Fresh Berries Market Size and Share

Fresh Berries Market Analysis by Mordor Intelligence

fresh berries market size in 2026 is estimated at USD 36.73 billion, growing from 2025 value of USD 35.24 billion with 2031 projections showing USD 45.14 billion, growing at 4.22% CAGR over 2026-2031. Steady gains arise from health-driven diets, rapid Adoption of protected cultivation systems, and wider global supply chains that guarantee year-round availability of premium fruit.[1]Source: U.S. Department of Agriculture, “U.S. Cranberries on the Up,” fas.usda.gov Growth is strengthened by berries overtaking all other organic fresh produce categories in U.S. retail, generating significant revenue in 2023. Technology-enabled yield gains, notably from proprietary cultivars, cut production risk while enhancing flavor consistency, and e-commerce adoption broadens consumer reach. Competitive dynamics reveal a dual structure in which grower cooperatives dominate individual berry types while capital-rich marketers expand through acquisitions and automation. Climate change remains a wildcard, but investment in protected tunnels, substrate systems, and shelf-life extension technology substantially offsets weather-driven volatility.

Key Report Takeaways

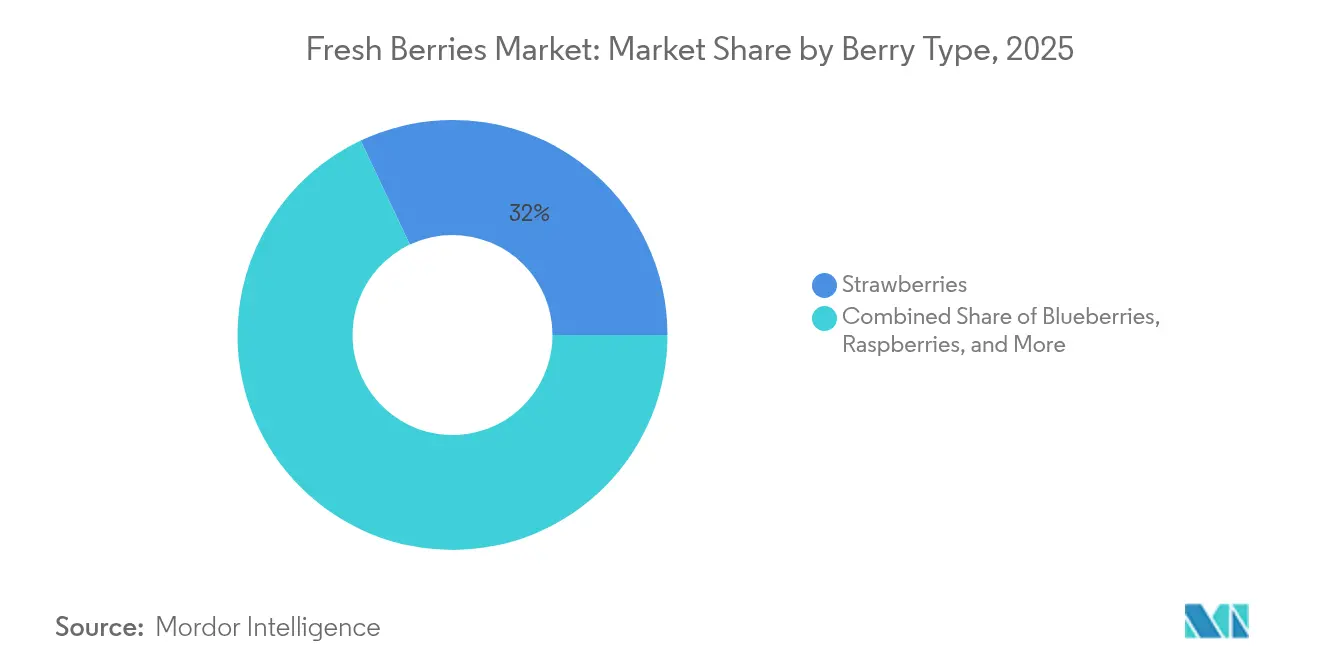

- By berry type, strawberries led with 32.02% of the fresh berries market share in 2025, and blueberries recorded the highest projected CAGR at 6.92% through 2031.

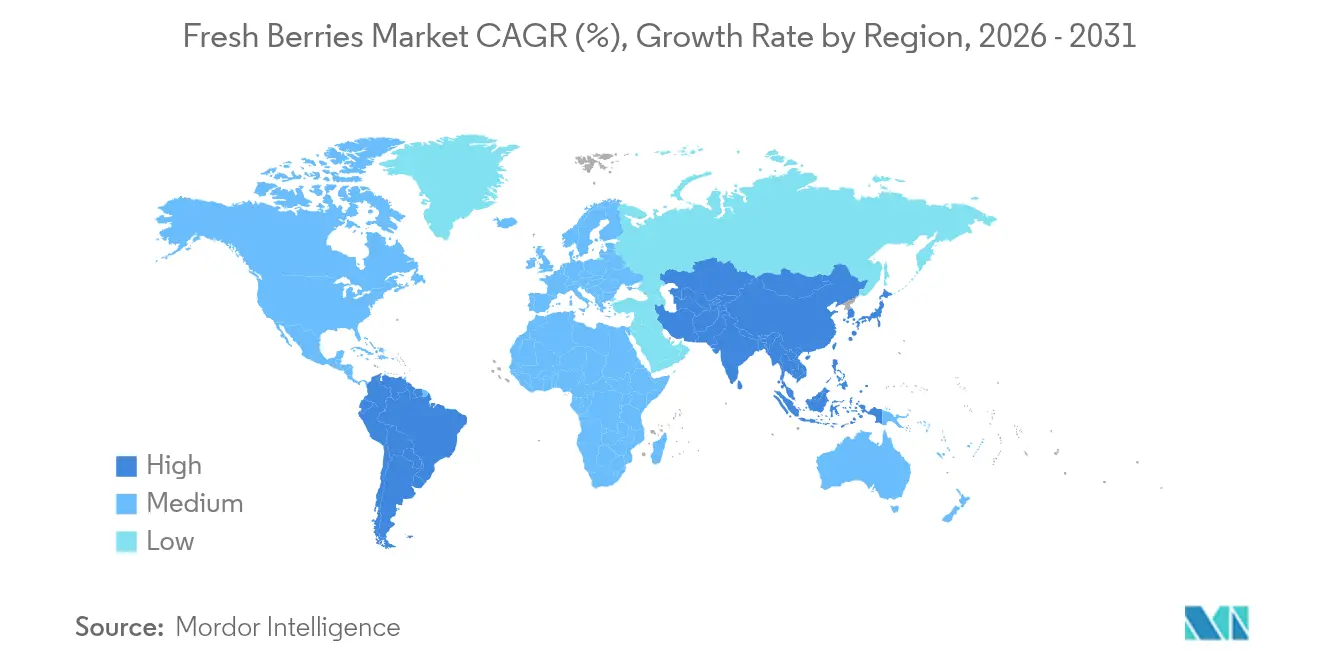

- By geography, North America held 31.12% of the fresh berries market size in 2025, and Asia-Pacific is forecast to expand at a 5.47% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fresh Berries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-centric diets fueling berry intake | +1.2% | North America and Europe | Medium term (2-4 years) |

| Demand from functional food and beverage launches | +0.8% | Global urban centers | Medium term (2-4 years) |

| Adoption of protected cultivation and high-density tunnels | +0.7% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Yield gains via proprietary cultivars and genetics | +0.6% | Global | Long term (≥ 4 years) |

| Advanced cold-chain logistics and modified-atmosphere packaging | +0.5% | Global, strongest in North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Premium pricing and margins for organic certification | +0.4% | North America, Europe, affluent Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health-centric diets fueling berry intake

Rising consumer focus on nutrient-dense foods positions berries as a cornerstone of preventive nutrition. Blueberries deliver the highest antioxidant density among common fruits, with anthocyanins linked to improved glycemic control and cardiovascular health. Millennials and Generation Z demonstrate the strongest preference, 33% of U.S. shoppers aged 18-29 purchase only organic strawberries, underscoring willingness to pay for perceived health benefits. Household penetration trails other fruit, so upside remains significant even in mature regions. Product developers respond by incorporating concentrates and powders into functional beverages, breakfast bars, and yogurts, expanding routes to market. The net result is a broad, price-resilient demand base that shields the fresh berries market from macroeconomic slowdowns.

Demand from functional food and beverage launches

Food and beverage manufacturers accelerate new concepts leveraging berries’ natural color and polyphenol content for specific health claims. High-pressure processing and gentle dehydration maintain bioactivity, allowing clean-label positioning without synthetic additives. Food manufacturers increasingly incorporate berries into products targeting metabolic health, with dried cranberries and berry-infused functional beverages capturing premium price points. The regulatory environment supports this trend, as berries generally receive favorable treatment under health claim regulations. The convergence of clean-label trends with functional nutrition creates sustained demand from food and beverage manufacturers.

Yield gains via proprietary cultivars and genetics

Breeding pipelines emphasize flavor, shelf life, and disease resistance without genetic modification. Driscoll’s patents multiple proprietary varieties, shielding margins, and curbing direct price competition. California Berry Cultivars introduced two new strawberries in 2025 that raise grower returns through higher sugar levels and firmer texture. Artificial intelligence accelerates selection cycles. USDA scientists deploy deep-learning tools to develop heat-resistant cranberry lines, cutting breeding timelines by 40%. Proprietary genetics thus serve as both a supply-chain stabilizer and brand-building asset in the fresh berries market.

Advanced cold-chain logistics and modified-atmosphere packaging

Investment in automated refrigerated warehouses, high-capacity tunnel freezers, and last-mile refrigerated vans reduces spoilage and widens export windows for fresh berries. Modified-atmosphere packaging (MAP) films extend shelf life by lowering oxygen and elevating carbon dioxide levels, slowing respiration and mold growth. In pilot programs, MAP punnets kept strawberries market-ready for 14 days versus 7 days in standard clamshells, enabling ocean freight substitution for air cargo and cutting logistics costs by 30%. North American operators added 300 million cubic feet of temperature-controlled storage space in 2024 alone, while European retailers moved to fully MAP-sealed berry packs across private-label lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile farm labor availability and rising wages | −1.1% | North America and Europe | Short term (≤ 2 years) |

| Climate-driven yield variability and extreme weather | −0.9% | Global | Medium term (2-4 years) |

| Inadequate cold chain in emerging consumer markets | −0.6% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Stricter phytosanitary and maximum-residue regulations | −0.4% | Global trade corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile farm labor availability and rising wages

The H-2A Temporary Agricultural Workers program certified 400,000 positions in fiscal 2024, yet average Adverse Effect Wage Rates climbed to USD 17.55 and surpassed USD 19 in high-cost states. Specialty crop operations now commit up to 40% of total expenses to labor, pressuring margins. Robots like Harvest CROO replace 25 pickers per machine, but capital outlays remain prohibitive for small farms. Labor uncertainty, therefore, tempers near-term expansion plans for the fresh berries market.

Stricter phytosanitary and maximum-residue regulations

The European Union caps thiacloprid residues at 0.01 mg/kg effective May 2025 and discontinues dimethomorph approval, forcing immediate practice changes. Australia classifies ready-to-eat berries as “risk food” from mid-2025, demanding Hazard Analysis and Critical Control Point (HACCP) certification for importers.[2]Source: Department of Agriculture, Fisheries and Forestry. "Berries that are ready-to-eat - DAFF," agriculture.gov.au Compliance costs disproportionally burden smaller exporters, potentially fast-tracking consolidation across the fresh berries market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Berry Type: Blueberries Drive Premium Growth

Strawberries captured 32.02% of the fresh berries market share in 2025, underpinned by stable global demand and year-round tunnel production. Blueberries exhibit a 6.92% CAGR, the highest within the fresh berries market size, as rising disposable incomes support premium fruit purchases across China, Peru, and emerging Asian economies. Proprietary genetics spur yield and flavor advances; 70% of Mexico’s blueberry acreage now features patented cultivars, securing price resilience. Raspberries and blackberries grow at moderate rates and benefit from robotics that lower labor intensity. Cranberries maintain volume stability through cooperative marketing.

Protected substrate cultivation lifts strawberry yields significantly, enabling growers to satisfy retail contracts consistently. Parallel gains occur in high-density blueberry orchards using evergreen pruning practices and precision fertigation. As functional food brands scale, demand for berry powders strengthens the “others” category (mulberries, gooseberries), though supply remains concentrated in small geographies. Innovation, therefore, progressively segments the fresh berries market by flavor profile, nutritional density, and proprietary branding.

Geography Analysis

North America holds the dominant position with a 31.12% market share in 2025, driven by sophisticated infrastructure, established distribution networks, and premium organic positioning that enables higher margins despite increasing production costs. The United States leads global cranberry production with approximately two-thirds of world output, generating USD 343 million in exports during 2023, while Canada serves as both a major producer and key import destination for counter-seasonal supplies. Mexico emerges as a critical supply source, with berry exports projected to reach 752,000 metric tons in 2025, representing continued growth in blackberries, raspberries, and strawberries despite blueberry production facing competitive pressure from Peru.

Asia-Pacific represents the fastest-growing region with a 5.47% CAGR from 2026-2031, led by China's transformation into the world's largest blueberry producer with 77,000 hectares under cultivation, yielding 520,000 metric tons annually. China's Yunnan Province alone contributes 30% of national output, generating over CNY 3 billion (USD 413 million) in revenue while creating employment for over 100,000 people. Driscoll’s acquisition of Costa Group expands high-tech greenhouse acreage in Australia and China, improving year-round output. Yet inadequate last-mile refrigeration in India and Southeast Asia constrains wider market penetration.

Europe shows steady gains, but climate extremes undermine traditional open-field production. Two-fifths of U.K. berry growers risk insolvency by 2026 due to rising costs and retailer price pressure. EU mandates on pesticide reduction elevate compliance expenses yet encourage transition to protected culture and biocontrols. South America remains export-oriented, with Peru doubling blueberry shipments over five years. Government incentives spur cold-chain hubs at Atlantic ports, linking to North America and Europe. The Middle East and Africa contribute small volumes, but import demand accelerates, especially for premium blueberries, as modern retail expands in the Gulf Cooperation Council region.

Recent Industry Developments

- March 2025: Costa Group established a berry cultivation operation in Laos, beginning with 17 hectares of blueberries, with plans to expand to 200 hectares by 2028. The operation utilizes Laos' climate conditions and geographic position to provide berries to Asian markets, while creating employment opportunities and supporting agricultural growth in the region.

- March 2025: California Berry Cultivars introduced two new strawberry varieties. Castaic, which produces high yields in short-day conditions, and Alhambra, which addresses flavor and performance requirements in the day-neutral market. These additions expand CBC's product range by offering solutions for different growing seasons and production requirements.

- January 2024: India reduced import tariffs on fresh blueberries from 30% to 10% through a trade agreement with the United States. This tariff reduction resolves World Trade Organization (WTO) disputes and increases market access for U.S. blueberry exporters, strengthening agricultural trade between the two countries.

Global Fresh Berries Market Report Scope

A berry is a small, pulpy, and edible fruit. Berries are bright-colored and sweet or sour. Berries are a good source of fiber, antioxidants, vitamin C, vitamin K, and manganese. The report presents a wide-ranging analysis of the market size of the fresh berries market globally. The following have been included in the study - strawberries, blueberries, cranberries, blackberr ies, gooseberries, and other berry kinds. The fresh berries market is segmented by geography (North America, Europe, Asia-Pacific, South America, and Africa). The report includes the Production analysis (volume), consumption analysis (volume and value), import analysis (volume and value), export analysis (volume and value), and price trend analysis. The report offers the market size and forecasts regarding value (USD) and volume (metric tons) for all the above segments.

| Strawberries |

| Blueberries |

| Raspberries |

| Blackberries |

| Cranberries |

| Others (Mulberries, Gooseberries, etc.) |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Russia | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South America | Brazil |

| Argentina | |

| Middle East | Turkey |

| Saudi Arabia | |

| Africa | South Africa |

| Egypt |

| By Berry Type | Strawberries | |

| Blueberries | ||

| Raspberries | ||

| Blackberries | ||

| Cranberries | ||

| Others (Mulberries, Gooseberries, etc.) | ||

| By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis) | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Russia | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South America | Brazil | |

| Argentina | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Africa | South Africa | |

| Egypt | ||

Key Questions Answered in the Report

How large is the fresh berries market in 2026?

The fresh berries market size stands at USD 36.73 billion in 2026 and is projected to reach USD 45.14 billion by 2031.

Which geography leads fresh berry sales?

North America holds 31.12% of the fresh berries market share, supported by advanced cold storage and established retail channels.

What is the fastest-growing berry segment?

Blueberries are forecast to post a 6.92% CAGR between 2026 and 2031 due to rising health awareness and wider protected-culture acreage.

How will labor shortages affect growers?

Rising wages and limited visa labor push growers toward robotic harvesters, raising capital needs but lowering long-term labor exposure.

Page last updated on: