Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

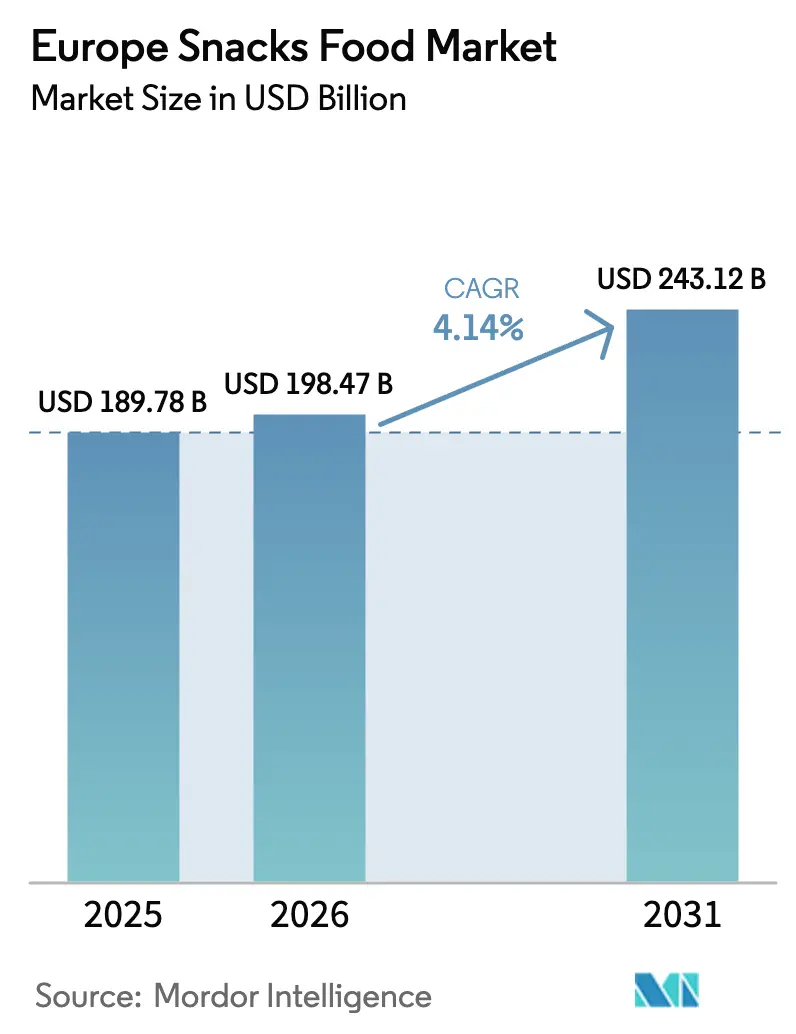

| Base Year Market Size (2025) | USD 189.78 Billion |

| Market Size (2026) | USD 198.47 Billion |

| Market Size (2031) | USD 243.12 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

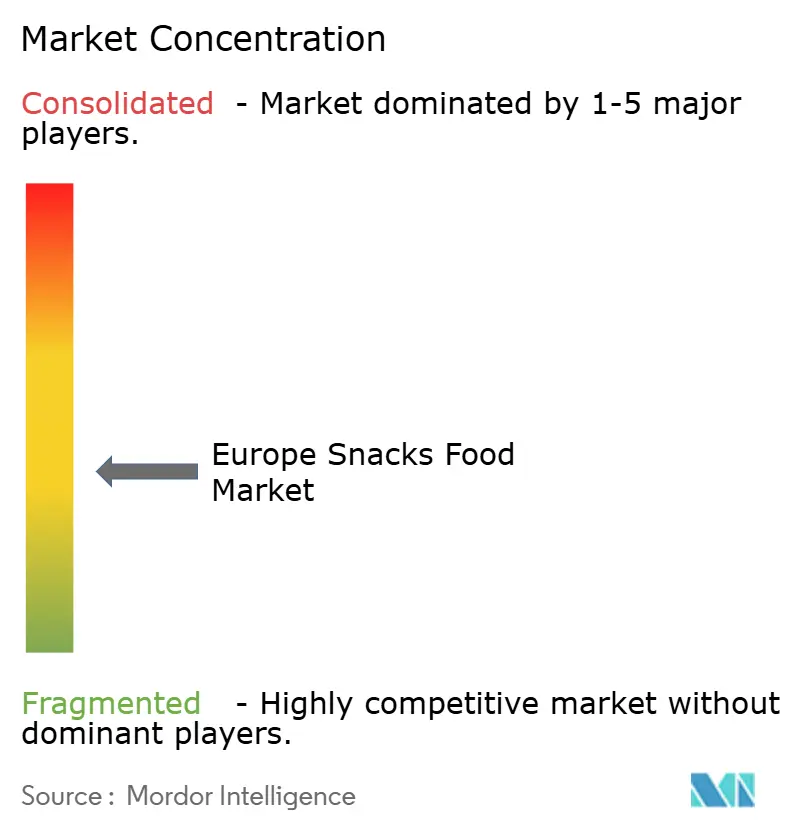

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Snacks Food Market Analysis by Mordor Intelligence

The Europe Snacks Food market size is projected to be USD 189.78 billion in 2025, USD 198.47 billion in 2026, and reach USD 243.12 billion by 2031, growing at a CAGR of 4.14% from 2026 to 2031. Convenience snacking now replaces meals for roughly half of daily eating occasions among consumers under 35, which is accelerating demand for portable, single-serve formats. Regulatory pressure around Nutri-Score labeling and the EU Packaging and Packaging Waste Directive is prompting wide-scale reformulation and packaging redesign, favoring companies able to fund compliance investments. Retailer consolidation has lifted private-label penetration to 39.1% of packaged food sales, squeezing branded margins while encouraging faster innovation cycles. At the same time, plant-based, organic, and frozen innovations are expanding assortment breadth, giving the European Snacks Food market fresh avenues for growth.

Key Report Takeaways

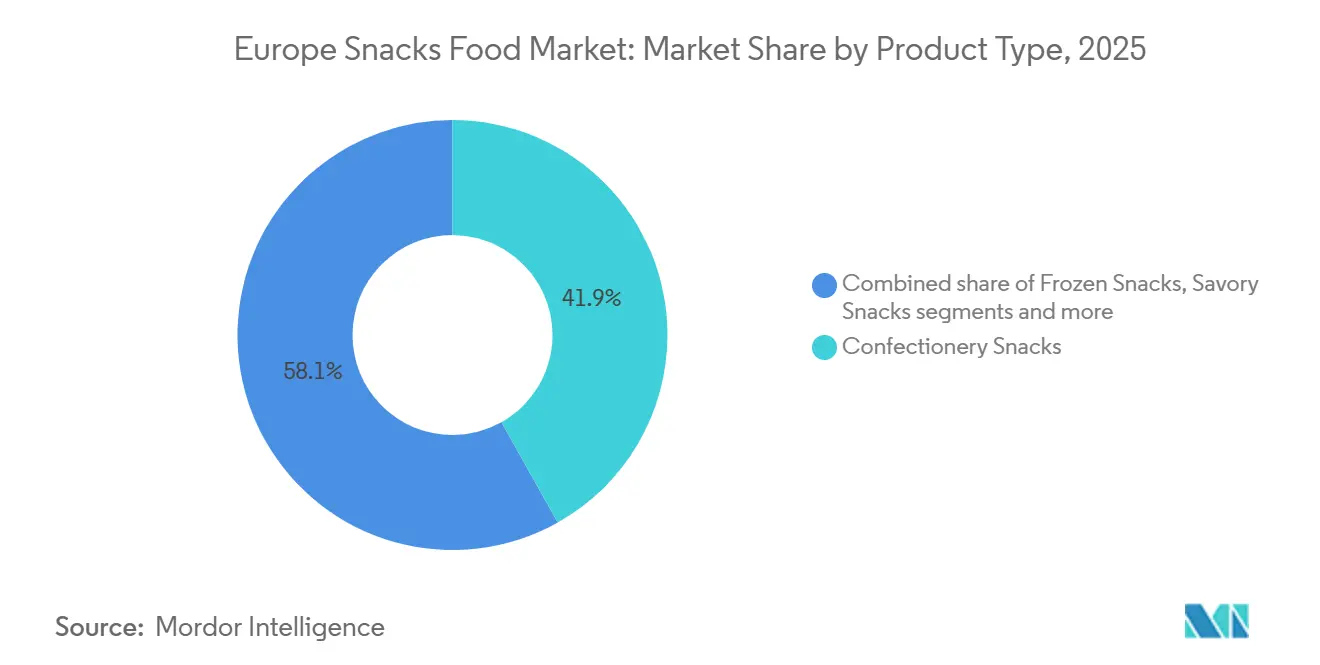

- By product type, confectionery snacks held 41.86% of the Europe Snacks Food market share in 2025, while frozen snacks are advancing at a 5.41% CAGR to 2031.

- By category, conventional products accounted for 63.12% of the Europe Snacks Food market size in 2025, yet organic and clean-label variants are growing at a 6.53% CAGR over 2026-2031.

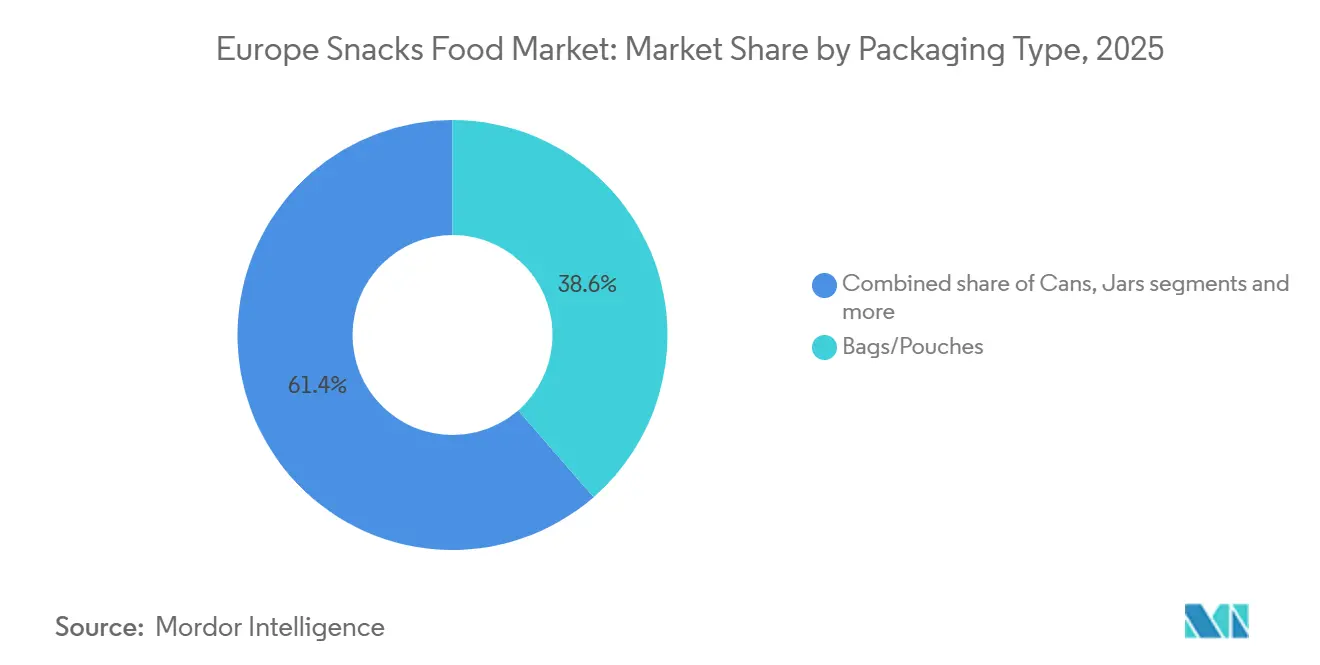

- By packaging, bags and pouches captured 38.55% of sales in 2025, whereas cans are expanding at a 4.73% CAGR through 2031 on the back of premiumization and recyclability advantages.

- By distribution, supermarkets and hypermarkets accounted for 54.62% of revenue in 2025, while online retail is growing at a 6.85% CAGR, supported by double-digit e-commerce growth expectations.

- By geography, the United Kingdom led with a 25.41% share in 2025, yet Germany is the fastest-growing country, with a 4.92% CAGR, driven by high per-capita organic spending.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Snacks Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenient on-the-go formats | +0.8% | Global, with highest penetration in UK, Germany, France | Medium term (2-4 years) |

| Growing consumer focus on health-oriented snacking | +0.7% | Western Europe core (UK, Germany, Netherlands, Sweden), expanding to Southern Europe | Long term (≥ 4 years) |

| Expansion of plant-based and vegan snacks | +0.6% | UK, Germany, Netherlands lead; spillover to France, Spain, Italy | Medium term (2-4 years) |

| Flavor innovation and gourmet premiumization | +0.5% | France, Italy, Spain Mediterranean corridor; UK premium retail | Short term (≤ 2 years) |

| Growth for premium organic, gluten-free, and clean-label snacks | +0.6% | Germany, Netherlands, Sweden, Switzerland; urban centers across Western Europe | Long term (≥ 4 years) |

| Popularity of Mediterranean and regional flavors | +0.4% | Southern Europe (Spain, Italy, France); export to Northern markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for convenient on-the-go formats

Snacking now constitutes half of daily eating occasions among European consumers under 35, fundamentally redefining meal architecture and driving demand for portable, single-serve formats that fit commuter lifestyles and hybrid work patterns. Mondelez International's 2025 State of Snacking report revealed that 59% of global consumers, rising to 64% in Western Europe, snack 2 to 3 times daily, with on-the-go consumption peaking during morning and afternoon dayparts[1]Source: Mondelez International, “The State of Snacking 2025,” mondelezinternational.com. This behavioral shift is propelling investment in resealable pouches, portion-controlled multipacks, and ambient-stable formats that eliminate refrigeration dependency. PepsiCo's July 2025 launch of "That's Nuts" coated peanuts in the UK, targeting a projected GBP 200 million (USD 255 million) segment by 2030, exemplifies how incumbents are engineering snacks for dashboard consumption and desk-drawer storage.

Growing consumer focus on health-oriented snacking

Health-conscious reformulation is no longer a niche differentiator but a baseline expectation, as 73% of European consumers actively seek snacks with reduced sugar, salt, or artificial additives, according to EIT Food's 2025 consumer trust survey. Glanbia's 2025 Better Nutrition report documented that 52% of global consumers, rising to 58% in Northern Europe, prioritize protein content when selecting snacks, driving the proliferation of high-protein bars, Greek yogurt-based bites, and legume-derived crisps[2]Source: Glanbia, “Better Nutrition Report 2025,” glanbia.com. This demand is reshaping product portfolios: Walkers reformulated its core range in August 2025 to comply with UK restrictions on high-fat, salt, and sugar (HFSS) products in prominent retail placements, cutting sodium by 15% without sacrificing taste perception. Mondelez's December 2025 introduction of sugar-free Oreos in select European markets signals a strategic pivot toward better-for-you indulgence, targeting consumers with diabetes and those managing their weight. The shift is quantifiable: UK organic snack sales reached GBP 3.7 billion (USD 4.7 billion) in 2024, growing 6% year-on-year, while Germany's organic food market hit EUR 16.1 billion, with snacks capturing an estimated 12% share, according to the Soil Association.

Expansion of plant-based and vegan snacks

Plant-based snacks are transitioning from specialty-store novelty to mainstream fixture, propelled by the European plant-based food market's expansion to EUR 5.4 billion in 2024, up 5.5% from the prior year, according to Good Food Institute Europe. Vegan and vegetarian consumers now represent 10% to 12% of the UK and German populations, yet flexitarians, those reducing animal product intake without full elimination, drive 60% of plant-based snack purchases, creating a TAM far exceeding strict dietary adherents, according to Good Food Institute Europe. This demographic breadth is attracting legacy players: Nestlé invested EUR 44.2 million in its Bulgarian KitKat factory in February 2025 to expand tablet production, including plant-based variants targeting the CHF 7.5 billion European tablet segment. The Centre for the Promotion of Imports from developing countries (CBI) documented that European imports of plant-based snacks from Asia and Latin America surged 18% in 2024, reflecting supply-chain diversification and cost arbitrage. Regulatory tailwinds include the EU's Farm to Fork strategy, which incentivizes plant-protein innovation through research and development grants and sustainability certifications, lowering barriers for startups and co-manufacturers.

Growth for premium organic, gluten-free, and clean-label snacks

Clean-label positioning, defined by short ingredient lists, recognizable components, and absence of artificial additives, has evolved from a marketing claim to table stakes, as 68% of European shoppers actively read ingredient panels before purchase, per EIT Food's 2025 trust index. Western European organic food sales reached EUR 22 billion in 2024, with the Organic Trade Association reporting sustained double-digit growth in snack subcategories such as organic nuts, seeds, and fruit bars[3]Source: Organic Trade Association, “Western European Organic Food Sales Reach EUR 22 Billion in 2024,” ota.com . Germany anchors this trend, with EUR 16.1 billion in organic food sales and per-capita organic expenditure exceeding EUR 190, the highest globally, according to the Federal Statistical Office of Germany. Gluten-free snacks are capturing incremental share beyond celiac sufferers, appealing to consumers who associate gluten avoidance with digestive wellness and weight management, despite limited clinical evidence for non-celiac populations. The UK's Soil Association certified over 8,500 organic products in 2024, including 1,200 snack SKUs, reflecting supply-side responsiveness to retailer mandates for clean-label assortments. Regulatory influence is indirect but material: the EU Organic Regulation (2018/848) standardizes certification criteria, reducing compliance friction for cross-border trade and enabling smaller producers to access pan-European distribution networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over salt, sugar, and ultra-processed foods | -0.5% | EU-wide, with strictest enforcement in France, Netherlands, Belgium, Germany | Long term (≥ 4 years) |

| Competition from fresh and whole-food alternatives | -0.3% | Western Europe urban centers; Nordic countries | Medium term (2-4 years) |

| Stringent EU regulations and labeling requirements | -0.4% | EU-27, with national variations in enforcement (France, Spain, Belgium lead) | Long term (≥ 4 years) |

| Environmental scrutiny on packaging waste | -0.3% | Germany, Netherlands, Sweden, France; EU-wide Extended Producer Responsibility | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns over salt, sugar, and ultra-processed foods

Public-health campaigns targeting sodium, added sugars, and consumption of ultra-processed foods are constraining formulation latitude and eroding category appeal among health-conscious segments. The World Health Organization's 2025 guidance recommends limiting ultra-processed foods to less than 10% of daily caloric intake, citing epidemiological links to obesity, cardiovascular disease, and metabolic syndrome. France's mandatory Nutri-Score labeling, effective from 2026 onward, assigns color-coded grades (A through E) based on nutrient profiles, with many traditional snacks scoring D or E, triggering consumer avoidance and retailer de-listing, according to the European Commission. Seven EU member states have adopted Nutri-Score or equivalent front-of-pack schemes, creating compliance fragmentation that raises labeling costs for pan-European brands. The European Commission's salt-reduction initiative targets 16% cuts across processed foods by 2030, forcing reformulation investments that can exceed EUR 50 million per major portfolio. Walkers' August 2025 reformulation to meet UK HFSS restrictions illustrates the operational complexity: the brand reduced sodium by 15% while maintaining taste through umami enhancers and flavor encapsulation, a process requiring 18 months of research and development.

Competition from fresh and whole-food alternatives

Fresh produce, nuts, and minimally processed whole foods are capturing snack occasions previously dominated by packaged goods, particularly among millennials and Gen Z consumers who prioritize ingredient transparency and sustainability. European shoppers increased their purchases of fresh food, with snacking occasions shifting toward fruit, vegetable sticks, and bulk nuts purchased from supermarket perimeter sections. This trend is structural rather than cyclical: urbanization and proximity to fresh-food retailers reduce the convenience premium of ambient snacks, while social-media influencers amplify whole-food narratives through platforms such as Instagram and TikTok. The British Retail Consortium reported that UK fresh produce sales reached GBP 12.8 billion (USD 16.3 billion) in 2024, growing 4.2% year-on-year, outpacing packaged snacks' 3.1% growth[4]Source: British Retail Consortium, “UK Retail Sales Data 2024,” brc.org.uk . Retailers are responding by expanding fresh-cut fruit and vegetable offerings in convenience formats, directly competing with packaged snacks for impulse purchases. The substitution effect is most pronounced in Northern Europe, where organic whole-food penetration exceeds 15% of grocery spend, and in Mediterranean markets, where cultural preferences for fresh ingredients remain entrenched.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Frozen Snacks Lead Innovation Velocity

Frozen Snacks are expanding at a 5.41% CAGR through 2031, the fastest pace among product types, as manufacturers leverage cold-chain infrastructure to deliver high-protein, portion-controlled formats that straddle indulgence and nutrition. Nomad Foods' 2024 consumer research revealed that 36% of European households prefer snacking from the freezer, driven by extended shelf life, reduced food waste, and the ability to stock a diverse range of options without daily shopping trips. Unilever's January 2026 launch of Carte D'Or Sundaes with dual-compartment packaging, separating ice cream from toppings until consumption, exemplifies the category's innovation trajectory, targeting premiumization through experiential eating. FRO ZEN Power's March 2025 introduction of high-protein ice cream bars in Austria and Germany, delivering 8.4 grams of protein per 60-gram serving, illustrates how frozen formats are absorbing health-and-wellness trends from ambient categories. Tesco's September 2025 relaunch of 270 frozen products, its largest refresh since 2018, signals retailer confidence in category momentum.

Confectionery Snacks commanded 41.86% market share in 2025, anchored by chocolate tablets, sugar confectionery, and gum, yet face headwinds from Nutri-Score labeling and sugar-reduction mandates. Nestlé's EUR 44.2 million investment in its Bulgarian KitKat factory in February 2025, targeting the CHF 7.5 billion (USD 8.4 billion) European tablet segment, underscores incumbents' commitment to defending share through capacity expansion and SKU proliferation. Savory Snacks, crisps, extruded snacks, nuts, benefit from on-the-go portability and flavor innovation, with PepsiCo's July 2025 "That's Nuts" launch projecting a GBP 200 million (USD 255 million) UK segment by 2030. Fruit Snacks and Bakery Snacks are capturing health-conscious consumers through clean-label positioning and whole-grain formulations, while Meat Snacks remain niche but are growing through protein-forward messaging. Other Product Types, including dairy-based and hybrid formats, are fragmenting the category into micro-segments that defy traditional classification.

By Category: Organic/Clean-Label Outpaces Conventional

Organic/Clean-Label snacks are advancing at a 6.53% CAGR through 2031, nearly double the overall market rate, as Western European consumers prioritize ingredient transparency and sustainability certifications. Western European organic food sales reached EUR 22 billion in 2024, with Germany contributing EUR 16.1 billion, and per-capita organic expenditure exceeding EUR 190, the highest globally, according to the Organic Trade Association. The UK's Soil Association certified over 8,500 organic products in 2024, including 1,200 snack SKUs, reflecting supply-side responsiveness to retailer mandates. Clean-label positioning, short ingredient lists, recognizable components, and the absence of artificial additives have evolved from niche differentiators to baseline expectations, with EIT Food's 2025 survey finding that 68% of European shoppers actively read ingredient panels before purchase. The EU Organic Regulation (2018/848) standardizes certification criteria, reducing compliance friction for cross-border trade and enabling smaller producers to access pan-European distribution networks.

Conventional snacks retained 63.12% market share in 2025, anchored by legacy brands, price-sensitive consumers, and impulse-purchase occasions where ingredient scrutiny is minimal. Conventional manufacturers are responding through reformulation and hybrid positioning, reducing sodium and sugar while maintaining mass-market pricing, as evidenced by Walkers' August 2025 HFSS-compliant reformulation. The category's resilience stems from its breadth: it encompasses value-tier products serving cost-conscious households, mid-tier brands balancing quality and affordability, and premium conventional SKUs that eschew organic certification while emphasizing provenance and craftsmanship.

By Packaging Type: Cans Gain Ground Through Premiumization

Bags/Pouches held 38.55% of packaging share in 2025, dominating crisps, extruded snacks, and confectionery through cost efficiency, lightweight logistics, and resealable convenience. However, Cans are expanding at a 4.73% CAGR through 2031, driven by premiumization in ready-to-eat segments, superior shelf-life performance, and recyclability credentials that resonate with sustainability-conscious consumers. Aluminum cans achieve 75% recycling rates in Europe, exceeding flexible plastics' 40% rates, and are exempt from many single-use plastic taxes, creating a cost-of-compliance advantage, according to the European Commission. The format is migrating beyond beverages into nuts, protein snacks, and portion-controlled confectionery, with brands leveraging the tactile premium cues of cans and billboard-sized labeling real estate. Jars capture niche segments such as olives, pickled vegetables, and nut butters, where glass conveys quality and enables pantry display, while Others, including rigid trays, cartons, and hybrid formats, serve specialized applications such as bakery snacks and frozen novelties.

The EU Packaging and Packaging Waste Directive's 65% recycling target by 2025 and proposed reuse mandates for 2030 are accelerating innovation in mono-material films, compostable substrates, and refillable pouches, each commanding 15% to 25% cost premiums over conventional polyethylene, according to the European Commission[5]Source: European Commission, “Packaging and Packaging Waste Directive,” europa.eu. Germany's VerpackG imposes EPR fees that escalate for non-recyclable materials, incentivizing paper-based pouches despite inferior moisture barriers. Mars' EUR 1 billion European investment includes commitments to 100% recyclable packaging by 2025 and 30% recycled content by 2030, targets that require supplier audits and material science research and development. Consumer sentiment is amplifying regulatory pressure: EIT Food's 2025 survey found that 62% of European shoppers consider packaging sustainability when selecting snacks, with 41% willing to pay premiums for eco-friendly alternatives.

By Distribution Channel: Online Retail Disrupts Traditional Footprints

Online Retail is surging at a 6.85% CAGR through 2031, the fastest-growing distribution channel, propelled by high internet penetration and annual expansion in European online food and beverage sales. TikTok's emergence as an online food and beverage retailer in Europe is compressing discovery-to-trial cycles, as viral snack content drives impulse purchases and enables niche brands to bypass traditional retail gatekeepers. Supermarkets/Hypermarkets captured 54.62% of the distribution share in 2025, leveraging scale economies, one-stop shopping convenience, and promotional firepower to defend incumbency. However, the channel faces margin pressure from private-label proliferation, driven by footfall declines in suburban big-box formats as urbanization concentrates populations near smaller-format stores.

Convenience Stores serve top-up missions and impulse purchases, capturing commuter traffic and late-night occasions, yet face competition from online rapid-delivery services that promise 15-minute fulfillment. Other Distribution Channels, including vending machines, petrol stations, and foodservice outlets, are fragmenting into micro-channels that require SKU-specific strategies and packaging formats. The British Retail Consortium reported that UK snack sales through convenience formats grew 5.2% in 2024, outpacing supermarkets' 3.1% growth, illustrating channel-mix shifts.

Geography Analysis

The United Kingdom accounted for 25.41% of Europe Snack Food market share in 2025, anchored by GBP 4.2 billion (USD 5.4 billion) in snack sales documented by the British Retail Consortium, yet faces structural headwinds from post-Brexit trade friction and HFSS regulations that restrict prominent placement of high-fat, salt, and sugar products. PepsiCo's July 2025 launch of "That's Nuts" coated peanuts, targeting a projected GBP 200 million (USD 255 million) segment by 2030, illustrates how incumbents are engineering products for regulatory compliance while capturing premiumization upside. The UK's Soil Association certified over 8,500 organic products in 2024, including 1,200 snack SKUs, reflecting supply-side responsiveness to clean-label mandates. Germany is expanding at 4.92% CAGR through 2031, the fastest geographic growth, driven by EUR 16.1 billion in organic food sales and per-capita snack expenditure exceeding EUR 200 annually, according to the Federal Statistical Office of Germany. German consumers prioritize sustainability certifications and ingredient transparency, with 72% actively seeking organic or clean-label snacks, per EIT Food's 2025 survey. France mandates Nutri-Score labeling from 2026 onward, forcing portfolio rationalization and reformulation investments that can exceed EUR 100 million per major manufacturer.

Italy and Spain anchor Mediterranean snack consumption, leveraging Protected Designation of Origin (PDO) and Protected Geographical Indication (PGI) certifications to command premium pricing and export to Northern markets. Spanish olive-oil crisp exports to Germany rose 22% in 2024, capitalizing on the Mediterranean diet's health halo and culinary tourism exposure Journal of Ethnic Foods. Ferrero's October 2025 launch of five new products in Italy, including Nutella Crêpe frozen snacks and Kinder extensions, illustrates how Southern European manufacturers are leveraging brand equity to enter adjacent premium categories. The Netherlands and Sweden lead Northern European sustainability trends, with Dutch and Swedish consumers exhibiting the highest willingness to pay premiums for eco-friendly packaging and organic certifications. The Netherlands' plastic tax of EUR 0.80 to EUR 1.20 per kilogram is incentivizing paper-based pouches and aluminum cans, despite inferior moisture barriers. Sweden's organic food penetration exceeds 15% of grocery spend, the highest in Europe, driven by government subsidies for organic agriculture and retailer commitments to sustainable sourcing.

Poland represents Eastern Europe's fastest-growing market, propelled by rising disposable incomes, urbanization, and Western-format retail expansion. Swiss consumers exhibit the highest per-capita snack expenditure in Europe, exceeding EUR 250 annually, driven by premium positioning and tourism-related consumption. Russia's market trajectory remains uncertain due to geopolitical sanctions and supply-chain disruptions, yet domestic manufacturers are capturing share previously held by Western multinationals. Rest of Europe, encompassing Belgium, Austria, Portugal, and smaller markets, collectively contributes approximately 15% of regional revenue, with Belgium's adoption of Nutri-Score in 2025 signaling regulatory convergence across smaller member states.

Competitive Landscape

The Europe Snacks Food market exhibits moderate fragmentation, signaling that the top 5 players, General Mills, PepsiCo, Nestlé, Intersnack, and Mondelez, collectively command approximately 35% to 40% share, leaving substantial white space for regional specialists and private-label programs. Mars Inc.'s USD 36 billion acquisition of Kellanova, approved in December 2025, consolidates Pringles, Cheez-It, and Mars' existing portfolio into a unified USD 36 billion snacking entity, reshaping competitive dynamics by creating a vertically integrated platform spanning savory, confectionery, and frozen segments. This mega-merger follows Ferrero's USD 3.1 billion purchase of WK Kellogg in late 2025, illustrating how incumbents are leveraging mergers and acquisitions to capture scale economies, cross-category synergies, and geographic footprint expansion. The European Commission's antitrust scrutiny throughout 2025 delayed several transactions, signaling heightened regulatory vigilance around market concentration and potential anti-competitive effects.

Strategy patterns cluster around three vectors: reformulation to comply with Nutri-Score and HFSS mandates, capacity investments in high-growth segments such as frozen and organic, and omni-channel distribution that integrates brick-and-mortar with direct-to-consumer e-commerce. Mars' EUR 1 billion European investment commitment through end-2026 includes EUR 300 million for regulatory compliance, EUR 400 million for capacity expansion, and EUR 300 million for sustainability initiatives, exemplifying the capital intensity of defending incumbency. White-space opportunities are emerging in plant-based frozen snacks, high-protein ambient formats, and hyper-local provenance narratives that smaller players can exploit without competing on scale. Fairfields Farm Crisps and Tayto Group are carving defensible niches through single-origin sourcing, heritage branding, and retail partnerships that emphasize traceability over volume.

TikTok's emergence as the online food and beverage retailer in Europe is democratizing access to consumers, enabling niche brands to bypass traditional retail gatekeepers and achieve viral distribution through influencer partnerships. Technology deployment is bifurcating: multinationals are investing in AI-driven demand forecasting, dynamic pricing algorithms, and blockchain-enabled traceability to optimize supply chains and substantiate sustainability claims, while smaller players leverage social commerce and subscription models to build direct relationships with consumers. The Good Food Institute Europe documented that the EUR 5.4 billion European plant-based food market, growing 5.5% in 2024, is attracting venture capital and corporate venture arms, signaling that disruptors are accessing capital to scale production and distribution. Regulatory compliance is emerging as a competitive moat: brands that proactively reformulate for Nutri-Score and invest in recyclable packaging gain first-mover advantages in retailer assortment decisions and consumer preference.

Europe Snacks Food Industry Leaders

General Mills, Inc.

PepsiCo Inc.

Nestlé S.A.

Intersnack Group GmbH

Mondelez International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Unilever launched Carte D'Or Sundaes featuring dual-compartment packaging that separates ice cream from toppings until consumption, targeting premiumization in the European frozen dessert segment through experiential eating and extended shelf life.

- December 2025: Mondelez International introduced sugar-free Oreos in select European markets, leveraging sucralose and acesulfame potassium to deliver zero-sugar indulgence and capture diabetic and weight-management demographics.

- November 2025: Frostkrone launched Cheesy Loops, a frozen snack targeting children and families, expanding its portfolio beyond traditional frozen meals into the high-growth frozen snacking category.

- October 2025: Ferrero unveiled five new products in Italy, including Nutella Crêpe frozen snacks, Kinder Bueno ice cream bars, and Kinder Chocolate extensions, investing EUR 25 million (USD 27 million) in production capacity to support the launches.

Europe Snacks Food Market Report Scope

Snack food is a small portion of food consumed between meals. There are different varieties of snack foods that are helpful when consumed, as they support weight management and enhance blood glucose control. The European snack food market (hereinafter, the market studied) is segmented by type, category, packaging type, distribution channel, and geography. By type, the market is segmented into frozen snacks, savory snacks, fruit snacks, confectionery snacks, bakery snacks, meat snacks, and other product types. The market is segmented into organic and conventional categories. Based on the packaging type, the market is segmented into bags/pouches, jars, cans, and others. Based on the distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online stores, and other distribution channels. It provides an analysis of emerging and established economies in Europe, comprising Spain, the United Kingdom, Germany, France, Italy, Russia, and the Rest of Europe. For each segment, market sizing and forecasts have been prepared on a value basis (USD million) and on a volume basis (tons).

By Product Type

| Frozen Snacks |

| Savory Snacks |

| Fruit Snacks |

| Confectionery Snacks |

| Bakery Snacks |

| Meat Snacks |

| Other Product Types |

By Category

| Conventional |

| Organic/Clean-Label |

By Packaging Type

| Bags/Pouches |

| Jars |

| Cans |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Poland |

| Switzerland |

| Russia |

| Rest of Europe |

| By Product Type | Frozen Snacks |

| Savory Snacks | |

| Fruit Snacks | |

| Confectionery Snacks | |

| Bakery Snacks | |

| Meat Snacks | |

| Other Product Types | |

| By Category | Conventional |

| Organic/Clean-Label | |

| By Packaging Type | Bags/Pouches |

| Jars | |

| Cans | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Switzerland | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe snacks food market in 2026?

The market is valued at USD 197.53 billion in 2026.

What CAGR is projected for European snack sales through 2031?

A 4.08% CAGR is forecast for the period 2026-2031.

Which category is growing fastest within European snacks?

Frozen snacks are expected to post the highest CAGR at 6.92%

Which country leads regional snack revenues?

The United Kingdom holds the largest share at 25.41% of 2025 sales.

Page last updated on: