South Africa Fruits And Vegetables Market Analysis by Mordor Intelligence

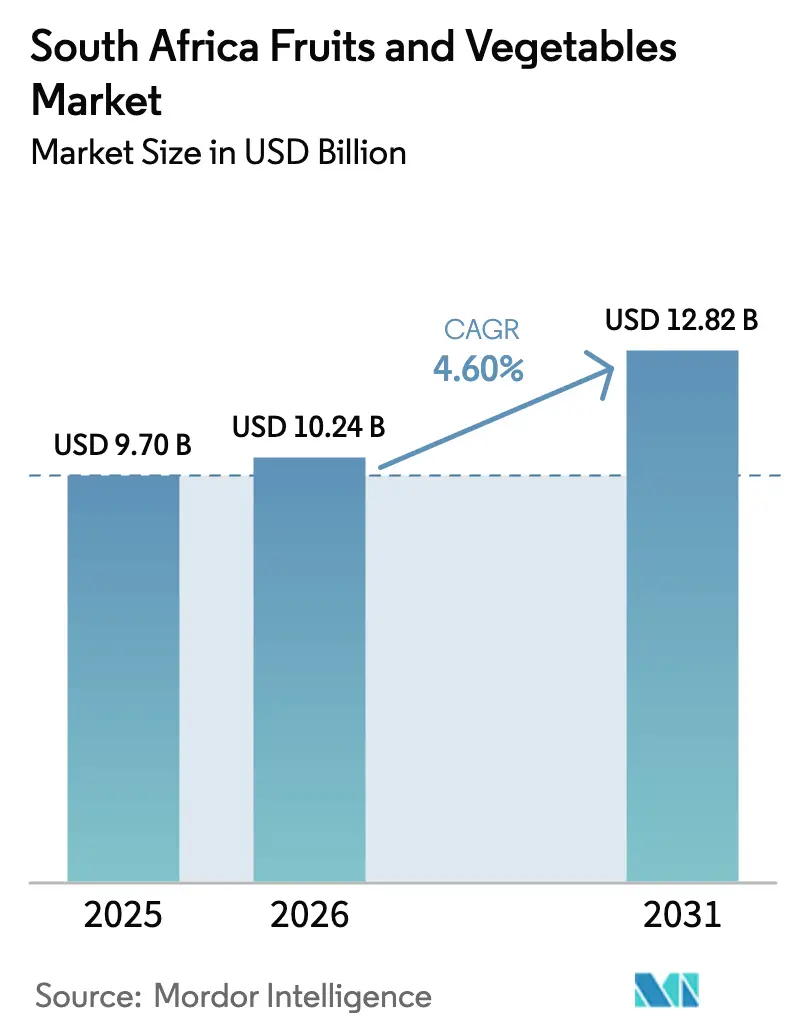

The South Africa fruits and vegetables market size was valued at USD 9.70 billion in 2025 and estimated to grow from USD 10.24 billion in 2026 to reach USD 12.82 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031). Vegetables constitute a significant portion of the market, with potatoes, onions, and tomatoes being primary staples in domestic and regional trade. These vegetables play a crucial role in meeting the population's dietary needs and are integral to the agricultural economy. Conversely, the fruit segment is projected to experience growth, supported by the export of premium citrus, avocados, and table grapes to Europe and Asia. This growth is attributed to increasing global demand for high-quality fruits and the expansion of export-oriented farming practices. Profit margins are being bolstered by government-backed agro-processing grants, new bilateral phytosanitary agreements, and the growing use of precision irrigation techniques, which improve water efficiency and crop yields. Challenges such as recurring droughts, water-use license restrictions, and non-tariff sanitary barriers remain obstacles to the agricultural sector's growth potential, requiring strategic interventions to mitigate their impact.

Key Report Takeaways

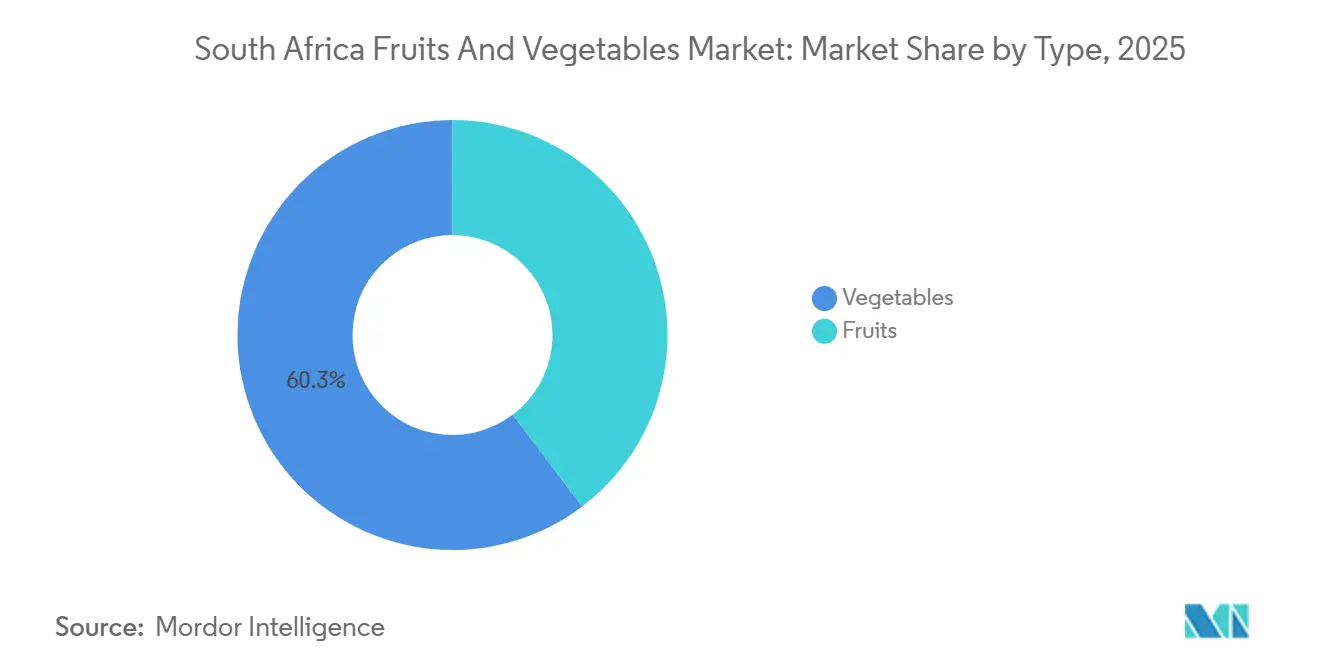

- By type, vegetables led with 60.3% of the South Africa fruits and vegetables market share in 2025. Fruits are forecast to expand at a 3.6% CAGR between 2026 and 2031, the fastest among product categories.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for nutrient-dense produce | +0.8% | Europe, United Kingdom, and Middle East | Medium term (2-4 years) |

| Government agro-processing incentives | +0.6% | National focus on Western Cape, Limpopo, and Mpumalanga | Short term (≤ 2 years) |

| Precision agri-tech and smart irrigation uptake | +0.7% | Early adoption in Western Cape and Limpopo | Medium term (2-4 years) |

| Controlled-atmosphere export logistics boost | +0.9% | Port hubs in Cape Town, Durban, and Gqeberha | Short term (≤ 2 years) |

| Cultivar-specific global marketing campaigns | +0.5% | Europe, Asia-Pacific, and Middle East | Long term (≥ 4 years) |

| Expansion of bilateral phytosanitary agreements | +1.0% | Vietnam, Philippines, India, and intra-Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Nutrient-Dense Produce

Soft-citrus exports, including mandarins and clementines, increased by 22% year-on-year, reaching 58.2 million cartons in 2024, as health-conscious European retailers favored easy-peel varieties[1]Source: Citrus Growers Association, “2024 Citrus Export Season Report,” cga.co.za. According to the ITC Trade Map, avocado exports totaled 82,784 metric tons in 2024, with the European Union accounting for nearly two-thirds of the volume. Domestic urban households followed a similar trend, increasing their purchases of vegetables and berries, which contributed to vegetable consumer inflation rising to 9.3% in August 2025. The high price elasticity enabled growers to offset rising fertilizer and diesel costs, particularly for premium products like blueberries and table grapes, which command price premiums exceeding 30% over conventional varieties. Retailers have aligned their procurement strategies with nutrient claims, establishing longer-term contracts that reduce market risks for large exporters and encourage smallholders to obtain GLOBALG.A.P. certification.

Government Agro-Processing Incentives

The Department of Agriculture, Land Reform, and Rural Development allocated ZAR 2.8 billion (USD 155 million) in 2024 to support cold-storage subsidies, pack-house upgrades, and export certification initiatives[2]Source: Department of Agriculture, Land Reform and Rural Development, “Agriculture and Agro-processing Master Plan Implementation,” dalrrd.gov.za. During 2024-2025, twelve new controlled-atmosphere facilities were established in the Western Cape and Limpopo, adding 8 million cubic feet of storage capacity, which extends the shelf life of apples and pears by six months. By mid-2025, the TITAN 2.0 digital traceability platform had achieved 95% adoption among exporters, resulting in an 18-hour reduction in port dwell times. Additionally, in 2023, smallholder-focused loans amounting to ZAR 450 million (USD 25 million) supported 1,769 beneficiaries cultivating 15,610 hectares under majority Black ownership, enabling compliance with stringent European retail standards. The introduction of faster fertilizer-import licensing in January 2025 addressed historical input bottlenecks and helped stabilize planting schedules.

Precision Agri-Tech and Smart Irrigation Uptake

The Council for Scientific and Industrial Research implemented drone-based imaging and soil sensors across 8,500 hectares in Limpopo and Mpumalanga, achieving a 24% reduction in irrigation water usage without compromising crop yields. In February 2025, Telkom’s Smart AgriTech pilot introduced fifth-generation mobile connectivity and Internet of Things (IoT) sensors to vineyards in the Western Cape, with plans to extend the technology to citrus farms by 2027. Aerobotics’ pest-prediction algorithms now safeguard 1.2 million hectares of local orchards, reducing chemical expenses by approximately 20%. Computer-vision graders analyze 26 images per fruit, significantly reducing manual labor requirements in citrus pack-houses by nearly two-thirds. However, cost challenges persist, with installation expenses ranging from ZAR 80,000 to ZAR 120,000 (USD 4,400–6,700) per hectare, while fourth-generation network limitations in rural Limpopo impede the use of real-time analytics.

Cultivar-Specific Global Marketing Campaigns

Industry bodies allocated ZAR 120 million (USD 6.7 million) in 2024 to promote Nadorcott mandarins, Forelle pears, and Hass avocados in Europe and the Middle East. Capespan introduced a blockchain label providing orchard-level carbon data, which premium retailers increasingly value. Premium product lines, such as Orri mandarins, achieved price increases exceeding 25% in European supermarkets during 2024. The South African Table Grape Industry (SATI) launched a R40 million (USD 2.2 million) campaign on Chinese e-commerce platforms in 2025, targeting mid-tier urban consumers. With over 200 export labels competing for shelf space, brand equity continues to lag behind competitors like Chile and Peru. Discussions regarding the adoption of a unified "Brand South Africa" logo remain ongoing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Non-tariff phytosanitary barriers | -0.8% | European Union and United States trade corridors | Long term (≥ 4 years) |

| Climate-induced droughts and heatwaves | -0.7% | Western Cape, Northern Cape, and Limpopo | Short term (≤ 2 years) |

| Water-use license constraints | -0.5% | Western Cape and Limpopo | Medium term (2-4 years) |

| Volatile currency exposure on imported inputs | -0.6% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Non-Tariff Phytosanitary Barriers

The European Union's cold-treatment protocols for citrus black spot increase costs by USD 0.08-0.12 per carton and delay shipments by up to one week, thereby raising working capital requirements. Temporary United States tariffs in 2025 resulted in penalties and contract renegotiations costing exporters ZAR 800 million (USD 44 million) before exemptions for citrus, avocado, and beef were reinstated. In China, avocado regulations exclude 40% of smallholders due to insufficient documentation capacity, leading to supply consolidation among vertically integrated players. Ongoing World Trade Organization arbitration with the European Union regarding citrus black spot creates significant uncertainty and compels exporters to maintain destination-specific pack-lines, increasing fixed overhead costs by up to 20%.

Climate-Induced Droughts and Heatwaves

In December 2024, Western Cape dam levels declined to 62% of their capacity, resulting in a 25% reduction in irrigation and a 9% decrease in apple production, which dropped to 35.8 million cartons[3]Source: Department of Water and Sanitation, “Water-Use Allocation Reports 2024,” dws.gov.za. The reduced water availability significantly impacted agricultural operations, forcing farmers to adopt water-saving measures and prioritize high-value crops. Heat events exceeding 40 degrees Celsius in Limpopo and Mpumalanga accelerated citrus maturation, shortening harvest windows by two weeks and increasing labor costs by 15%. This compression of harvest periods created logistical challenges, including the need for additional labor and faster processing to prevent spoilage. The South African Weather Service forecasts a 30%-40% increase in extreme heat events by 2030, driving the need for shade-netting investments estimated at ZAR 150,000-250,000 (USD 8,300-13,900) per hectare.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Vegetables Anchor Domestic Demand

Vegetables accounted for 60.3% of South Africa's fruits and vegetables market share in 2025, driven by substantial domestic consumption and robust cross-border trade within the Southern African Development Community. According to the North West Department of Agriculture and Rural Development, in 2025, potatoes led certified exports, with 24.45 million kilograms, followed by onions and butternut squash, with Botswana and Namibia being the key importers. Despite drought-related supply challenges and elevated diesel-driven logistics costs, retail inflation of 9.3% in 2025 highlights resilient demand. Hydroponic tomato facilities near Johannesburg and Cape Town ensure a year-round supply to supermarkets, reducing the seasonal dependency on imports.

Fruits are the fastest-growing segment, projected to grow at a 3.6% CAGR through 2031, surpassing staple vegetables and contributing an increasing share to South Africa's fruit and vegetable export earnings. Citrus exports reached 171.5 million cartons in 2024-2025, with mandarins and clementines showing the highest growth. Investments in cold-chain infrastructure and cultivar promotions in Asia aim to regain market momentum. Apples and pears face intensified competition from Latin American suppliers, but the adoption of genetically modified long-storage cultivars could help reclaim premium market positions.

Geography Analysis

The Western Cape accounted for 92% of the national pome-fruit production and 94% of table-grape and stone-fruit volumes in 2024. This was supported by its Mediterranean climate, extensive cold-chain infrastructure, and proximity to the ports of Cape Town and Gqeberha (formerly known as Port Elizabeth). Water-allocation reductions in the Berg and Olifants catchments necessitated the adoption of precision drip irrigation systems, costing between ZAR 80,000 and 120,000 (USD 4,400–6,700) per hectare. These costs were partially offset by increased pack-house automation, which reduced labor costs and improved product quality, enabling premium pricing.

Limpopo and Mpumalanga contributed 52% of the national citrus production in 2025, with 101,624 hectares of citrus orchards supplying the Durban port corridors for exports to Europe and the Middle East. The region's subtropical climate allows for staggered harvesting over eight months, optimizing packhouse utilization. Delays in license renewals and rising water tariffs have created investment uncertainties. As a result, some growers are diversifying into macadamia and mango orchards to mitigate risks if regulatory clarity does not improve.

The Eastern Cape and KwaZulu-Natal regions offer significant growth potential. In 2024, government grants totaling ZAR 450 million (USD 25 million) financed the construction of four new cold storage facilities and the refurbishment of eight packhouses, aiming to reduce spoilage by 20% by 2027. The African Continental Free Trade Area facilitated exports worth ZAR 1.386 billion (USD 77 million) from South Africa's fruit and vegetable market to Ghana and Kenya between January and July 2025. This suggests that coastal provinces could serve African markets more competitively compared to Western Cape exporters, who face higher costs due to longer road transport distances.

Competitive Landscape

Companies such as Westfalia Fruit, Capespan Group, and Dutoit Group collectively managed over 45% of certified export cartons in 2025. These firms leverage multi-country orchard portfolios, advanced pack-house robotics, and exclusive European retail contracts to maintain their market positions. The integration of advanced technologies and strategic partnerships has been pivotal in shaping the market's competitive landscape.

Technology scale serves as a significant competitive advantage in the market. Westfalia Fruit secured a USD 300 million revolving credit facility in 2023 to fund orchard upgrades across five continents. Additionally, the acquisition of Belgian processor Syros in January 2025 has enabled the company to expand into higher-margin guacamole and frozen product formats. Capespan Group, on the other hand, has implemented blockchain-enabled labeling to meet retailer provenance requirements. This initiative aims to recover market share after an 8-10% volume decline during a period of restructuring.

Emerging competitors include cooperative smallholders supported by ZAR 450 million (USD 25 million) in blended capital. This funding facilitates GLOBALG.A.P. certification and provides direct access to supermarket supply chains. Aerobotics' pest-analytical tools, which now cover 1.2 million hectares nationally, offer cost advantages to users. The potential consolidation around a unified "Brand South Africa" export mark could enhance collective bargaining power in international markets, provided industry consensus is achieved.

Recent Industry Developments

- October 2025: South Africa's fruit industry shifted focus to Asian markets to offset the effects of newly imposed 30% tariffs on exports to the United States. These tariffs were introduced under a "reciprocal" trade policy implemented by the U.S. in August 2025, following the expiration of the African Growth and Opportunity Act (AGOA) in September of that year.

- October 2025: Maersk has inaugurated the Belcon Cold Store in Cape Town, a key facility designed to significantly enhance and expand South Africa's fruit export capacity. This initiative is part of a broader strategic investment exceeding USD 100 million in the country's cold chain infrastructure.

- October 2025: South Africa has signed a significant trade protocol with China in Shanghai, granting access for South African stone fruit to the Chinese market for the first time. The agreement was signed by the South African Minister of Agriculture and the head of China's General Administration of Customs (GACC).

- February 2025: Telkom, in collaboration with Stellenbosch University and Aizatron, launched Smart AgriTech, utilizing fifth-generation networks and sensors to reduce irrigation water usage by 20% in Western Cape vineyards. This initiative aims to enhance water efficiency and sustainability in agriculture by leveraging advanced technology to monitor and optimize irrigation processes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the South African fruits and vegetables market as the value of fresh, whole produce picked, graded, and traded in domestic wholesale, retail, and export channels during the calendar year. Harvests diverted to on-farm animal feed or further processing (frozen, dried, juiced, canned, or powdered) are counted only up to the point of fresh produce sale.

Scope exclusion: processed derivatives beyond the first fresh sale are deliberately left outside this sizing.

Segmentation Overview

- By Type

- Vegetables

- Potatoes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Onions

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Tomatoes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Carrots

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Cabbage and Brassicas

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Pumpkins and Squash

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Others (Spinach, Sweet Corn, etc.)

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Potatoes

- Fruits

- Citrus (Oranges, Lemons/Limes, Grapefruit)

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Apples and Pears

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Grapes

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Avocados

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Bananas

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Stone Fruits

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Exotic and Other Fruits (Dragon Fruit, Passion Fruit, etc.)

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destination Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis

- Citrus (Oranges, Lemons/Limes, Grapefruit)

- Vegetables

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed commercial farmers, market agents at the four largest national fresh markets, procurement managers at leading food retailers, and agri-exporters in Western Cape and Limpopo. These conversations clarified planting intentions, post-harvest loss rates, and average free-on-board prices, which we then reconciled with desk figures to refine conversion factors and stress test assumptions.

Desk Research

We drew on national data sets such as Statistics South Africa crop surveys, the Department of Agriculture's export inspections, and the National Agricultural Marketing Council's fresh produce market bulletins, which together map output, prices, and trade flows. Trade body portals, including Citrus Growers Association and Potatoes SA, provided cultivar-level shipment splits that sharpen provincial demand patterns. Macro series from the South African Reserve Bank, FAOSTAT, and UN Comtrade anchored currency, inflation, and bilateral trade. To enrich company intelligence, our team accessed D&B Hoovers and Dow Jones Factiva for distributor revenues and expansion news. These examples are illustrative; many additional public and paid sources were consulted during validation.

A second sweep covered climate journals and peer-reviewed irrigation studies to gauge rainfall deviations and water cost pressure likely to sway margins over the outlook period. We believe this lens keeps the desk review practical yet sufficiently granular for market modeling.

Market Sizing and Forecasting

We built a top-down demand pool that begins with provincial production tonnage, net exports, and import substitution; volumes are multiplied by weighted average farm-gate prices and then cross-checked through selective bottom-up supplier roll-ups. Key variables in the model include per capita fresh produce intake, citrus and table grape export volumes, producer price inflation, rainfall anomalies, and retail penetration of formal supermarkets. A multivariate regression was applied to project each driver through 2030, with coefficients vetted by interviewed experts. Any data gaps, particularly in informal trade, were bridged using calibrated ratios from comparable provinces before final triangulation.

Data Validation and Update Cycle

Our outputs pass a two-step senior analyst review, followed by anomaly checks against independent trade statistics. The dashboard is refreshed annually; ad hoc updates are triggered when exchange rate swings, extreme weather, or trade policy shifts move the market materially.

Why Mordor's South Africa Fruits and Vegetables Baseline Commands Reliability

Published estimates differ, and buyers often struggle to reconcile them. Divergences usually stem from inconsistent scope, differing exchange rate benches, and infrequent refresh cycles.

Key gap drivers here include whether processed forms are included, if informal sales are captured, and the point in the chain at which value is booked. Our team reports the fresh only value for 2025 at USD 8.5 billion, based on transparent farm-gate metrics, annual refresh, and local currency conversion at actual realized rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.5 B (2025) | Mordor Intelligence | - |

| USD 14.0 B (2024) | Global Consultancy A | Includes frozen, dried, and processed lines; allocates MEA totals down by GDP weight |

| USD 2.38 B (2024) | Regional Consultancy B | Focuses on formal retail turnover only; omits farm-gate and direct export values |

The comparison shows that wider scopes inflate figures, while narrow retail only cuts them sharply. Mordor's disciplined selection of fresh only value, verified drivers, and yearly updates delivers a balanced, repeatable baseline decision makers can trust.

Key Questions Answered in the Report

How large is the South Africa fruits and vegetables market in 2026 and how fast will it grow?

The market reached USD 10.24 billion in 2026 and is set to grow to USD 12.82 billion by 2031 at a compound annual growth rate of 4.60%.

Which product category currently holds the largest share?

Vegetables lead with 60.3% of South Africa fruits and vegetables market share in 2025, supported by staple demand for potatoes, onions, and tomatoes.

Which category is expanding the fastest?

Fruits, especially citrus, avocados, and table grapes, are projected to expand at a 3.6% CAGR through 2031 due to premium export demand.

Which province contributes most to export-oriented horticulture?

Western Cape dominates pome fruit, table grapes, and stone fruit while Limpopo and Mpumalanga lead in citrus, reflecting distinct regional specialization.

What are the main risks facing growers?

Key risks include European Union and United States sanitary barriers, drought-related water restrictions, rising irrigation tariffs, and exchange-rate volatility on imported inputs.

Which companies command the largest infrastructure footprint?

Vertically integrated groups such as Westfalia Fruit, Capespan Group, and Dutoit Group collectively process about 45% of certified export cartons and possess extensive pack-house and cold-chain capacity.

Page last updated on: