Bakery Premixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.74 Billion |

| Market Size (2031) | USD 2.47 Billion |

| Growth Rate (2026 - 2031) | 7.26% CAGR |

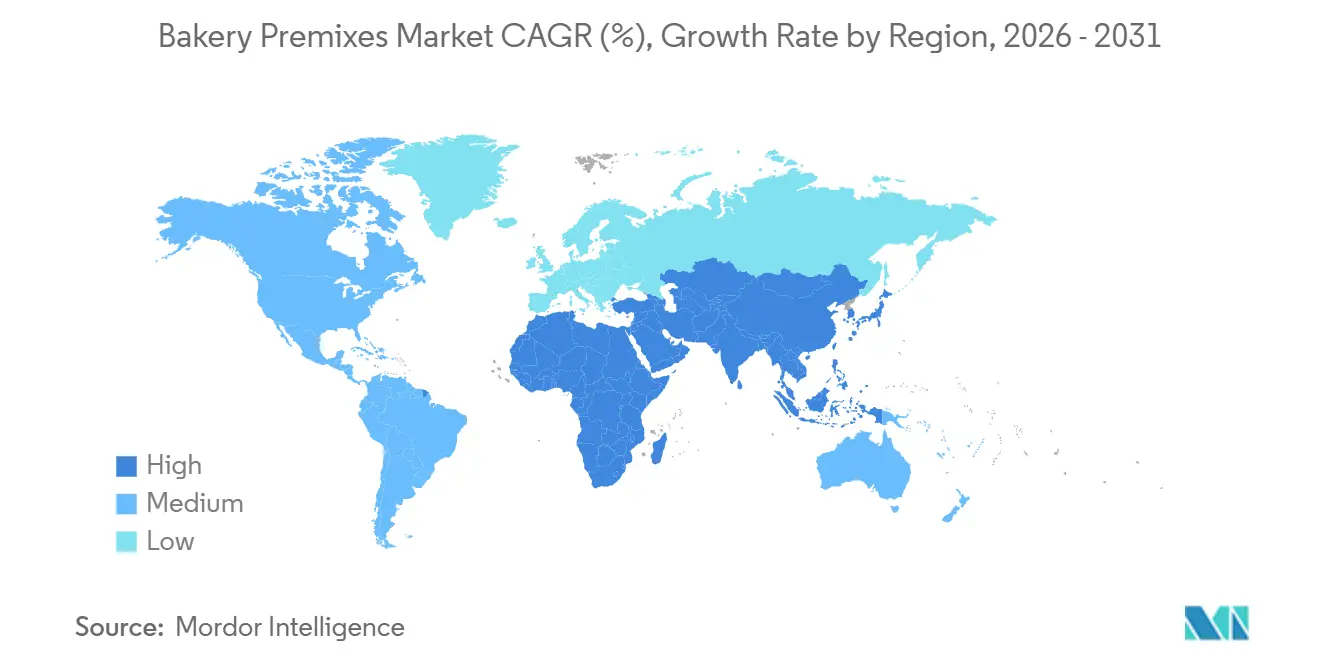

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bakery Premixes Market Analysis by Mordor Intelligence

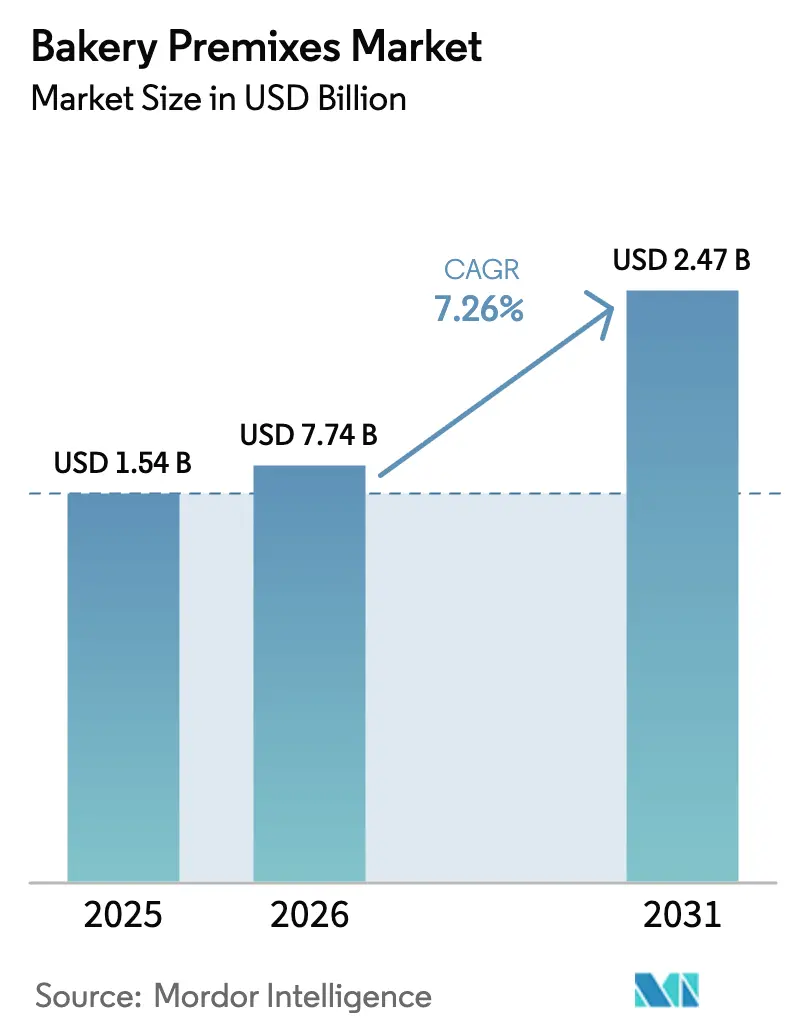

The Bakery Premixes Market size was valued at USD 1.54 billion in 2025 and is estimated to grow from USD 7.74 billion in 2026 to reach USD 2.47 billion by 2031, at a CAGR of 7.26% during the forecast period (2026-2031). Industrial bakeries are optimizing operations by utilizing standardized ingredient systems, which help reduce labor hours and minimize waste. Simultaneously, quick-service restaurant chains in emerging markets are adopting bulk premixes to ensure batch consistency and enhance service speed. In Europe and North America, reformulation mandates are boosting the demand for specialty blends that focus on reduced sodium, higher fiber content, and natural enzymes. Additionally, innovations such as cloud-connected mixers and inventory software enable bakers to track moisture and temperature in real-time, increasing the switching costs for operators still relying on traditional scratch recipes. Although price volatility in wheat and dairy presents challenges, vertical integration by leading suppliers helps stabilize margins and ensures consistent supply to both on-trade and off-trade channels.

Key Report Takeaways

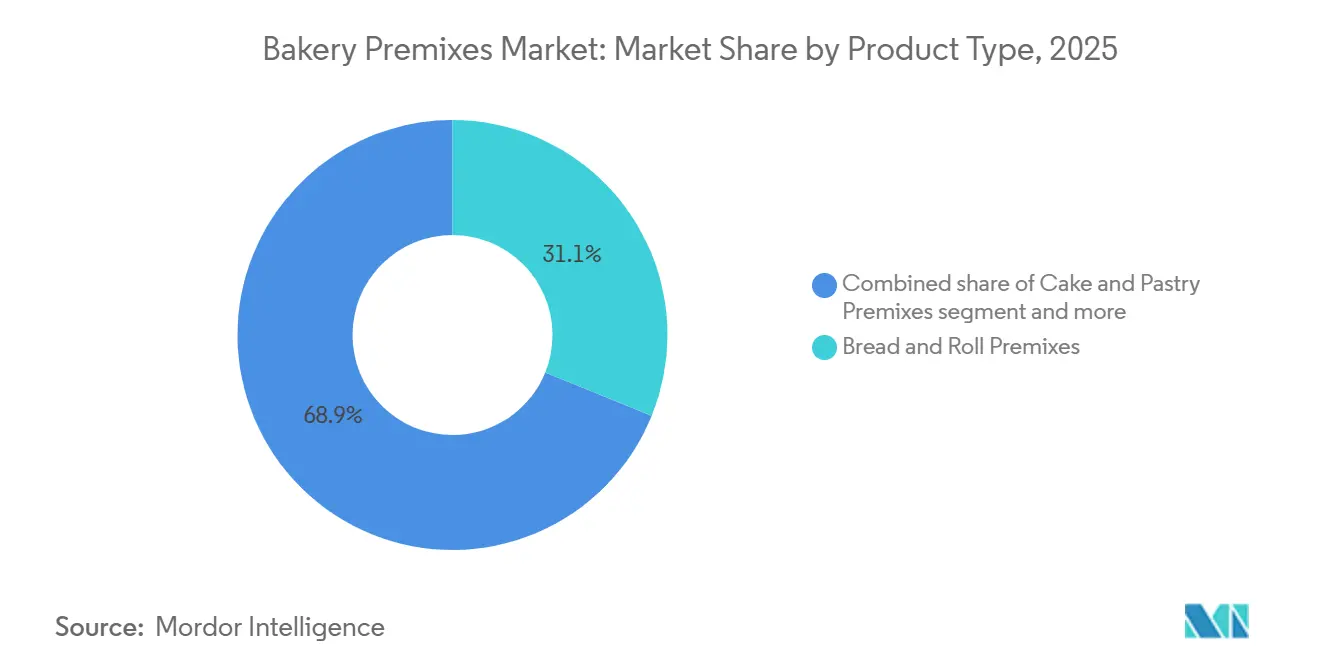

- By product type, bread and roll formats led with 31.12% of the bakery premixes market share in 2025, while muffin and pancake mixes are projected to record a 7.88% CAGR through 2031.

- By category, conventional blends accounted for 76.27% of the 2025 value, whereas specialty variants are poised to expand at a 7.69% CAGR during 2026-2031.

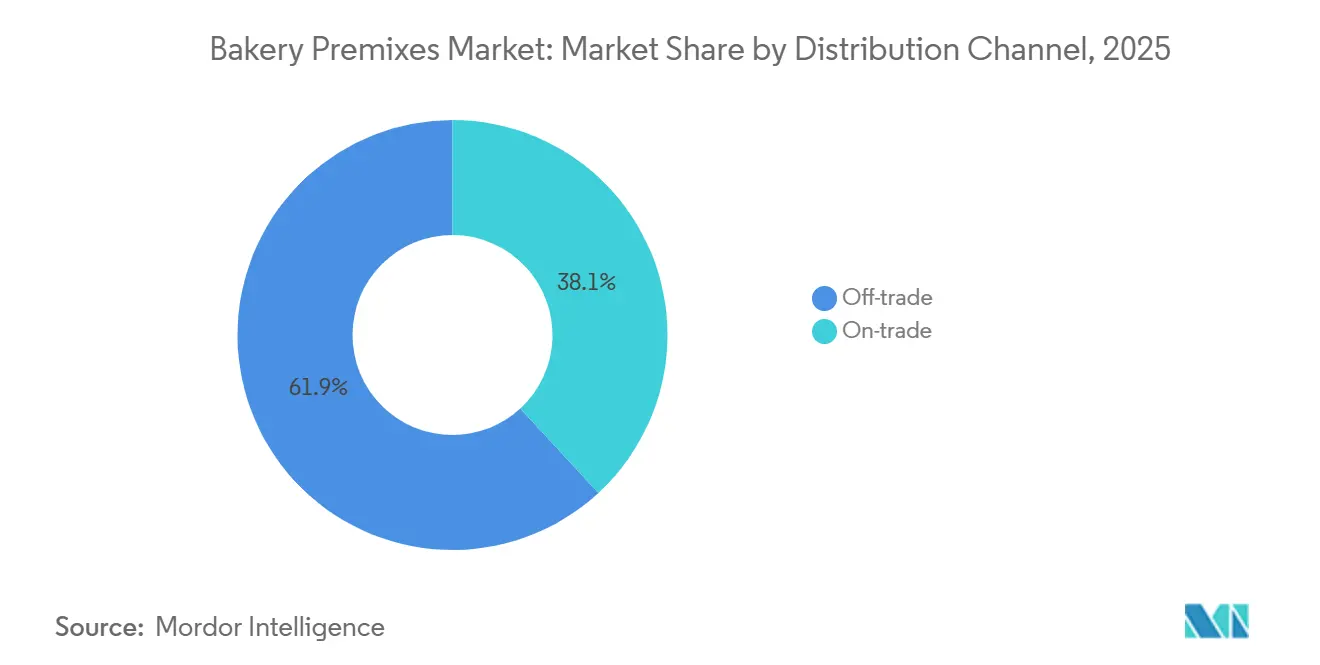

- By distribution channel, off-trade held 61.87% of 2025 sales, yet on-trade is the fastest-rising route with an 8.24% CAGR forecast.

- By geography, Europe captured 34.57% share in 2025, and Asia-Pacific is expected to grow the quickest at an 8.13% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bakery Premixes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenience foods streamlines bakery operations | +1.3% | Global, with acceleration in Asia-Pacific urban centers and North America QSR chains | Medium term (2-4 years) |

| Home baking surge, amplified by social media and post-pandemic habits | +0.9% | North America, Europe, Australia; spillover to urban Latin America | Short term (≤ 2 years) |

| Innovation in flavors, textures, and product varieties | +1.1% | Global, led by Europe and North America; rapid adoption in Asia-Pacific premium segments | Medium term (2-4 years) |

| Technological advancements in food processing | +0.8% | North America, Europe, Japan; diffusion to China and India manufacturing hubs | Long term (≥ 4 years) |

| Preference for consistency and product standardization | +1.0% | Global, especially QSR and hotel chains in Asia-Pacific, Middle East, and Latin America | Medium term (2-4 years) |

| Foodservice expansion drives bulk premix adoption | +1.4% | Asia-Pacific (Thailand, Indonesia, India), Middle East (Saudi Arabia), Sub-Saharan Africa (Nigeria) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenience foods streamlines bakery operations

Urbanization and the increasing prevalence of dual-income households are significantly reducing the time available for meal preparation. In 2024, the United States Bureau of Labor Statistics reported that 49.6% of married couples in the United States had both spouses employed, highlighting the growing need for convenient food solutions[1]Source: United States Bureau of Labor Statistics, "TED: The Economics Daily image", bls.gov. Additionally, the Population Reference Bureau projected that by 2025, 53% of Asia's population would reside in urban areas, with the Asia-Pacific region experiencing the most pronounced urbanization trends[2]Source: Population Reference Bureau, "World Population Data Sheet", prb.org. This trend is prompting bakeries and foodservice operators to increasingly adopt premixes, which streamline ingredient handling processes and reduce dependency on labor. In Nigeria, the quick-service restaurant sector is expanding at a rapid pace, signaling a strong demand for locally produced premixes. These premixes not only have the potential to replace imports but also offer an opportunity to capture higher profit margins by catering to localized preferences. Furthermore, advancements in automation, driven by Industry 4.0 technologies such as sensors and recipe-management software, are further accelerating the adoption of premixes. These technologies enable bakeries to automate mixing and portioning processes, achieving batch variances of less than 1% while eliminating the need for skilled labor. This combination of convenience, efficiency, and precision is making premixes an increasingly attractive solution for the evolving foodservice industry.

Home baking surge, amplified by social media and post-pandemic habits

Although the home-baking trend that gained momentum during the pandemic has slowed, it has not disappeared entirely. Instead, it has evolved into two primary segments: a committed group of regular hobbyists who bake frequently and a larger segment of occasional bakers who prefer the convenience of premixes. These premixes allow them to achieve bakery-quality results without requiring advanced baking skills. Social media platforms, particularly Instagram and TikTok, have played a pivotal role in reshaping the baking landscape. Viral recipes on these platforms often feature specific branded premixes, ensuring followers can replicate the results successfully. This approach has effectively transformed influencer reach into measurable retail sales growth. For premix manufacturers, this trend highlights a critical opportunity: to maintain and expand household penetration, retail brands must prioritize investments in digital recipe ecosystems and establish strategic partnerships with influencers. These efforts are essential as the initial enthusiasm for home baking transitions into a more normalized, routine activity.

Innovation in flavors, textures, and product varieties

Flavor innovation is no longer limited to sweet applications. Savory premixes, incorporating umami enhancers, fermented ingredients, and global spice profiles, are becoming increasingly popular in markets where bakery products are consumed as meal components rather than desserts. Pulse-based premixes made from lentil and chickpea flours provide dual benefits: increasing protein content and lowering the glycemic index. These features support claims of reduced sugar and fat, aligning with the EU's regulatory nutrition-labeling requirements and Latin America's voluntary front-of-pack initiatives. In 2024, the EU approved insect powder (Alphitobius diaperinus) for human consumption, driving the development of niche premixes for high-protein, sustainable bakery formats. However, commercial scaling remains limited to specialty channels. Fiber systems such as Nutriose and PromOat are being incorporated into reformulation platforms, enabling bakers to reduce sugar and fat by up to 30% without compromising mouthfeel. These capabilities are becoming essential as governments enforce stricter added-sugar thresholds.

Technological advancements in food processing

Ohmic heating, which uses electrical current to directly heat food matrices for a rapid and uniform temperature increase, is being tested in premix production. This method aims to minimize the thermal degradation of heat-sensitive vitamins and enzymes, thereby extending their functional shelf life and supporting clean-label enzyme declarations. In January 2026, Archer Daniels Midland allocated USD 26 million to expand its innovation facility in Erlanger, Kentucky, by 40%. This expansion incorporates digitalization, automation, and integrated processing capabilities to meet the growing demand for reformulation. This investment highlights the recognition among major ingredient players that premix customization represents a significant growth opportunity. Blockchain-enabled traceability is being integrated into premix supply chains to meet retailer requirements for ingredient provenance, particularly for organic and non-GMO claims. At the same time, IoT sensors are actively monitoring humidity and temperature in bulk premix storage to prevent clumping and microbial growth. Nisshin Seifun's efforts at its Mizushima plant exemplify the industry's digital transformation. By combining automation with real-time quality analytics, the company demonstrates how digitalization can reduce labor costs and batch variance, making premix production cost-effective even for smaller lot sizes.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High raw material price volatility | -0.7% | Global, acute in import-dependent regions (Middle East, Sub-Saharan Africa, Southeast Asia) | Short term (≤ 2 years) |

| Additive and preservative concerns | -0.5% | North America, Europe, Australia; emerging in urban Asia-Pacific | Medium term (2-4 years) |

| Regulatory and certification complexity | -0.4% | Global, highest friction in cross-border trade (EU-Asia, US-Latin America) | Long term (≥ 4 years) |

| Shelf life and storage constraints | -0.3% | Tropical and subtropical regions (Southeast Asia, Sub-Saharan Africa, Latin America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High raw material price volatility

During 2024-2025, wheat, dairy, and vegetable oil prices experienced significant volatility due to adverse weather in the Black Sea and North American growing regions, export restrictions by India and Indonesia, and speculative activity in commodity futures markets. Although the company operates grain elevators and manages a wheat merchandising business to limit spot-market exposure, mark-to-market volatility on commodity derivatives continues to impact segment profitability. This highlights that even vertically integrated players cannot fully protect premix pricing from upstream disruptions. In the same period, molasses, a key input for yeast production, faced supply shortages. This affected Nisshin Seifun's yeast operations and increased input costs for premixes containing yeast and flour. Premix suppliers without hedging mechanisms or long-term supply agreements are vulnerable to margin erosion when input costs rise faster than they can renegotiate customer pricing, a challenge that disproportionately impacts smaller regional players lacking procurement scale.

Additive and preservative concerns

Clean-label activism has transitioned from niche organic outlets to mainstream retail, with consumers paying closer attention to ingredient lists for synthetic emulsifiers, artificial colors, and chemical preservatives. Data from the UK Food and Drink Federation in Q2 2025 showed that 84% of food manufacturers are prioritizing reformulation efforts. This shift is primarily driven by regulatory requirements, such as the Extended Producer Responsibility costs, totaling GBP 1.1 billion (USD 1.4 billion), and increasing consumer demands for transparency. In Argentina, AB Mauri, a division of Associated British Foods, introduced its INNOVA 360° BIENESTAR premix range. This range features a 25% reduction in sodium, is free from preservatives and artificial colors, and is high in fiber. Achieving these characteristics required a multi-year research and development investment in enzyme systems and natural antioxidants to ensure shelf stability. The reformulation trend has created a divided market: larger suppliers with dedicated research and development centers can manage the costs of clean-label development and transfer them to premium-tier customers. Meanwhile, smaller premix manufacturers are either exiting the market or focusing on more price-sensitive conventional segments Certification requirements add another layer of complexity. Claims such as organic, non-GMO, and Halal necessitate separate audits and documentation, increasing fixed costs and delaying the time-to-market for new SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Muffin Formats Capture Breakfast Daypart

In 2025, bread and roll premixes accounted for 31.12% of the market share, driven by industrial bakeries prioritizing labor cost optimization and supply chain efficiency over artisanal differentiation. Cake and pastry premixes serve both retail bakeries and foodservice operators, with formulations increasingly focusing on reduced-sugar and gluten-free variants as Europe enforces stricter nutrition labeling regulations and Latin America adopts more voluntary front-of-pack schemes. Cookie and biscuit premixes benefit from advancements in texture engineering, such as the use of pulse-based flours like lentil and chickpea, which enhance protein content and support low glycemic index positioning. However, commercial production remains concentrated in specialty channels, awaiting broader consumer acceptance. The "others" segment includes niche applications like donut mixes, waffle batters, and savory bakery formats, where regional flavor preferences drive the expansion of localized SKUs.

Between 2026 and 2031, muffin and pancake premixes are projected to grow at a 7.88% CAGR, supported by the increasing popularity of breakfast-on-the-go in urban areas and the standardization of portion sizes in hotel chains and quick-service restaurants. DreamPak's ready-to-cook pancake batter, which offers extended shelf life and does not require refrigeration, exemplifies how packaging innovations can address distribution challenges in regions with limited cold-chain infrastructure, such as Southeast Asia and Sub-Saharan Africa. General Mills' fiscal 2025 results revealed a slight decline in net sales for baking mixes and ingredients, totaling USD 1.94 billion, while its North America Foodservice segment grew by 2%, indicating that rising demand for bulk premixes from commercial operators is offsetting retail market challenges. Muffin premixes, in particular, are being reformulated with high-fiber flours like Nisshin Seifun's Amuleia and Wise Wheat, enabling health claims that appeal to institutional buyers aiming to meet voluntary nutrition standards.

By Category: Specialty Premixes Gain Traction Amid Reformulation Mandates

In 2025, conventional premixes accounted for 76.27% of the market share. This stronghold stems from established distribution networks, cost sensitivity among smaller bakeries, and the difficulties of switching suppliers, particularly in markets where technical support and credit terms are as important as ingredient pricing. These conventional formulations perform well in cost-competitive retail channels and regions with voluntary regulatory nutrition labeling, enabling manufacturers to delay expensive reformulation efforts. However, rising raw material costs and the growing presence of retailer private-label products are pressuring conventional premix suppliers. To maintain their market position, they are either consolidating or adopting automation. For example, Nisshin Seifun has implemented smart-factory initiatives to lower labor expenses and reduce batch inconsistencies.

Specialty premixes, including organic, gluten-free, high-fiber, and clean-label varieties, are expected to grow at a 7.69% CAGR from 2026 to 2031. This growth is driven by regulatory requirements, increasing consumer demand for transparency, and the premiumization of bakery products in developed markets. Although gluten-free premixes currently represent a smaller portion of the total volume, they are expanding rapidly in North America and Europe. In these regions, greater awareness of celiac disease and gluten sensitivities has created a dedicated consumer base willing to pay a premium for certified formulations. Similarly, organic certification, despite its high maintenance costs, provides significant benefits. It ensures better shelf placement in natural retailers and allows for margin premiums, which help offset higher input costs, making it a viable option for larger suppliers.

By Distribution Channel: On-Trade Gains as Foodservice Consolidates

In 2025, off-trade channels, which include supermarkets, hypermarkets, convenience stores, and online retail, accounted for 61.87% of the market share. Supermarkets and hypermarkets, the dominant sub-channels, leverage shelf-space control and private-label programs to optimize margins from branded premix suppliers. Convenience stores focus on impulse purchases and smaller pack sizes, which yield higher per-unit prices. Although online retail constitutes a smaller share of the total premix volume, it is growing rapidly. E-commerce platforms in China, India, and Southeast Asia are driving this growth by offering subscription models and recipe-bundling, ensuring repeat purchases. This trend is further supported by increasing internet penetration. According to the International Telecommunication Union (ITU), approximately 6 billion people, or about three-quarters of the global population, were internet users in 2025[3]Source: International Telecommunication Union (ITU), "ITU's Facts and Figures 2025", itu.int. Off-trade distribution prioritizes conventional premixes with long shelf lives and ambient storage, as retailers emphasize inventory turnover over product differentiation.

Between 2026 and 2031, on-trade distribution is expected to grow at a CAGR of 8.24%. This expansion is driven by the recovery of foodservice in emerging markets and the consolidation of supplier rosters by QSR chains and hotel groups. These groups increasingly require bulk packaging, extended payment terms, and technical support. In Thailand, the hotel-restaurant-institutional sector experienced growth, with pancake mixes identified as a significant volume driver. Additionally, QSR operators, accounting for 17% of the HRI market, are standardizing premix specifications to ensure consistency across their multiple locations. On-trade growth is also evident in the Middle East, supported by tourism, a growing expatriate population, and government investments in hospitality infrastructure. For premix suppliers, the strategic takeaway is clear: on-trade clients prioritize consistency, technical support, and flexible packaging over unit pricing. This creates opportunities for suppliers with specialized foodservice sales teams and co-packing capabilities to secure premium market positioning.

Geography Analysis

In 2025, Europe accounted for 34.57% of the market share, supported by its well-established bakery infrastructure, high per-capita consumption of bread and pastries, and regulatory policies promoting clean-label reformulation. A BDO survey revealed that 95% of UK food manufacturers have a positive outlook, with 90% prioritizing new product development. Significant bakery M and A activities, such as Village Bakery's GBP 160 million (USD 202 million) and Finsbury's GBP 143 million (USD 181 million) deals, highlight a consolidation trend that benefits premix suppliers with scale and technical service capabilities. Germany, France, Italy, and Spain, known for their artisanal bakery traditions, are increasingly adopting premixes to address labor shortages and rising wage costs. On the other hand, while Russia and Eastern Europe offer growth opportunities, geopolitical tensions and currency volatility hinder investments.

Asia-Pacific is projected to grow at a CAGR of 8.13% from 2026 to 2031, driven by urbanization, a growing middle class, the expansion of quick-service restaurants (QSRs), and premix formulations customized to regional preferences. Nisshin Seifun Group, which holds 59.5% of Japan's household tempura-mix market and 56.9% of the karaage deep-fry mix market, is expanding its commercial premix capacity in Vietnam and across the ASEAN region. By leveraging vertical integration, covering flour milling, yeast production, and premix research and development, and its technical service platforms, the company is creating switching costs to capture increasing foodservice demand. In China and India, urban millennials and Gen Z are driving bread consumption as they increasingly view bakery products as convenient breakfast and snack options. Meanwhile, countries such as Indonesia, South Korea, Australia, and New Zealand are contributing to incremental growth, with Australia's Wise Wheat high-fiber flour exemplifying how regional ingredient innovations can differentiate premix offerings.

North America, comprising the U.S., Canada, and Mexico, remains a mature market characterized by high branded premix penetration, intense competition from retailer private labels, and margin pressures due to rising input costs. Archer Daniels Midland's USD 26 million investment in its Erlanger, Kentucky, innovation facility in January 2026 increased raw-material handling capacity by 40% and integrated digitalization for reformulation support. This move underscores a strategic shift toward specialty premixes and clean-label solutions that command premium pricing. In South America, Brazil, Argentina, Colombia, and Chile lead the market, but growth remains volatile due to currency instability and trade policy changes. The Middle East and Africa, including the UAE, Saudi Arabia, Egypt, Nigeria, and Turkey, are emerging as high-growth regions. Investments by Saudi Arabia's food processing firms in food infrastructure reflect the government's focus on food security and reducing imports, creating opportunities for premix suppliers willing to establish local production or joint ventures.

Competitive Landscape

The Global Bakery Premixes Market demonstrates moderate to high competition, characterized by a fragmented structure where global ingredient conglomerates compete with regional specialists and vertically integrated flour millers. Market concentration is higher in developed regions (North America, Europe, Japan), where economies of scale in research and development, distribution, and quality assurance benefit established players. However, in emerging markets, the market remains fragmented due to localized taste preferences, distribution challenges, and flexible credit terms that allow smaller players to maintain their market share.

Strategic approaches focus on vertical integration, technical service platforms, and reformulation capabilities. For instance, Nisshin Seifun Group integrates flour milling, yeast production, and premix research and development to create switching costs, protecting itself from price-based competition. Similarly, Associated British Foods' AB Mauri division operates a global network of technology centers and food scientists. Its INNOVA 360° BIENESTAR premix range in Argentina, developed through multi-year research and development efforts on enzyme systems and natural antioxidants, achieves a 25% sodium reduction and clean-label positioning.

White-space opportunities are evident in on-trade foodservice channels in emerging markets (Thailand, Nigeria, UAE, Egypt), where QSR penetration is growing, but local premix supply remains underdeveloped. This creates opportunities for suppliers offering bulk packaging, extended shelf life, and technical support. Emerging disruptors include niche organic and gluten-free specialists leveraging e-commerce platforms and direct-to-consumer models to bypass traditional distribution barriers, though their scale remains limited. Technology adoption, such as automation, digitalization, and blockchain traceability, is becoming a key differentiator. For example, Archer Daniels Midland's USD 26 million Erlanger expansion in January 2026 incorporated digitalization and automation to meet reformulation demand and accelerate time-to-market for custom premix formulations.

Bakery Premixes Industry Leaders

-

Puratos Group

-

Archer Daniels Midland Company (ADM)

-

Lesaffre

-

Bakels Group

-

Cargill, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AWL Agri Business has expanded its product line with the launch of its new Fortune Cake Premix for professional bakers. According to the brand, the new Cake Premix will be available in three variants: Classic Vanilla, Premium Vanilla, and Premium Chocolate.

- March 2025: Krusteaz has launched its new Cheesecake Muffin Mix, which combines the moistness of a muffin with a creamy cheesecake-flavored center. According to the brand, the new mix is designed for easy, at-home baking, requiring minimal added ingredients while delivering a rich, dessert-like experience.

- January 2025: D’aromas has introduced a new Jaggery Cookie Premix, bringing the traditional sweetness and warmth of jaggery into modern kitchens across India. According to the brand, the product comes with pre-measured ingredients, ensuring quick and hassle-free baking for everyone from beginners to seasoned bakers, and is available in 500g packs, as well as 1kg, 3kg, and 5kg bulk sizes for larger needs.

- March 2024: Pillsbury Baking has introduced its Creamy Cake Mix Line featuring two flavors: Moist Supreme Creamy Almond Cake Mix and Moist Supreme Creamy Vanilla Cake Mix. According to the brand, these mixes are crafted to deliver rich, subtly fruity, and velvety cake experiences for both home bakers and professionals.

Global Bakery Premixes Market Report Scope

Baked goods premixes are pre-prepared blends of dry ingredients designed specifically for baking. The global bakery premixes market is segmented by product type, category, distribution channel, and geography. By product type, the market is segmented into bread and roll premixes, cake and pastry premixes, cookie and biscuit premixes, muffin and pancake premixes, and others. By category, the market is segmented into conventional and specialty premixes. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. The market forecasts are provided in terms of value (USD) and volume (Tons) for all the segments above.

| Bread and Roll Premixes |

| Cake and Pastry Premixes |

| Cookie and Biscuit Premixes |

| Muffin and Pancake Premixes |

| Others |

| Coventional |

| Specialty Premixes |

| On-trade | |

| Off-trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online retail stores | |

| Other distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Bread and Roll Premixes | |

| Cake and Pastry Premixes | ||

| Cookie and Biscuit Premixes | ||

| Muffin and Pancake Premixes | ||

| Others | ||

| By Category | Coventional | |

| Specialty Premixes | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online retail stores | ||

| Other distribution channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the bakery premixes market by 2031?

The market is forecast to reach USD 2.47 billion by 2031, growing at 7.26% CAGR from 2026.

Which region will grow the fastest through 2031?

Asia-Pacific is set to record an 8.13% CAGR, the highest among all regions.

Which product segment led sales in 2025?

Bread and roll mixes held 31.12% share, the largest in 2025.

Why are specialty premixes gaining momentum?

Regulatory reformulation mandates and consumer demand for clean labels drive specialty blends, which are forecast to rise at a 7.69% CAGR.

Page last updated on: