Vietnam Telecom Towers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

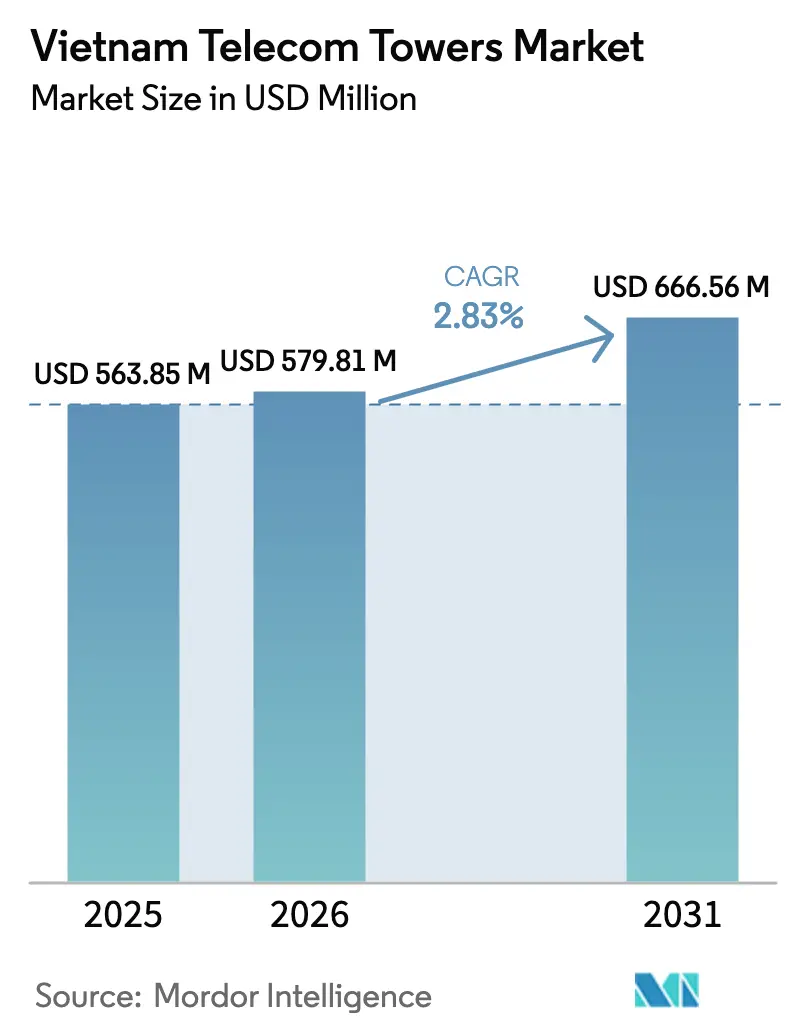

| Base Year Market Size (2025) | USD 563.85 Million |

| Market Size (2026) | USD 579.81 Million |

| Market Size (2031) | USD 666.56 Million |

| Growth Rate (2026 - 2031) | 2.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Telecom Towers Market Analysis by Mordor Intelligence

The Vietnam Telecom Towers Market size is expected to grow from USD 563.85 million in 2025 to USD 579.81 million in 2026 and is forecast to reach USD 666.56 million by 2031 at 2.83% CAGR over 2026-2031.

This outlook captures the industry’s shift from aggressive network build-out to a phase focused on densification, energy efficiency, and asset monetization. Heightened 5G coverage targets, supportive regulations under the 2024 Telecom Law, and rising power-system upgrades underpin demand for new structures, although the pace moderates as nationwide 4G coverage has largely been achieved. Government subsidies covering 15% of eligible 5G equipment costs and streamlined permitting for shared passive assets are catalyzing site additions, while operator investment discipline steers capital toward high-return urban hotspots. Independent tower companies are strengthening footholds as sale-and-lease-back transactions help mobile network operators (MNOs) unlock cash for spectrum and radio upgrades, sustaining steady growth in the Vietnam telecom tower market.

Key Report Takeaways

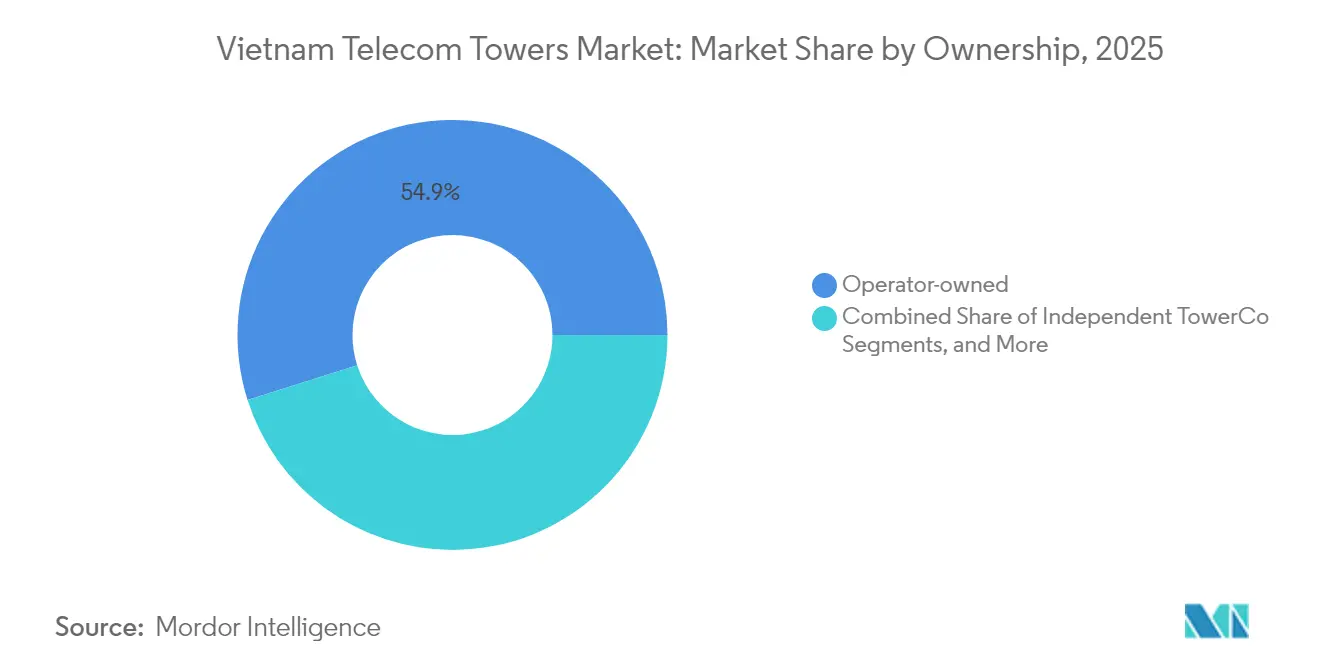

- By ownership, operator-owned assets captured 54.88% of the Vietnam telecom tower market share in 2025, whereas independent tower companies are projected to register the fastest 12.1% CAGR through 2031.

- By installation, ground-based towers led with a 68.73% revenue share in 2025; rooftop installations are forecast to expand at a 5.01% CAGR to 2031.

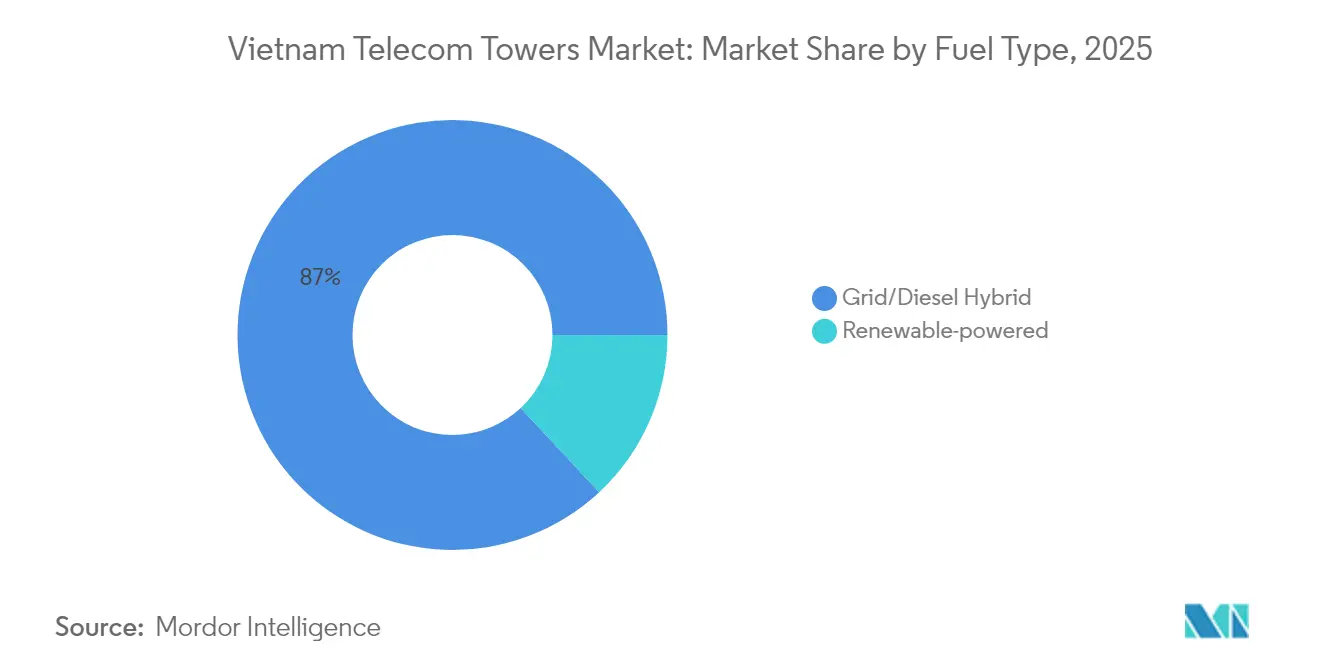

- By fuel type, grid/diesel hybrid solutions accounted for 86.95% of the Vietnam telecom tower market size in 2025, while renewable-powered sites are set to surge at a 28.1% CAGR to 2031.

- By tower type, monopoles commanded 45.12% of the Vietnam telecom tower market share in 2025; stealth or concealed designs hold the highest growth outlook at 7.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Telecom Towers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding mobile‐data traffic from video and gaming apps | +0.8% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Accelerated 5G rollout mandated by MIC (nation-wide 2025 target) | +1.2% | National, prioritizing provincial capitals and industrial zones | Medium term (2-4 years) |

| Sale-and-lease-back appetite to unlock MNO capex for 5G | +0.6% | National, with early adoption in Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Government incentives for shared passive infrastructure | +0.4% | National, with regulatory support from MIC | Long term (≥ 4 years) |

| Edge-AI and micro-data-center nodes driving urban densification | +0.3% | Urban centers, particularly Ho Chi Minh City, Hanoi, Da Nang | Long term (≥ 4 years) |

| Solar-hybrid power PPAs that slash diesel OPEX | +0.5% | National, with higher impact in rural and off-grid areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding Mobile Data Traffic from Video and Gaming Apps

Streaming and e-sports usage keep Vietnamese cellular networks under constant pressure, compelling operators to add capacity sites in shopping districts, transit hubs, and university corridors. By February 2025, the nationwide median 5G download speed reached 187.58 Mbps, triple the 4G baseline, yet video streaming at 1080p and multiplayer gaming quickly saturate available bandwidth during evening peaks [1]GenK Editorial Team, “Which carrier has the fastest 5G speed in Vietnam?,” GenK, genk.vn . Viettel counted 5.5 million 5G subscriptions with a median 226.27 Mbps speeds, whereas VNPT served 3 million lines at 157.17 Mbps, underscoring differentiated quality strategies that shape tower loading patterns. Hotspot congestion triggers a need for both additional macro structures and rooftop small cells, sustaining demand in the Vietnam telecom tower market. Urban edge-computing nodes introduced by Viettel support ultra-low-latency services, yet each node also increases power load, encouraging hybrid energy solutions. Consequently, operators rely on neutral-host towers to accelerate dense deployments without overextending balance sheets, reinforcing multi-tenant leasing momentum.

Accelerated 5G Rollout Mandated by MIC

The Ministry of Information and Communications (MIC) requires commercial 5G service across all 63 provinces by the end of 2025, framing the most ambitious network timetable to date [2]VietnamPlus Staff, “Vietnam accelerates 5G commercialisation,” VietnamPlus, vietnamplus.vn. Resolution 193 reimburses up to 15% of qualified radio equipment costs once operators exceed 20,000 accepted 5G base stations, compressing typical deployment cycles into 24-30 months. Viettel already operates 6,500 5G sites that cover more than 90% of outdoor areas in provincial capitals, industrial parks, and major airports, and further district-level builds are slated for 2025. Meeting the government’s 99% population-coverage target by 2030 will require 15,000-20,000 additional macro locations plus significant rooftop infill, translating into stable structural demand for the Vietnam telecom tower market. The spectrum roadmap also earmarks mid-band allocations for shared passive infrastructures, which shortens permitting cycles and reduces duplication of street furniture.

Sale-and-Lease-Back Appetite to Unlock MNO Capex for 5G

Sharp increases in radio, core upgrade, and spectrum fees compel Vietnamese MNOs to extract capital from non-core assets. Early pilot transactions in Ho Chi Minh City reveal tower valuations reaching USD 100,000 per site, a level attractive to global infrastructure funds searching for stable yield. Although 85% of towers remained in operator hands in 2024, management teams publicly indicated willingness to divest secondary portfolios provided long-term leaseback terms are secured. This shift enables independent TowerCos to scale faster, improving tenancy ratios while letting carriers funnel sales proceeds into 5G radios and transport upgrades. Viettel Construction’s 2024 infrastructure-for-lease revenue jumped 39%, illustrating the financial logic of infrastructure monetization [3]Viettel Construction, “Annual Report 2023,” Viettel Construction, viettelconstruction.com.vn. The evolution is expected to keep transaction volumes rising and extend the runway for the Vietnam telecom tower market.

Government Incentives for Shared Passive Infrastructure

Vietnam’s Telecom Law 2024 formalizes co-location mandates that aim to reduce redundant steel and concrete in densely built environments. Municipalities now grant expedited one-stop approvals for projects featuring multi-tenant readiness, shaving months off construction schedules and aligning with national sustainability targets. Passive sharing can lower total network build cost by 20-30% over a decade, which MIC positions as crucial for rural inclusion objectives. Operators responding to these incentives design new macro structures with pre-installed mounts, power cabinets, and fiber ducts that simplify second-tenant onboarding. This framework, together with 5G coverage targets, broadens addressable revenue for TowerCos in the Vietnam telecom tower market and stabilizes occupancy rates across asset vintages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 85% towers still MNO-owned limiting independent tenancy growth | -0.9% | National, with higher concentration in rural areas | Medium term (2-4 years) |

| Slow municipal permitting and land-use approval cycles | -0.6% | National, with severe bottlenecks in major cities | Short term (≤ 2 years) |

| Spectrum-fee discounts for active-network sharing cut tower-lease upside | -0.3% | National, affecting all operators equally | Long term (≥ 4 years) |

| Patchy rural grid forcing costly diesel logistics | -0.4% | Rural and remote areas, particularly mountainous regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

85% Towers Still MNO-Owned Limiting Independent Tenancy Growth

Operator control over roughly 40,000 structures limits immediate co-location opportunities for neutral hosts. Average tenancy sits at 1.034 per site, well below the 1.8 level seen in mature ASEAN peers, restricting revenue scalability per structure. Independent TowerCos must therefore pursue greenfield builds or wait for carriers to divest, both of which slow near-term growth in the Vietnam telecom tower market. Regulatory nudges encouraging divestitures are present, yet institutional inertia inside large state-owned groups remains strong. Until substantial portfolios change hands, tower companies will operate under an occupancy-constrained environment, dampening network economics despite robust demand for additional tenants.

Slow Municipal Permitting and Land-Use Approval Cycles

Provincial authorities lack uniform criteria for evaluating telecom structures, resulting in timelines that stretch 6-12 months in Ho Chi Minh City and Hanoi. Complex land-use classifications, environmental checks, and community consultations contribute to sequential rather than parallel reviews, delaying service launches and increasing financing costs. Small tower operators face higher friction given their limited in-house regulatory teams, whereas state-owned incumbents leverage established government relationships. Decision 240/QD-TTg seeks to digitize cross-agency approvals, but fragmented execution has yet to produce material time savings. Extended lead times hamper network densification plans, curbing the speed at which the Vietnam telecom tower market can capitalize on 5G traffic growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership: Independent TowerCos Scale as Monetization Accelerates

Operator-owned structures accounted for 54.88% of the Vietnam telecom tower market size in 2025. Independent TowerCos posted a robust 12.1% CAGR outlook, reflecting rising sale-and-lease-back pipelines and supportive legislation.

Operator dominance stems from Vietnam’s historic mandate requiring carriers to build coverage rapidly across 63 provinces. Viettel, VNPT, and MobiFone financed their own steel to meet universal service goals, thereby anchoring strategic control. As 5G capital needs balloon, internal rate-of-return discipline encourages operators to unlock trapped equity in towers, catalyzing divestitures into the Vietnam telecom tower market. Independent players such as EdgePoint Infrastructure and OCK Group leverage global fund backing to craft acquisition term sheets that fit MNO lease requirements, raising the likelihood of larger portfolio transfers. International capital flows also introduce professional asset-management practices, which lift tenancy ratios through targeted marketing to Internet of Things and fixed-wireless providers. The shift from asset-heavy to asset-light strategies thus represents the structural inflection shaping future tower tenancy economics.

By Installation: Rooftop Uptick Complements Ground-Based Core

Ground-based structures captured 68.73% of the Vietnam telecom tower market share in 2025, owing to favorable land economics outside dense city blocks. Rooftop cells are on track for 5.01% CAGR through 2031 as 5G millimeter-wave capacity layers take shape in commercial cores.

Traditional macro towers remain essential for blanket coverage across plains, deltas, and mountainous regions. Their taller elevations maximize radio footprint, enabling cost-efficient reach into rural districts where subscriber densities stay modest. Yet Vietnam’s two mega-cities exhibit land scarcity and aesthetic codes that discourage fresh macro builds, making rooftop deployments and integrated street furniture key supplements. Operators partner with real-estate firms to negotiate long leases on hotel roofs, shopping-mall facades, and municipal lighting poles, sharply reducing civil engineering costs while speeding time-to-on-air. The result is a hybrid topology where ground and rooftop assets coexist, each optimized for propagation environment, regulatory constraints, and return on invested capital. Diverse installation profiles give the Vietnam telecom tower market resilience against zoning delays and enable granular capacity placement aligned with data-traffic heat maps.

By Fuel Type: Renewable Momentum Reduces OPEX

Grid/Diesel hybrids delivered 86.95% of the Vietnam telecom tower market size in 2025, but renewable-powered solutions are set for an eye-catching 28.1% CAGR to 2031.

Vietnam’s patchy rural grid coverage forces diesel generators to serve as primary or standby power in 22 provinces. Fuel logistics add 14-18% to site operating costs, pressing tower owners to adopt solar, wind, or battery-hybrid packages. EdgePoint’s pilot solar-hybrid tower showed a 78% reduction in diesel runtime and 30% lower total energy cost within six months of launch. LiFePO4 storage with ≥6,000 cycles now displaces lead-acid banks, delivering ten-year life and smaller footprints. Government power-purchase-agreement regulations under PDP8 cap rooftop solar at 2,600 MW yet earmark preferential feed-in rates for off-grid telecommunications facilities, further stimulating uptake. Over the forecast horizon, tower owners will blend grid, solar PV, and low-sulfur diesel in variable ratios attuned to local irradiation and uptime targets, diversifying revenue streams through power-as-a-service offerings to colocated tenants.

By Tower Type: Stealth Designs Ease Urban Resistance

Monopole towers held 45.12% of the Vietnam telecom tower market share in 2025, while stealth or concealed variants show a 7.02% CAGR outlook as urban regulators tighten visual-impact criteria.

Monopoles dominate due to smaller footprints, faster foundation work, and competitive material consumption. They function well for up to three tenants, making them ideal for suburban and rural builds. Conversely, lattice towers, though structurally robust, face community pushback in residential precincts and heritage zones. This scenario fuels demand for camouflaged street poles and multipurpose smart poles integrating 5G radios, LED lighting, and CCTV equipment. Viettel’s pilot smart pole program demonstrates how concealed designs accelerate permitting by positioning towers as civic utilities rather than intrusive infrastructure. Over time, aesthetic requirements will spread beyond megacities into tier-two urban centers, increasing the addressable market for specialized concealment vendors and aluminum composite materials. The Vietnam telecom tower market thus evolves from pure structural concerns toward holistic urban design integration.

Geography Analysis

Tower distribution tracks Vietnam’s economic geography, with roughly 60% of active sites concentrated along the southern growth corridor and the northern Red River Delta. Ho Chi Minh City reports an average 5G download speed of 158.18 Mbps, edging Hanoi’s 144.78 Mbps, yet Da Nang tops the chart at 324.05 Mbps, reflecting early optimization in this coastal tech hub. Urban performance advantages derive from higher spectrum reuse, rooftop density, and proactive municipal coordination. Viettel alone operates branches in all 63 provinces, highlighting the logistical scale required for nationwide coverage commitments.

Provincial capitals enjoy first-wave 5G benefits because operators focus subsidies and capital on high population density. District-level rollouts are planned through 2026 to hit universal 5G targets, yet mountainous northern provinces face terrain challenges that inflate per-site capex. Border areas such as Quang Binh recently saw the completion of a ninth mobile station funded at USD 40,000 per site to ensure strategic connectivity. Such projects blend commercial and national-security goals and often rely on shared passive infrastructure to achieve cost parity with low-income subscriber bases.

Islands and coastal tourist destinations add unique deployment hurdles tied to corrosive environments and limited grid reach. Renewable microgrids paired with satellite backhaul prove critical, expanding tower-owner services into integrated energy and connectivity bundles. Over the forecast, geographic growth will increasingly stem from densification within existing coverage footprints rather than pure greenfield expansion, underscoring the Vietnam telecom tower market’s maturity trajectory.

Competitive Landscape

Vietnam’s tower arena remains moderately concentrated. Viettel Construction anchors the field with 6,436 sites, leveraging vertical integration in planning, civil works, and maintenance to compress build schedules and cost structures. The company intends to erect 4,000 additional structures by 2026, maintaining decisive scale economies. Independent challenger EdgePoint Infrastructure targets a 5,000-tower portfolio by 2025, backed by DigitalBridge funding, intensifying competition for rooftop leases in tier-one cities. OCK Group Vietnam operates nearly 2,000 structures, pursuing smaller tenancy markets and turnkey build-to-suit contracts.

Competitive focus is shifting from steel count toward energy solutions and digital twins. Viettel deploys smart construction management to deliver real-time progress dashboards, cutting average site delivery times to 52 days and elevating customer satisfaction. EdgePoint pilots solar-hybrid integrations to differentiate on operating expenses, while EDOTCO’s analytics platform teases possible market entry offering predictive maintenance and carbon-tracking services. Consolidation potential remains significant because fragmented, smaller portfolios under 100 structures face difficulty securing affordable financing to replace diesel gensets with green systems. Overall, strategic interplay between state-owned incumbents holding spectrum and private equity-backed TowerCos searching for tenancy maximization will define competitive intensity in the Vietnam telecom tower market.

Vietnam Telecom Towers Industry Leaders

Viettel Construction (CTR)

OCK Group Berhad (OCK Vietnam)

VNPT Net Corporation

EdgePoint Vietnam

Vinaphone

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: EdgePoint Towers deployed its first solar-hybrid solution aimed at reducing diesel runtime and emissions in rural sites.

- March 2025: MobiFone launched commercial 5G across major urban centers, becoming Vietnam’s third 5G operator.

- January 2025: DigitalBridge-backed EdgePoint announced plans to add more than 5,000 cell towers by 2025, signaling aggressive capacity expansion.

- December 2024: Viettel signed 13 international contracts valued at USD 8 million covering 5G systems and infrastructure during the Vietnam Defense Exhibition.

Vietnam Telecom Towers Market Report Scope

Telecommunication towers encompass a variety of structures, such as monopoles, tripoles, lattice towers, guyed towers, self-supporting towers, poles, masts, and other similar forms. These towers, equipped with one or more telecommunication antennas, facilitate radio communications. They can be situated on the ground or atop a building's rooftop and often include storage for equipment and electronic components.

The Vietnam telecom towers market is segmented by ownership (operator-owned, private-owned, and MNO captive sites), by installation (rooftop and ground-based), and by fuel type (renewable and non-renewable). The market size and forecasts are provided in terms of installed base (thousand units) for all the above segments.

| Operator-owned |

| Independent TowerCo |

| Joint-Venture TowerCo |

| MNO Captive |

| Rooftop |

| Ground-based |

| Renewable-powered |

| Grid/Diesel Hybrid |

| Monopole |

| Lattice |

| Guyed |

| Stealth / Concealed |

| By Ownership | Operator-owned |

| Independent TowerCo | |

| Joint-Venture TowerCo | |

| MNO Captive | |

| By Installation | Rooftop |

| Ground-based | |

| By Fuel Type | Renewable-powered |

| Grid/Diesel Hybrid | |

| By Tower Type | Monopole |

| Lattice | |

| Guyed | |

| Stealth / Concealed |

Key Questions Answered in the Report

How large is the Vietnam Telecom Towers Market in 2026?

The market is valued at USD 579.81 million in 2026, with a projected climb to USD 666.56 million by 2031.

What is the predicted CAGR for Vietnam’s tower sector?

The forecast CAGR stands at 2.83% for the 2026-2031 period.

Which ownership model is growing the fastest?

Independent TowerCos display the quickest growth, estimated at 12.1% CAGR as operators adopt sale-and-lease-back strategies.

Why are renewable-powered tower sites gaining attention?

Renewable-hybrid systems cut diesel operating costs by up to 30% and support ESG targets, driving a 28.1% CAGR for such sites.

How do 5G roll‐out mandates affect tower demand?

MIC’s requirement for nationwide 5G by 2025 accelerates macro and rooftop builds, creating steady demand for new structures and upgrades.

Page last updated on: