Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

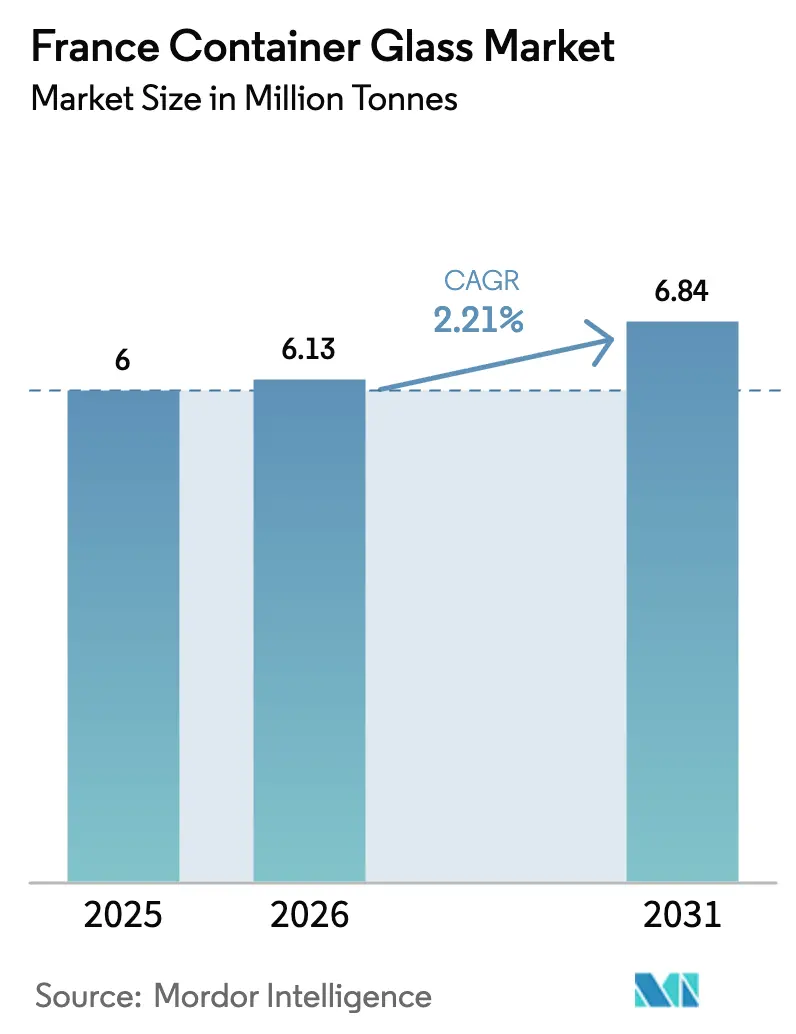

| Base Year Market Size (2025) | 6 Million tonnes |

| Market Volume (2026) | 6.13 Million tonnes |

| Market Volume (2031) | 6.84 Million tonnes |

| Growth Rate (2026 - 2031) | 2.21% CAGR |

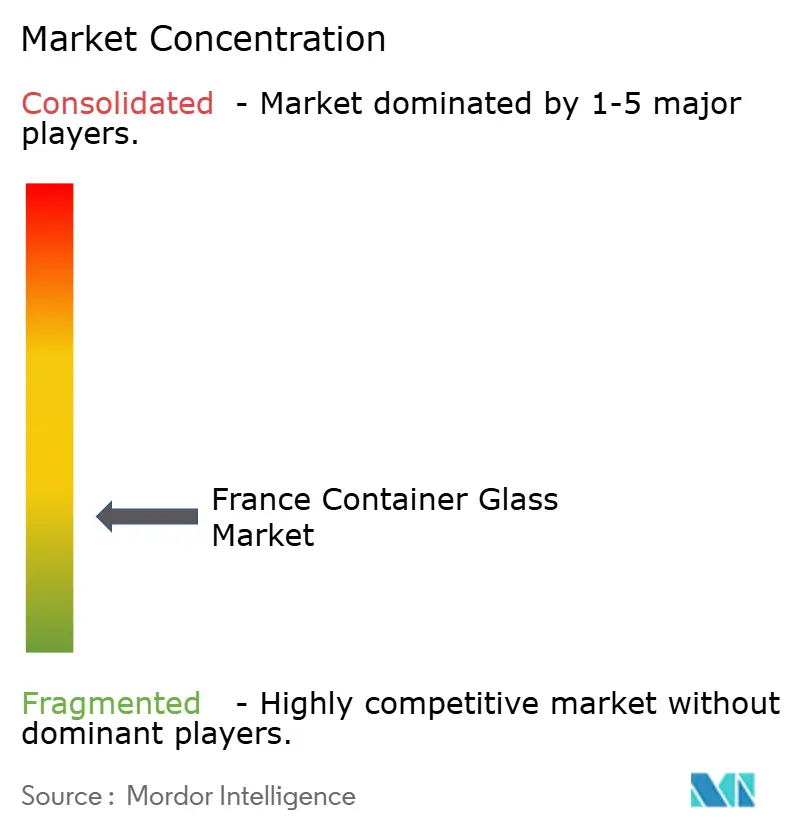

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Container Glass Market Analysis by Mordor Intelligence

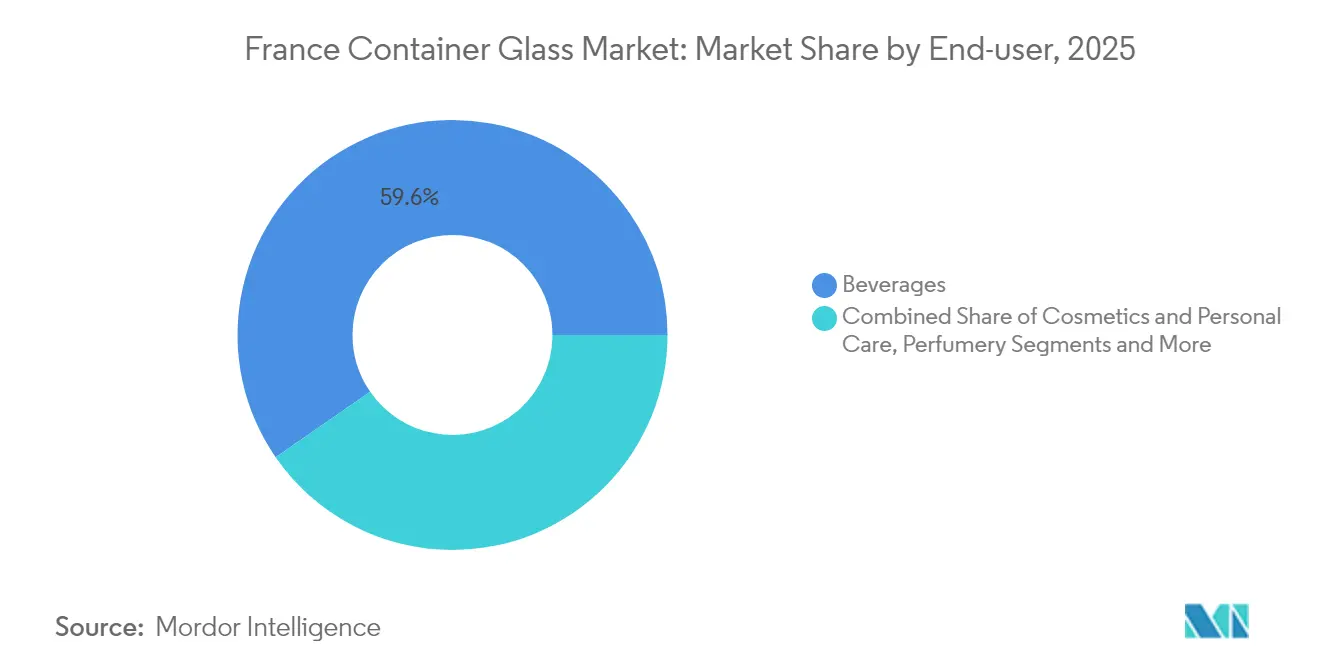

The France Container Glass Market size was valued at 6 million tonnes in 2025 and estimated to grow from 6.13 million tonnes in 2026 to reach 6.84 million tonnes by 2031, at a CAGR of 2.21% during the forecast period (2026-2031). Steady growth reflects a mature yet resilient ecosystem anchored in premium alcoholic beverages, luxury cosmetics, and high-end food segments. Deposit-return legislation that came into force in June 2025, with EUR 0.20-0.30 (USD 0.23-0.34) deposits per container, is improving reverse-logistics economics and raising effective recycling rates. Meanwhile, France’s EUR 5.6 billion (USD 6.33 billion) industrial-decarbonization program is accelerating furnace-electrification and hybrid-fuel trials that promise lower CO₂ intensity but require sizable capital commitments. Demand remains concentrated in beverages, which represented 60.28% of 2024 shipments, yet the cosmetics and personal-care channel is expanding at a faster 2.83% CAGR, propelled by glass’s perceived luxury cues and regulatory pressure against certain plastics. Competitive positioning increasingly revolves around furnace-retrofit investments, as evidenced by Verallia’s fully electric furnace in Cognac and O-I’s USD 65 million hybrid project in central France.[1]Greg Morris, “Verallia: No further furnace shutdowns planned,” Glass International, glass-international.com

Key Report Takeaways

- By end-user, beverages captured 59.62% of the France container glass market share in 2025.

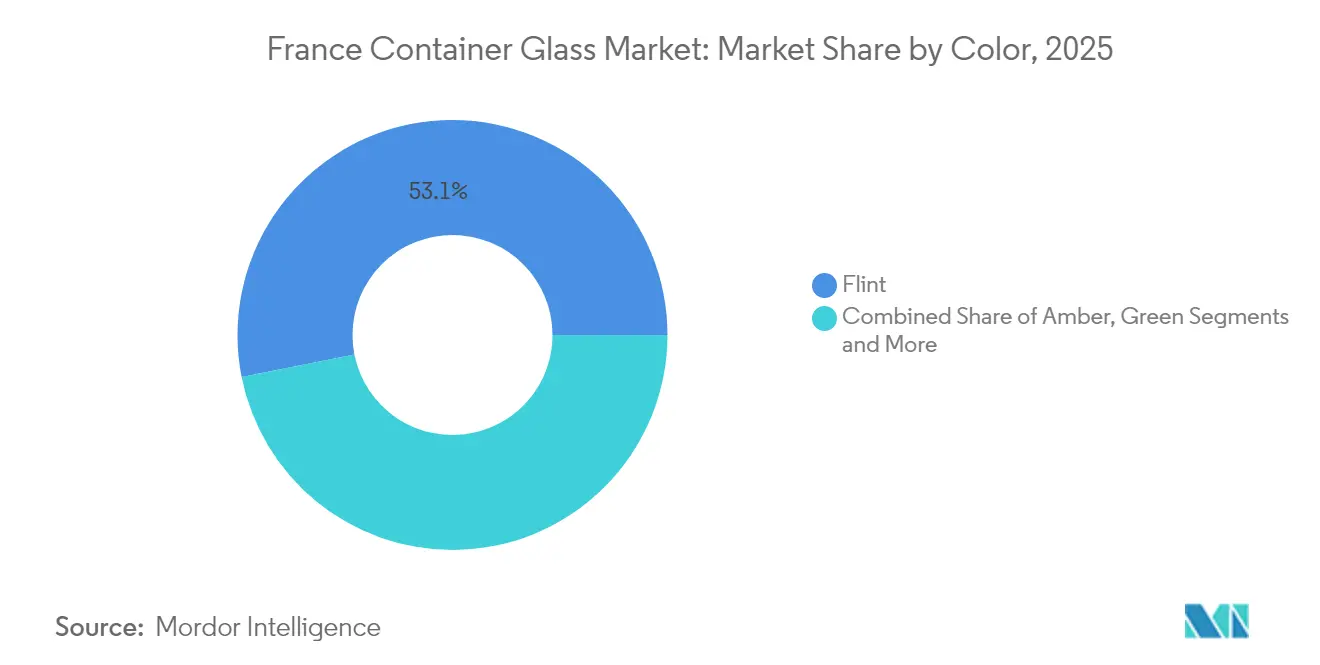

- By color, the France container glass market size for amber glass is projected to grow at a 2.74% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in premium alcoholic beverages | +0.8% | Champagne, Cognac, export hubs | Long term (≥ 4 years) |

| Expansion of cosmetics and luxury perfumes | +0.5% | Île-de-France, PACA, EU exports | Medium term (2–4 years) |

| Consumer preference for non-toxic packaging | +0.4% | Nationwide, EU | Medium term (2–4 years) |

| Technological advances in lightweight glass | +0.3% | Nouvelle-Aquitaine, Grand Est | Long term (≥ 4 years) |

| Rise in eco-conscious consumer behavior | +0.3% | National, EU | Long term (≥ 4 years) |

| Export demand for French packaged goods | +0.2% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Growth in Premium Alcoholic Beverages

Champagne and cognac houses continue to specify thick-wall flint and specialty amber flasks to reinforce brand heritage, making glass effectively non-substitutable despite price sensitivity in other beverage niches. Wine export earnings rose to EUR 9.58 billion (USD 10.83 billion) in 2024, even as volumes plateaued, illustrating value migration to premium SKUs where elaborate punted bottles and embossing justify higher unit economics. Diageo’s stated goal of seizing 12% of French spirits sales by 2030 underscores external appetite for high-margin formats anchored in glass. Protected-designation rules under AOC further cement glass’s role in authenticity verification, locking in structural demand.

Expansion of Cosmetics and Luxury Perfumes Sector

Luxury perfume houses in Grasse and Paris favor intricately molded flacons with metallized necks and acid-etched logos that only container glass can deliver at scale. The segment is growing at 2.83% CAGR through 2030, outpacing the broader France container glass market, helped by regulatory curbs on certain plastic components and consumer pursuit of recyclable prestige packaging. SGD Pharma invested EUR 31 million (USD 35 million) in 2024 to modernize two domestic furnaces geared toward cosmetic formats, signaling entrenched demand. Internal siliconization treatments such as SEALIAN mitigate interaction with volatile fragrance bases while enabling further lightweighting.

Consumer Preference for Non-Toxic Packaging

Post-COVID surveys by French retailers show willingness to pay premiums of up to 6% for food packaged in inert materials, elevating glass’s appeal for preserves and gourmet condiments. FEVE’s June 2025 response to microplastics research re-emphasized glass’s chemical stability, driving private-label conversions in dairy and non-alcoholic beverages. The nascent deposit-return scheme is accelerating circular-economy messaging, giving retailers additional marketing leverage.

Technological Advancements in Lightweight Glass Manufacturing

Verallia’s all-electric Cognac furnace and O-I’s 70% electric hybrid installation cut thermal energy needs by at least 25%, enabling wall-thickness reductions that drop bottle mass from 400 g to 300 g without compromising strength. Ardagh’s finite-element modeling shifts glass distribution toward the heel and shoulder, letting wine bottles shed 40 g and still pass ASTM impact tests. Lower freight weight plus higher cullet ratios, Saverglass hit 73.3% cullet in 2024, offsetting rising electricity tariffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy consumption in glass production | –0.6% | Nationwide plants, EU ETS zone | Short term (≤ 2 years) |

| Competition from lightweight alternatives | –0.4% | Domestic and export markets | Medium term (2–4 years) |

| Fragility and higher transport costs | –0.3% | Export corridors | Long term (≥ 4 years) |

| Volatility in raw material prices | –0.2% | Global sand and soda ash supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Consumption in Glass Production

Melting temperatures of 1,600°C keep energy intensity elevated, amplifying exposure to electricity prices that nearly doubled for French industry in 2024. Phase IV of the EU ETS slices free allocations, lifting carbon compliance costs by EUR 80–90 (USD 90–102) per ton of CO₂ emitted for a standard end-fired furnace. Verallia’s 8.7% revenue drop in 2024 shows immediate margin erosion when price hikes cannot fully cover energy surcharges.[2]Verallia, “Verallia URD 2023,” verallia.com

Competition from Lightweight Alternatives

PET bottles weigh 85% less than equivalent glass units and enjoy mature recycling pathways, especially in still-water and carbonated-soft-drink categories. Aluminum cans deliver rapid line-change flexibility and are gaining shelf appeal among craft beverages, eating into commodity beer bottle demand. Smart labels embedded in plastics add digital-engagement features that are costlier to incorporate in glass, raising switching temptations for marketing teams. Regulation curbing single-use plastics nonetheless tempers the threat in premium SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user: Beverages Dominate Despite Premiumization Pressures

The beverages channel generated 59.62% of 2025 shipments, equal to 3,577.2 kilotons of the France container glass market size. Growth in Champagne, cognac, and premium still wines secures baseline volume even as lighter PET erodes entry-level cider and juice bottles. Premium alcoholic labels retain glass for superior oxygen ingress protection and tactile cues that rationalize higher shelf prices. Domestic microbreweries lean into embossed, returnable glass to emphasize craft provenance, slightly offsetting aluminum’s surge among mass-market lagers.

Food, cosmetics, and pharmaceuticals collectively account for the remaining 40.38% of France's container glass market volume, yet cosmetics and personal care are expanding at a 2.69% CAGR on strong luxury exports.Cartier, Dior, and Hermès launch limited-edition scents in sculptural flacons, stimulating demand for specialty furnaces with color-changing forehearths. Pharmaceutical firms adhere to type-I borosilicate vials for biologics, reinforcing baseline throughput during beverage cyclicality.

By Color: Amber Glass Accelerates Through Premium Applications

Clear flint retained 53.12% of 2025 output thanks to its versatility across wine, food, and cosmetics. Growth expectations remain moderate at 2.02% through 2031 amid trade-down trends in value wine tiers. The France container glass market share of amber glass is forecast to reach 29.65% by 2031, up from 27.25% in 2025, buoyed by UV-sensitive pharmaceuticals and dark rum presentations.

Saverglass’s 73.3% cullet incorporation in colored lines lowers energy intensity by 3-4%, letting amber compete more effectively on cost per unit. Specialty hues such as cobalt and antique green occupy niche volumes under 4% but command margins exceeding 20%, appealing to craft gin and apéritif brands seeking shelf differentiation. O-I’s modular forehearths allow rapid switchover among tints, aligning capacity with promotional runs and seasonal limited editions.

Geography Analysis

France’s 11 operating container-glass furnaces are concentrated in Nouvelle-Aquitaine, Hauts-de-France, and Grand Est, giving manufacturers proximity to sand quarries and premium beverage clients. The Champagne and Cognac corridors together represented 38% of national off-take in 2025, reflecting entrenched luxury-beverage clusters. Those districts are predicted to log a 2.07% CAGR, consistent with premium wine growth trajectories and AOC production quotas.

Hauts-de-France houses France’s largest cullet-processing center, enabling flint producers to average 60% recycled content and sidestep higher soda-ash prices. The region is forecast to expand at a 2.45% CAGR between 2026 and 2031, topping the national mean, supported by government grants targeting industrial decarbonization projects.

Export dynamics further elevate domestic throughput. In 2024, container-glass exports worth EUR 189.8 million (USD 214.5 million) moved to the UK, confirming France’s hub role for high-end packaging across Northern Europe. Access to low-carbon nuclear and renewable power gives French plants an emission-factor advantage versus German peers relying heavily on gas, a differentiator as Scope 3 reporting gains traction among multinational beverage brands.

Competitive Landscape

Competitive intensity is moderate, with the top five suppliers accounting for roughly 80% of domestic capacity. Verallia dominates premium spirits bottles through embedded client relationships in Cognac and Epernay, while O-I specializes in hybrid furnaces serving beer, food, and soft drinks. Saverglass emphasizes ultra-premium short-run designs, leveraging multi-color forehearths and micro-embossing to command higher ASPs.

Strategic investments focus on decarbonization and lightweighting. Verallia is allocating EUR 420 million (USD 474 million) through 2028 for electrified and hydrogen-ready melters, aiming for a 46% CO₂ cut versus the 2019 baseline. O-I completed a 100% biofuel trial at its Harlow facility that slashed Scope 1 emissions by 90%, signaling potential replication in French furnaces contingent on feedstock supply. Saverglass works with Fives Group on next-generation electric forehearths, a partnership that could reduce changeover downtime by 30%.

M&A is reshaping capacity distribution. Verallia’s EUR 230 million (USD 259 million) acquisition of Vidrala’s Italian plants bolsters Southern European coverage, reinforcing economies of scale in cullet sourcing. BWGI’s August 2025 buy-out of 77.05% of Verallia stock layers financial heft behind long-range capex ambitions. Emerging disruptors such as Q-Tech are piloting additive-manufactured molds that cut tooling lead times by 40%, but remain outside top-tier share rankings for now.

France Container Glass Industry Leaders

O-I Glass, Inc.

Verallia Packaging

Gerresheimer AG

SGD S.A.

Stoelzle Glass Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BWGI completed a voluntary tender offer for Verallia shares, securing 77.05% of capital and 69.15% of voting rights.

- July 2025: Verallia reported a 2.5% revenue decline in Q2 2025 but reiterated full-year guidance.

- March 2025: O-I Glass completed a 100% biofuel trial at Harlow, producing amber bottles with 88% cullet.

- March 2025: Verallia advanced hydrogen-powered melting trials at Essen-Karnap.

- January 2025: SGD Pharma unveiled its SEALIAN siliconization platform at Pharmapack Europe 2025.

France Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

France container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the projected volume for France’s container glass sector by 2031?

Output is expected to reach 6.84 million Tonnes by 2031, reflecting a 2.21% CAGR from 2026 (2026-2031).

How does the new French deposit-return scheme influence glass demand?

Deposits of EUR 0.20-0.30 (USD 0.23-0.34) incentivize returns, lift cullet availability, and reinforce glass’s circular-economy credentials.

Which end-use category is expanding fastest?

Cosmetics and personal care shipments are growing at 2.69% CAGR through 2031 on luxury export momentum.

Why is amber glass gaining share?

Its UV-blocking properties suit pharmaceuticals and premium spirits, driving a 2.74% CAGR that outpaces clear and green variants.

What decarbonization technologies are French plants adopting?

Manufacturers are trialing all-electric furnaces, hybrid biofuel melters, and hydrogen-assisted combustion to lower Scope 1 emissions by up to 90%.

How concentrated is supplier power in France’s container glass arena?

The top five companies command about 80% of capacity, yielding a moderate-to-high concentration score of 3.

Page last updated on: