Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

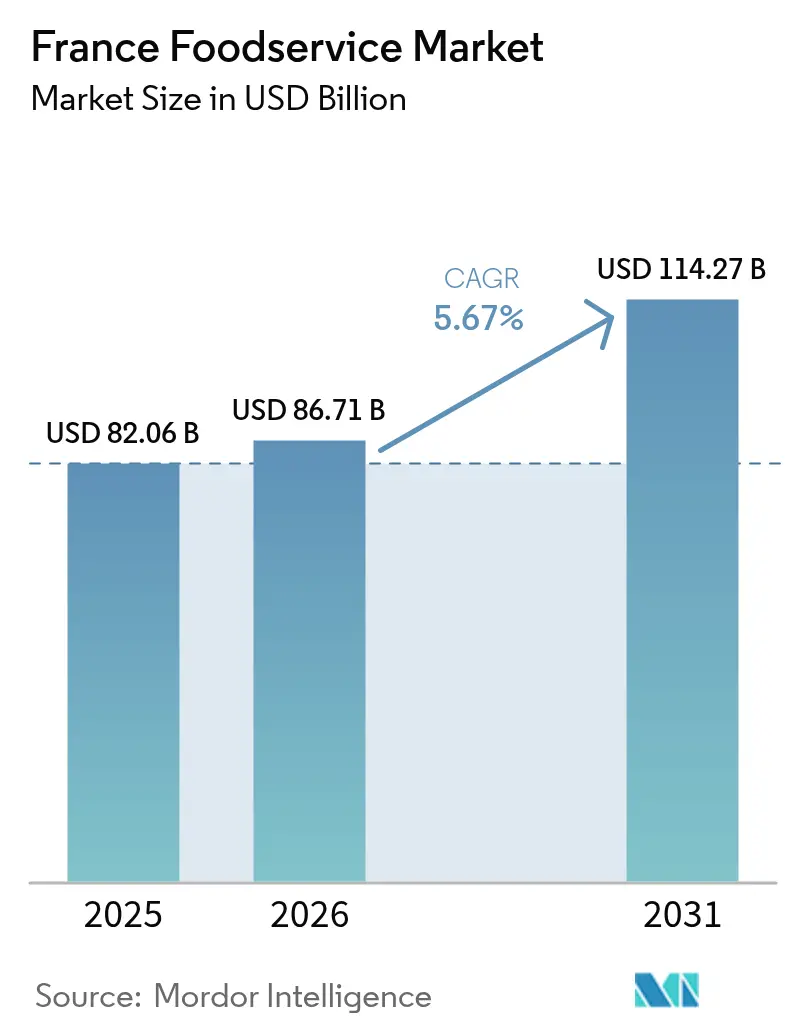

| Base Year Market Size (2025) | USD 82.06 Billion |

| Market Size (2026) | USD 86.71 Billion |

| Market Size (2031) | USD 114.27 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

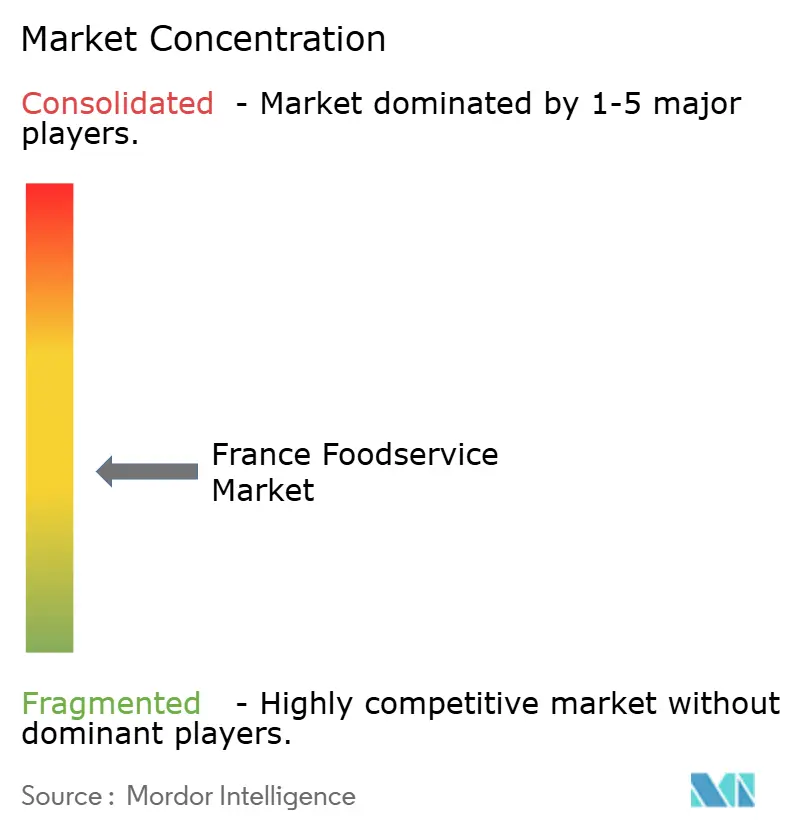

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Foodservice Market Analysis by Mordor Intelligence

France foodservice market size in 2026 is estimated at USD 86.71 billion, growing from 2025 value of USD 82.06 billion with 2031 projections showing USD 114.27 billion, growing at 5.67% CAGR over 2026-2031. Growth is driven by digital ordering systems, sustainability mandates, and a lasting consumer preference for convenience post-pandemic. Quick service restaurants (QSRs), or fast-food restaurants, are expanding the market with innovative menus and kitchen automation, while cloud kitchens, also known as virtual kitchens, attract entrants by reducing real estate risks and accelerating market entry. Technological advancements, such as artificial intelligence (AI)-enabled inventory tracking and smart kitchen equipment, address labor shortages by optimizing operations and reducing waste. Mandatory carbon footprint audits and over 100 MICHELIN Green Star restaurants are driving investments in renewable energy and recycled packaging. Tourism recovery boosts transit location sales, though seasonality in coastal and alpine markets challenges working-capital management. Independent operators increasingly use digital platforms with dynamic demand forecasting to adapt to consumer demand, secure contracts, and improve efficiency.

Key Report Takeaways

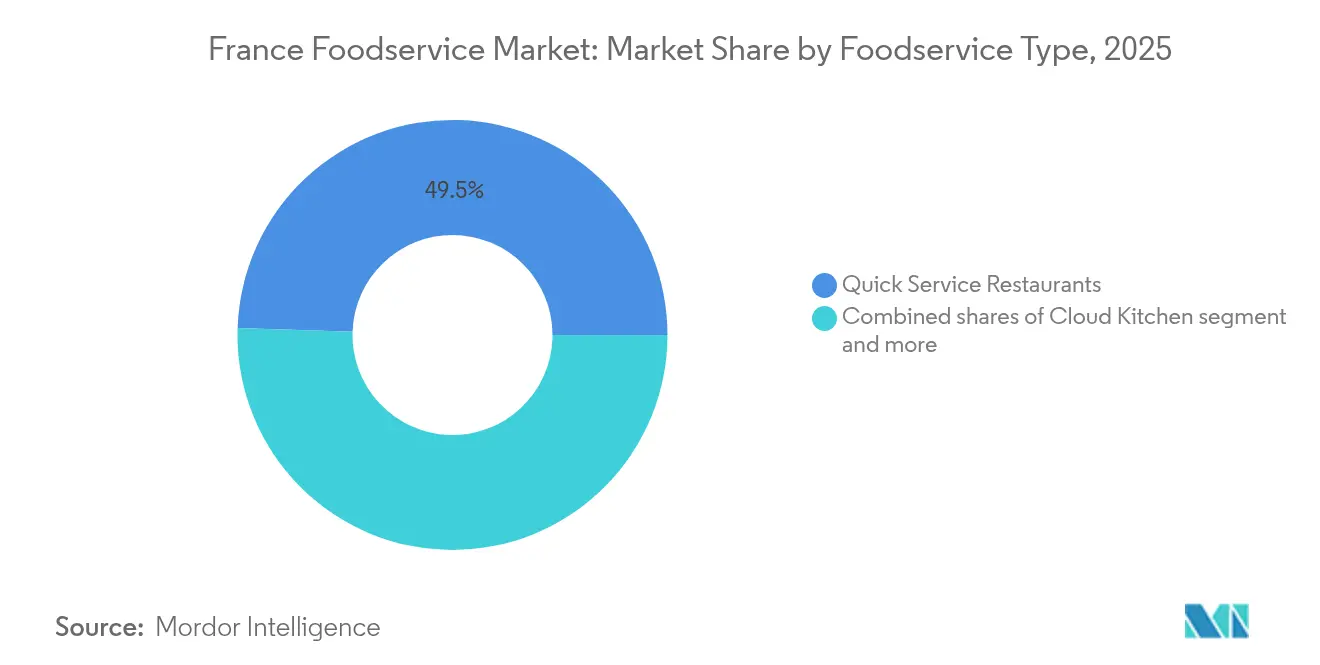

- By foodservice type, quick service restaurants accounted for 49.48% of the France foodservice market share in 2025, while cloud kitchens registered the highest CAGR of 11.83% during the forecast period through 2031.

- By outlet, independent operators commanded 68.05% share of the France foodservice market size in 2025, whereas chained outlets recorded the fastest 6.88% CAGR through 2031.

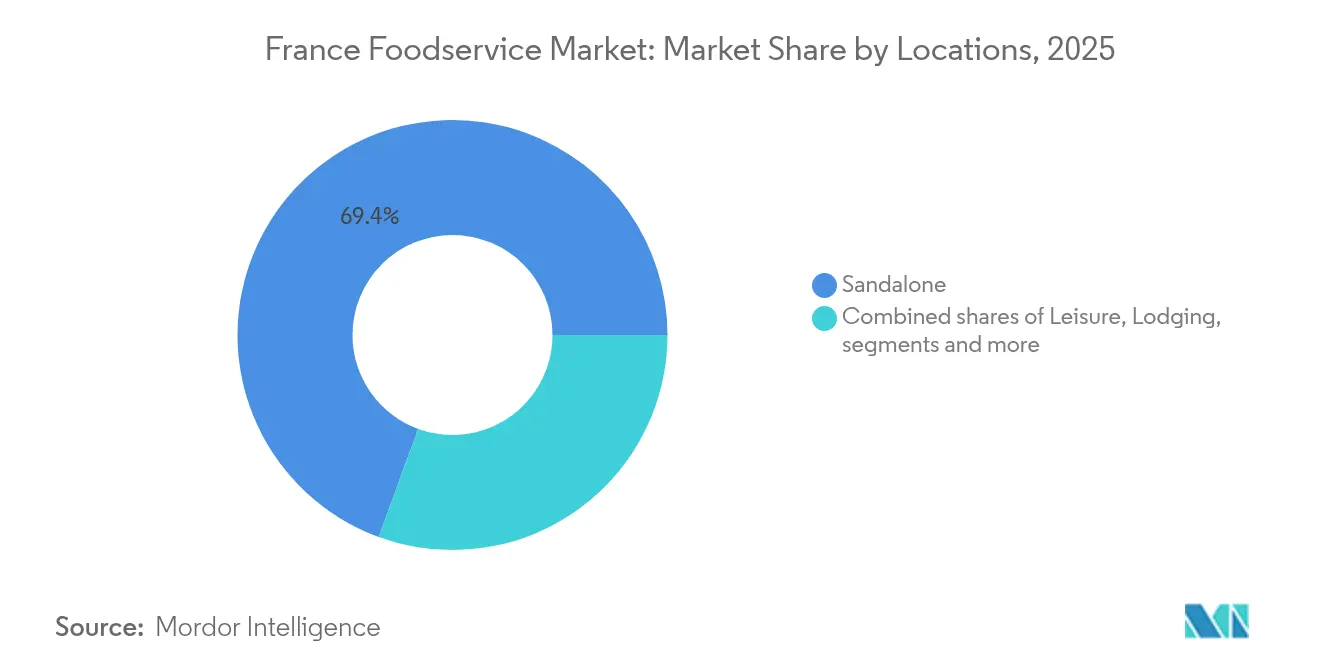

- By location, standalone venues captured 69.42% share of the France foodservice market size in 2025, while travel-focused formats are advancing at a 9.71% CAGR to 2031.

- By service type, dine-in represented 54.76% revenue share in 2025, yet delivery is expanding at an 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for plant-based and organic menu options | +1.2% | National, with concentration in Paris, Lyon, Marseille | Medium term (2-4 years) |

| Adoption of sustainability initiatives | +0.8% | National, driven by urban centers and tourist regions | Long term (≥ 4 years) |

| Rising interest in health-conscious and allergen-free menus | +0.9% | National, particularly in metropolitan areas | Short term (≤ 2 years) |

| Proliferation of cloud kitchens and virtual restaurant brands | +1.1% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Innovation in menu personalization and smart kitchen solutions | +0.7% | Major cities, gradual rollout to regional markets | Medium term (2-4 years) |

| Expansion of convenience-focused takeaway and ready-to-eat offerings | +0.6% | National, with urban concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Plant-Based and Organic Menu Options

Plant-based menu adoption gained momentum after the Paris 2024 Olympics, where 60% of meals served included plant-based options, setting a new standard for large-scale foodservice operations [1]Source: ProVeg International, “Plant-Based Catering at Paris 2024 Olympics,” proveg.com. French consumers increasingly view plant-based dining as a premium experience rather than a dietary limitation, with organic food sales in the foodservice sector growing at an annual rate of 15%. This trend reflects broader cultural changes, where sustainability is becoming a status symbol, particularly among urban millennials and Gen Z consumers who prioritize environmental considerations in their dining choices. Restaurant chains report that plant-based menu items yield 23% higher profit margins compared to traditional offerings, driven by lower ingredient costs and consumer acceptance of premium pricing. This trend is not limited to vegetarian-specific establishments; traditional bistros and brasseries are also incorporating plant-forward dishes to attract growing market segments while preserving their culinary identity.

Adoption of Sustainability Initiatives

The MICHELIN Green Star program, introduced in France with over 100 certified restaurants, highlights the role of sustainability certifications in fostering competitive differentiation and customer loyalty. French establishments are increasingly seeking Écotable labels and conducting carbon footprint assessments, while collective catering facilities are required to report their environmental impact by 2025 under ADEME guidelines [2]Source: ADEME, “Carbon Footprint Assessment Guidelines for Collective Catering,” ademe.fr. This regulatory framework provides first-mover advantages for operators adopting comprehensive sustainability initiatives, such as waste reduction and renewable energy integration. Beyond regulatory compliance, restaurants are utilizing sustainability credentials to achieve premium market positioning and attract talent in competitive labor markets. Additionally, sustainability investments often lead to operational cost savings through reduced waste and energy consumption, creating a reinforcing cycle that strengthens market positions over time.

Rising Interest in Health-Conscious and Allergen-Free Menus

French food safety regulations emphasize the importance of comprehensive allergen disclosure and the implementation of effective management systems, holding establishments accountable with significant liability risks for non-compliance. In response, health-conscious menu development has evolved to address broader consumer expectations, extending beyond allergen management to include clear nutritional transparency, appropriate portion control, and the incorporation of functional ingredients designed to meet specific wellness goals. This shift is largely influenced by an aging population and a growing focus on health and well-being, with restaurants that provide detailed nutritional information experiencing stronger customer loyalty and retention. The adoption of digital menu platforms has further enhanced this approach, enabling dynamic allergen filtering and personalized recommendations, which not only ensure regulatory compliance but also create a competitive edge. Additionally, operators who prioritize investments in allergen-free preparation areas and comprehensive staff training are able to command premium pricing, reduce legal risks, and establish a sustainable position in a market that increasingly values health-focused dining options.

Proliferation of Cloud Kitchens and Virtual Restaurant Brands

Cloud kitchen concepts have experienced significant growth across French urban centers, with operators such as Clone establishing networks of delivery-only facilities. These facilities significantly lower real estate costs compared to traditional restaurants. Virtual restaurant brands utilize existing kitchen infrastructure to experiment with new concepts while requiring minimal capital investment. This approach enables swift market entry and efficient validation of business ideas. Entrepreneurs, particularly those grappling with high commercial real estate expenses in prime locations, find this model highly appealing. Cloud kitchens are able to achieve higher profit margins by streamlining delivery operations. This expansion has introduced new competitive dynamics, where the importance of location diminishes, and the focus shifts to operational efficiency and digital marketing capabilities as primary drivers of success. Established restaurant chains are increasingly adopting hybrid models that integrate traditional dining with cloud kitchen operations, aiming to optimize revenue generation and cater to the growing demand for delivery services.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labor shortages and challenges attracting/retaining skilled staff | -0.4% | National, acute in tourist regions and major cities | Short term (≤ 2 years) |

| Seasonal fluctuations in demand, especially for tourism-driven locations | -0.6% | Coastal regions, alpine areas, tourist destinations | Medium term (2-4 years) |

| Limited space for kitchen expansion and automation in historic sites | -0.3% | Historic city centers, protected heritage areas | Long term (≥ 4 years) |

| Risks associated with food allergen management and legal liability | -0.5% | National, particularly affecting multi-location operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labor Shortages and Challenges Attracting/Retaining Skilled Staff

The French hospitality sector is grappling with significant staffing challenges, with a large proportion of establishments reporting difficulties in recruiting, particularly for skilled roles such as chefs and service managers [3]Source: HOTREC–EFFAT, “Labour Shortages in European Hospitality Sector,” hotrec.eu. Labor shortages become even more pronounced during peak tourism seasons when demand rises sharply, but the workforce remains constrained due to factors like high housing costs and preferences for seasonal employment. These challenges often compel operators to make difficult decisions, such as increasing wages, reducing operating hours, or scaling back service offerings, all of which can hinder their potential for revenue growth. Independent operators face additional pressure, as they often find it challenging to compete with the comprehensive benefits packages and career advancement opportunities provided by chain restaurants. In response, many establishments are turning to solutions like automation and cross-training programs to optimize productivity with their existing staff. However, these approaches require considerable capital investment and may not fully address the labor shortages in service-intensive areas of the industry.

Seasonal Fluctuations in Demand, Especially for Tourism-Driven Locations

Tourism-dependent regions often experience significant variations in demand between peak and off-peak periods, with coastal and alpine establishments particularly affected by these seasonal challenges. These fluctuations result in operational inefficiencies, as businesses are required to maintain infrastructure and retain essential staff during periods of low demand while rapidly scaling up operations to meet peak-season requirements. This dynamic creates challenges in managing cash flow and planning investments, as operators frequently face difficulties in generating adequate revenue during high-demand periods to sustain operations throughout the year. Furthermore, climate change and evolving tourism trends add layers of uncertainty to traditional seasonal forecasts, making capacity planning increasingly complex. In response, establishments implement diversification strategies such as targeting local markets, hosting events, and adjusting off-season offerings. However, these measures often deliver lower profit margins compared to the revenue generated during peak tourism seasons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: QSR Dominance Drives Digital Innovation

Quickservice Restaurants are anticipated to account for 49.48% of the market share in 2025, underscoring the increasing preference among French consumers for fast-casual dining options. These formats successfully combine the convenience of quick service with the quality that consumers expect, making them a popular choice. Meanwhile, Cloud Kitchens are emerging as the fastest-growing segment, with a compound annual growth rate (CAGR) of 11.83% projected through 2031. This growth is largely attributed to the expansion of delivery platforms and the cost-efficiency of operating without traditional dine-in spaces. These factors enable businesses to test new concepts quickly and enter the market with reduced financial risk.

Fullservice Restaurants continue to cater to traditional dining preferences, offering a more formal experience. However, they are increasingly facing challenges such as rising labor costs and a noticeable shift in consumer preferences toward more casual dining experiences. Across all segments, digital transformation is playing a pivotal role in shaping the industry. Quick Service Restaurant operators, in particular, are leveraging technologies such as mobile ordering, kitchen automation, and AI-powered menu optimization to enhance operational efficiency and maintain a competitive edge in the evolving market landscape.

By Outlet: Independent Resilience Meets Chain Efficiency

Independent outlets are projected to maintain a 68.05% market share in 2025, reflecting the enduring consumer preference for locally-owned establishments. These outlets continue to attract customers by offering personalized service and unique culinary experiences that resonate with those seeking authenticity and a connection to local culture. This strong market presence underscores the value placed on individuality and the distinctive character that independent operators bring to the dining experience.

On the other hand, chained outlets are expected to grow at a CAGR of 6.88% through 2031, capitalizing on their ability to leverage operational efficiencies, standardized processes, and purchasing power. These advantages enable them to offer competitive pricing and deliver consistent quality, appealing to consumers who prioritize convenience and predictability. The contrasting growth trends highlight a shift in consumer priorities, where independent operators are responding by forming purchasing cooperatives, adopting shared technology platforms, and developing unique brand identities to stand out from the standardized offerings of chain establishments.

By Location: Standalone Strength Amid Travel Recovery

Standalone locations are anticipated to capture 69.42% of the market share in 2025. This dominance is attributed to their ability to operate with lower rental costs and greater operational flexibility. Additionally, these locations foster direct customer relationships, which allow businesses to offer personalized services and integrate more effectively within local communities. By addressing specific customer needs and preferences, standalone establishments continue to strengthen their position in the market.

Travel-oriented establishments are expected to experience the fastest growth, with a projected CAGR of 9.71% through 2031. This growth is fueled by the recovery of the tourism industry and significant infrastructure investments that are increasing passenger volumes at airports, train stations, and highway service areas. The expansion reflects a combination of pent-up travel demand and evolving traveler expectations for high-quality dining options during transit. Meanwhile, leisure locations are benefiting from the rise in domestic tourism and outdoor recreational activities. Lodging-integrated restaurants are also capitalizing on the recovery in hotel occupancy rates and the growing popularity of extended-stay accommodations.

By Service Type: Dine-in Adaptation Versus Delivery Acceleration

Dine-in services are anticipated to maintain a 54.76% market share in 2025, reflecting the enduring significance of social experiences and the enjoyment of meals in French dining culture. This preference highlights a resistance to complete digitalization, as many consumers continue to value the communal and immersive aspects of dining out. The strong performance of dine-in services underscores the cultural importance of traditional dining occasions, which remain a cornerstone of the French culinary experience.

In contrast, delivery services are expected to grow at a robust CAGR of 7.98% through 2031. This growth is fueled by the rapid expansion of quick commerce platforms and shifting lifestyle patterns that prioritize convenience and time efficiency. The increasing reliance on delivery networks signifies a fundamental change in consumer behavior, where at-home consumption is becoming a strong competitor to traditional dining. Takeaway services, positioned between dine-in and delivery, offer a balanced option by providing convenience without delivery fees while preserving a degree of personal interaction with restaurant staff.

Geography Analysis

France's foodservice market reflects unique regional characteristics shaped by tourism, demographics, and local culinary traditions. These factors create both opportunities for growth and operational challenges. Paris and the Île-de-France region stand out with the highest concentration of restaurants per capita and a quick adoption of technology-driven dining options like cloud kitchens and delivery platforms. The capital benefits from international tourism, business travel, and a diverse population, fueling demand for a wide range of cuisines and innovative dining experiences. Regional hubs such as Lyon, Marseille, and Toulouse have developed their own foodservice ecosystems, blending strong local identities with national trends at a pace that aligns with regional preferences and economic conditions.

Coastal regions face pronounced seasonality, with summer tourism driving demand that can surge 200-300% above off-season levels in popular Mediterranean and Atlantic destinations. This creates operational challenges, as businesses must generate enough revenue during peak periods to sustain operations year-round while managing labor and inventory fluctuations. Similarly, Alpine regions experience seasonal demand tied to winter sports and summer hiking, prompting establishments to adopt tailored strategies to attract different tourist groups throughout the year. However, the heavy reliance on tourism makes these regions sensitive to external factors like weather, economic shifts, and travel restrictions, which can significantly impact performance.

Rural and secondary urban markets present promising growth opportunities as urbanization and improved transportation infrastructure increase dining-out frequency and raise expectations for food quality and service. These areas often offer lower real estate costs and less competition, allowing businesses to achieve higher profit margins while catering to underserved populations. At the same time, challenges such as limited labor availability, seasonal agricultural employment patterns, and aging populations may limit long-term growth. To succeed, operators must adapt their strategies to local market conditions while maintaining operational efficiency and consistent brand standards across diverse regions.

Competitive Landscape

The France foodservice market is moderately fragmented, offering opportunities for consolidation while still accommodating a variety of competitive strategies. Major players like McDonald's Corporation, Starbucks Corporation, and Yum! Brands use their global scale and standardized operations to secure market share. At the same time, regional companies such as Groupe Le Duff and Groupe Bertrand leverage their local expertise and heritage branding to maintain strong positions. The competitive environment is evolving as digital transformation allows smaller operators to access advanced tools like cloud-based platforms, reducing the traditional advantages of larger chains in areas such as inventory management, customer analytics, and marketing automation.

Technology is becoming a critical factor in standing out in the market. Businesses that adopt AI-powered menu optimization, automated kitchen systems, and integrated delivery platforms are achieving greater operational efficiency, which translates into cost savings and better customer experiences. Additionally, there is growing interest in hybrid concepts that combine traditional French dining culture with modern convenience. Examples include premium takeaway formats and experiential dining options that celebrate France's rich culinary heritage.

Emerging players are focusing on sustainability, plant-based menu innovations, and hyper-local sourcing to appeal to environmentally conscious consumers. These strategies help them differentiate from standardized chain offerings. Meanwhile, the regulatory framework, managed by the DGCCRF, ensures a level playing field by enforcing food safety standards and consumer protection measures, creating consistent operational requirements for all participants in the market.

France Foodservice Industry Leaders

Agapes Restauration

AmRest Holdings SE

Compass Group PLC

Areas SAU

Accor S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: A new French café, Côte France, has opened in downtown Tampa, attracting locals with Parisian pastries, quiches, and desserts. The café features buttery croissants, baguettes, and rotating quiche flavors, earning perfect 5-star reviews on Yelp and Google for its authentic menu and inviting atmosphere.

- August 2025: Un Deux Trois Café is set to open, in Rogers, Arkansas, offering French-inspired artisanal pastries, specialty beverages, and a sustainable, community-focused café experience at The Plaza at Pinnacle Hills, enhancing local hospitality options.

- July 2024: Inspire Brands has partnered with Swiss group QSRP to launch Dunkin’ in France via a master franchise agreement. QSRP, backed by Kharis Capital, will develop Dunkin’ outlets nationwide, with the first Paris store opening in 2025, expanding Dunkin’s European footprint.

France Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.By Foodservice Type

| Café and Bars | By Cuisine | Bars & Pubs |

| Café | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Locations

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

By Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Café and Bars | By Cuisine | Bars & Pubs |

| Café | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Sandalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms