France Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

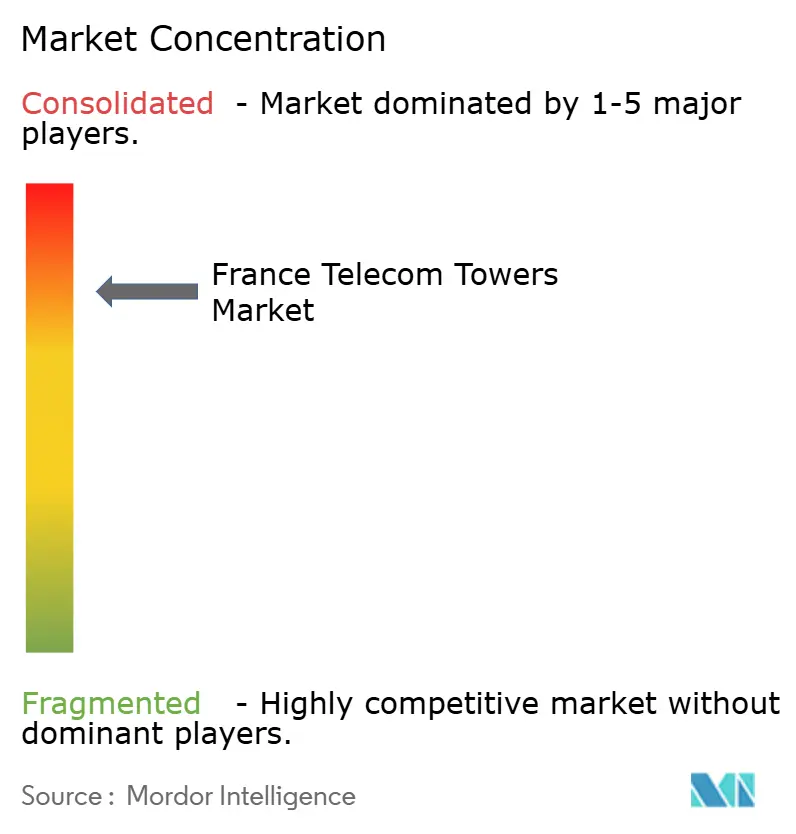

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Telecom Towers Market Analysis by Mordor Intelligence

The France Telecom Towers Market size is expected to grow from USD 1.79 billion in 2025 to USD 1.87 billion in 2026 and is forecast to reach USD 2.36 billion by 2031 at 4.72% CAGR over 2026-2031.

Accelerated 5G roll-out obligations, the expanding footprint of independent TowerCos, and renewable-energy adoption underpin the growth momentum of the France telecom towers market. Operator divestment strategies continue to reshape ownership structures, while rooftop densification in Paris, Lyon, and Marseille sustains premium lease rates. Rising steel prices and longer rural grid-connection lead times exert cost pressures, yet targeted government subsidies mitigate economic barriers in underserved communes. The commercial appeal of neutral-host models, coupled with fiber-to-the-tower upgrades that enable edge-computing monetization, broadens the revenue mix for tower owners.

Key Report Takeaways

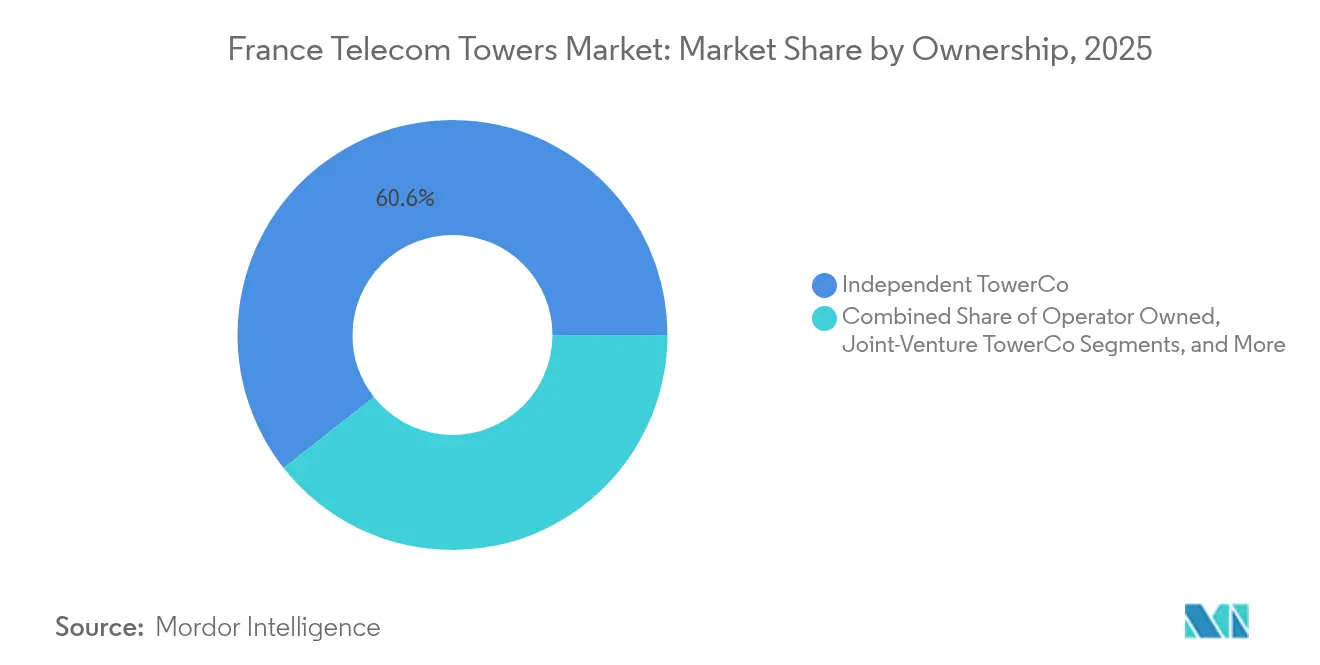

- By ownership, independent TowerCos commanded 60.62% France telecom towers market share in 2025 and are advancing at a 6.44% CAGR through 2031.

- By installation type, rooftop deployments accounted for 49.86% of the France telecom towers market size in 2025, whereas ground-based sites are trailing but still expanding at 5.53% CAGR through 2031.

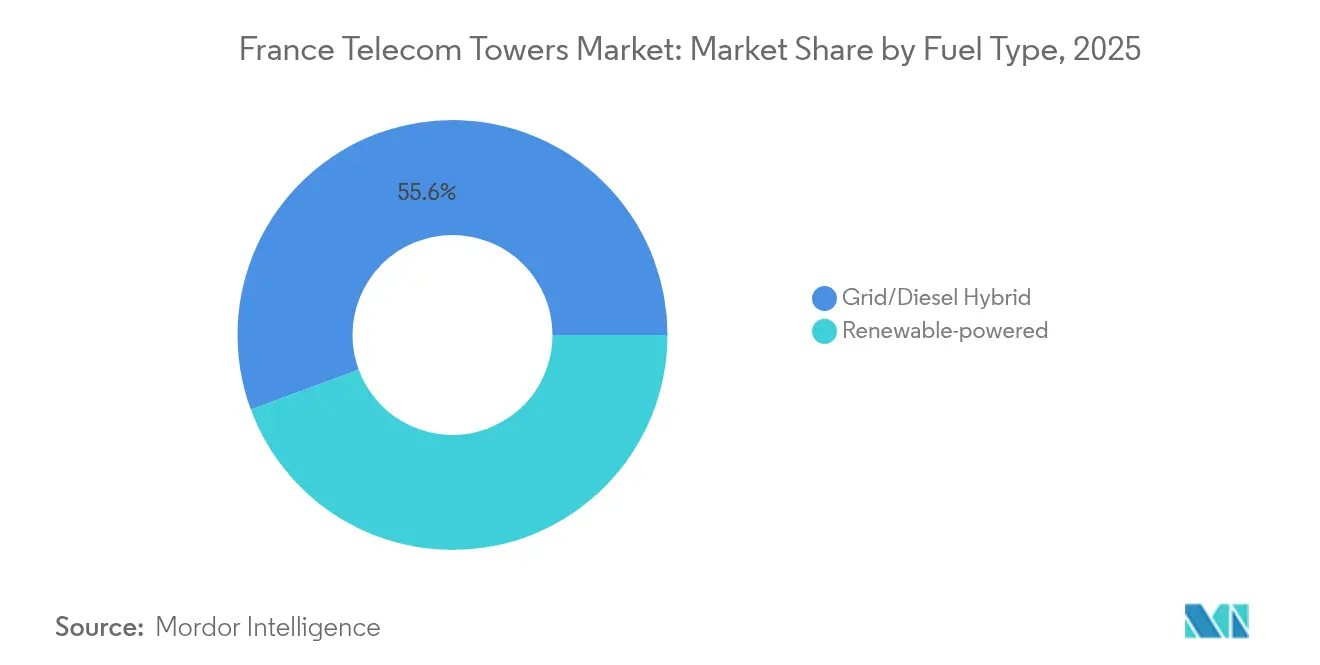

- By fuel type, grid/diesel hybrids held 55.63% France telecom towers market share in 2025, while renewable-powered sites are surging at a 13.78% CAGR to 2031.

- By tower type, monopoles captured 44.72% of the France telecom towers market size in 2025; stealth and concealed structures are projected to increase at an 10.84% CAGR during 2026-2031.

- Across geography, the Île-de-France region generated the highest revenue in 2025, and Provence-Alpes-Côte d’Azur is forecast to exhibit the fastest 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expedited 5G roll-out mandates | +1.8% | National focus on Paris, Lyon, Marseille | Medium term (2-4 years) |

| Growing neutral-host demand from MVNOs | +1.2% | Business districts and industrial zones | Long term (≥ 4 years) |

| Rural “New Deal Mobile” subsidies | +0.9% | Rural communes prioritized by ARCEP | Short term (≤ 2 years) |

| Fiber-to-the-tower backhaul upgrades | +1.1% | Urban and suburban high-traffic corridors | Medium term (2-4 years) |

| Rooftop-lease expiries around Paris Olympics | +0.3% | Île-de-France venue corridors | Short term (≤ 2 years) |

| Green-energy power-purchase agreements | +0.6% | Regions with favorable renewable policies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expedited 5G roll-out mandates drive infrastructure acceleration

Regulatory license conditions require nationwide 5G coverage by 2030, compelling operators to front-load tower construction schedules and upgrade existing sites ahead of organic demand. Free Mobile leads with more than 20,420 authorized 5G sites, while Orange controls the largest 3.5 GHz footprint at roughly 11,128 locations. [1]Agence Nationale des Fréquences, “Observatoire ANFR au 1er avril 2025,” anfr.frThe mandatory milestones create predictable revenue for the France telecom towers market through guaranteed tenancy commitments even when consumer adoption is still maturing. Compliance monitoring by ARCEP reduces investment risk and encourages TowerCos to pre-position assets in rural corridors scheduled for phased activation, thus locking-in premium lease rates.

Growing neutral-host demand from MVNOs transforms utilization economics

MVNOs and enterprise private networks prefer infrastructure-agnostic landlords, enabling independent TowerCos to attract additional tenants per site versus operator-captive portfolios. TOTEM France, for instance, reached a 1.43 tenancy ratio in Q1 2025 and targets 1.5 by 2026, highlighting rising multi-tenant monetization. The shared-asset model reduces duplication costs for smaller operators and accelerates time-to-market for industrial IoT deployments. Higher tenancy lifts cash-flow yields for landlords, which in turn supports debt-financed expansion across the France telecom towers market. [2]Orange SA, “Press Release on 5G and Edge Strategy,” orange.com

Rural connectivity subsidies create targeted growth opportunities

The New Deal Mobile framework underwrites as much as EUR 2.133 billion of operator investment, with 4,374 validated zones and more than 2,600 sites live by September 2023 ARCEP.FR. Subsidized multi-operator towers guarantee baseline revenue streams in sparsely populated communes, improving the economic viability of two- to three-tenant configurations. Independent TowerCos are strategically positioned to capture these contracts, leveraging their neutrality to host all carriers on a single mast.

Fiber-to-the-tower upgrades enable edge-computing monetization

Migration from microwave to fiber backhaul raises individual site capacity from below 1 Gbps to double-digit gigabit levels, laying the groundwork for on-tower edge nodes and CDN caches. Orange’s technology roadmap emphasizes reusing existing macro sites instead of erecting new poles, provided they are fiber-enabled. TowerCos can therefore lease additional space to cloud or content providers, diversifying revenue sources beyond radio equipment tenancy.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent RF-exposure zoning laws | -0.8% | Dense urban cores including Paris, Lyon, Marseille | Long term (≥ 4 years) |

| Municipal opposition to macro sites >30 m | -0.6% | Nationwide, strongest in residential and heritage districts | Medium term (2-4 years) |

| Rising rural grid-connection lead times | -0.4% | Remote communes with limited electrical capacity | Short term (≤ 2 years) |

| Higher steel prices inflating capex | -0.7% | National impact across all new-build programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent RF-exposure regulations constrain urban deployment

French municipalities apply lower EMF thresholds than international guidelines, obliging operators to perform extended public consultations that can stretch approval cycles by up to 12 months.[3]Ville de Paris, “Rapport d’Information sur la Réglementation EMF,” paris.fr The additional testing, documentation, and potential redesigns inflate project budgets and delay on-air dates, tempering the growth rate of the France telecom towers market in some metropolitan zones.

Municipal opposition drives preference for concealed solutions

Residents frequently contest macro structures taller than 30 meters for aesthetic and property-value reasons, steering operators toward stealth installations that are 20-40% more expensive but faster to approve under heritage codes. The premium cost adds pressure to capital budgets yet simultaneously fuels demand for specialized stealth designs, influencing both product mix and supplier ecosystems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Lead Market Transformation

Independent TowerCos controlled 60.62% of the France telecom towers market share in 2025, the highest among ownership categories, and are expected to expand at a 6.44% CAGR to 2031. This trajectory underscores a decade-long shift from operator-captive assets toward neutral hosting, catalyzed by sale-leaseback transactions and regulatory encouragement for infrastructure sharing. Cellnex France alone agreed to acquire over 12,300 additional masts from Bouygues, Free Mobile, and SFR/Hivory in deals exceeding EUR 371 million in the first half of 2024, pushing its domestic footprint toward 30 % of total third-party sites.

MNOs continue to divest non-strategic poles to unlock balance-sheet capacity for spectrum and RAN investments, yet they retain high-value urban rooftops and defense-critical locations. Joint-venture structures also appear, allowing carriers to share financial risk while accessing TowerCo balance-sheet leverage. The France telecom towers market therefore tilts toward a hybrid model where independent landlords dominate greenfield expansion, whereas operators focus on optimizing fiber and spectrum resources.

By Installation: Rooftop Deployments Capitalize on Urban Densification

Rooftops represented 49.86% of the France telecom towers market size in 2025, reflecting city-level preferences for masked antennas that blend into skylines. Municipalities favor these solutions because they avoid ground-level land-use conflicts and shorten public-hearing cycles. In high-density arrondissements of Paris, one rooftop can accommodate three or more tenants, squeezing incremental revenue out of scarce structural space and boosting landlord yields.

Ground-based towers still dominate rural landscapes where land is abundant and zoning is lenient. However, environmental impact assessments and heritage-protection overlays are extending pre-build timelines, especially along national parks and châteaux corridors. Rooftop growth therefore continues at 5.53% CAGR, outstripping new ground-based starts, and reinforces the urban-centric revenue composition of the France telecom towers market.

By Fuel Type: Renewable-Energy Adoption Accelerates Despite Grid Dominance

Grid/diesel hybrids accounted for 55.63% France telecom towers market share in 2025, a legacy of reliable national power infrastructure and standardized backup practices. Operators nevertheless face mounting stakeholder pressure to decarbonize, prompting trial deployments of solar-plus-battery solutions on remote masts and high-altitude relay stations. Renewable-powered sites are tracking a 13.78% CAGR through 2031, the fastest among all fuel segments, driven by corporate net-zero pledges and anticipated EU carbon-pricing expansions.

Market uptake is tempered by limited appetite for long-duration PPAs; only 4% of Cleee member load was under green contracts in 2025 because CFOs fear future solar price deflation. Even so, hybrid kits featuring modular battery packs and smart controllers are becoming cost-competitive as lithium-ion prices fall. TowerCos see an opportunity to cross-sell turnkey renewable packages along with lease agreements, deepening tenant stickiness and differentiating service offerings within the France telecom towers market.

By Tower Type: Stealth Designs Gain Traction Amid Aesthetic Constraints

Monopoles retained 44.72% of the France telecom towers market size in 2025, largely because of their favorable capex-to-height ratio and straightforward permitting in non-heritage zones. Yet stealth and concealed variants are exhibiting an 10.84% CAGR, reflecting city councils’ insistence on minimal visual impact. In medieval quarters around Lyon and Bordeaux, façade-mounted canisters disguised as chimneys or church spires sidestep objections that often sink conventional lattice bids.

Advanced RF-transparent materials and antenna miniaturization now allow stealth poles to match the loading capacity of small monopoles, eroding the historical cost-performance penalty. TowerCos that invest in design libraries and digital-twin modeling can satisfy local planners more quickly, thereby capturing time-to-revenue advantages that outweigh incremental material costs. The pivot to stealth is therefore both a compliance response and a commercial lever inside the France telecom towers market.

Geography Analysis

Île-de-France generated the highest revenue contribution to the France telecom towers market in 2025, benefiting from the densest population, elevated data-traffic demand, and accelerated 5G coverage mandates ahead of the 2024-2025 Olympic cycle. Average monthly lease rates here run 18-25% above the national mean, and typical rooftop tenancies exceed 1.6 per site owing to strong MVNO presence.

Provence-Alpes-Côte d’Azur and Auvergne-Rhône-Alpes are growing swiftly, supported by tourism traffic and industrial digitalization clusters around Marseille harbor logistics and Lyon’s biotech corridor. These regions face stricter heritage restrictions, prompting a higher mix of concealed or façade-mounted antennas, yet subsidy programs for rural communes help fund connectivity in mountainous hinterlands. Over the next five years, Provence-Alpes-Côte d’Azur is projected to post a 6.08% CAGR, the fastest regional clip in the France telecom towers market.

The New Deal Mobile initiative directs EUR 2 billion into multi-operator build-outs across sparsely populated departments such as Lozère and Creuse, narrowing the historical penetration gap between metropolitan and rural France. Overseas territories—including Réunion and Guadeloupe—offer niche expansion paths, though extreme weather calls for cyclone-resistant designs and higher maintenance budgets.

Competitive Landscape

Independent TowerCos dominate the strategic narrative, yet the France telecom towers industry still exhibits mid-level concentration due to continued operator control of select urban assets. Cellnex France closed its acquisition of Hivory and is on track to integrate another 12,000 sites via multi-phase conversions from Bouygues and Free Mobile, reinforcing its national leadership. To satisfy antitrust remedies, Cellnex divested 3,226 locations for USD 835 million, a move that opened white-space for Phoenix Tower International and other challengers.

TOTEM France remains Orange’s infrastructure arm and reported EUR 178 million in Q1 2025 revenue, driven by a climbing tenancy ratio and ancillary services such as site energy management. Its portfolio emphasizes fiber-fed urban rooftops, positioning the company to monetize forthcoming edge-computing demand without heavy greenfield expansion.

Strategic differentiation increasingly hinges on digital capabilities—drone-enabled inspections, 3D twins, and AI-driven maintenance scheduling—which TDF Infrastructure is rolling out nationwide. Renewable-energy integration and micro-edge data modules represent the next competitive frontier, with several landlords piloting battery-backed solar shelters that host both RAN and low-latency compute workloads.

France Telecom Towers Industry Leaders

Cellnex France

TOTEM France (Orange)

TDF Infrastructure

American Tower France

Phoenix Tower International France

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ARCEP opened a public consultation on cloud-service regulation under the SREN law, potentially shaping edge-node economics.

- March 2025: TDF Infrastructure deployed drone-based digital twins for nationwide asset optimization.

- January 2025: DIF Capital Partners acquired TDF’s fiber arm, underscoring strategic focus on core tower assets.

- December 2024: ARCEP released expanded FttH quality indicators that indirectly influence tower backhaul standards.

France Telecom Towers Market Report Scope

Telecom towers, designed to support antennas and communication equipment, play a pivotal role in wireless transmission. These towers empower mobile networks to cover vast areas, facilitating the seamless broadcasting and reception of signals between mobile devices and the network infrastructure. Telecom towers come in various designs and sizes depending on the location and network requirements, such as lattice towers, monopoles, and guyed towers.

The French telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of volume (Units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the France telecom towers market in 2026?

The France telecom towers market size reached USD 1.87 billion in 2026 and is projected to climb to USD 2.36 billion by 2031.

What CAGR is expected for French tower revenues through 2031?

Industry revenues are forecast to advance at a 4.72% CAGR between 2026 and 2031.

Which ownership model holds the biggest share?

Independent TowerCos led with 60.62% market share in 2025 and continue to outpace other models.

Why are rooftop deployments growing faster than ground-based towers?

Municipal visual-impact rules and the need for dense urban 5G coverage drive landlords toward building-mounted antennas that face fewer local objections.

How are renewable-powered towers trending?

Renewable-only sites represent the fastest-growing fuel segment, expanding at 13.78% CAGR as operators pursue net-zero pledges.

What is the outlook for tenancy ratios among neutral-host providers?

TOTEM France targets a tenancy ratio of 1.5 by 2026, and similar gains are expected across peers as MVNO and private-network demand rises.

Page last updated on: