Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.99 Billion |

| Market Size (2026) | USD 1.08 Billion |

| Market Size (2031) | USD 1.66 Billion |

| Growth Rate (2026 - 2031) | 9.00% CAGR |

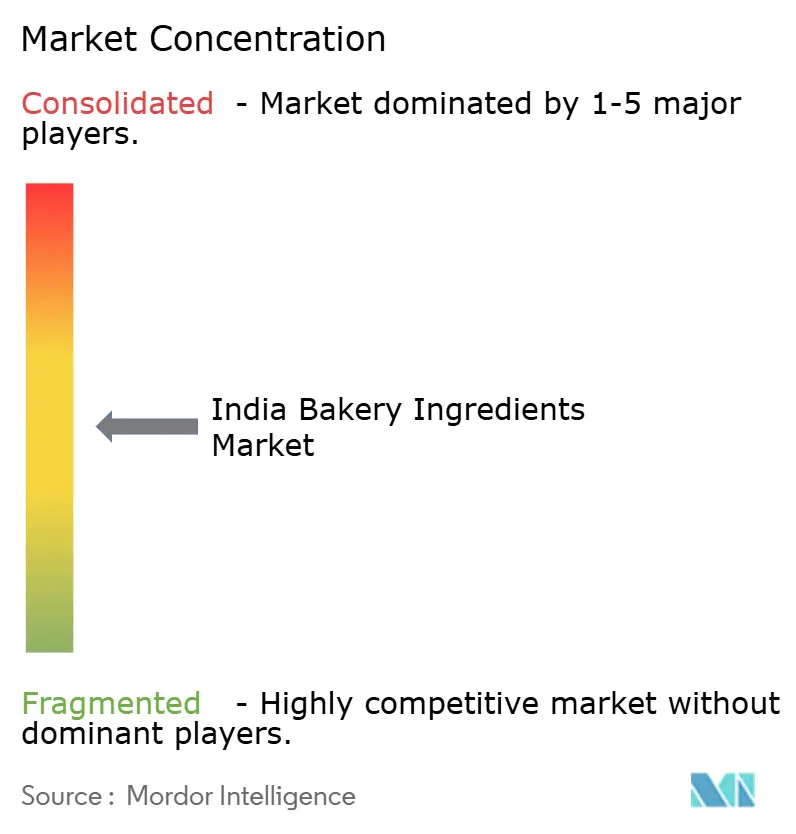

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Bakery Ingredients Market Analysis by Mordor Intelligence

The India Bakery Ingredients Market size was valued at USD 0.99 billion in 2025 and estimated to grow from USD 1.08 billion in 2026 to reach USD 1.66 billion by 2031, at a CAGR of 9.00% during the forecast period (2026-2031). This expansion in the Indian Bakery Ingredients Market is driven by the penetration of café culture, rising on-the-go eating habits, and policy incentives that favor clean-label reformulation. Multinational chains such as Starbucks aim to target 1,000 Indian outlets by 2028, thereby encouraging demand for laminating fats, enzymes, and natural colors. Ingredient suppliers are refining portfolios toward specialty enzymes that replace conventional emulsifiers, and toward trans-fat-free shortenings that satisfy FSSAI’s ≤2% mandate. At the same time, cold-chain investments in metro clusters lift adoption of liquid formats, while wheat and palm oil price swings test the resilience of suppliers that lack hedging strategies. The India Bakery Ingredients Market continues to reward companies able to balance functionality, regulatory compliance, and cost containment.

Key Report Takeaways

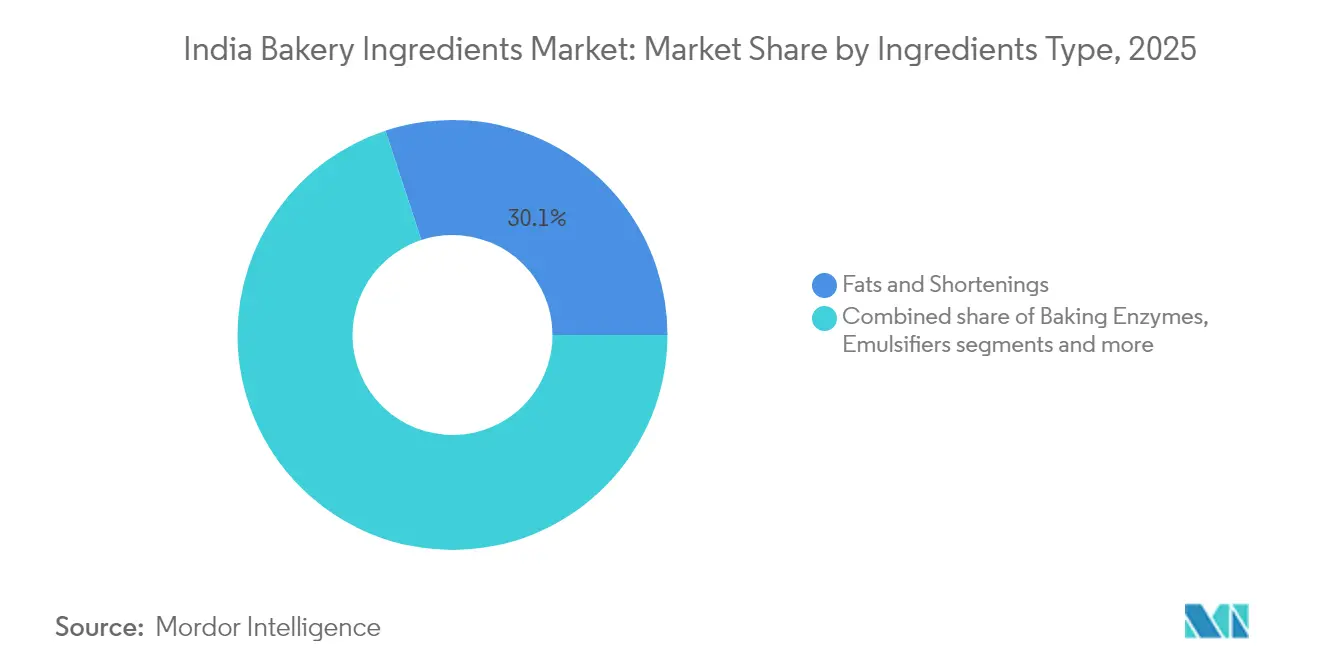

- By ingredient type, fats and shortenings led with 30.05% revenue share in 2025; baking enzymes are advancing at a 9.41% CAGR through 2031.

- By application, bread captured 39.71% of the India Bakery Ingredients market share in 2025, while cakes and pastries are set to grow at a 10.02% CAGR by 2031.

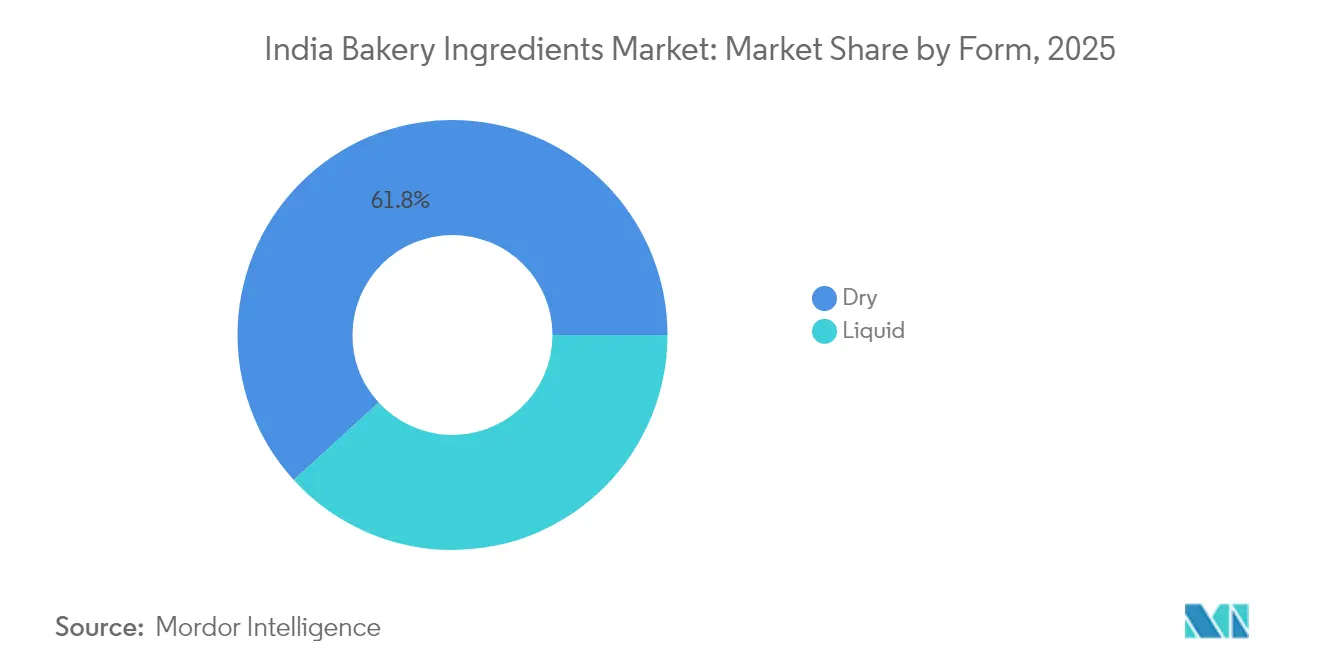

- By form, dry ingredients accounted for 61.78% of the India Bakery Ingredients market size in 2025; liquid formats are forecast to rise at a 10.35% CAGR to 2031.

- By distribution channel, the commercial-industrial segment held 49.55% share of the India Bakery Ingredients Market in 2025, whereas foodservice/HoReCa is recording the highest projected CAGR at 10.08% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Bakery Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising exposure to Western-style eating and café culture | +1.8% | Metro cities (Delhi NCR, Mumbai, Bengaluru, Pune), expanding to Tier-1 cities | Medium term (2-4 years) |

| Shift to convenience and on-the-go foods | +2.1% | National, with concentration in urban centers and transport hubs | Short term (≤ 2 years) |

| Increasing demand for clean-label and natural ingredients | +1.5% | National, led by metros and Tier-1 cities | Medium term (2-4 years) |

| Health and wellness reformulation | +1.3% | National, stronger in affluent urban segments | Medium term (2-4 years) |

| Millet-based flours boom post IYoM 2023 | +0.9% | National, with government procurement driving rural uptake | Long term (≥ 4 years) |

| PLISFPI and PMFME incentives accelerate local ingredient capacity | +1.2% | National, cluster development in Uttar Pradesh, Maharashtra, Tamil Nadu | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising exposure to Western-style eating and café culture

The increasing exposure to Western-style eating habits and the growing café culture are reshaping the demand for bakery ingredients in India. This trend is driving the popularity of products such as croissants, Danish pastries, and artisan breads, which require specialized ingredients like laminating fats, emulsifiers, and enzyme blends that are not traditionally used in Indian baking. International chains such as Starbucks, which aims to establish 1,000 stores by 2028, along with domestic brands like Blue Tokai and Third Wave Coffee, are expanding their presence beyond metropolitan areas into Tier-1 cities. These outlets typically rotate between eight to twelve baked stock-keeping units weekly, creating a dynamic demand for a diverse range of ingredients. Suppliers are addressing this demand by offering products such as butter substitutes, natural vanilla extracts, and dough conditioners that can adapt to India's varied climatic conditions, ensuring consistent quality and crumb structure. The café channel acts as a significant driver of demand and innovation, introducing premium ingredients like Belgian chocolate compounds, fruit purées, and enzyme-treated flours, which eventually find their way into supermarket bakery sections and cloud kitchens. As café culture expands to cities like Coimbatore and Jaipur, the pace of innovation accelerates, benefiting suppliers who collaborate on limited-edition flavors and provide technical expertise in processes such as lamination and proofing. This collaboration enhances the sophistication of the baking ecosystem in India while increasing consumer acceptance of premium and diverse bakery products. Brands like The Coffee Bean and Tea Leaf further illustrate this trend by incorporating artisanal bakery offerings that require advanced ingredient solutions, highlighting the critical role of café culture in shaping ingredient demand and driving innovation in the Indian bakery ingredients market.

Shift to convenience and the on-the-go foods

The increasing demand for convenience and on-the-go foods is driving significant changes in ingredient requirements within the bakery market. Quick commerce platforms and modern trade channels are encouraging bakers to create products with extended ambient shelf-life and precise portion control. This shift is supported by a growing culture of out-of-home snacking, with food services projected to double by 2030 as office commuters, students, and travelers seek convenient breakfast and snack options. These evolving preferences necessitate the use of preservatives that align with clean-label guidelines set by the Food Safety and Standards Authority of India, emulsifiers to prevent oil migration in wrapped products like muffins, and enzymes that delay staling without relying on synthetic additives. The quick commerce model, which promises rapid delivery times, is also pressuring cloud kitchens to pre-bake and store goods, increasing the need for moisture-retention agents and antifungal solutions to maintain sensory quality during ambient storage. Manufacturers are innovating with single-dose sachets and liquid enzyme systems to reduce weighing errors and contamination in high-pressure kitchen environments, enhancing operational efficiency. Transport hubs such as airports and metro stations, where bakery products are exposed to temperature fluctuations and rough handling, are further driving demand for stabilizers and packaging-compatible coatings. The Household Consumption Expenditure Survey for 2023–24 by the Ministry of Statistics and Programme Implementation highlights the substantial share of food in monthly per-capita expenditure, 48.4% in rural areas and 40.3% in urban areas, indicating robust demand for packaged foods [1]Source: Ministry of Statistics and Programme Implementation (MOSPI), "Household Consumption Expenditure Survey: 2023-24 Fact Sheet", mospi.gov.in. Brands such as Noice through Swiggy are addressing this trend by offering pre-packaged bakery snacks designed for on-the-go consumption through quick commerce platforms, reflecting the critical ingredient trends shaping this evolving market segment.

Millet-based flours boom post IYoM 2023

The increasing adoption of millet-based flours is transforming formulations in the bakery ingredients market, driven by heightened consumer demand for nutrient-dense alternatives such as ragi, jowar, and bajra flours. Bakers are incorporating these flours into breads, cookies, and cakes to meet health-conscious preferences while maintaining desirable texture and rise. This trend is supported by India's projected millet production of 180.15 lakh tonnes in 2024–25, reflecting an increase of 4.43 lakh tonnes compared to the previous year, as per Press Information Bureau, ensuring sufficient domestic supply for bakery applications that enhance fiber and mineral content without compromising flavor [2]Source: Press Information Bureau, "Shree Anna for Shreshta Bharat - Empowering India through Millets", pib.gov.in. Ingredient suppliers are addressing challenges such as denser crumb and shorter shelf life by blending these grains with enzymes and emulsifiers, enabling their seamless integration into premium multigrain loaves and gluten-free pastries. The momentum generated by the International Year of Millets has further spurred innovation, with ready mixes combining millet flours with ingredients like sourdough or jaggery to create authentic taste profiles that appeal to urban wellness-focused consumers. This development aligns with the clean-label movement, as millet flours naturally reduce reliance on synthetic additives, promoting sustainable sourcing and nutritional enhancement in everyday baking. Brands such as Puratos India are capitalizing on this trend with products like Easy Puravita Millet Bread Mix, a blend of five millets with Dutch-origin sourdough, and Tegral Satin Millet Cake Mix, which incorporates sorghum, finger, and pearl millet flours while excluding refined sugar and maida. As production scales, millet-based flours are transitioning from artisanal bakeries to industrial production lines, streamlining reformulation processes and strengthening millet's role in the evolving bakery market.

PLISFPI and PMFME incentives accelerate local ingredient capacity

The Production Linked Incentive Scheme for Food Processing Industry (PLISFPI) and the Prime Minister’s Formalisation of Micro Food Enterprises (PMFME) scheme are driving significant advancements in local ingredient production capacity within the bakery ingredients market. These government initiatives, as outlined by the Ministry of Food Processing Industries, aim to increase processed food output to INR 33,494 crore by 2026-27 [3]Source: Ministry of Food Processing Industries, "Production Linked Incentive Scheme for Food Processing Industry (PLISFPI)", mofpi.gov.in. By enhancing the sourcing of locally processed flours, emulsifiers, and natural additives, these schemes reduce dependency on imports and improve cost efficiency for both ingredient suppliers and bakers. They also promote the adoption of advanced technologies, ensure quality assurance, and enforce compliance with food safety standards, thereby fostering a more resilient manufacturing ecosystem capable of addressing modern bakery requirements, including clean-label and health-oriented formulations. Companies such as Puratos India leverage these initiatives by collaborating with local millers and ingredient manufacturers, ensuring a reliable supply of high-quality millet flour blends and enzyme systems. Furthermore, the focus on micro-enterprises supports artisan and regional bakeries by enabling wider distribution and encouraging innovation with local flavors and grain varieties. This alignment of policy support with market demand strengthens the bakery ingredients supply chain, catering to the growing urban and rural consumer demand for diverse and nutritious baked products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility | -1.4% | National, acute in import-dependent coastal states | Short term (≤ 2 years) |

| Stringent and evolving food regulations | -0.8% | National, compliance burden higher for SMEs | Medium term (2-4 years) |

| Limited cold-chain in Tier-2/3 curbs liquid-enzyme uptake | -1.1% | Tier-2/3 cities across Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan | Long term (≥ 4 years) |

| Consumer concerns over "chemicals" in food | -0.6% | National, more pronounced in educated urban demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw material price volatility

Volatility in raw material prices significantly impacts the bakery ingredients market, as it heavily depends on agricultural commodities such as wheat, vegetable oils, sugar, and dairy derivatives. This reliance exposes manufacturers to unpredictable price fluctuations, which erode profit margins. For example, wheat and sugar prices rose by 14% and 15%, respectively, in 2022-23, according to the Food and Agriculture Organization. These increases directly inflate the costs of essential inputs like flour and sweeteners, forcing bakers to either absorb the additional expenses or pass them on to consumers, often disrupting long-term supply agreements. Frequent cost changes complicate planning for large-scale operations, slowing the adoption of premium or innovative solutions such as enzyme blends or clean-label emulsifiers, which carry higher baseline costs. Smaller regional suppliers and artisanal bakeries, lacking access to hedging tools, face intensified financial pressure, further fragmenting the market and limiting investments in research and development or capacity expansion. Companies like Dawn Foods India address these challenges by securing vertical integration with local oilseed processors and diversifying into palm-based shortenings, which are less affected by dairy price volatility. However, even these companies must frequently adjust formulations to maintain competitive pricing for fats and shortenings used in products like cookies and bread. Supply chain disruptions caused by weather events or global crises further amplify risks for imported specialty inputs such as cocoa derivatives, with cocoa prices surging approximately 300% in recent years. These challenges push the entire supply chain, from millers to multinational ingredient manufacturers, toward strategies like strategic sourcing, long-term supplier agreements, and alternative ingredient blends, often hindering seamless growth in a market that demands consistent, affordable, and high-performance ingredients.

Limited cold-chain in Tier-2/3 curbs liquid-enzyme uptake

The limited availability of cold-chain infrastructure in Tier-2 and Tier-3 cities, marked by inadequate refrigerated transport and last-mile storage, significantly impacts the adoption of liquid enzymes such as amylases, proteases, and xylanases in the bakery ingredients market. These enzymes, which provide superior dough conditioning and extend shelf life, require storage temperatures between 2-8°C and are prone to degradation under ambient transit conditions. Bakers in these regions often opt for dry-form enzymes or avoid enzyme usage altogether, which compromises product quality, texture consistency, and freshness while allowing them to bypass the risks and costs associated with cold-chain logistics. This reliance on less efficient alternatives is further compounded by challenges in distributing fresh compressed yeast, which offers improved fermentation control and enhanced flavor compared to active dry yeast but has a refrigerated shelf life of only 4-6 weeks, making it impractical for areas beyond metropolitan and Tier-1 cities. These limitations restrict innovation in premium formulations, forcing regional bakeries to depend on ambient-stable products rather than advanced enzyme-yeast systems for artisan breads or extended-shelf-life pastries. Companies such as AB Enzymes India have introduced hybrid dry-liquid enzyme blends stabilized for warmer conditions to address these challenges, but their adoption remains limited outside urban centers, underscoring how cold-chain deficiencies fragment the market and hinder the transition to high-performance bakery ingredients nationwide.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredients Type: Enzymes Gain as Fats Plateau

Baking enzymes are anticipated to drive significant growth in the bakery ingredients market, with a projected compound annual growth rate of 9.41% from 2026 to 2031. This growth is expected to outpace fats and shortenings, which, despite holding a dominant 30.05% market share in 2025, are seeing reduced emphasis. Bakers are increasingly focusing on enzymes for their ability to improve dough conditioning and extend shelf life, aligning with clean-label trends that prioritize natural and functional ingredients over traditional fat-based texturizers. Emulsifiers, such as lecithin, diacetyl tartaric acid esters of monoglycerides, and sodium stearoyl lactylate, remain critical for stabilizing texture in laminated pastries and aerated cakes. However, their growth is limited by consumer demand for alternatives to synthetic surfactants. Leavening agents, while maintaining stable volumes due to their commodity nature, face margin pressures from pricing volatility and limited innovation opportunities, resulting in moderate growth.

Sweeteners are diverging into bulk sugars and premium specialty options like stevia and erythritol, which appeal to health-conscious consumers but require flavor-masking technologies to address off-flavors. Colors and flavors are transitioning to natural alternatives, with turmeric, beetroot, and spirulina extracts replacing synthetic dyes. Vanilla and chocolate flavors increasingly utilize natural extracts and fruit purées to meet clean-label requirements. Preservatives are undergoing reformulation, with cultured wheat and vinegar-based systems replacing traditional options like calcium propionate and potassium sorbate. Meanwhile, fats and shortenings are adapting to trans-fat bans, driving innovation in enzymatic interesterification and oleogel technologies to replicate the functionality of traditional fats. Brands such as AB Mauri India are leading this transition by offering enzyme systems and clean-label emulsifiers that align with evolving consumer and baker preferences.

By Application: Cakes and Pastries Outpace Bread

Cakes and pastries are expected to experience significant growth in ingredient spending, with a compound annual growth rate of 10.02% projected through 2031. This trend is driven by the expanding bakery assortments in café chains, quick-service restaurants, and modern retail outlets. Bread, which is anticipated to account for 39.71% of ingredient spending in 2025 due to its staple status and high production volumes, is witnessing slower growth due to market saturation and price competition. The rapid expansion of café chains, including global brands like Starbucks targeting 1,000 stores by 2028 and domestic players such as Blue Tokai and Third Wave Coffee increasing their presence in Tier-1 cities, is fueling demand for premium bakery products like croissants, Danish pastries, and layered cakes. These products require specialized ingredients such as specialty fats, emulsifiers, and enzyme blends, which are not commonly used in bread, driving innovation in premium bakery formulations.

Besides, cookies and biscuits, led by established brands like Britannia and Parle, are undergoing reformulation to reduce trans fats and added sugars in response to regulatory labeling changes. This has increased demand for fat replacers, sugar-reduction enzymes, and natural flavors to maintain product quality. Smaller segments, including rolls and pies, are gaining momentum with the growth of foodservice, particularly in cloud kitchens and quick-commerce platforms. Additionally, donuts and muffins are expanding in modern retail and café channels, supported by moisture-retention systems and anti-staling enzymes that extend shelf life. The "others" category, encompassing pizza bases and ethnic flatbreads, is growing due to the popularity of fusion cuisine and international chains, requiring ingredient flexibility to meet diverse baking needs.

By Form: Liquid Gains Despite Dry Dominance

Liquid bakery ingredients are experiencing significant growth, with a projected compound annual growth rate of 10.35% between 2026 and 2031. This growth is attributed to the adoption of automated dosing systems by industrial bakers and the expansion of cold-chain infrastructure in metropolitan and Tier-1 cities. These advancements enable the efficient handling of liquid enzymes such as amylases, proteases, and xylanases, which offer benefits like uniform dispersion, faster activation, reduced mixing times, and improved batch consistency. These attributes make liquid enzymes particularly appealing for premium bakery formulations. For instance, Cargill’s planned 2025 launch of a large-scale corn milling plant in Gwalior aims to expand its portfolio of liquid glucose syrups and maltodextrins, supporting the shift toward liquid-based humectants and sweeteners. Additionally, liquid emulsifiers like lecithin and monoglycerides are increasingly preferred in high-speed bakeries for resolving dusting and clumping issues associated with powdered alternatives, although higher freight and storage costs limit their adoption in cost-sensitive segments.

Dry bakery ingredients continue to dominate the market due to their logistical advantages, including ambient storage, longer shelf life, and lower freight costs. These factors are particularly important in Tier-2 and Tier-3 cities, where cold-chain infrastructure penetration remains below 5%. Dry enzyme blends, leavening agents, and powdered emulsifiers are essential for smaller and mid-tier bakeries that lack refrigerated storage and prefer consolidated dry mixes for operational simplicity. While staple categories such as bread and cookies favor dry formats for cost-effectiveness and ease of use, cakes, pastries, and premium artisan products increasingly specify liquid systems to achieve superior functional outcomes. Companies like Puratos India address this diverse demand by offering both dry and liquid enzyme systems tailored to the varied needs of bakery customers across the country.

By Distribution Channel: Foodservice Surges as Industrial Holds

The foodservice distribution channel in the bakery ingredients market is projected to experience significant growth, with a compound annual growth rate of 10.08% through 2031. This expansion is fueled by the rising number of cloud kitchens, café chains, and quick-service restaurants, which require pre-portioned and consistent-quality ingredients to streamline operations. These ingredients help reduce labor and minimize waste in fast-paced kitchen environments. To address these needs, suppliers are introducing innovations such as single-dose sachets, liquid enzyme systems, and technical advisory services tailored for high-turnover operations with limited storage and unskilled labor. The rapid growth of brands like Zepto Cafe, which operates on quick commerce and cloud kitchen models, highlights the evolving ingredient requirements in this channel.

The commercial channel continues to dominate, holding a 49.55% market share in 2025. This segment primarily serves large-scale bakeries and biscuit manufacturers that purchase bulk quantities of fats, enzymes, and emulsifiers, focusing on cost efficiency and supply reliability. In contrast, the retail channel, which caters to home bakers and hobbyists, remains the smallest segment due to the relatively low frequency of home baking in the region compared to Western markets. However, this segment is growing as urban millennials and Gen-Z consumers increasingly take up baking as a leisure activity, influenced by digital tutorials and social media. These distinct channel dynamics drive suppliers like Puratos India and Dawn Foods to develop differentiated product offerings and marketing strategies to meet the unique needs of each segment.

Geography Analysis

Regional differences in urbanization, cold-chain infrastructure, and dietary habits significantly influence the bakery ingredients market. Metro cities such as Delhi NCR, Mumbai, Bengaluru, and Pune, along with Tier-1 hubs, account for over 60.00% of the projected 2025 ingredient value consumption. These urban centers, characterized by a high density of café chains, modern retail outlets, and industrial bakeries, drive demand for advanced specialty enzymes, natural flavors, and clean-label emulsifiers that cater to premium Western-style baking. Western and southern states, including Maharashtra, Karnataka, and Tamil Nadu, lead in ingredient sophistication, supported by multinational bakeries, export processors, and proximity to ports that facilitate the import of specialty fats and flavor systems. Suppliers like Dawn Foods India play a pivotal role by offering customized blends for high-volume cake and pastry production, seamlessly connecting urban demand with global supply chains.

Tier-2 and Tier-3 cities such as Lucknow, Indore, Coimbatore, and Visakhapatnam are emerging as growth areas, though their ingredient preferences lean toward affordable dry formats and basic commodity fats due to price sensitivity and limited cold-chain infrastructure. These regions face challenges, including a 70% spoilage rate for perishables caused by inadequate refrigerated transport and last-mile storage, which restricts the adoption of liquid enzymes and fresh yeast despite their advantages in dough performance and shelf-life extension. Government initiatives such as the Production Linked Incentive Scheme for the Food Processing Industry and the Pradhan Mantri Formalisation of Micro Food Processing Enterprises scheme aim to establish ingredient manufacturing clusters in states like Uttar Pradesh, Madhya Pradesh, and Rajasthan. Brands like SwissBake address these challenges by offering ambient-stable dry mixes tailored to local constraints, bridging the gap between growing demand and infrastructural limitations.

Northern states, with their wheat-centric diets, maintain steady bulk demand for bread and biscuit ingredients, including flours, leavening agents, and shortenings in traditional formats. In contrast, southern states exhibit strong demand for rice-based and millet-blended products, driven by campaigns promoting nutrient-rich bakery innovations following the International Year of Millets 2023. These grain preferences result in distinct regional formulations, with the north favoring wheat-heavy products and the south adopting millet-infused alternatives. Companies like Jiwa are capitalizing on these shifts by offering millet flour blends for gluten-free cookies, demonstrating how dietary diversity drives targeted ingredient development across the bakery market.

Competitive Landscape

The bakery ingredients market in India is moderately fragmented, with global companies such as Cargill, ADM, and DSM-Firmenich holding significant positions. These companies leverage their scale in research and development, regulatory expertise, and extensive multi-ingredient portfolios, including fats, enzymes, emulsifiers, and flavors. Regional players like Advanced Enzymes Technologies and emerging yeast producers compete by offering localized solutions, cost-efficient operations, and a deeper understanding of Indian baking requirements. Competitive strategies focus on broad product portfolios for comprehensive solutions, technical co-development through application labs to support clean-label and shelf-life reformulations, and proactive regulatory compliance by aligning with mandates from the Food Safety and Standards Authority of India. This approach allows global firms to drive innovation while regional companies focus on customized blends, creating a dynamic and balanced competitive environment.

Growth opportunities are emerging in millet-based systems that address flavor masking, shelf-life extension, and nutritional fortification, aligning with trends following the International Year of Millets. Other areas of potential include liquid enzyme blends designed for automated dosing in high-speed production lines, supported by advancements in cold-chain infrastructure, and halal-certified emulsifiers and flavors catering to India's Muslim population and export markets in the Middle East. These opportunities align with broader market drivers such as health, convenience, and regulatory compliance, favoring companies that can integrate regional dietary preferences with global standards. Biotech startups developing precision-fermented fats and proteins to replicate dairy and egg functionalities without animal sources present potential for plant-based innovation, though regulatory and cost challenges may delay their market entry by several years. Multinational companies are utilizing advanced technologies for rapid innovation, while regional firms focus on process optimization and practical refinements to address market needs.

Government initiatives, including the Production Linked Incentive Scheme for the Food Processing Industry and the Pradhan Mantri Formalisation of Micro Food Processing Enterprises scheme, are intensifying competition by reducing capital expenditure risks for mid-tier producers. These policies are compressing margins in commodity segments such as leavening agents and bulk fats while driving premiums for differentiated products like enzymes, natural flavors, and functional blends. Global players are focusing on technology-driven differentiation, regional firms are scaling operations through government incentives, and startups are pursuing biotech innovations. The competitive landscape increasingly favors agile companies offering specialized solutions, with co-development labs becoming critical for fostering customer loyalty. Companies such as DSM-Firmenich are leading in halal-certified flavors, combining regulatory foresight with export ambitions and domestic clean-label demands, reflecting the market's shift toward hybrid models that integrate scale with specialization.

India Bakery Ingredients Industry Leaders

-

Cargill, Incorporated

-

Associated British Foods PLC

-

Puratos NV

-

DSM-Firmenich AG

-

Archer Daniels Midland Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Sensarom partnered with Angel Yeast, a China-based company, to distribute and sell its products across South India. Sensarom Foods served as the official distributor for yeast extract powders used in various applications, including seasonings, soups, packaged meals, ready-to-eat foods, plant-based meat products, and bakery ingredients. The bakery segment included products such as bread improvers, instant dry yeast, and dough relaxing agents for leavening and texture enhancement. These products were available for direct sales and distribution in the Indian and Southwest Asian markets.

- August 2024: Corbion, a provider of sustainable ingredient solutions, acquired the bread improver business of Novotech Food Ingredients, headquartered in Delhi, India. This acquisition enabled Corbion to provide Indian bakers with access to its global customer support network, enhancing its market position and ability to deliver customized functional solutions.

- March 2023: Cargill introduced a range of products at AAHAAR 2023, held in New Delhi. It participated in one of India’s largest food ingredients exhibitions, which was themed "Re(discover) what’s possible together." Cargill showcased product applications focused on health and nutrition, fusion baking, and innovation. These offerings were co-developed with its bakery partners to cater to Indian consumers.

India Bakery Ingredients Market Report Scope

The ingredients used in baking and making bakery products are called bakery ingredients. They are intended to bring about taste, flavor, and freshness and increase the shelf life of baked commodities. The Indian bakery ingredients market is segmented on the basis of type and applications. By type, the market is segmented into baking enzymes, fats and shortenings, leavening agents, emulsifiers, enzymes, sweeteners, colors and flavors, preservatives, and other types. By application, the market is segmented into bread, cakes and pastries, rolls and pies, cookies and biscuits, and other applications. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Ingredients Type

| Baking Enzymes |

| Leavening Agents |

| Emulsifiers |

| Fats and Shortenings |

| Sweeteners |

| Colors and Flavors |

| Preservatives |

| Others |

By Application

| Bread |

| Cakes and Pastries |

| Cookies and Biscuits |

| Rolls and Pies |

| Donuts and Muffins |

| Others |

By Form

| Dry |

| Liquid |

By Distribution Channel

| Commercial/Industrial |

| Retail/Household |

| Foodservice/HoReCa |

| By Ingredients Type | Baking Enzymes |

| Leavening Agents | |

| Emulsifiers | |

| Fats and Shortenings | |

| Sweeteners | |

| Colors and Flavors | |

| Preservatives | |

| Others | |

| By Application | Bread |

| Cakes and Pastries | |

| Cookies and Biscuits | |

| Rolls and Pies | |

| Donuts and Muffins | |

| Others | |

| By Form | Dry |

| Liquid | |

| By Distribution Channel | Commercial/Industrial |

| Retail/Household | |

| Foodservice/HoReCa |

Key Questions Answered in the Report

How large is the India Bakery Ingredients Market in 2026 and how fast is it growing?

The market measures USD 1.08 billion in 2026 and is projected to expand at a 9.00% CAGR during the forecast period (2026-2031).

Which ingredient type is expanding fastest?

Baking enzymes lead growth at a 9.41% CAGR as bakers pursue clean-label dough conditioning and shelf-life extension.

What application segment will outpace overall market growth?

Cakes and pastries are forecast to rise at a 10.02% CAGR, ahead of bread and cookies, due to café and QSR expansion.

Why are liquid ingredient formats gaining popularity?

Industrial bakeries adopt automated dosing, and improved metro cold-chain networks support liquid enzymes and emulsifiers, driving a 10.35% CAGR for liquid formats.

Which distribution channel shows the highest CAGR?

Foodservice/HoReCa is advancing at 10.08% CAGR, fueled by cloud kitchens and café chains that demand pre-portioned, high-performance ingredients.

Page last updated on: