Germany Telecom Towers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

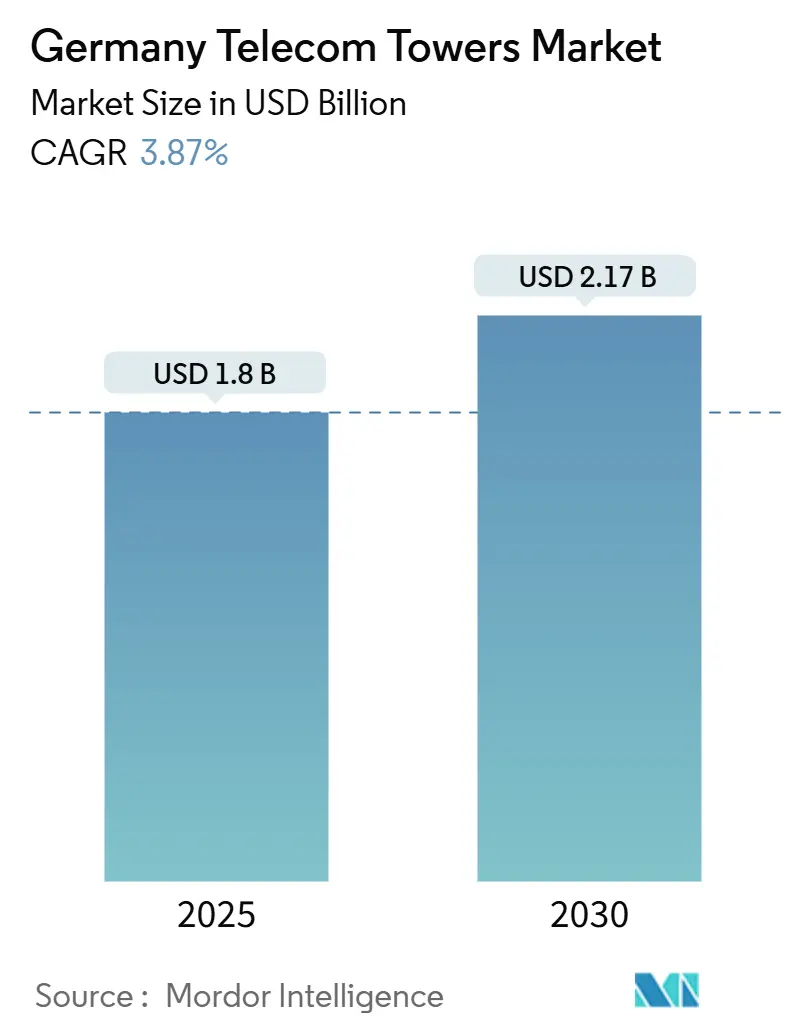

| Market Size (2025) | USD 1.8 Billion |

| Market Size (2030) | USD 2.17 Billion |

| Growth Rate (2025 - 2030) | 3.87% CAGR |

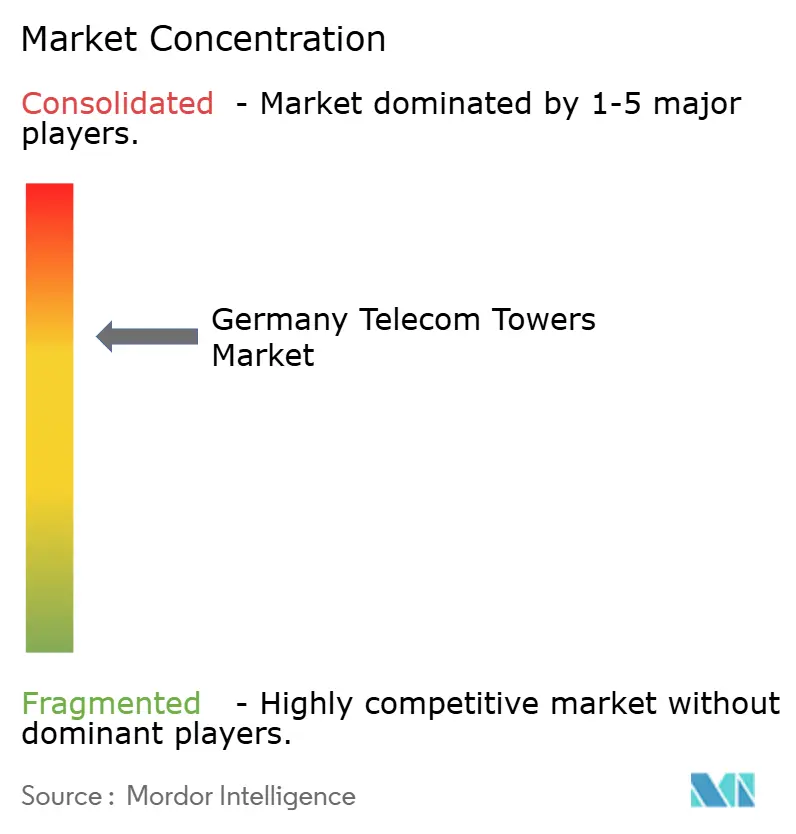

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Telecom Towers Market Analysis by Mordor Intelligence

The Germany Telecom Towers Market size is estimated at USD 1.8 billion in 2025, and is expected to reach USD 2.17 billion by 2030, at a CAGR of 3.87% during the forecast period (2025-2030). In terms of installed base, the market is expected to grow from 80.51 thousand units in 2025 to 89.83 thousand units by 2030, at a CAGR of 2.21% during the forecast period (2025-2030). The sector shifts from rapid 5G rollout toward network densification and asset-optimization phases. Demand momentum comes from 1&1 AG’s arrival as the fourth mobile network operator (MNO), government-backed rural coverage subsidies, and tower-energy transition projects that bring new revenue streams but also higher capital requirements. Independent tower companies deepen their hold on the German telecom tower market by purchasing legacy MNO portfolios and offering neutral-host leasing models that accelerate site sharing, while Open-RAN and edge-computing upgrades widen addressable infrastructure scope. At the same time, municipal permitting delays, rising financing costs, and Bundeskartellamt antitrust probes constrain near-term build-to-suit (BTS) economics, making disciplined capital allocation and digital operations crucial for sustaining margins. The German telecom tower industry demonstrates resilience, yet portfolio owners must balance inflation-linked lease escalators with tenant rent-compression risk as rooftop landlords renegotiate contracts in high-value city centers.

Key Report Takeaways

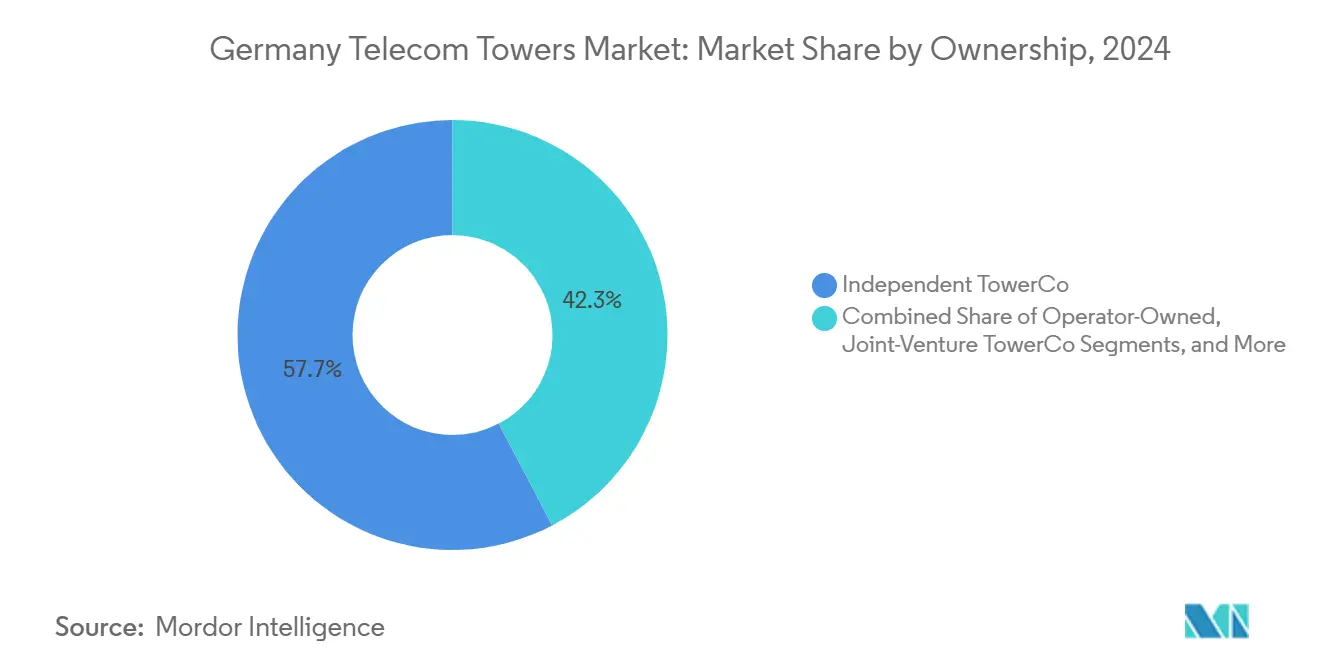

- By ownership, independent TowerCos led the German telecom tower market with 57.67% in 2024 and are also advancing at a 7.07% CAGR through 2030.

- By installation, rooftop installations accounted for a 50.44% share of the German telecom tower market in 2024 and are projected to expand at a 4.72% CAGR through 2030.

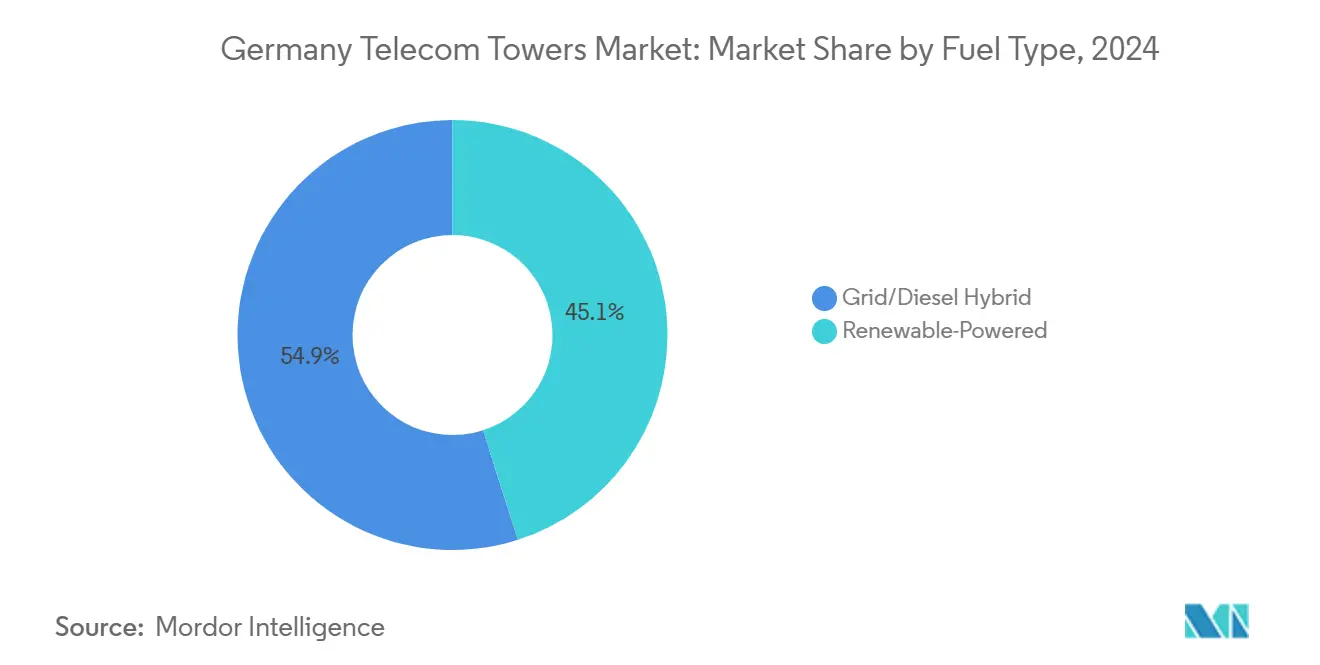

- By fuel type, grid/diesel hybrid sites captured 54.93% of the German telecom tower market in 2024, while renewable-powered sites are expected to grow at a 12.54% CAGR through 2030.

- By tower type, monopole towers accounted for 48.42% of the German telecom tower market in 2024, while lattice tower structures are expected to grow at a 12.27% CAGR through 2030.

Germany Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising 5G Macro- and Small-Cell Densification Mandates | +1.2% | National–dense urban zones | Medium term (2-4 years) |

| Government-Subsidized Rural Mast program | +0.8% | Rural, eastern states | Long term (≥4 years) |

| Entry of 1&1 AG as 4th MNO Boosting Lease-Up Demand | +0.9% | Nationwide corridors | Short term (≤2 years) |

| Tower Energy-Transition (Onsite Renewables, Wooden Towers) | +0.6% | Nationwide pilots | Long term (≥4 years) |

| Open-RAN and Edge-Computing Upgrades Needing Additional Sites | +0.7% | Transport routes | Medium term (2-4 years) |

| EU Cross-Border Transport-Corridor 5G Projects | +0.3% | Border regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising 5G Macro- and Small-Cell Densification Mandates

Deutsche Telekom added 1,500 new sites in 2025 to strengthen coverage beyond the existing 98% population reach, underscoring how millimeter-wave frequencies force operators to deploy closer-spaced nodes for capacity uplift. [1]Deutsche Telekom Press Office, “5G network expansion continues,” Deutsche Telekom, telekom.comO2 Telefónica activated 500 new 5G transmitters in Q1 2025, while Vodafone lit 2,200 antennas during the same span, mirroring a nationwide race to maintain parity. [2]O2 Telefónica Communications, “O2 Telefónica builds 5G network further,” Telefónica Deutschland, telefonica.deSmall-cell conversions of 12,000 legacy phone booths further expand addressable leasing inventory, giving tower companies a scalable urban footprint without lengthy permit cycles. Spectrum license obligations require quantified coverage thresholds, guaranteeing a multi-year installation pipeline. Consequently, Germany telecom tower market landlords gain predictable multi-tenant revenue streams, yet must invest in fiber backhaul and power upgrades to accommodate dense equipment loads.

Government-Subsidized Rural Mast program

Federal subsidies continue to target underserved localities after Mobilfunkinfrastrukturgesellschaft transitions to BMDV stewardship, ensuring more than 400 mast projects proceed under outcome-based funding rules. Eastern Lander such as Saxony-Anhalt and Mecklenburg-Western Pomerania receive priority, narrowing the digital divide and unlocking rental revenue for rural tower portfolios. Co-funding models improve the internal rate of return (IRR) on greenfield builds, though operators must incorporate renewable power and satellite backhaul in remote zones. Program evolution toward post-construction performance metrics aligns with EU Digital Decade targets, bolstering long-term tenancy and maintenance income for the German telecom tower market.

Entry of 1&1 AG as 4th MNO Boosting Lease-Up Demand

1&1 AG has activated 1,000 base stations and mapped 5,000 additional sites to meet its statutory 50% population-coverage target by 2030, stimulating immediate multi-tenant leasing across independent portfolios. Deployment delays attributed to exclusive site access disputes triggered Bundeskartellamt intervention, subsequently broadening 1&1’s procurement beyond Vantage Towers to include American Tower Germany and Deutsche Funkturm. The operator’s fully Open-RAN network with Rakuten requires flexible equipment racks, driving modifications, and fresh capex for rooftop and lattice structures. Heightened demand lifts lease-up ratios and supports mid-single-digit rent escalators, sustaining earnings before interest, tax, depreciation, and amortization (EBITDA) growth in the German telecom tower market.

Tower Energy-Transition (Onsite Renewables, Wooden Towers)

Vantage Towers erected Germany’s first commercial wooden tower in North Rhine-Westphalia, reducing embodied carbon by 30% compared with steel equivalents while meeting structural standards. [3]Vantage Towers Corporate Blog, “Our first wooden tower,” Vantage Towers, vantagetowers.comDeutsche Telekom and Ericsson pilot solar-wind hybrids that reduce grid reliance and trim operating expenses by up to 40% under high electricity price scenarios. O2 Telefónica’s energy-autonomous Bavarian site demonstrates that renewable-only electrification can be financially viable when grid extension exceeds EUR 70,000 (USD 76,000) per kilometer. These initiatives align with EU Fit-for-55 mandates, positioning green sites for preferential municipal permits. Renewable retrofits generate incremental service fees for tower owners, diversifying revenue streams in the German telecom tower market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal Permitting Delays and NIMBY Opposition | -0.7% | Nationwide–residential zones | Short term (≤2 years) |

| Rooftop Lease Renegotiation Risk Squeezing Margins | -0.5% | Tier-1 cities | Medium term (2-4 years) |

| Rising Financing Costs Dampening BTS Economics | -0.6% | Nationwide | Short term (≤2 years) |

| Antitrust Scrutiny of MNO-Controlled Towercos | -0.4% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Municipal Permitting Delays and NIMBY Opposition

Local authorities wield zoning power that can freeze projects for 12-18 months, as seen when Aschheim residents opposed a 21-meter mast and secured a Baustopp order, forcing temporary coverage gaps. Such objections revolve around perceived health risks and aesthetics, compelling tower owners to allocate budget to stakeholder engagement and stealth designs. Inconsistent federal-state regulations exacerbate uncertainty, leading to contingency leasing of mobile cell-on-wheels that inflate project costs. Cumulative delays depress the net present value of long-term contracts, dampening near-term construction pipelines within the German telecom tower market.

Rising Financing Costs Dampening BTS Economics

Benchmark European interest rates climbed from near-zero in 2022 to an average of 4.5% in 2025, raising the weighted-average cost of capital for leveraged TowerCos by 180 basis points. With Western Europe's build costs averaging EUR 135,000 (USD 147,000) per tower, higher debt service eats into equity returns, slowing speculative builds in marginal coverage areas. Asset-backed securities such as Vantage Towers’ GBP 600 million issuance help diversify funding, yet coupons now price 120-150 basis points above swap rates, materially higher than pre-2023 levels. Smaller TowerCos face tightened bank covenants, prompting consolidation or joint-venture structures. Consequently, capital discipline remains essential for sustaining EBITDA margins in the German telecom tower market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Lead Market Evolution

Independent TowerCos controlled 57.67% of the German telecom tower market in 2024 and are projected to advance at a 7.07% CAGR through 2030, as MNOs keep divesting passive assets to free capital for spectrum and core-network upgrades. Deutsche Funkturm, with 34,000 sites, exemplifies this shift after DigitalBridge and Brookfield acquired a 51% stake at an enterprise value of EUR 17.5 billion (USD 19.1 billion) in 2024, setting valuation benchmarks that encouraged further transactions. Vantage Towers’ portfolio of 19,400 German locations, following Vodafone’s gradual stake reduction, illustrates how independent ownership unlocks multitenant synergies and operational automation that lift tenancy ratios from 1.4x to 1.6x on mature sites.

Operator-owned residual portfolios continue to shrink, yet they retain strategic assets where immediate capacity upgrades or critical national-security links necessitate direct control. Joint-venture TowerCos emerge as hybrid models enabling MNOs to keep partial economic interest while tapping external capital. MNO-captive structures persist for niche rooftops atop proprietary data centers or broadcast facilities that demand high security or bespoke power feeds. Regulatory oversight favors neutral-host frameworks, and Bundeskartellamt scrutiny of vertical integration pressures MNO-controlled TowerCos to maintain transparent access terms that foster competition in the Germany telecom tower market.

By Installation: Rooftop Solutions Drive Urban Densification

Rooftops represented a 50.44% share of the German telecom tower market size in 2024 and will grow at a 4.72% CAGR through 2030 as dense urban 5G networks depend on unobtrusive, high-elevation points already connected to power and backhaul. Converting 12,000 decommissioned phone booths into micro-rooftop sites illustrates creative real-estate re-use that shortens permitting cycles and monetizes dormant assets. TCS and Vantage Towers’ digital service platform for landlord engagement automates thousands of lease negotiations, ensuring predictable site retention and rent escalations.

Ground-based towers remain indispensable for rural and highway coverage, especially where lattice structures support multi-band antennas required for Open-RAN deployments. Wooden tower pilots balance environmental goals with community aesthetics, winning permits in sensitive areas such as nature reserves. The benign visual profile and quicker civil works timeline of monopoles keep them relevant for suburban infill, yet rooftop expansion remains the major contributor to incremental tenancy in the German telecom tower market.

By Fuel Type: Renewable Energy Transformation Accelerates

Grid/diesel hybrid solutions maintained a 54.93% share of the German telecom tower market size in 2024, but renewable-powered installations are scaling at a 12.54% CAGR to 2030, riding EU Fit-for-55 and German Energiewende policies. Energy-autonomous towers eliminate diesel logistics and cut carbon output, appealing to ESG-minded landlords and municipal regulators. Deutsche Telekom’s trial of integrated solar-wind turbines plus lithium-ion storage achieved 70% grid independence during summer months, while Vodafone outfitted 1,500 urban rooftops with solar arrays to meet its 2025 carbon-neutral target.

Capex intensity remains a hurdle, yet battery storage prices dropped 18% year-over-year in 2025, narrowing the payback gap to under six years on high-irradiance sites. Specialized energy-as-a-service providers now bundle storage, maintenance, and carbon-credit monetization, enabling TowerCos to adopt renewables without large up-front outlays. These trends broaden ancillary revenue pools and reinforce the German telecom tower market’s sustainability narrative.

By Tower Type: Lattice Growth Driven by 5G Requirements

Monopole structures captured 48.42% of Germany's telecom tower market size in 2024, and lattice structures are forecast to grow at a 12.27% CAGR to 2030 as multiple-input multiple-output (MIMO) antennas and Open-RAN radios require heavier-load-bearing frames. Deutsche Telekom’s pledge to roll out 3,000 Open-RAN sites by 2027 underscores demand for towers that can host multi-vendor arrays plus edge cabinets. Traditional monopoles still command a 48.42% share, favored for cost-efficient suburban deployments and sites under 40 meters.

Guyed masts retain relevance in sparsely populated flat terrains where land prices are low, while stealth/concealed towers satisfy stringent heritage or visual-impact rules in historic city cores. Wooden variants offer a middle ground by combining lattice geometry with eco-friendly materials, helping TowerCos win community approval. Structural diversity enables the German telecom tower market to tailor solutions to local zoning, load, and aesthetic constraints.

Geography Analysis

Germany's telecom tower market shows dense clustering in Berlin, Munich, Hamburg, and the Rhine-Ruhr corridors, where data traffic is highest and rooftop availability eases densification. Deutsche Telekom’s 2025 rollout plan added new sites in Darmstadt-Dieburg, Wurzburg, Munster, and Elbe-Elster, illustrating a phased approach that pairs urban infill with rural expansion. Federal subsidies target eastern states to correct legacy infrastructure gaps, improving mobile broadband parity and unlocking industrial IoT adoption in Brandenburg’s manufacturing parks.

Border regions benefit from EUR 1 billion EU Connecting Europe Facility Digital grants that fund 5G transport corridors, such as the 60-kilometer A6 Saarbrucken-Metz “5G Autobahn to Autoroute.” Vantage Towers, TOTEM, Orange, and O2 Telefonica jointly deploy neutral-host infrastructure that supports autonomous-vehicle platooning and cross-border handover testing. The Hamburg-Berlin rail modernization will integrate FRMCS and 5G by 2026, catalyzing additional tower nodes along the 278-kilometer route to guarantee continuous gigabit connectivity for high-speed trains.

Industry hubs such as Munich’s automotive belt prioritize low-latency edge computing, spurring rooftop micro-data-center attachments on existing macro sites. Meanwhile, federal states like Bavaria and Baden-Württemberg streamline permitting with digital portals that cut approvals to under 90 days, contrasting with 180-plus days in parts of North Rhine-Westphalia. Such policy disparities influence portfolio allocation within the German telecom tower market and dictate risk-adjusted hurdle rates for investors.

Competitive Landscape

The German telecom tower market exhibits moderate concentration as Deutsche Funkturm, Vantage Towers, and American Tower Germany collectively operate roughly 68,000 sites. Strategic moves emphasize digital twin platforms, automated lease accounting, and AI-driven predictive maintenance that shrink site-level opex by 8-12%. Deutsche Funkturm’s post-acquisition integration plan channels USD 300 million into advanced asset-management software, aiming to lift the average tenancy ratio to 1.8x by 2027.

Regulatory scrutiny remains high. Bundeskartellamt charged Vodafone and Vantage Towers for allegedly hindering 1&1’s site access, signaling tougher enforcement against vertical foreclosure. Vodafone divested an additional EUR 1.3 billion stake in Vantage Towers in July 2024, while Cellnex exited Ireland to focus on core continental markets, selling to Phoenix Tower International for EUR 971 million.

Technology partnerships expand service scope. TCS and Vantage Towers jointly launched a pan-EU landlord-management portal in March 2025 that automates contract renewals and real-time energy-consumption monitoring, enhancing landlord retention and ESG reporting. American Tower Germany pilots edge-computing cabinets on 50 sites, leasing micro-data-center capacity to cloud providers seeking low-latency access to urban users. These initiatives illustrate portfolio owners’ shift from passive landlords to integrated digital-infrastructure operators in the German telecom tower market.

Germany Telecom Towers Industry Leaders

Deutsche Funkturm (GD Towers)

Vantage Towers AG

American Tower Germany

Phoenix Tower International (NOVEC GmbH)

Vodafone Germany

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Germany’s regulator sided with 1&1 in a dispute with Vodafone over 5G rollout obligations, potentially reshaping site-sharing agreements.

- March 2025: TCS partnered with Vantage Towers to launch a digital service platform for landlord management across Europe, targeting rooftop lease automation.

- February 2025: Phoenix Tower International acquired Cellnex’s Ireland business for EUR 971 million, underscoring sustained investor appetite for European tower assets.

Germany Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The German telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), installation (rooftop and ground-based), and fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Operator-Owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-Based |

| Renewable-Powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth/Concealed |

| By Ownership | Operator-Owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-Based | |

| By Fuel Type | Renewable-Powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth/Concealed |

Key Questions Answered in the Report

What is the forecast CAGR for the Germany telecom tower market through 2030?

The Germany telecom tower market is projected to grow at a 3.87% CAGR from 2025 to 2030.

How large will German tower assets be worth by 2030?

Germany telecom tower market size is expected to reach USD 2.17 billion in 2030.

Which ownership model is expanding fastest in German towers?

Independent TowerCos are advancing at a 7.07% CAGR as MNOs monetize passive assets.

Why are renewable-powered sites gaining traction?

Renewable systems cut carbon emissions and operating costs, aligning with EU Fit-for-55 mandates.

What regulatory body oversees tower competition issues in Germany?

Bundeskartellamt monitors antitrust compliance and site-access fairness among tower operators.

Page last updated on: