Organic Fruits And Vegetables Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 89.5 Billion |

| Market Size (2031) | USD 138.90 Billion |

| Growth Rate (2026 - 2031) | 9.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

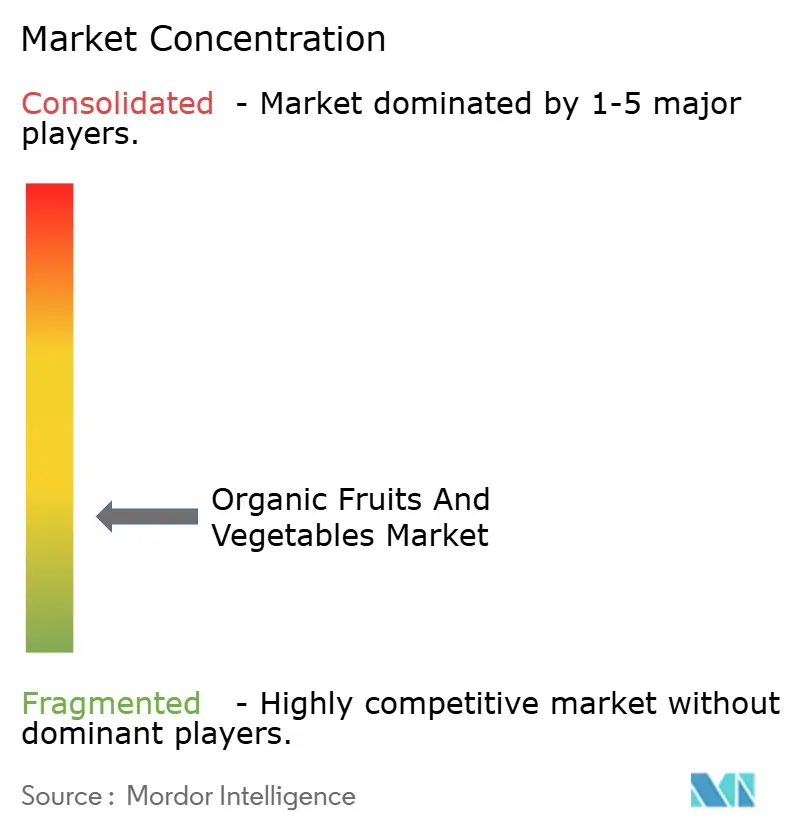

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Fruits And Vegetables Market Analysis by Mordor Intelligence

The organic fruits and vegetables market size was valued at USD 78.8 billion in 2025 and estimated to grow from USD 89.5 billion in 2026 to reach USD 138.9 billion by 2031, at a CAGR of 9.20% during the forecast period (2026-2031). Strong health awareness, expanding policy incentives, and maturing cold-chain logistics are widening the customer base beyond early adopters. Retailers are giving larger shelf space to certified produce as residue findings on conventional items sharpen consumer risk perception. On the supply side, subsidized transition programs in the United States and the European Union are shortening payback periods, encouraging mid-sized growers to convert acreage. Online platforms are translating that momentum into double-digit volume growth as next-day delivery becomes reliable in major cities. Private capital is also flowing toward soil-health technologies, bringing scale efficiencies that help offset yield penalties. Collectively, these forces keep the organic fruits and vegetables market on an expansion trajectory even as macro headwinds pressure discretionary spending.

Key Report Takeaways

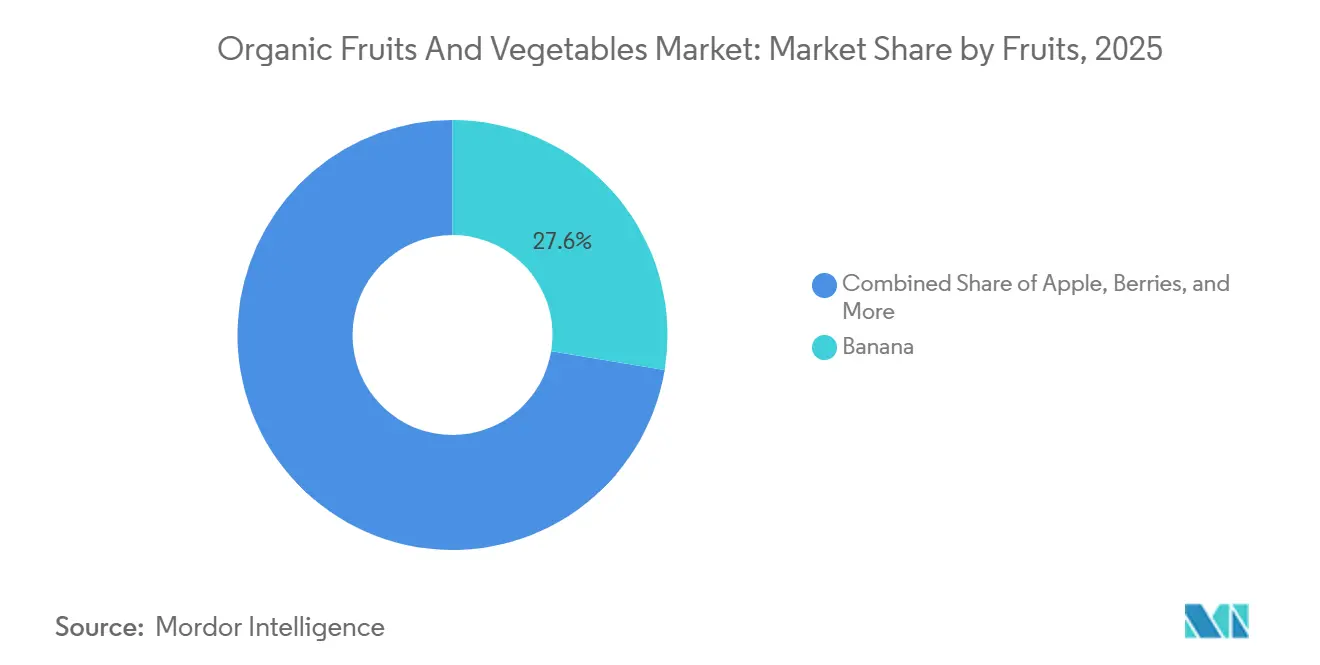

- By fruit type, bananas were the largest segment, accounting for 27.6% of the organic fruits and vegetables market share in 2025, whereas berries were projected to be the fastest-growing segment, advancing at an 11.6% CAGR through 2031.

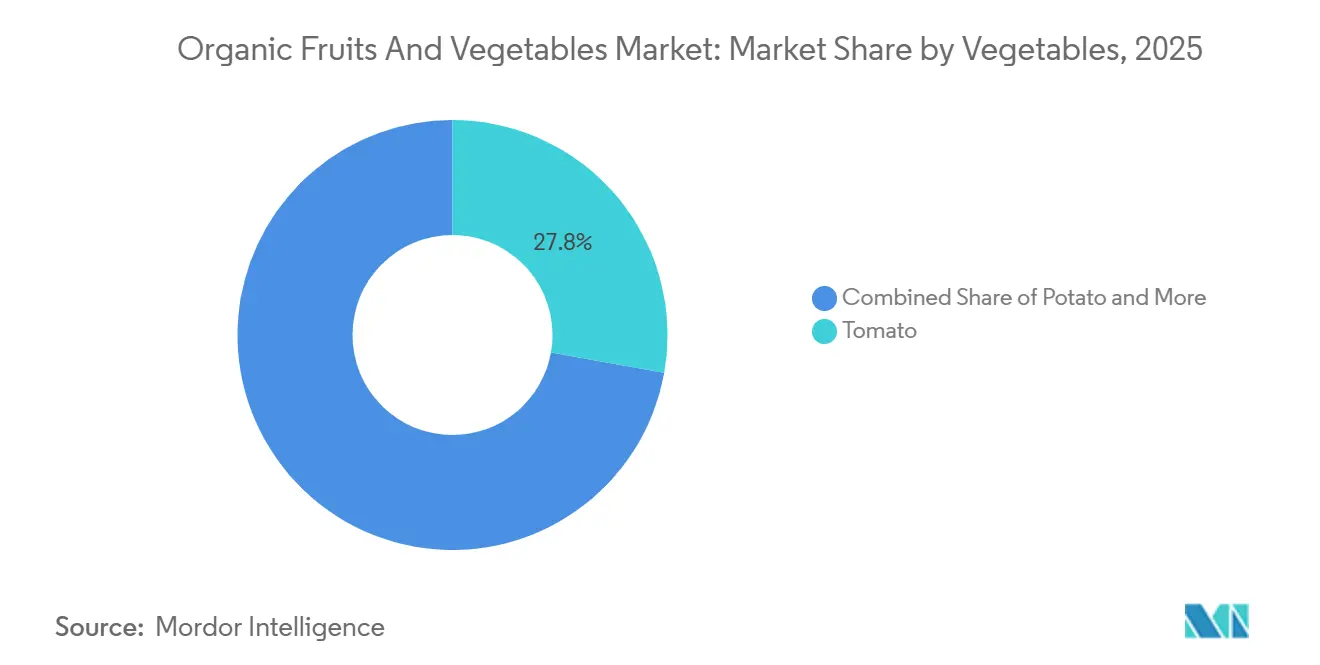

- By vegetable type, tomatoes were the largest segment, accounting for 27.8% of the organic fruits and vegetables market size in 2025, while leafy vegetables are anticipated to be the fastest-growing segment, advancing at a 10.9% CAGR through 2031.

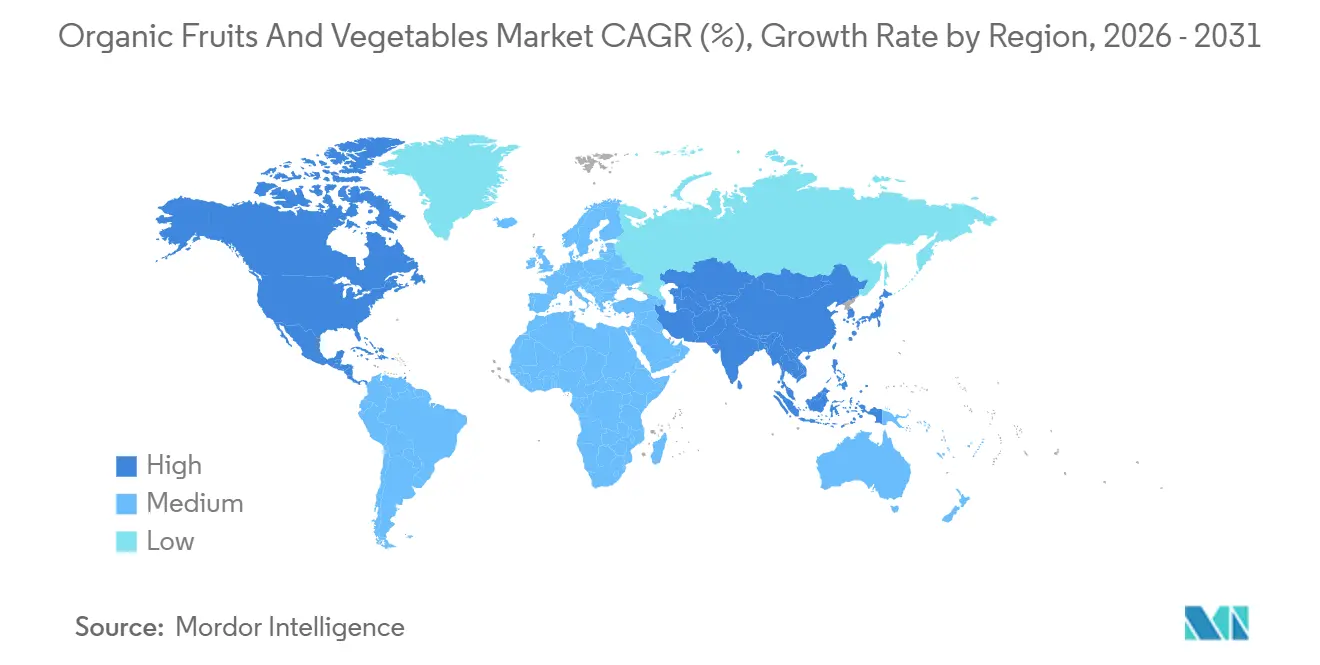

- By geography, North America was the largest region, holding 34.20% of the organic fruits and vegetables market share in 2025, while Asia-Pacific is projected to exhibit the fastest-growing region, advancing at a 10.0% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Organic Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health-driven consumer demand surge | +2.8% | Global, with peak intensity in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government conversion subsidies and incentives | +2.1% | North America and Europe core, expanding to India and China | Short term (≤ 2 years) |

| Price premium boosting farm profitability | +1.5% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Environmental, Social, and Governance (ESG)-focused capital favoring climate-resilient supply | +1.3% | North America, Europe, and Australia, and with spillover to South America | Long term (≥ 4 years) |

| Retail-vertical-farm alliances for year-round yields | +0.9% | North America and Europe, pilot projects in Asia-Pacific | Medium term (2-4 years) |

| Regenerative-organic certification unlocking food-service deals | +0.6% | North America and Europe, limited adoption in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health-Driven Consumer Demand Surge

The primary structural driver of the global organic fruit and vegetable market is the ongoing shift toward health-conscious consumption. Consumers increasingly perceive organic produce as having lower pesticide residues, higher nutrient content, and contributing to improved long-term health. Growing awareness of chronic illnesses associated with dietary habits, such as obesity, diabetes, and cardiovascular diseases, has led households to prioritize "clean-label" and minimally processed foods. This trend has driven demand for immune-boosting foods like organic citrus, leafy greens, and berries. Retailers in North America and Europe have reported double-digit growth in organic fresh produce sales, according to the United States Department of Agriculture, retail sales of organic fresh fruits and vegetables reached USD 21.5 billion in 2021 and have shown consistent growth over the past two decades. Even after the pandemic, demand remains structurally high, as health consciousness has become a habitual rather than a temporary behavior.

Government Conversion Subsidies and Incentives

Government policy support is crucial in increasing organic cultivation acreage. Transitioning from conventional to organic farming typically involves a 2–3 year conversion period, during which yields may decline, and farmers are unable to secure organic price premiums. To address this challenge, many governments offer subsidies, technical assistance, and reimbursement for certification costs. In the European Union, the Common Agricultural Policy (CAP) includes eco-schemes that provide financial incentives for adopting organic and regenerative practices. India’s Paramparagat Krishi Vikas Yojana (PKVY) promotes organic cluster development, while China has enhanced its organic certification frameworks to meet growing domestic and export demand. These policy measures directly contribute to increasing the supply of organic fruits and vegetables, supporting stable long-term growth.

Environmental, Social, and Governance-Focused Capital Favoring Climate-Resilient Supply

Environmental, Social, and Governance (ESG) investment flows are increasingly focused on sustainable agriculture. Institutional investors, impact funds, and development banks are prioritizing organic farming due to its reduced use of synthetic chemicals, promotion of soil health, and support for biodiversity. Organic fruit and vegetable production aligns with climate-resilience strategies, including carbon sequestration, reduced fertilizer runoff, and regenerative soil management practices. As food companies face growing pressure to decarbonize their supply chains, they are increasingly sourcing organic and regenerative produce to achieve Scope 3 emissions targets. In 2024, the European Union’s Common Agricultural Policy Eco-Schemes has provided financial incentives to producers for converting and maintaining certified organic farmland. This initiative, part of the European Green Deal's goal to achieve 25% organic farmland by 2030, allocates EUR 612 million (USD 673 million) annually in direct support[2]Source: European Commission, Directorate-General for Agriculture and Rural Development, “Eco-schemes - Agriculture and rural development,” agriculture.ec.europa.eu .

Price Premium Boosting Farm Profitability

Organic fruits and vegetables generally command significant price premiums over their conventional counterparts in retail channels. These premiums help offset lower yields and higher labor costs, enhancing profitability for growers in established markets. The premium pricing structure also encourages new farmers to transition acreage to organic production. In developed markets such as the United States and Western Europe, consumers are willing to pay higher prices due to perceived health and environmental benefits. Retailers support this positioning through differentiated branding and strategic shelf placement. Over time, stable premiums provide long-term financial visibility for producers and investors. For instance, while prices for organic fruits and vegetables increased at a similar rate to conventional products over the past year, individual items showed considerable variation. Between the end of January 2024 and January 2025, the average price increase for organic items was 2.4%, compared to 2.5% for conventional items.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher unit production cost and yield gaps | -1.8% | Global, most acute in regions with limited organic input availability | Medium term (2-4 years) |

| Certification complexity and audit fatigue | -1.2% | Global, particularly burdensome for smallholders in Asia-Pacific and Africa | Short term (≤ 2 years) |

| Biological-input shortages in organic supply chains | -0.9% | Global, with acute shortages in Asia-Pacific and South America | Medium term (2-4 years) |

| Retailer carbon-footprint caps on long-haul perishables | -0.7% | Europe and North America, affecting suppliers in South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Certification Complexity and Audit Fatigue

Organic certification requires adherence to stringent documentation, inspection, and traceability standards. Smallholder farmers in Asia-Pacific and Africa often encounter financial and administrative challenges in meeting international certification criteria, which restricts the expansion of global supply. The distinct requirements of the United States National Organic Program, European Union Regulation 2018/848, and Japan Agricultural Standard compel exporters to manage overlapping documentation processes. While equivalency agreements facilitate trade between the United States and Europe, the absence of similar agreements with countries such as China, India, and Brazil limits cross-border trade flexibility.

Retailer Carbon-Footprint Caps on Long-Haul Perishables

Tesco and Carrefour now restrict air-freighted produce to under 5% of organic volume, pushing African and South American suppliers toward slower sea routes. Transit times extend to two to three weeks, heightening spoilage risk even with modified-atmosphere packaging. Producers unable to finance cold-chain upgrades face market-access erosion, particularly in berries and asparagus that have short post-harvest windows. Although organic production minimizes chemical inputs, the environmental benefits can be diminished by long-distance logistics. Retailers may prefer locally sourced conventional produce over imported organic options when carbon intensity is significant, affecting the organic fruit and vegetable market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fruits: Berries Capture High-Value Momentum

Bananas were the largest segment, led with 27.6% of the organic fruits and vegetables market share in 2025. Bananas continue to dominate overall fruit revenue, supported by established certification processes in tropical regions and consistent consumer demand for staple produce. Stable supply chains contribute to steady banana pricing, solidifying their position as a key volume driver in the organic fruits and vegetables market. Apples represent another significant sub-segment, utilizing controlled-atmosphere storage to minimize spoilage and extend sales periods. Citrus fruit consumption is increasing, driven by the demand for organic orange juice in North America and Europe. Supply is limited due to citrus greening disease, which significantly impacts organic groves that cannot use synthetic pesticides.

Berries are fastest fastest-growing segment, advancing at an 11.6% CAGR through 2031. The shift toward berries highlights a broader consumer focus on nutrient density rather than caloric value. That technology underpins food-service demand by preserving anthocyanins and extending shelf life, supporting steady penetration into institutional menus. Grapes highlight how regenerative farming practices can significantly boost farm-gate prices by linking soil health improvements to brand narratives. Kiwi, passion fruit, and dragon fruit remain niche products but benefit from superfood marketing, drawing health-conscious consumers and contributing to the expansion of the organic fruits and vegetables market in specialty retail outlets.

By Vegetables: Leafy Vegetables Lead Salad Kit Upswing

Tomatoes were the largest segment, accounting for 27.8% of the organic fruits and vegetables market size in 2025. This performance was supported by greenhouse production, which enables more efficient organic certification compared to traditional field systems. For instance, the company has continued to expand and emphasize its organic product lines, particularly focusing on Organic Hiiros Tomatoes and Organic Ombre Cherry Tomatoes. In 2024, the company received recognition for its organic products, including Organic Red Bell Peppers, which won the Chef’s Choice Award at the 17th Annual Leamington Greenhouse Competitions. This achievement enabled the company to supply major retailers with consistent, year-round organic volumes that field growers cannot provide.

Leafy vegetables are the fastest-growing segment, advancing at a 10.9% CAGR through 2031, the fastest among vegetable segments. This growth is primarily driven by the increasing popularity of fresh-cut salad kits, which reduce preparation time and minimize food waste, particularly for single-person households. Potatoes also held a significant share in 2025, driven by demand for organic French fries from food-service operators such as Chipotle. Despite this demand, growth in the potato segment remains limited due to a lack of differentiation at the point of sale.

Geography Analysis

North America were largest region held 34.20% of the organic fruits and vegetables market share in 2025, supported by subsidies from the United States Department of Agriculture and retailer initiatives to increase organic shelf space. In 2025, the United States accounted for a significant share of the North American market, with California, Washington, and Oregon representing significant share of domestic organic acreage. Production in these states faces challenges due to water scarcity and labor shortages. In Canada, growth is driven by greenhouse production in Ontario and British Columbia, which more readily achieves organic certification compared to field systems. Nature Fresh Farms plays a key role by supplying major retailers across North America.

Asia-Pacific exhibits fastest growing region, advancing at an 10.0% CAGR to 2031, marking the fastest growth rate globally. This growth is driven by rising incomes and urbanization, which are fostering the adoption of organic products in countries such as China, India, and Japan. In 2000, only 4,000 hectares of China’s arable land were certified as organic. By 2023, this figure had increased to 2.9 million hectares, according to Research Institute of Organic Agriculture (FiBL). In 2025, the Indian government is promoting organic farming through two initiatives, the Paramparagat Krishi Vikas Yojana (PKVY), implemented across all states, and the Mission Organic Value Chain Development for North Eastern Region (MOVCDNER), focused on northeastern states to produce organic fruit and vegetable.

Europe is projected to hold the largest regional share in 2025, as market saturation in Germany, France, and the United Kingdom drives competition toward prioritizing margins over volume. According to the International Federation of Organic Agriculture Movements, the total area of farmland under organic production, including fruits and vegetables, in the European Union increased to 18.1 million hectares in 2024, compared to 2023, the number of organic producers grew by 1%[3]Source: Helga Willer and Julia Lernoud, “The World of Organic Agriculture 2025 Statistical Yearbook,” ifoam.bio. The United Kingdom is experiencing growth post-Brexit, with domestic subsidies replacing European Union programs and retailers such as Tesco committing to expanding organic product assortments. Italy and Spain are concentrating on organic olive oil and wine, which yield higher premiums compared to fresh produce. Meanwhile, Austria continues to have the highest organic penetration of total agricultural land, driven by strong consumer demand and government incentives.

Competitive Landscape

The organic fruits and vegetables market is fragmented, with key players including Dole plc, Fresh Del Monte Produce Inc., Driscoll’s Inc., Greenyard, and Calavo Growers Inc. The market's structure reflects low barriers to entry for regional growers and limited economies of scale due to the perishable nature of the supply chain. Dole plc holds a significant market share, supported by its vertically integrated banana and pineapple operations across Latin America and the Philippines. Fresh Del Monte Produce Inc. maintains a strong position through its diversified organic product portfolio, including avocados, melons, and pineapples.

Competitive strategies are increasingly focused on vertical integration, with major players acquiring upstream farms and downstream processing facilities to enhance margins and ensure consistent supply. The adoption of advanced technologies is also a key differentiator. For instance, companies like Nature Fresh Farms utilize hydroponic systems that achieve organic certification without the standard three-year transition period required for traditional field farms, enabling quicker scaling of supply.

Growth opportunities are emerging in underserved categories such as organic root vegetables and tropical fruits, where certification challenges and limited acreage restrict supply. Smaller players, such as Healthy Buddha in India, are disrupting the market with e-commerce-first models that bypass retail intermediaries, allowing them to capture higher margins. Additionally, regenerative-organic certification is creating a premium segment, offering significant price premiums over standard organic products.

Organic Fruits And Vegetables Industry Leaders

Dole plc

Fresh Del Monte Produce Inc.

Driscoll’s Inc.

Greenyard

Calavo Growers Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Bigbasket established a partnership with the Andhra Pradesh government in India through a Memorandum of Understanding (MoU) to procure organic fruits, vegetables, and staples from local farmers for nationwide distribution. The agreement includes the establishment of four collection centers to enhance market connectivity and increase farmer income.

- September 2024: Big Basket, a Tata Group subsidiary, has introduced organic fruits, vegetables, and staple foods at prices similar to conventional products. This initiative aims to make organic food more accessible while supporting over 30,000 farmers in its supply chain.

- May 2024: Almaverde Bio, an Italian organic brand, introduced the Elodì strawberry variety, which is grown exclusively in Romagna. The strawberry was developed through collaborative research between the Newplant Group and CREA in Forlì.

Global Organic Fruits And Vegetables Market Report Scope

Organic fruits and vegetables refer to fruits and vegetables that are grown without synthetic pesticides and are certified as organic. The Organic Fruits and Vegetables Market Report is Segmented by Fruits (Banana, Apple, Berries, Grapes, Kiwi, and Other Fruits(Passion Fruit, Dragon Fruit, etc.)), Vegetables (Leafy Vegetables, Tomato, Potato, and Other Vegetables (Asparagus, Sweet Corn, etc.)), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Banana |

| Apple |

| Berries |

| Grapes |

| Kiwi |

| Other Fruits(Passion Fruit, Dragon Fruit, etc.) |

| Leafy Vegetables |

| Tomato |

| Potato |

| Other Vegetables (Asparagus, Sweet Corn, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Austria | |

| Spain | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| Rest of Asia-pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Fruits | Banana | |

| Apple | ||

| Berries | ||

| Grapes | ||

| Kiwi | ||

| Other Fruits(Passion Fruit, Dragon Fruit, etc.) | ||

| By Vegetables | Leafy Vegetables | |

| Tomato | ||

| Potato | ||

| Other Vegetables (Asparagus, Sweet Corn, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Austria | ||

| Spain | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| Rest of Asia-pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will global demand for organic fruits and vegetables be by 2031?

The organic fruits and vegetables market size was valued at USD 78.8 billion in 2025 and estimated to grow from USD 89.5 billion in 2026 to reach USD 138.9 billion by 2031, at a CAGR of 9.20% during the forecast period (2026-2031).

Which fruit group is growing the fastest in certified-organic formats?

Berries are the front-runner, advancing at an 11.6% CAGR through 2031, as IQF technology boosts year-round food-service and retail demand.

Which region offers the highest growth potential for suppliers?

Asia-Pacific leads with a projected 10.0% CAGR through 2031, driven by China's Green Food scheme and Indias cluster programs that widen consumer access.

How concentrated is competition among major brands?

The top five companies hold significant share of global revenue, reflecting a fragmented field where regional specialists can still obtain shelf space and negotiate directly with retailers.

Page last updated on: