United Kingdom Fruits And Vegetables Market Analysis by Mordor Intelligence

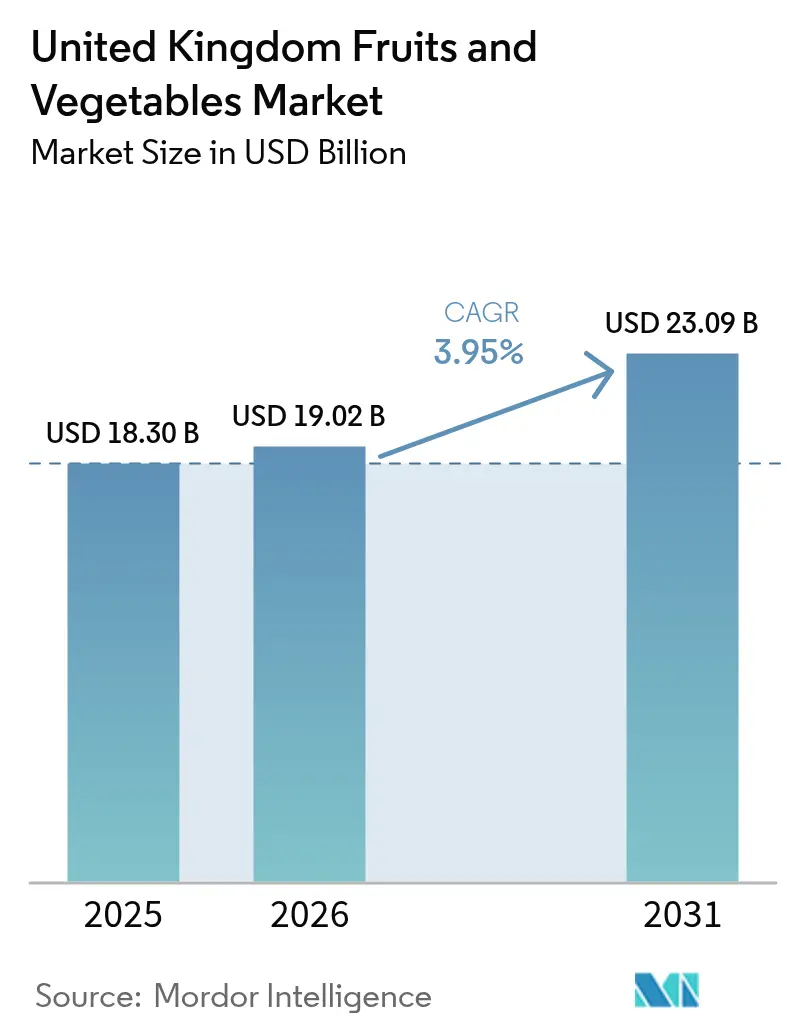

The United Kingdom fruits and vegetables market size is expected to grow from USD 18.3 billion in 2025 to USD 19.02 billion in 2026 and is forecast to reach USD 23.09 billion by 2031 at 3.95% CAGR over 2026-2031. The expansion reflects a structural shift toward higher domestic output, stronger import-substitution policies, and rapid mainstreaming of controlled-environment agriculture. Government grants for renewable energy installations, retailer commitments to long-term supply contracts, and heightened consumer demand for low-carbon produce are sustaining investment momentum. At the same time, labor shortages, volatile energy costs, and evolving United Kingdom–European Union phytosanitary requirements are reshaping competitive dynamics and accelerating automation uptake. As the market transitions toward greater resilience, vertically integrated growers and technology-driven producers are consolidating share while smaller, labor-intensive farms evaluate partnership models and joint investment pathways.

Key Report Takeaways

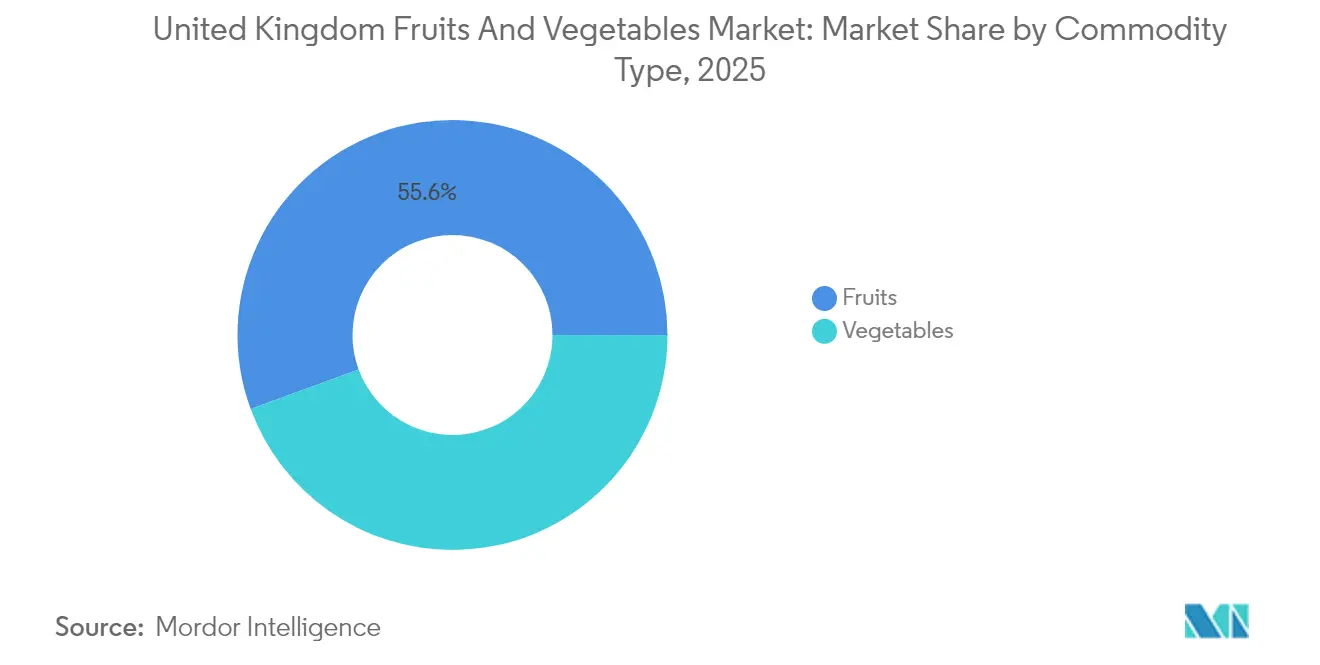

- By commodity type, fruits led with 55.60% of United Kingdom fruits and vegetables market size in 2025, and are projected to expand at a 4.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing retailer-backed long-term supply contracts | +0.8% | England, Scotland, and Wales | Medium term (2-4 years) |

| Rising consumer demand for local, low-carbon produce | +0.6% | National, with concentration in urban areas | Long term (≥ 4 years) |

| Rapid expansion of controlled-environment agriculture capacity | +0.9% | England, particularly East Anglia and Kent | Short term (≤ 2 years) |

| Government grants for on-farm renewable energy integration | +0.4% | England, with spillover to Wales and Scotland | Medium term (2-4 years) |

| Digitization of produce traceability systems | +0.3% | National, early adoption in major supply chains | Medium term (2-4 years) |

| Adoption of regenerative practices to meet ESG (Environmental, Social, and Governance) targets | +0.5% | National, concentrated in corporate farming operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing retailer-backed long-term supply contracts

Major supermarket groups are shifting from annual tenders to multiyear agreements that cover volumes, pricing frameworks, and joint investment in sustainable infrastructure. These contracts provide growers with stable cash flows that de-risk capital-intensive greenhouse projects and robotics upgrades. Supermarkets capture differentiated supply while signaling support for domestic food security objectives. The trend also mitigates waste by locking in harvest planning and committing retailers to predictable offtake volumes.

Rising consumer demand for local, low-carbon produce

United Kingdom consumers demonstrate a strong preference for produce with verified local origin and low transportation emissions. Retailers now highlight “grown-in-Britain” labels and carbon-footprint scores on shelf tags, enabling price premiums that offset higher domestic production costs. Public health campaigns encouraging fruit and vegetable intake further amplify demand, especially among urban shoppers who value traceability and freshness.

Government grants for on-farm renewable energy integration

The United Kingdom government has allocated substantial funding to support renewable energy adoption in agriculture, recognizing energy costs as a critical factor affecting sector competitiveness and sustainability. The Improving Farm Productivity Grant provides up to GBP 100,000 (USD 125,000) for solar installations, covering up to 25% of eligible costs for farmers and horticultural businesses.[1]Source: UK Government, “About the Improving Farm Productivity Grant Round 2,” GOV.UK Government support extends beyond direct grants to include planning permission streamlining for renewable energy installations and integration with Environmental Land Management schemes that provide additional payments for sustainable practices.

Adoption of regenerative practices to meet ESG (Environmental, Social, and Governance) targets

Corporate sustainability commitments are driving widespread adoption of regenerative agriculture practices across the United Kingdom's fruit and vegetable production, with major retailers and food companies establishing specific targets for supplier environmental performance. The Agriculture and Horticulture Development Board's Environment Baselining Pilot provides fully funded carbon audits and tailored action plans to support the industry's transition to net zero by 2050.[2]Source: Agriculture and Horticulture Development Board, “GrowSave: Energy Management in Protected Cropping,” horticulture.ahdb.org.ukRegenerative practices offer multiple benefits, including improved soil health, enhanced biodiversity, reduced input costs, and carbon sequestration potential that can generate additional revenue streams through carbon credit markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages post-Brexit | −1.2% | Seasonal growing regions | Short term (≤ 2 years) |

| Volatile energy prices affecting greenhouse economics | −0.8% | Protected-cropping clusters | Medium term (2-4 years) |

| Phytosanitary trade barriers with the European Union | −0.6% | Export-dependent operations | Medium term (2-4 years) |

| Limited cold-chain infrastructure for perishables exports | −0.4% | Port regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labor shortages post-Brexit

The United Kingdom's agriculture sector faces acute labor shortages that threaten production capacity and operational efficiency, with Brexit restrictions on European Union worker mobility exacerbating pre-existing workforce challenges. Post-Brexit labor constraints have intensified due to restrictive access to EU workers, affecting 40% of food supply chains and creating particular pressure in labor-intensive fruit and vegetable harvesting operations. The British Berry Growers survey revealed that half of strawberry and raspberry growers could cease operations by 2026, with labor shortages cited as a primary concern alongside inadequate retailer pricing.

Limited cold-chain infrastructure for perishables exports

The United Kingdom's cold-chain infrastructure faces capacity constraints and technological limitations that restrict export potential for fresh produce, particularly affecting time-sensitive perishables requiring precise temperature control throughout transportation. The Cold Chain Federation has identified worker shortages and inadequate recognition of cold-chain infrastructure as critical national infrastructure as key challenges facing the sector. Investment in cold-chain infrastructure requires substantial capital commitments and coordination across multiple stakeholders, creating barriers to rapid capacity expansion that could support increased domestic production and export growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Commodity Type: Fruits Maintain Value Leadership amid Shifting Production Patterns

Fruits represented 55.60% of the United Kingdom fruits and vegetables market share in 2025, and are projected to expand at a 4.42% CAGR through 2031, supported by strong demand for berries and convenience packs. Soft-fruit revenue slightly declined to GBP 734 million (USD 857.5 million) in 2024 as protected cultivation and substrate systems extended picking seasons. In contrast, orchard-fruit output fell as growers replanted toward higher-margin raspberries. Retail promotions and healthy-snacking trends sustain premium price elasticity that cushions growers against input-cost shocks.

Vegetables remained essential for daily diets but faced tighter margins. Domestic supply met just over half of the demand in 2023, highlighting both import reliance and productivity gains from precision irrigation and disease-resistant seeds. Cucumber self-sufficiency rose markedly after the Fenland complex came online, evidencing the scalability of renewable-energy greenhouses. Tomato growers confronted disease risk and heating expenses, prompting trials of heat-tolerant cultivars, waste-wood biomass boilers, and intercropping rotations to retain production viability.

Geography Analysis

England dominates commercial output, hosting extensive glasshouse corridors in East Anglia and Kent that leverage proximity to distribution centers and advanced agronomy services. These counties attract the lion’s share of renewable-energy grants and robotics pilots, translating to productivity levels that outpace national averages.

Scotland excels in soft-fruit cultivation, where cooler summers favor high-brix berries with fewer pesticide applications. The Science and Advice for Scottish Agriculture (SASA) program accelerates cultivar trials that lengthen harvest windows and bolster export readiness. Wales and Northern Ireland emphasize niche vegetable lines and organic acreage, benefitting from Environmental Land Management payments that reward regenerative practices.

Climate modeling indicates Southern counties could soon support mandarins and avocados, while milder northern conditions may improve brassica yields. These shifts will prompt region-specific investment in irrigation, varietal Research and Development, and cold-chain assets, reshaping the spatial profile of the United Kingdom fruits and vegetables market.

Regulatory Landscape

The United Kingdom fruits and vegetables market operates under a post-Brexit, risk-based import and plant health control regime led by Defra and implemented through systems such as IPAFFS for pre-notification. High and medium-risk plants and plant products require phytosanitary certification, and they are subject to documentary, identity, and physical checks. This increases compliance costs and lead times for import-dependent supply chains.

Policy timing is also shaping planning for importers and packers. Defra guidance indicates that marketing standards controls for fruit and vegetables imported from the EU are not scheduled before 1 February 2027, and the easement for medium-risk fruit and vegetables from the EU, Switzerland, and Liechtenstein runs to 31 January 2027. Alongside this, the Food Standards Agency is preparing for a potential UK-EU SPS Agreement intended to reduce routine checks and documentation, with mid-2027 referenced as a target implementation window. Pesticide compliance is reinforced through the Great Britain multi-annual control plan for pesticide residues covering 2026 to 2028.

Value Chain Analysis

The UK fruits and vegetables value chain covers input suppliers (seed, substrate, crop protection, irrigation, and protected-cropping equipment), primary production (open-field and controlled-environment horticulture), post-harvest handling (grading, packing, and storage), wholesale and foodservice distribution, and retail-led merchandising. Import dependence remains a structural feature, with around 65% of supply coming from imports in 2024, versus about 35% from domestic production. This increases exposure to border processes, refrigerated logistics capacity, and climate-related volatility in supplier regions.

Retailers and large packers influence outcomes through specifications, service levels, and contracting practices, while trade associations and grower bodies participate in governance and assurance discussions. Defra has been developing mandatory regulations for fresh produce contracts under section 29 of the Agriculture Act 2020 to address contractual unfairness and improve transparency, which can shift how risks and costs are allocated across growers, intermediaries, and retailers. On logistics, concentration risk persists, with approximately 29% of imported fruit and vegetables entering via the Short Straits in 2023, strengthening the case for diversified routing, resilient cold chain capacity, and tighter inventory planning for perishables.

Market Opportunities and Future Outlook

Controlled-environment agriculture and low-carbon protected cropping continue to be a key route for import substitution and year-round availability, supported by concrete project progress and planning approvals. In April 2026, Essex County Council granted planning permission for the GBP 150 million Rivenhall Greenhouse project, a 40-hectare site positioned to supply large volumes of tomatoes. March 2026 also brought financial close for the GBP 86 million Fenland Greenhouse project via AGR Renewables with Greencoat Capital, targeting year-round cucumber production. Together, these initiatives create adjacent opportunities across greenhouse engineering, low-carbon heat integration, specialist substrates, crop IP, and packhouse upgrades tied to higher, steadier domestic throughput.

Labor scarcity and tighter service requirements are pushing adoption of automation and data-driven production practices, creating room for robotics, sensing, and packhouse automation. June 2026 grower-led trials such as the ADOPT Smart Pollination Project by AgriSound, and UK Berry Growers work using bioacoustic sensors and AI analytics across commercial strawberry farms, point to demand for scalable solutions in soft fruit. UK Agri-Tech Centre programs such as FLEXBOT, announced July 2026 with Antobot, University of Surrey, and Dogtooth Technologies, further reinforce the pull for decision support and mechanization. On the policy front, ongoing work on supply-chain fairness rules under the Agriculture Act 2020, alongside the government’s June 2026 Farming Roadmap 2050 (including a Farming and Food Partnership Board and horticulture growth planning) provides a clearer investment framework for productivity, energy efficiency, and resilience. Import compliance timelines through early 2027 also keep traceability and border-readiness tooling relevant for importers and packers.

Recent Industry Developments

- July 2026: Dogtooth Technologies raised more than GBP 14 million in growth capital to scale its robotic harvesting systems. The funding supports wider deployment of autonomous harvesting capabilities that address farm labor constraints in labor-intensive fruit and vegetable production. It also strengthens the UK agri-robotics supplier base serving commercial growers.

- June 2026: Suntory Beverage & Food GB&I partnered with Bevisol to open a GBP 14.5 million blackcurrant processing facility in Ledbury, Herefordshire. The investment expands domestic processing capacity for berry supply chains and supports more value capture within the UK horticulture ecosystem. It also raises quality and throughput requirements upstream for growers and logistics partners.

- May 2024: The UK government doubled horticulture funding to GBP 80 million annually under the Blueprint for Growing the United Kingdom Fruit and Vegetable Sector. The expanded funding base reinforced the policy direction toward increasing domestic supply and improving productivity across fresh produce operations. It also underpinned project pipelines in areas such as protected cropping, on-farm energy integration, and post-harvest infrastructure.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of fresh fruits and fresh vegetables consumed in the United Kingdom, including domestically supplied produce and imports sold through common trade channels in the country.

Scope exclusions: Processed, frozen, canned, dried, and ingredient-grade fruit and vegetable products are excluded from this sizing.

Segmentation Overview

- By Commodity Type

- Fruits

- Apple

- Strawberry

- Pear

- Raspberry

- Cherries

- Vegetables

- Carrot

- Cauliflower

- Onion

- Pea

- Tomato

- Cucumber

- Fruits

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with the most consistent public series that describe UK fresh produce availability, trade, and demand. We relied on sources such as DEFRA horticulture and food statistics, HM Revenue and Customs import and export data, the UK Office for National Statistics consumer price and household spending series, and FAOSTAT for long-run crop and supply context.

To translate supply and trade signals into market value, we also reviewed audited company filings, annual reports, and investor presentations from relevant growers, importers, wholesalers, and retailers where category wording could be mapped to fresh fruits and vegetables. In a few cases, paid subscriptions were used to speed up company financials screening, patent lookups linked to packaging and shelf life themes, and shipment-level import and export checks. The sources named here are illustrative, and other public and secondary references were used for cross-checking, validation, and clarifying definitions.

Primary Interviews and Surveys

Primary work focused on validating price realization and channel behavior for fresh produce, since that is where published numbers often drift. We spoke with a mix of growers and producer groups, importers, wholesalers, large retailers, and foodservice-linked buyers to confirm seasonality, sourcing splits, wastage assumptions, and typical markups from farmgate to retail.

Because this is a United Kingdom study, our discussions were structured around national supply flows and major consumption hubs, then used to stress-test the desk assumptions before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | |

| Mid tier: 55% | Functional/Unit leaders: 34% | |

| Smaller Players: 16% | Managers: 50% |

Market-Sizing & Forecasting

Sizing was built using a top-down and bottom-up mix. We first used production and import and export series to reconstruct the fresh fruits and vegetables supply available for UK consumption, and then valued it using observed price indicators. When the data series did not align across products or seasons, the steps were kept simple and the assumptions were documented so they can be repeated.

Key inputs included fresh produce production volumes, import and export values and volumes, retail food price movements, seasonal availability patterns for key items, and observed wastage and shrink norms along the cold chain. These variables help separate demand changes from price inflation, and they also help avoid counting re-exports or trade timing effects as consumption.

Forecasts used scenario analysis anchored to the historical trend line. Drivers were adjusted using expert feedback on expected sourcing patterns, weather-related volatility, labor availability, and likely retail pricing behavior. Bottom-up checks were then used selectively, such as sampled price per kilogram by high-volume items and channel checks on typical margin bands. Any gaps were handled by conservative interpolation rather than forcing granular roll-ups that cannot be validated consistently.

Data Validation & Update Cycle

Validation was done through cross-checks, followed by analyst review before sign-off. We compared model outputs with independent signals such as trade balances, price indices, and broad retailer category commentary, and then investigated any sharp jumps that could be caused by short-term supply shocks or currency conversion timing.

If an outlier could not be explained with available evidence, assumptions were revisited and a targeted re-contact was triggered with industry participants to confirm the direction of change. Reports are refreshed annually, and interim updates are made when material events materially shift supply, pricing, or import dependence. Before delivery, the latest public data releases are re-checked so clients receive an updated view aligned to the most recent signals.

Mordor Intelligence's United Kingdom Fruits and Vegetables Market Size Versus Other Published Estimates

Published market sizes for UK fresh fruits and vegetables can differ even when they sound similar, since the cut between fresh and non-fresh, the treatment of trade flows, and the price basis used are not always consistent. Differences also show up when one estimate relies on a single pricing proxy, or when the refresh cycle misses a year with unusual import pricing or weather impacts.

Import and export values and volumes, along with observed fresh produce price movements, are the checks that keep Mordor Intelligence's USD 18.3 B (2025) estimate tied to UK consumption, rather than being pulled upward by processed formats or broader grocery totals. The remaining spread versus other figures usually comes from mixing retail value with farmgate value without a clear bridge, or applying aggressive price escalation that does not match what buyers report in contracts.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 18.3 B (2025) | |

| Industry Association A | USD 16.9 B (2025) | Uses a narrower product basket for fresh produce and applies more conservative pricing that can sit closer to farmgate levels for part of the mix, which reduces the total versus a full retail-value view. |

| Trade Journal B | USD 21.4 B (2025) | Blends fresh produce with adjacent non-fresh forms and uses faster price uplift assumptions, which can inflate totals in years with elevated food inflation and import cost volatility. |

Taken together, the table shows that scope boundaries and price application explain most of the difference across sources. Our model stays easier to audit because it starts from supply and trade availability, then values the pool with stated price indicators, and finally runs variance checks before the forecast is extended.

Key Questions Answered in the Report

What is the current value of the United Kingdom fruits and vegetables market?

The market is valued at USD 19.02 billion in 2026.

How fast is the market projected to grow?

It is projected to grow at a 3.95% CAGR to 2031.

Which commodity type holds the largest share?

Fruits lead with 55.60% share in 2025.

What is the main labor challenge for growers?

Post-Brexit seasonal worker shortages continue to limit harvest capacity.

Page last updated on: