Food Texturizers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 16.97 Billion |

| Market Size (2031) | USD 22.01 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

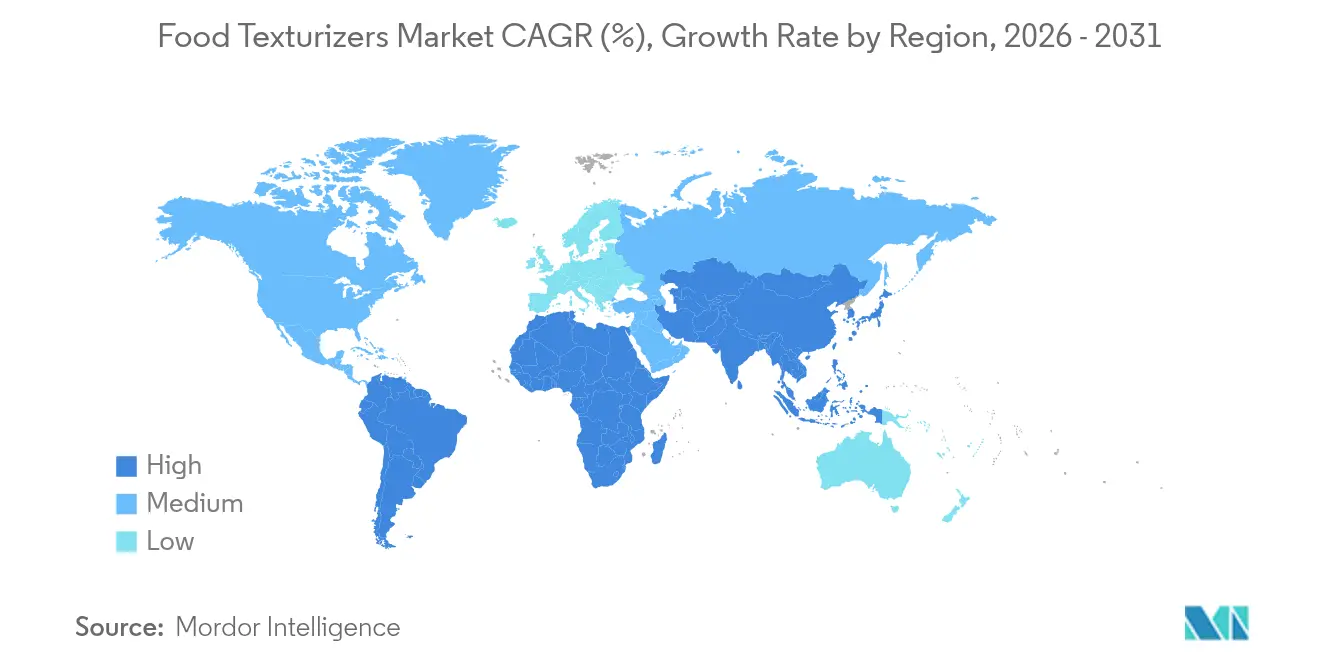

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

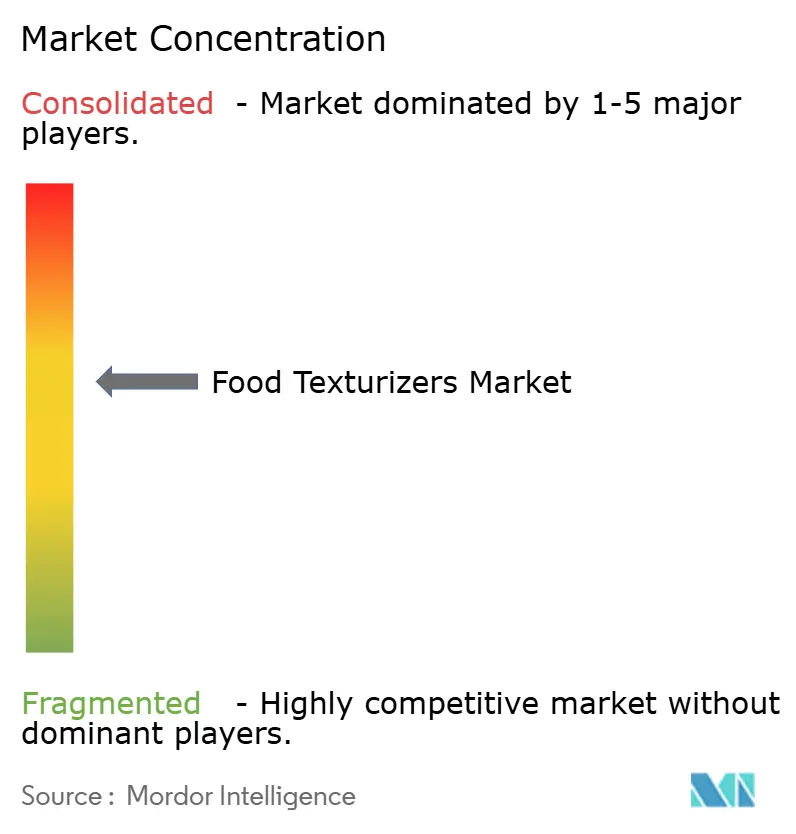

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Food Texturizers Market Analysis by Mordor Intelligence

The food texturizers market size in 2026 is estimated at USD 16.97 billion, growing from 2025 value of USD 16.11 billion with 2031 projections showing USD 22.01 billion, growing at 5.34% CAGR over 2026-2031. The market's growth is primarily driven by the industrial expansion of plant-based proteins, which require advanced hydrocolloids, along with regulatory support for clean-label declarations. Additionally, the increasing demand for premium packaged foods with enhanced texture is contributing to the market's upward trajectory. Cellulose derivatives continue to play a crucial role in maintaining stability in gluten-free bakery and dairy products, while inulin is gaining popularity due to its dual functionality as a prebiotic fiber and texture enhancer. Natural-source ingredients are witnessing higher demand as consumers increasingly avoid chemically modified additives, reflecting a shift in consumer preferences toward more natural options. North America remains the leading region in terms of revenue generation, while the Asia-Pacific region is emerging as a key driver of global growth. This expansion is supported by rising disposable incomes and the growing adoption of Western dietary habits in the region. Ingredient suppliers are moving away from commodity-based sales and focusing on research and development (R&D) collaborations. These partnerships aim to develop proprietary gum and starch systems, helping suppliers strengthen customer relationships and maintain profit margins.

Key Report Takeaways

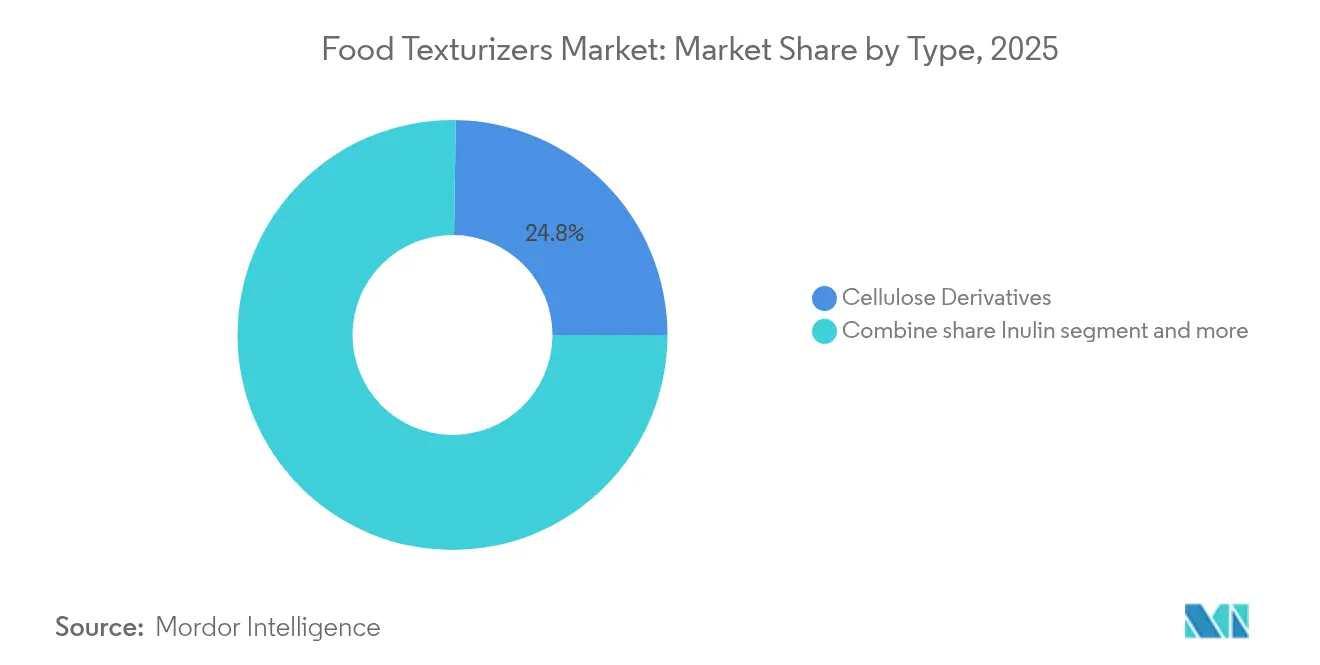

- By type, cellulose derivatives led with 24.76% of Food texturizers market share in 2025, while inulin is forecast to grow at a 6.46% CAGR through 2031.

- By source, natural texturizers accounted for 60.98% revenue in 2025; synthetic variants trail, but natural systems are projected to expand at a 6.55% CAGR to 2031.

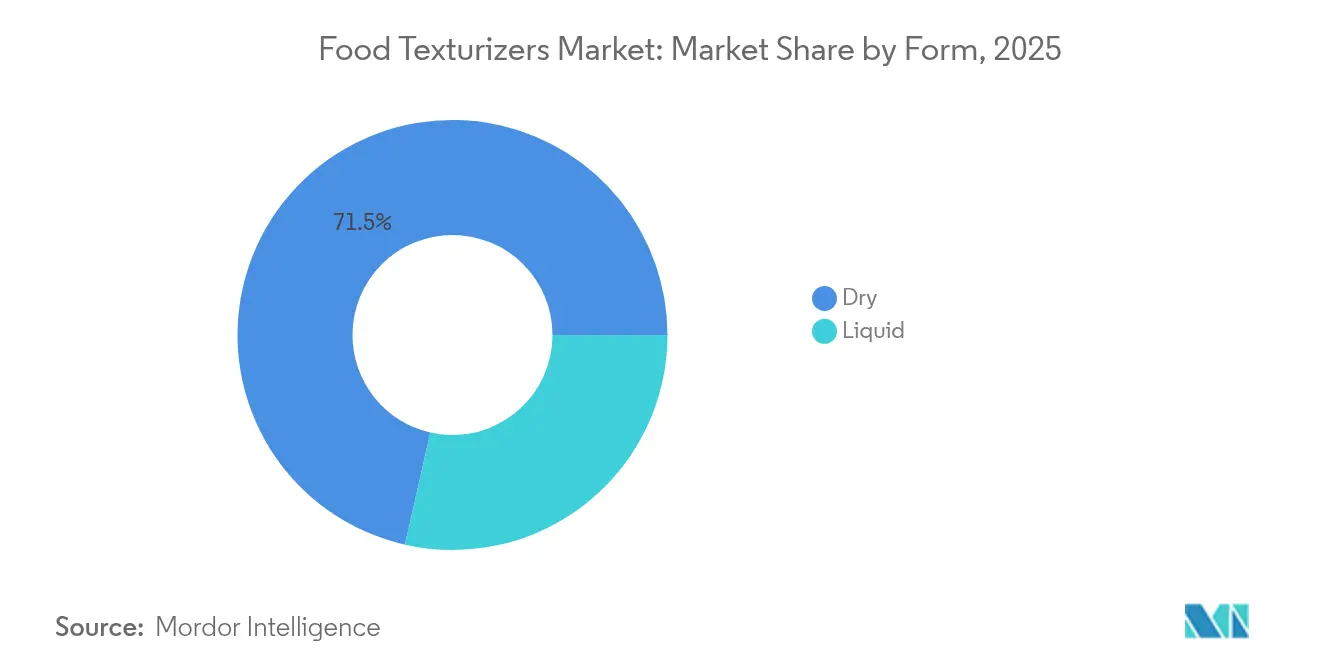

- By form, dry products captured 71.45% volume in 2025; liquid formulations represent the fastest track, advancing at a 6.52% CAGR to 2031.

- By geography, North America held 29.08% of global revenue in 2025, whereas Asia-Pacific is poised for a 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Texturizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for processed foods requiring stabilizers and hydrocolloids for texture and shelf life | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Plant-based and vegan products need advanced texturizers to replicate animal-product textures | +1.5% | North America, Europe, Asia-Pacific urban centers | Medium term (2-4 years) |

| Clean-label trends drive use of minimally processed texturizers like gums, pectins, and starches | +1.3% | Global, led by North America and Western Europe | Long term (≥ 4 years) |

| Technological advancements enhance hydrocolloids and starches for stability under various conditions | +0.9% | Global, with Research and Development hubs in North America and Europe | Long term (≥ 4 years) |

| Premium products emphasize unique textures as a key value proposition | +0.7% | North America, Europe, affluent Asia-Pacific markets | Short term (≤ 2 years) |

| Functional foods and beverages use texturizers to mask off-notes from added nutrients | +0.8% | Global, with early adoption in North America and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High demand for processed foods requiring stabilizers and hydrocolloids for texture and shelf life

Processed food consumption continues to climb in urbanizing economies where dual-income households prioritize convenience, yet the texture stability that consumers expect across temperature fluctuations and extended shelf life depends on hydrocolloid networks that prevent syneresis in refrigerated sauces and retard staling in baked goods. Xanthan gum and carboxymethyl cellulose have become standard in salad dressings and ice cream because they maintain viscosity under shear stress during pumping and filling operations, a technical requirement that commodity starches cannot meet without chemical modification. The United States Department of Agriculture reported that per-capita consumption of ready-to-eat meals rose 8% between 2019 and 2024, a trend that correlates with increased hydrocolloid tonnage in industrial kitchen This demand is not merely about preservation; it reflects a shift toward engineered eating experiences where texture cues signal freshness and quality, even in products with 90-day ambient shelf life. The economic implication is that texturizer spend per finished-goods ton is rising faster than ingredient inflation, as brands compete on sensory differentiation rather than price alone.

Plant-based and vegan products need advanced texturizers to replicate animal-product textures

Plant-based meat and dairy alternatives face a structural challenge as legume and grain proteins lack the fibrous structure of muscle tissue and the emulsifying properties of casein, resulting in a texture gap. Methylcellulose and konjac glucomannan are uniquely positioned to address this issue. Methylcellulose demonstrates reverse thermal gelation, forming a gel network above 50 degrees Celsius that replicates the binding and juiciness of animal fat during cooking. This property has been utilized by companies such as Impossible Foods and Beyond Meat in their flagship burger formulations. DuPont reported in its 2024 annual report that sales of its Ticaloid texturizer blends for plant-based applications increased by 22% year-over-year, indicating the category's progression from niche to mainstream. The challenge is not limited to meat alternatives. Plant-based cheese formulations require a combination of tapioca starch, carrageenan, and nutritional yeast to replicate the stretch and melt characteristics of mozzarella. However, consumer acceptance depends on addressing the "gummy" mouthfeel caused by excessive hydrocolloid use. To overcome this, formulators are now micro-dosing multiple texturizers, typically using three to five in a single product, to achieve the desired balance of firmness, cohesiveness, and melt. While this approach increases formulation costs, it also creates switching barriers once a recipe is optimized.

Clean-label trends drive use of minimally processed texturizers like gums, pectins, and starches

Consumer skepticism toward synthetic additives has reduced the range of acceptable ingredients, prompting manufacturers to focus on options like gums, pectins, and native starches that can be labeled as "fruit pectin" or "tapioca starch" instead of E-numbers or chemical names. The European Food Safety Authority's (EFSA) 2024 re-evaluation of titanium dioxide, which resulted in its ban across the European Union, has increased scrutiny of functional additives [1]Source: European Food Safety Authority, “Genetically Modified Organisms,” efsa.europa.eu. This has encouraged brands to reformulate products using recognizable plant extracts, even when such changes involve performance compromises. Pectin derived from citrus peel or apple pomace offers strong clean-label appeal. However, its calcium-dependent gelation mechanism limits its use in low-pH beverages, creating demand for enzymatically modified pectins that can gel without requiring divalent cations while still being labeled as "pectin." Ingredion, during its Q3 2024 earnings call, highlighted the growth of its clean-label starch portfolio, which includes physically modified starches that avoid chemical cross-linking.

Technological advancements enhance hydrocolloids and starches for stability under various conditions

Hydrocolloid functionality has traditionally been limited by sensitivity to extreme pH levels, high salt concentrations, and freeze-thaw cycles. However, advancements in enzyme engineering and controlled depolymerization are driving the development of next-generation texturizers with broader processing capabilities. In 2024, CP Kelco introduced a gellan gum variant that remains stable in acidic protein beverages at a pH of 3.5. This innovation eliminates the need for high-methoxyl pectin, simplifying formulation processes. Modified starches produced through extrusion or heat-moisture treatment exhibit shear-thinning behavior, which enhances pumpability in high-solids sauces while maintaining adhesion on vertical surfaces. These characteristics are critical for applications such as ketchup and barbecue sauces. Cargill, in its 2024 sustainability report, highlighted that its enzymatically debranched waxy maize starch reduces retrogradation in refrigerated doughs by 40% compared to native starch. This improvement extends product shelf life without requiring additional preservatives. The competitive advantage in the market now lies in application-specific customization. For example, a texturizer designed for plant-based yogurt must tolerate high-temperature short-time (HTST) pasteurization, resist syneresis during cold storage, and provide a clean flavor profile that does not overshadow fruit inclusions. Achieving this level of customization requires pilot-plant trials and sensory validation, offering a competitive edge to suppliers with strong technical service teams and regional application centers.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer skepticism toward synthetic or unfamiliar food additives | -0.8% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Increasing regulatory scrutiny and complex labeling requirements | -0.6% | Global, with stringent enforcement in Europe and North America | Long term (≥ 4 years) |

| Rising concerns regarding the potential health effects of certain emulsifiers | -0.7% | Europe and North America, emerging in Asia-Pacific | Medium term (2-4 years) |

| Fluctuating availability and quality of natural raw materials | -0.5% | Global, with acute impact in Asia-Pacific and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer skepticism toward synthetic or unfamiliar food additives

Ingredient transparency has shifted from being a niche preference to a common consumer expectation. Consumers are increasingly avoiding products with additives they cannot recognize or pronounce, which has significantly impacted synthetic texturizers such as sodium stearoyl lactylate and polysorbate 80. A 2024 survey conducted by the International Food Information Council (IFIC) revealed that 67% of United States consumers actively avoid foods with "chemical-sounding" ingredients, up from 52% in 2020. This skepticism also extends to naturally derived but less familiar hydrocolloids like gellan gum and konjac glucomannan [2]Source: International Food Information Council, “IFIC Spotlight Survey: From “Chemical-sounding” To “Clean”: Consumer Perspectives On Food Ingredients,” ific.org. In response, brands are reformulating products using familiar "kitchen-cupboard" ingredients such as cornstarch, gelatin, and pectin. However, these substitutions often lead to compromises, including shorter shelf life or changes in texture, as part of efforts to maintain clean-label positioning. A significant challenge arises from the inability of simple starches to achieve the desired texture in many plant-based and functional applications. For example, methylcellulose, known for its unique thermal gelation properties, remains essential for plant-based meat products. However, its E-number designation (E461) creates negative consumer perceptions, particularly in Europe. This situation is driving regional variations in formulations. For instance, a product sold in Germany may use citrus fiber and native potato starch, while the same product in the United States may include modified food starch and carrageenan. These regional differences add complexity and increase supply chain costs.

Increasing regulatory scrutiny and complex labeling requirements

Regulatory frameworks for food additives are becoming stricter worldwide, with authorities requiring more detailed safety documentation, allergen disclosures, and origin traceability. These requirements place a significant burden on smaller texturizer suppliers and delay the approval of new products. The European Union's Farm to Fork strategy mandates complete supply-chain traceability for all food ingredients by 2027. This compels hydrocolloid suppliers to document the geographic origin of seaweed used for carrageenan or the microbial strain involved in xanthan gum fermentation. In the United States, the Food and Drug Administration's (FDA) 2024 guidance on "natural" claims prohibits the use of the term for any ingredient subjected to chemical modification. This effectively excludes modified starches and chemically cross-linked celluloses from being marketed as clean-label ingredients [3]Source: U.S. Food & Drug Administration, “Guidance for Industry: Nutrition and Supplement Facts Labels Questions and Answers Related to the Compliance Date, Added Sugars, and Declaration of Quantitative Amounts of Vitamins and Minerals,” fda.gov. These evolving standards create compliance challenges that favor multinational suppliers with dedicated regulatory affairs teams. For example, Ingredion and Cargill maintain regulatory dossiers for over 200 texturizer variants across 50 jurisdictions, a capability that regional processors often cannot match. Consequently, the increasing complexity of regulatory requirements is consolidating the supplier base, as food manufacturers prefer to work with vendors who can ensure global regulatory compliance rather than managing multiple regional suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cellulose Derivatives Lead, Inulin Surges on Prebiotic Appeal

Cellulose derivatives accounted for 24.76% of the market share in 2025, driven by their essential role in gluten-free baking. Hydroxypropyl methylcellulose (HPMC), in particular, provides dough extensibility and crumb structure that native starches cannot replicate. Inulin is projected to grow at an annual rate of 6.46% through 2031, marking the fastest growth among all texturizer types. This growth is attributed to its dual functionality as a prebiotic fiber and fat replacer in reduced-calorie formulations.

Gums and pectins continue to play a significant role in dairy and beverage applications. For instance, xanthan gum's pseudoplastic rheology enables the production of pourable salad dressings that adhere to salad greens, enhancing consumer satisfaction and driving repeat purchases. Gelatins are facing challenges due to the increasing popularity of plant-based diets. Agar and pectin are gradually replacing porcine and bovine gelatin in confectionery jellies, although the texture remains imperfect, with agar producing a firmer and more brittle bite. Starch and its derivatives dominate cost-sensitive applications such as gravies, soups, and pie fillings. Modified waxy maize starch, for example, delivers viscosity at one-third the cost of hydrocolloids. However, clean-label trends are shifting demand toward physically modified or native starches, which offer reduced freeze-thaw stability.

By Source: Natural Texturizers Capture Value, Synthetic Faces Margin Pressure

Natural-source texturizers accounted for 60.98% of the market share in 2025 and are expected to grow at a rate of 6.55% through 2031. This growth is driven by clean-label requirements and increasing consumer concerns about chemically modified ingredients, which are reshaping procurement strategies. The performance gap between natural and synthetic texturizers is narrowing. For instance, enzymatically modified pectins now offer cold-water solubility comparable to synthetic cellulose ethers, while fermentation-derived xanthan gum provides viscosity stability across varying pH and temperature ranges, matching the performance of chemically cross-linked starches.

Synthetic texturizers, such as sodium carboxymethyl cellulose (CMC) and hydroxypropyl distarch phosphate, continue to maintain cost advantages, typically being 20% to 30% less expensive per functional unit. These synthetic options remain widely used in industrial bakery and processed meat applications, where ingredient labeling is subject to less scrutiny. However, the pricing structure is diverging. Natural texturizers command price premiums of 15% to 25% but face higher raw material price volatility. In contrast, synthetic alternatives compete on volume in commoditized segments, where margins are increasingly compressed.

By Form: Dry Dominates Logistics, Liquid Gains in Beverage Applications

In 2025, dry-form texturizers held a 71.45% market share. This dominance is attributed to their logistical benefits, including ease of bulk handling, extended shelf life without refrigeration, and suitability for precise dosing in automated manufacturing processes. These features make dry-form texturizers a preferred choice for many manufacturers seeking efficiency and cost-effectiveness in their operations.

On the other hand, liquid formulations are expected to grow at an annual rate of 6.52% through 2031. This growth is driven by beverage and sauce manufacturers who prioritize rapid dispersion and uniformity over storage convenience. The technical differences between the two are notable. For instance, dry xanthan gum requires high-shear mixing to fully hydrate and prevent the formation of "fish eyes." In contrast, liquid concentrates disperse instantly, reducing batch preparation time and energy usage in high-throughput production. Additionally, liquid texturizers enable micro-dosing in low-viscosity applications, such as sports drinks and flavored waters, where powder forms may lead to clumping and uneven distribution.

Geography Analysis

North America emerged as the leading segment in 2025, capturing 29.08% of the global market share. This dominance is attributed to the region's highest per-capita consumption of processed and convenience foods, where texturizers are integral across various categories, including frozen dinners and shelf-stable sauces. The region benefits from well-established supply chains, stringent oversight by the Food and Drug Administration (FDA), which favors suppliers with comprehensive safety documentation, and a consumer base willing to pay premium prices for clean-label formulations. These formulations often incorporate recognizable ingredients such as gums and starches. Furthermore, the United States Department of Agriculture's (USDA) 2024 dietary guidelines, which emphasize increased fiber intake, have indirectly driven demand for inulin and resistant starches. These ingredients not only provide prebiotic benefits but also enhance textural functionality in food products.

The Asia-Pacific region is projected to be the fastest-growing segment, with an anticipated compound annual growth rate (CAGR) of 6.18% through 2031. This growth is primarily driven by rising disposable incomes in countries such as China and India, which are influencing dietary shifts toward processed foods, plant-based proteins, and premium dairy products. In China, the plant-based meat market heavily depends on texturizers to replicate the fibrous texture of traditional meats like pork and chicken. Ingredients such as methylcellulose and konjac glucomannan have become standard in popular food items, including dumplings and buns, as they help achieve the desired texture and quality.

In Europe, the market dynamics are shaped by the European Food Safety Authority's (EFSA) rigorous re-evaluation processes, which mandate periodic safety reviews for all food additives. Additionally, consumer activism has played a significant role in making clean-label positioning a competitive necessity rather than a mere differentiation strategy. The European Union's (EU) ban on titanium dioxide in 2024 has further intensified scrutiny of functional additives. This regulatory change has prompted brands to reformulate their products using botanical extracts and native starches, even when such adjustments involve trade-offs in performance. These developments reflect the region's commitment to safety and transparency in food production.

Competitive Landscape

The food texturizers market is moderately consolidated, with 5 to 7 multinational ingredient conglomerates accounting for a significant share of global revenue. These companies leverage diversified portfolios, vertical integration into raw material sourcing, and extensive regulatory expertise, creating high barriers to entry. Key players such as Archer Daniels Midland, Cargill, DuPont, Ingredion, and Kerry Group dominate through advantages in procurement, application development, and global reach. At the same time, regional specialists like CP Kelco in hydrocolloids and Roquette in starches focus on niche expertise and close customer relationships to capture premium market segments.

The market is shifting from commodity supply to co-development partnerships. Texturizer suppliers are increasingly embedding technical service teams within customer research and development (R&D) facilities to collaboratively optimize formulations. This approach fosters customer loyalty by creating switching costs and ensuring long-term revenue stability. Additionally, opportunities are emerging in fermentation-derived texturizers, such as precision-fermented gelatin and microbial exopolysaccharides. These innovations bypass agricultural supply chains, offer clean-label credentials, and are attracting venture capital and corporate investments as companies seek to mitigate raw material volatility. Emerging disruptors include biotechnology firms utilizing synthetic biology to produce animal-free gelatin and collagen. These ingredients command price premiums of 3 to 5 times in plant-based and halal-certified applications.

Technology is also becoming a key competitive factor. For instance, Ingredion's digital viscosity-prediction tool, launched in 2024, enables customers to simulate texturizer performance virtually, reducing formulation cycle times by 30 percent and enhancing customer retention. Patent activity is concentrated in areas such as enzyme-modified hydrocolloids and encapsulation technologies that mask off-flavors in functional foods. In 2024, DuPont filed 12 patents related to texturizers, focusing on methylcellulose variants with improved thermal stability and clean-label attributes. The competitive landscape is increasingly bifurcated. Volume leaders compete on cost and reliability in commodity categories like gravies and soups, while innovation-driven suppliers achieve higher margins in segments such as plant-based meats, functional beverages, and premium dairy alternatives, where texture is a critical purchase factor.

Food Texturizers Industry Leaders

Archer Daniels Midland Co.

Cargill Inc.

DuPont de Nemours Inc.

Ingredion Inc.

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSM-Firmenich has increased its ownership in Yantai DSM Andre Pectin Company Limited from 75% to 90.5% by acquiring an additional 15.5% of shares. This move reinforces its position in the specialty food ingredient market. Andre Pectin, a prominent producer of apple and citrus pectin, retains 9.5% of its shares under the ownership of Rich Spring Holdings Limited.

- March 2025: Cargill launched a cost-effective pectin replacer intended as an alternative to the high-cost pectin used in gummies and jellies, catering to price-sensitive consumers in India. This product, presented alongside bake-stable fillings and other functional blends, underscores Cargill's focus on providing versatile, high-quality solutions for the changing needs of the food industry.

- November 2024: Tate & Lyle has completed the acquisition of CP Kelco, establishing a prominent global specialty food and beverage solutions business with expanded expertise in natural ingredients, including pectin and specialty gums.

Global Food Texturizers Market Report Scope

Food texturizing agents are food additives that are incorporated into food products to enhance both their texture and stability. Food texturizing additives can be derived from a range of sources, including seaweeds, animals, and plants.

The global food texturizer market is segmented by type, application, and geography. Based on type, the market is segmented into Cellulose derivatives, gums, pectins, gelatins, starch, inulin, dextrins, and other types. Based on application, the market is segmented into dairy products & ice creams, confectionery, jams, layers, fillings, bakery, meat products, ready meals, sauces, beverages, and others. Based on geography, the study provides an analysis of the food texturizers market in emerging and established markets across the globe, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

For each segment, the market sizing and forecast have been done based on value (USD million).

| Cellulose Derivatives |

| Gums and Pectins |

| Gelatins |

| Starch and Derivatives |

| Inulin |

| Other Types |

| Natural |

| Synthetic |

| Dry |

| Liquid |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Chile | |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Cellulose Derivatives | |

| Gums and Pectins | ||

| Gelatins | ||

| Starch and Derivatives | ||

| Inulin | ||

| Other Types | ||

| By Source | Natural | |

| Synthetic | ||

| By Form | Dry | |

| Liquid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big is the food texturizers market in 2026 and how fast is it growing?

It reached USD 16.97 billion in 2026 and is forecast to record a 5.34% CAGR through 2031.

Which product type holds the largest share of global demand?

Cellulose derivatives command 24.76% of 2025 revenue, driven by gluten-free bakery and dairy stabilization.

Which geographic region leads revenues today?

North America accounted for 29.08% of 2025 sales, reflecting high processed-food consumption and strict FDA oversight.

Where is the fastest regional growth expected?

Asia-Pacific is projected to advance at a 6.18% CAGR to 2031 on rising disposable incomes and plant-based diet adoption.

What segment is expanding quickest by form?

Liquid texturizers are set for a 6.52% CAGR, buoyed by beverage and sauce manufacturers prioritizing rapid dispersion.

Page last updated on: