Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Morocco Telecom Towers Market Report is Segmented by Ownership (Operator-Owned, Independent TowerCo, Joint-Venture TowerCo, MNO Captive), Installation (Rooftop, Ground-Based), Fuel Type (Renewable-Powered, Grid/Diesel Hybrid), and Tower Type (Monopole, Lattice, Guyed, Stealth/Concealed). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Installed Base).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

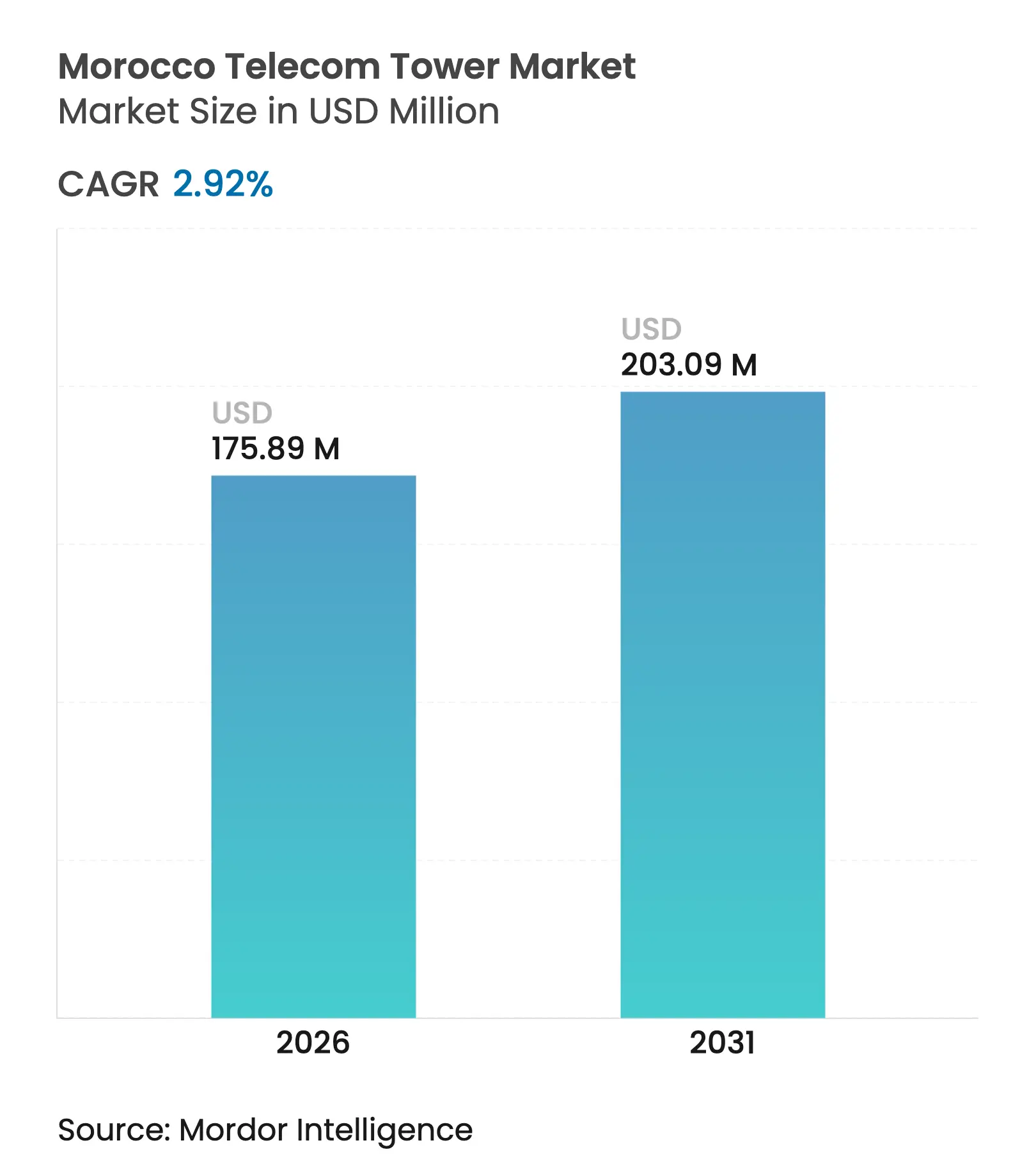

| Market Size (2026) | USD 175.89 Million |

| Market Size (2031) | USD 203.09 Million |

| Growth Rate (2026 - 2031) | 2.92 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

This growth rate appears modest at first glance, yet it masks rapid structural change as operators pivot from stand-alone asset builds to collaborative infrastructure-sharing that trims redundant capital and accelerates 5G readiness. Joint-venture models, advancing renewable-power adoption, and dense urban rooftop rollouts are reshaping competitive dynamics while keeping total tower counts on a measured trajectory. Market opportunities lie in densification for 5G, rural subsidy programs, and smart-city corridor builds, whereas pressures stem from lengthy municipal permitting, high spectrum license fees, and grid upgrade delays. Strategic choices around fuel mix, tower aesthetics, and ownership partnerships will determine how effectively stakeholders monetize the Morocco telecom towers market during the transition from 4G to full 5G coverage.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

5G rollout acceleration and network densification mandates

5G rollout acceleration and network densification mandates

| +1.2% | National; early focus on Casablanca, Rabat, Marrakech | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+1.2%

|

Geographic Relevance

:

National; early focus on Casablanca, Rabat, Marrakech

|

Impact Timeline

:

Medium term (2-4 years)

|

Government universal-service subsidies for rural coverage

Government universal-service subsidies for rural coverage

| +0.8% | Atlas Mountains, southern provinces | Long term (≥ 4 years) | |||

Rising mobile-data traffic and smartphone penetration

Rising mobile-data traffic and smartphone penetration

| +0.6% | Urban centers nationwide | Short term (≤ 2 years) | |||

Tower-sharing joint ventures reduce CAPEX burden

Tower-sharing joint ventures reduce CAPEX burden

| +0.4% | National deployment zones | Medium term (2-4 years) | |||

Solar-plus-storage OPEX savings at off-grid sites

Solar-plus-storage OPEX savings at off-grid sites

| +0.3% | Desert and remote rural areas | Long term (≥ 4 years) | |||

Smart-city corridor builds along new highways

Smart-city corridor builds along new highways

| +0.2% | Highway corridors, economic zones | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

5G Rollout Acceleration and Network Densification Mandates

Morocco’s first commercial 5G services arrive in November 2025, backed by a government target of 25% population coverage in 2026 and 70% by 2030. Meeting these thresholds demands roughly 6,000 additional sites, most in dense urban clusters where millimeter-wave requires tighter cell spacing. The Morocco telecom towers market therefore enters a phase where site count grows more quickly than tenancy ratios, compelling operators to offset costs through shared passive assets. The Maroc Telecom-Inwi TowerCo, capitalized at USD 460 million, exemplifies how collaboration trims individual tower CAPEX by about 40% while keeping rollout timelines intact. ANRT’s open-access rules ensure that Orange Morocco can co-locate on shared sites, preserving competitive neutrality while enhancing capital efficiency. [1]“Morocco Sets 70% 5G Coverage Goal by 2030,” Tech Africa News,

Government Universal-Service Subsidies for Rural Coverage

The national universal-service fund reimburses 60-80% of tower build costs in locations with fewer than 50 inhabitants per square kilometer, making low-ARPU rural sites economically viable. [2]ANRT, “Universal Service Fund Guidelines,” anrt.maSubsidy commitments last a minimum of 10 years, giving investors predictable cash flows that underpin long-term tenancy contracts. For the Morocco telecom towers market, such subsidies soften ROI risk in the Atlas Mountains and Saharan fringe where grid power is scarce and backhaul expensive. Operators leverage these funds to extend basic 4G today and prepare for 5G fixed-wireless as device costs fall, aligning rural coverage goals with broader territorial-cohesion policy.

Rising Mobile-Data Traffic and Smartphone Penetration

Smartphone adoption hit 89% in cities and 67% in rural districts by 2024, pushing video streaming and e-commerce usage that strains existing 4G cell sites. Average data revenue advanced 15.6% year-on-year, justifying additional site builds even in mature coverage footprints. Operators can no longer rely solely on spectrum refarming; they must densify networks to avoid congestion-related churn. The Morocco telecom towers market therefore benefits from capacity-driven demand that remains resilient even when subscriber additions plateau, providing a steady pipeline of new tenancies and equipment upgrades.

Tower-Sharing Joint Ventures Reduce CAPEX Burden

The MAD 4.4 billion (USD 423 million) Maroc Telecom-Inwi TowerCo shows how shared ownership curbs redundant builds while retaining competition at the active-equipment layer. A guaranteed dual-anchor tenancy structure secures early cash flow, and third-party leasing at regulated rates generates incremental revenue. With spectrum costs rising, operators allocate scarce capital toward antenna-level differentiation rather than duplicative steel-and-concrete. This paradigm elevates tenancy ratios, improves EBITDA margins, and accelerates the shift toward professional tower management practices typical of more mature African markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lengthy municipal permitting cycles for new sites

Lengthy municipal permitting cycles for new sites

| -0.7% | Casablanca, Rabat, Marrakech heritage districts | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-0.7%

|

Geographic Relevance

:

Casablanca, Rabat, Marrakech heritage districts

|

Impact Timeline

:

Short term (≤ 2 years)

|

High spectrum-license fees crowd out infra budgets

High spectrum-license fees crowd out infra budgets

| -0.5% | National allocations | Medium term (2-4 years) | |||

Land-owner push-back in heritage zones

Land-owner push-back in heritage zones

| -0.3% | UNESCO medinas and coastal resorts | Long term (≥ 4 years) | |||

Slow utility-grid upgrades delaying green-power sites

Slow utility-grid upgrades delaying green-power sites

| -0.2% | Off-grid rural areas | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Lengthy Municipal Permitting Cycles for New Sites

Environmental reviews, architectural approvals, and community consultations extend average permitting to 12-18 months in major cities. The timeline stretches further for stealth installations near UNESCO World Heritage assets, where aesthetic scrutiny is intense. These administrative delays consume as much as 60% of project schedules and lift soft-cost shares of total capex to 15-20% for small rooftop builds. For the Morocco telecom towers market, such bottlenecks threaten the timely realization of 5G densification plans, pressing stakeholders to streamline one-stop approval frameworks.

High Spectrum-License Fees Crowd Out Infrastructure Budgets

ANRT’s 5G auctions require upfront payments near USD 100-150 million per operator, diverting capital away from tower builds. Smaller carriers face disproportionate strain, often deferring coverage obligations until cash flows rebound. The capex squeeze constrains independent TowerCo demand in the near term and places a ceiling on how quickly the Morocco telecom towers market can scale renewable retrofits or rural expansion programs. [3]“Morocco 5G Spectrum Auction Raises USD 300 Million,” Light Reading, lightreading.com

By Ownership: Joint Ventures Transform Market Structure

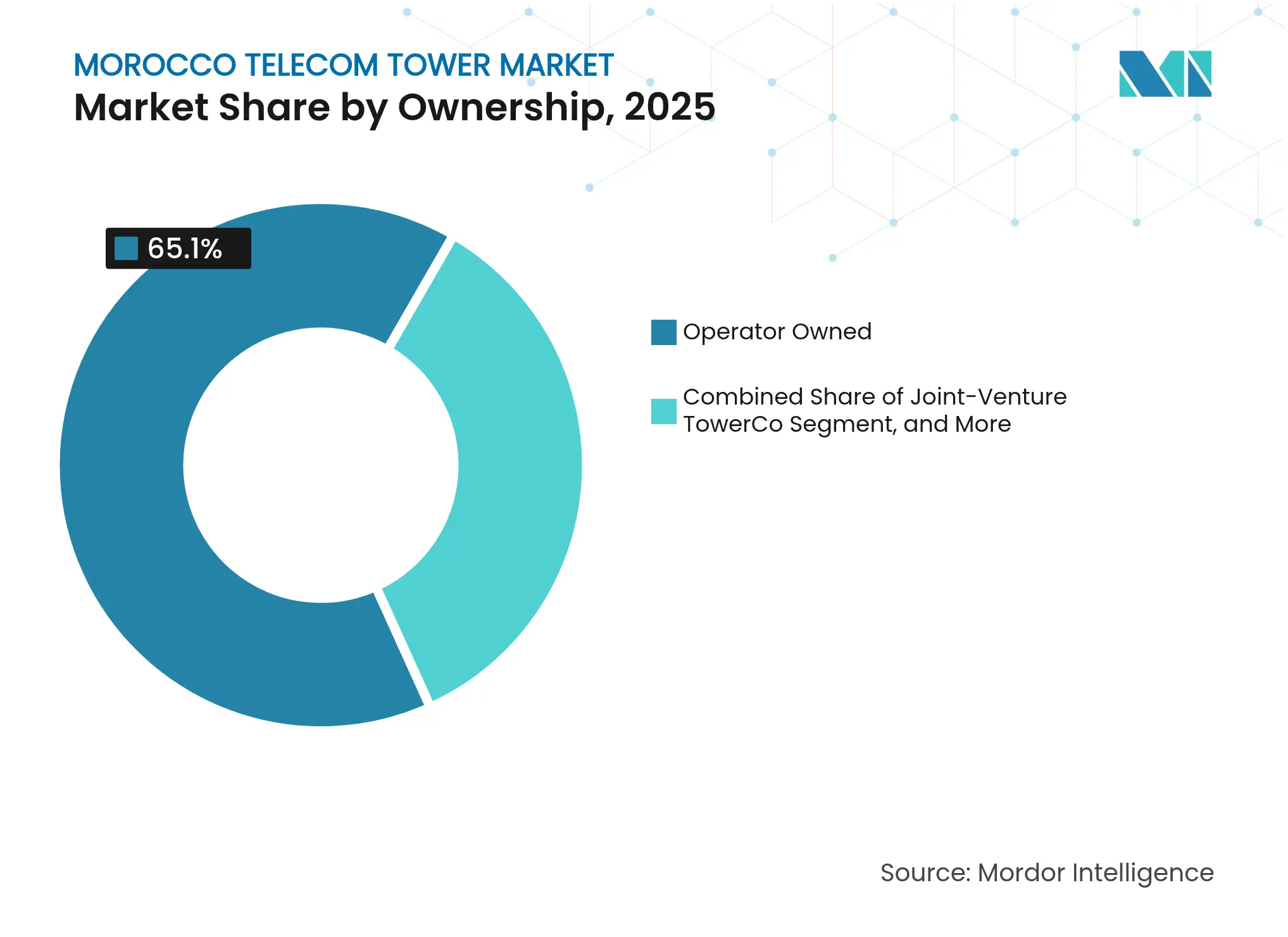

Joint-venture TowerCos hold the fastest growth trajectory at a 13.15% CAGR even as operator-controlled assets keep 65.10% of the Morocco telecom towers market share in 2025. The Maroc Telecom-Inwi partnership unlocks capital by shifting non-core passive assets into a separate vehicle, allowing both operators to redeploy funds toward spectrum and fiber. This structure limits overlap in suburban fringes where single-operator sites once proliferated, improving tenancy ratios and overall asset utilization.

Continued regulatory backing for open-access principles ensures that joint ventures remain attractive to third-party tenants, including MVNOs and emerging IoT network providers. While independent TowerCos remain sparse compared with Nigeria or Kenya, the success of the initial partnership could catalyze secondary divestments from Orange Morocco, further expanding the Morocco telecom towers market. Integration of AI-driven asset-management platforms in joint ventures promises lower maintenance costs and faster fault resolution, thereby strengthening EBITDA margins and freeing cash for future 5G small-cell projects.

Note: Segment shares of all individual segments available upon report purchase

By Installation: Urban Density Drives Rooftop Growth

Ground-based structures still account for 53.80% of the Morocco telecom towers market size in 2025, but rooftop assets lead growth at a 4.38% CAGR amid rising urban land scarcity. High-rise rooftops enable quick densification without new land acquisition, aligning with municipal efforts to preserve green space. Rooftop setups typically reach breakeven faster because civil works are minimal and backhaul fiber is closer, lowering capex per tenant by up to 25%.

Heritage districts in Marrakech and Fes favor discreet rooftop and church-steeple blends to avoid visual intrusion, accelerating demand for compact tri-band antennas and integrated small cells. Rooftop adoption also eases 5G millimeter-wave deployment, where line-of-sight and street-level clutter complicate traditional macro-tower designs. These factors combine to keep rooftops central to the Morocco telecom towers market as 5G coverage obligations tighten.

By Fuel Type: Renewable Transition Accelerates

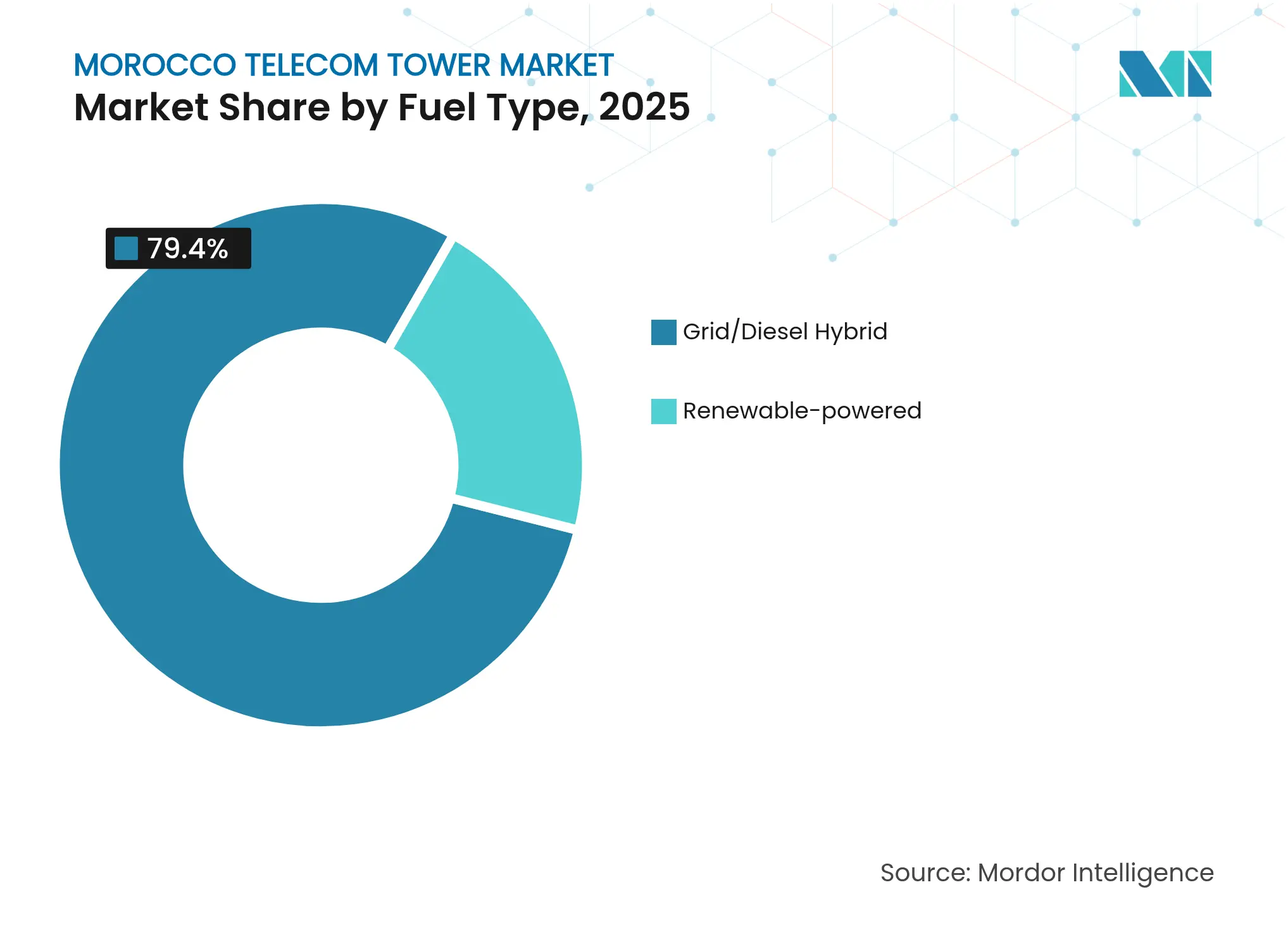

Grid/diesel hybrids dominate 79.40% of the Morocco telecom towers market size in 2025, yet renewable-powered sites post an 17.95% CAGR as operators chase OPEX savings and ESG targets. Solar irradiation exceeding 2,800 kWh/m² in southern provinces, plus falling battery costs, lifts internal rates of return on solar-plus-storage retrofits above 18%, compared with sub-10% for diesel-only upgrades. Orange Africa’s regional program reports 80% fuel reduction and avoids 330,000 tCO₂e annually, validating commercial viability.

Energy spend accounts for up to 45% of site OPEX for diesel-reliant rural towers; switching to renewables cuts that share by one-third while increasing uptime where grid outages average eight hours daily. For the Morocco telecom towers industry, renewable retrofits deliver both cost savings and regulatory goodwill, positioning operators favorably for green-bond financing and foreign direct investment.

Note: Segment shares of all individual segments available upon report purchase

By Tower Type: Stealth Solutions Address Aesthetic Concerns

Monopoles lead with 48.05% of the Morocco telecom towers market share, but stealth and concealed variants grow fastest at 4.29% CAGR as tourism-rich municipalities tighten aesthetic rules. Concealed palm-tree or minaret-style designs cost 20-30% more upfront but shorten permitting cycles by months, offsetting higher capex with faster revenue realization. Lattice structures remain essential along highways or mountainous routes needing high wind-load capacity, while guyed masts serve broadcast applications.

Stealth adoption is particularly strong near 2030 World Cup venue cities, where authorities seek visual neutrality. As ESG and community-engagement metrics gain weight in operator scorecards, concealed designs could exceed 15% of new builds by 2030, adding a premium but defensible niche within the Morocco telecom towers market.

The Atlantic corridor from Casablanca to Rabat houses more than 40% of Morocco’s population and the majority of mobile data traffic, driving disproportionate tower density. This region anchors early 5G deployments, pushing operators toward rooftop small cells inside dense business districts. Secondary hubs—Marrakech, Agadir, and Tangier—follow closely, balancing tourist influx with heritage-protection mandates that favor stealth towers.

Rural expanses in the Atlas Mountains and Saharan periphery rely heavily on universal-service subsidies. These zones often demand satellite backhaul and renewable power due to rugged terrain and sparse grid links. Government programs guarantee minimum 10-year service commitments, keeping the Morocco telecom towers market economically viable where pure commercial ROI would falter.

Highway corridors linking economic zones receive smart-city investments that bundle fiber, IoT sensors, and small-cell clusters. This integrated approach reinforces Morocco’s role as a Europe-Africa trade gateway and supports the 70% 5G coverage goal by 2030. Together, these regional nuances shape capex allocation, tenancy pricing, and technology choices across a diverse national footprint.

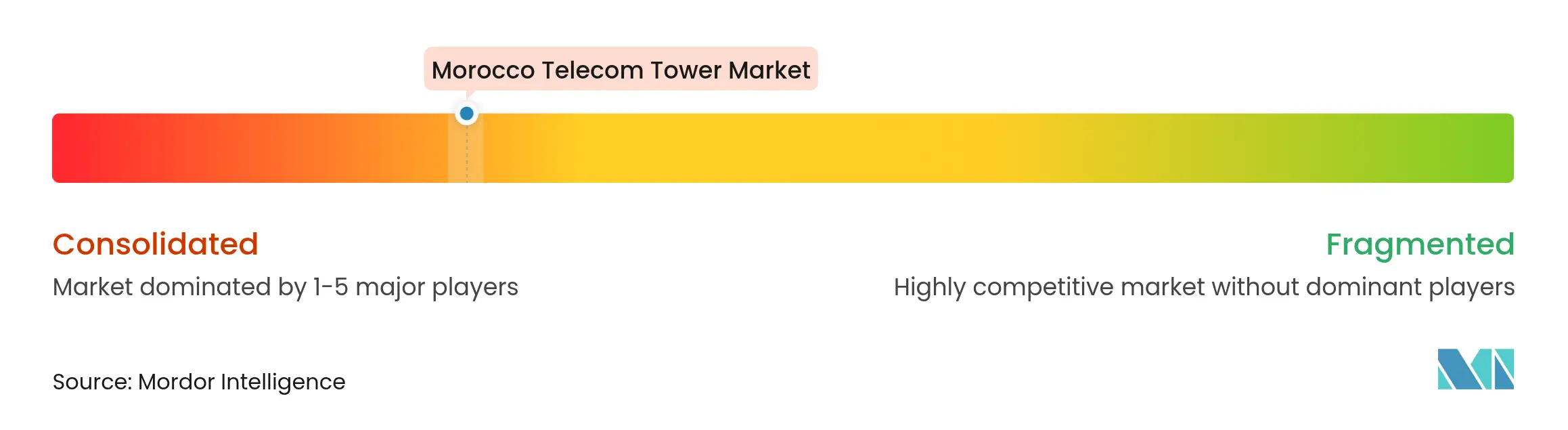

Market Concentration

Market structure centers on three integrated MNOs—Maroc Telecom, Inwi, and Orange Morocco—whose combined scale defines investment rhythm. Instead of erecting competing steel in parallel, the leading players now favor shared TowerCos that deliver higher tenancy ratios and lower debt loads. Maroc Telecom’s new FiberCo and TowerCo entities illustrate how portfolio separation attracts strategic investors while enhancing regulatory transparency.

Inwi leverages private funding agility to co-lead joint ventures, signaling a shift from market share battles toward cooperative efficiency. Orange Morocco prepares a parallel 5G rollout but may increasingly lease rather than build, especially after ANRT’s open-access rules cap rental margins. Limited independent TowerCo presence leaves whitespace for specialized rural or renewable-energy players, yet any entrant must navigate concentrated demand and regulatory scrutiny.

Technology partnerships with Vodafone Business and Zoho expand service layers beyond connectivity into SD-WAN, cybersecurity, and cloud. These alliances support revenue diversification as pure voice and SMS streams wane. Together, strategic collaboration, portfolio carve-outs, and digital-service adjacencies define the competitive tempo of the Morocco telecom towers market through 2030.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The telecommunication market is largely concerned with the operations and provision of infrastructure for transmitting data - voice, image, sound, text, and video. To expand its network and services, the telecommunication market relies on towers, which are used to mount telecommunication networking and power equipment.

The Report Covers Morocco Telecom Tower Companies and the Market is Segmented by Ownership (Operator-Owned, Private-Owned, MNO Captive Sites), by Installation (Rooftop, Ground-Based), by Fuel Type (Renewable, Non-Renewable). The Market Sizes and Forecasts are Provided in Terms of Installed Base (in Thousand Units ) for all the above Segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.