Mexico Fruits And Vegetables Market Analysis by Mordor Intelligence

The Mexico fruits and vegetables market size is projected to expand from USD 28.4 billion in 2025 and USD 29.6 billion in 2026 to USD 37.9 billion by 2031, registering a 5.07% CAGR between 2026 and 2031. Liberalized trade under the United States–Mexico–Canada Agreement has made Mexico the principal winter-window supplier to North American retailers, creating stronger price signals for greenhouse tomatoes, bell peppers, and cucumbers. Simultaneously, domestic shoppers are buying more washed and cut vegetables along with premium berries, a shift that channels capital toward high-tech packing houses near large cities. Export-led berry plantings in Jalisco and Michoacán are growing 4 times faster than acreage for domestic staples, and cold-chain start-ups are compressing post-harvest losses to 19%, thereby raising delivered quality and extending shelf life. Competitive intensity remains low with the top five players accounting for a limited share of Mexico fruits and vegetables market size, leaving mid-tier cooperatives and technology-oriented newcomers room to scale through crop specialization and automation.

Key Report Takeaways

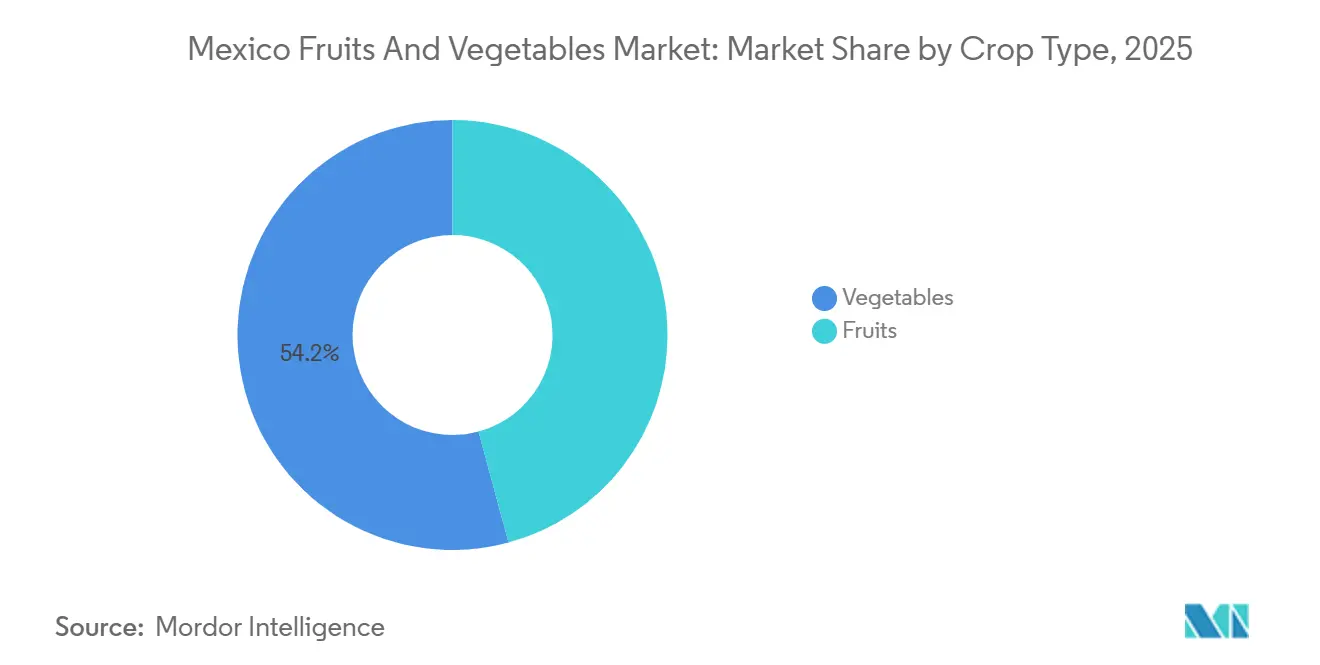

- By crop type, vegetables led with 54.2% of Mexico fruits and vegetables market share in 2025, while fruits are forecast to post the fastest growth at a 6.0% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising United States import demand post-United States-Mexico-Canada Agreement (USMCA) | +1.2% | Sinaloa, Sonora, Baja California, Jalisco, and Michoacán | Medium term (2–4 years) |

| Expansion of greenhouse/protected cultivation acreage | +1.0% | Bajío, Northwest, and Zacatecas | Long term (≥ 4 years) |

| Government production-linked subsidies and social-program purchases | +0.7% | Oaxaca, Chiapas, and Puebla | Short term (≤ 2 years) |

| Cold-chain logistics start-ups lowering post-harvest losses | +0.5% | Export corridors to Nogales, and Laredo, McAllen | Medium term (2–4 years) |

| Export-oriented berry acreage boom | +0.9% | Jalisco, Michoacan, and Baja California | Medium term (2–4 years) |

| Niche growth of organic banana clusters in Chiapas and Tabasco | +0.3% | Chiapas and Tabasco | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising United States Import Demand Post-United States–Mexico–Canada Agreement (USMCA)

While the United States–Mexico–Canada Agreement (USMCA) maintained duty-free access under the North American Free Trade Agreement (NAFTA), Mexican horticultural imports accounted for 34% of U.S. agricultural imports from Mexico in 2024, underlining the Mexico fruits and vegetables market’s reliance on cross-border demand. The 25% universal tariff imposed in early 2025, along with the end of the Tomato Suspension Agreement, has disrupted these trade flows [1]Source: USDA Economic Research Service, “U.S.–Mexico Fruit and Vegetable Trade 2025,” ers.usda.gov. In 2025, from November to April, Mexican growers supply 90% of U.S. fresh tomato imports, so any tariff shock quickly ripples through the Mexico fruits and vegetables market’s winter-window revenue. The July 2025 termination of the Tomato Suspension Agreement and a 17.09% anti-dumping duty have reduced seasonal pricing leverage, leading to a 25% drop in 2026 plantings in regions like Sinaloa. Rules-of-origin clauses preferentially treat Mexican produce over Central American re-exports, steering North American retailers toward direct contracts. Trade policy certainty is therefore catalyzing greenhouse investment and reshaping regional cropping patterns, with long-run implications for the Mexico fruits and vegetables market’s capacity mix.

Expansion of Greenhouse and Protected Cultivation Acreage

By 2025, Mexico's protected agriculture sector is set to reach nearly 78,000 hectares, with the Bajío region and states like Sinaloa and Jalisco as key hubs for this USD 8 billion industry [2]Source: Servicio de Información Agroalimentaria y Pesquera, “Mexico Agricultural Production Statistics 2025,” gob.mx, a footprint that directly enlarges the Mexico fruits and vegetables market. Netafim precision irrigation enables high-tech greenhouses to produce 250-600 metric tons of tomatoes per hectare, a 6- to 10-fold increase over traditional open-field yields of 37-75 metric tons. The adoption of Netafim precision irrigation systems in advanced greenhouses plays a critical role in the Mexican fruit and vegetable market's efforts to address climate variability and sustain its position as the world's seventh-largest agricultural exporter. Israeli irrigation suppliers and Dutch climate-control firms are partnering with Mexican cooperatives to install sensor networks that adjust fertigation in real time. Year-round output smooths pack-house utilization, reducing idle months and stabilizing labor demand, which ultimately supports supply consistency inside the Mexico fruits and vegetables market. The resulting margin lift encourages smaller growers to lease land to greenhouse operators, gradually bifurcating the supply base while expanding total marketable volume.

Government Production-Linked Subsidies and Social-Program Purchases

In 2025, the Agriculture and Rural Development Secretariat (SADER) launched the Fertilizers for Wellbeing program, allocating 23.8% of its MXN 74.5 billion (USD 4.32 billion) budget to distribute 1 million tons of free fertilizer to over 2 million smallholders across 3.3 million hectares, bolstering cost structures within the Mexico fruits and vegetables market. Food-bank procurement under Sembrando Vida absorbed 340,000 metric tons of produce, granting growers a reliable off-take at administered prices. These transfers shield ejido cooperatives in Oaxaca and Chiapas from commodity price swings, allowing them to continue planting during downturns. Traceability clauses tied to subsidies push small farms toward formal record-keeping, which serves as a stepping stone toward export certification and wider market access. Critics fear that blanket incentives may induce overproduction of low-value crops, yet political momentum makes program rollback unlikely before 2031, suggesting continued government influence on market supply dynamics.

Export-Oriented Berry Acreage Boom

Between 2020 and 2025, Mexican berry acreage stabilized at 48,000 to 50,000 hectares as the industry adopted high-yield genetics, maintaining a sizable fruit platform inside the Mexico fruits and vegetables market. Blueberries and raspberries drove growth, with raspberry planted area reaching 11,220 hectares in 2025 [3]Source: USDA Foreign Agricultural Service, “Mexico Fresh Fruit and Vegetable Annual Report 2025,” fas.usda.gov. Jalisco alone planted 7,200 new hectares, financed by retailer contracts that guarantee USD 8.50 per kilogram for certified organic fruit. International buyers are seeking to diversify away from drought-stricken California, so high-altitude Michoacán orchards that require less irrigation are attracting capital. Multi-year agreements from Driscoll’s and Hortifrut de-risk the three-year maturation lag for blueberry bushes, spurring rapid conversion of vegetable plots. Overlapping harvest windows for blueberries and raspberries have tightened seasonal labor, pushing wages 40% higher and accelerating interest in mechanized pickers that help sustain export reliability, a critical pillar of the Mexico fruits and vegetables market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Farm-labor shortages and rising rural wages | -0.8% | Sinaloa, Sonora, and Jalisco | Short term (≤ 2 years) |

| Climate volatility prolonged droughts and hurricanes | -0.6% | Northwest and Pacific Coast | Medium term (2–4 years) |

| Strong peso compressing exporter margins | -0.5% | Sinaloa, Michoacan, Jalisco, and Baja California | Short term (≤ 2 years) |

| Tomato Brown Rugose Fruit Virus recurrence in Sonora and Sinaloa | -0.3% | Sonora and Sinaloa greenhouses | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Climate Volatility, Droughts, and Hurricanes

Severe drought in Sinaloa during 2024 reduced reservoir levels to as low as 3% by mid-year, cutting 2025 vegetable production forecasts by 3% and driving a shift to protected agriculture to counter open-field yield losses that threaten overall supply for the Mexico fruits and vegetables market. After Hurricane Otis in 2023 damaged over 20,000 hectares of crops in Guerrero, Mexican growers are adopting drought-tolerant agave as an alternative to traditional staples. However, the high costs of climate-adaptive infrastructure, such as wind-resistant systems, remain a challenge for small-scale farmers. Mexico's sovereign parametric insurance program, scaled from a 10,000-farmer pilot, aims to cover 200,000 smallholders by 2026. Despite premiums of 4.5% of insured value, its automated payouts for rainfall and wind events are narrowing the climate protection gap. Climatic extremes, therefore, introduce revenue volatility that can deter long-term investment, constraining capacity expansion in the Mexico fruits and vegetables market.

Strong Peso Compressing Exporter Margins

Between January 2025 and early 2026, the Mexican peso appreciated from 20.59 to 17.20 per U.S. dollar, reducing peso-denominated receipts for agricultural exporters by narrowing the currency conversion margin, a direct profitability squeeze on the Mexico fruits and vegetables market’s export segment. A metric ton of tomatoes that sold for MXN 20,160 (USD 1,167.81) in 2025, down from MXN 21,840 (USD 1,265.12) two years earlier. While dollar-denominated debt costs declined, most growers pay wages and inputs in pesos, so net margins narrow. Hedging tools such as forward contracts remain inaccessible to small cooperatives unfamiliar with derivatives markets. Persistent strength in the peso could accelerate a shift toward organic or specialty crops that command foreign-currency premiums, partially offsetting margin pressure but also reshaping product mix in the Mexico fruits and vegetables market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Diverging Momentum Between Vegetables and Berries

Vegetables led Mexico fruits and vegetables market share with 54.2% in 2025, owing to year-round greenhouse output of tomatoes, bell peppers, and cucumbers. In contrast, fruits are the fastest-growing segment, advancing at a 6.0% CAGR to 2031 on the strength of blueberry and raspberry plantings in Jalisco and Michoacán. Robust U.S. demand during winter months sustains premium pricing for greenhouse vegetables, while multi-year retailer contracts lock in volume for organic berries. Together, these dynamics show how protected cultivation and export agreements shape both the dominant share leader and the highest-growth category.

Tomatoes continue to dominate individual crop rankings but face compliance costs tied to Tomato Brown Rugose Fruit Virus testing, which erode margins for open-field growers. Bell peppers and cucumbers benefit from lighter trade scrutiny, and their mini-cucumber niche is expanding in organic aisles across the United States. Avocado exports remain sizable but are growing only 2.1% annually because land and security constraints slow new orchard development in Michoacán. Persian limes from Veracruz and Colima fill a supply gap left by Florida citrus greening, yet their overall contribution remains smaller than berries, underscoring the crop-mix shift toward higher-margin fruit clusters.

Geography Analysis

West-Central Mexico accounted for significant share of national revenue in 2026, driven by Jalisco berries and Michoacan avocados. Proximity to the Port of Manzanillo and direct highways to Laredo shortens transit times and raises delivered freshness. The Bajío region is the fastest-growing territory, projected to expand at a rapid CAGR through 2031 as new greenhouses multiply in Guanajuato and Querétaro. Investors favor Bajío sites because central geography cuts freight costs to both Mexico City and northern border crossings, improving margins for year-round shipments.

Northwest Mexico, anchored by Sinaloa and Sonora, remains the winter vegetable hub that supplies United States stores from November to April. Drought in 2024 and virus protocols have trimmed tomato yields, but greenhouse clusters near Hermosillo continue to upgrade climate control to stabilize output. Southern states such as Chiapas and Oaxaca focus on organic bananas and heirloom tomatoes that win premiums in the European Union. Veracruz and Colima sustain steady lime exports, capitalizing on Florida citrus disease to keep packhouses operating at near capacity.

West-Central cooperatives are installing drip irrigation and shade nets that lower water use and protect berries from heat spikes. Bajío operators deploy sensor-guided fertigation to boost greenhouse yields and meet the demands of premium grocers for uniform produce. Northwest growers are adding controlled-atmosphere storage near Culiacan to offset climatic shocks and extend shelf life for Midwest deliveries. Progress across these corridors shows that logistics and technology upgrades will keep regional output climbing and widen Mexico's fruit and vegetable market reach through 2031.

Competitive Landscape

By company concentration, the top five players together accounted for a decent share Mexico fruits and vegetables market in 2025. Result of Hortifrut México, Lineage Logistics, and Grupo Alt. Grupo Driscoll’s de México and Wonderful Citrus are the two largest branded exporters, which together account for a decent share of Mexico fruits and vegetables market, driven by proprietary berry genetics and large-scale lime estates, respectively. Both firms leverage multi-year retailer contracts that guarantee floor prices in exchange for exclusive supply, stabilizing cash flows and funding continuous research and development. Their packing facilities integrate optical sorters and near-infrared sensors to enforce the uniformity demanded by premium grocers. As a result, these firms set quality benchmarks that smaller growers must meet to enter club-store channels.

Hortifrut has accelerated blueberry plantings in Jalisco and Michoacán, while Lineage captures value through fee-based controlled-atmosphere storage rather than owning farmland. Grupo Alta is converting 600 hectares of Sonoran table grapes to organic protocols, targeting the European Union, and differentiating through sustainability labels. None of these firms spans every crop, reinforcing a structure where scale advantage remains crop-specific rather than market-wide. Competition is evolving along two axes, including technological sophistication and certification depth.

Large growers integrate robotics and machine vision to offset labor shortages, whereas mid-tier cooperatives pursue Fair Trade, Rainforest Alliance, and organic seals to reach high-margin niches. Cold-chain specialists plan additional ammonia-based warehouses in Baja California to serve the Nogales corridor, a move that could lock up logistics capacity and raise entry barriers. Private equity interest in protected agriculture and infrastructure signals an approaching consolidation wave that may lift the market concentration score modestly by 2031.

Recent Industry Developments

- January 2026: The Ministry of Agriculture and Rural Development (SADER) in Mexico launched a MXN 2.7 billion (USD 153.9 million) Fair Trade program that guarantees floor prices and infrastructure grants for small and medium farmers of white corn, bread wheat, rice, beans, coffee, cocoa, honey, and key vegetables, aiming to raise rural incomes and cut reliance on intermediaries in marginalized regions.

- September 2025: Multilateral lender IDB Invest arranged USD 130 million in long-term and revolving credit for Dinvertech to install 50 hectares of high-tech greenhouses for mini-pepper production, targeting 97% export volumes and creating jobs for rural women while implementing climate-smart fertigation in water-scarce Bajío zones.

- December 2024: SL Produce unveiled a 2025 expansion plan that scales vegetable acreage, adds precision-agriculture tools, and installs new packing and cold-storage lines to support its Tenderland-branded products for U.S. customers.

Mexico Fruits And Vegetables Market Report Scope

Fruits and vegetables include various edible parts of plants, such as fruits, leaves, stems, shoots, and roots. These plant parts can be cultivated or collected from the wild and are usually consumed raw or with minimal processing. The Mexican market for fruits and vegetables is divided by crop type into two main categories such as fruits and vegetables. This report provides a comprehensive analysis of the production (in volume), consumption (both in volume and value), imports (in volume and value), exports (in volume and value), and price trends of fruits and vegetables in Mexico. Additionally, the report presents market estimates and forecasts, detailing both volume (in metric tons) and value (in USD million) for the studied segment.

By Crop Type

| Fruits | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Vegetables | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destinations Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| By Crop Type | Fruits | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Vegetables | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destinations Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

How fast is the Mexico fruits and vegetables market growing through 2031?

It is projected to register a 5.07% CAGR between 2026 and 2031, rising from USD 29.6 billion in 2026 to USD 37.9 billion by 2031.

Which segment leads revenue within the Mexico fruits and vegetables market?

Vegetables, anchored by tomatoes, bell peppers, and cucumbers, accounted for 54.2% of revenue in 2025.

Which crop group is expanding the quickest?

Fruits, especially blueberries and raspberries, are advancing at a 6.0% CAGR to 2031 on the back of export contracts with U.S. retailers.

What is the biggest operational risk facing growers?

Labor shortages that lifted daily harvest wages by 40% between 2023 and 2025, prompting investment in robotic pickers.

How concentrated is the competitive landscape?

The top five grower-exporters together control about a descent of revenue, reflecting moderate fragmentation and opportunities for mergers.

Page last updated on: