Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

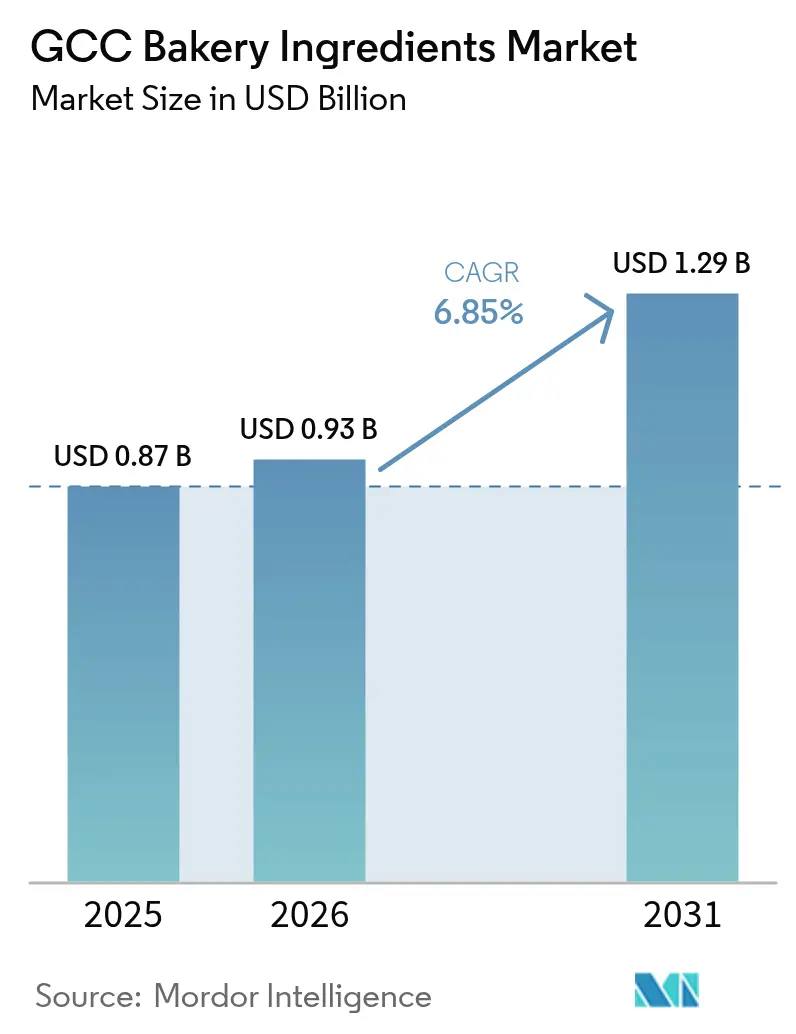

| Base Year Market Size (2025) | USD 0.87 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

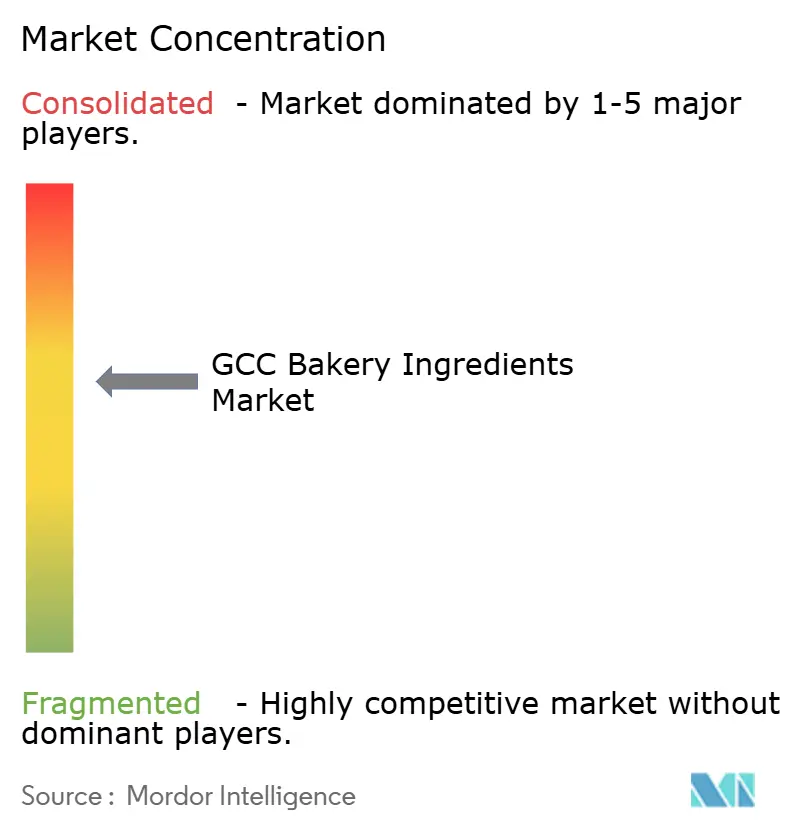

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Bakery Ingredients Market Analysis by Mordor Intelligence

The GCC Bakery Ingredients Market size is expected to grow from USD 0.87 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.29 billion by 2031 at 6.85% CAGR over 2026-2031. This upward trajectory aligns with broader shifts in the region’s food manufacturing sector, which is progressively transitioning from cottage-scale artisanal production toward semi-industrial and fully industrial bakery operations, driven by rising demand for convenience and standardized quality in baked goods. Such industrial modernisation also responds to evolving regulatory environments; for instance, the Saudi Food and Drug Authority (SFDA), in collaboration with the Saudi Halal Center, has reinforced the mandatory requirement for Halal certification for food imports, that contain animal-derived components, including certain oils, fats, dairy, and bakery ingredients, thereby reinforcing quality and compliance standards for regional supply chains. Overall, the GCC bakery ingredients market is positioned for sustained premiumization, deeper halal adherence, and rising investment in localized sourcing.

Key Report Takeaways

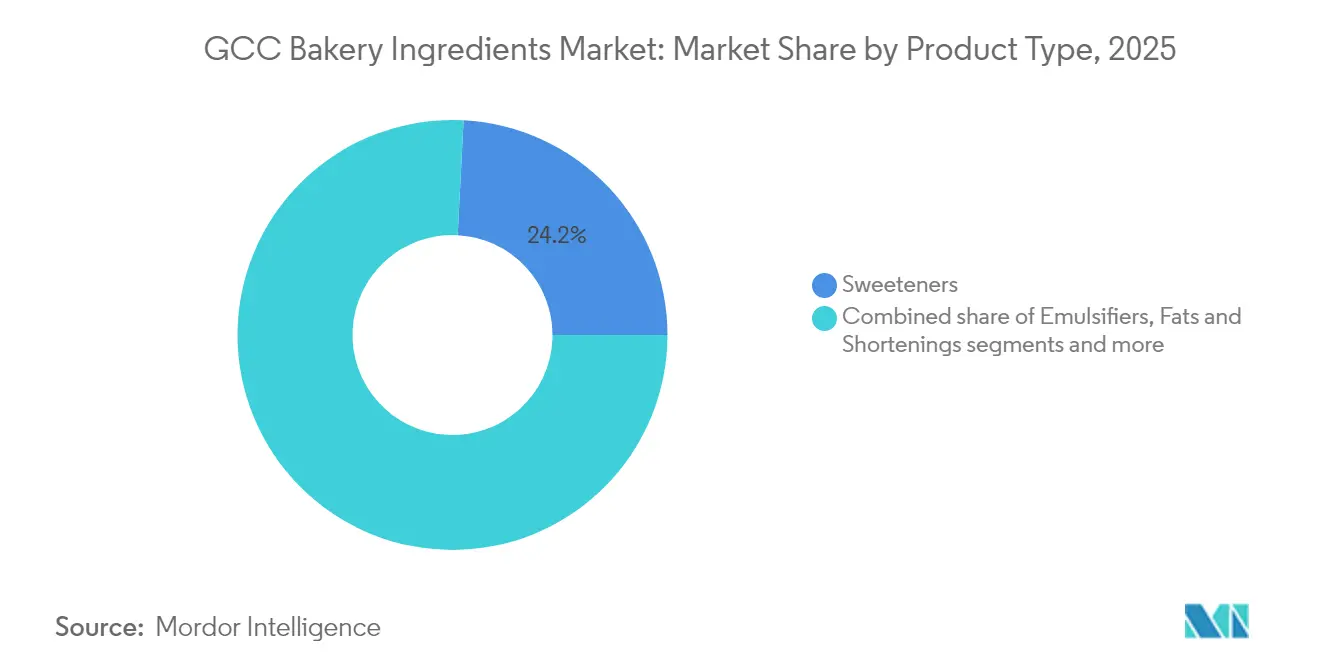

- By ingredient type, sweeteners led with 24.18% revenue share in 2025, while baking enzymes are projected to advance at an 8.25% CAGR through 2031.

- By form, dry ingredients captured 62.90% revenue in 2025; liquid formats are forecast to expand at a 6.35% CAGR to 2031.

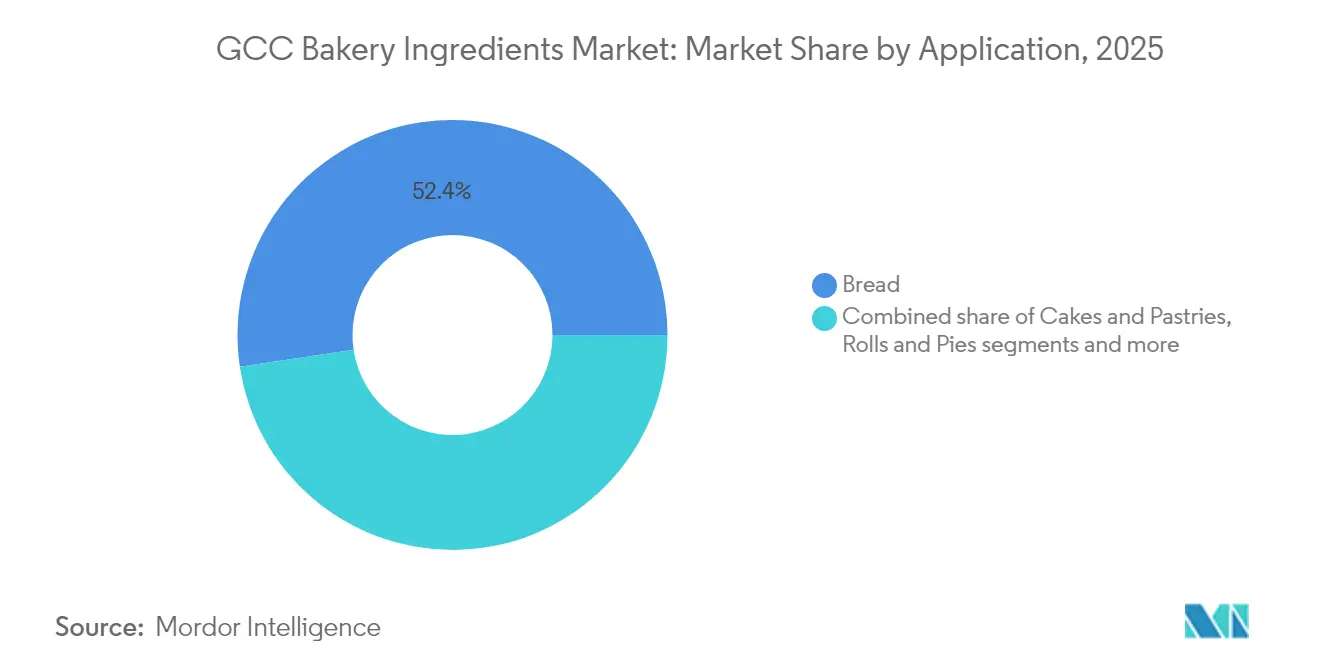

- By application, bread accounted for 52.35% revenue in 2025, and cakes and pastries are set to grow at a 7.38% CAGR through 2031.

- By end use, commercial and industrial bakeries held a 50.85% share in 2025, whereas foodservice and HoReCa channels are projected to rise at a 6.66% CAGR to 2031.

- By geography, Saudi Arabia secured 45.20% in the GCC bakery ingredients market share in 2025; Qatar is expected to log the highest 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Bakery Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of processed and convenience foods | +1.8% | Saudi Arabia, United Arab Emirates, Qatar | Medium term (2-4 years) |

| Growth of regional tourism fuels bakery ingredient demand in GCC | +2.1% | United Arab Emirates, Qatar, Saudi Arabia | Short term (≤ 2 years) |

| Rising popularity of gluten-free bakery products increase the demand for binders and thickeners | +0.6% | United Arab Emirates, Saudi Arabia, Kuwait | Long term (≥ 4 years) |

| Consumer shift toward clean-label and natural additives amid health awareness | +1.4% | Saudi Arabia, United Arab Emirates, Kuwait | Medium term (2-4 years) |

| Expat communities drive demand for specialty baked goods and ingredients | +1.0% | United Arab Emirates, Qatar, Kuwait | Medium term (2-4 years) |

| GCC bakery ingredients market shifts towards industrialization amid rising demand | +1.3% | Saudi Arabia, Oman, Bahrain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid growth of processed and convenience foods

Rising urbanization and the prevalence of dual-income households are significantly reducing meal-preparation time across the GCC, driving the demand for shelf-stable bakery products that combine nutrition and indulgence with convenience. Saudi Arabia, with a current population of 32.5 million, is projected to reach 40 million by 2030, while the influx of millions of foreign workers annually, drawn by large-scale construction projects, is creating substantial opportunities for packaged ethnic foods. The region's young demographic, with 63% of the population under the age of 30, is increasingly prioritizing convenience in food choices [1]Source: United States Department of Agriculture, "Retail Foods Annual - Saudi Arabia (September 2025)", fas.usda.gov. Additionally, in 2024, the United Arab Emirates recorded 568 food processors, many of which are shifting toward convenience-focused offerings such as individually wrapped muffins, pre-sliced sandwich loaves, and frozen dough that can be baked at home in under 15 minutes. Ingredient suppliers are addressing these demands by introducing enzyme blends and emulsifiers that enhance shelf life without refrigeration, a critical feature for products displayed in ambient retail environments or transported in last-mile delivery vans under extreme temperatures exceeding 40°C. For instance, Kerry offers Biobake Fresh Rich enzyme, which extends the shelf life of sweet baked goods by up to 30% without E-number preservatives, aligning with retailer requirements for cleaner labels and reducing waste in high-temperature climates. Additionally, the growing health consciousness among Saudi consumers, who actively seek healthier eating options and are willing to pay a premium for natural products, is creating a dual challenge for ingredient suppliers to deliver both shelf stability and clean-label formulations, further shaping the bakery ingredients market in the region.

Growth of regional tourism fuels bakery ingredient demand in GCC

The post-pandemic recovery in tourism and investments in mega-event infrastructure are driving significant shifts in bakery ingredient demand across the GCC hospitality sector. Hotel occupancy rates in the United Arab Emirates reached 79.3% during the first 10 months of 2025, ranking the country among the top performers globally and regionally, according to the Ministry of Economy and Tourism [2]Source: United Arab Emirates Ministry of Economy and Tourism, "Dubai Tourism Boom: UAE Hotel Occupancy Hits 79.3% in 2025", moet.gov.ae. This growth has sustained demand for liquid emulsifiers, enzyme solutions, and specialty fats, which are essential for hotel bakeries and airline catering. To meet these evolving needs, ingredient suppliers are offering bulk enzyme blends and liquid emulsifiers that enhance central kitchen efficiency while reducing labor costs, a critical factor in markets facing workforce shortages and rising wage inflation. Airline catering is also emerging as a key growth area, with carriers such as Emirates, Etihad, and Qatar Airways collectively serving millions of passengers annually. These airlines require pre-proofed rolls, frozen pastries, and individually portioned desserts that maintain quality through freeze-thaw cycles and cabin reheating, challenges that favor enzyme solutions over traditional improvers. Beyond luxury hotels, the ripple effects of tourism are evident in the expansion of mid-market hospitality and quick-service restaurant (QSR) chains across the GCC. International franchises like Dunkin', Tim Hortons, and Starbucks are increasing their store counts to capture breakfast and snacking occasions, further driving demand for liquid enzyme solutions that extend shelf life and maintain product softness in ambient display conditions. These developments underscore the critical role of innovative bakery ingredients in supporting the region's growing hospitality and foodservice sectors.

Rising popularity of gluten-free bakery products increase the demand for binders and thickeners

Health awareness and dietary diversification are driving the demand for gluten-free bakery products across the GCC, presenting technical challenges that are increasing the need for hydrocolloids and modified starches. A consumer survey in Saudi Arabia highlights that a majority of respondents actively strive to eat healthily, with gluten-free products gaining traction as cleaner and more natural options, even among non-celiac consumers. The removal of gluten, a protein essential for structure, elasticity, and gas retention in wheat-based doughs, compels bakers to utilize binders such as xanthan gum, guar gum, and pectin, along with thickeners like modified starches and psyllium husk, to replicate texture and prevent crumbling. Al Ghurair Foods' corn-starch facility in KEZAD, Abu Dhabi, is producing modified starches specifically designed for gluten-free bread and biscuit formulations, offering superior moisture retention and crumb softness compared to raw starches. Regulatory developments are further supporting this trend, with GSO standards mandating clear gluten-free labeling and threshold limits (typically <20 ppm gluten), creating compliance requirements that benefit ingredient suppliers with robust traceability systems and certified gluten-free production lines. Additionally, Saudi Arabia's mandatory halal certification for imported confectionery, dairy, oils, and fats intersects with the gluten-free market, as many hydrocolloids, including xanthan gum and guar gum, require halal certification to ensure their microbial fermentation sources are not derived from pork. These factors collectively underscore the growing opportunities for ingredient suppliers to cater to the evolving demands of the gluten-free bakery segment in the region.

Consumer shift toward clean-label and natural additivies amid health awareness

Consumer preferences in the GCC region are increasingly shifting toward clean-label and natural additives, driven by heightened health awareness and a focus on lifestyle-related health concerns. This trend has led to greater scrutiny of ingredient labels, with consumers actively avoiding artificial preservatives, synthetic colors, and chemical emulsifiers. Instead, there is a growing demand for bakery products made with minimally processed, naturally sourced, and easily recognizable ingredients. The prevalence of health issues such as obesity, diabetes, digestive disorders, and food sensitivities across GCC countries has further amplified this shift. For instance, data from the General Authority for Statistics revealed that in 2024, 23.1% of adults aged 15 years and above in Saudi Arabia were classified as obese, underscoring the need for healthier and more transparent food options [3]Source: General Authority for Statistics, "Health Determinants Statistics Publication 2024", stats.gov.sa. In response, bakery manufacturers are adapting their formulation strategies to align with these evolving consumer expectations. They are increasingly incorporating clean-label enzymes, natural emulsifiers like lecithin, fermentation-based dough improvers, plant-derived colors, and natural preservation solutions into their products. These adjustments aim to meet consumer demands for healthier options while ensuring that product quality and shelf life remain uncompromised. This shift in consumer behavior and manufacturing practices is fundamentally reshaping the bakery ingredients market in the GCC, presenting both challenges and opportunities for industry stakeholders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price volatility of raw materials | -1.2% | All Gulf Cooperation Council countries | Short term (≤ 2 years) |

| Supply chain dependency on imports for specialty ingredients | -0.9% | Kuwait, Bahrain, Oman | Medium term (2-4 years) |

| Stringent regulatory fragmentation across GCC | -0.5% | All Gulf Cooperation Council countries | Long term (≥ 4 years) |

| Climate-driven shelf-life and storage challenges | -0.4% | Saudi Arabia, United Arab Emirates, Oman | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High price volatility of raw materials

High price volatility of raw materials poses a significant challenge in the bakery ingredients market across the GCC region, creating cost pressures throughout the supply chain and complicating pricing strategies for manufacturers. Essential ingredients such as emulsifiers, enzymes, and specialty natural additives are particularly affected by global commodity price fluctuations, climate-related supply disruptions, geopolitical tensions, and changes in trade policies. With most GCC countries heavily reliant on imports for these raw materials, variations in international prices, freight costs, and currency exchange rates directly influence procurement expenses for bakery ingredient producers and industrial bakeries. This volatility makes it difficult to establish long-term sourcing contracts, often forcing manufacturers to either absorb rising costs, which compresses profit margins, or pass them on to consumers, thereby reducing price competitiveness in the highly price-sensitive mass bakery segment. The situation is further complicated for clean-label and natural ingredients, which are generally more expensive and have less adaptable supply chains compared to synthetic alternatives. As a result, frequent raw material price fluctuations disrupt formulation consistency, hinder production planning, and slow the adoption of premium and innovative bakery ingredients. These factors collectively restrain the overall growth of the bakery ingredients market in the GCC region, as manufacturers face ongoing challenges in maintaining cost efficiency and meeting consumer demand for high-quality, affordable products.

Supply chain dependency on imports for specialty ingredients

Reliance on imports for specialty ingredients poses a significant challenge to the stability of the GCC bakery ingredients market, increasing its exposure to external disruptions. Most GCC countries depend on imported specialty bakery ingredients such as clean-label enzymes, natural emulsifiers, functional fibers, cocoa derivatives, specialty fats, yeast extracts, and plant-based additives due to limited domestic manufacturing capabilities and raw material availability. This dependency heightens the market's vulnerability to risks stemming from global supply chain disruptions, geopolitical tensions, port congestion, regulatory changes, and fluctuations in freight costs and lead times. Delays in shipments or sudden supply shortages can disrupt production schedules for industrial bakeries and ingredient manufacturers, particularly those producing premium, clean-label, or functional bakery products that require precise formulations. Additionally, the reliance on imported specialty ingredients often results in higher landed costs, import duties, and compliance expenses associated with varying food safety and labeling regulations, which can strain profit margins and limit pricing flexibility. These challenges reduce the market's ability to respond effectively to demand fluctuations, increase operational uncertainty, and discourage smaller or mid-sized players from adopting advanced specialty ingredients. As a result, the overall growth of the GCC bakery ingredients market is restrained, with supply chain dependency acting as a critical barrier to the adoption of innovative and functional ingredients in the region.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Enzymes Lead Innovation, Sweeteners Dominate Volume

In 2025, sweeteners commanded a dominant 24.18% share of the GCC bakery ingredients market, primarily fueled by their demand in bread, biscuits, and pastries. This trend underscores the region's deep-rooted affinity for traditional and sweet bakery items. The region's cultural penchant for sugar-rich delicacies, from cakes to sweet breads, has historically shaped ingredient purchasing patterns for both commercial and retail bakers. In response, market players are introducing innovative products to cater to the demand; for instance, Tate & Lyle offers TASTEVA® M. The stevia-based sweetener uses proprietary bioconversion technology to offer a clean, sugar-like taste at an economical cost, ideal for bakery products. Meanwhile, baking enzymes have emerged as the market's fastest-growing segment, boasting an impressive 8.25% CAGR. This surge signals a strategic shift towards clean-label solutions, enhancing shelf-life, texture, and consistency. Other ingredient categories are evolving, addressing supply and functionality challenges. Bakers are increasingly gravitating towards functional solutions, moving away from traditional chemical improvers. These solutions not only cater to nutritional needs, like gluten-free or low-additive breads, but also resonate with consumer demands for freshness and natural processing aids.

The growing adoption of enzymes, including amylases, proteases, and lipases, underscores a technological shift in ingredient usage. These enzymes enhance fermentation control, crumb softness, and overall product consistency, gaining traction in both industrial and artisan baking. The GCC's ingredient landscape is thus characterized by a harmonious blend of traditional sweeteners for flavor and the rapid ascent of enzyme systems for functional quality. As the region responds to health, quality, and clean-label trends, this dual focus is reshaping product portfolios, steering them towards sustainable and health-conscious bakery solutions.

By Form: Liquid Gains on Precision Dosing, Dry Holds Cost Edge

In 2025, dry ingredients dominated the GCC bakery ingredients market, accounting for approximately 62.90% of the total share, primarily due to their advantages of lower freight costs and convenient ambient storage. Nevertheless, liquid systems, including pre-dispersed lecithin and ready-to-dose enzyme blends, are experiencing robust growth at a 6.35% CAGR, reflecting rising investments in automation that demand precise metering and dust-free handling. For example, Cargill’s liquid monoglyceride blends reduce mixing time by up to 20%, a feature particularly attractive to large and mid-sized commercial bakeries seeking to improve production efficiency.

Despite this industrial shift, smaller bakeries continue to favor powders, as these formats provide the flexibility, extended shelf life, and ease of handling essential for retail and small-scale operations. In parallel, Al Ghurair’s starch production aligns with biscuit manufacturers’ preference for dry ingredients while also enhancing moisture retention in finished products, demonstrating the continued relevance of powders in certain applications. Consequently, while industrial and semi-industrial settings increasingly adopt liquid ingredients for efficiency gains, cost-sensitive and smaller operators in the GCC market maintain a reliance on dry powders, resulting in a coexistence of both ingredient formats across the region.

By Application: Bread Anchors Volume, Cakes and Pastries Accelerate

Bread holds a significant 52.35% share of the bakery ingredients market in the GCC in 2025, driven by the region's consistent consumption of flatbreads and sandwich loaves. This demand sustains the need for essential ingredients such as flours, enzymes, and preservatives tailored for staple production. Bread's dominance anchors the ingredient ecosystem, ensuring stable demand for bulk suppliers while enabling formulators to adapt bread-specific improvers for related segments like rolls and pies, which are widely used in airline and hotel catering. Almarai’s L’Usine brand highlights how clean-label sourdough and puff pastries bridge bread's volume leadership with premium aspirations, fostering innovation in natural leavening agents and stable emulsifiers that extend shelf life without synthetic additives, aligning traditional staples with evolving consumer preferences for quality upgrades.

Cookies and biscuits have gained momentum through e-grocery channels post-pandemic, leveraging their shelf stability to drive demand for texturizers and antioxidants that maintain crispness during extended distribution. Cakes and pastries are expanding at a CAGR of 7.38%, supported by rising disposable incomes and expatriate demand for premium patisseries, which intensifies the need for specialized ingredients such as aerators, fruit purees, and chocolate inclusions. Specialty items like gluten-free wraps and plant-based croissants are emerging to address health-conscious consumer trends, driving demand for alternative flours, hydrocolloids, and plant proteins. These developments align with the clean-label stabilizers supporting cookies' e-commerce growth, broadening ingredient portfolios to cater to both premium product advancements and quick-service restaurant innovations, ensuring the market balances traditional staples with diversification to meet shifting consumer demands.

By End Use: Industrial Scale Dominates, Foodservice Channels Surge

Commercial and industrial bakeries are expected to account for 50.85% of bakery ingredients demand in 2025. These bakeries capitalize on economies of scale and high-volume production to secure long-term supermarket contracts, ensuring consistent procurement of key ingredients such as flours, enzymes, and preservatives optimized for mass production of flatbreads and loaves. This industrial dominance establishes a stable volume base, encouraging supplier investments in bulk logistics. These investments directly support the foodservice and HoReCa (Hotels, Restaurants, and Cafés) sectors, which are projected to grow at a CAGR of 6.66%, driven by tourism expansion, new restaurant openings, and advanced hotel catering operations. For example, Dubai Industrial City's leasing of 1.7 million square feet to over 25 food and beverage customers in 2024 demonstrates how industrial infrastructure supports ingredient demand, linking large-scale bakery efficiencies to downstream service requirements.

The rapid growth of foodservice and HoReCa is further supported by e-grocery platforms like Noon and Talabat, which deliver specialty flours, enzyme improvers, and ready-to-bake solutions directly to households, enhancing ingredient versatility across channels. Digital procurement tools, such as The Chefs’ Warehouse’s ordering system and Bidfood’s myBidfood app, streamline supply chains by improving traceability and enabling just-in-time deliveries for large-scale operations. Ingredient providers like Puratos and Lesaffre play a strategic role by offering enzyme blends, dough conditioners, and improver systems tailored for both industrial-scale production and the sophisticated demands of HoReCa. Central kitchens emerge as critical hubs, requiring technical support and customized solutions to meet modernization demands. Simultaneously, e-grocery platforms extend professional-grade ingredients, such as Bunge's specialty wheat flours, into home baking, creating unified demand patterns that reward suppliers with cross-channel expertise and solidify growth in the bakery ingredients market.

Geography Analysis

In 2025, Saudi Arabia commanded a dominant position in the GCC bakery ingredients market, capturing roughly 45.20% of the total revenue. This leadership is bolstered by the kingdom's ambitious target of investing USD 70 billion in food processing by 2030, spurring a robust demand for industrial-scale enzyme blends, specialty fats, and natural sweeteners. Regulatory dynamics have also played a pivotal role: since 2019, the imposition of mandatory halal certification for imported confectionery, fats, and other ingredients has established a compliance barrier. This favors suppliers with local production or established traceability systems, while posing challenges for smaller international players unfamiliar with Saudi FDA mandates.

Qatar is rapidly emerging as the GCC's fastest-growing market, boasting a projected CAGR of 7.88% through 2031. This growth is bolstered by the post-World Cup hospitality infrastructure and the nation's Vision 2030 diversification goals. The Qatar National Tourism Council reports that the country received 4 million visitors in 2023, marking a 60% year-on-year surge. Concurrently, the accommodation and food services sector saw a 13.6% expansion in H1 2025. Coupled with an expatriate population of 3.1 million in Q1 2024, this surge has amplified the demand for specialty bakery ingredients, spanning sweeteners, flavors, fats, shortenings, and more.

The United Arab Emirates (UAE) stands as the second-largest market, propelled by Dubai's prominence as a regional foodservice hub and Abu Dhabi's forward-thinking investments in food security infrastructure. Data from the Ministry of Economy, United Arab Emirates, highlights a 7% uptick in hotel revenues in H1 2024, alongside a 10.5% rise in guest arrivals. This surge pushed occupancy rates to 79.5%, subsequently amplifying the demand for liquid emulsifiers, enzyme solutions, and specialty fats in hotel bakeries and airline catering operations. While Kuwait, Bahrain, and Oman command smaller market shares, they present unique niche opportunities. In Kuwait, a discerning consumer base is gravitating towards premium European-style pastries, spurring a heightened demand for specialty flours, emulsifiers, and sweeteners. Bahrain's limited geography streamlines the swift distribution of fresh bakery products, paving the way for just-in-time ingredient supply chains. On the other hand, Oman's burgeoning tourism, especially in Muscat and Salalah, is catalyzing the growth of hotel and resort bakeries, all of which necessitate a steady supply of high-quality ingredients, from clean-label enzymes to functional fats and natural sweeteners.

Regulatory Landscape

Bakery ingredients placed on the GCC market must meet Gulf Standardization Organization (GSO) technical requirements, with national authorities running registration, labeling, and import-clearance workflows. Key cross-cutting anchors include GSO 9:2022 on labeling of prepackaged foods and the updated permitted additives framework, and GSO 2500:2025 (which replaced GSO 2500:2022 as of October 2025), affecting emulsifiers, colors, sweeteners, and enzyme-containing improver systems used across bread, cakes, and biscuits.

Country-level compliance processes go beyond harmonized standards. In Saudi Arabia, SFDA oversight and the reinforced halal certification requirement for imported foods containing animal-derived components affect ingredient categories such as fats, oils, dairy-derived inputs, and select processing aids. In the UAE, product registration is routed through the mandatory ZAD platform under the Ministry of Industry and Advanced Technology (MoIAT), with UAE.S requirements often aligned to GSO and Codex/ISO benchmarks, which puts greater emphasis on dossier readiness (specifications, labeling, and traceability) for suppliers serving multi-country GCC accounts.

Value Chain Analysis

The GCC bakery ingredients value chain relies on global sourcing of specialty inputs and local value-add through blending and application support. Upstream inputs such as specialty fats, enzymes, hydrocolloids, flavors, and functional sweeteners are commonly imported, while domestic activity focuses on secondary processing, including dry blending, liquid mixing, and systems formulation tailored to industrial bakeries and foodservice central kitchens. The UAE and Saudi Arabia operate as key hubs for formulation, distribution, and technical service, supported by national food-industry clusters and cross-border trade within the GCC framework.

Downstream, ingredients move through direct supply to large commercial and industrial bakeries, as well as distribution partners serving mid-sized bakeries, HoReCa, and retail/household channels. Value-chain frictions center on documentation-heavy compliance for additives and labeling under GSO requirements, alongside halal assurance for formulations that use animal-derived components or fermentation-based inputs. Climate and storage constraints in the Gulf also shape logistics decisions, favoring suppliers that can provide stable packaging formats, controlled storage, and consistent quality during high-temperature transport.

Competitive Landscape

The GCC bakery ingredients market is characterized by intense competition between global leaders such as Cargill Incorporated, Archer Daniels Midland (ADM), Kerry Group, Puratos Group, and Lesaffre, alongside regional powerhouses including IFFCO Group, Almarai, and Agthia. These companies strategically focus on enzyme blends, specialty fats, and natural colors to capture market share, reflecting a moderately consolidated market. While international players emphasize technical services, clean-label innovations, and enzyme solutions to address shelf-life extension, dough machinability, and product consistency, regional firms leverage local manufacturing, halal-certified supply chains, and established distribution networks, particularly in high-volume bread and biscuit segments.

The market is also witnessing emerging opportunities driven by evolving consumer demands and functional innovations. Enzyme-based emulsifier substitutes, plant-derived proteins for vegan bakeries, and heat-stable formulations designed for high-temperature GCC climates are gaining prominence as manufacturers seek clean-label, shelf-life-enhancing solutions without synthetic preservatives. In May 2025, Novonesis launched emulsifier-elimination enzyme solutions, allowing bakers to replace DATEM and SSL with amylase blends that enhance dough machinability while complying with clean-label requirements, a solution particularly relevant amid rising ingredient costs and stricter Gulf Standardization Organization (GSO) labeling standards. Smaller players, such as Gulf Flavours & Fragrances FZCO and Bakels Group, are carving out niches by providing customized flavor systems and pre-mixed ingredient solutions tailored to regional tastes, including date, cardamom, and saffron, simplifying formulation for mid-sized bakeries lacking in-house research and development capabilities.

Technological advancements are accelerating the industry’s evolution. At Gulfood Manufacturing 2025, exhibitors showcased tunnel ovens with 480 m² of baking surface, wafer lines producing 200–250 pieces per minute, and automated flour and sugar handling systems, highlighting the trend toward high-throughput, automated production. These developments favor suppliers providing liquid ingredient formats, precision-dosing systems, and technical support, aligning with the Industry 4.0 emphasis on process monitoring, consistency, and waste reduction. However, regulatory complexity remains a key challenge. Strict GSO standards and Saudi FDA halal certification requirements create high entry barriers, benefitting established players with local technical expertise and traceable supply chains, while new entrants struggle to navigate six distinct national regulatory frameworks. Consequently, the market favors companies capable of combining technological innovation, functional ingredient expertise, and regulatory compliance, positioning them to capture both volume and value in the GCC bakery ingredients sector.

GCC Bakery Ingredients Industry Leaders

-

Cargill Inc.

-

Archer Daniels Midland

-

Kerry Group

-

Lesaffre

-

Puratos Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Localization of ingredient and bakery manufacturing capacity is creating room for growth in starch derivatives, sweeteners, and functional bakery systems that reduce import exposure. Al Ghurair Foods is a direct anchor, as the company announced at Gulfood 2026 a growth strategy that includes launching PURL, an ingredients portfolio spanning starches, sweeteners, specialty flours, and liquid egg, alongside investments tied to industrial food ingredients. The company has also been associated with building the UAE's first corn starch manufacturing plant in KEZAD to produce starches, glucose, and maltodextrin. These moves support local availability of key bulking and texture ingredients used in biscuits, cakes, and gluten-free formulations.

Scale-up of regional bakery manufacturing and integration across channels supports demand for consistent, standardized ingredient systems and technical services. In January 2026, Salalah Mills inaugurated a RO25 million bakery manufacturing plant in Khazaen Economic City, Oman. BinDawood Holding completed the acquisition of a 51% stake in Wonder Bakery for AED 96.9 million, reflecting continued investment in industrial bakery capacity and supply chain resilience. Alongside these capacity additions, stricter additive governance under GSO 2500:2025 and labeling requirements under GSO 9:2022 increase the value of compliant reformulation tools, including clean-label enzyme systems, emulsifier reduction solutions, and traceable ingredient sourcing that can be implemented across multiple GCC markets.

Recent Industry Developments

- March 2026: Cargill announced an expansion of its Port Klang, Malaysia facility with a new specialty fats production line serving bakery and confectionery applications. The added capacity supports availability of specialty fats used in shortenings and fillings, which can tighten lead times and broaden formulation options for multinational and regional bakery customers supplied through global networks.

- December 2025: GNT opened an application laboratory in Dubai to support manufacturers using EXBERRY plant-based colors across the Middle East. With local color matching and stability testing, the facility strengthens speed-to-market for clean-label bakery color systems under GCC labeling and additive requirements.

- November 2024: Tate & Lyle introduced TASTEVA M stevia sweetener at Gulfood Manufacturing, positioned for sugar reduction in cakes and pastries while preserving mouthfeel. The launch expanded the toolkit for reformulation in sweet bakery categories as manufacturers respond to clean-label and reduced-sugar product development needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of ingredients used to make bakery products across GCC countries, counted at the point where ingredients are sold into commercial bakeries, retail baking, and foodservice baking.

Scope exclusions: It excludes finished baked goods sales, baking equipment, packaging, and in-store bakery labor and services.

Segmentation Overview

-

By Ingredient Type

- Baking Enzymes

- Emulsifiers

- Fats and Shortenings

- Sweeteners

- Colors and Flavors

- Others

-

By Form

- Dry

- Liquid

-

By Application

- Bread

- Cakes and Pastries

- Cookies and Biscuits

- Rolls and Pies

- Donuts and Muffins

- Others

-

By End Use

- Commercial/Industrial

- Retail/Household

- Foodservice/HoReCa

-

By Geography

- Saudi Arabia

- United Arab Emirates

- Kuwait

- Qatar

- Bahrain

- Oman

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a fact base on bakery production and food demand across the GCC, then mapping how ingredient use typically follows those volume patterns. We rely on public sources such as national statistics offices and central bank releases, customs and trade portals for import and export trends, FAOSTAT for broader food and grain indicators, and Codex Alimentarius or Gulf standards bodies for ingredient and labeling rules.

To tighten assumptions, we also review company annual reports and investor presentations where regional exposure is discussed, together with credible press and association websites linked to baking and food processing. In addition, we use paid subscriptions focused on company financials, patent databases, and shipment-level import and export data to sanity check supplier presence, new formulations, and trade-linked supply patterns. These examples are not exhaustive, and other public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews are used to confirm real buying patterns for bakery mixes and functional ingredients, and to validate how usage differs between industrial bakers, retail bakeries, and HoReCa kitchens across the GCC. We spoke with ingredient manufacturers, distributors, importers, and commercial bakery procurement and technical teams, and the responses were cross-checked by country to avoid over-weighting any single part of the region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 56% |

Market-Sizing & Forecasting

The sizing model starts with a top-down build where bakery output and consumption signals are translated into an ingredient demand pool for the GCC, then split by the ingredient groups covered in the study. To keep it grounded, we run selective bottom-up checks, such as sampled supplier revenue ranges, channel checks with importers and distributors, and simple volume times average selling price logic for higher-visibility inputs.

Key inputs shaping the model include bakery production growth by country, shifts in bread and sweet bakery consumption, wheat and sugar price movements that affect formulation economics, the mix shift toward industrial baked formats, and trade intensity for imported ingredients that are not widely produced locally. For forecasting, we use scenario-based modeling supported by exponential smoothing on stable series, and then adjust using expert input on pricing pass-through, reformulation trends, and foodservice demand cycles. Where bottom-up checks have gaps, we avoid forcing a full supplier roll-up and instead apply conservative ranges that are reconciled back to the demand pool before finalizing totals.

Data Validation & Update Cycle

Outputs are validated through a sequence of checks, starting with sanity tests on growth rates, pricing movement, and country shares, followed by deeper variance reviews when a segment moves outside expected bounds. We then compare results against independent signals such as trade direction, key raw material cost swings, and reported capacity or expansion announcements that can explain step changes.

Before sign-off, the model and assumptions go through multi-step analyst review, and follow-up calls are triggered when a gap cannot be explained by documented drivers. The report is refreshed annually, and interim updates are made when material events occur, such as regulation changes affecting ingredient approvals or sudden price shocks. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Gcc Bakery Ingredients Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for GCC bakery ingredients because studies do not always count the same ingredient basket, selling point in the value chain, or countries in exactly the same way. Differences also come from whether value is built using demand indicators or inferred mainly from supplier revenues, and from how pricing is treated during high inflation periods.

By tracking import intensity, bakery output proxies, and average selling price updates each year, Mordor Intelligence keeps the GCC bakery ingredients total focused on ingredient sales into baking applications only, which avoids mixing in finished baked product value or broader food ingredient pools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.87 B (2025) | |

| Global Consultancy A | USD 3.92 B (2024) | This estimate appears to use a wider value pool, which can happen when adjacent food ingredients or downstream baked product value is included, and when the year and currency timing differ from a 2025 base. |

| Industry Publisher B | USD 0.89 B (2025) | The number is close but can vary due to slightly different treatment of ingredient types and end-use coverage, plus differences in how pricing and country-level weights are updated across the GCC. |

The spread across sources is mainly explained by scope boundaries and how demand is reconstructed from production and trade signals versus broader category roll-ups. When the ingredient-only boundary and yearly price updates are kept consistent, the resulting market size stays easier to trace back to clear variables and repeatable steps that users can audit.

Key Questions Answered in the Report

How large is the GCC Bakery Ingredients market in 2026?

The GCC Bakery Ingredients market size stands at USD 0.93 billion in 2026 and is forecast to grow at 6.85% CAGR to 2031.

Which ingredient type grows fastest through 2031?

Baking enzymes record the highest 8.25% CAGR, driven by clean-label and shelf-life demands.

What segment captures most application revenue?

Bread accounts for 52.35% of 2025 revenue, underpinned by staple flatbread and sandwich loaf consumption.

Which country leads regional revenue?

Saudi Arabia contributes 45.20% of 2025 sales, supported by Almarai’s scale and mandatory halal rules.

What is the main supply-chain challenge?

High import dependency for specialty enzymes and emulsifiers exposes producers to freight disruptions and currency swings.

Page last updated on: