Potato Starch Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.54 Billion |

| Market Size (2031) | USD 6.14 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

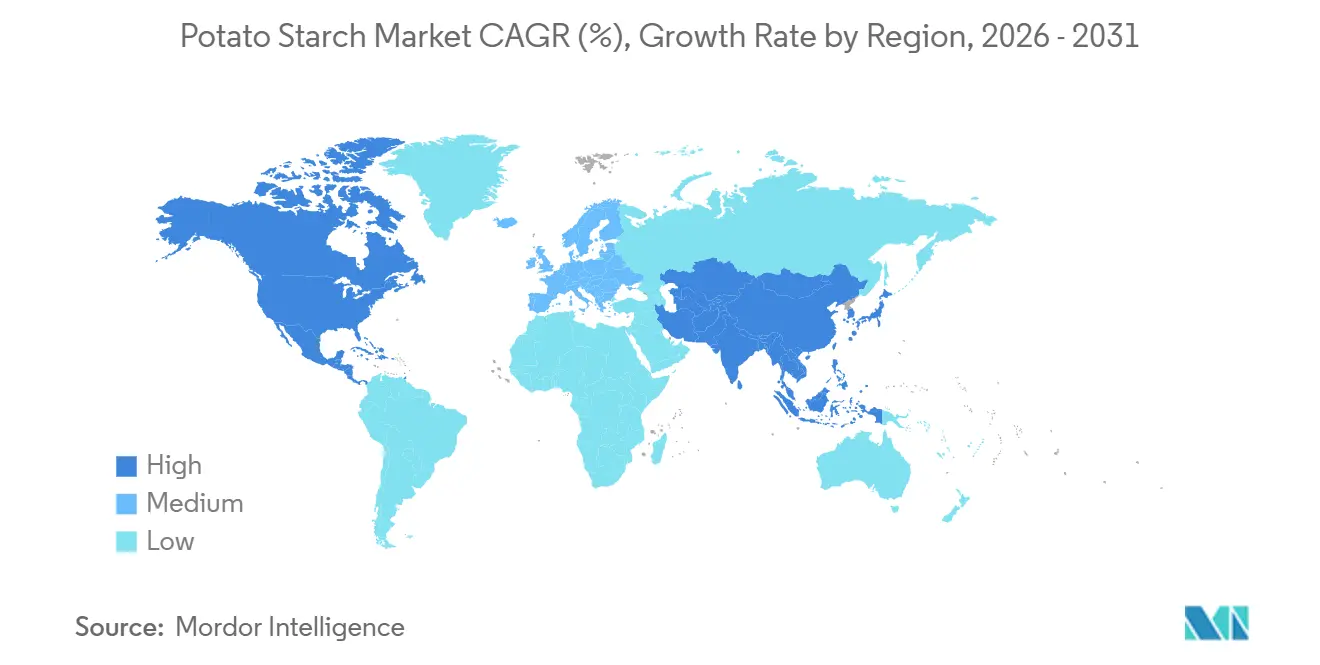

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Potato Starch Market Analysis by Mordor Intelligence

The Potato Starch Market size is expected to increase from USD 4.29 billion in 2025 to USD 4.54 billion in 2026 and reach USD 6.14 billion by 2031, growing at a CAGR of 6.22% over 2026-2031. The market's expansion is fueled by food manufacturers aiming to balance clean-label requirements with functional performance. This trend is particularly significant as precision-fermentation platforms increasingly adopt ultra-low-protein grades as microbial feedstock. Specialty potato starch grades, designed to endure retort cycles, high-shear processing, and repeated freeze-thaw events, are replacing commodity native starch in applications such as sauces, ready meals, and plant-based cheese. Additionally, organic certification and non-GMO positioning have become critical price-resilient factors in categories like baby food, premium bakery products, and dairy alternatives. The competitive landscape is becoming more challenging as tapioca and pea starches offer similar melt-stretch and clarity properties at a lower cost. This competition is driving potato-starch suppliers to focus on improving process efficiency, innovating resistant starches, and implementing sustainability upgrades.

Key Report Takeaways

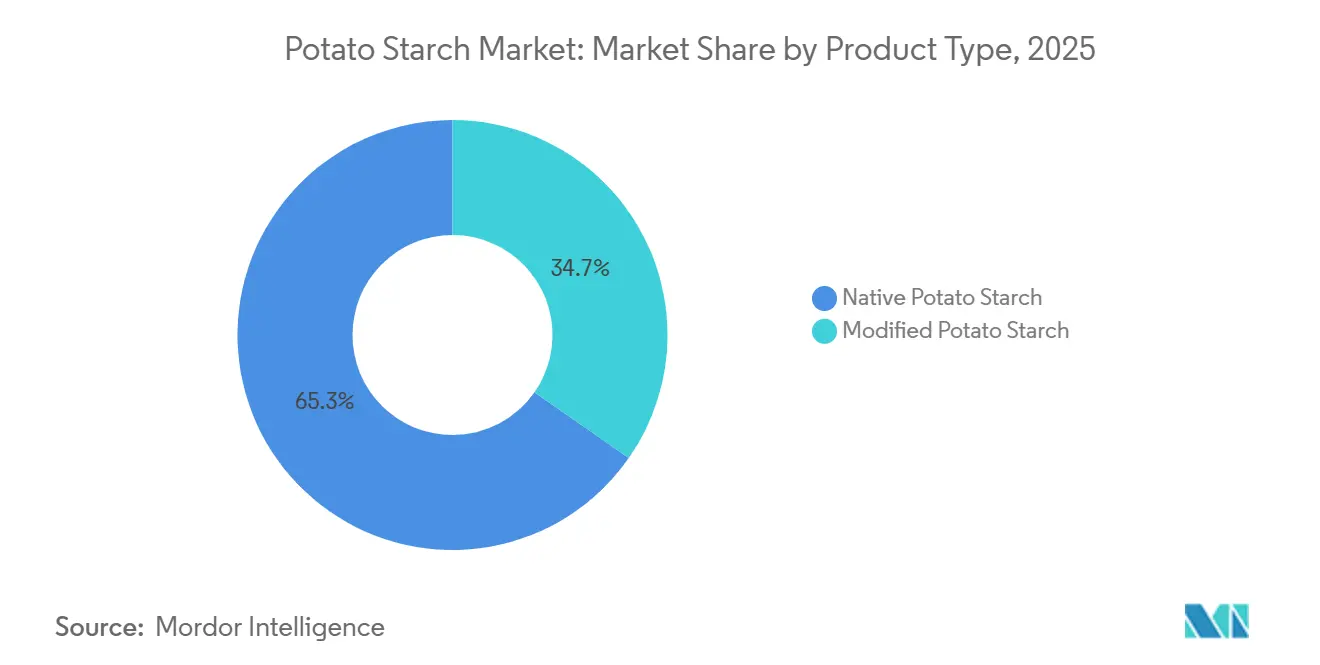

- By product type, native potato starch led with 64.96% of potato starch market share in 2025, while modified variants are advancing at a 7.82% CAGR through 2031.

- By nature, conventional grades accounted for 87.56% share of the potato starch market size in 2025, but organic grades are projected to post a 7.95% CAGR to 2031.

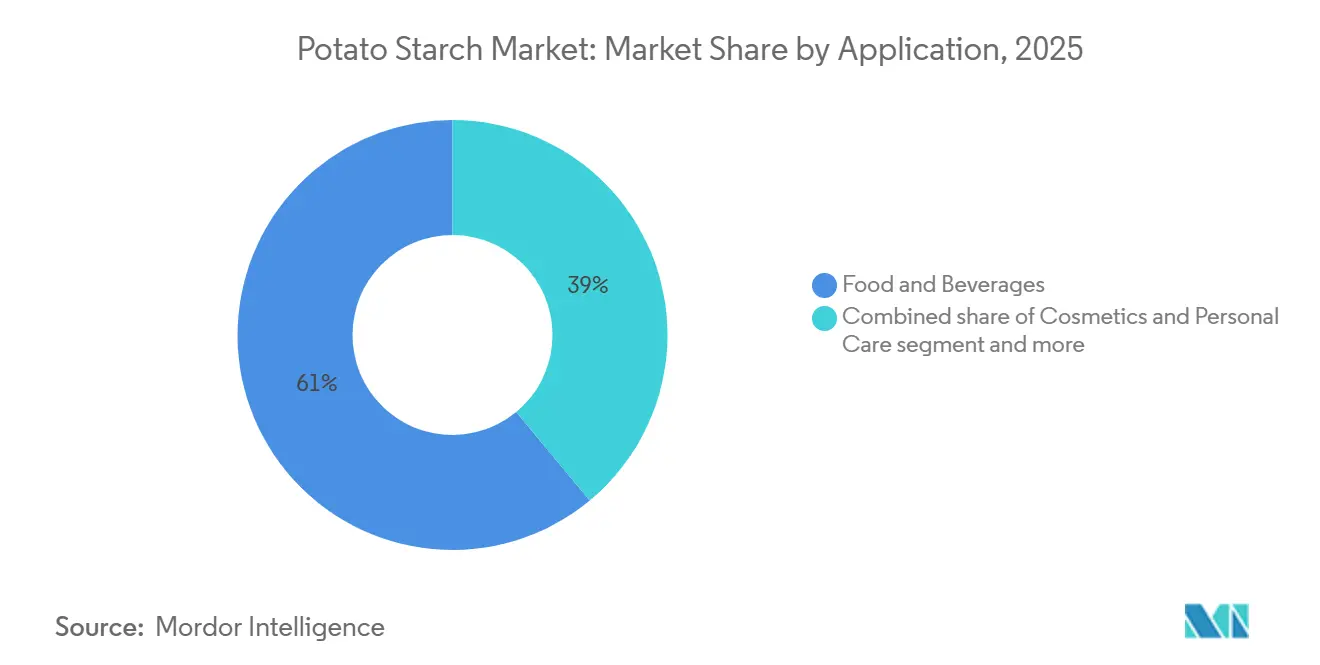

- By application, food and beverages held 61.02% of revenue in 2025, whereas cosmetics and personal care is forecast to expand at a 6.86% CAGR through 2031.

- By geography, Europe commanded 41.09% of the potato starch market in 2025; Asia-Pacific is the fastest-growing region at 7.57% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Potato Starch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing popularity of gluten-free ingredients | +0.8% | Global, with concentration in North America and Western Europe | Medium term (2-4 years) |

| Rising demand for processed and convenience foods | +1.2% | Global, strongest in Asia-Pacific urban centers and North America | Short term (≤ 2 years) |

| Growing adoption of plant-based and vegan ingredients | +1.0% | North America, Europe, Asia-Pacific urban markets | Medium term (2-4 years) |

| Technological advances in extraction and processing | +0.7% | Europe (Germany, Netherlands, Belgium), North America | Long term (≥ 4 years) |

| Organic and non-GMO positioning | +0.6% | North America, early adoption in Australia | Medium term (2-4 years) |

| Demand for ultra-low-protein starch as precision-fermentation feedstock | +0.5% | North America, Singapore, Israel (precision-fermentation hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing popularity of gluten-free ingredients

Gluten-free product formulators are increasingly utilizing potato starch due to its excellent water-binding capacity and neutral flavor. This approach helps replicate the tender crumb and moisture retention typically provided by wheat gluten. Substituting 10-20% of ingredients with potato starch in gluten-free bread and cakes allows formulators to achieve a desirable texture while avoiding the pasty mouthfeel often associated with corn or rice starches. Additionally, potato starch offers anti-staling properties that extend the shelf life of packaged bakery goods. Its functional benefits are particularly significant in frozen gluten-free products, where its freeze-thaw stability prevents syneresis and preserves structural integrity throughout distribution cold chains. According to the Celiac Disease Foundation, by 2025, over 70% of individuals with celiac disease will remain undiagnosed, with no treatments available beyond a gluten-free diet[1]Source: Celiac Disease Foundation, "2025 ANNUAL REPORT ", celiac.org. The prevalence of celiac disease in Western populations, coupled with the growing adoption of gluten-free diets for perceived health benefits, is expanding the market. This shift includes not only diagnosed patients but also health-conscious consumers willing to pay a premium for clean-label bakery alternatives. By blending potato starch with tapioca or corn starches, formulators can achieve an optimal balance. This combination integrates the rigid structure provided by corn with the elasticity of potato, enabling the development of multi-starch systems that meet both sensory and processing needs in high-volume gluten-free production lines.

Rising demand for processed and convenience foods

Urbanization and the increase in dual-income households are driving the demand for ready-to-eat meals, frozen entrees, and shelf-stable soups. These products depend on starches that can withstand retort sterilization, freeze-thaw cycles, and extended ambient storage without experiencing retrogradation or weeping. In 2024, the World Bank reported that 57.7% of the global population lived in urban areas[2]Source: World Bank, "World Population Data Sheet", worldbank.org. Potato starch, with its high amylopectin content (75-80% amylopectin compared to 20-25% amylose), creates smooth, glossy gels with minimal syneresis. This property makes it the preferred thickener for premium sauces, gravies, and dairy-alternative yogurts, where visual appeal and spoon-coating viscosity are key indicators of quality for consumers. The growing middle class in the Asia-Pacific region, particularly in China and India, is boosting demand for Western-style convenience foods such as instant noodles, snack bars, and microwaveable curries. These products utilize potato starch's dispersibility and low-temperature gelatinization (58-65°C) to ensure quick hydration and consistent texture during industrial batch processing. Processors value potato starch for its neutral pH (5-7) and lack of off-flavors, which simplify formulation across savory and sweet applications without the need for masking agents or flavor adjustments. The shift from traditional cooking to convenience foods is especially noticeable in Tier 2 and Tier 3 cities across Asia. In these areas, the expansion of modern retail and improvements in cold-chain infrastructure are enabling large-scale frozen food distribution. This trend is driving sustained growth in demand for functional starches, which help deliver restaurant-quality textures in meals reheated at home.

Growing adoption of plant-based and vegan ingredients

Potato starch, known for its film-forming and gelling properties, addresses technical challenges in plant-based dairy and meat alternatives, including emulsion stability, cheese melt-stretch, and burger moisture binding. KMC's CheeseMaker CF66, introduced in November 2024 and a finalist at the Fi Innovation Awards 2024, enables formulators to incorporate up to 8% plant protein (from pea and faba bean) into vegan cheese while maintaining the melt and stretch characteristics similar to dairy mozzarella. Avebe's ETENIA, a thermo-reversible potato starch, allows a 1% inclusion to replace 3% milk fat or 1% milk protein in both dairy and dairy-alternative formulations. This approach reduces ingredient costs while preserving a creamy mouthfeel and clean-label appeal. Potato starch also benefits plant-based meats, with its water-holding capacity of 74.95% (as supported by peer-reviewed studies) binding moisture during cooking and mitigating the dry, crumbly texture that has historically limited the acceptance of meat analogs. As precision fermentation scales up the production of animal-free proteins, the demand for ultra-low-protein potato starch (less than 0.1% protein) is increasing. This starch serves as a carbon and nitrogen source for microbial fermentation, creating a niche but high-value segment. This segment commands premium pricing and secures long-term supply agreements with biotech startups developing next-generation dairy and egg proteins. In 2025, The Good Food Institute reported that 24% of Americans were frequent or occasional consumers of plant-based meat, eating it at least once a month[3]Source: The Good Food Institute, "Consumer-Snapshot-Plant-Based-Meat-in-the-US," gfi.org. These consumption trends highlight the growing significance of potato starch in the expanding plant-based food sector.

Technological advances in extraction and processing

From 2024 to 2026, patent activity highlights a growing focus on specialty starches with customized functionalities. In 2025, Roquette obtained a US patent (12,247,088) that outlines a heat-modification process. This process enhances resistant-starch content to 60-66%, targeting gut-health applications in functional foods and pet nutrition, where prebiotic fibers are priced at a premium. Similarly, a Chinese patent (CN111171163A) introduces hydro-cyclone separator configurations. These configurations improve starch purity to over 99% while reducing water usage by recirculating process streams. This approach meets the high-quality standards for pharmaceutical excipients and addresses sustainability challenges in water-scarce regions. The reactor's advanced automation ensures batch-to-batch consistency by minimizing human error, which is critical for pharmaceutical-grade starches. These starches must comply with the stringent requirements of USP and European Pharmacopoeia monographs regarding swelling power (40.74 g/g), water-holding capacity, and solubility. Furthermore, the adoption of closed-loop water systems and enzyme-based modifications, which replace chemical cross-linking, is on the rise. These advancements enable processors to produce "clean-label modified starches" that cater to consumer demand for minimal processing while maintaining the freeze-thaw stability and shear resistance essential for industrial food production.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-potato prices | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Competition from alternative starches (corn, cassava, wheat) | -1.1% | Global, strongest in Asia-Pacific and Latin America | Medium term (2-4 years) |

| EU acrylamide-mitigation cost burden on fry and bakery processors | -0.4% | Europe | Medium term (2-4 years) |

| Slow, high-cost certification pipeline for organic potato starch | -0.3% | North America and EU, emerging in Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in raw-potato prices

FAO AgriPrice Monitor data indicates that by June 2026, potato prices rose 12.4% year-on-year. Processing-grade potatoes in the EU reached EUR 28.70 per 100 kg, reflecting a 9.2% increase, while US chipping stock prices increased by 14.6% to USD 32.40 per hundredweight. These price hikes have squeezed starch processor margins, prompting some operators to redirect lower-quality tubers from starch extraction to animal feed or biogas production. Climate-related yield disruptions, such as droughts in key European growing regions and excessive rainfall in North America, reduced average yields. Furthermore, post-harvest losses, driven by storage rot and mechanical damage during handling, surpassed historical norms. During the 2026 price spike, processors with fixed-price long-term contracts experienced margin erosion, while those relying on spot purchases faced rising input costs that outpaced their ability to pass them on to food manufacturers locked into annual supply agreements. The perishability of potatoes and their storage limitations, 6 to 9 months under controlled conditions, further exacerbate the volatility. Unlike grains, which can be stored for several years, potatoes cannot be stockpiled to buffer against price fluctuations.

Competition from alternative starches (corn, cassava, wheat)

Thailand exports 5.3 million tonnes of tapioca starch annually, representing 47% of the global cassava-starch trade. This tapioca starch, priced 15-25% lower than potato starch, features a neutral flavor, high clarity, and superior freeze-thaw stability. Consequently, it is capturing market share in sectors such as frozen ready meals, vegan cheese, and snack coatings, where its functional performance can be effectively replicated with modified blends. The Asia-Pacific region contributes approximately 72% of native tapioca starch production. Global cassava cultivation exceeds 313 million tonnes, primarily concentrated in tropical regions like Thailand, Vietnam, Indonesia, and Nigeria. These regions benefit from year-round growing cycles and lower labor costs, providing a structural cost advantage over potato production in temperate zones. Corn starch, although it has inferior freeze-thaw stability and tends to be opaque, dominates high-volume commodity applications, such as paper sizing, textile finishing, and adhesives, due to its lower cost and the scale efficiencies of integrated corn-wet-milling operations, which also produce sweeteners, ethanol, and animal feed. Modified tapioca starches are increasingly replacing potato starch in plant-based cheese applications. Ingredion's PURITY® P pea starch, along with other tapioca-based texturants, delivers comparable melt-stretch properties at lower formulation costs. This trend is pushing potato-starch suppliers to emphasize clean-label positioning and organic certification rather than functional superiority.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Modified Variants Gain as Processors Demand Retort Stability

Forecasts indicate that modified potato starch will achieve a robust CAGR of 7.82% through 2031, significantly outpacing the overall growth of the potato starch market. This growth is primarily attributed to the superior performance of enzyme-treated and oxidized grades, which demonstrate exceptional resilience against sterilization, shear forces, and freeze-thaw cycles. Emsland's innovative ROxy reactor plays a pivotal role in this segment by enhancing the production of specialty starches while simultaneously reducing energy consumption by 12%. This advancement positions Emsland as a cost-competitive supplier in the market. Additionally, Roquette's breakthrough patent on resistant starch has increased the RS2 content to 66%, enabling the company to penetrate high-value niches such as gut health and pet nutrition, both of which command premium pricing.

In 2025, native potato starch maintained a dominant 64.96% share of revenues, driven by its strong appeal in clean-label applications, particularly in gluten-free bakery products and baby foods. The anticipated delisting of organic corn starch in the U.S. is expected to further strengthen this segment. However, unmodified grades of potato starch face limitations, such as susceptibility to retrogradation, which restricts their use in frozen entrées. To address these challenges, processors are adopting a dual-sourcing strategy that combines the label-friendly simplicity of native starch with the functional reliability of modified starch. This balanced approach is expected to remain a key trend in the market through 2031.

By Nature: Organic Certification Unlocks Premium Pricing Despite Supply Constraints

Organic potato starch is anticipated to grow at a robust CAGR of 7.95%, driven by increasing demand for verified non-GMO ingredients in applications such as baby food, premium bakery products, and plant-based dairy alternatives. Northern Europe dominates the supply landscape, capitalizing on cooperative business models and Common Agricultural Policy (CAP) subsidies to reduce the risks associated with transitioning to organic production.

Conventional potato starch, which accounted for 87.56% of the market share in 2025, continues to benefit from economies of scale. However, challenges such as yield variability and the enforcement of stricter sustainability regulations are compelling processors to expand their portfolios into specialty and organic product lines. This strategic diversification helps mitigate risks related to raw material supply disruptions and profit margin pressures.

By Application: Cosmetics Surge as Talc-Free Formulations Gain Traction

In 2025, the food and beverage sector contributed 61.02% of the total revenue, highlighting the extensive versatility of potato starch in various applications. These include its use in sauces, dairy alternatives, meat binders, and gluten-free baked goods. A notable example is KMC's CheeseMaker CF66, a specialized functional grade that enables the inclusion of up to 8% plant protein in vegan cheese formulations, emphasizing the expanding and innovative use cases of potato starch.

In the cosmetics and personal care sector, which is projected to grow at a 6.86% CAGR, potato-starch powders are increasingly replacing talc. These powders not only effectively absorb oil but also provide a smooth, silky texture to the skin, enhancing product appeal. Furthermore, hydrogenated derivatives of potato starch improve the wearability of color cosmetics, while their biodegradable nature aligns with the growing demand for eco-friendly and sustainable product designs. Additionally, niche markets such as pharmaceuticals and animal feed offer incremental growth opportunities. This is particularly evident in the rising demand for resistant-starch fractions and protein concentrates, which are derived from process side-streams, further diversifying the applications of potato starch.

Geography Analysis

In 2025, Europe accounted for 41.09% of the global potato-starch market share. This dominance was supported by production hubs in Northern and Western Europe, particularly in Germany, the Netherlands, Belgium, and Poland. These countries significantly contribute to global potato-starch output and benefit from cooperative processing models, proximity to high-value food and pharmaceutical clients, and subsidies under the EU's Common Agricultural Policy, which promote organic transitions and sustainable farming practices. Additionally, Commission Regulation 2017/2158 established acrylamide-mitigation benchmarks of 500 µg/kg for French fries and 750 µg/kg for potato crisps. This regulation requires processors to implement measures such as low-temperature blanching, asparaginase enzyme pretreatment, and careful variety selection. However, these compliance costs disproportionately impact smaller fry and bakery processors, particularly in Southern and Eastern Europe.

Between 2026 and 2031, the Asia-Pacific region is expected to grow at a notable 7.57% CAGR, the fastest among all regions. This growth is driven by urbanization, rising middle-class incomes, and increasing demand for Western-style convenience foods, such as instant noodles, frozen entrees, and snack bars. These products require starches with rapid hydration, freeze-thaw stability, and consistent texture for industrial processing. China and India present the largest growth opportunities, with Tier 2 and Tier 3 cities experiencing rapid expansion of modern retail and cold-chain infrastructure. These developments enable large-scale frozen-food distribution, driving sustained demand for functional starches. However, the region faces strong competition from tapioca starch. Thailand, which exports 5.3 million tonnes annually, representing 47% of global cassava-starch trade, offers a neutral flavor and superior freeze-thaw stability. With prices 15-25% lower than potato starch, tapioca is gaining market share in frozen ready-meals and vegan cheese applications, where its functional properties can substitute potato starch. The region's growth will depend on potato-starch suppliers differentiating through organic certifications, specialty modifications like resistant and pre-gelatinized starches, and partnerships with precision-fermentation platforms developing animal-free proteins that require ultra-low-protein starch as fermentation feedstock.

North America, South America, and the Middle East and Africa are emerging as growth areas. North America benefits from its established food-processing infrastructure, export markets for specialty potato products, and early adoption of precision-fermentation technologies, which drive niche demand for ultra-low-protein starch as microbial feedstock. For instance, Ingredion announced a USD 50 million investment in its Cedar Rapids, Iowa facility, targeting specialty industrial starches for the packaging and papermaking industries. This investment highlights a shift toward biodegradable packaging and circular-economy materials. In South America, the potato-starch industry faces challenges such as fragmented production, infrastructure limitations, and competition from cassava and corn starches. Meanwhile, the Middle East and Africa struggle with supply constraints due to water scarcity, limited cold-chain infrastructure, and reliance on imports to meet domestic demand. A regulatory change by the USDA National Organic Standards Board, which plans to phase out conventional corn starch from the National List by 2027, is expected to drive short-term demand for organic potato starch in North America. However, supply constraints and a 20-30% price premium over conventional grades may pose challenges.

Competitive Landscape

The potato starch market shows moderate fragmentation. Companies such as Royal Avebe, Emsland Group, and Cargill hold significant shares of the market. Their dominance stems from their extensive operational scales, advanced processing capabilities, and diverse product portfolios that cater to a wide range of applications. These firms have built strong distribution networks and fostered long-term partnerships with suppliers and customers, which play a crucial role in maintaining their leadership positions within the market.

To remain competitive, companies are strategically focusing on increasing production capacities, adopting sustainable practices, and upgrading technological capabilities. A significant portion of their investments is directed toward organic production methods and compliance with stringent environmental regulations. The market offers substantial growth opportunities in specialized segments, such as pharmaceutical excipients, biodegradable packaging, and food applications requiring unique starch properties. These segments are particularly attractive due to their higher profit margins and the growing demand for tailored starch products that meet specific consumer and industrial needs.

New entrants, including technology-driven firms developing innovative processing methods and smaller companies targeting organic and specialty markets, are introducing fresh ideas and solutions to the industry. The increasing emphasis on environmental sustainability has led companies to participate in initiatives like the Science Based Targets program, which aims to reduce greenhouse gas emissions and enhance sustainability profiles. Achieving success in this market requires companies to effectively integrate advanced processing technologies with traditional production methods. This approach enables the creation of specialized, high-value products while maintaining cost efficiency and adhering to strict quality standards, ensuring they meet the evolving demands of the market.

Potato Starch Industry Leaders

-

KMC A/S-Kartoffelmelcentralen A.M.B.A.

-

Royal Avebe U.A.

-

Emsland Group

-

Cargill, Incorporated

-

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emsland Group has unveiled Emjel® LC 15, a novel functional starch tailored for vegan and vegetarian sweets. This innovative starch replicates gelatin's texture and processing simplicity, enabling atmospheric cooking and sidestepping the complexities of high-energy or vacuum systems.

- May 2025: KMC, a Danish specialist in potato ingredients, has partnered with Daymer Ingredients to distribute clean-label and functional potato starches in the UK food industry. The partnership begins with the distribution of native potato starch and plans to include specialized and modified starch solutions. This collaboration addresses the increasing demand for plant-based, allergen-free, and sustainable alternatives to gelatine, eggs, and dairy proteins.

- March 2025: Brenntag Specialties expanded its partnership with Royal Avebe into Poland. The agreement enables Brenntag to distribute Royal Avebe's potato starch and derivatives to food and nutrition customers in Poland. This expansion extends their existing collaboration across multiple European regions and aligns with Brenntag Specialties' portfolio optimization strategy.

Global Potato Starch Market Report Scope

Potato starch is starch extracted from potatoes. The cells of the root tubers of the potato plant contain leucoplasts. The potato starch market report is segmented by product type, nature, application, and geography. By product type, the market is segmented into native and modified. By nature, the market is segmented into conventional and organic. By application, the market is segmented into food and beverages, animal feed, pharmaceuticals, and cosmetics. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle east and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (Tons).

| Native Potato Starch |

| Modified Potato Starch |

| Conventional |

| Organic |

| Food and Beverages | Bakery and Confectionery |

| Snacks and Savory Products | |

| Dairy Alternatives | |

| Soups and Sauces | |

| Meat and Seafood Processing | |

| Others | |

| Animal Feed and Pet Nutrition | |

| Pharmaceuticals | |

| Cosmetics and Personal Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Vietrnam | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By product Type | Native Potato Starch | |

| Modified Potato Starch | ||

| By Nature | Conventional | |

| Organic | ||

| By Application | Food and Beverages | Bakery and Confectionery |

| Snacks and Savory Products | ||

| Dairy Alternatives | ||

| Soups and Sauces | ||

| Meat and Seafood Processing | ||

| Others | ||

| Animal Feed and Pet Nutrition | ||

| Pharmaceuticals | ||

| Cosmetics and Personal Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Vietrnam | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the global potato starch market by 2031?

It is forecast to reach USD 6.14 billion in 2031, expanding at a 6.22% CAGR between 2026-2031.

Which region is expected to record the fastest growth in demand for potato starch?

Asia-Pacific is projected to advance at a 7.57% CAGR through 2031, led by rising consumption of convenience foods in China and India.

Why are modified potato starch grades gaining share over native grades?

Enzyme-treated and oxidized variants withstand retort, freeze-thaw, and high-shear processing conditions without sacrificing clean-label status, making them better suited to ready meals, sauces, and vegan cheese.

What are the main competitive threats facing potato-starch producers?

Lower-cost tapioca and pea starches now match freeze-thaw stability and melt-stretch in many applications, pressuring potato-based solutions on price unless suppliers differentiate with specialty functionalities or certifications.

Page last updated on: