Baking Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

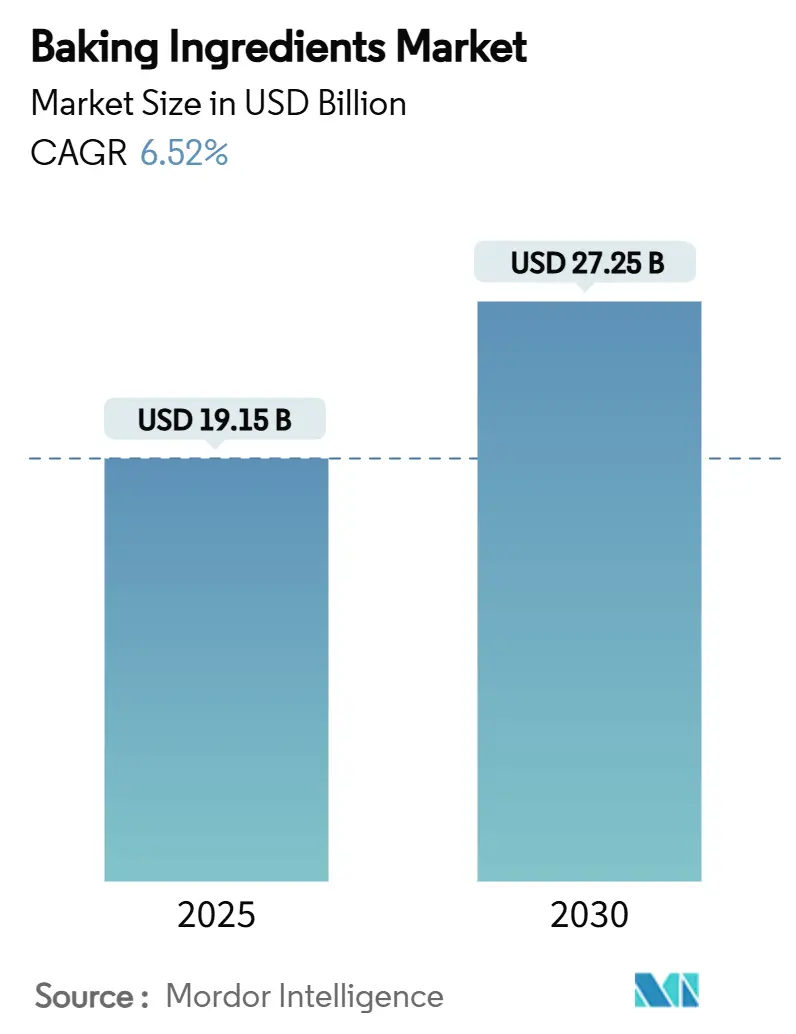

| Market Size (2025) | USD 19.15 Billion |

| Market Size (2030) | USD 27.25 Billion |

| Growth Rate (2025 - 2030) | 6.52% CAGR |

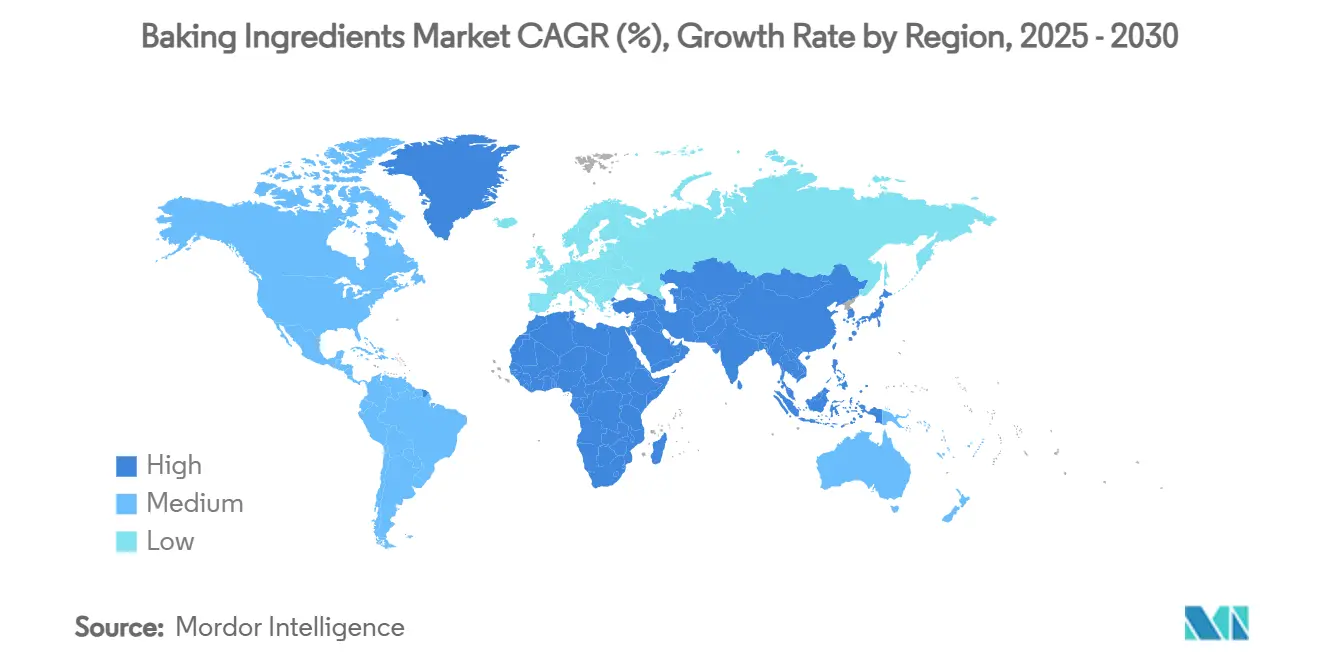

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Baking Ingredients Market Analysis by Mordor Intelligence

The baking ingredients market size is valued at USD 19.15 billion in 2025 and is set to reach USD 27.25 billion by 2030, advancing at a 6.52% CAGR. Sustained growth reflects steady household and commercial demand for clean-label, functional, and sustainably sourced ingredients. Emulsifiers continue to underpin texture and shelf-life performance in industrial baking, while enzymes post the fastest expansion on the back of gluten-free and wheat quality optimization. Manufacturers allocate capital to renewable raw-material sourcing and traceability systems that meet new food-safety rules and consumer transparency expectations. Concurrently, e-commerce has widened the retail reach of premium home-baking kits, broadening channel diversity and buffering suppliers against foodservice volume swings.

Key Report Takeaways

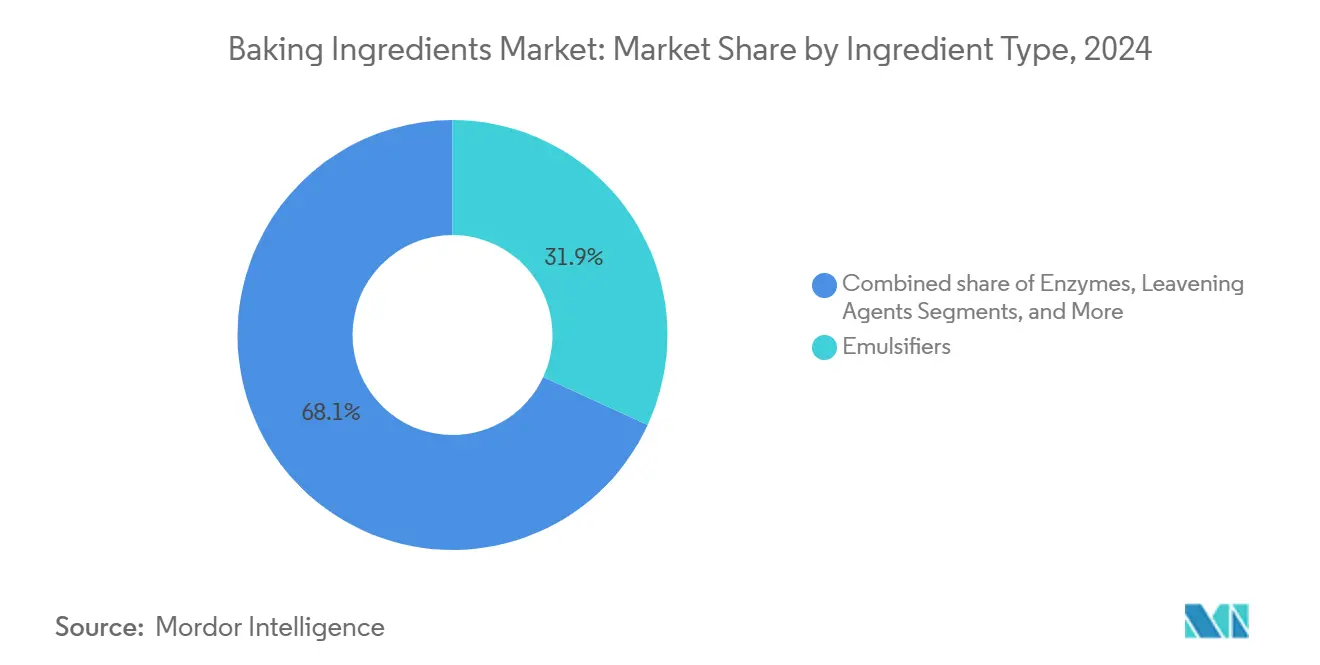

- By ingredient type, emulsifiers led with a 38.26% 2024 revenue share; enzymes are forecast to grow at 7.21% CAGR between 2025 and -2030.

- By form, dry/powder products held 65.10% of the 2024 market; liquid formulations are projected to expand at 6.59% CAGR through 2030.

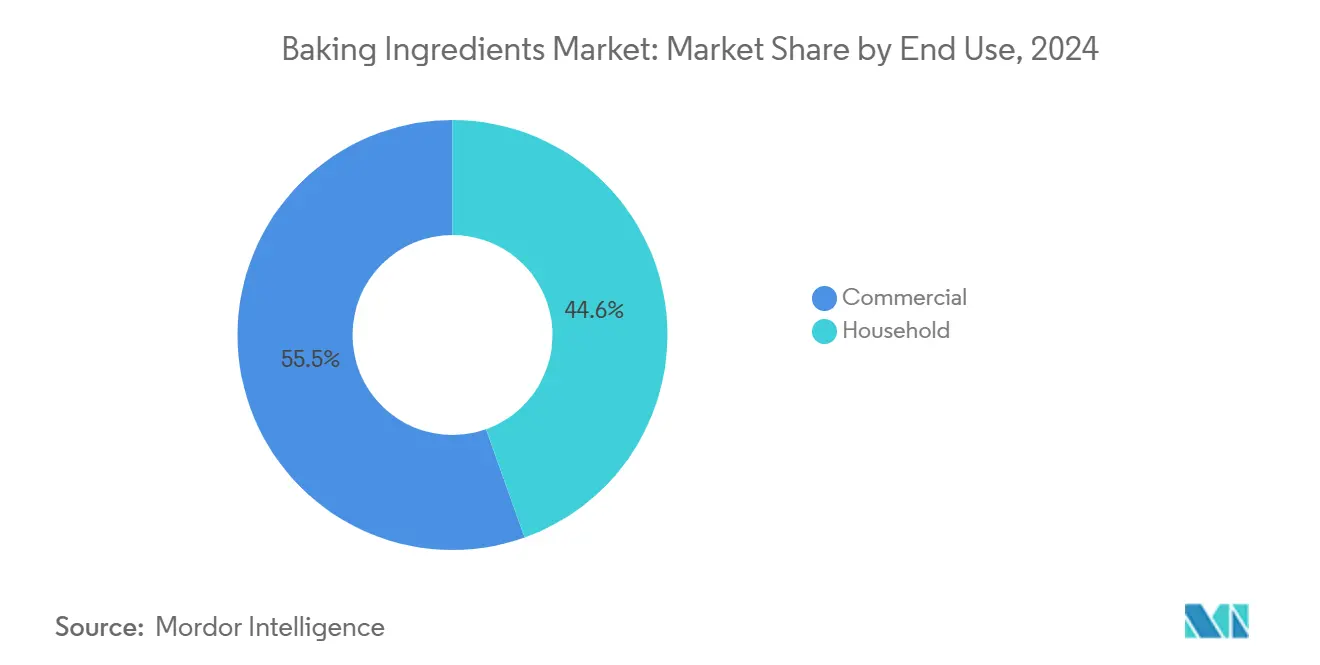

- By end use, commercial bakeries accounted for 55.45% of the 2024 revenue; household demand is projected to track a 6.79% CAGR to 2030.

- By application, bread maintained a 42.33% share in 2024; cakes and pastries are on a 7.66% CAGR over 2025-2030.

- By geography, Europe dominated with a 33.50% share in 2024; Asia-Pacific is advancing at a 7.12% CAGR to 2030.

Global Baking Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for clean-label and natural bakery inputs | +1.2% | Global, with strongest impact in North America andEurope | Medium term (2-4 years) |

| Rising bread and pastry consumption | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Functional ingredients targeting gut-health and high-protein needs | +0.8% | Global, with early gains in North America, Europe, Australia | Medium term (2-4 years) |

| Technological advancements in baking processes | +0.7% | Global, with concentration in developed markets | Long term (≥ 4 years) |

| E-commerce expansion of home-baking ingredient kits | +0.5% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Upcycling food waste into novel fibre-rich flours | +0.3% | Europe and North America, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging demand for clean-label and natural bakery inputs

Ingredient procurement strategies are undergoing a fundamental shift due to rising consumer transparency expectations. Clean-label formulations have transitioned from being a premium offering to a baseline requirement. Reflecting this trend, the European Food Safety Authority (EFSA) issued guidance in 2024 on novel food authorization, emphasizing the demand for recognizable and minimally processed ingredients[1]EFSA Panel on Nutrition, Novel Foods and Food Allergens, “Guidance on Novel Food Applications,” efsa.europa.eu. Suppliers that invest in natural extraction technologies and sustainable sourcing practices stand to gain competitive advantages in this evolving landscape. Puratos, a key player in the industry, has seen 32% of its sales portfolio driven by clean-label positioning, underscoring the commercial viability of transparency-focused product development. This shift in focus isn't limited to ingredient lists; companies are broadening their clean-label commitments to include production methods. Many are now harnessing renewable energy sources and opting for sustainable packaging. Furthermore, market leaders are forging direct ties with agricultural suppliers, ensuring traceability and consistent quality. This strategy not only enhances their product offerings but also erects barriers for competitors who lack such integrated supply chains.

Rising bread and pastry consumption

As emerging markets urbanize, dietary habits are evolving, with bread and pastry consumption reflecting economic growth and modern lifestyles. This reliance on imports not only opens doors for global suppliers but also underscores vulnerabilities in the supply chain, prompting domestic players to pivot towards local sourcing. Ingredient suppliers are spearheading consumer education campaigns, hastening the shift towards functional bread formulations. Today, enhancements like protein fortification and added fiber are becoming the norm, not just niche offerings. Additionally, the growing awareness of health and wellness trends is driving demand for clean-label and organic bread products, further influencing product innovation. Regional tastes are shaping product development, leading suppliers to tailor enzyme profiles and fermentation methods to align with distinct cultural preferences. These localized adaptations are critical for suppliers aiming to establish a competitive edge in diverse markets.

Functional ingredients targeting gut-health and high-protein needs

From basic vitamin supplementation to the integration of sophisticated bioactive compounds, nutritional fortification has come a long way. Today, gut health and protein content are at the forefront of consumer decision-making. The 2025 nutritional trends report highlights a growing demand for protein across diverse food formats. Notably, bakery products are emerging as prime vehicles for delivering high-quality protein. Technological advancements are evident in enzyme applications for gluten-free formulations. Enzymes like transglutaminase, glucose oxidase, and xylanase are enhancing both dough properties and nutritional profiles. Integrating functional ingredients demands a deep understanding of their interaction effects. In response, suppliers are channeling investments into application laboratories, fine-tuning formulations to meet specific nutritional goals. The fusion of taste and nutrition is spurring innovations in natural flavor systems. Companies are pioneering masking technologies, ensuring that additions of protein and fiber don't compromise sensory appeal. Meanwhile, the race for regulatory approvals on novel functional ingredients is creating competitive advantages for early adopters, bolstered by patent protections that extend market exclusivity.

Technological advancements in baking processes

Industry 4.0 technologies are revolutionizing the bakery ingredients value chain, enhancing production efficiency and customer engagement. These technologies facilitate real-time quality monitoring and predictive maintenance. The adoption of robotics, automation, blockchain, and wireless sensor networks not only boosts production efficiency but also enhances product traceability and customer interactions, especially through e-commerce platforms. Enzyme technology is emerging as a pivotal area of advancement. Suppliers are crafting specialized formulations, like optimizing wheat quality, to counter climate-induced variations. Artificial intelligence is streamlining formulation development, hastening the market entry of new products. Machine learning algorithms are playing a crucial role, predicting ingredient interactions and fine-tuning nutritional profiles. Blockchain technology is stepping up to meet traceability demands. Prominent suppliers are forging transparent supply chains, ensuring regulatory compliance and fostering consumer trust. As companies invest in digital infrastructure, it's becoming evident that this investment is a key competitive edge. Those without technological prowess are grappling with shrinking margins and dwindling market shares.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat and edible-oil prices squeezing margins | -0.9% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Stringent regulations and food safety standards | -0.6% | Global, with varying intensity by jurisdiction | Medium term (2-4 years) |

| Supply chain disruptions and ingredient shortages | -0.5% | Global, with concentration in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Competition from homemade and artisanal bakery products | -0.4% | North America and Europe, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile wheat and edible-oil prices squeezing margins

Volatility in commodity prices is posing challenges to profitability throughout the bakery ingredients supply chain. Wheat prices, in particular, have seen significant fluctuations, hitting smaller manufacturers who often lack hedging capabilities especially hard. The outlook for the wheat market in 2025 suggests this volatility will persist. Global wheat stocks are projected to decline, reaching a 32.1% stocks-versus-use ratio for the 2024/25 crop year. Meanwhile, U.S. wheat export sales are holding strong, sitting 32% above levels from the previous year, even when faced with currency challenges. In another instance of commodity volatility, cocoa prices have surged by roughly 300% over the past year. This spike, driven by disruptions in the supply chain and various agricultural challenges, underscores the broader trend affecting specialized ingredient categories. In response to these challenges, industry players are adopting strategic measures. These include initiatives for vertical integration, securing long-term contracts with suppliers, and exploring alternative ingredient sources. Such moves aim to mitigate the risks associated with fluctuations in single-commodity prices.

Stringent regulations and food safety standards

As major markets tighten their grip on food safety standards, smaller suppliers find themselves bearing the brunt of rising compliance costs. The FDA's 2024 updates to the Food Code mandate significant operational shifts across the supply chain, introducing enhanced measures for disinfecting surfaces, bolstering food defense, and refining food safety management systems[2]Food and Drug Administration, “2024 Food Code Updates,” fda.gov. Meanwhile, the European Union's Commission Regulation 2023/915 sets stringent maximum contaminant levels for bakery products, backed by enforcement mechanisms that bar non-compliant items from the market. In the U.S., state-level regulatory differences, such as California's Food Safety Act, which bans specific additives, complicate operations for national suppliers juggling diverse compliance mandates. On a global scale, Canada's alignment of food additive regulations with the Canadian Food Compositional Standards underscores a worldwide pivot towards agile regulatory frameworks. As suppliers invest heavily in testing equipment, documentation, and staff training, regulatory expertise is emerging as a key competitive edge, helping them deftly navigate the intricate approval maze.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Emulsifiers Lead Despite Enzyme Innovation

In 2024, emulsifiers command a dominant 38.26% market share, underscoring their pivotal role in optimizing texture and extending shelf life across a range of bakery applications. While the stability of this segment stands in stark contrast to the rapid 7.21% CAGR projected for enzymes through 2030, the latter's growth is fueled by technological advancements in gluten-free formulations and eco-friendly wheat processing. Flours and starches, the cornerstone of the ingredient category, are witnessing innovations centered on alternative grain sources and enhanced functionalities through processing tweaks. Meanwhile, sugars and sweeteners grapple with pressures from health-driven reformulation trends, leading to a surge in the adoption of natural alternatives and reduction technologies.

Fats and shortenings are evolving in response to trans-fat elimination mandates. Suppliers are now crafting clean-label alternatives that not only uphold functional performance but also align with nutritional standards. A testament to this innovative trajectory is CSM Ingredients' 2024 debut of the SlimBAKE emulsion, which allows a 30% fat reduction without compromising on sensory attributes. Leavening agents, while stable, are reaping benefits from a clean-label approach, with an emphasis on natural sourcing and minimal processing. The "Others" category, which includes colors, flavors, and fibers, is poised for significant growth as the integration of functional ingredients shifts from being a premium offering to a standard practice.

By Form: Liquid Formulations Gain Processing Advantages

In 2024, dry/powder formulations hold a commanding 65.10% market share, thanks to their established supply chains, extended shelf life, and familiar handling procedures in both commercial and household applications. Meanwhile, liquid formulations are on a growth trajectory, expanding at a 6.59% CAGR through 2030. This growth is fueled by improvements in processing efficiency and enhanced ingredient dispersion, leading to reduced mixing times and consistent product quality. The rise of the liquid segment is also attributed to technological advancements in stabilization and packaging innovations, which effectively tackle traditional shelf-life challenges.

Commercial bakeries are increasingly turning to liquid formulations for their automated production lines. Here, the benefits of precise dosing and consistent mixing translate directly to operational efficiency and reduced waste. While household applications predominantly lean towards dry/powder formulations for their convenience and storage benefits, there's a noticeable uptick in premium liquid products within specialty baking. The choice between formats is becoming more application-specific, prompting suppliers to develop dual-format offerings. This strategy not only caters to diverse customer needs but also optimizes production economies of scale.

By End Use: Household Segment Accelerates Growth

In 2024, commercial applications dominate the market with a 55.45% share, underscoring the scale advantages and technical demands of industrial bakery operations. Meanwhile, the household segment, boasting a 6.79% CAGR projected through 2030, signals a significant shift in consumer behavior. This shift, initially spurred by pandemic-induced home baking trends, is now bolstered by the rise of e-commerce platforms and the pervasive influence of social media. Such a growth trajectory suggests these changes are lasting, prompting suppliers to tailor product formulations and packaging to be more consumer-friendly.

The bakery sector's digital evolution is evident in the surge of e-commerce and the rise of personalized offerings. Notably, ingredient kits for home baking have emerged as a lucrative revenue stream for suppliers, traditionally anchored in commercial markets, as highlighted by Melesse, Tsega Y. The household segment's trend towards premiumization opens doors for integrating functional ingredients, as consumers increasingly opt for health-boosted and artisanal-quality products, even at a premium price. While the commercial segment appears stable, there's a fierce competitive undercurrent. Suppliers are vying not just on price, but on technical services, the reliability of their supply chains, and their innovative prowess.

By Application: Cakes and Pastries Drive Premiumization

In 2024, bread applications command a dominant 42.33% market share, underscoring their pivotal role in global diets and the vast scale of commercial bread production. The cakes and pastries segment, projected to grow at a 7.66% CAGR through 2030, highlights consumers' readiness to invest in premium, indulgent products, spurring innovations in texture and flavor. Cookies and biscuits, while stable, present avenues for integrating functional ingredients and promoting clean-label attributes.

Rolls and pies enjoy consistent demand, with room for innovations centered on convenience. Meanwhile, the "Others" category, encompassing croissants, waffles, and doughnuts, reaps benefits from the expansion of foodservice and the growing embrace of international cuisines. In a nod to evolving regulations, the FDA's 2024 decision to revoke standards for frozen cherry pies paves the way for greater manufacturing flexibility, fostering ingredient innovation and product differentiation. Suppliers are honing their craft, developing specialized solutions tailored to distinct baking processes and evolving consumer tastes.

Geography Analysis

In 2024, Europe commands a dominant 33.50% market share, bolstered by its rich bakery traditions, discerning consumer tastes, and regulatory frameworks prioritizing clean-label and sustainable ingredients. The region's mature market landscape not only paves the way for premium product positioning but also encourages the integration of functional ingredients. Suppliers are increasingly investing in application laboratories and technical services, underscoring their commitment to fostering customer innovation. Europe's stringent food safety and environmental standards, often setting the global benchmark, compel suppliers to adapt their formulations. A case in point: the European Food Safety Authority's 2024 re-evaluation of silicon dioxide (E 551) as a food additive, which included updated toxic element limit specifications, underscores the region's vigilance in ingredient safety. Meanwhile, the ramifications of Brexit linger, impacting supply chain logistics and regulatory adherence. In response, suppliers are adopting dual-location strategies, balancing market access with the complexities of heightened administrative demands.

Asia-Pacific is on a rapid ascent, boasting a 7.12% CAGR projected through 2030. This growth is largely attributed to urbanization, increasing disposable incomes, and a westernized diet, all of which are driving up bread and pastry consumption. Efforts to harmonize regulations across ASEAN markets are not only dismantling trade barriers but also aligning food safety standards with global best practices. This alignment presents a golden opportunity for suppliers adept in compliance. Additionally, owing to the rising consumption, the import of baked goods is also increasing in the region. According to the Observatory of Economic Complexity data from 2024, China imported USD 952 million worth of baked goods[3]Observatory of Economic Complexity, "Bakery Imports in China", oec.world. As the region cements its status as a manufacturing hub, it enjoys supply chain advantages for global distribution.

North America is witnessing steady growth, thanks to its well-entrenched commercial bakery infrastructure and a discerning household baking segment that fuels demand for premium ingredients. Navigating the region's regulatory maze, which includes FDA updates and state-specific additive restrictions, is no small feat. Yet, this complexity is driving innovation, particularly in clean-label formulations. Looking at Canada, the bakery and tortilla products market is set for a 3.4% nominal sales dip in 2024, but a rebound with a 4.3% volume growth is on the horizon. This uptick is bolstered by declining flour prices, which enhance profitability even as other ingredient categories exert margin pressures. E-commerce is reshaping the landscape, with a surge in home baking ingredient kit sales. Suppliers are seizing this moment, crafting direct-to-consumer strategies that not only sidestep traditional retail channels but also foster brand loyalty and elevate consumer education.

Competitive Landscape

The bakery ingredients market showcases a competitive tussle between established multinationals and rising regional players. Major players are focusing on vertical integration, tech advancements, and expanding their geographical footprint. They're pouring investments into application labs, championing sustainable sourcing, and fostering direct ties with customers to bolster their competitive edge. Cargill's deepened alliance with ENOUGH to amplify mycoprotein production underscores the industry's pivot towards alternative proteins.

With ambitions to churn out over 1 million tons of ABUNDA by 2033, Cargill is keenly addressing the surging appetite for sustainable protein. Meanwhile, Tate & Lyle's eyeing a USD 1.8 billion takeover of CP Kelco signals a consolidation wave in specialty ingredients. They foresee an annual revenue boost of at least USD 50 million, thanks to bolstered sweetening, mouthfeel, and fortification capabilities. There's a burgeoning potential in weaving functional ingredients, pioneering sustainable sourcing tech, and crafting digital platforms for direct customer engagement, catering to both commercial and household clients. New entrants are championing upcycled ingredients, plant-based solutions, and tailored formulations for dietary needs.

In response, established giants are either acquiring these disruptors or innovating from within. Suppliers are increasingly leaning into automation, data analytics, and ensuring supply chain transparency. This digital shift isn't just a trend; it's pivotal for nurturing customer bonds and streamlining operations. dsm-firmenich's inauguration of a bakery innovation hub in Princeton, New Jersey, backed by a hefty EUR 700 million global R&D investment, underscores the critical role of technical services and customer partnerships in solidifying market stature.

Baking Ingredients Industry Leaders

-

Cargill Inc.

-

Archer Daniels Midland Company

-

Kerry Group

-

Associated British Foods Plc

-

General Mills Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BRAIN Biotech acquired remaining shares of Breatec B.V. With this acquisition the company expanded its baking application center in the Netherlands. The new production site offers enzyme-based baking applications.

- May 2025: Angel Yeast launched its series of Feravor Series. this is an innovative series of flavored yeast products. the yeast is available in fruity and butter flavors. The yeasts are clean label and natural.

- March 2024: Pillsbury brand launched the Creamy Cake Mix line and Stuffed Cookie Kits. The products are available in 2 flavors: Moist Supreme Creamy Almond Cake Mix and Moist Supreme Creamy Vanilla Cake Mix.

- March 2024: Kerry launched Biobake Fresh Rich, an enzyme system designed for sweet baked goods. This system not only enhances the perception of softness, freshness, and moistness throughout the product's shelf life but also plays a role in reducing food waste. Specifically, the starch-acting enzyme ensures that sweet treats with over 20% sugar content maintain their freshness for an extended period.

Global Baking Ingredients Market Report Scope

| Flours and Starches |

| Sugars and Sweeteners |

| Fats and Shortenings |

| Emulsifiers |

| Leavening Agents |

| Enzymes |

| Others (Colors and Flavors, Fibers) |

| Dry/Powder |

| Liquid |

| Commercial |

| Household |

| Bread |

| Cakes and Pastries |

| Cookies and Biscuits |

| Rolls and Pies |

| Others (Croissants, Waffles, Doughnuts) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Ingredient Type | Flours and Starches | |

| Sugars and Sweeteners | ||

| Fats and Shortenings | ||

| Emulsifiers | ||

| Leavening Agents | ||

| Enzymes | ||

| Others (Colors and Flavors, Fibers) | ||

| Form | Dry/Powder | |

| Liquid | ||

| End Use | Commercial | |

| Household | ||

| Applications | Bread | |

| Cakes and Pastries | ||

| Cookies and Biscuits | ||

| Rolls and Pies | ||

| Others (Croissants, Waffles, Doughnuts) | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global bakery ingredients market size and growth outlook?

The bakery ingredients market is valued at USD 19.15 billion in 2025 and is projected to reach USD 27.25 billion by 2030 at a 6.52% CAGR.

Which ingredient segment holds the largest share?

Emulsifiers lead with 38.26% revenue share in 2024 due to their critical role in texture and shelf-life stability.

Which region shows the fastest expansion for bakery ingredients?

Asia-Pacific is the fastest-growing region with a projected 7.12% CAGR through 2030 driven by urbanisation and rising disposable income.

How are clean-label trends influencing product development?

Regulatory and consumer pressure for natural inputs has moved clean-label from niche to baseline, prompting investments in traceable sourcing and natural extraction technologies.

Page last updated on: