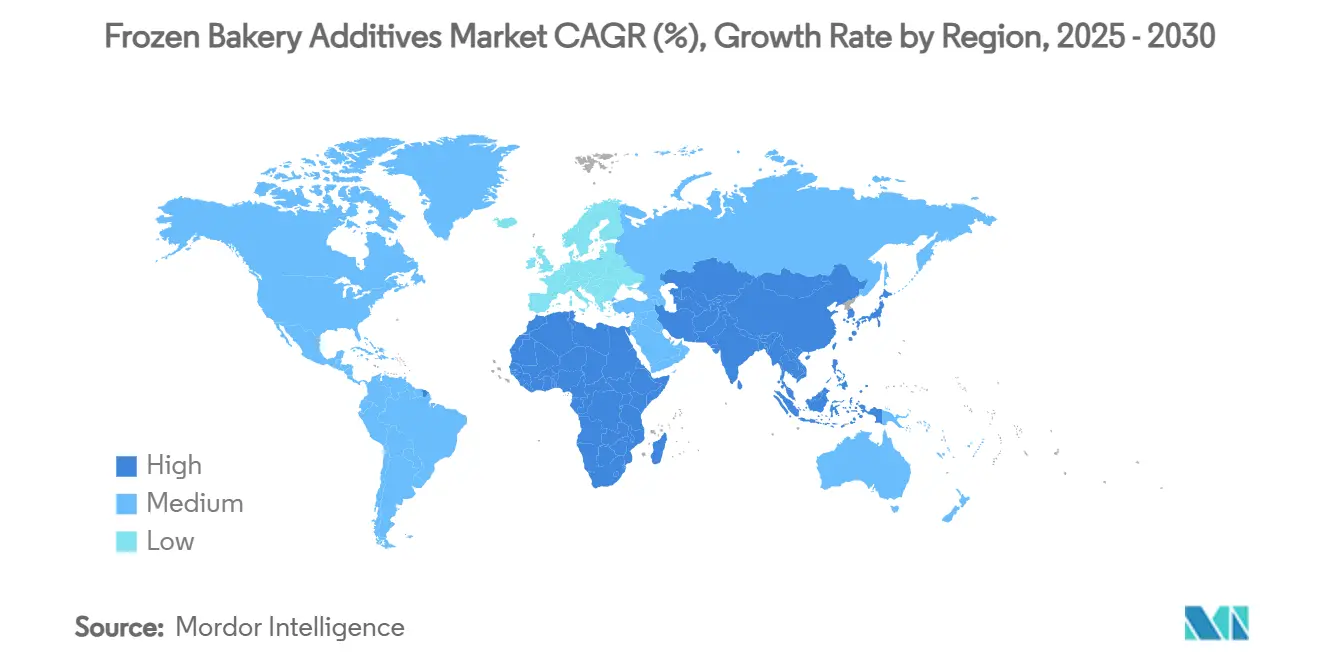

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

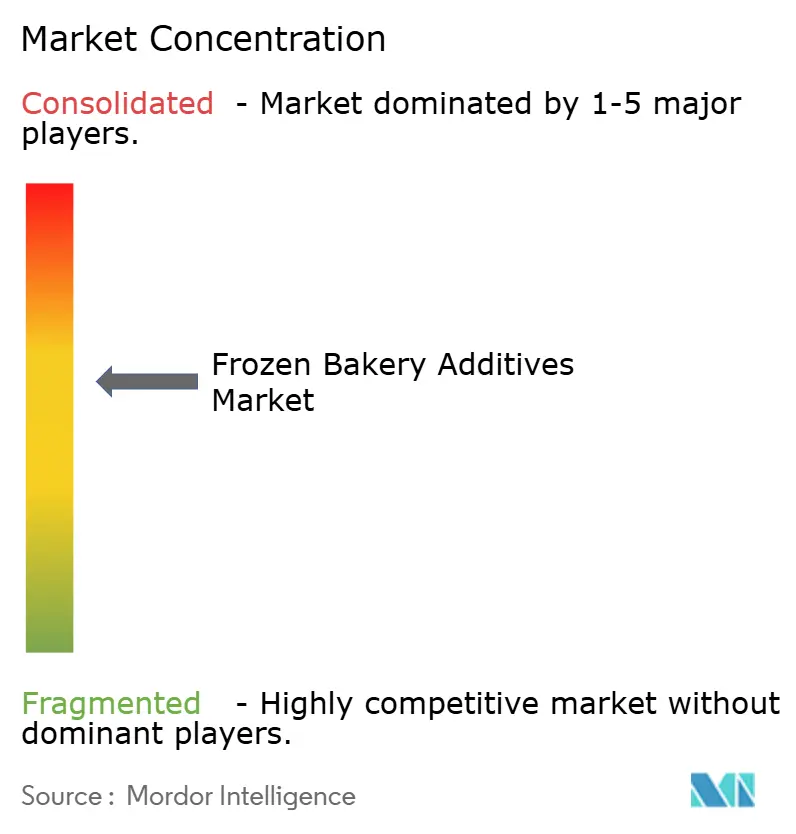

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frozen Bakery Additives Market Analysis by Mordor Intelligence

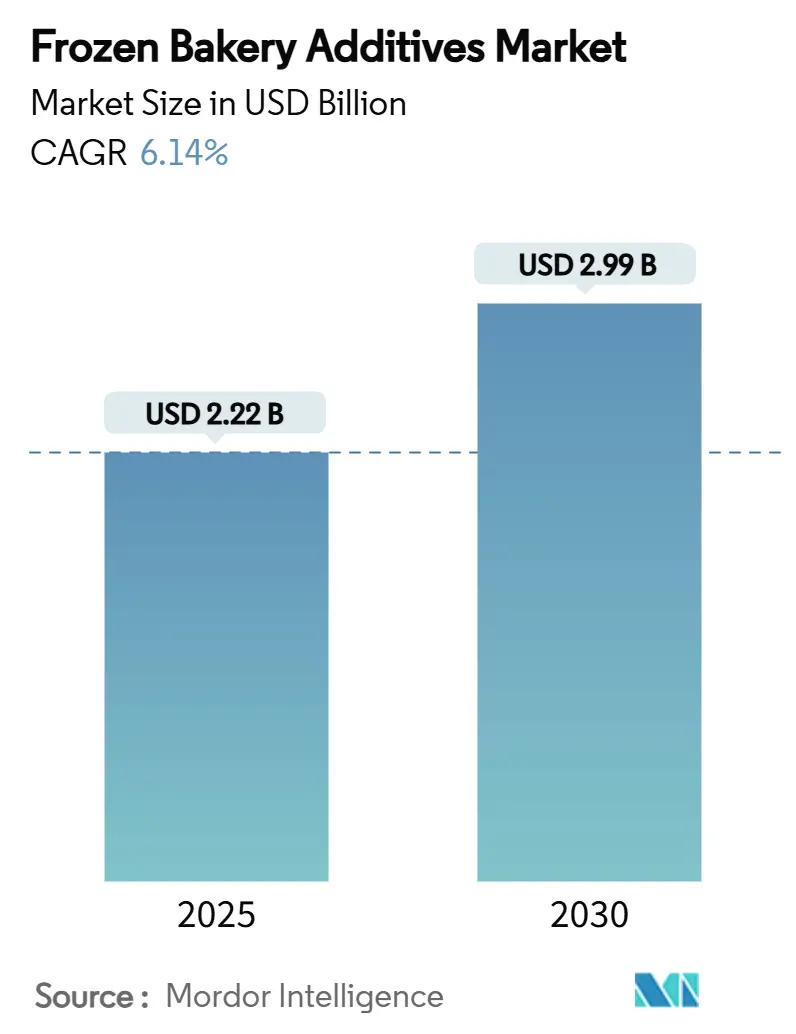

The global frozen bakery additives market size is valued at USD 2.22 billion in 2025 and is expected to reach USD 2.99 billion by 2030, growing at a CAGR of 6.14%. The market expansion is primarily influenced by the increasing consumer preference for ready-to-eat bakery products and significant technological improvements in food preservation methods. The frozen bakery additives industry plays a fundamental role in enhancing product longevity while addressing the growing consumer demand for natural and clean-label ingredients, establishing itself as an indispensable element within the global frozen food industry. This strategic position enables manufacturers to meet both operational efficiency requirements and evolving consumer preferences in the bakery sector.

Key Report Takeaways

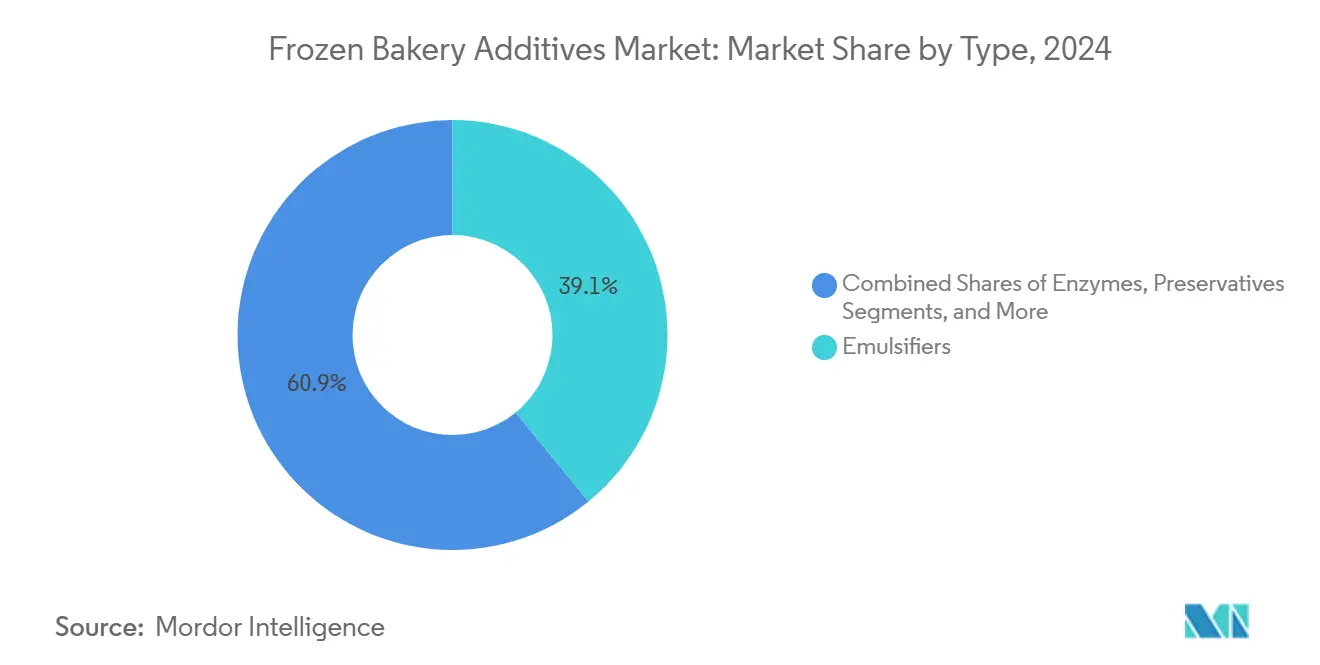

- By type, emulsifiers led with 39.11% of frozen bakery additives market share in 2024, whereas enzymes are forecast to expand at a 7.12% CAGR through 2030.

- By form, powder held 64.11% share of the frozen bakery additives market size in 2024, while liquid additives are set to grow at 6.99% CAGR from 2025 to 2030.

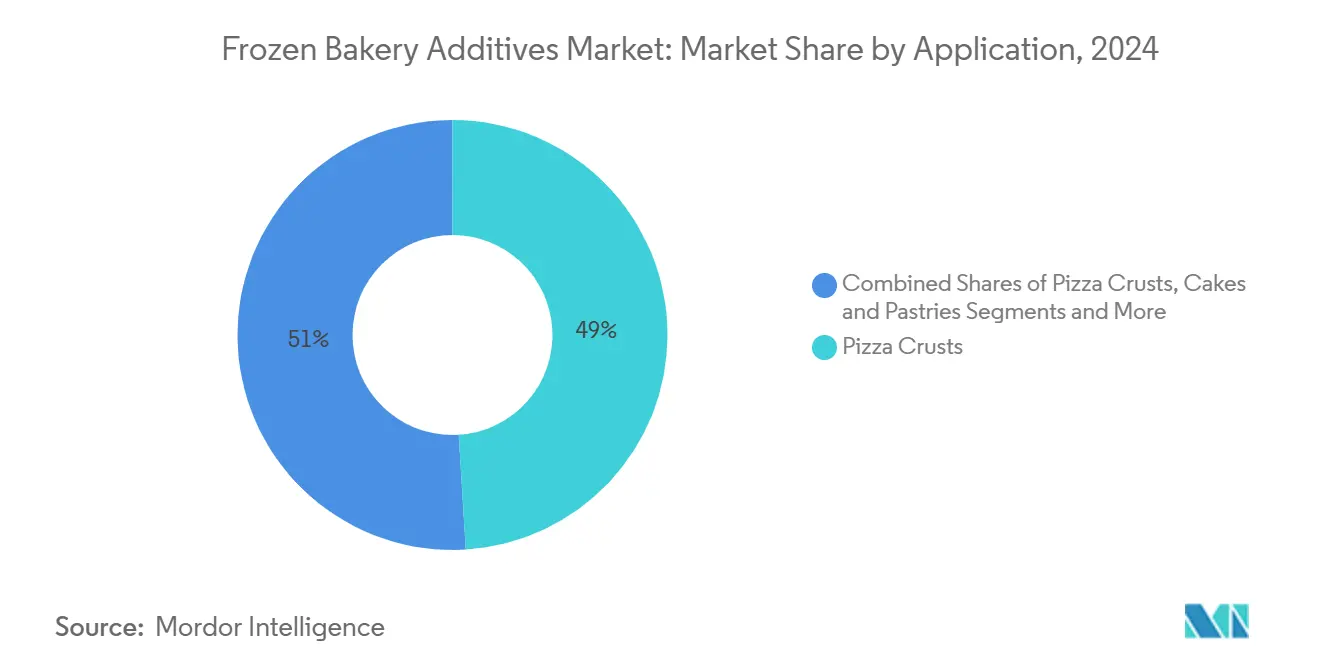

- By application, pizza crusts captured 49.01% of frozen bakery additives market share in 2024; cakes and pastries are projected to rise at 7.32% CAGR over the same period.

- By geography, Europe commanded 32.09% of the frozen bakery additives market in 2024, but Asia-Pacific is on track for a 7.01% CAGR to 2030.

Global Frozen Bakery Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | impact timeline |

|---|---|---|---|

| Rising demand for processed and ready-to-eat frozen bakery products | +1.8% | Global, highest in Asia-Pacific and North America | Medium term (2-4 years) |

| Advancements in food preservation technologies improving shelf life | +1.2% | Europe and North America | Long term (≥ 4 years) |

| Expansion of organized retail network enabling frozen food distribution | +1.0% | Asia-Pacific core, spill-over to Latin America and MEA | Medium term (2-4 years) |

| Increasing use of plant-based and vegan frozen bakery goods additives | +0.8% | North America & EU, expanding to APAC urban centers | Short term (≤ 2 years) |

| Growing consumer interest in clean-label, natural ingredient additives | +0.9% | Global, strongest in developed markets | Medium term (2-4 years) |

| Technological advancements in additive formulation | +0.7% | Innovation hubs in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Processed and Ready-to-Eat Frozen Bakery Products

The rapid pace of urbanization and evolving consumer lifestyles have fundamentally transformed the demand landscape for convenient bakery products. The frozen pizza market continues to demonstrate robust performance, with premium products experiencing stronger momentum compared to traditional offerings. Market expansion has diversified into artisanal bread products, particularly evident in Asian regions where Western-style soft breads are gaining significant traction through specialized techniques like tangzhong. This sustained market growth has intensified pressure on additive suppliers to develop sophisticated formulations that maintain product quality throughout extended freezer storage periods. The increasing consumer preference for single-serve and snack-sized portions has accelerated the adoption of liquid additive systems, ensuring precise dosing capabilities and consistent product attributes. Consumer willingness to pay premium prices for restaurant-quality frozen products has created a strong business case for investments in advanced additive technologies, successfully bridging the gap between convenience and superior product quality.

Advancements in Food Preservation Technologies Improving Shelf Life

Enzyme technology extends product shelf life through starch modification, with maltogenic amylases being the most effective for anti-staling applications due to their heat stability and controlled starch interaction. Novozymes' Novamyl has demonstrated consistent bread quality maintenance over 30 years. Current enzyme formulations combine amylases, xylanases, and lipases to address multiple degradation mechanisms. Natural mold inhibition solutions, such as Corbion's cultured wheat-based systems, replace synthetic preservatives while extending product shelf life in April 2025. Packaging technologies, including nitrogen-filled and vacuum systems, enhance the performance of shelf-life extending additives. These preservation methods allow manufacturers to expand their distribution reach and reduce food waste, offsetting the cost of premium additives.

Expansion of Organized Retail Network Enabling Frozen Food Distribution

The expansion of cold-chain infrastructure continues to drive frozen bakery market growth, particularly in emerging economies. The Indian frozen food sector demonstrates significant growth potential over the next five years. Advanced Transportation Management Systems enhance distribution efficiency between major markets, as evidenced by the Thailand-Japan frozen food corridors achieving substantial cost reductions through route optimization and real-time monitoring. The expansion of organized retail establishes comprehensive quality requirements, leading to increased adoption of advanced additive formulations over traditional preservation methods. The proliferation of modern retail formats across smaller cities and towns generates increased demand for frozen bakery products with enhanced shelf life capabilities. Industry leaders such as McCain Foods are making strategic investments in cold storage facilities to address infrastructure gaps, creating new opportunities for additive suppliers to support diversified product portfolios.

Increasing Use of Plant-Based and Vegan Frozen Bakery Goods Additives

CSM Ingredients has achieved significant fat reduction with its SlimBAKE emulsion technology while preserving sensory qualities across ambient and frozen applications. Lesaffre's innovative yeast-based bitter blockers and flavor enhancers serve as clean-label alternatives to synthetic additives, enabling food manufacturers to advance their plant-forward formulations. The egg replacer market demonstrates substantial growth, although starch-based alternatives continue to face technical challenges in matching the functional characteristics of eggs, particularly in applications requiring specific volume and texture profiles. The strategic partnership between Tate & Lyle and BioHarvest has introduced advanced botanical synthesis technology, creating proprietary plant-derived molecules that deliver sugar-like taste profiles without unwanted aftertaste, with market implementation anticipated by year-end 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited penetration of cold-chain logistics in emerging countries | -0.9% | Asia-Pacific emerging markets, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Challenges meeting stringent regulatory standards for food additives | -0.7% | Global, most severe in EU and California | Short term (≤ 2 years) |

| Potential health concerns linked to synthetic additives and preservatives | -0.5% | North America & EU, spreading to APAC urban centers | Long term (≥ 4 years) |

| Safety concerns tied to chemical additives like MSG reactions | -0.3% | Global, concentrated in health-conscious demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Penetration of Cold-Chain Logistics in Emerging Countries

Cold chain infrastructure limitations continue to create significant barriers for market expansion in developing regions. In India, the insufficient cold storage network results in substantial product wastage and operational inefficiencies, necessitating strategic intervention from both government bodies and private sector investors to develop robust infrastructure. The significant gap between urban and rural cold storage capabilities has created an imbalanced market landscape, where frozen bakery products predominantly reach metropolitan consumers while rural markets remain untapped. The operational costs associated with maintaining frozen distribution networks pose considerable economic challenges for businesses operating in emerging markets. Although renewable energy solutions and government infrastructure development programs present viable pathways forward, the uncertainty surrounding implementation schedules impacts strategic planning for additive suppliers aiming to establish their presence in these regions.

Challenges Meeting Stringent Regulatory Standards for Food Additives

California's Food Safety Act marks a significant shift in food safety regulations by prohibiting the use of potassium bromate and Red Dye No. 3 by 2027. This regulatory change has influenced other states, with New York and Illinois developing similar protective measures [1]Source: CalMatters, “New California law,” calmatters.org. The European Union maintains a more conservative approach through its precautionary principle, implementing stricter approval requirements compared to the U.S. Generally Recognized as Safe (GRAS) system. This difference requires manufacturers to undergo extensive authorization processes when introducing new natural alternatives to the European market. The FDA's expansion of its post-market assessment program has intensified the scrutiny of previously approved additives, creating operational challenges for manufacturers who rely on established formulation processes [2]Source: U.S. Food & Drug Administration, “Post-Market Assessment of Chemicals in Food” fda.gov. Companies now face increased compliance costs as they work to navigate the diverse regulatory requirements across different states while ensuring their products maintain consistency across all markets. These regulatory changes have particularly impacted small manufacturers, who often struggle with limited financial and technical resources needed for comprehensive safety documentation and product reformulation initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Enzymes Drive Clean-Label Innovation

Emulsifiers dominate the market with a substantial 39.11% share in 2024. This significant presence stems from their fundamental role in maintaining stability between water and fat components while extending the shelf life of various bakery products. The widespread adoption of emulsifiers across industrial bakeries and food manufacturing facilities underscores their importance in modern food production processes.

The enzyme segment shows remarkable growth potential, projected to expand at a 7.12% CAGR through 2030. This growth reflects the industry's deliberate movement toward clean-label formulations, where biological alternatives replace traditional chemical additives. Novozymes' comprehensive enzyme portfolio, featuring products like Valena and Optiva, exemplifies this transition by enhancing nutritional value and eliminating emulsifier requirements while improving product quality. The preservatives market maintains steady momentum through innovations in natural alternatives, particularly with products like Corbion's cultured wheat systems. Similarly, the color and flavor additives segment continues to evolve with FDA approval of natural ingredients, including butterfly pea flower extract, meeting consumer demands for natural food solutions.

By Form: Liquid Systems Enable Precision Processing

Powder additives hold a dominant 64.11% market share in 2024, supported by established supply chains, extended shelf stability, and standardized handling procedures in industrial bakery operations. The powder format offers reduced transportation costs, simpler storage requirements, and compatibility with existing mixing equipment, minimizing manufacturers' capital investment needs.

Liquid additives are growing at a 6.99% CAGR due to their processing advantages, including precise dosing, improved dispersion, and enhanced stability in frozen applications. These systems are particularly effective in applications requiring uniform distribution and immediate activation. For example, CSM Ingredients' SlimBAKE emulsion system demonstrates 30% fat reduction while maintaining product sensory properties. The liquid format also enables Pickering emulsion technology to encapsulate sensitive bioactive compounds, creating opportunities for functional bakery products with enhanced nutritional profiles.

By Application: Premium Desserts Outpace Traditional Segments

The bakery additives market demonstrates a significant concentration in pizza crust applications, which currently command a substantial 49.01% market share in 2024. This dominance reflects the evolution of the frozen pizza market, where manufacturers have shifted their focus from volume-based growth to quality enhancement strategies. In the mature pizza segment, additive suppliers are finding new opportunities by developing sophisticated formulations that replicate authentic restaurant-quality characteristics. This strategic shift aligns with changing consumer preferences, as customers increasingly seek products with clean-label ingredients and distinctive flavor profiles. The bread and rolls category continues to serve as the industry's cornerstone, with technological advancements in enzyme development enabling improved freshness retention while accommodating the growing demand for specialized products, including gluten-free alternatives and high-fiber formulations that respond to contemporary dietary requirements.

The cakes and pastries segment has emerged as the market's growth leader, achieving a remarkable 7.32% CAGR. This exceptional performance is attributed to successful premiumization initiatives and innovative seasonal flavor introductions that resonate with consumer preferences. According to Puratos's comprehensive Taste Tomorrow research, several key trends are expected to shape the market through 2025, including the expansion of sourdough applications beyond traditional bread products, the integration of diverse culinary fusion flavors, and the development of nutritionally balanced chocolate products. These trends are driving increased demand for specialized additives. Meanwhile, the cookies and biscuits segment is undergoing significant transformation through the implementation of clean-label reformulation strategies, which focus on maintaining optimal texture characteristics and extended shelf life while meeting consumer demands for more natural ingredients.

Geography Analysis

The European market demonstrates its dominance with a substantial 32.09% market share in 2024, underpinned by its sophisticated cold-chain infrastructure and rigorous quality standards. This infrastructure enables manufacturers to prioritize premium additive formulations over basic preservation methods. The region's progressive regulatory environment for natural ingredient approval creates distinct competitive advantages for companies that successfully navigate the complex authorization procedures. The German market stands out as the primary consumption hub due to its deeply integrated bakery sector, while France's robust jam production industry and the UK's expanding smoothie market contribute to a diverse application landscape [3]Source: Centre for the Promotion of Imports, “European market potential for frozen berries” cbi.eu.

The Asia-Pacific region exhibits remarkable market dynamics with the highest regional growth rate of 7.01% CAGR through 2030. This exceptional growth trajectory is fueled by accelerating urbanization and increasing consumer acceptance of Western bakery products in traditionally rice-consuming nations. The strategic importance of this region is exemplified by Corbion's strategic acquisition of Novotech's bread improver business in India, positioning the company for sustained regional expansion. Additionally, the growing adoption of techniques like tangzhong in commercial baking operations demonstrates the region's evolving approach to achieving optimal bread characteristics.

The North American market exhibits characteristics of maturity, with industry focus primarily directed toward clean-label reformulations and maintaining regulatory compliance. Meanwhile, South America and Middle East & Africa regions present promising growth opportunities, although their potential is currently constrained by infrastructure limitations. The ongoing geographic shift toward Asia-Pacific creates a complex operating environment for additive suppliers, requiring them to adapt their strategies to navigate diverse regulatory frameworks and address varying consumer preferences across different markets.

Competitive Landscape

The frozen bakery additives market exhibits a balanced competitive landscape where both global corporations and specialized ingredient suppliers thrive through their unique strengths. Multinational companies such as International Flavors & Fragrances, Cargill, and Kerry Group harness their extensive international networks and substantial research capabilities to develop wide-ranging additive solutions that address various customer requirements across regions. In this dynamic environment, mid-tier companies including Corbion, Puratos, and Lesaffre have successfully carved out their market positions by focusing on specialized applications and developing clean-label innovations that respond to specific market needs.

Success in this market largely depends on companies' ability to manage complex regulatory frameworks while delivering cost-effective solutions to their customers. A notable example is Tate & Lyle's strategic acquisition of CP Kelco for USD 1.8 billion in June 2024, which significantly enhanced their capabilities in sweetening, mouthfeel, and fortification solutions. The industry has witnessed a growing emphasis on innovation partnerships, as illustrated by Tate & Lyle's strategic collaboration with BioHarvest to develop botanical synthesis technology for plant-derived molecules. Companies are making substantial investments in technological advancements, particularly in enzyme development, natural color alternatives, and digital formulation tools, which have become crucial differentiators in capturing market share.

The market landscape presents significant growth potential across various segments, particularly in plant-based formulations, functional additives, and expansion into emerging markets. While stringent regulatory compliance requirements create substantial barriers to entry, these challenges ultimately benefit established companies with robust compliance frameworks. Smaller companies have found success by adopting focused strategies in niche applications or regional markets, while ingredient startups are actively developing innovative solutions such as guar protein and upcycled ingredients to address growing sustainability requirements and evolving consumer preferences. This diverse range of market approaches enables companies of different sizes to establish and maintain strong competitive positions within their chosen market segments.

Frozen Bakery Additives Industry Leaders

International Flavors & Fragrances Inc.

Cargill, Incorporated

Kerry Group PLC

Corbion N.V.

Puratos Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tate & Lyle and BioHarvest have partnered to develop next-generation botanical-based ingredients under the Botanicalis platform, aiming to enhance natural functionality and sustainability in frozen bakery formulations. This collaboration supports innovation in clean-label, plant-derived ingredients that improve product quality and meet evolving consumer demand.

- August 2024: Corbion’s acquisition of Novotech’s bread improver business strengthens its portfolio of functional bakery ingredients, enhancing local manufacturing and tailored solutions for the Indian frozen bakery sector.

- June 2024: Tate & Lyle has enhanced its proprietary formulation tools, advancing texture and mouthfeel solutions specifically designed to improve moisture retention, freeze-thaw stability, and sensory appeal in frozen bakery products.

Global Frozen Bakery Additives Market Report Scope

| Emulsifiers |

| Enzymes |

| Preservatives |

| Color Additives |

| Flavor Additives |

| Others |

| Powder |

| Liquid |

| Bread and Rolls |

| Pizza Crusts |

| Cakes and Pastries |

| Cookies and Biscuits |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Emulsifiers | |

| Enzymes | ||

| Preservatives | ||

| Color Additives | ||

| Flavor Additives | ||

| Others | ||

| By Form | Powder | |

| Liquid | ||

| By Application | Bread and Rolls | |

| Pizza Crusts | ||

| Cakes and Pastries | ||

| Cookies and Biscuits | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the frozen bakery additives market?

The sector is valued at USD 2.22 billion in 2025 and is forecast to reach USD 2.99 billion by 2030.

Which additive type is growing the fastest?

Enzymes lead with a projected 7.12% CAGR, driven by clean-label reformulation trends.

Why is Asia-Pacific the fastest-growing region?

Rapid urbanization, evolving diets, and expanding cold-chain networks support a 7.01% CAGR to 2030.

How are regulatory shifts influencing product reformulation?

FDA and state-level bans on certain synthetic additives are pushing manufacturers toward natural colors and enzymes.

Which application segment offers the highest growth potential?

Cakes and pastries are set for a 7.32% CAGR as consumers seek premium, indulgent frozen desserts.

Page last updated on: