Bakery Enzymes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

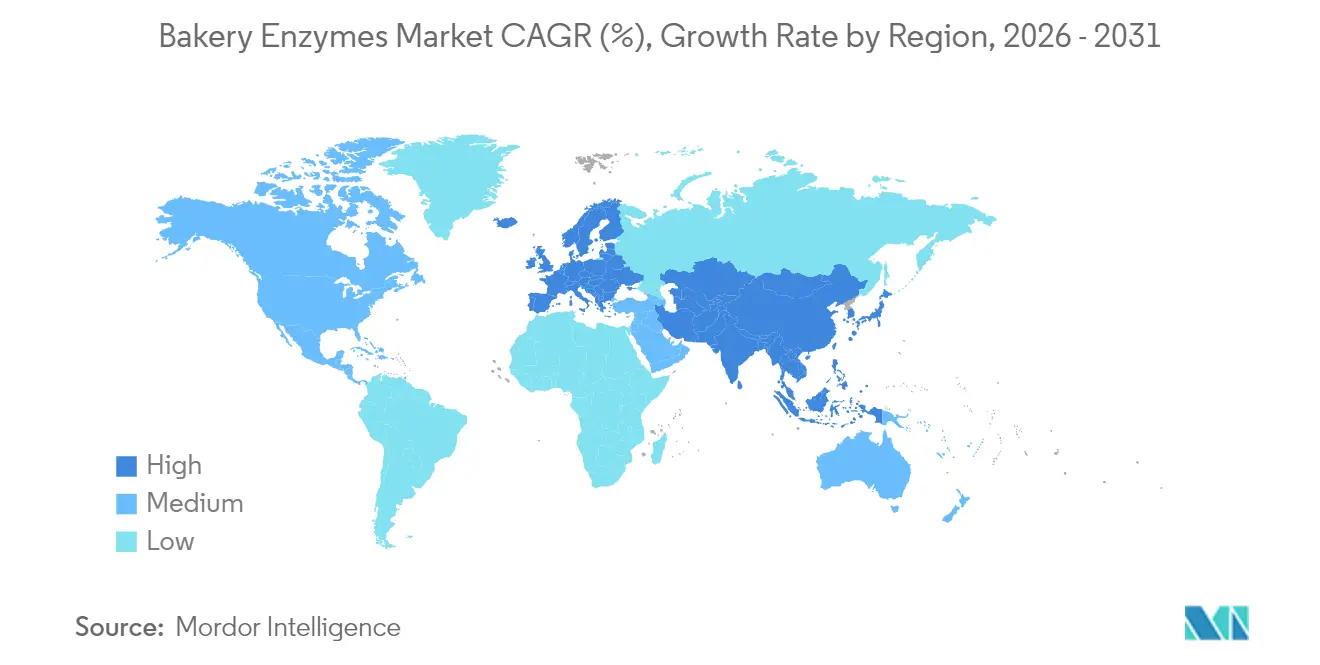

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakery Enzymes Market Analysis by Mordor Intelligence

The bakery enzymes market size is expected to grow from USD 1.58 billion in 2025 to USD 1.68 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at 6.38% CAGR over 2026-2031. This growth is fueled by a rising consumer appetite for clean-label and organic bakery products, coupled with strides in enzyme biotechnology. Clean-label products, which are free from artificial additives and preservatives, are increasingly preferred by health-conscious consumers, while organic bakery products align with the growing demand for natural and sustainably sourced ingredients. Furthermore, as the food industry shifts towards cost-effective and sustainable ingredients, enzymes are emerging as a more functional alternative to traditional chemical additives, driving the market's growth. Enzymes offer multiple benefits, such as improving dough elasticity, enhancing crumb structure, and extending the shelf life of baked goods, which are critical factors for manufacturers aiming to meet consumer expectations. Additionally, the ability of enzymes to reduce production costs by optimizing baking processes and minimizing waste further strengthens their adoption in the bakery sector.

Key Report Takeaways

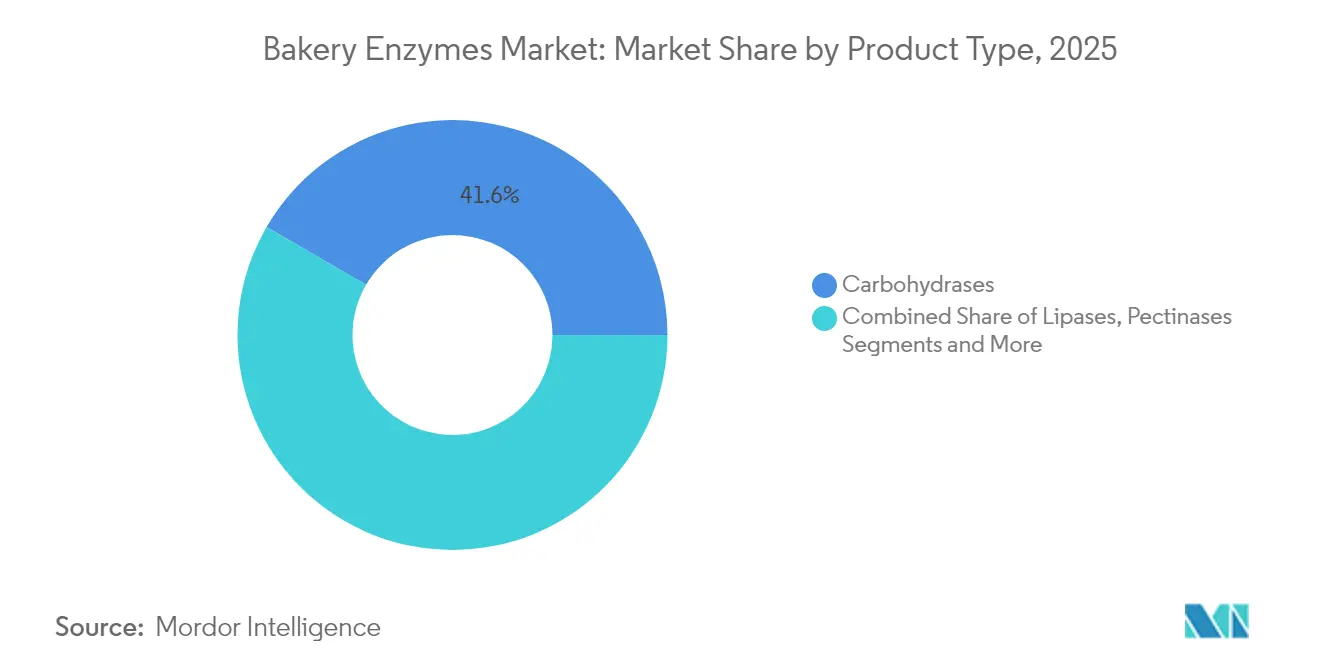

- By product type, carbohydrases led with 41.62% revenue share in 2025; lipases are projected to advance at an 7.95% CAGR to 2031.

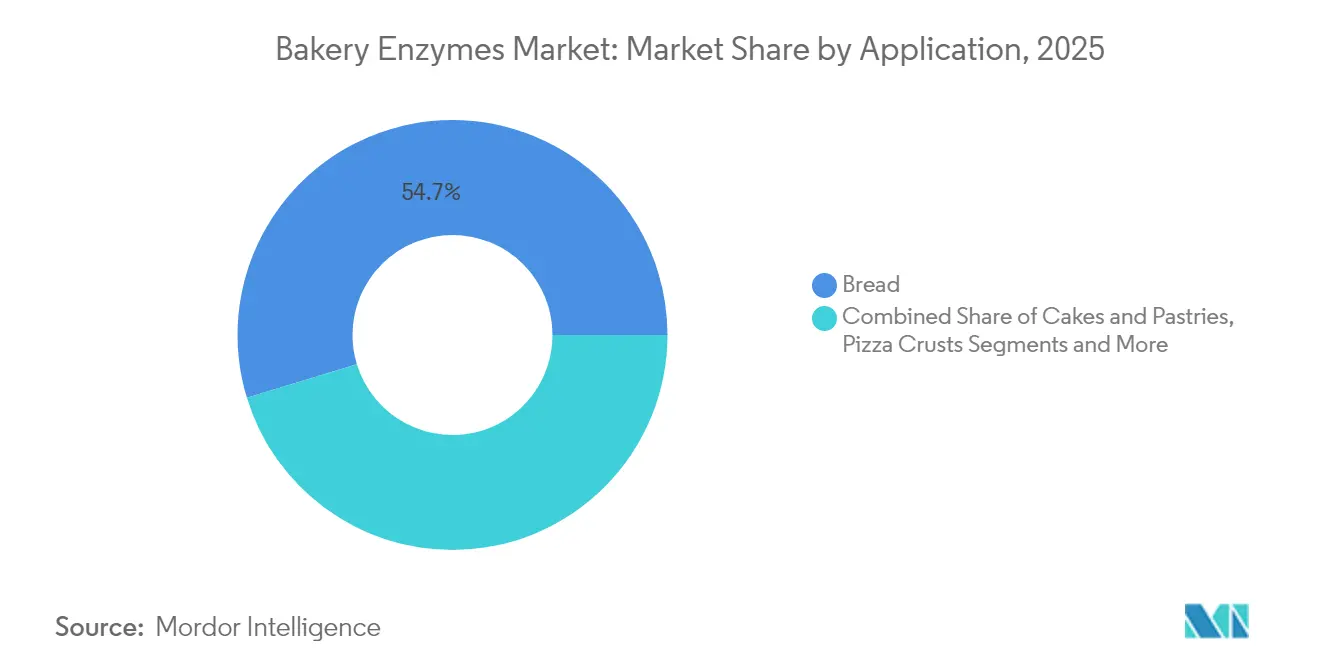

- By application, bread held 54.72% of bakery enzymes market share in 2025, while cakes and pastries are set to grow at a 7.05% CAGR through 2031.

- By source, microbial offerings accounted for 61.35% of the bakery enzymes market size in 2025; plant-sourced counterparts are forecast to expand at an 8.05% CAGR between 2026-2031.

- By form, powder captured 65.62% of the market in 2025, whereas liquid formulations are tracking a 7.55% CAGR.

- By geography, Europe commanded 37.54% of global revenue in 2025; Asia-Pacific is pacing ahead with an 8.62% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bakery Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Clean-Label and Organic Bakery Products | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Growing Demand for Artisanal Bread Extends Enzyme Requirements | +0.8% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Advancements in Enzyme Biotechnology | +1.5% | Global, with Research and Development concentration in North America and Europe | Long term (≥ 4 years) |

| Replacement of Emulsifiers amid Volatile Egg & Lipid Costs | +0.9% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Growing Demand for Gluten-free and High-protein Bakery Products | +1.1% | North America and Europe primary, Asia-Pacific emerging | Medium term (2-4 years) |

| Growing Demand for Cost-effective Dough Improvers | +0.7% | Global, with emphasis on emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Clean-Label and Organic Bakery Products

Driven by a growing consumer preference for transparency in ingredient lists, bakery manufacturers are increasingly turning to enzyme-based solutions as substitutes for synthetic additives. This shift marks a significant change in their product formulation strategies. The increasing demand for clean-label and organic bakery products is a key driver in the bakery enzymes market. Consumers are becoming more health-conscious and are actively seeking products with natural, recognizable ingredients. Enzyme-based solutions align with these preferences by enabling manufacturers to eliminate synthetic additives while maintaining or enhancing product quality. Additionally, enzymes support the production of organic bakery products by meeting regulatory requirements for natural and GMO-free ingredients, further boosting their adoption. The USDA's 2024 Limited Scope Technical Report underscores the importance of using enzymes from edible, non-toxic sources in organic bakery products. Furthermore, it highlights the stringent compliance mandates for GMO-free production processes. Such regulatory stipulations offer a distinct advantage to microbial enzyme producers. Their fermentation-derived products not only resonate with the clean-label trend but also boast enhanced functionality over their plant or animal-derived counterparts.

Growing Demand for Artisanal Bread Extends Enzyme Requirements

Artisanal bread production is moving from traditional craft bakeries to industrial settings. This evolution necessitates enzyme solutions that can mimic the quality of hand-crafted bread while streamlining production. In the United Kingdom, artisan bread sales increased by 9.4% between 2021 and 2024, and sourdough bread sales rose by 4.3% between March 2023 and March 2024, highlighting the growing demand for these products [1]Source: Arta Alba, "Artisanal bread in Europe, a joint venture between tradition and innovation", www.artaalba.ro. Research into sourdough fermentation reveals that specific enzyme combinations not only boost protein functionality but also reduce anti-nutritional factors. This breakthrough facilitates the mass production of artisanal-style products with a longer shelf life. By blending freeze-dried sourdough cultures with targeted enzyme systems, industrial bakers can reliably replicate the flavor profiles and textures previously exclusive to small-batch production. Moreover, enzyme-assisted protein modification is being employed in long-fermentation bread processes, which are gaining popularity in premium markets. This method not only develops intricate flavor compounds but also guarantees dough stability during extended fermentation.

Advancements in Enzyme Biotechnology

The advancements in enzyme biotechnology are driving the growth of the bakery enzymes market. Enzymes play a crucial role in improving the quality, texture, and shelf life of bakery products. Innovations in enzyme technology have enabled manufacturers to develop tailored solutions that cater to specific baking needs, such as enhancing dough stability, improving crumb structure, and increasing production efficiency. Additionally, the growing demand for clean-label and natural ingredients in bakery products has further propelled the adoption of enzyme-based solutions. These advancements not only meet consumer preferences but also help manufacturers optimize processes and reduce costs, making enzyme biotechnology a key driver in the bakery enzymes market. Furthermore, the development of advanced enzyme formulations has allowed manufacturers to address challenges such as gluten-free baking, which requires specific enzyme solutions to mimic the properties of gluten. Enzyme biotechnology has also facilitated the production of low-sugar and low-fat bakery products, aligning with the increasing health-consciousness among consumers.

Replacement of Emulsifiers amid Volatile Egg and Lipid Costs

Commodity price volatility for traditional emulsifying agents creates economic incentives for bakery manufacturers to adopt enzyme-based alternatives that provide consistent functionality at predictable costs. The U.S. Bureau of Labor Statistics documented persistent inflation in bakery input costs despite declining wheat prices, with producer price indices rising 10.5% from May 2022 to December 2023 [2]Source: U.S. Bureau of Labor Statistics, "What is behind the rise in prices for bakery products?", www.bls.gov, highlighting the need for cost-stable ingredient alternatives. Lipase enzymes particularly benefit from this trend, as they modify fat structures to improve dough handling properties while reducing dependence on expensive lecithin and mono-diglyceride emulsifiers. Enzyme-based emulsification systems offer additional advantages including improved freeze-thaw stability in frozen dough applications and enhanced shelf-life characteristics that reduce waste throughout the supply chain. The economic case strengthens in markets experiencing currency volatility, where locally-produced enzymes provide cost stability compared to imported emulsifying agents subject to exchange rate fluctuations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict Regulatory Guidelines and Approval Processes | -0.8% | Global, with varying intensity by region | Long term (≥ 4 years) |

| Safety Concerns Impact Consumer Acceptance of Enzymes | -0.6% | North America and Europe primary, emerging in Asia-Pacific | Medium term (2-4 years) |

| Limited Raw Material Availability Hindering Market Growth | -0.9% | Global, with acute impact in developing regions | Short term (≤ 2 years) |

| Temperature and pH Sensitivity | -0.7% | Global, with higher impact in automated production | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Regulatory Guidelines and Approval Processes

Regulatory complexity across major markets creates significant barriers to enzyme commercialization, with approval timelines extending 2-3 years and requiring substantial investment in safety documentation. The European Food Safety Authority's comprehensive evaluation process for food enzymes demands extensive toxicological studies, genotoxicity assessments, and allergenicity evaluations, as demonstrated by recent approvals for β-glucosidase and α-galactosidase formulations that required months of review. China's implementation of GB 2760-2024 standards introduces additional compliance requirements for enzyme manufacturers seeking market access, with specific documentation standards for production processes and safety assessments. Regulatory divergence between markets compounds compliance costs, as manufacturers must navigate different approval pathways for identical enzyme products across regions. The complexity particularly impacts smaller enzyme developers lacking resources for comprehensive regulatory submissions, creating competitive advantages for established players with dedicated regulatory affairs capabilities.

Limited Raw Material Availability Hindering Market Growth

The challenges in enzyme biotechnology are restraining the growth of the bakery enzymes market. Despite the numerous benefits enzymes offer, several factors hinder their widespread adoption. One major restraint is the high cost associated with the development and production of advanced enzyme formulations. The research and development processes required to create tailored enzyme solutions are resource-intensive, making it difficult for small and medium-sized enterprises (SMEs) to compete in the market. Additionally, the sensitivity of enzymes to environmental factors, such as temperature and pH, poses challenges in maintaining their efficacy during storage and application. Regulatory hurdles also act as a significant barrier, as stringent approval processes and compliance requirements increase the time and cost for manufacturers to bring new enzyme products to market. Furthermore, the lack of awareness and technical expertise among end-users, particularly in emerging markets, limits the adoption of enzyme-based solutions. These restraints collectively impact the growth potential of the bakery enzymes market, despite the advancements in enzyme biotechnology.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Carbohydrases Lead Despite Lipase Innovation

In 2025, carbohydrases dominated the bakery enzymes market, holding a 41.62% share. These enzymes are essential due to their critical role in starch hydrolysis, dough conditioning, and improving crumb softness, which are key factors in producing high-quality baked goods. Carbohydrases enhance the texture, volume, and overall appeal of products such as bread, cakes, and pastries, making them indispensable for manufacturers aiming to meet consumer expectations. Their functional versatility has been well-established over the years, ensuring consistent demand even as specialized alternatives continue to emerge. Additionally, the ability of carbohydrases to optimize production processes and improve product consistency further solidifies their position as a cornerstone in the bakery enzymes market.

Lipases, starting from a smaller market base, are projected to achieve an 7.95% CAGR through 2031. These enzymes are gaining significant traction due to their ability to replace volatile emulsifiers, which not only helps manufacturers extend the shelf life of baked goods but also aligns with the growing demand for clean-label products. Lipases contribute to improving the dough's handling properties and enhancing the overall quality of the final product without altering its label, making them an attractive option for manufacturers targeting health-conscious consumers. Furthermore, their role in reducing dependency on synthetic additives supports sustainability goals, which are becoming increasingly important in the food industry. As consumer preferences shift toward transparency and natural ingredients, lipases are expected to play an increasingly significant role in the bakery enzymes market during the forecast period, driving innovation and growth in the segment.

By Source: Microbial Dominance Accelerates Plant Innovation

In 2025, microbial fermentation dominated the bakery enzymes market, contributing 61.35% of the market share. This dominance is attributed to its unmatched scalability, consistent activity profiles, and widespread regulatory acceptance. Microbial fermentation enables the production of enzymes with high precision and efficiency, making it a preferred choice for industrial applications. The use of advanced genetic modification tools has further enhanced the capabilities of microbes, allowing them to produce designer enzymes with specific pH and temperature optima. These tailored enzymes seamlessly integrate into automated bakery lines, improving production efficiency and ensuring consistent product quality. The reliability and adaptability of microbial fermentation continue to position it as a cornerstone of the bakery enzymes market.

On the other hand, plant-based enzymes are gaining traction and are projected to grow at a CAGR of 8.05% during the forecast period. This growth is driven by increasing consumer demand for natural and sustainable ingredients, as label-conscious consumers perceive botanical sources as more environmentally friendly and health-conscious. Plant-based enzymes are particularly appealing in clean-label formulations, aligning with the growing trend of transparency in food production. Despite their slower adoption compared to microbial enzymes, plant-based alternatives are carving out a niche in the market, supported by advancements in extraction technologies and the rising popularity of plant-derived products in the bakery industry.

By Application: Bread Dominance Faces Dessert Disruption

In 2025, bread accounted for a significant 54.72% share of the bakery enzymes market, highlighting its critical importance in the industry. The demand for bakery enzymes in bread production is primarily driven by their ability to enhance dough volume, improve gas retention, and delay staling. These functionalities are essential for maintaining the quality and shelf life of bread, making enzymes indispensable for both industrial-scale manufacturers and artisanal bakeries. As bread remains a staple food item across various regions, its dominance in the bakery enzymes market is expected to persist, supported by ongoing innovations in enzyme formulations to meet evolving consumer preferences for texture and freshness.

Meanwhile, cakes and pastries are emerging as a high-growth segment within the bakery enzymes market. This category is projected to expand at a CAGR of 7.05% through 2031, driven by increasing consumer demand for indulgent textures and vibrant flavors. The rising popularity of premium and artisanal baked goods, coupled with a growing trend toward personalized and visually appealing desserts, is fueling the adoption of enzymes in this segment. Enzymes play a crucial role in improving the softness, crumb structure, and overall quality of cakes and pastries, making them a key ingredient for manufacturers aiming to cater to the evolving tastes of consumers seeking unique and high-quality bakery products. Furthermore, the growing influence of social media and food photography has amplified the demand for visually appealing and innovative baked goods, further driving the growth of this segment.

By Form: Powder Stability Meets Liquid Convenience

In 2025, powders accounted for a dominant 65.62% share of the bakery enzymes market. Their popularity stems from their stability at ambient temperatures, making them ideal for regions with limited refrigeration infrastructure. Additionally, powders are easy to transport and integrate seamlessly with dry bakery premixes, further driving their adoption. Their long shelf life is particularly advantageous in emerging economies where cold-chain infrastructure remains underdeveloped. These attributes make powder formats a cost-effective and practical choice for manufacturers and bakeries operating in challenging logistical environments.

Liquid enzymes, however, are steadily gaining traction, registering a 7.55% CAGR during the forecast period. Advances in microencapsulation and glycerol-based stabilization techniques have significantly improved their shelf life, eliminating the need for refrigeration. This innovation has expanded their usability across various geographies and operational setups. Large-scale bakeries increasingly prefer liquid enzymes due to their ability to provide precise, dust-free dosing, which enhances operational efficiency and ensures a cleaner work environment. Additionally, liquid enzymes are easier to handle in automated systems, reducing manual intervention and minimizing the risk of contamination. These benefits, combined with their adaptability to modern bakery processes, are driving the growing demand for liquid enzyme formats in the bakery enzymes market.

Geography Analysis

In 2025, Europe commands a dominant 37.54% share in the bakery enzymes market, bolstered by its robust regulatory frameworks, rich bakery traditions, and a rising appetite for clean-label ingredients. According to research by CBI ministry of foreign affairs, clean-label products are projected to constitute over 70% of portfolios in 2025 and 2026, increasing from 52% in 2021. The region's established bakery industry and consumer preference for high-quality, natural products further drive its leadership position. Additionally, the presence of key market players and continuous innovation in enzyme technology contribute to the region's sustained dominance. Europe's leadership is also supported by the increasing demand for healthier bakery options, including gluten-free and low-sugar products. Consumers in the region are becoming more health-conscious, leading to a surge in the adoption of bakery enzymes that enable manufacturers to produce healthier alternatives without compromising on taste or texture.

Asia-Pacific, fueled by swift urbanization, evolving dietary habits, and a growing penchant for Western-style bakery goods in nations like China, India, and across Southeast Asia, stands out as the region with the fastest growth, boasting an 8.62% CAGR projected through 2031. The increasing disposable income and expanding middle-class population in these economies are key factors contributing to the region's rapid growth. Furthermore, the rising influence of international bakery brands and the growing trend of home baking, particularly in urban areas, are creating new opportunities for bakery enzyme manufacturers in the region.

North America holds a significant share in the bakery enzymes market, driven by the strong presence of established bakery chains, high consumer awareness regarding functional ingredients, and the growing demand for gluten-free and organic bakery products. The region benefits from advanced food processing technologies and a well-developed supply chain, which ensures the availability of high-quality bakery enzymes. Additionally, the increasing focus on reducing food waste and enhancing product shelf life has led to greater adoption of bakery enzymes among manufacturers. Meanwhile, South America is witnessing steady growth, supported by the rising popularity of convenience foods and increasing adoption of bakery enzymes to enhance product quality and shelf life in countries like Brazil and Argentina.

Competitive Landscape

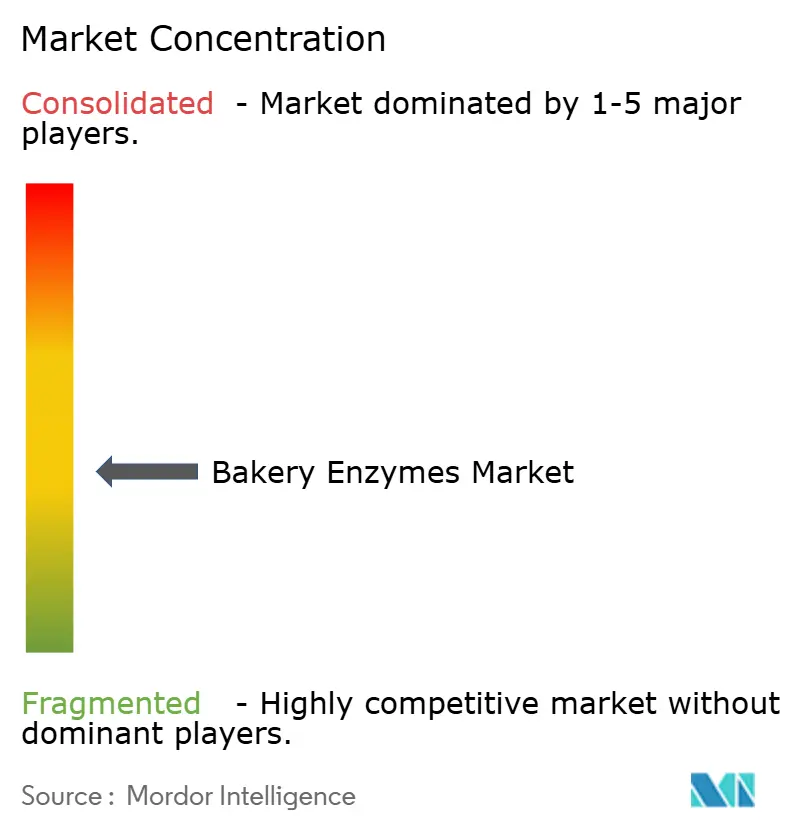

The bakery enzymes market, with a concentration score of 4 out of 10, demonstrates moderate fragmentation. This competitive landscape creates opportunities for specialized players to target niche applications, such as gluten-free and clean-label bakery products, which are gaining traction among health-conscious consumers. For instance, smaller companies are focusing on developing enzymes tailored to specific functionalities like dough conditioning and shelf-life extension, enabling them to carve out a distinct position in the market. Meanwhile, the demand for customized solutions continues to rise, further encouraging innovation among these niche players.

Established leaders in the bakery enzymes market leverage their scale advantages to dominate core segments, such as bread and pastry production. Companies like Novozymes have been investing heavily in research and development to enhance their product portfolios and maintain a competitive edge. These players are also forming strategic partnerships with bakery manufacturers to co-develop enzyme solutions that address specific production challenges, such as improving dough elasticity or reducing sugar content without compromising taste and texture. Such collaborations enable them to strengthen their market presence and cater to evolving consumer preferences.

Vertical integration remains a key strategic focus for major players in the bakery enzymes market. Leading companies are investing in fermentation capacity and biotechnology capabilities to gain greater control over production costs and streamline their supply chains. For example, DSM has been expanding its fermentation facilities to support the production of high-quality enzymes while reducing dependency on external suppliers. This approach not only helps in cost management but also accelerates innovation cycles, allowing these companies to bring advanced enzyme solutions to the market more quickly. As a result, vertical integration is becoming a critical factor in sustaining competitiveness in this dynamic market.

Bakery Enzymes Industry Leaders

-

DSM-Firmenich

-

International Flavors & Fragrances Inc.

-

Kerry Group PLC

-

BASF SE

-

Corbion N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BRAIN Biotech AG announced the complete acquisition of Breatec B.V. and the establishment of a new production facility near Eindhoven, Netherlands, to support its growing bakery enzymes business. The new site will serve as a continental European production hub and include an expanded Baking Application Center, enhancing the company's ability to collaborate with customers on product development. This strategic expansion reflects the increasing demand for specialized enzyme solutions in the European bakery sector .

- April 2025: Corbion has developed a mold inhibition for bakers called Verdad Essence WH100. The ingredient is a cultured wheat solution that is perceived as natural and provides bakers with an alternative to artificial preservatives.

- March 2024: Kerry launched Biobake Fresh Rich, a starch-acting enzyme specifically designed for sweet baked goods with over 20% sugar content. The enzyme enhances softness, freshness, and moistness throughout shelf life while reducing food waste. Available in a dispersible dry format with neutral taste, this innovation addresses the growing demand for extended shelf life in premium bakery products.

- June 2023: Kerry introduced Biobake™ EgR, an enzyme solution that reduces the need for eggs in baking applications by up to 30% without compromising product quality. This innovation addresses the challenges of rising egg prices, which increased by 30% in early 2023, while also supporting sustainability goals by potentially reducing CO2 emissions. The product enables manufacturers to transition from caged to free-range or organic eggs without increased costs.

Global Bakery Enzymes Market Report Scope

Bakery enzymes are usually added to reduce mix times, increase oxidation and improve machinability in baked goods. The bakery enzymes market is segmented into product type, application, source, form and geography. By product type, the market is segmented into carbohydrases, proteases, lipases, oxidoreductases and others. Based on application, the market is segmented into bread, biscuits & cookies, pizza crusts, frozen dough & par-baked items and others. By source, the market is segmented into animal, plant and microbial. By form, the market is segmented into powder and liquid. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, Middle East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Carbohydrases | Amylase |

| Xylanase | |

| Pectinases | |

| Cellulases | |

| Others | |

| Proteases | |

| Lipases | |

| Oxidoreductases | |

| Others |

| Bread |

| Biscuits and Cookies |

| Cakes and Pastries |

| Pizza Crusts |

| Frozen Dough and Par-baked Items |

| Other Bakery |

| Animal |

| Plant |

| Microbial |

| Powder |

| Liquid |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Carbohydrases | Amylase |

| Xylanase | ||

| Pectinases | ||

| Cellulases | ||

| Others | ||

| Proteases | ||

| Lipases | ||

| Oxidoreductases | ||

| Others | ||

| By Application | Bread | |

| Biscuits and Cookies | ||

| Cakes and Pastries | ||

| Pizza Crusts | ||

| Frozen Dough and Par-baked Items | ||

| Other Bakery | ||

| By Source | Animal | |

| Plant | ||

| Microbial | ||

| By Form | Powder | |

| Liquid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the bakery enzymes market?

The bakery enzymes market size is USD 1.68 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at a 6.38% CAGR.

Which product segment dominates sales today?

Carbohydrases lead with 41.62% revenue share, primarily because they improve starch breakdown, dough conditioning, and crumb softness.

Why are lipases growing faster than other enzyme types?

Lipases support the replacement of volatile emulsifiers, extend shelf life, and reduce egg or lecithin costs, driving an 7.95% forecast CAGR.

Which region is expanding fastest?

Asia-Pacific is projected to grow at an 8.62% CAGR, powered by rising urban incomes, Westernized eating habits, and streamlined regulatory paths.

Page last updated on: