Canada Fruits And Vegetables Market Analysis by Mordor Intelligence

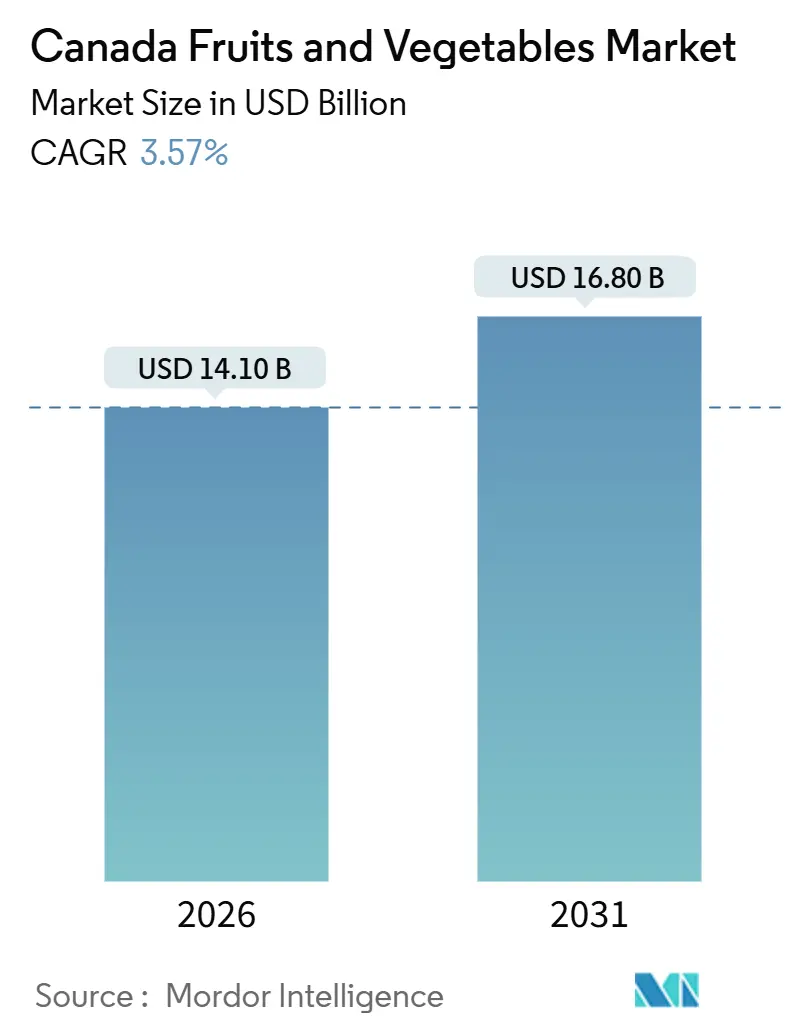

The Canada fruits and vegetables market size reached USD 14.10 billion in 2026 and is projected to climb to USD 16.80 billion by 2031, advancing at a 3.57% CAGR during the forecast period. Yield intensification, rather than acreage gains, is the primary growth lever, as greenhouse area has been increasing in recent years, underscoring the productivity dividend of controlled-environment agriculture (CEA). Federal subsidy programs, including AgriStability and AgriInvest, delivered more than CAD 2.0 billion (USD 1.5 billion) of support in 2024, helping to cushion growers against climatic shocks and price fluctuations. Locally grown produce with provenance resonates strongly with consumers, with 88% of shoppers in Quebec and 84% in British Columbia seeking domestic produce, although price sensitivity persists, prompting retailers to balance premium in-season supply with lower-cost imports during the shoulder months[1]Source: Agriculture and Agri-Food Canada, “Consumer Trends in Fresh Fruits and Vegetables in Canada, 2024,” agriculture.canada.ca. Structural headwinds remain, including labor vacancies, tariff-rate quotas under the Canada-United States-Mexico Agreement (CUSMA), and weather volatility, all of which temper the pace of expansion. However, rising off-take from plant-based food processors and indigenous greenhouse initiatives open up fresh demand channels that reinforce the positive baseline outlook.

Key Report Takeaways

- By consumption, vegetables accounted for 54.8% of Canada fruits and vegetables market size in 2025, while fruits are forecast to post a 3.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Fruits And Vegetables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for locally grown produce | +0.7% | National, strongest in Quebec, British Columbia, and Ontario | Medium term (2-4 years) |

| Federal and provincial subsidy programs | +0.6% | National, jointly funded | Long term (≥ 4 years) |

| Expansion of controlled-environment agriculture | +0.9% | Ontario, British Columbia, and Quebec greenhouse clusters | Medium term (2-4 years) |

| Climate resilience and crop diversification strategies | +0.4% | British Columbia and Ontario | Long term (≥ 4 years) |

| Indigenous community-led horticulture projects | +0.2% | Northern Ontario, Nunavut, and remote First Nations territories | Long term (≥ 4 years) |

| Off-take demand from plant-based food processors | +0.5% | Prairie provinces and Ontario | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Preference for Locally Grown Produce

Surveys conducted in 2024 revealed that 88% of Quebec consumers and 84% in British Columbia prioritize domestic produce, with three-quarters willing to pay premiums averaging 12% above those for imported items. Higher-income households drive most of the uplift, widening the market for premium berries and organic apples while price-sensitive shoppers switch to imports when budgets tighten. Retailers respond with province-specific branding and “grown close to home” shelf tags that lift in-season velocity. Despite the enthusiasm, 62% of Canadians admit they will revert to cheaper imports during economic slowdowns, signaling that loyalty is conditional on price parity. Growers, therefore, rely on traceability technologies and direct-to-consumer channels to protect their margins without losing volume when exchange-rate shifts or logistics bottlenecks favor offshore supply.

Federal and Provincial Subsidy Programs

AgriStability and AgriInvest together transferred more than CAD 2.0 billion (USD 1.5 billion) to producers in 2024, yet only a minority of horticulture operators fully utilized the benefits, as reference-margin formulas and paperwork hurdles deterred enrollment. Tailored interventions at the provincial level help bridge some gaps, as British Columbia offered CAD 70 million (USD 51 million) for tree-fruit replanting after the 2024 freeze[2]Source: Government of British Columbia, “Province Supports Tree Fruit Growers with 70 Million CAD Replanting Program,” gov.bc.ca. Audits show 38% of eligible farms in Quebec and Atlantic Canada left funds on the table, highlighting an administrative barrier rather than a funding shortfall. Streamlined digital sign-ups and crop-specific indexing would unlock additional coverage, stabilizing income when pest outbreaks or tariff swings compress margins.

Expansion of Controlled-Environment Agriculture

Canada's greenhouse vegetable area reached 33.3 million square meters in 2024. Ontario’s Leamington-Kingsville corridor controls 56% of the national area, leveraging low-cost natural gas and proximity to Detroit distribution hubs. Yield consistency is key, with greenhouse tomatoes capable of delivering 60-80 kg/m² annually, compared to 8-12 kg for field crops, enabling dependable winter volumes that crowd out Mexican imports. Capital intensity remains high, as building a 10-hectare glasshouse costs CAD 30-40 million (USD 22-30 million). Yet, payback is compressed to roughly eight years as energy prices normalize post-2023 and retailers widen pesticide-free premiums.

Indigenous Community-Led Horticulture Projects

Federal programs supporting food sovereignty have financed dozens of 500 to 2,000-square-meter hydroponic greenhouses in northern Ontario and Nunavut, thereby reducing reliance on air-freighted imports that historically carried spoilage rates above 15%[3]Source: Indigenous Services Canada, “Community-Based Climate Monitoring Program,” sac-isc.gc.ca. A 2024 Kuujjuaq pilot produced 3.2 metric tons of lettuce in eight months and cut household produce spending by an estimated 18%. High diesel energy costs and seasonal supply lags for substrates complicate operations; however, projects foster local employment and a nascent Arctic horticulture skill base. Long-term continuity hinges on multi-cycle funding, as most grants expire within five years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climatic volatility and extreme weather | -0.8% | National, acute in British Columbia, Prairies, and Atlantic Canada | Short term (≤ 2 years) |

| Farm-labor shortages and rising wages | -0.6% | National, most severe in Ontario and British Columbia greenhouses | Medium term (2-4 years) |

| Seasonal tariff gaps under the Canada-United States-Mexico Agreement | -0.4% | National, concentrated in Ontario and Quebec | Short term (≤ 2 years) |

| Refrigerated logistics bottlenecks in remote areas | -0.3% | Northern Ontario, Atlantic provinces, and Prairie rural zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climatic Volatility and Extreme Weather

British Columbia’s January 2024 freeze destroyed entire stone-fruit crops and 85% of sweet cherries, inflicting more than CAD 700 million (USD 500 million) in losses. Drought stress affected 70% of the country's farmland in 2024, resulting in a 12% reduction in Atlantic berry yields. Prairie potato growers faced water allocation cuts of 20-30%, forcing acreage abandonment. Frost fans, hail netting, and drip systems are shifting from optional to mandatory, yet, at CAD 10,000-30,000 (USD 7,500-22,500) per hectare, few smallholders can afford the upgrades. Crop insurance uptake remains patchy, with only 54% of British Columbia's horticulture acreage carried coverage in 2024, prompting the exploration of parametric weather policies that pay out automatically when key thresholds are breached.

Farm-Labor Shortages and Rising Wages

More than 28,000 agricultural vacancies persisted in 2022, and the gap could reach 15% of required workers by 2030 despite the Temporary Foreign Worker (TFW) Program comprising 29% of crop-production labor in 2019[4]Source: Employment and Social Development Canada, “Temporary Foreign Worker Program 2019 Statistics,” canada.ca. Farm wages rose 9% in 2024 as horticulture competed with construction and hospitality. Large greenhouse operators are piloting robotic harvesters, which offer five-to-six-year payback horizons, but capital constraints leave smallholders reliant on family labor or informal networks. The average operator age now stands at 56, raising succession concerns that exacerbate consolidation as farms with less than 10 hectares exit the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consumption: Vegetables Dominate Value, Fruits Capture Growth Momentum

In 2025, vegetables accounted for 54.8% of the Canada fruits and vegetables market share, reflecting the overall Canada fruits and vegetables market size and supported by greenhouse-grown tomatoes, peppers, and cucumbers, as well as field-grown potatoes and onions. Fruits are projected to grow at a faster CAGR of 3.8% through 2031, driven by export-oriented blueberries and high-margin apple varieties. Fruit demand is typically higher among higher-income households and health-conscious consumers, while vegetables remain more sensitive to price changes.

Berry production in Canada is driven by export competitiveness and varietal specialization, with blueberries leading the way due to their scalability, storage durability, and high international demand. Strawberries and cranberries support regional production and value-added processing. Apple growers are shifting to premium cultivars, focusing on texture, sweetness, and brand recognition to optimize margins. Leafy greens, such as lettuce, face climate and seasonal challenges, making Canada reliant on cross-border sourcing and vulnerable to fluctuations in trade costs. Potatoes balance fresh consumption with processing demand, with contracts, storage, and proximity to processors shaping planting decisions.

Geography Analysis

Ontario and British Columbia generated approximately 62% of the national horticulture production in 2025. Ontario’s leverage derives from its Leamington-Kingsville greenhouse hub, which reported CAD 1.5 billion (USD 1.1 billion) in sales, most of which flows to Michigan and Ohio retail chains. British Columbia’s Fraser Valley and Okanagan regions contributed CAD 1.0 billion (USD 750 million) from a mix of berries, apples, and greenhouse peppers, branding produce under low-carbon certifications that resonate with West Coast consumers.

Quebec accelerates the fastest, as greenhouse acreage climbed significantly from 2022 to 2024. Growers channel 34% of their produce through farmers’ markets or community-supported agriculture programs, which is double the national average. This direct route allows for the retention of up to 70% of the retail price, versus 30-40% via wholesale. Prairie provinces specialize in storage crops, as Manitoba planted 27,000 hectares of potatoes in 2024, while Alberta harvested 85,000 metric tons of onions. Yet a multi-year drought forced southern Alberta irrigation districts to cut allocations by up to 30%, nudging some growers toward pulses.

The Atlantic provinces rely heavily on potatoes and blueberries for export, but their narrow growing season makes them net importers of most fresh produce. Prince Edward Island shipped 540,000 metric tons of processing potatoes to the United States in 2024, although labor constraints and volatile pricing triggered accelerated consolidation among farms with less than 20 hectares of land. Northern territories host emerging indigenous greenhouse ventures, but are hampered by energy and logistics overheads. Regulatory compliance under the Safe Food for Canadians Regulations imposes traceability obligations that weigh proportionally heavier on micro-scale operators, adding indirect pressure toward regional concentration.

Competitive Landscape

Canada’s fresh-produce sector remains fragmented, yet consolidation is accelerating as capital-intensive greenhouse operations expand. Ten Ontario greenhouses, including Mastronardi Produce Ltd and Red Sun Farms, account for roughly 40% of the province's tomato output and have invested more than CAD 200 million (USD 150 million) in robotics and cogeneration since 2022. Field potatoes and onions operate under regional oligopolies, with Cavendish Farms and McCain Foods Limited anchoring supply contracts that lock in pricing below spot during surplus years.

Large food retailers, including Loblaw Companies, Sobeys Inc., and Metro Inc., exert significant buyer power by forming direct-sourcing agreements and private-label programs that absorb 15-20% of the margins once held by wholesalers. Compliance with Good Agricultural Practices certifications costs CAD 10,000-20,000 (USD 7,500-15,000) per year, erecting barriers for farms below 20 hectares. Technology penetration remains uneven, with fewer than 5% of sites utilizing AI-enabled platforms, presenting an opportunity for providers to bundle financing with yield guarantees.

Disruptors include vertical-farming specialist GoodLeaf Farms, which operates energy-intensive indoor modules that claim 95% water savings but still struggle with electricity costs. Government research institutes file patents, such as Agriculture and Agri-Food Canada’s 2024 machine-learning harvest predictor, yet commercialization pathways often favor larger private firms that can license and deploy technologies at scale. Overall, the industry is shifting toward a hub-and-spoke structure, where well-capitalized producers secure long-term contracts with retailers, while smallholders either niche into organic and farm-gate channels or exit the market.

Recent Industry Developments

- December 2025: The governments of Canada and Alberta introduced the three-year CAD 10 million (USD 7.3 million) "Growing Greenhouses" program under the Sustainable Canadian Agricultural Partnership. This initiative aims to promote the construction and expansion of commercial greenhouses and vertical farms, increasing year-round fresh fruit and vegetable production, reducing dependence on imports, and strengthening the resilience of the local food supply chain.

- September 2025: Canada and Ontario stated investments of up to CAD 4.7 million (USD 3.5 million) in 48 agri-food R&D projects. This initiative, part of the Ontario Agri-Food Research Initiative, supports 20 companies in adopting innovative technologies and advancing commercialization efforts. The program aims to improve production efficiency and enhance market competitiveness for fruit and vegetable producers.

- August 2025: Canada revised its Plant Breeders’ Rights Regulations to limit the farmers’ privilege exemption, enhancing protections for breeders of horticultural fruits and vegetables. This amendment aligns intellectual property protections for new varieties with international standards, encouraging both private and public investment in breeding and varietal innovation.

Canada Fruits And Vegetables Market Report Scope

A fruit develops from the flower of a plant and contains seeds. Vegetables are a culinary classification that includes edible plant parts, such as roots, stems, leaves, and flowers, that are typically not sweet. Culinary usage often distinguishes fruits as sweet or tart foods used in desserts or snacks, while vegetables are commonly savory and served as part of main or side dishes.

The Canadian fruits and vegetables market is analyzed by production (volume), consumption (volume and value), imports (volume and value), exports (volume and value), and Wholesale price trends. The report offers market sizes and forecasts in terms of value (USD) and volume (metric tons) for all the above segments.

Fruits

| Apple | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Berries | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Grapes | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Citrus | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Bananas | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

Vegetables

| Potato | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Tomato | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Lettuce | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Chillies and Peppers | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Onions | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis |

| Fruits | Apple | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Berries | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Grapes | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Citrus | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Bananas | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Vegetables | Potato | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Tomato | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Lettuce | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Chillies and Peppers | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Onions | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

How large is the Canada fruits and vegetables market in 2026?

The Canada fruits and vegetables market size is valued at USD 14.10 billion in 2026.

What is the projected growth rate for Canada fruits and vegetables market through 2031?

The market is projected to expand at a 3.57% CAGR, reaching USD 16.80 billion by 2031.

Which segment is growing fastest?

Fruits are forecast to post the higher 3.8% CAGR due to rising berry exports and premium apple varieties.

Why are Ontario and British Columbia so dominant in Canadian horticulture?

Ontario benefits from a large greenhouse corridor near United States markets, while British Columbia leverages hydroelectric power and sustainability branding to capture high-value output.

How are growers addressing labor shortages?

Large operators invest in robotic harvesters and AI-enabled systems, while smaller farms rely on the Temporary Foreign Worker Program and selective mechanization grants.

Page last updated on: