Fresh Herbs Market Size and Share

Fresh Herbs Market Analysis by Mordor Intelligence

The fresh herbs market size is projected to grow from USD 4.17 billion in 2025 to USD 5.17 billion in 2026 and is forecast to reach USD 6.35 billion by 2031 at a 4.20% CAGR over 2026-2031. Demand for clean-label flavorings, rapid adoption of controlled-environment agriculture, and the growth of hyper-local distribution are reshaping competitive dynamics. Europe remained the largest revenue center in 2025, yet Asia-Pacific is adding the most incremental value as urban vertical farms compress cold-chain risks and lift year-round output. Commercialization of disease-resistant basil, investments in sovereign food security projects across the Middle East, and micro-fulfillment logistics that cut delivery windows to under 24 hours are reinforcing structural growth. Fragmentation persists because thousands of smallholders and a wave of venture-backed indoor farms operate side by side, creating space for integrators to aggregate hyper-local volumes into national networks.

Key Report Takeaways

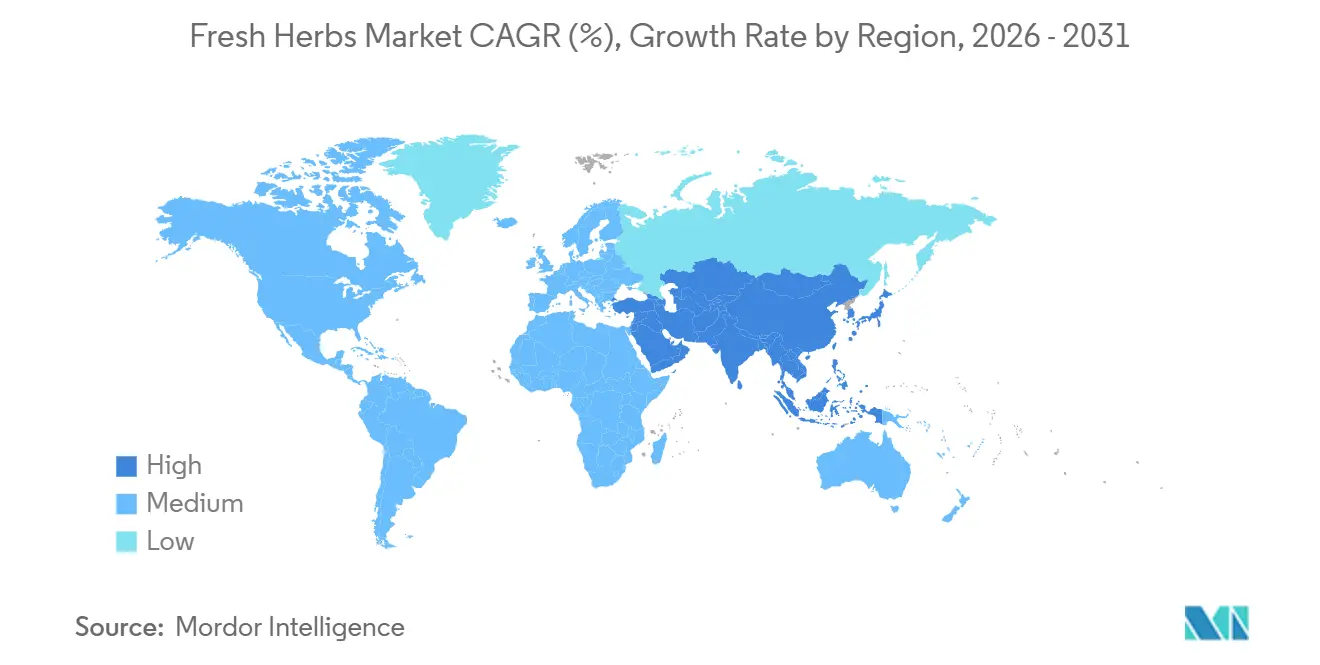

- By geography, Europe led with 31.2% of the fresh herbs market share in 2025, while Asia-Pacific is forecast to post a 9.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fresh Herbs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label natural ingredients | +0.8% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Growth in organic food consumption | +0.7% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Surge in food-service menu penetration of fresh herbs | +0.6% | Global, led by North America and Europe quick-service chains | Short term (≤ 2 years) |

| Expansion of controlled-environment agriculture | +0.9% | Asia-Pacific core, Middle East, and North America urban corridors | Long term (≥ 4 years) |

| Hyper-local distribution via micro-fulfillment | +0.5% | Metropolitan North America and Europe, and emerging Asia-Pacific hubs | Medium term (2-4 years) |

| Commercialization of downy-mildew-resistant seed | +0.4% | Mid-Atlantic North America, Mediterranean Europe, and India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Clean-Label Natural Ingredients

Food manufacturers are substituting artificial flavor compounds with fresh herb extracts as 83% of consumers now prioritize natural ingredients according to McCormick’s 2024 annual filing [1]Source: McCormick and Company, “Annual Report 2024,” MCCORMICK.COM. Premium brands are locking multi-year contracts with greenhouse operators that certify pesticide-free output, while value-tier producers still rely on field supply that faces higher residue rejection rates. Prepared sauces and dressings launched in 2024 included 12% more fresh herb content across the top 20 stock-keeping units, signaling category-wide reformulation. The United States Food and Drug Administration tightened the definition of natural flavoring in early 2025, excluding several oleoresins and expanding addressable volume for fresh-cut suppliers [2]Source: United States Food and Drug Administration, “Guidance on Natural Flavoring Definitions,” FDA.GOV. This regulatory nudge, combined with expanding organic shelf space, sustains price premiums that offset the cost gap versus synthetics.

Growth in Organic Food Consumption

United States organic herb acreage expanded in 2024, outpacing overall organic food growth as households paid 40-60% premiums for certified produce. European Union Organic Regulation 2018/848 raised traceability thresholds, consolidating the share among integrated greenhouse operators that can fund compliance. The organic premium narrowed from 65% to 48% in Germany between 2023 and 2025, yet it still tops in emerging Asian markets where certification remains a status symbol [3]Source: European Commission, “Commission Regulation 2024/1009,” EC.EUROPA.EU. Mexican exporters used lower certification fees and a favorable peso to lift organic cilantro shipments to the United States in 2024.

Surge in Food-Service Menu Penetration of Fresh Herbs

Quick-service and fast-casual chains treat fresh herbs as cost-efficient premium cues, as illustrated by Chipotle Mexican Grill's 2024 move to increase cilantro procurement to support cauliflower rice and plant-based proteins. A five-gram basil garnish adds USD 0.15 to food cost yet supports a USD 1.50 menu upcharge, delivering a ten-fold return. Independent restaurants followed suit, with mentions of cilantro, basil, and mint on menus rising year over year in 2024. Distribution networks faced stockouts during summer peaks, prompting direct contracts between chefs and local greenhouse farms. The channel now absorbs global fresh herb volumes, and its share continues to climb.

Expansion of Controlled-Environment Agriculture

Venture investment in controlled-environment agriculture significantly increased in 2024, highlighted by Plenty Unlimited’s USD 680 million United Arab Emirates joint venture and Oishii’s USD 150 million Series B. Vertical farms routinely yield 25-30 kilograms of basil per square meter annually, about fifteen times field productivity, by stacking grow trays and achieving six harvest cycles under optimized LED lighting. While initial capital spend runs eight to ten times that of field operations, renewable energy and automation are narrowing operating gaps, cutting labor inputs to 0.12 hours per kilogram. Saudi Arabia earmarked USD 500 million in 2024 for 12 vertical farms as part of its Vision 2030 food security strategy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short shelf life and high post-harvest losses | -0.6% | Global, most acute where cold-chain gaps persist | Short term (≤ 2 years) |

| Weather-driven price volatility | -0.5% | North America, Mediterranean Europe, and South America field zones | Short term (≤ 2 years) |

| DNA metabarcoding raising authentication costs | -0.3% | Europe and North America import-dependent markets | Medium term (2-4 years) |

| Stricter maximum-residue limits | -0.4% | European Union, spillover to Turkey and Egypt export growers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Short Shelf Life and High Post-Harvest Losses

Fresh basil wilts within 48-72 hours at ambient temperature because chilling injury occurs below 10 degrees Celsius, and respiration is rapid, driving 15-20% retail shrink even with optimal refrigeration. Modified-atmosphere packaging, which extends shelf life to 10-12 days, adds USD 0.08-0.12 per clamshell, a cost many mass merchants avoid. Electrolyzed oxidizing water treatments approved in 2024 for organic use cut microbial load two to three logs and delay senescence, yet require USD 50,000-80,000 per line, beyond smallholder reach. Consequently, waste rates in South America and sub-Saharan Africa exceed 30-50%, contrasting with sub-5% losses inside vertically integrated controlled-environment agriculture facilities in North America and Europe.

Weather-Driven Price Volatility

California’s 2024 drought cut basil yields, spiking wholesale prices from USD 18 to USD 29 per pound in eight weeks. Unilever disclosed a 1.2% increase in the cost of goods for its sauces unit, tied to herb shortages. Mediterranean Europe saw similar stress when a July heatwave above 38 degrees Celsius for fourteen consecutive days reduced marketable yields. No futures market exists for fresh herbs, leaving growers fully exposed to weather risk. Retailers responded by lifting controlled-environment agriculture sourcing 35% in 2024 to stabilize supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Europe retained 31.2% of global value in 2025, anchored by Mediterranean field output in Italy, Spain, and Greece, plus Northern European greenhouse clusters in the Netherlands and Belgium that supply basil, cilantro, and parsley year-round. In 2024, Italy's Lazio and Campania regions were significant producers, while Dutch Venlo-style greenhouses exported a majority of their yield to Germany, France, and the United Kingdom, where organic premiums ranged between 40% and 60%. High natural-gas prices accelerated the switch to LED lighting and geothermal heating, helping operators defend margins despite stricter chlorpyrifos limits that cut Turkish and Egyptian imports 18% in 2024, according to the European Union.

Asia-Pacific is expanding at a 9.9% CAGR through 2031 as vertical farms in China and Japan bypass cold-chain bottlenecks and deliver herbs within 24 hours of harvest. China’s controlled-environment output reached about 90,000 metric tons in 2024, concentrated around Shanghai, Beijing, and Shenzhen, while Japan’s Spread Company and Mirai Corporation grew roughly 15,000 metric tons of basil and shiso, two-thirds of which flowed into convenience-store salads and bento boxes. India’s cilantro exports to the Middle East and Europe rose despite 35-40% domestic post-harvest loss, and Australia’s greenhouse crop grew 8.5% to satisfy supermarkets that expanded organic herb assortments.

North America is projected to account for a significant share of revenue in 2025, driven by significant production in California's Salinas Valley and Oxnard Plain, along with contributions from Northeastern greenhouse farms supporting premium retail programs. Canadian facilities in Ontario and British Columbia added close to 10,000 metric tons, covering winter demand when Mexican field growers face frost. Mexico exported 40,000 metric tons of cilantro in 2024 but incurred USD 600-900 per hectare in new Food Safety Modernization Act compliance costs. Sovereign-backed vertical farms in the United Arab Emirates and Saudi Arabia are on track to supply up to 1,500 metric tons annually by 2027, aiming to cut import dependence to 65-70%.

Competitive Landscape

The top ten suppliers hold only a minimal share of global revenue, giving the fresh herbs market a low score as thousands of smallholders coexist with venture-funded vertical farms. Field producers keep cost leadership in bulk cilantro and parsley for processors, whereas greenhouse and indoor operators win retail shelf space with pesticide-free certification, consistent sizing, and longer shelf life. Compliance with tighter maximum-residue limits and DNA-based authentication are becoming must-have capabilities that many fragmented growers cannot match.

Technology is the primary differentiator. Plenty Unlimited uses machine-learning climate control to push basil yields to 25-30 kilograms per square meter, fifteen times field output, while Gotham Greens leverages rooftop real estate inside major cities to eliminate freight and cut spoilage below 5%. Mexican greenhouse cooperatives narrow the gap by deploying low-cost Internet of Things sensors that increase water-use efficiency and reduce fertilizer waste, preserving their price advantage. In-store units from Infarm and other hyper-local pioneers shrink order-to-delivery windows to hours, command 20-25% price premiums, and strengthen retailer loyalty.

Strategic alliances and recapitalizations are reshaping the field. Plenty Unlimited has entered a significant joint venture with Mawarid Holding to construct a large-scale facility in the United Arab Emirates, projected to meet substantial production demands by 2027. Meanwhile, GoodLeaf Farms has secured considerable funding to establish a new site in Calgary with a notable production capacity. AeroFarms has successfully emerged from Chapter 11 bankruptcy protection with USD 40 million in new funding and will license its aeroponics platform abroad in 2023. As capital flows toward large, tech-driven players and residue regulations tighten, competitive power is migrating to firms that pair production scale with data-rich traceability systems.

Recent Industry Developments

- May 2025: AutoStore and OnePointOne have introduced Opollo Farm, the world’s first fully robotic vertical farm, providing fresh herbs and leafy greens to select Whole Foods Market locations in Phoenix.

- June 2025: Hydropolis sp. z o.o. has launched Green City Jungle in Kraków, Poland, a fully operational vertical farm powered by renewable wind and solar energy. This high-efficiency pilot project focuses primarily on basil and employs advanced hydroponic technology to produce approximately 500 pots daily. The initiative aims to validate a scalable, sustainable, and local food production model.

- March 2024: Eden Green Technology, an indoor vertical farming company, has launched its flagship herb program, becoming the first to grow, package, and ship a complete range of herbs from a single facility. The program utilizes Eden Green's patented microclimate technology and networked distribution model to enhance logistics, minimize environmental impact, and expand access to fresh, affordable herbs.

Global Fresh Herbs Market Report Scope

The Fresh Herbs Market Report is Segmented by Geography (North America, Europe, Asia-Pacific, and More). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, Regulatory Framework, Logistics and Infrastructure, and Seasonality Analysis. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | ||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | ||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | ||

| Wholesale Price Trend Analysis and Forecast | ||

| Regulatory Framework | ||

| List of Key Players | ||

| Logistics and Infrastructure | ||

| Seasonality Analysis | ||

| By Geography | North America | United States | Production Analysis (Area Harvested, Yield, and Production Volume) |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Canada | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Mexico | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Europe | Germany | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| France | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Spain | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Italy | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Russia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Asia-Pacific | China | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| India | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Japan | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Australia | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| South America | Brazil | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Argentina | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Middle East | Saudi Arabia | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| United Arab Emirates | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Turkey | Production Analysis (Area Harvested, Yield, and Production Volume) | ||

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

| Africa | South Africa | Production Analysis (Area Harvested, Yield, and Production Volume) | |

| Consumption Analysis (Consumption Value and Volume) | |||

| Import Market Analysis (Import Value, Volume, and Key Supplying Markets) | |||

| Export Market Analysis (Export Value, Volume, and Key Destination Markets) | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Regulatory Framework | |||

| List of Key Players | |||

| Logistics and Infrastructure | |||

| Seasonality Analysis | |||

Key Questions Answered in the Report

How large is the global fresh herbs market in 2026?

The fresh herbs market size is estimated at about USD 5.17 billion in 2026, on track with a 4.20% CAGR toward USD 6.35 billion by 2031.

Which region leads sales of fresh herbs?

Europe accounted for 31.2% of fresh herbs market share in 2025, supported by Mediterranean field output and Dutch greenhouse clusters.

What segment grows fastest inside the fresh herbs market?

Asia-Pacific shows the highest growth with a projected 9.9% CAGR through 2031 as urban vertical farms in China and Japan scale production.

Why are vertical farms important for fresh herb supply?

Controlled-environment agriculture produces up to fifteen times the yield per square meter, eliminates pesticide residues, and supports 24-hour hyper-local distribution.

What drives rising organic herb demand?

Consumers accept 40-60% premiums for certified products while regulations tighten residue limits, motivating retailers to widen organic shelf space.

Page last updated on: