French Fries Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

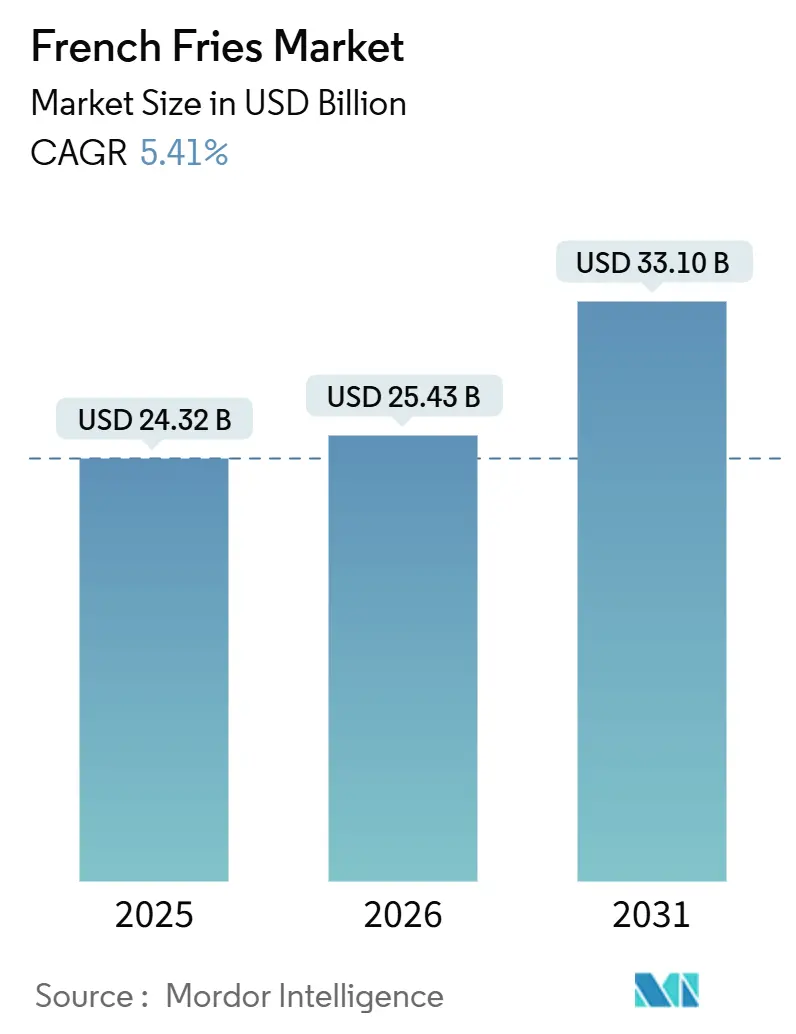

| Market Size (2026) | USD 25.43 Billion |

| Market Size (2031) | USD 33.10 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

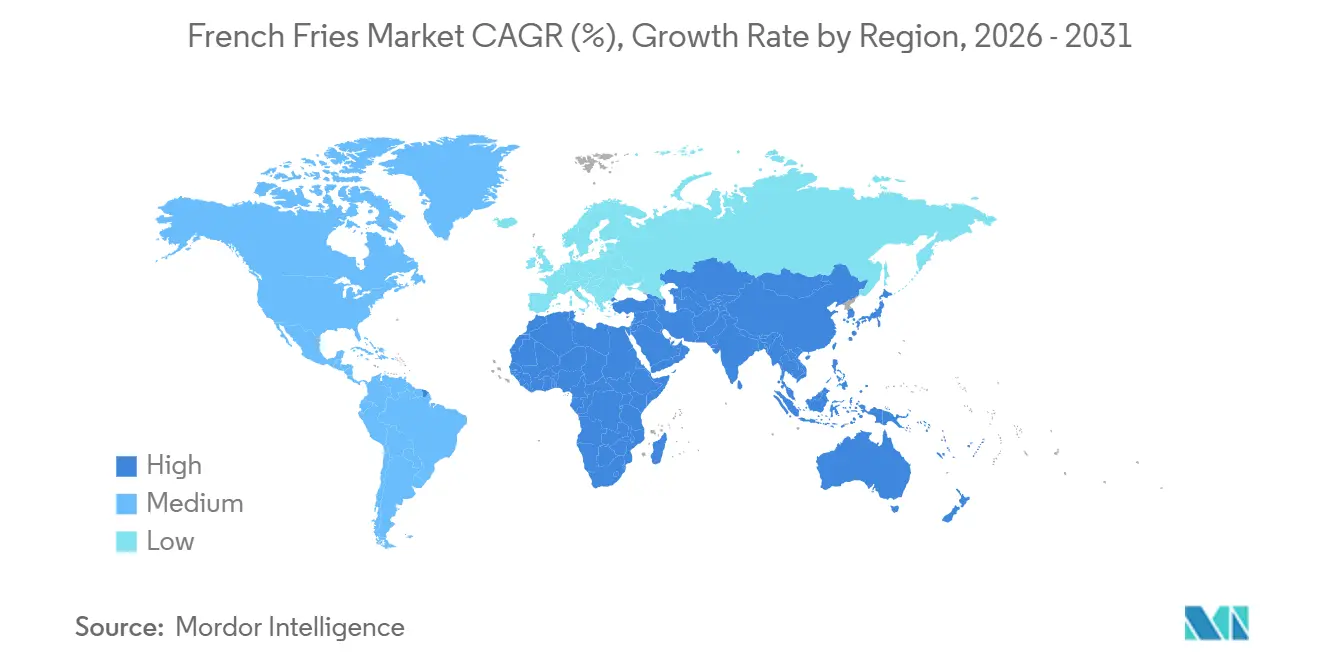

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

French Fries Market Analysis by Mordor Intelligence

The global French fries market was valued at USD 24.32 billion in 2025, estimated at USD 25.43 billion in 2026, and is projected to reach USD 33.10 billion by 2031, growing at a CAGR of 5.41% during the forecast period (2026-2031). This growth reflects a significant shift in consumer preferences toward convenience foods, driven by urbanization, rising disposable incomes, and the expansion of quick-service restaurant (QSR) chains, where french fries remain a menu staple. The market's strength lies in the dual appeal of frozen fries, catering to institutional buyers seeking operational efficiency and retail households prioritizing quick and consistent meal options. The growth trajectory faces certain restraints. In early 2026, processors in Belgium and the Netherlands temporarily halted production due to oversupply, while Indian and Chinese exporters doubled their capacity to capture market share in the Asia-Pacific and Middle Eastern regions. This situation underscores how regional supply imbalances and the scaling of manufacturing in emerging markets are reshaping competitive dynamics more rapidly.

Key Report Takeaways

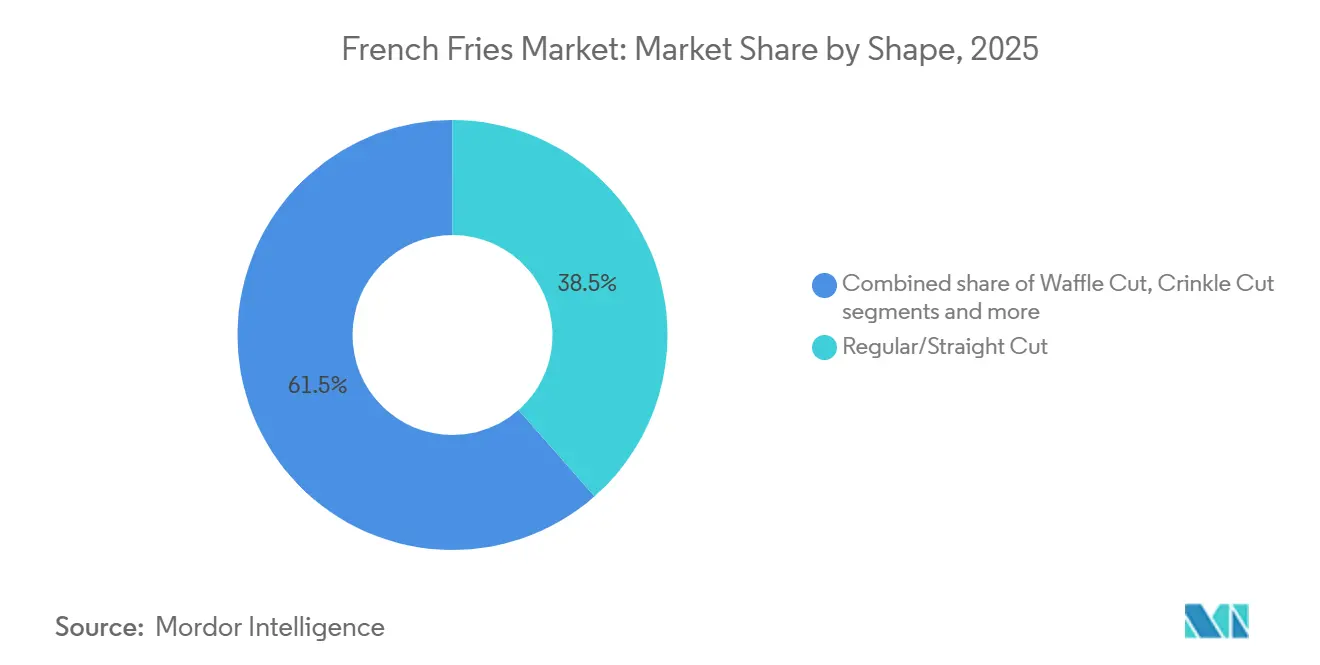

- By shape, regular/straight cut led with 38.51% revenue share in 2025, while waffle cut is projected to expand at a 6.42% CAGR to 2031.

- By form, frozen fries products dominated 88.17% of the French fries market share in 2025 and are projected to register the highest CAGR of 5.72% through 2031.

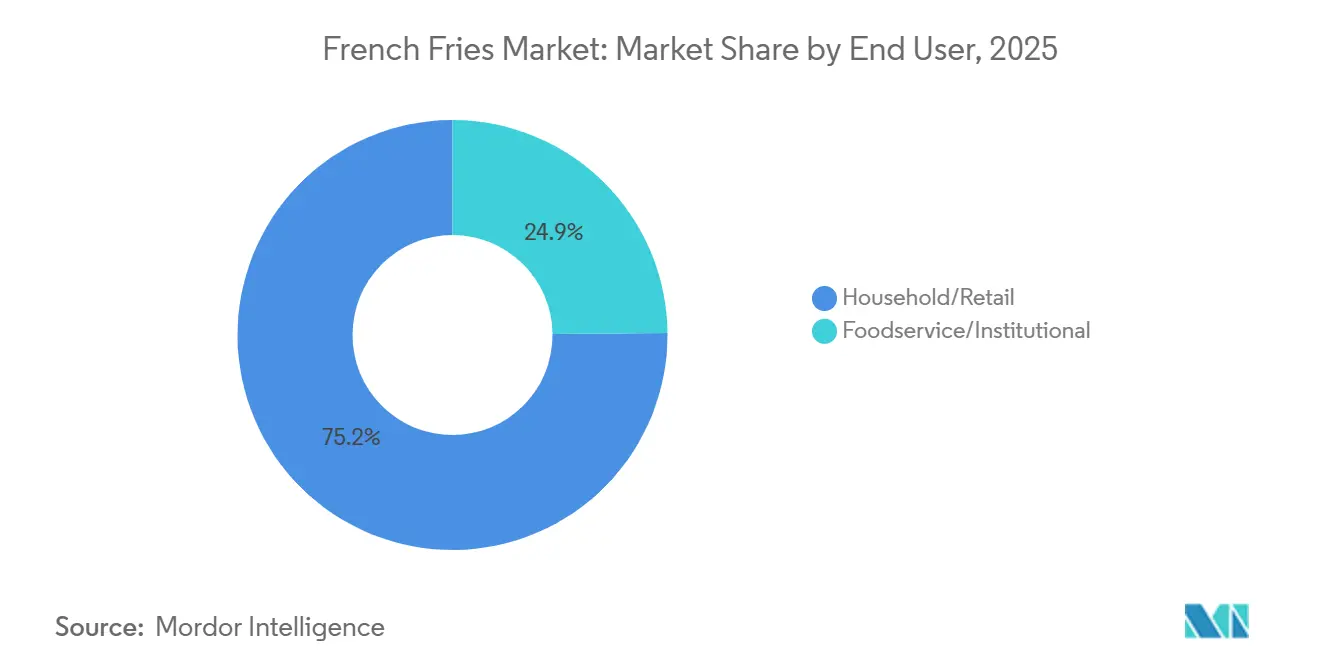

- By end user, the household/retail segment accounted for 75.15% of the French fries market size in 2025 and is advancing at a 6.82% CAGR through 2031.

- By geography, Europe captured 34.16% of the French fries market share in 2025, while Asia-Pacific is expected to grow at a 5.98% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global French Fries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient ready-to-eat snack options | +1.2% | Global, with pronounced uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of quick service restaurant chains globally | +1.5% | Asia-Pacific core (China, India, Japan), spill-over to Middle East and South America | Long term (≥ 4 years) |

| Increasing consumption of fast food among millennials | +0.8% | North America, Europe, and emerging urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Product innovation with new flavors and seasoning options | +0.7% | North America and Europe retail, selective quick service restaurant rollouts in Asia-Pacific | Medium term (2-4 years) |

| Advancements in cold storage and supply chain infrastructure | +0.9% | Asia-Pacific (China, India, Indonesia), Middle East, and select South American markets | Long term (≥ 4 years) |

| Growth in frozen food retail and distribution channels | +1.0% | Global, with accelerated e-commerce penetration in North America, Europe, and urban Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of quick service restaurant chains globally

QSR chains are a key driver of demand in the global frozen french fries market. As of fiscal 2024, Yum! Brands parent company of KFC, Taco Bell, Pizza Hut, and Habit Burger & Grill operates over 63,000 restaurants across more than 155 countries and territories. These outlets are primarily run by approximately 1,500 franchisees worldwide[1]Source: Yum! Brands RSC, "Investors", investors.yum.com. The company is aggressively expanding in markets like China, India, and other emerging economies, where french fries are widely accepted as a neutral and universal side dish. This trend highlights a critical market dynamic: processors with long-term supply agreements with global QSR chains benefit from consistent volume demand and stronger pricing power. On the other hand, processors relying on spot sales face the risk of margin pressures, particularly during periods of reduced restaurant traffic.

Rising demand for convenient ready-to-eat snack options

Urbanization and the increasing prevalence of dual-income households are driving the demand for convenient meal solutions, positioning frozen french fries as a key market driver in the global french fries market. These products have evolved from being a restaurant side dish to a household staple, offering restaurant-quality taste in under 20 minutes. Their appeal lies not only in their quick preparation but also in eliminating the need for peeling, cutting, and oil management, making them highly convenient for time-strapped consumers. As reported by The American Frozen Food Institute (AFFI), data from 2026 revealed that 40% of shoppers now consume frozen foods every few days or daily, a notable increase from 35% in 2019[2]American Frozen Food Institute, "Why Frozen Foods Are an Everyday Kitchen Essential", affi.org. This structural shift in consumer behavior supports the household/retail segment's robust 6.82% CAGR. Additionally, processors investing in portion-controlled, oven-ready formats are well-positioned to capture a larger market share as convenience increasingly becomes a critical purchasing criterion.

Product innovation with new flavors and seasoning options

Flavor innovation and health-focused reformulations drive differentiation in a commodity-adjacent category. In February 2026, Roots Farm Fresh launched organic waffle fries, free from seed oils and cooked in avocado oil, aiming at natural-retail channels and consumers cautious of industrial seed oils. McCormick introduced air-fryer seasoning kits in 2024, enabling home chefs to achieve restaurant-style flavors like garlic parmesan, Cajun spice, and truffle on standard frozen fries. This effectively separates flavor from the processor, shifting profit margins to the spice supplier. Such innovations splinter the market, establishing premium tiers that fetch higher prices, while simultaneously elevating expectations for established players dependent on scale and cost leadership.

Advancements in cold storage and supply chain infrastructure

One of the major drivers of the global French fries market is the growing investment in cold-chain infrastructure across Asia-Pacific and the Middle East. These developments are opening access to previously untapped markets, minimizing spoilage, and ensuring the consistent year-round availability of frozen fries. In India, HyFun Foods is significantly expanding its contract farming operations, now covering 30,000 hectares in Gujarat and Madhya Pradesh, to cater to the rising demand. Moreover, China's export performance underscores the market's rapid expansion. Between January and May 2025, China exported 139,000 tons of frozen French fries, a notable figure compared to the 206,000 tons exported throughout 2024. Over the last seven years, China's frozen fries exports have grown nearly 26-fold, with the most significant growth starting in 2020. Additionally, trade dynamics are shifting as regions that traditionally imported frozen fries are now emerging as exporters, reshaping the global supply landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high fat and calorie intake | -0.9% | Global, with heightened regulatory scrutiny in Europe and select United States municipalities | Medium term (2-4 years) |

| Volatile agricultural yields posing significant risks to the stability of potato supply | -1.1% | North America (Pacific Northwest), Europe (Belgium, Netherlands, France), emerging in India | Short term (≤ 2 years) |

| Stricter acrylamide limits in fried foods | -0.6% | Europe (EFSA jurisdiction), potential United States Food and Drug Administration action | Long term (≥ 4 years) |

| High transportation costs for frozen fries distribution | -0.8% | Global, with acute pressure on long-haul export routes (Europe to Middle East, North America to Asia) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns over high fat and calorie intake

The rising prevalence of obesity and chronic diseases is emerging as a significant restraint in the global french fries market. Policymakers and health organizations are increasingly targeting fried foods, including french fries, due to their high calorie and saturated fat content. The World Health Organization (WHO), through its Acceleration Plan to Stop Obesity, has proposed measures such as marketing restrictions, and reformulation incentives to encourage healthier eating habits[3]Source: World Health Organization, "WHO acceleration plan to stop obesity", WHO.org. In response, processors like Lamb Weston are reformulating products, introducing low-oil fries marketed as "better-for-you" alternatives. However, these reformulations come with challenges. The use of enzyme treatments, alternative oils, and air-frying equipment requires substantial capital investment. Additionally, consumer acceptance remains uneven, as changes in taste and texture limit broader adoption. While health-conscious consumers are reducing their consumption or switching to baked alternatives, a segment of the market is willing to pay a premium for lower-fat options.

Volatile agricultural yields posing significant risks to the stability of potato supply

The global frozen fries market faces significant restraints due to the high dependency on unbroken cold-chain logistics from production to retail. Transportation costs remain a persistent challenge, particularly as distances increase and fuel prices fluctuate. In 2024-2025, refrigerated trucking and container shipping rates surged, driven by rising diesel prices and ongoing disruptions in global logistics networks following post-pandemic adjustments. European processors, especially in Belgium and the Netherlands, exporting to the Middle East a key market for their fries encountered dual pressures. These included elevated energy costs at home and increased freight rates, further aggravated by geopolitical tensions disrupting Red Sea shipping routes. By early 2026, the Belgian potato trade association reported conflict-related disruptions impacting exports to Saudi Arabia and Gulf countries. This compounded oversupply issues, as processors struggled to economically ship surplus volumes, according to Potato Business.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Shape: Waffle Cut Drives Premium Growth

Regular/Straight Cut fries emerged as the largest segment in 2025, holding 38.51% of the global market share. Their dominance stems from their extensive use in QSRs, where standardization and consumer familiarity drive demand. These fries are favored in foodservice due to their operational efficiency, including consistent cooking times, predictable oil absorption, and minimal equipment adjustments. However, the growth of this segment is slowing as QSR chains increasingly explore signature cuts to enhance menu differentiation. Processors relying solely on straight-cut production may face challenges as the market shifts toward greater variety and innovation.

Waffle Cut fries are projected to be the fastest-growing segment, with a robust CAGR of 6.42% through 2031. This rapid growth is fueled by a premiumization trend in retail frozen aisles, where waffle-cut and crinkle-cut formats command premium price over straight-cut alternatives due to their unique appearance and superior sauce-holding capabilities. In February 2026, Roots Farm Fresh, a smaller brand, made waves in specialty retail by launching seed-oil-free organic waffle fries, showcasing the power of shape differentiation. The increasing popularity of waffle-cut fries highlights retail consumers' preference for novelty and their willingness to pay a premium, presenting opportunities for processors to invest in flexible cutting lines to meet this growing demand.

By Form: Frozen Dominance Reinforces Convenience Trend

In 2025, frozen french fries accounted for 88.17% of the market, making it the largest segment. This segment's dominance is driven by operational convenience and cost efficiency, as frozen formats simplify storage, extend shelf life, and streamline kitchen processes for foodservice operators. Frozen fries eliminate daily preparation labor, reduce waste, and enable centralized production that benefits from economies of scale. Quick Service Restaurant (QSR) chains universally adopt frozen formats to ensure consistent taste across thousands of locations, a critical factor for maintaining brand identity. This widespread adoption underscores the segment's entrenched position in the market.

The fastest-growing segment, frozen french fries, is projected to expand at a 5.72% CAGR through 2031. This growth is self-reinforcing, as processors continue to invest in capacity due to predictable demand, which lowers per-unit costs and widens the price gap compared to fresh fries. This dynamic further accelerates the shift from fresh to frozen formats. Meanwhile, fresh-cut fries, which hold an 11.83% market share in 2025, face structural challenges such as labor shortages, rising minimum wages, and the high capital costs of peeling and cutting equipment. Disruptors targeting the fresh segment must focus on automation, such as robotic peeling and cutting, or position themselves in the ultra-premium category, where labor-intensive preparation can justify higher pricing. For the frozen segment, sustainability remains a key focus, with leading processors like McCain and Lamb Weston investing in renewable energy and regenerative agriculture to address carbon-footprint concerns.

By End User: Household/Retail Drives Market Evolution

In 2025, households and retail channels dominated the global French fries market, accounting for 75.15% and is expected to grow with a CAGR of 6.82% through 2031. Within the retail segment, supermarkets and hypermarkets emerged as the leading sub-channel, attributed to their extensive availability and strong consumer inclination toward in-store shopping experiences. Meanwhile, foodservice and institutional channels, including Quick Service Restaurants (QSRs) and restaurants, are experiencing notable growth. This expansion is driven by increasing urbanization and a rise in out-of-home dining, which collectively sustain the demand for ready-to-cook potato products.

Online retail is rapidly gaining traction, driven by subscription services and bulk discounts that resonate with budget-minded families. As more consumers opt for at-home dining and quick meal solutions, the demand for frozen fries has surged, with many seeking swift, restaurant-quality dishes. The swift uptake of air fryers across North America and Europe has given this segment a boost, allowing frozen fries to rival the crispy, oven-baked taste of deep-fried versions from Quick Service Restaurants (QSRs). Moreover, the growth of organized retail and e-commerce has made these products more accessible, further propelling global household consumption of frozen french fries.

Geography Analysis

Europe emerged as the largest regional segment in the global french fries market in 2025, accounting for 34.16% of the total revenue. This dominance is attributed to Belgium and the Netherlands, the world's leading exporters of french fries. Companies like Lamb Weston and Aviko are actively expanding production capacity in Europe. For instance, Aviko has invested in processing facilities in the Netherlands and Belgium, enhancing the supply of frozen fries for both retail and foodservice markets. Moreover, the strong presence of quick-service restaurants and the expansion of fast-food chains sustain a high and consistent demand for frozen and ready-to-cook potato products. Additionally, increasing consumer preference for convenience foods, driven by busy urban lifestyles and the rise in dual-income households, further boosts consumption.

Asia-Pacific is projected to be the fastest-growing regional segment, with a CAGR of 5.98% through 2031. This growth is driven by the rapid expansion of Quick Service Restaurants (QSRs), rising middle-class incomes, and increased domestic processing capacity, which reduces dependency on imports. China's frozen fries exports surged to 290,000 tonnes in 2024-2025, a tenfold increase over five years, with Japan, the Philippines, Thailand, and Indonesia as key destinations. Additionally, China has achieved self-sufficiency, no longer ranking among major importers. Investments such as HyFun Foods' USD 108 million expansion in Gujarat and Agristo's Rs 750 crore (USD 88 million) plant in Bijnor, in partnership with Wave Group, highlight the scaling efforts of Indian processors to meet domestic QSR demand where KFC operates over 600 stores and McDonald's over 500 and to tap into export opportunities in Southeast Asia and the Middle East.

North America, encompassing the United States, Canada, and Mexico, balances established per-capita consumption with active capacity investments, aiming to maintain its market share against Asian exporters. Canada plays a critical role as a major exporter of frozen fries, particularly to the United States The region's production landscape is dominated by companies such as McCain Foods and Cavendish Farms. For example, Cavendish Farms has made significant investments in its North American facilities, reflecting Canada's strategy to strengthen cross-border supply chains under the USMCA agreement.

Competitive Landscape

The European French fries market is moderately concentrated, featuring a mix of large multinational processors, regional specialists, and emerging entrants. Key players such as McCain Foods, Lamb Weston, and J.R. Simplot Company dominate the market through their strong control over sourcing, advanced processing capabilities, and extensive distribution networks. Their scale and operational efficiency ensure consistent product quality and a broad market reach. Meanwhile, regional players compete by leveraging localized supply chains and addressing specific consumer preferences.

Technology is a critical factor in establishing a competitive advantage within the market. Companies are increasingly adopting advanced processing and quality control systems to improve efficiency and maintain product consistency. Automation and AI-driven inspection technologies are enhancing throughput capacity, minimizing waste, and ensuring standardized output, which is essential in high-volume production environments. Additionally, competition is intensifying around product differentiation, driven by the rising demand for healthier and specialty options such as low-fat, gluten-free, and alternative oil-based fries that cater to changing consumer preferences.

Beyond product innovation, market participants are focusing on brand positioning and adapting to shifting consumption patterns to strengthen their market presence. Multinational companies benefit from strong brand recognition and established partnerships with foodservice chains. In contrast, smaller and regional manufacturers compete by offering flexibility, cost efficiency, and the use of locally sourced ingredients. The competitive landscape is further influenced by increasing consolidation and collaboration across the value chain, as companies aim to enhance operational efficiency, optimize supply chains, and maintain consistent quality standards in a dynamic, demand-driven market.

French Fries Industry Leaders

-

McCain Foods Ltd

-

Lamb Weston Holdings Inc

-

J.R. Simplot Company

-

Aviko B.V. (Royal Cosun)

-

Cavendish Farms

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Lamb Weston has expanded into the Malaysian retail market by introducing its frozen potato fries for household consumption. This follows the company's retail debut in Singapore in November 2025 and highlights its continued growth across Southeast Asia.

- November 2025: Seabrook Crisps launched a new line of frozen French fries and flavored potato snacks. The company's French fries were made available in the popular cheese-and-onion and salt-and-vinegar flavors. Meanwhile, Seabrook's potato crinkles were offered in a beefy flavor and the brand's renowned Sea Salt.

- October 2025: Lamb Weston established a state-of-the-art frozen French fry production facility in Argentina, marking a significant development that enhanced the supply of frozen French fries across the Latin American market.

Global French Fries Market Report Scope

| Regular / Straight Cut |

| Crinkle Cut |

| Waffle Cut |

| Steak Fries |

| Curly Cut |

| Fresh French Fries |

| Frozen French Fries |

| Foodservice / Institutional | |

| Household / Retail | Supermarkets / Hypermarkets |

| Convenience / Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Shape | Regular / Straight Cut | |

| Crinkle Cut | ||

| Waffle Cut | ||

| Steak Fries | ||

| Curly Cut | ||

| By Form | Fresh French Fries | |

| Frozen French Fries | ||

| By End User | Foodservice / Institutional | |

| Household / Retail | Supermarkets / Hypermarkets | |

| Convenience / Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What will the french fries market be worth by 2031?

Forecasts place value at USD 33.10 billion, supported by a 5.41% CAGR over 2026-2031.

Which shape category grows fastest?

Waffle-cut fries, projected at a 6.42% CAGR through 2031, led by premium retail demand in North America and Europe.

Why do frozen products dominate the french fries market?

Frozen fries deliver standardized quality, reduce kitchen labor, and now air-fry crisply at home, securing an 88.17% share in 2025 and sustained 5.72% CAGR.

Which region posts the highest growth rate?

Asia-Pacific, with a 5.98% CAGR, fueled by expanding QSR chains and investment in domestic processing capacity.

Page last updated on: