Fresh Vegetables Market Size and Share

Fresh Vegetables Market Analysis by Mordor Intelligence

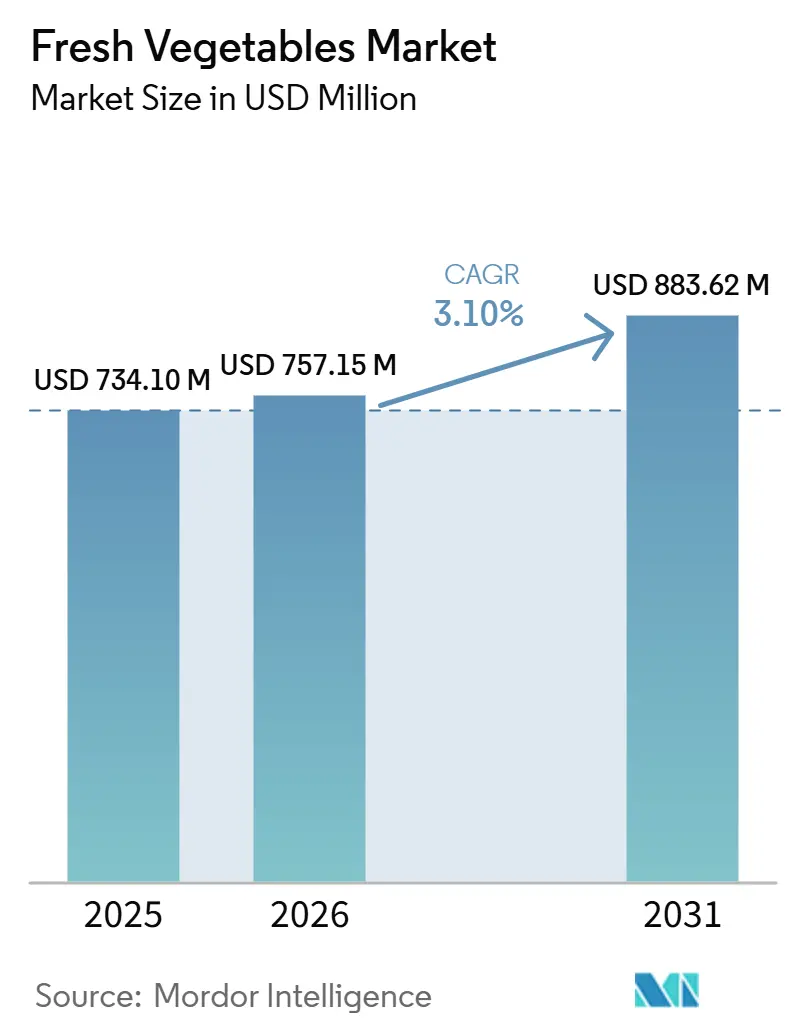

The fresh vegetables market size is forecasted to grow from USD 734.0 billion in 2025 to USD 757.15 billion in 2026 and is projected to reach USD 883.62 billion by 2031, with a CAGR of 3.10% during the period 2026 to 2031. According to the OECD-FAO outlook, global fresh vegetable production is anticipated to reach 1,204 million metric tons by 2033, reflecting consistent moderate growth. The fresh vegetables market is driven by rising health-conscious consumption, government initiatives focused on nutrition and food security, and increased investment in cold chain infrastructure along major trade routes. Demand is also becoming more resilient as vegetables are increasingly regarded as an essential component of daily diets in economies undergoing nutritional transition. However, the market continues to face challenges from post-harvest losses, fertilizer prices that increased by 10% to USD 336 per metric ton in 2024, water stress in major producing regions, and persistent productivity gaps between technology-enabled farming systems and traditional growing belts.

Key Report Takeaways

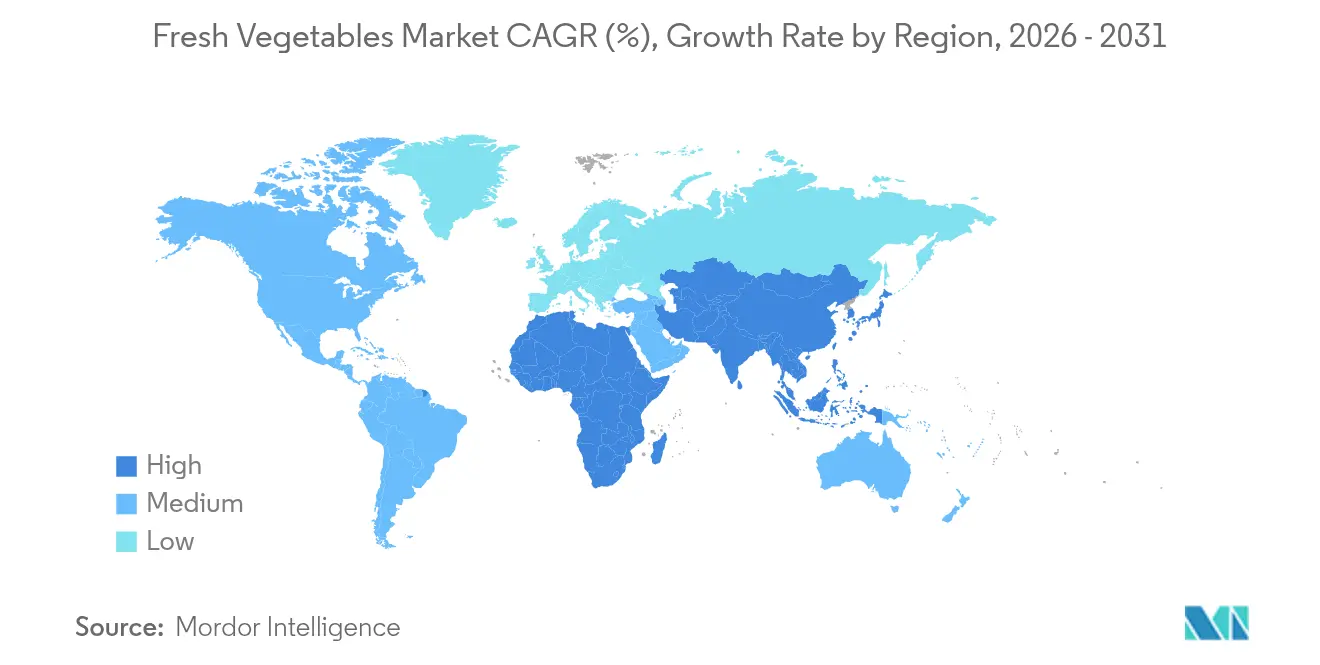

- By geography, Asia-Pacific is the largest region, accounting for 45.6% of the fresh vegetables market share in 2025, while Africa is projected to be the fastest-growing region, with a 5.1% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fresh Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and dietary shift toward nutrient-dense foods | +0.8% | Global, strongest in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Urbanization and expanding middle-class demand in emerging economies | +0.7% | Asia-Pacific core, Africa, and the Middle East | Long term (≥ 4 years) |

| Cold chain infrastructure investment and e-commerce channel growth | +0.5% | North America and Europe, expanding into the Asia-Pacific and Africa | Medium term (2-4 years) |

| Government subsidies and national food security programs | +0.4% | Global, concentrated in North America, India, and South Africa | Short term (≤ 2 years) |

| Precision agriculture and controlled environment agriculture technologies | +0.3% | North America, Europe, the Middle East, and high-tech Asia-Pacific markets | Long term (≥ 4 years) |

| Food service sector growth and institutional procurement | +0.3% | Global, urban-concentrated across all regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health Consciousness and Dietary Shift Toward Nutrient-Dense Foods

Increasing health awareness and a dietary shift toward nutrient-rich foods are key drivers of the fresh vegetable market's growth. Consumers are placing greater emphasis on balanced diets that include vitamins, minerals, fiber, and antioxidants, resulting in higher demand for fresh vegetables as vital components of daily nutrition. In the fresh vegetables market, dietary guidance is influencing commercial demand more directly than it did in the past. The 2020-2025 Dietary Guidelines for Americans stated that average United States vegetable intake reached only 70% of recommended levels, which kept policy attention on access to produce and the quality of intake. The United States Department of Agriculture (USDA) expanded support through the Marketing Assistance for Specialty Crops program and increased total funding to USD 650 million in January 2025, following strong producer demand[1]Source: United States Department of Agriculture, “USDA Expands Marketing Assistance for Specialty Crops to USD 650 Million,” usda.gov.

Urbanization and Expanding Middle-Class Demand in Emerging Economies

The fresh vegetables market in emerging economies is being reshaped by rapid urbanization, expanding middle-class populations, and rising food spending. The OECD-FAO Agricultural Outlook 2025–2034 projects that Africa’s per capita root vegetable consumption will increase from 43 kg to 48 kg per year by 2034. India’s Union Budget 2025 introduced the Comprehensive Vegetable Program, reflecting a policy shift toward improving vegetable supply chains alongside farm production. As urban populations grow, consumers have greater access to organized retail, supermarkets, and online grocery platforms offering a wider variety of fresh vegetables year-round. In countries such as India, China, Brazil, and Indonesia, changing dietary preferences and increasing awareness of nutrition are further driving demand for fresh, organic, and nutrient-rich vegetables.

Cold Chain Infrastructure Investment and E-Commerce Channel Growth

Investments in cold chain infrastructure and the growth of e-commerce channels are significantly driving the fresh vegetable market. Enhanced cold storage facilities, refrigerated transportation, and efficient logistics systems ensure the freshness, quality, and extended shelf life of vegetables across the supply chain. In 2024, the Philippines committed PHP 3 billion (USD 51.4 million) for 99 hybrid cold storage facilities to reduce crop losses. These advancements help reduce post-harvest losses and support year-round availability. Simultaneously, the expansion of online grocery platforms and digital delivery services has improved accessibility and convenience for consumers, particularly in urban areas. E-commerce channels provide advantages such as doorstep delivery, a broader product range, competitive pricing, and easy comparison of fresh and organic produce, encouraging increased consumer spending on vegetables.

Precision Agriculture and Controlled Environment Agriculture Technologies

Precision agriculture and controlled environment agriculture technologies are driving growth in the fresh vegetable market by enhancing productivity, crop quality, and resource efficiency. Precision farming methods, such as IoT sensors, GPS-guided equipment, drones, and data analytics, enable real-time monitoring of soil conditions, irrigation, nutrient levels, and crop health. This leads to optimized yields and reduced waste. Similarly, controlled environment agriculture techniques, including hydroponics, vertical farming, and greenhouse cultivation, facilitate vegetable production under highly regulated conditions, minimizing reliance on climate and seasonal factors. Qatar reported a 98% increase in domestic fresh vegetable production over a 5-year period as of 2024 after government-backed investment in controlled environment agriculture. In July 2024, Plenty Unlimited and Mawarid Holding Investment launched a joint venture worth over AED 500 million (USD 130 million) to build an indoor vertical farm in AbuDhabi.These approaches enable year-round production, conserve water and land resources, reduce pesticide usage, and ensure a consistent supply of high-quality fresh vegetables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High post-harvest losses across low- and middle-income supply chains | -0.6% | Africa, South Asia, Southeast Asia, and South America | Short term (≤ 2 years) |

| Water scarcity and climate-driven agricultural stress | -0.4% | Mediterranean, Sub-Saharan Africa, South Asia, and western North America | Long term (≥ 4 years) |

| Fertilizer price volatility and elevated input costs compressing producer margins | -0.3% | Global, with the highest exposure in import-dependent developing economies | Short term (≤ 2 years) |

| Stringent food safety regulations and non-tariff barriers limiting cross-border market access | -0.3% | European Union import markets, North America, and East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Post-Harvest Losses Across Low- and Middle-Income Supply Chains

In the fresh vegetables market, post-harvest loss remains one of the biggest supply constraints because it removes sellable volume before trade and retail data capture it. According to FAOSTAT, globally, vegetables account for the highest losses, 25.4% in 2023, due to their high perishability and handling requirements[2]Source: Food and Agriculture Organization, “Global Food Losses by Commodity 2023,” FAOSTAT, fao.org. High post-harvest losses in supply chains across low- and middle-income countries significantly impact the fresh vegetable market. These losses reduce the quantity of produce available to consumers, drive up prices, and decrease farmers' incomes. A substantial portion of vegetables is lost after harvesting due to poor handling practices, insufficient storage facilities, inadequate transportation systems, limited cold-chain infrastructure, and damage caused by pests or microbes. Given the perishable nature of fresh vegetables, these inefficiencies result in spoilage before the products reach the market.

Water Scarcity and Climate-Driven Agricultural Stress

Water stress is a structural restraint on the fresh vegetables market because vegetables depend heavily on reliable irrigation and stable growing conditions. The World Resources Institute reported in October 2024 that one-quarter of the world’s crops are grown in areas of high water stress, and that vegetables are concentrated in many of those zones. This pressure is already changing trade competitiveness, as exporters with better drip irrigation and desalination investments can expand more reliably than water-stressed rivals. Water deficits significantly affect the growth of fresh vegetables, leading to reduced leaf expansion, smaller vegetable size, and lower overall quality. This results in decreased marketable yield and reduced consumer acceptance. In many regions, drought conditions also elevate production costs, as farmers need to invest in irrigation systems or adopt less water-efficient practices, further increasing prices across the supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Asia-Pacific is the largest region, accounting for 45.6% of the fresh vegetables market share in 2025, supported by high vegetable consumption in countries such as China and India, where vegetables are dietary staples in daily meals, which increases fresh vegetable production. According to FAOSTAT, China produced 603.6 million metric tons in 2024, and India produced 146.0 million metric tons, keeping the region far ahead of other production clusters[3]Source: Food and Agriculture Organization, “Crops and Livestock Products – Vegetables 2024,” FAOSTAT, fao.org. Rapid urbanization, rising middle-class income, and expanding modern retail channels are boosting demand for fresh, packaged, and hygienically handled produce. High-growth products include leafy greens (lettuce, spinach), fruiting vegetables (tomatoes, cucumbers, peppers), and convenience-oriented items like pre-cut and ready-to-cook vegetables. The region is also seeing strong adoption of greenhouse farming and digital grocery platforms to meet year-round demand.

Africa is projected to be the fastest-growing region, with a 5.1% CAGR through 2026 to 2031, the market is experiencing the fastest growth driven by rising population, urban migration, and increased awareness of nutrition. Demand for affordable vegetables, such as onions, tomatoes, leafy greens, and root crops, is expanding, especially in urban centers. Supply chains remain constrained by limited cold storage and logistics infrastructure, creating significant investment opportunities in post-harvest handling and distribution systems. Despite these challenges, increased retail modernization and scaling of local production are supporting steady market expansion.

In North America, the market is highly developed and driven by strong consumer preference for organic, locally sourced, and convenience-oriented fresh vegetables. Demand is particularly high for salad vegetables, leafy greens, tomatoes, cucumbers, carrots, and snack-sized vegetable packs. The growth of e-grocery platforms, meal kits, and farm-to-table trends is further strengthening consumption patterns. The region is also increasingly focused on sustainability, traceability, and controlled-environment agriculture (such as vertical farming) to ensure year-round supply and quality consistency.

Competitive Landscape

The global fresh vegetables market remains fragmented, with thousands of regional growers, cooperatives, and national distributors rather than a small group of dominant firms. Greenyard, Fresh Del Monte Produce, and Grimmway Produce Group compete mainly through logistics reach, grower networks, and retailer relationships instead of pure product differentiation. This structure keeps concentration low at the farm level, but it creates stronger scale advantages in distribution, packing, and cross-border handling. Greenyard’s 2025 delisting and the later majority investment from Solum Partners showed that private capital is moving into the sector to support longer-horizon supply chain upgrades. That change is consistent with a fresh vegetables market where ownership is spreading across capital providers even as operational scale becomes more important.

Technology is becoming the clearest dividing line inside the fresh vegetables market, especially for leafy greens, vine tomatoes, and other fast-turn categories. Controlled environment agriculture operators such as NatureSweet, BrightFarms, and Nature Fresh Farms are using greenhouse scale and year-round consistency to challenge field-grown supply in North America. BrightFarms began shipping from its 1.5 million-square-foot greenhouse in Macon, Georgia, in March 2025, expanding its reach across a large share of the United States consumer base.

Brand integration is also becoming more relevant in the fresh vegetables market. Fresh Del Monte Produce completed the acquisition of select Del Monte Foods assets for USD 285 million in March 2026, which reunited the Del Monte brand under one owner for the first time in nearly 4 decades. The fresh vegetables market still leaves large openings in Sub-Saharan African cold chain logistics, digital traceability, and premium low-residue export supply, but access to those spaces will increasingly favor operators with stronger capital, certification, and systems.

Recent Industry Developments

- June 2025: Cooperation Green 2000 launched Senegal's Community Agricultural Estates Program (PRODAC), supporting greenhouse development across Africa through multilateral financing. The initiative boosts the fresh vegetables market by enabling year-round production and increasing the supply of high-quality produce.

- February 2025: India's Union Budget 2025 introduced the Comprehensive Programme for Vegetables to support farmers and consumers. The initiative promotes increased vegetable and Shree-Anna (nutri-cereal) consumption in line with growing awareness of healthy diets and rising incomes.

- February 2024: NatureSweet invested USD 5 million in a new greenhouse in Arizona, United States, for producing premium tomatoes and peppers, demonstrating the growing demand for high-quality fresh vegetables in the market.

Global Fresh Vegetables Market Report Scope

Fresh vegetables are edible plant parts harvested in their natural state, characterized by high water content, natural taste, and a rich nutrient profile. The Fresh Vegetables Market Report is segmented by geography into North America, Europe, Asia-Pacific, the Middle East, and Africa. It includes analyses of production (volume), consumption (value and volume), imports (value and volume), exports (value and volume), wholesale price trends and forecasts, the regulatory framework, logistics and infrastructure, seasonality, and profiles of key market players. The market forecasts are provided in terms of value (USD) and volume (metric tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistic and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Oman | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistic and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Oman | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | Kenya | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

Which region leads to global demand for fresh vegetables?

Asia-Pacific leads with 45.6% of global value in 2025, supported by very large production in China and India and high domestic consumption.

Which region is growing the fastest through 2031?

Africa is the fastest-growing region with a projected 5.1% CAGR through 2026 to 2031, driven by urbanization, population growth, and rising investment in cold chain and export capacity.

What is the main demand driver behind higher vegetable consumption?

Health-oriented eating patterns are a major driver, reinforced by government support programs and stronger clinical interest in vegetable-rich diets.

What are the biggest supply risks affecting growers and distributors?

The main risks are post-harvest losses, water scarcity, volatility in fertilizer costs, and tougher food safety compliance requirements in export markets.

Page last updated on: