Leafy Greens Market Size and Share

Leafy Greens Market Analysis by Mordor Intelligence

The leafy greens market size is projected to be USD 60.2 billion in 2025, USD 62.5 billion in 2026, and reach USD 76.5 billion by 2031, growing at a CAGR of 4.1% from 2026 to 2031. Rising global wellness priorities, rapid deployments of controlled-environment agriculture (CEA), and retailer innovation in prepared salad kits are reinforcing steady volume growth across every major sales channel of the leafy greens market. Conventional open-field farms still dominate supply, yet their cost advantage is narrowing as water-use restrictions, labor shortages, and climate volatility reduce yields and drive up compliance costs. Meanwhile, vertical and greenhouse operators are capitalizing on year-round production to win premium contracts with foodservice chains that demand consistent quality. Competition is intensifying as multinational packers integrate upstream while local CEA specialists carve out hyper-regional niches rooted in freshness claims and reduced truck mileage from farm to shelf.

Key Report Takeaways

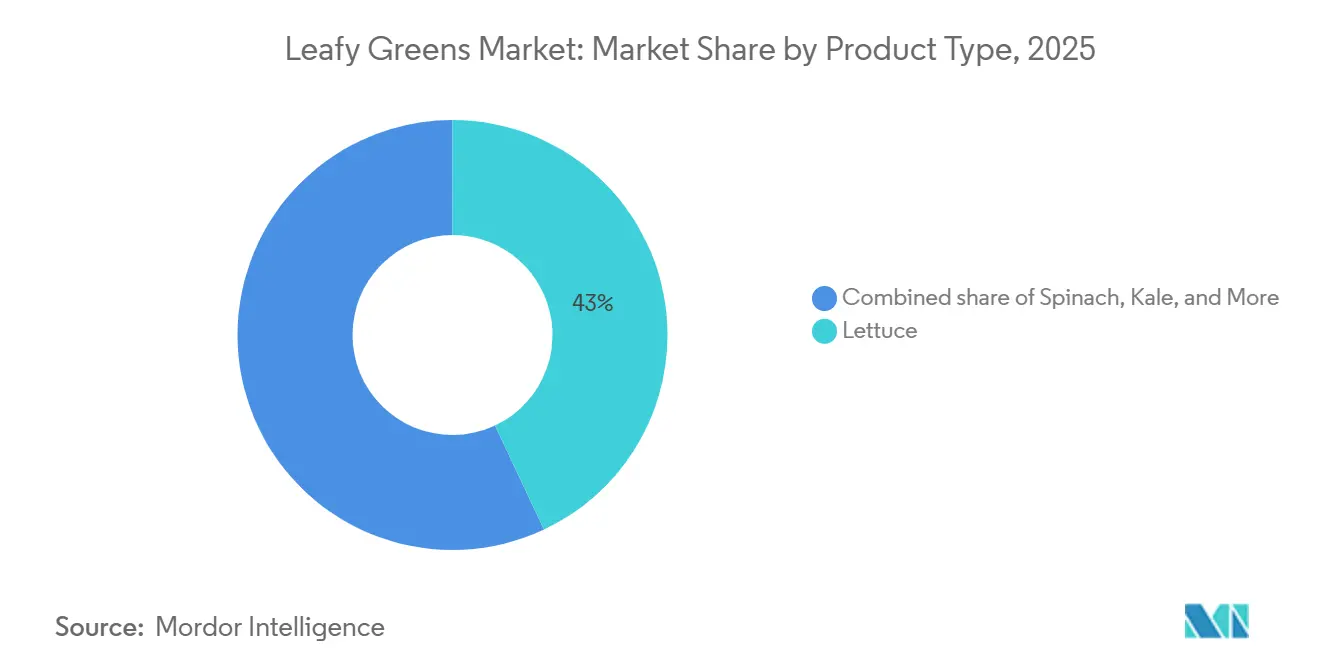

- By product type, lettuce accounted for the largest segment, led with 43% of the leafy greens market share in 2025, whereas microgreens registered the fastest growth during the forecast period at an 11.8% CAGR through 2031

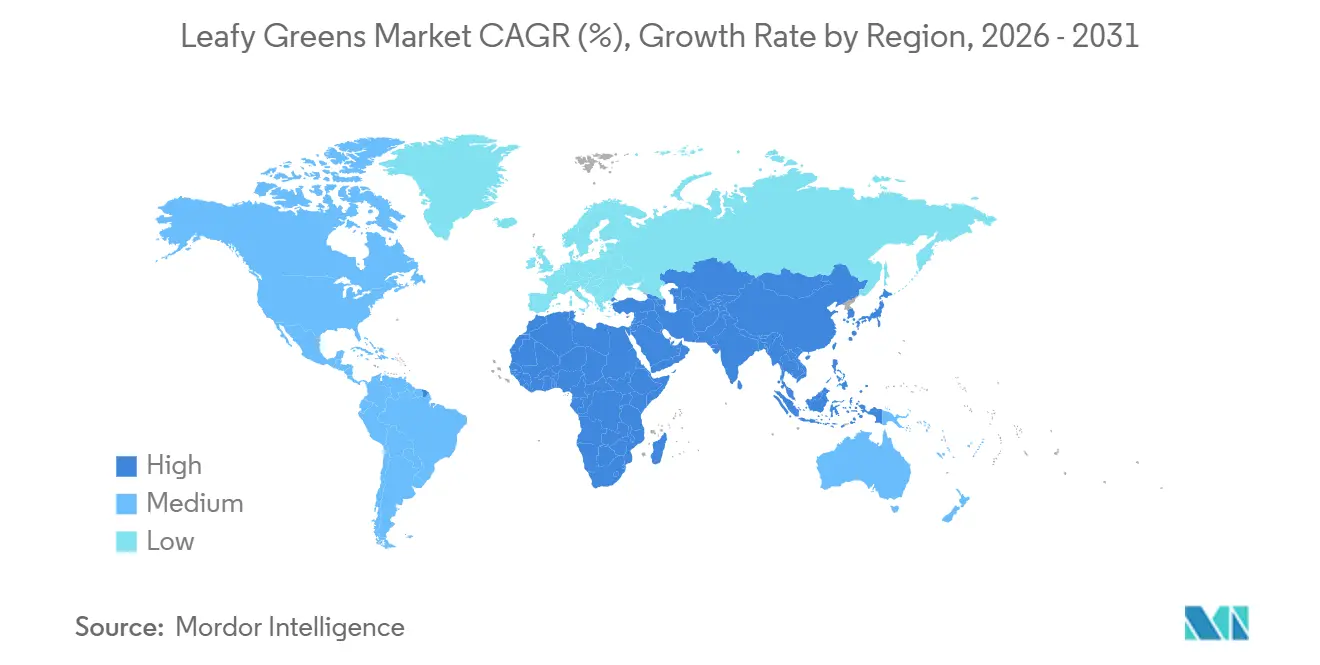

- By geography, Asia-Pacific is the largest market, accounting for 46.2% of the leafy greens market in 2025, while the Middle East registered the fastest growth at a 7.2% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Leafy Greens Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for nutrient-dense foods | +0.5% | Global, with the strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of controlled-environment agriculture | +0.5% | North America and the Middle East lead, secondary growth in Europe and the Asia-Pacific | Long term (≥ 4 years) |

| Corporate net-zero commitments advancing indoor farming | +0.3% | Europe and North America, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Retailer private-label salad-kit innovation | +0.4% | North America and Europe, limited adoption in the Asia-Pacific and the Middle East | Short term (≤ 2 years) |

| Emergence of carbon-credit revenue streams for CEA farms | +0.2% | Europe and California, pilot programs in the Middle East | Long term (≥ 4 years) |

| Genome-edited lettuce varieties with extended shelf life | +0.2% | Global, with early research and development in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Nutrient-Dense Foods

Health-conscious shoppers continue to reallocate grocery budgets toward low-calorie, micronutrient-rich vegetables following the 2025 post-pandemic wellness surge. Leafy greens supply folate, vitamin K, and iron at minimal caloric cost, making them staples in weight-management and chronic-disease-prevention regimens championed by public-health campaigns[1]Source: Centers for Disease Control and Prevention, “Dietary Guidelines and Chronic Disease Prevention,” cdc.gov. Urban households purchase pre-washed kits at elevated rates because two-income families value time savings, and meal-kit services often feature greens as the base ingredient. Asia-Pacific middle-class families are following similar patterns as disposable incomes climb and Western food habits diffuse through supermarket expansion. The result is sustained unit growth even when average retail prices edge higher, reinforcing long-run demand in the leafy greens market.

Expansion of Controlled-Environment Agriculture

CEA has shifted from pilots to industrial-scale assets, enabling multiple harvests each year and tighter yield predictability than field production. Partnerships such as Plenty and Mawarid in Abu Dhabi exemplify sovereign efforts to reduce import dependence with vertical infrastructure. GigaFarm, under construction in Dubai Food Tech Valley, will push regional annual output to 3 million kilograms once operational in late 2026[2]Source: United States Department of Agriculture, “Vegetables and Pulses Yearbook 2025,” Economic Research Service, ers.usda.gov. North American incumbents are mirroring the move, as Taylor Farms bought Equinox Growers in March 2026 to lock in 6 million pounds of greenhouse capacity per year. Energy costs remain the biggest constraint, but falling photovoltaic prices and power-purchase agreements are improving economics for new builds in the leafy greens market.

Corporate Net-Zero Commitments Advancing Indoor Farming

Retailers and consumer-goods companies embed Scope 3 mitigation targets into sourcing programs, which favors greens grown close to distribution centers. Greenspace pledged carbon neutrality by 2027, and Vitacress secured Science Based Targets approval for a 2040 net-zero pathway, both of which promise higher CEA procurement. Marks and Spencer’s Plan A for 2030 requires all produce suppliers to adopt low-carbon practices, nudging growers toward CEA and precision irrigation. The European Union Carbon Border Adjustment Mechanism, starting in 2026, adds a cost to high-emission imports, indirectly advantaging regional CEA farms that can certify lower footprints[3]Source: European Commission, “Carbon Border Adjustment Mechanism Introduction,” europa.eu. In the United States, 7-Eleven began stocking farmed salads in 1,300 California stores vertically in 2024, validating commercial demand for reduced-mileage produce. These policies and deals are channeling capital toward CEA operators across the leafy greens market.

Retailer Private-Label Salad-Kit Innovation

Supermarkets view salad kits as a margin-rich battlefield and are launching chef-curated blends that rival restaurant dishes. Fresh Express rolled out four Mediterranean-themed kits in March 2026 aimed at Millennials and Gen Z seeking convenient gourmet flavors. Taylor Farms followed with an eleven-product protein-forward line combining grilled chicken and quinoa to court fitness-oriented shoppers. Mann Packing teamed with Newman’s Own in January 2025 to co-brand organic options that donate profits to charity, appealing to values-driven buyers. Ark Foods’ Taco Truck kit taps fast-casual flavor trends for cross-category excitement. Category expansion has expanded refrigerator door space allocation in major chains, increasing visibility for all players in the leafy greens market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy costs in vertical farming | −0.5% | Global with acute pressure in Europe and grids lacking renewables | Short term (≤ 2 years) |

| Labor shortages in harvesting and packing | −0.4% | North America and Europe, emerging in the Asia-Pacific | Medium term (2-4 years) |

| Price sensitivity versus field-grown produce | −0.4% | Global, with the strongest effect in South America, Africa, and rural Asia-Pacific | Short term (≤ 2 years) |

| Water-use regulations in drought-prone regions | −0.3% | California, Spain, Australia, and parts of the Middle East and North Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Energy Costs in Vertical Farming

Electricity for LED lighting, cooling, and nutrient pumps drives a large share of vertical-farm operating budgets. European facilities faced cost spikes during the 2024 energy crisis, forcing production pauses at peak tariff hours. Some growers installed solar arrays and batteries to hedge volatility, but these upgrades lengthen payback horizons and raise capital intensity. Sites in the Middle East enjoy cheap solar power yet still need storage to smooth nighttime demand. Until renewable penetration rises and storage costs fall globally, energy will remain the most immediate brake on CEA expansion inside the leafy greens market.

Labor Shortages in Harvesting and Packing

Field and packinghouse workforces are aging and shrinking as immigration caps tighten and rural youth migrate to cities. United States growers reported persistent vacancies in 2025 despite wage hikes, prompting higher overtime costs and crop losses. Canada responded with the Growing Greenhouses program valued at CAD 10 million (USD 7.9 million) to subsidize automation investments. European farms grapple with post-Brexit visa barriers and are now trialing robotic harvesters, although unit prices remain high. Automation eases the squeeze but increases capital requirements for small operators in the leafy greens market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Microgreens Command Premium Foodservice Channels

Lettuce accounted for 43% of global consumption in 2025, underscoring its ubiquity in salads, sandwiches, and wraps, which anchor the leafy greens market. Spinach and kale maintained stable demand, backed by smoothie culture and nutrient-dense messaging, though their growth trailed lettuce's due to narrower culinary uses. Arugula is gaining popularity in Europe and North America as diners crave its peppery flavor, while beet greens and Swiss chard remain niche beyond Mediterranean and Middle Eastern cuisines. Microgreens deliver premium margins as chefs value intense flavor and visual appeal, and their seven-to-fourteen-day cycles align perfectly with vertical farm economics. Seed companies and CEA operators are co-developing proprietary microgreen cultivars that extend shelf life and elevate nutrient density, differentiating this subsegment inside the leafy greens commodity industry.

Vertical farms are particularly suited to microgreens because lighting and space requirements are lower per revenue dollar than for mature heads, thereby compressing energy costs per kilogram. As a result, microgreens are advancing at a 11.8% CAGR and are projected to capture an outsized share of incremental value in the leafy greens market by 2031. Genome-edited lettuce, still in pre-commercial trials, could unlock fresh growth vectors if regulators approve nutrient-boosted lines that justify premium pricing. Open-field systems continue to supply price-sensitive channels but face mounting water and labor challenges that erode historical cost edges. Greenhouse operations provide a middle path, using natural light to curb power bills while offering more climate resilience than fields. Strategic acquisitions like Taylor Farms’ purchase of Equinox Growers highlight how mainstream packers are hedging risk by balancing all three production modes within their leafy greens market portfolio.

Geography Analysis

Asia-Pacific held 46.2% of global consumption in 2025 and is set to grow at a descent CAGR through 2031. China’s middle class is boosting salad-kit uptake as Western retail formats spread across tier-one and tier-two cities, while public health campaigns promote iron-rich dark greens. Japan’s aging population is embracing nutrient-dense vegetables to manage hypertension and diabetes, fueling steady demand for ready-to-eat packs. India’s urban centers are adding salad bars and subscription meal boxes, yet rural diets still lean toward sautéed or stewed greens, which use longer-cooking varieties. Regional CEA investment is nascent but accelerating in densely populated metros where land prices and climatic risks favor vertical systems, reinforcing Asia-Pacific’s leadership in the leafy greens market.

The Middle East is the fastest-growing region, with a 7.2% CAGR, as sovereign wealth funds bankroll CEA megaprojects to reduce import dependence. Companies such as GigaFarm contribute to industry growth in Dubai, and Saudi Arabia’s Public Investment Fund has aligned with AeroFarms to replicate the model regionwide. Extreme heat and chronic water scarcity make indoor agriculture a policy imperative, shifting share away from imports flown in from Europe and Africa. Local shoppers are willing to pay a premium for home-grown freshness, underpinning revenue upside in the leafy greens market.

North America accounted for a significant share of revenue in 2025 and is expanding at a prominent CAGR, driven by relentless salad-kit innovation and CEA integration by legacy packers. California’s Salinas Valley and Arizona’s Yuma region remain field powerhouses but confront water caps under the Sustainable Groundwater Management Act that could limit acreage by 2031. Canada's greenhouse industry is growing with support from federal and provincial grants, as well as the Growing Greenhouses program for automation and renewable energy investments. Mexico leverages lower labor costs to ship romaine and iceberg north, yet trade friction remains a latent risk as antidumping disputes in other produce categories illustrate. Europe’s CAGR is slower as mature markets saturate and Spanish output faces irrigation curbs, but Dutch and Belgian greenhouses are poised to fill winter gaps, maintaining regionwide supply stability in the leafy greens market.

Competitive Landscape

Dole, Taylor Farms, Bonduelle, Fresh Express, and Greenyard compete chiefly on throughput, private label execution, and geographic coverage, yet none holds a majority share, limiting pricing power. Regional vertical-farm players use freshness, pesticide-free claims, and local branding to differentiate, challenging incumbents in metropolitan premium tiers. Taylor Farms’ March 2026 acquisition of Equinox Growers shows mainstream packers are buying CEA assets to protect year-round contracts and mitigate climate risks.

Vertical-farming specialists still face capital hurdles, such as Plenty filed for Chapter 11 in March 2025 and exited leafy greens to focus on strawberries with higher margins, while Bowery Farming shuttered operations in November 2024. Automation and data analytics are emerging as decisive differentiators, growers are deploying vision-guided robots for harvesting, predictive models for yield forecasting, and blockchain for traceability to meet strict retailer food-safety mandates. Taylor Farms’ joint purchase of Bonduelle’s German salad business with Foodiverse in April 2025 consolidated three sites, enabling cross-border logistics optimization across Europe and signaling a shift toward vertical integration rather than geographic spread.

Retailers keep squeezing packers on price through aggressive private-label rollouts, driving companies to pursue efficiency gains or risk replacement. Sovereign-backed Middle East CEA entrants gain cost advantages from subsidized solar power and low-interest financing, setting up future export ambitions that could reshape trade lanes by 2031. Genome-edited varieties, carbon-credit monetization, and direct-to-consumer subscription boxes stand out as white-space opportunities where incumbents hold limited equity, inviting specialized startups to capture value. The competitive narrative, therefore, pivots from pure volume toward technology enablement and supply-chain resilience within the leafy greens market.

Recent Industry Developments

- March 2025: BrightFarms began shipping pesticide-free leafy greens from its new 1.5 million-square-foot greenhouse in Macon, Georgia, representing the state's most advanced facility and part of the company's broader expansion strategy following its acquisition by Cox Enterprises.

- January 2025: GoodLeaf Farms welcomed Farm Credit Canada as a strategic investor, bolstering the capital base of Canada’s largest indoor vertical farm operator with 280 000 square feet across three sites and more than 2,700 retail points, underscoring institutional support for scaling controlled-environment capacity inside the leafy greens market.

- July 2024: Plenty revealed a USD 680 million joint venture with the United Arab Emirates firm Mawarid to roll out vertical farms across the Gulf and beyond, signaling robust Middle East investment momentum that is accelerating controlled-environment growth within the leafy greens market.

Global Leafy Greens Market Report Scope

The Leafy Greens Market Report is Segmented by Product Type (Lettuce, Spinach, Kale, Arugula, Beet Greens, Microgreens, and Swiss Chard) and by Geography (North America (United States, Canada, and Mexico), Europe (Germany, United Kingdom, and France), South America (Brazil, Argentina, and Chile), Asia Pacific (China, India, Japan, and Australia), Middle East (Saudi Arabia and United Arab Emerates), and Africa (South Africa, Nigeria, and Egypt). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Lettuce | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Spinach | Similar to Lettuce | ||

| Kale | Similar to Lettuce | ||

| Arugula | Similar to Lettuce | ||

| Beet Greens | Similar to Lettuce | ||

| Microgreens | Similar to Lettuce | ||

| Swiss Chard | Similar to Lettuce | ||

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Iran | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Product Type | Lettuce | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Spinach | Similar to Lettuce | |||

| Kale | Similar to Lettuce | |||

| Arugula | Similar to Lettuce | |||

| Beet Greens | Similar to Lettuce | |||

| Microgreens | Similar to Lettuce | |||

| Swiss Chard | Similar to Lettuce | |||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Chile | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| United Kingdom | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Iran | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Nigeria | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

| Egypt | Production Analysis (Area Harvested, Yield, and Production Volume) | |||

| Consumption Analysis (Consumption Value and Volume) | ||||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Regulatory Framework | ||||

| List of Key Players | ||||

| Logistics and Infrastructure | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

What is the projected value of the leafy greens market in 2031?

It is forecast to reach USD 76.5 billion by 2031, advancing at a 4.1% CAGR from 2026.

Which product type is growing the fastest within global greens?

Microgreens are expanding at an 11.8% CAGR through 2031, driven by premium foodservice demand and vertical-farm economics.

Why are sovereign funds investing in indoor farming in the Middle East?

Food-security mandates and water scarcity push governments to localize production projects like Dubai's GigaFarm will supply 3 million kilograms annually by 2026.

What are the main headwinds facing vertical farms?

High electricity costs, labor shortages, premium price gaps relative to field produce, and regulatory ambiguity regarding gene-edited crops restrain near-term growth.

Page last updated on: