Spain Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.98 Billion |

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.23 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Telecom Towers Market Analysis by Mordor Intelligence

The Spain Telecom Towers Market size was valued at USD 0.98 billion in 2025 and estimated to grow from USD 1.02 billion in 2026 to reach USD 1.23 billion by 2031, at a CAGR of 3.91% during the forecast period (2026-2031).

Ongoing 5G densification, a decisive swing toward neutral-host infrastructure, and steady renewable-energy retrofits underpin this measured expansion. Independent TowerCos continue to acquire portfolios from mobile operators, converting single-tenant sites into multi-tenant assets that lift tenancy ratios and preserve cash flow. Grid-connected diesel hybrids remain the dominant power solution, yet every major tower company now links long-term renewable power-purchase agreements to cut exposure to volatile electricity prices. Meanwhile, municipal green-lighting of rooftop small cells in Madrid, Barcelona, and Valencia accelerates urban coverage gains, and private 5G networks at ports and logistics hubs create fresh tenancy demand from non-telecom customers.

Key Report Takeaways

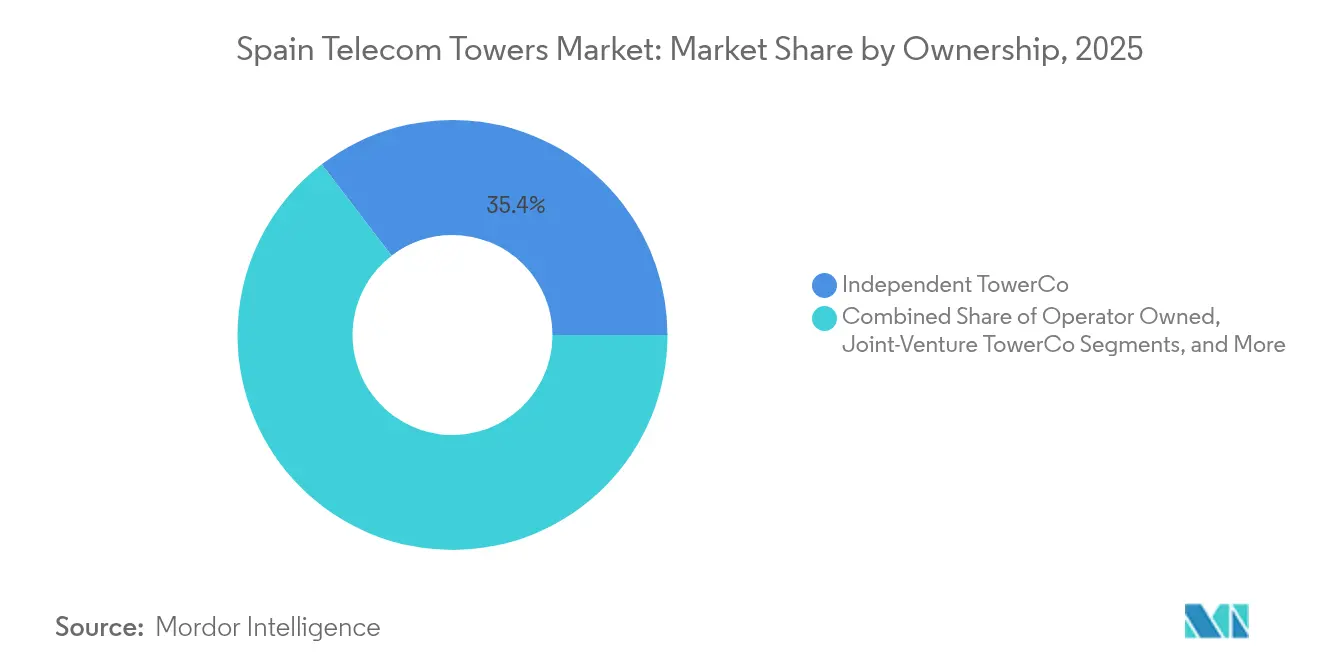

- By ownership, Independent TowerCos led with 35.41% revenue share in 2025; the same segment is expanding at a 5.43% CAGR through 2031.

- By installation, ground-based sites captured 51.22% of the Spain telecom tower market share in 2025, while rooftop deployments are projected to grow at 4.48% CAGR to 2031.

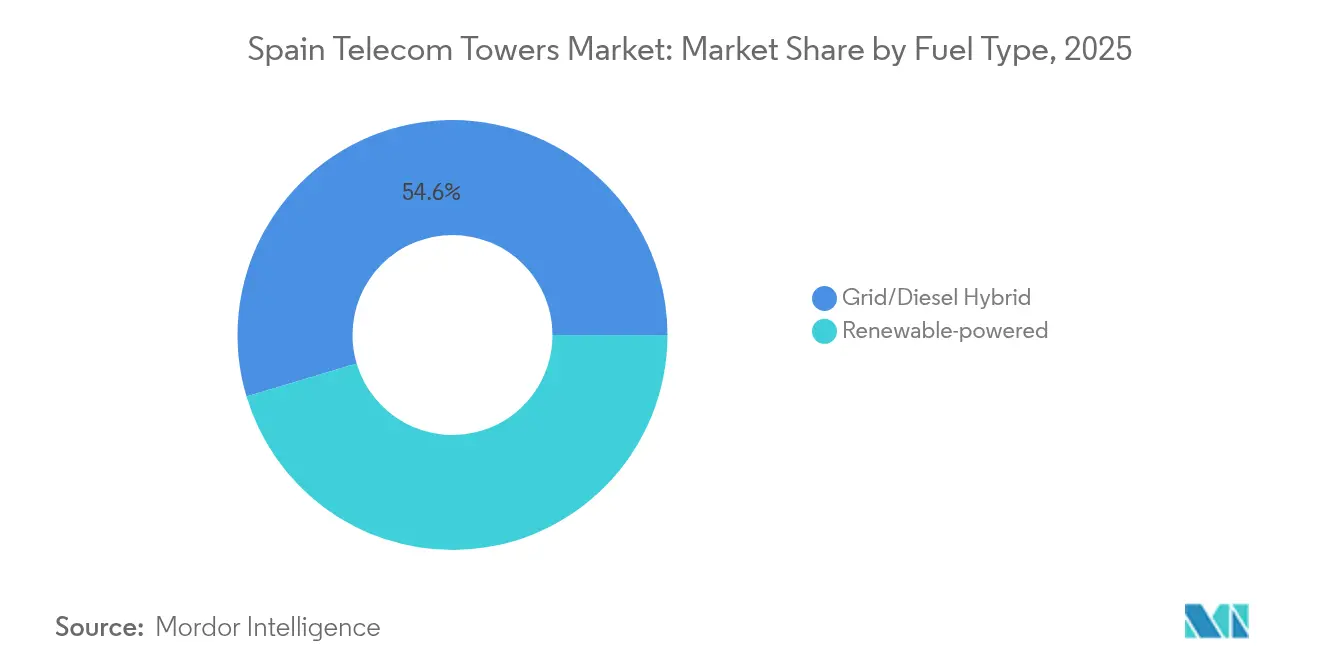

- By fuel type, grid/diesel-hybrid systems held 54.62% share of the Spain telecom tower market size in 2025, whereas renewable-powered towers are rising at a 12.67% CAGR through 2031.

- By tower type, monopole structures accounted for 49.87% share in 2025, and stealth/concealed designs are advancing at 5.53% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G macro & small-cell densification wave | +1.2% | Madrid, Barcelona, Valencia metropolitan areas | Medium term (2-4 years) |

| Accelerating RAN-sharing & build-to-suit | +0.8% | National, early adoption in urban corridors | Short term (≤ 2 years) |

| Rural broadband obligations (UNICO) | +0.6% | Castilla-La Mancha, Extremadura, other rural regions | Long term (≥ 4 years) |

| TowerCo consolidation unlocking capex | +0.5% | National, M&A clustered around major markets | Medium term (2-4 years) |

| Private LTE/5G networks for industry & ports | +0.4% | Valencia, Barcelona, Bilbao coastal corridors | Medium term (2-4 years) |

| EU-funded green-energy retrofit incentives | +0.3% | National, priority renewable zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Macro & Small-Cell Densification Wave

Government grants under the UNICO program allocate EUR 508 million for rural 5G plus EUR 161.3 million for advanced connectivity, accelerating macro-site upgrades and urban small-cell grids. [1]TM Forum Staff, “Spain Allocates UNICO Funds to Rural 5G,” TM Forum, tmforum.orgSmall-cell nodes are forecast to grow over 35% per year to 2030, shifting tower economics from passive leasing toward end-to-end connectivity solutions. Operators now bundle rooftop small cells with macro sites to secure contiguous coverage, pushing tenancy ratios higher on existing infrastructure. CNMC spectrum allocations and streamlined municipal permits in Madrid and Barcelona dictate roll-out velocity, while smart-city projects ensure stable urban demand.

Accelerating RAN-Sharing & Build-to-Suit Outsourcing by MNOs

The April 2024 Orange-MásMóvil merger created MasOrange with 42.5% mobile lines, spurring fresh RAN-sharing agreements as overlapping sites are rationalized. [2]Staff Reporter, “MasOrange Clears Regulatory Hurdles,” Cinco Días, cincodias.elpais.comIndependent TowerCos seize the moment: TOTEM targets a 1.5× tenancy factor by 2026 and Vantage Towers has contracted 500 carry-cash build-to-suit sites for Vodafone and NOVA. Outsourcing transfers permit risk and capex from operators to specialist landlords, freeing operator cash for spectrum fees and software-defined network investments. The model has cut average site payback below six years, supporting the Spain telecom tower market’s resilience against macroeconomic uncertainty.

Rural Broadband Obligations Under Spain’s UNICO Programme

UNICO’s rural tranche finances towers in low-density provinces where commercial returns are thin. Grants covering up to 90% of build cost make rollout viable across Castilla-La Mancha, Extremadura, and parts of Galicia. CNMC oversees tender fairness, ensuring at least two neutral-host applicants per cluster to curb regional monopolies. TowerCos that win leases enjoy 20-year visibility with inflation-linked pricing, mitigating revenue volatility. As rural 5G devices proliferate, follow-on tenancy from IoT-enabled agriculture and emergency services will reinforce site economics.

Consolidation Among TowerCos Unlocking Capex Fire-Power

Cellnex posted EUR 3.941 billion revenue in 2024 and continues to recycle assets to fund new builds, while American Tower doubled Spanish dividends above EUR 92 million in 2024, proving the cash-engine effect of scale. [3]Bloomberg News, “Cellnex FY2024 Results Highlight European Scale,” Bloomberg, bloomberg.comLarger balance sheets unlock cheaper debt and syndicated sustainability-linked loans, lowering weighted-average cost of capital. Consolidated platforms harmonize maintenance and digital-twin inspection, trimming opex per site by up to 15%. CNMC caps regional concentration, yet still green-lights mergers that demonstrate service-quality gains and rural coverage commitments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy municipal permitting and heritage curbs | –0.7% | Historic city centers, protected zones nationwide | Short term (≤ 2 years) |

| Public opposition to EMF and visual impact | –0.4% | Residential districts in urban and suburban municipalities | Medium term (2-4 years) |

| Volatile electricity prices | –0.3% | National, all tower operators | Short term (≤ 2 years) |

| Macroeconomic uncertainty delaying MNO capex | –0.2% | National, region-specific GDP swings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy Municipal Permitting and Heritage-Site Restrictions

Spain’s 8,131 municipalities apply divergent rules, so timelines for a single ground-based mast vary from eight weeks in Alcobendas to 18 months in Toledo’s UNESCO district. Heritage sites require façade-integrated antennas and stone-colored shrouds, inflating build budgets by up to 40%. Small-cell deployments on street furniture meet fewer heritage checks but still face traffic-management hearings, delaying dense-urban rollouts. TowerCos mitigate risk by front-loading multi-site permit packages, yet fragmented processes still erode the Spain telecom tower market CAGR by 0.7 percentage points.

Rising Public Opposition Over EMF and Visual Pollution

Although Real Decreto 1066/2001 sets EMF limits mirroring ICNIRP standards, community groups routinely petition for stricter thresholds near schools. Municipalities in Catalonia now demand stealth monopines or façade-flush antennas, lifting project spend and engineering complexity. Concealed structures cost 40-60% more than monopoles, but their 5.66% CAGR proves tenants will pay premiums to secure permits. Industry associations promote transparent EMF dashboards and virtual site-walk tools to ease resident concerns and compress objection cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Sustain Momentum Through Shared-Tenant Economics

The segment accounted for 35.41% of the Spain telecom tower market in 2025, reflecting asset carve-outs by operators eager to deleverage. Independent platforms benefit from higher tenancy ratios and activate build-to-suit deals that anchor 10-year inflation-linked contracts, anchoring predictable cash flows. Cellnex’s 8,771 Spanish sites make it Europe’s scale leader, while TOTEM España’s 7,300 macrosites straddle urban rooftops and rural ground-based towers.

Independent players also lead on digital transformation, rolling out drone-based inspections and AI-driven asset management that cut routine OandM costs by 12%. Operator-owned portfolios keep strategic assets in dense urban clusters, but capital constraints slow upgrade cycles, driving more sale-and-leaseback activity. Joint-venture TowerCos act as transitional vehicles, allowing operators to cash out gradually while retaining strategic influence. MNO captives now represent a niche for defense and other critical-coverage commitments.

By Installation: Ground-Based Sites Retain Primacy as Rooftops Scale in Urban Cores

Ground-based towers controlled 51.22% of the Spain telecom tower market share in 2025 thanks to broad coverage radius and easier multiband antenna configurations. These structures suit suburban rings and rural corridors where land prices stay moderate. Yet rooftop sites, projected to grow 4.48% CAGR through 2031, offer rapid densification without the land-acquisition drag.

Madrid alone issued more than 900 rooftop permits in 2024 as operators filled mid-band gaps. Structural load limits and landlord negotiations lengthen contract cycles, but rent premiums stay modest compared with ground leases inside city limits. Government tax incentives for 5G smart-building retrofits further widen rooftop appeal. By 2030, TowerCos expect blended tenancy across rooftops to approach 1.3 compared with today’s 1.1, providing incremental upside to the Spain telecom tower market size.

By Fuel Type: Renewable Powered Sites Accelerate on Economic and Regulatory Tailwinds

Grid/diesel hybrids held 54.62% of the Spain telecom tower market size in 2025 because they guarantee runtime during grid outages. That dominance now erodes as solar-battery hybrids achieve a 12.67% CAGR amid falling PV costs and EU carbon-credit incentives.

Pilot solar arrays in Extremadura show payback inside five years thanks to 2,800 annual sunlight hours and rising wholesale power prices. TowerCos bundle smart-inverter telemetry with site-management dashboards to predict battery degradation and pre-empt truck rolls, safeguarding uptime. Diesel use remains critical for emergency back-up, especially on remote mountain sites lacking grid stability. Yet by 2030, operators forecast renewables to supply 40% of network power needs, reinforcing sustainability narratives that resonate with institutional investors.

By Tower Type: Monopole Designs Dominate as Stealth Solutions Tackle Visual Impacts

Monopoles absorbed 49.87% of 2025 revenue because their small footprint and quick-install design fit suburban and highway corridors. Standardized steel pole kits allow just-in-time fabrication, compressing deployment cycles.

Stealth and concealed forms, camouflaged cypress trees and lamp-post antennas, will log a 5.53% CAGR through 2031 driven by municipal aesthetic ordinances. Although capital-intensive, these designs unlock permits that conventional lattices cannot secure in heritage zones. Lattice structures persist for high-load broadcast clusters and tower farms along the Mediterranean ridge, while guyed masts remain sparse given Spain’s limited wide-open plains.

Geography Analysis

Greater Madrid and Barcelona head Spain’s 5G investment wave, accounting for nearly half of new small cells permitted in 2024. Each city’s tech corridors host private 5G testbeds for logistics automation, driving dense rooftop deployments and micro-edge shelters. Catalonia’s smart-industrial projects secure EU regional-development grants that co-finance sub-6 GHz macro upgrades, boosting the Spain telecom tower market size in the region.

Coastal hubs, Valencia, Bilbao, and Algeciras, prioritize port digitization and logistics corridor coverage, anchoring private network tenancies that stabilize lease revenue beyond the mobile sector. Andalusia leverages abundant solar irradiance for renewable-powered towers, compelling operators to retrofit legacy diesel sites. Meanwhile, Basque Country towns like San Sebastián accelerate street-level small cells for tourism season surges.

UNICO’s rural tranche channels investment into Castilla-La Mancha, Extremadura, Galicia, and Asturias, where rugged terrain and sparse populations previously inhibited build-outs. TowerCos package solar-battery kits with fiber backhaul to satisfy coverage mandates while trimming opex. The Balearic and Canary Islands pose logistical challenges, equipment is ferried or flown in, but seasonal tourism spikes justify compact monopole grids integrated with emergency-services spectrum.

Competitive Landscape

Spain’s independent tower segment hosts three heavyweight players alongside residual operator-owned estates. Cellnex wields continental scale and closed 2024 with EUR 3.941 billion in revenue, funneling cash into site densification and edge-compute pilots. American Tower leverages global procurement to negotiate energy PPAs and launched a dividend step-up that topped EUR 92 million from Spanish operations in 2024. Vantage Towers, backed by private equity, prioritizes build-to-suit commitments, having secured Vodafone contracts for 500 new sites.

TOTEM España, Orange’s carve-out, narrows its focus on high-tenancy urban rooftops and aims for 1.5× tenancy by 2026. Each firm invests in digital-twin software and drone inspections, shrinking preventive-maintenance visits and improving predictive fault analytics. Sustainability remains a contest ground: Cellnex’s 200 MW solar PPA edges rivals on green-power credibility, while American Tower trials modular lithium-iron-phosphate batteries to cut diesel runtime 70%. CNMC’s antitrust guardrails maintain tenant choice, requiring divestitures if site concentration exceeds regional thresholds.

White-space potential persists in industrial 5G and rural broadband clusters, where first-mover TowerCos can lock in 20-year concessionary leases funded by UNICO. Competitive advantage increasingly hinges on bundled offerings—macro, rooftop, small cell, and edge compute—over legacy passive-only models. As consolidation eases financing pressure, operators turning capex toward spectrum and software further enlarge the Spain telecom tower market opportunity for neutral hosts.

Spain Telecom Towers Industry Leaders

Cellnex Telecom

American Tower Corporation

Vantage Towers

TOTEM España

Axión Infraestructuras de Telecomunicaciones

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: American Tower reported Q4 2024 consolidated revenue of USD 2.548 billion, with Europe contributing USD 835 million and a 55% operating margin.

- December 2024: CNMC certified MasOrange as Spain’s largest mobile operator with 42.5% market share, reshaping tenancy dynamics.

- November 2024: American Tower doubled Spanish dividends to exceed EUR 92 million, underscoring Iberian cash generation.

- November 2024: TOTEM signed a strategic pact with Spain’s government to streamline future tower deployments under UNICO.

Spain Telecom Towers Market Report Scope

Telecommunication towers, encompassing monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar structures, are crucial for radio communications. These towers, often grounded or situated on rooftops, are outfitted with one or more antennas.

The Spanish telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

What is the current value of the Spain telecom tower market?

The market is valued at USD 1.02 billion in 2026 and is forecast to climb to USD 1.23 billion by 2031.

How fast is renewable power adoption at Spanish tower sites growing?

Renewable-powered sites are expanding at a 12.67% CAGR, propelled by EU incentives and falling solar costs.

Which ownership model is growing quickest?

Independent TowerCos lead growth with a 5.43% CAGR as operators divest tower portfolios to focus on core services.

How does the Orange-MásMóvil merger affect tower demand?

The merger, creating MasOrange, consolidates 42.5% of mobile lines, reshaping tenancy patterns and fueling new RAN-sharing contracts.

What are the main regulatory hurdles for new tower builds?

Lengthy municipal permits and heritage-site rules can stretch approval to 18 months in historic zones, dampening rollout speed.

Where are private 5G networks creating fresh tower opportunities?

Ports in Valencia and Bilbao and logistics corridors near Zaragoza lead demand for neutral-host masts supporting industrial 5G.

Page last updated on: