Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

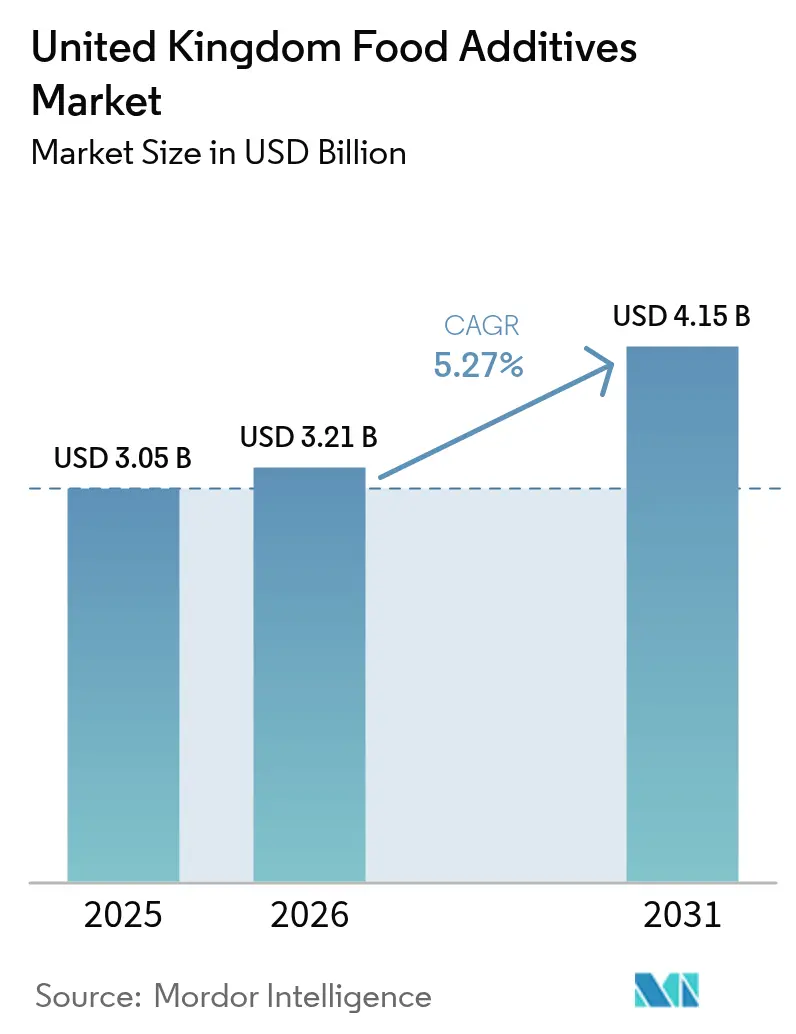

| Base Year Market Size (2025) | USD 3.05 Billion |

| Market Size (2026) | USD 3.21 Billion |

| Market Size (2031) | USD 4.15 Billion |

| Growth Rate (2026 - 2031) | 5.27% CAGR |

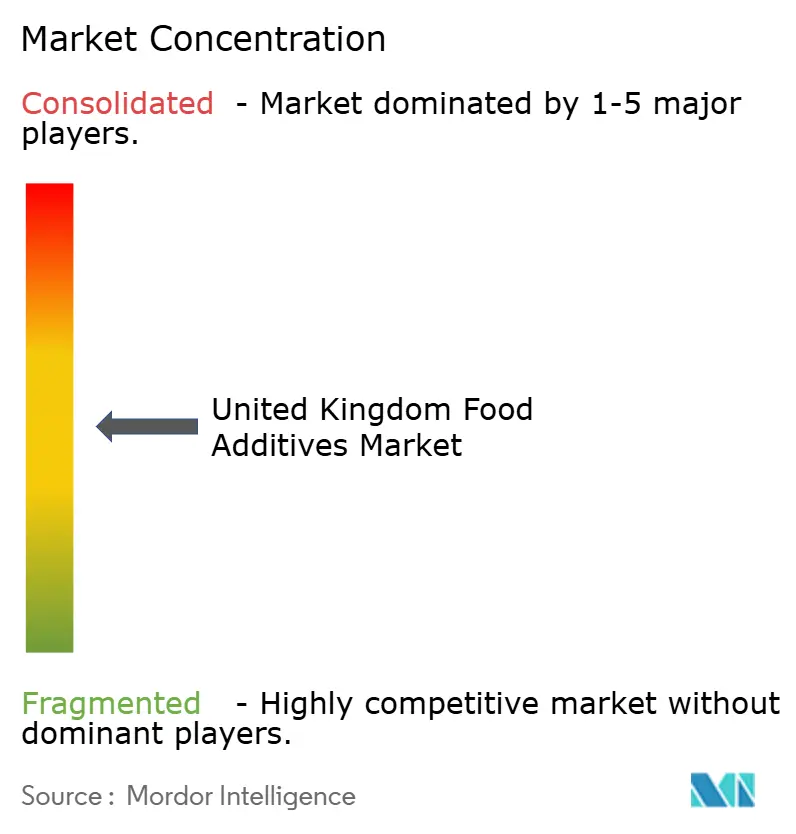

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Food Additives Market Analysis by Mordor Intelligence

The United Kingdom food additives market size in 2026 is estimated at USD 3.21 billion, growing from 2025 value of USD 3.05 billion with 2031 projections showing USD 4.15 billion, growing at 5.27% CAGR over 2026-2031. It is projected to touch USD 3.96 billion by 2030, advancing at a 5.34% CAGR over the forecast period. This expansion mirrors a decisive industry pivot toward natural solutions as the Soft Drinks Industry Levy encourages sugar reduction and consumer trust in E-numbers wanes. Demand also rises as e-commerce grocery penetration stretches supply-chain timelines, elevating the role of preservatives that keep products safe during longer distribution cycles. Suppliers with fermentation capacity or crop contracts cushion input-price fluctuations, whereas mid-tier players absorb steeper costs when stevia or lecithin prices spike. Competitive intensity remains moderate, with global conglomerates contesting share against specialist enzyme and flavor houses that often reach the market first with clean-label innovations.

Key Report Takeaways

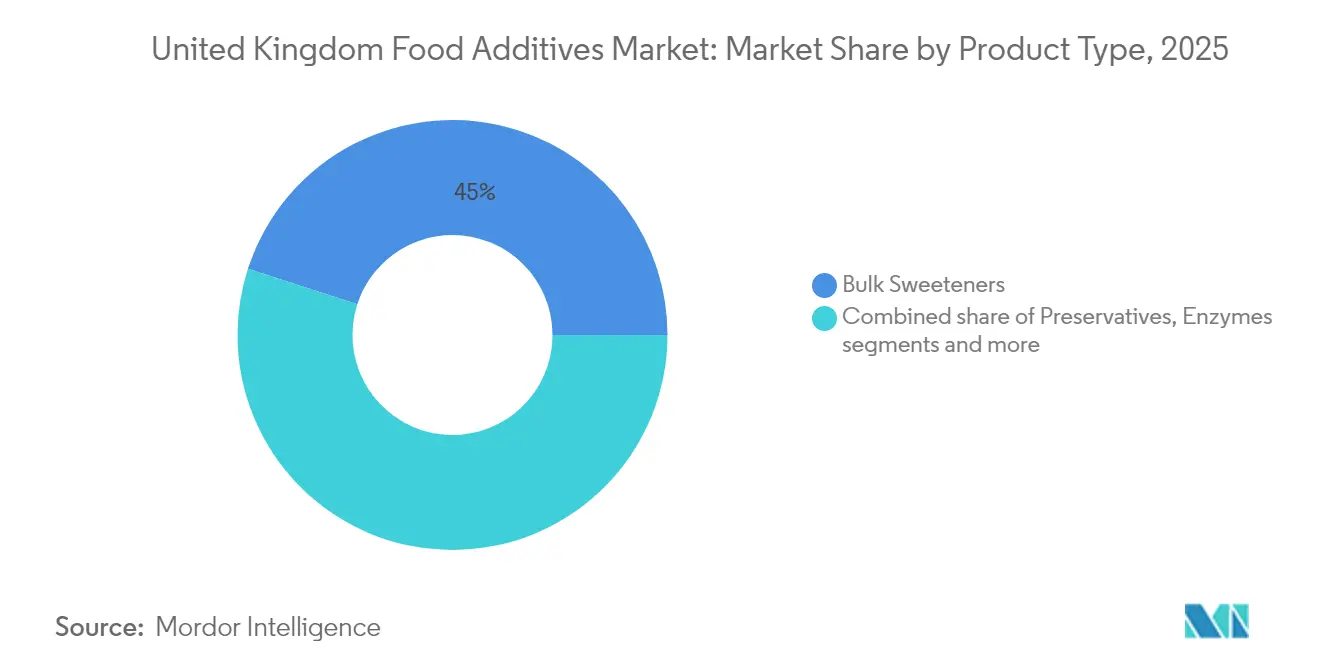

- By product type, bulk sweeteners led with 45.02% of the United Kingdom food additives market share in 2025, while sugar substitutes are forecast to grow at a 6.63% CAGR through 2031.

- By source, synthetic additives accounted for 64.45% of the United Kingdom food additives market size in 2025, whereas natural variants will expand at a 6.89% CAGR to 2031.

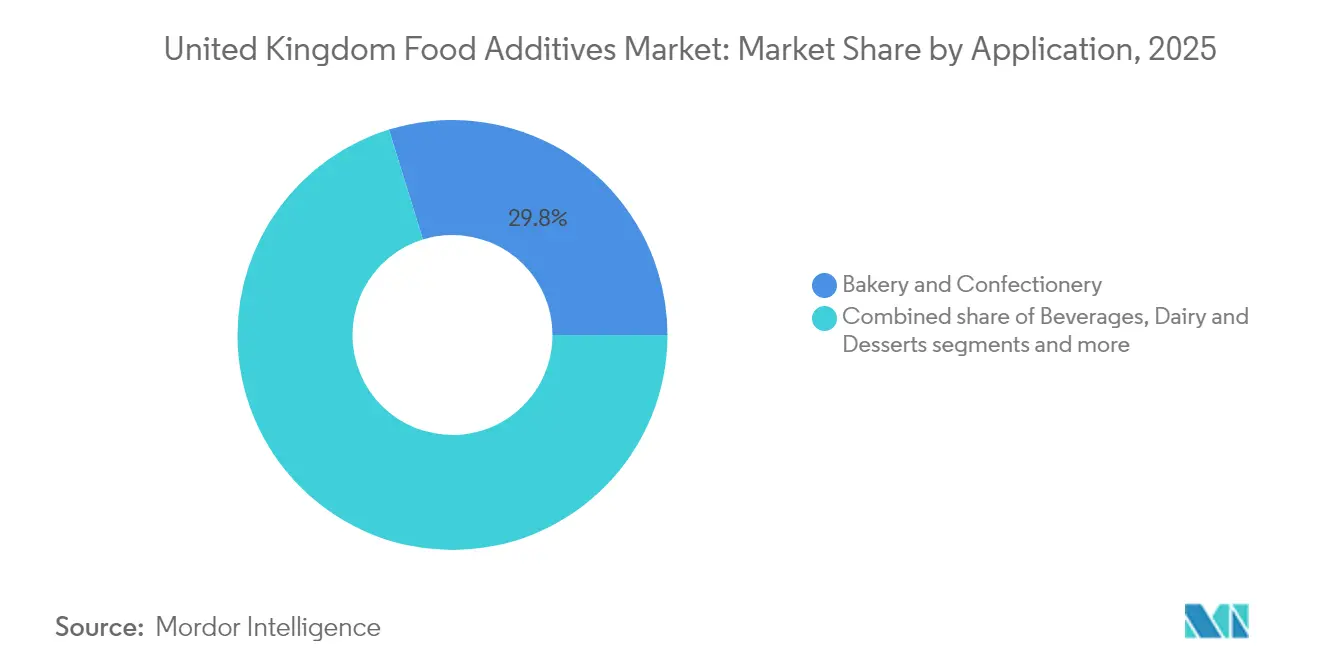

- By application, bakery and confectionery captured 29.78% share of the United Kingdom food additives market size in 2025, but beverages record the highest projected CAGR at 6.27% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Food Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of processed and convenience foods | +0.8% | Nationwide, concentrated in Greater London, Manchester, Birmingham | Medium term (2-4 years) |

| Increasing popularity of reduced-sugar products fuels demand for sugar substitutes | +1.2% | Nationwide, accelerated by Soft Drinks Industry Levy compliance | Short term (≤ 2 years) |

| Rising demand for functional foods and beverages | +0.9% | Nationwide, early adoption in health-conscious urban centers | Medium term (2-4 years) |

| Consumer shift toward clean-label and natural additives amid health awareness | +1.0% | Nationwide, strongest in premium retail channels | Long term (≥ 4 years) |

| Innovation in specialty emulsifiers and texturants for better product texture | +0.6% | Nationwide, focused on bakery and dairy segments | Medium term (2-4 years) |

| Demand for extended shelf-life in ready-to-eat items supports preservatives | +0.7% | Nationwide, driven by e-commerce grocery expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of processed and convenience foods

Rising demand for processed and convenience foods is accelerating the use of blueberry ingredients, including frozen, dried, purees, and powders, across various ready-to-eat products. These ingredients are integrated into items such as yogurt parfaits, energy bars, and smoothie packs, with frozen blueberries offering consistent freshness and nutrient retention, while dried variants cater to shelf-stable snack options. Expanding applications in bakery and confectionery further support this growth, as demonstrated by brands like Chobani, which use blueberry purees in Greek yogurts to deliver creamy textures for busy consumers, and KIND bars, which incorporate dried blueberries for convenient nutrition. The preference for natural and plant-based options is also driving demand, with blueberry juice concentrates enhancing flavor in bottled smoothies from brands like Innocent Drinks, appealing to health-conscious and vegan-friendly consumers. According to the Department for Environment, Food and Rural Affairs, average weekly per-person expenditure on food and drink in the United Kingdom reached GBP 47.19 for the financial year ending 2024, reflecting increased demand for convenient products such as Clif energy gels infused with blueberry extracts for functional benefits [1]Source: Department for Environment, Food and Rural Affairs, "Family Food FYE 2024", gov.uk. Advances in processing techniques are extending shelf life, enabling the use of blueberry extracts and powders in products like Quaker instant oatmeal, while clean-label trends promote the inclusion of organic blueberries in premium ready meals, addressing consumer demand for real-fruit convenience.

Increasing popularity of reduced-sugar products fuels demand for sugar substitutes

The introduction of the Soft Drinks Industry Levy in 2018, reinforced through compliance audits in 2024, has significantly influenced sugar reduction efforts in the United Kingdom. According to HM Revenue and Customs, 46% of soft drink stock-keeping units now contain less than 5 grams of sugar per 100 milliliters, prompting manufacturers to incorporate sugar substitutes that balance sensory appeal with regulatory requirements [2]Source: HM Revenue & Customs, "Soft Drinks Industry Levy uprating", gov.uk. This regulatory impact extends to the confectionery and bakery industries, where companies are reformulating products to avoid potential future taxation. This has driven demand for advanced sweeteners capable of achieving substantial sugar reductions without compromising product integrity. For instance, Tate and Lyle's TASTEVA M stevia sweetener, launched in 2024, offers 30% improved taste masking compared to earlier stevia extracts, enabling chocolate and biscuit producers to reduce sugar content by up to 40% while maintaining flavor profiles. Similarly, Cargill's EverSweet, a fermentation-derived Reb M stevia, has gained traction in yogurt and ice cream applications, closely replicating the mouthfeel of sucrose and facilitating smoother transitions in dairy desserts. High-intensity sweeteners such as sucralose and acesulfame-K are increasingly used in cost-sensitive private-label products, though consumer preferences for clean-label ingredients limit their growth compared to plant-derived alternatives like stevia and monk fruit extracts. These innovations integrate regulatory compliance with formulation flexibility, positioning sugar substitutes as essential for food producers navigating health-driven reformulation across beverages, confectionery, bakery, and dairy categories.

Rising demand for functional foods and beverages

Consumer demand for functional foods and beverages is increasing, driven by a focus on health benefits such as improved gut health, enhanced immunity, and energy management. This has prompted the integration of bioactive additives, including probiotics, prebiotics, and fortification agents, into everyday products. Manufacturers are aligning with clean-label preferences by incorporating functional enzymes and fibers without compromising taste or texture, enabling the launch of products such as gut-friendly yogurts, fortified cereals, and energy-boosting drinks that support wellness claims. For instance, Humiome prebiotic fiber from DSM-Firmenich enhances microbiome support in smoothie and bar formulations, offering clinically validated digestive benefits while maintaining natural ingredient lists. Similarly, the LGG probiotic strain from Novonesis is utilized in fortified dairy drinks to deliver targeted immune support, addressing post-pandemic health concerns and encouraging repeat purchases. Enzymes from Novonesis improve nutrient bioavailability in plant-based milks by breaking down anti-nutrients, making fortified options more effective for vegan consumers seeking improved protein and vitamin absorption. Hydrocolloids such as pectin variants from CP Kelco stabilize beverages by preventing separation in high-fiber energy shots and ensuring shelf stability for functional ready-to-drink formats popular in gyms and convenience stores. These additives drive innovation in product formulations, enabling differentiation and positioning functional foods as key growth drivers across dairy, beverages, bakery, and snacks.

Consumer shift toward clean-label and natural additivies amid health awareness

Consumer demand for clean-label and natural additives, driven by heightened health awareness, is influencing reformulation strategies across the food industry in the United Kingdom. Concerns about ultra-processed foods and additives are significant, with a 2024 survey by the United Kingdom Food Standards Agency indicating that 77% of respondents are highly or somewhat concerned about ultra-processed or over-processed foods, and 73% express similar concerns regarding ingredients and additives [3]Source: Advisory Committee for Social Science (ACSS) and Food Standards Agency, "Consumer Concerns, Beliefs and Behaviours Around Ultra-processed Foods", acss.food.gov.uk . This has prompted companies like Kerry Group to commit to ensuring that 70 percent of their European ingredient portfolio meets clean-label criteria by 2026, driven by the demand for transparent formulations in snacks and ready meals. Natural colors, such as those from GNT Group's EXBERRY line made from fruit and vegetable concentrates, are replacing synthetic azo dyes in confectionery products like fruit gums and jellies, though their lower heat stability requires adjustments in baked goods production. Sunflower lecithin, supplied by companies like IMCOPA, is increasingly used as a substitute for soy lecithin in premium chocolate and spreads, despite a 25 percent cost premium, due to its avoidance of genetically modified organism associations and allergen concerns. In preservatives, fermented cane sugar and cultured dextrose from Corbion are now standard in premium bakery products like artisan sourdoughs, inhibiting mold through organic acids but reducing shelf life by 10 to 15% compared to calcium propionate, necessitating optimized packaging. Sensient's natural flavor enhancers, derived from yeast extracts, amplify umami in low-sodium soups without chemical profiles, supporting transparency and functional reformulations. These shifts underscore the critical role of natural additives in addressing consumer health concerns and regulatory mandates while maintaining product quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent government regulations on approval and usage | -0.6% | Nationwide, FSA jurisdiction post-Brexit | Long term (≥ 4 years) |

| Negative perceptions of food additives fuel demand for additive-free alternatives | -0.5% | Nationwide, strongest in organic and premium segments | Medium term (2-4 years) |

| Supply chain and pricing volatility | -0.4% | Nationwide, import-dependent categories | Short term (≤ 2 years) |

| Significant costs associated with research and development and innovation | -0.3% | Nationwide, disproportionate impact on mid-tier suppliers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent government regulations on approval and usage

Regulatory frameworks in the United Kingdom impose stringent requirements on the approval and usage of food additives, significantly impacting market dynamics. These regulations, enforced by the Food Standards Agency and retained European Union frameworks, mandate rigorous safety evaluations, including comprehensive toxicological dossiers and exposure assessments for novel additives. This process extends timelines for market entry and necessitates formulation adjustments. Innovative preservatives and colors face delays, while established synthetic options, such as certain azo dyes, are subject to phase-outs or reformulation mandates. For instance, manufacturers utilizing Danisco (now part of IFF) cultured dextrose for natural preservation in deli meats must navigate pre-market notification requirements, leading to higher compliance costs that disproportionately affect mid-sized suppliers. Maximum permitted levels for high-intensity sweeteners, such as saccharin in beverages, necessitate cautious blending with approved alternatives like cyclamates to avoid product recalls. Post-Brexit purity specifications for acidulants, such as citric acid, ensure additive integrity but slow import-dependent supply chains for bakery and sauce products. Enzyme blends used in functional cereals require efficacy validations under novel food rules, linking approval processes to research and development investments, which favor established companies with regulatory expertise. These layered restrictions channel innovation toward pre-approved natural profiles, such as vinegar ferments, balancing public health safeguards with constraints on market growth across preservatives, sweeteners, and functional additives.

Negative perceptions of food additives fuel demand for additive-free alternatives

Consumer concerns regarding the safety and naturalness of food additives are influencing purchasing decisions, driving demand for additive-free alternatives. Synthetic preservatives, colors, and flavor enhancers are increasingly perceived as unnatural or potentially harmful, prompting brands to highlight "no additives" labels on products such as snacks, beverages, and ready meals. This trend aligns with the clean-label movement, where skepticism about E-numbers, fueled by media reports on potential health risks, has led major retailers like Tesco and Sainsbury's to prioritize additive-free private-label offerings, reducing the market share of traditional formulations. For instance, brands adopting vinegar-based preservatives, such as those from Kemin's Mantrol, instead of sorbates, must emphasize "natural preservation" to address consumer concerns, necessitating greater marketing investments to enhance transparency. Emulsifier-heavy categories, such as margarine, are also affected, with palm-free sunflower-based options from AAK gaining traction over standard lecithins due to consumer concerns about processing, despite functional equivalence. Similarly, hydrocolloid applications in sauces face challenges, with pectin marketed as "fruit-derived" to avoid additive-related stigma in premium ketchups, though higher costs impact margins for volume producers. Flavor enhancers like yeast extracts are being used to replicate monosodium glutamate profiles without synthetic associations, yet fully additive-free claims dominate premium shelves, pressuring suppliers to innovate clean-label solutions across bakery, dairy, and convenience foods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sugar Substitutes Outpace Bulk Sweeteners Despite Smaller Base

Bulk sweeteners, projected to hold a 45.02% market share in 2025, remain dominant due to their cost-effectiveness and functional versatility in baked goods, providing bulk and mouthfeel that substitutes often lack. However, their growth is slower than the market average as sugar-reduction mandates become stricter, prompting formulators to adopt blends incorporating substitutes to achieve compliance without full reformulation. Ingredion's Vitessence pea fiber serves as a partial bulking agent, enhancing texture in low-sugar cookies while meeting clean-label demands, further reducing reliance on pure bulk sweeteners. Besides, sugar substitutes are witnessing significant growth, surpassing bulk sweeteners despite their smaller market base. This growth is driven by manufacturers addressing regulatory requirements, such as the Soft Drinks Industry Levy, and reformulating products in confectionery and bakery categories. High-intensity and novel sweeteners enable substantial sugar reduction while preserving taste and texture. Novonesis's lactase enzymes further support this trend by facilitating the production of lactose-free dairy products with reduced sugar content, integrating enzymatic solutions into broader sugar substitute strategies.

Sugar substitutes are forecast to grow at a compound annual growth rate of 6.63% from 2026 to 2031, driven by innovations that replicate sensory performance in reformulated confectionery products such as gums and chocolates, with substitutes like allulose offering caramelization without added calories. Hydrocolloids, including xanthan gum and carrageenan, stabilize sauces and dressings in ready meals, ensuring viscosity under heat and shear conditions. Food flavors and enhancers are expanding alongside functional beverages, masking off-notes from probiotics and plant proteins while enhancing natural fruit flavors. Food colorants are shifting toward natural alternatives like GNT Group's EXBERRY concentrates, aligning with clean-label trends. Anti-caking agents remain essential for powdered soups and seasoning blends, ensuring flowability in humid conditions, with Brenntag's silica-based agents exemplifying their utility.

By Source: Natural Additives Gain Share as Clean-Label Mandates Accelerate

Synthetic additives, which accounted for 64.45% of the market share in 2025, continue to dominate due to cost advantages and superior functional performance in high-volume applications such as carbonated soft drinks and ambient bakery products. However, growing retailer pressures and advancements in natural alternatives are gradually narrowing the performance gap, challenging the dominance of synthetic options. Moreover, natural additives are gaining prominence as clean-label mandates drive demand for transparent ingredient portfolios. Retailers are increasingly prioritizing plant-based, microbial, and fermentation-derived options over traditional synthetic additives. This shift aligns with consumer preferences to avoid E-numbers and supports the development of premium product lines in beverages and snacks with health-focused labeling. For example, fermentation-derived vanillin from DSM-Firmenich delivers authentic flavor without synthetic precursors, reinforcing natural claims in bakery fillings and ice creams.

Natural additives are projected to grow at a compound annual growth rate of 6.89% from 2026 to 2031, outpacing synthetic alternatives as regulatory mandates prompt portfolio realignments across categories. Innovations are addressing performance trade-offs associated with natural sources. For instance, Cargill's EverSweet Reb M stevia, produced through precision fermentation, offers the taste profile of sucrose without the agricultural land requirements of leaf-based stevia, making it a scalable solution for low-sugar drinks and confections. Similarly, stabilized anthocyanin extracts from Sensient enhance shelf vibrancy in natural colors, addressing challenges like fading under UV light. Rosemary extract, a popular natural antioxidant, is paired with masking agents to mitigate off-flavors in neutral applications, while sunflower lecithin is replacing soy lecithin in chocolate and spreads to avoid genetically modified organism associations. Despite its higher cost and lower emulsification efficiency, sunflower lecithin is gaining favor in allergen-free premium spreads produced by chocolatiers.

By Application: Beverages Lead Growth as Functional and Low-Sugar Launches Multiply

Bakery and confectionery are anticipated to account for a 29.78% market share in 2025, driven by their reliance on emulsifiers, enzymes, and bulk sweeteners. These additives play a critical role in extending shelf life and enhancing texture in ambient goods. They ensure crumb softness and chewiness in mass-market biscuits, linking their volume dominance to cost-effective functionality amid stable processed food consumption. Beverages are projected to grow at a compound annual growth rate of 6.27% from 2026 to 2031, emerging as the fastest-growing application. This growth is fueled by the increasing use of additives that mask bitterness in stevia-sweetened colas and probiotic-infused teas. The segment benefits from e-commerce-driven demand for low-calorie mixers and aligns with the rising popularity of functional and low-sugar beverages. Reformulation efforts in ready-to-drink formats further support this growth, with brands enhancing gut-health shots and energy waters without compromising refreshment. For instance, emulsifiers from Palsgaard stabilize high-fiber protein shakes, ensuring a creamy mouthfeel and extended shelf life for gym-focused beverages.

Dairy and desserts utilize hydrocolloids and enzymes to meet evolving consumer demands. Lactase preparations from Novonesis enable the production of lactose-free milk without sacrificing sweetness, while probiotic strains from companies such as Symrise and IFF are incorporated into premium yogurts to retain texture and enhance flavor for lactose-intolerant consumers. Meat and meat products rely on preservatives and antioxidants to extend shelf life, with natural extracts from Archer Daniels Midland delaying lipid oxidation and supporting longer distribution cycles. Soups, sauces, and dressings demand emulsifiers and anti-caking agents to maintain stability during extended distribution, while other applications, including pet food, nutraceuticals, and infant formula, maintain steady growth through basic preservation and fortification.

Geography Analysis

The food additives market in the United Kingdom, projected to reach USD 3.21 billion by 2026 and grow at a compound annual growth rate of 5.27% through 2031, reflects a regulatory framework shaped by post-Brexit developments. While the country has diverged from European Union frameworks, it maintains alignment on essential safety standards. The Food Standards Agency's independent approval pathway, introduced in 2024, has resulted in dual-compliance costs for multinational suppliers operating in both markets. However, the system integrates retained European Union safety dossiers to streamline approvals for established additives, such as preservatives and emulsifiers. Companies that secure early authorizations for innovative additives, including fermentation-derived sweeteners, gain a competitive advantage in reformulating low-sugar beverages and snacks, positioning themselves ahead in the market.

Urban centers such as Greater London, Manchester, and Birmingham drive demand due to their dense populations and the prominence of convenience retail and e-commerce grocery channels. These factors necessitate additives that enhance shelf life and maintain product quality across complex distribution networks. Stabilizers like hydrocolloids are widely used in ready meals, while antioxidants are critical for chilled sandwiches. Urban logistics challenges have increased the demand for high-performance preservatives, such as those offered by Kemin, which prevent spoilage during last-mile delivery. Brands in these regions rely on such additives to ensure consistent product availability in high-street stores and online platforms.

In contrast, Scotland and Wales exhibit slower adoption of premium clean-label products, influenced by lower household incomes and a preference for traditional formulations in bakery and confectionery staples. However, urban areas like Edinburgh and Cardiff align with broader trends in functional beverage consumption, where natural flavors are used to mask off-notes in probiotic drinks. Gradual shifts in regional preferences are evident, with preservatives supporting extended shelf life in value-oriented dairy products and premium urban niches driving the adoption of natural colors, such as beetroot extracts, for yogurt toppings. Additionally, Northern Ireland's alignment with European Union regulations under the Windsor Framework enables ingredient suppliers to access both United Kingdom and European Union markets from a single production base. However, this benefit is tempered by the region's smaller market size and limited local manufacturing capacity.

Competitive Landscape

The food additives market in the United Kingdom is characterized by a moderate level of fragmentation, with global conglomerates maintaining a dominant position while leaving space for specialist and emerging players. Major multinational companies, including Tate and Lyle, Cargill, International Flavors & Fragrances, Inc., Kerry Group, and DSM Firmenich, utilize vertically integrated supply chains and in-house fermentation capabilities to manage costs and ensure a stable supply of sweeteners, texturants, and functional systems. This approach allows bakery and beverage manufacturers in the United Kingdom to source complete ingredient systems, such as sweetener-starch blends or taste and nutrition solutions, rather than individual additives. This strategy increases switching costs for customers and strengthens the influence of these companies in formulation decisions.

Specialist players dominate niche technical domains, leveraging their expertise and regulatory portfolios to create high entry barriers. Novonesis leads the enzyme segment, offering tailored bakery and brewing enzyme systems that enhance product softness and optimize dough handling. Similarly, DSM Firmenich and DuPont-heritage product lines are key players in dairy and meat processing enzymes. In the flavors and taste modulation segment, Givaudan and Symrise provide complex flavor systems for snacks, beverages, and plant-based brands, while Corbion’s lactic-acid-based solutions and vinegar blends support natural preservation systems used in chilled meats and ready meals. Mid-tier suppliers, lacking the resources of larger players, are increasingly confined to commodity additives such as bulk sweeteners and basic citric acid, facing intense price competition and limited differentiation.

Growth opportunities are concentrated in clean-label solutions that replicate synthetic performance in demanding applications. Heat-stable natural colors for beverages, fermentation-derived emulsifiers for plant-based products, and innovative preservation systems are gaining traction. Companies like Givaudan, Sensient, and Novonesis are advancing solutions aligned with retailer standards, emphasizing attributes such as non-GMO and allergen-free profiles. Meanwhile, United Kingdom-based disruptors are exploring plant-protein texturizers and algae-derived natural colors, though their limited production scale and regulatory challenges restrict their impact to premium product lines, leaving the volume business to established multinationals.

United Kingdom Food Additives Industry Leaders

-

Tate & Lyle PLC

-

Kerry Group PLC

-

Cargill Incorporated

-

Archer Daniels Midland Company

-

International Flavors & Fragrances, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: JPL Flavours, the only flavourist-owned flavor house in the United Kingdom, inaugurated its new headquarters in Bromborough, Wirral. The GBP 11 million investment underscored JPL's dedication to expanding its operations and strengthening its capabilities in the competitive flavor industry. The 75,000-square-foot facility substantially increased JPL Flavors' production capacity, enabling the company to provide a broader range of flavor solutions to its clients.

- September 2025: PINC, the venture arm of the international food and beverage company Paulig, announced its investment in Scindo, a UK-based biotech startup that specialized in AI-driven enzyme engineering to develop sustainable, bio-based ingredients. This approach provided an environmentally friendly alternative to conventional manufacturing processes that typically depended on petroleum-based inputs. By designing enzymes to execute complex biotransformations more efficiently, Scindo enabled the scalable production of natural flavors and fragrances with a lower environmental footprint.

- October 2024: The Dutch food technology company Revyve partnered with Daymer Ingredients to introduce its natural and sustainable texturizing ingredients to the United Kingdom. This collaboration represented Revyve's first international distribution agreement, enabling British food and beverage manufacturers to access its yeast-based egg replacement ingredients. The partnership aligned with Daymer's commitment to expanding the availability of high-performance, natural, and sustainable ingredients in the United Kingdom market.

United Kingdom Food Additives Market Report Scope

Food additives are substances added to food to maintain or improve its safety, freshness, taste, texture, or appearance. The United Kingdom food additives market is segmented by product type, source, and application. By product type, the market is segmented into preservatives, bulk sweeteners, sugar substitutes, emulsifiers, anti-caking agents, enzymes, hydrocolloids, food flavors and enhancers, food colorants, acidulants), source (natural, synthetic), and application (bakery and confectionery, dairy and desserts, beverages, meat and meat products, soups, sauces, and dressings, other applications). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Preservatives |

| Bulk Sweeteners |

| Sugar Substitutes |

| Emulsifiers |

| Anti-Caking Agents |

| Enzymes |

| Hydrocolloids |

| Food Flavors and Enhancers |

| Food Colorants |

| Acidulants |

By Source

| Natural |

| Synthetic |

By Application

| Bakery and Confectionery |

| Dairy and Desserts |

| Beverages |

| Meat and Meat Products |

| Soups, Sauces, and Dressings |

| Other Applications |

| By Product Type | Preservatives |

| Bulk Sweeteners | |

| Sugar Substitutes | |

| Emulsifiers | |

| Anti-Caking Agents | |

| Enzymes | |

| Hydrocolloids | |

| Food Flavors and Enhancers | |

| Food Colorants | |

| Acidulants | |

| By Source | Natural |

| Synthetic | |

| By Application | Bakery and Confectionery |

| Dairy and Desserts | |

| Beverages | |

| Meat and Meat Products | |

| Soups, Sauces, and Dressings | |

| Other Applications |

Key Questions Answered in the Report

How large is the United Kingdom food additives market in 2026?

The market is valued at USD 3.21 billion in 2026 and is forecast to grow at a 5.27% CAGR through 2031.

Which product type is growing fastest?

Sugar substitutes will post a 6.63% CAGR between 2026 and 2031, outpacing bulk sweeteners.

Why are natural additives gaining share?

Retailers and consumers are pushing clean-label products, and natural variants are expected to grow at a 6.89% CAGR.

Which application segment leads growth?

Beverages are the fastest-growing application at 6.27% CAGR, driven by zero-sugar and functional drink launches.

Page last updated on: