Fortified Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

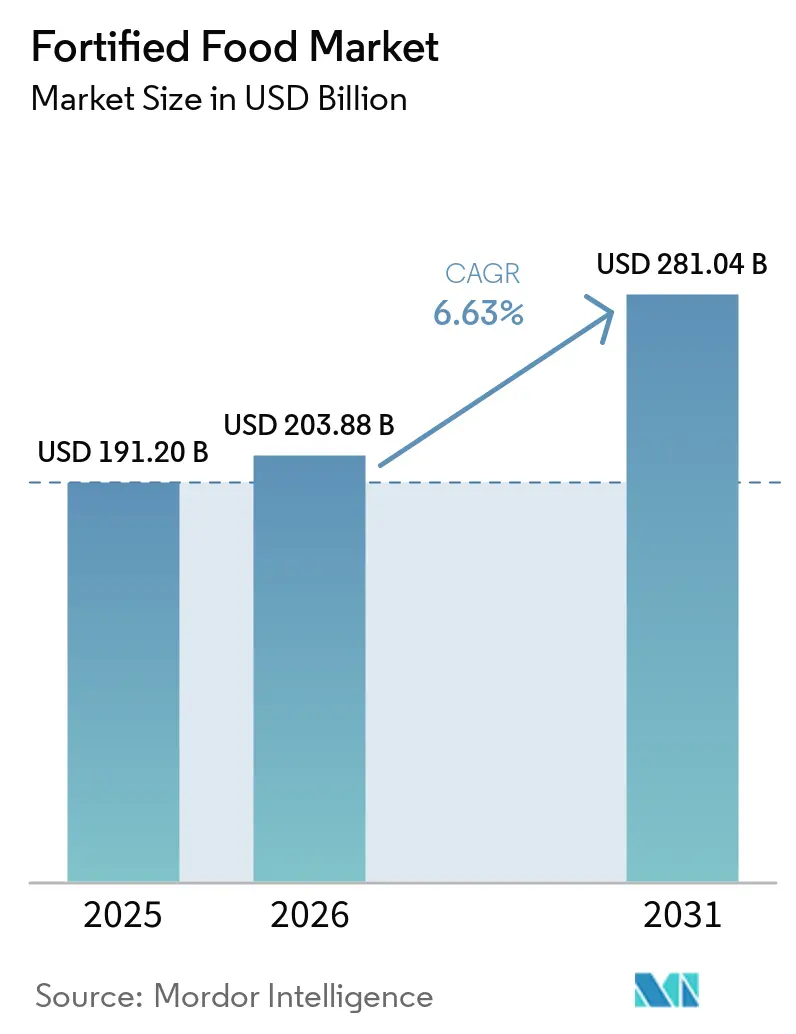

| Market Size (2026) | USD 203.88 Billion |

| Market Size (2031) | USD 281.04 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

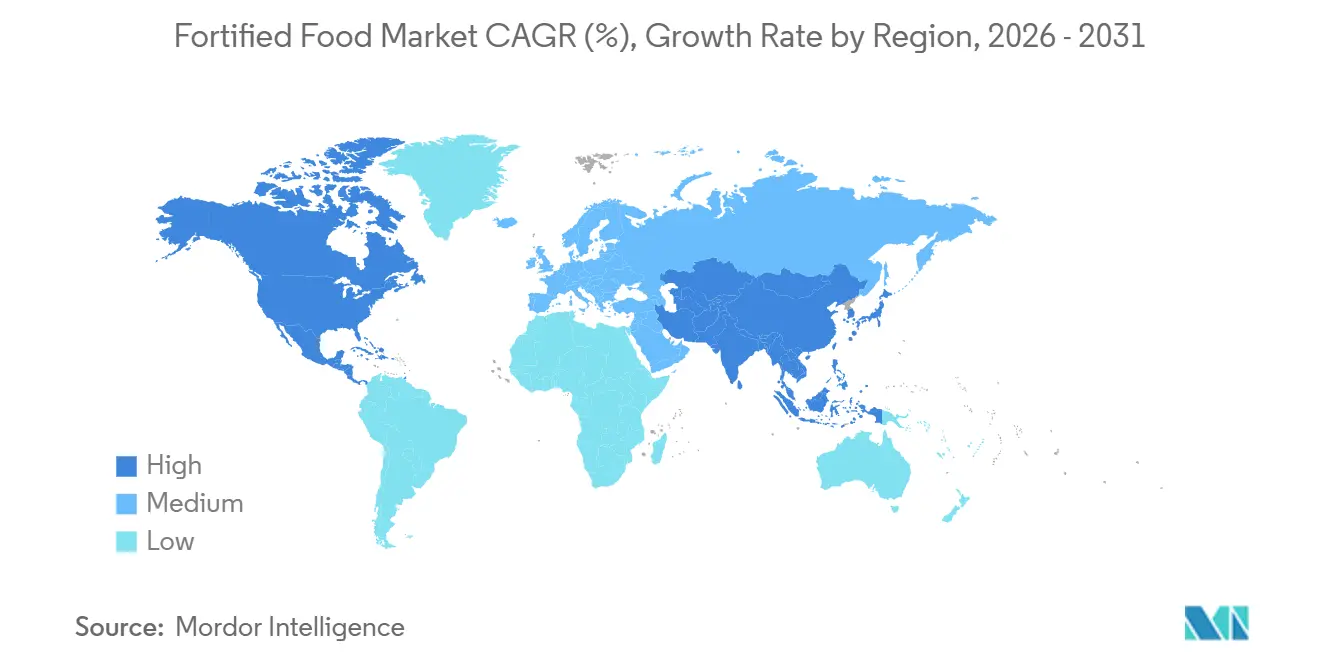

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

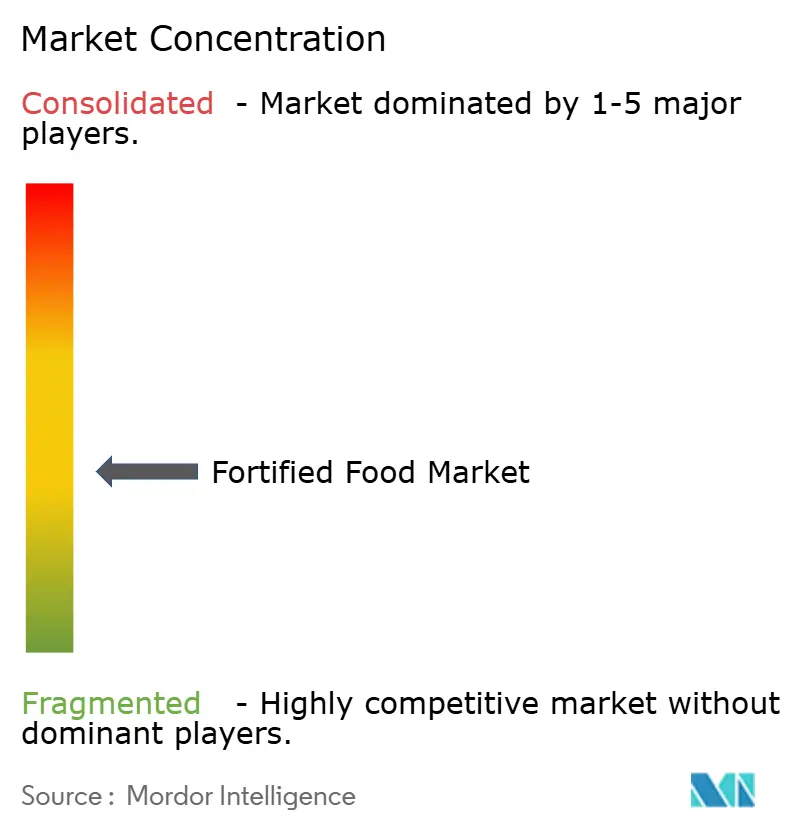

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fortified Food Market Analysis by Mordor Intelligence

The fortified food market expanded from USD 191.2 billion in 2025 to USD 203.88 billion in 2026 and is forecast to reach USD 281.04 billion by 2031, advancing at a 6.63% CAGR over 2026-2031. Governments are now mandating biofortification, especially in staple foods like wheat flour, rice, and edible oils, marking a shift from voluntary enrichment. This shift is driven by heightened public awareness of hidden micronutrient deficiencies, a trend towards premiumization in functional snacks and beverages, and technological advancements that reduce nutrient-loss costs during processing. Biofortification initiatives are increasingly being integrated into national nutrition policies, emphasizing their importance in addressing malnutrition. Additionally, partnerships between public and private sectors are fostering innovation and expanding the reach of fortified products. In the Asia-Pacific region, large-scale procurement programs in India and Indonesia are converting subsidies into fortified staples, positioning the area to outpace North America. Meanwhile, multinationals are consolidating by acquiring direct-to-consumer brands, and regional cooperatives are employing localized fortification strategies to capture a larger share of the fortified food market.

Key Report Takeaways

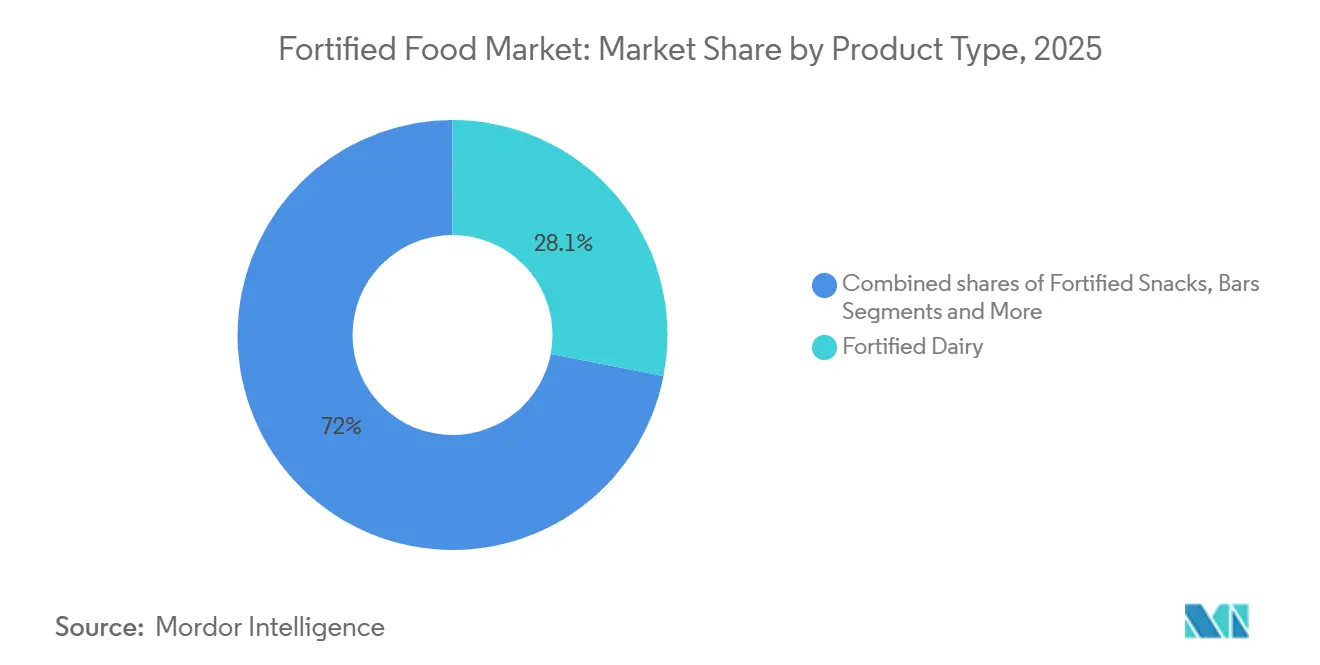

- By product type, fortified dairy led with 28.05% of the fortified food market share in 2025, while fortified snacks and ready-to-eat foods are projected to expand at an 8.11% CAGR through 2031.

- By ingredient source, plant-based inputs captured 68.32% of the fortified food market in 2025; the same segment is forecasted to grow at an 8.55% CAGR from 2026 to 2031.

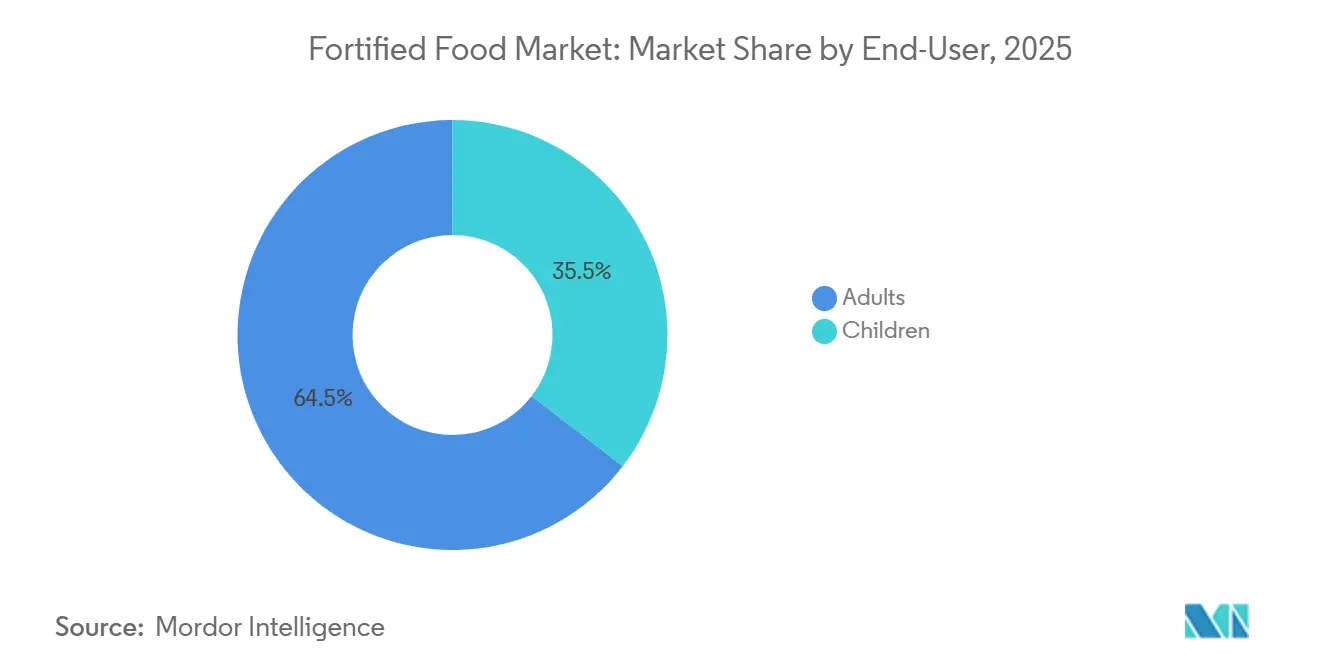

- By end-user, adults accounted for 64.54% of demand in 2025, whereas the children segment is projected to grow at an 7.48% CAGR over the forecast period.

- By distribution channel, supermarkets and hypermarkets held 47.03% share in 2025, while online retail is the fastest-growing channel is projected to grow at a 6.78% CAGR to 2031.

- By geography, North America commanded 36.92% of the fortified food market size in 2025, yet Asia-Pacific is the fastest-growing region with a 7.93% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fortified Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global health awareness | +1.2% | Global, with early gains in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Government-mandated staple fortification expands addressable volume | +1.8% | Asia-Pacific core, spill-over to Sub-Saharan Africa and Latin America | Long term (≥ 4 years) |

| Technological advances (micro- and nano-encapsulation, precision fermentation) cut nutrient-loss costs | +1.5% | Global, led by North America and Europe research and development hubs | Medium term (2-4 years) |

| Demand surge for plant-based fortified formats in flexitarian diets | +1.0% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Brand and influencer-led nutrition education | +0.8% | Global, with higher impact in digitally connected markets | Short term (≤ 2 years) |

| Premiumization in functional snacks and beverages widens margins in developed markets | +0.4% | North America and Europe, early adoption in the Gulf Cooperation Council | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global health awareness

Post-pandemic, consumers have shifted their focus from calorie counting to prioritizing micronutrient density. This shift has spurred a surge in demand for fortified foods, particularly in beverages, dairy, and snacks. In its 2025 guidelines, the World Health Organization endorsed the fortification of edible oils and fats with vitamins A and D, highlighting their importance in addressing micronutrient deficiencies and improving public health outcomes globally[2]Source: World Health Organisation, "WHO guideline on fortification of edible oils and fats with vitamins A and D for public health", who.int. This endorsement has led to a swift reformulation of both milk and plant-based drinks. Following this trend, Arla Foods introduced a vitamin D milk line, which commanded a notable 15% price premium within just a year. The fortified food market is also benefiting from increasing consumer awareness about the role of micronutrients in preventing chronic diseases. This awareness is driving innovation and investment in the development of fortified products across various categories. Additionally, with the aid of wearable trackers and smartphone-linked blood tests, consumers can now self-diagnose deficiencies, enabling them to make informed choices when selecting fortified products online. Brands, recognizing these data-driven preferences, have shortened their product development cycles to as little as nine months, allowing for rapid responses in the fortified food market.

Government-mandated staple fortification expands addressable volume

Large-scale mandates are shifting food fortification from premium niches to mass-market staples. In Egypt, fortification efforts led to the treatment of 9.2 million tons of wheat flour, ensuring that 95% of subsidized bread was covered[1]Source: World Food Programme, "The Government of Egypt revives its national flour fortification programme in collaboration with WFP to prevent the spread of iron deficiency anaemia", wfp.org. As a result, anemia rates in women dropped by 12 percentage points in just 18 months. This success highlights the effectiveness of targeted fortification programs in addressing public health challenges. It also demonstrates the potential for similar initiatives to be replicated in other regions facing nutritional deficiencies. In India, an order for edible oil, impacting 22 million tons annually, has managed to stabilize retail prices, even with the added costs of vitamins. This initiative not only ensures nutritional benefits for a large population but also demonstrates how policy interventions can balance health objectives with economic considerations. Similarly, Nigeria, Mexico, and Bangladesh have implemented rice and milk programs that, while compressing margins, have successfully boosted baseline volumes. These programs showcase the scalability of fortification efforts and their ability to address widespread nutritional gaps. These initiatives not only integrate fortification into daily diets but also support the long-term growth of the fortified food market.

Technological advances cut nutrient-loss costs

Owing to micro- and nano-encapsulation, vitamins retain over 90% potency during high-heat extrusion, transforming shelf-stable snacks into effective delivery vehicles. This technology ensures that essential nutrients remain intact even under extreme processing conditions, making it a game-changer for the functional food market. Additionally, it opens up opportunities for manufacturers to innovate with nutrient-dense snack options. Precision fermentation has slashed the costs of vitamin B12 and heme iron to under USD 50/kg, bridging the gap with animal sources and paving the way for plant-based fortification. Xampla's innovative pea-protein coating keeps vitamin D3 potent for an entire year at room temperature. This advancement addresses a critical challenge in vitamin stability, particularly for products stored in non-refrigerated environments. It also supports the growing demand for fortified foods with extended shelf lives. FrieslandCampina's ProHeat technology safeguards protein integrity in UHT milk, which is fortified with calcium and vitamin D, ensuring it competes on equal footing with regular milk in terms of repeat purchases.

Demand surge for plant-based fortified formats in flexitarian diets

Flexitarian shoppers, aiming for complete amino acid profiles, are increasingly opting for plant-based fortification, which has become a key driver of growth in the fortified food market. Pea protein, now competitively priced with whey, enables cereals like Wheaties Protein to provide 16 g of protein per serving at affordable, mainstream prices, making high-protein options more accessible to consumers. The approval of algal omega-3 has created significant opportunities in the infant formula segment, addressing the demand for plant-based alternatives in early nutrition. Danone's Actimel+ line experienced a 22% volume growth in its first year in Western Europe, reflecting strong consumer acceptance of fortified products. Furthermore, in 2024, regulatory clarity from the European Food Safety Authority encouraged major players like Nestlé and Abbott to increase their investments in plant-based pediatric nutrition, signaling a shift toward innovation in this category.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Taste and texture challenges from high-load nutrient addition | -0.7% | Global, with higher impact in fortified bakery and beverages | Short term (≤ 2 years) |

| Nutrient loss during thermal processing and long supply chains | -0.5% | Asia-Pacific and Sub-Saharan Africa, where cold-chain infrastructure is limited | Medium term (2-4 years) |

| Patchy enforcement of fortification standards in low-income regions | -0.6% | Sub-Saharan Africa, South Asia, and parts of Latin America | Long term (≥ 4 years) |

| Consumer scepticism over synthetic additives and "over-fortification" claims | -0.4% | North America and Europe, where clean-label trends are strongest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Taste, Texture, and Sensory Limitations

Iron fortification in wheat flour can introduce metallic off-notes, which not only affect taste but also potentially shorten its shelf life by up to 30% unless specialty encapsulates are used to mitigate these effects[3]Source: Journal of Food Science, "Rapid identification of flaxseed oil based on portable fiber optic Raman spectroscopy combined with an oil microscopy method", ift.onlinelibrary.wiley.com. In plant-based milks, calcium can lead to sedimentation, a common issue that stabilizers address by altering viscosity. However, this approach often conflicts with the preferences of clean-label shoppers, who prioritize minimal processing and natural ingredients. Vitamin D3, when introduced in high-moisture bakery settings, tends to lose its potency over time. Consequently, fortification levels are capped at 400 IU per serving, significantly lower than the clinically desired 1,000 IU, which limits its nutritional impact. Furthermore, reformulating products to address these challenges can inflate ingredient costs by 15-25% and delay product launches, creating additional barriers to near-term growth in the market.

Nutrient-loss during thermal processing and long supply chains

Producers often over-fortify by 30-50% to counteract vitamin losses during extrusion and warm storage, ensuring that the final product meets nutritional label claims and regulatory standards. In Bangladesh, cold-chain deficiencies lead to over a 50% degradation of vitamin A in milk powder, significantly undermining both label compliance and consumer trust. This degradation not only impacts the nutritional value but also affects the marketability and competitiveness of the product in the market. While technologies like ProHeat can mitigate these losses by preserving vitamin content during processing and storage, they also increase production costs by up to USD 0.08 per liter. This added cost poses a significant challenge for manufacturers operating in lower-income markets, where affordability and cost sensitivity are critical factors for both producers and consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Infant Formula Drives Premiumization

In 2025, fortified dairy products dominated the fortified food market, capturing 28.05% of the total market share. This surge was largely fueled by the demand for high-value, clinical-grade infant nutrition. Premium infant formulas, often priced 30–50% above their standard counterparts, have been pivotal in driving growth among affluent consumers. For instance, Abbott’s Similac 360 Total Care raked in a whopping USD 1.2 billion in its inaugural year. Meanwhile, Nestlé’s NAN Supreme Pro swiftly clinched a 12% stake in China's premium segment within just 18 months. Such robust commercial outcomes underscore the efficacy of premiumization strategies, solidifying dairy's foundational role in the fortified foods arena. With ongoing innovations in functional benefits and clinical positioning, this segment's leadership is poised to continue.

Fortified snacks and ready-to-eat meals are the market's fastest-growing segments, boasting a CAGR of 8.11% through 2026 and 2031. This growth is largely attributed to evolving lifestyles that prioritize convenience and nutrition. Urban commuters, in particular, are increasingly opting for protein-rich, fiber-boosted bars, beverages, and meat snacks over traditional meals. Brands are capitalizing on this trend, using claims of combined macronutrient and micronutrient fortification to command price premiums of 40–60%, thereby enhancing perceived value. While achieving the desired taste and texture poses challenges, innovations like ingredient encapsulation are making strides in addressing these sensory concerns. With continued advancements in palatability and functionality, this segment is set to maintain its brisk growth pace.

By Ingredient Source: Plant-Based Fortification Outpaces Animal-Based

In 2025, plant-based ingredients seized a commanding 68.32% share of the fortified food market, propelled by a strong alignment with clean-label and sustainability trends. Inputs like pea protein, algal DHA, and lichen-derived vitamin D3 have achieved cost parity with their traditional counterparts, paving the way for wider adoption across diverse product categories. These ingredients resonate with health-conscious consumers who prioritize transparency and plant-forward nutrition, all while ensuring functionality. Their inherent versatility empowers manufacturers to diversify their fortified offerings, bolstering overall market growth. Notably, this expansion is largely incremental, broadening the fortified food market's size without significantly encroaching on established dairy-based channels.

Plant-based inputs are emerging as the fastest-growing segment, with projections indicating a robust CAGR of 8.55% from 2026 to 2031. This surge underscores a rapidly growing consumer inclination towards alternative nutrition sources. Moreover, advancements in plant-derived fortification are not only enhancing nutrient delivery but also elevating sensory performance, solidifying their presence in mainstream products. While animal-based ingredients remain pivotal in niche areas like infant and medical nutrition thanks to their superior bioavailability plant-based alternatives are swiftly narrowing this advantage. Technologies such as ProHeat are ensuring dairy products retain their nutrient stability and texture. Yet, the overarching trend leans towards plant-based innovations. With a global surge in clean-label demand, plant-based inputs are poised to spearhead the next growth wave in fortified foods.

By End-User: Children Segment Accelerates on School Feeding Programs

In 2025, adults dominated the fortified food market, making up 64.54% of total demand. This trend was bolstered by workplace wellness initiatives and a growing preference for convenient nutrition. As lifestyles became busier, adults increasingly turned to fortified snacks, beverages, and meal replacements tailored to their health needs. Purchases in this segment were largely driven by functional benefits like energy support, immunity boosts, and digestive health. Moreover, employers and corporate wellness programs have been actively promoting these fortified products as essential components of daily nutrition. As a result, adults have emerged as the leading revenue contributors in the fortified food landscape.

Children are the fastest-growing segment in the fortified food market, with projections indicating a CAGR of 7.48% from 2026 to 2031. This growth is largely attributed to government-led nutrition programs and innovative product targeting. Public initiatives are integrating fortified items, such as milk and yogurt, into school meal programs, significantly boosting early-age consumption. Concurrently, infant formulas enriched with HMOs and DHA are experiencing double-digit growth, underscoring a heightened parental emphasis on early-life nutrition. Additionally, new product launches, like fortified cereals tailored for vegetarian children in markets such as India, are effectively addressing dietary gaps. Collectively, these initiatives are not only broadening market penetration but also instilling lasting consumption habits from a young age.

By Distribution Channel: Online Retail Gains Share Through Subscription Models

In 2025, supermarkets/hypermarkets led the fortified food market, capturing 47.03% of the total share, bolstered by robust in-store visibility and promotional tactics. Strategies like end-cap displays, bundled offers, and point-of-sale education play a pivotal role in swaying consumer purchases. Physical retail stands out for impulse buys and products demanding consumer trust, such as fortified foods. The strength of this channel is further cemented by established distribution networks and strong retailer relationships. Consequently, even with the digital surge, offline retail remains the dominant sales force.

Online channels, however, are on a rapid ascent, with projections indicating a CAGR of 6.78% from 2026 to 2031. This growth is fueled by a rising appetite for personalized and convenient nutrition solutions. Brands like Nestlé’s Puritan’s Pride and Danone’s Huel are reaping the benefits of direct-to-consumer models, with a significant 40–80% of their revenue stemming from subscription-based platforms. Such channels not only facilitate recurring purchases and bolster customer retention but also lessen dependence on physical shelf space. Moreover, digital platforms offer invaluable consumer insights, enhancing targeted marketing and product innovation. This e-commerce pivot is not just altering distribution strategies but also propelling growth in the fortified food market.

Geography Analysis

In 2025, North America is poised to seize a commanding 36.92% share of the fortified food market, propelled by mandates on folic-acid tortillas and a rise in disposable incomes. Recent FDA regulations have greenlit the inclusion of 400 IU of vitamin D3 in plant-based milks, setting the stage for fortified almond and oat beverages. The region's robust regulatory framework not only supports but also fuels innovation in fortified food products, encouraging manufacturers to develop new and diverse offerings. Furthermore, as consumer demand for health-centric food options surges, manufacturers are responding by broadening their fortified product portfolios to cater to evolving preferences and nutritional needs.

Asia-Pacific is charting a swift upward trajectory, boasting a commendable 7.93% CAGR from 2026 to 2031. This momentum is largely attributed to India's aggressive push for oil fortification and a burgeoning demand for premium infant formulas in China. Governments across the region are championing nutritional programs to address malnutrition, such as large-scale initiatives to fortify staple foods like rice and wheat flour, bolstering market growth. Coupled with a burgeoning middle class that leans towards premium and fortified food products, the region's market is witnessing a rapid expansion, driven by increasing awareness of health and wellness among consumers.

Europe is in the midst of recalibrating its vitamin regulations. Yet, the UK's impending folic-acid mandate for flour, slated for December 2026, is projected to nudge compliance costs by a mere GBP 0.02/kg. This slight uptick pales in comparison to the anticipated public health dividends, such as reducing neural tube defects in newborns. Concurrently, there's a discernible uptick in consumer awareness about the significance of micronutrient-rich diets, driven by educational campaigns and government-backed initiatives. The premium pricing of fortified items, exemplified by vitamin-D milk in Scandinavia, underscores a consumer readiness to invest in health-boosting food choices, reflecting a growing prioritization of long-term health benefits over cost considerations.

Competitive Landscape

The fortified food market shows moderate fragmentation. While Nestlé, Danone, and Abbott dominate the fortified food market with a combined global revenue share of about 45%, regional dairy cooperatives and mid-tier brands are increasingly capturing market share through localized formulations and online sales channels. These smaller players leverage their agility to cater to specific regional tastes and preferences, which larger corporations often struggle to address. Additionally, the rise of e-commerce platforms has enabled these brands to reach a broader audience without significant investment in traditional retail infrastructure.

In the realm of technology, DSM-Firmenich has achieved a breakthrough with a 90% retention of vitamin A, making ambient snacks feasible. This innovation opens up new product categories that were previously considered impractical due to nutrient degradation. Furthermore, precision fermenters are offering vitamin B12 at a lower cost than traditional suppliers, paving the way for startups and private-label brands to enter the market more easily. This cost advantage not only lowers entry barriers but also intensifies competition among established players.

Fortified oils present an opportunity: India's mandate spans 22 million tonnes, yet 60% compliance remains elusive, primarily due to cost concerns. The lack of affordability for fortified oils among lower-income groups continues to hinder widespread adoption. Digital-first brands are finding success, as evidenced by subscription-based meal replacements boasting an 85% repeat purchase rate. These high retention rates highlight the potential for strong customer loyalty and recurring revenue streams in the segment. Kellanova's swift introduction of protein bites in 4,500 stores within just six months underscores the industry's rapid innovation pace, pushing established players to either hasten their product pipelines or risk losing market segments. This accelerated product development cycle reflects the growing pressure on incumbents to remain competitive in a dynamic market landscape.

Fortified Food Industry Leaders

-

Nestlé S.A.

-

General Mills Inc.

-

Kellanova

-

PepsiCo, Inc.

-

Danone SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: PepsiCo has debuted its latest fiber-enriched snacks in the U.S., rolling them out under the Sunchips and SmartFood brands. These new offerings aim to cater to the growing consumer demand for healthier snack options. The company's Smartfood FiberPop, a popcorn-based treat, boasts 10 grams of whole grains and 6 grams of fiber, providing a nutritious alternative for snack enthusiasts.

- July 2025: Innophos, a leader in leavening and baking solutions, has expanded its LEVAIR portfolio with the launch of LEVAIR Fortify, specifically designed for nutrient-dense bars. This innovative technology empowers manufacturers to elevate the taste and texture of protein-enriched baked bars. With LEVAIR Fortify, Innophos tackled the challenge of enhancing both the texture and volume of these bars. Bars made with LEVAIR Fortify not only retained their softness but also achieved a notable 30% increase in protein content, making them perfect for meal replacements or convenient snacks on the go.

- July 2025: Danone's plant-based brand, Alpro, has rolled out a new product line aimed at children. The lineup includes a chocolate-flavored oat drink, a strawberry-flavored soya drink, and vanilla and strawberry soya-based yogurt alternatives. These vegan-friendly, dairy-free products contain 30% less sugar than comparable children's items on the market. Furthermore, they are enriched with vital nutrients like calcium, vitamin D2, iodine, and vitamins B2 and B12. Proudly devoid of artificial colorings, preservatives, and flavorings, the range is also naturally lactose-free.

- October 2024: Australian firm Coco2 has launched what it claims to be the world's inaugural coconut-based infant formula. Coco2's offering is not only nutritionally comprehensive but also enriched with vital vitamins and minerals, boasting a protein and fat composition that closely mirrors that of breast milk.

Global Fortified Food Market Report Scope

Fortified food is a product enriched with essential nutrients, usually vitamins or minerals, to enhance its nutritional value. Based on the product type, the market is segmented into fortified dairy, fortified bakery and cereals, fortified beverages, fortified oils and fats, fortified infant formula, fortified snacks, bars and ready-to-eat foods, and others. By ingredient source, the market is segmented into plant-based and animal-based. By end-user, the market is segmented into adults and children. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retailers, and other distribution channels. The report offers a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Fortified Dairy |

| Fortified Bakery and Cereals |

| Fortified Beverages |

| Fortified Oils and Fats |

| Fortified Infant Formula |

| Fortified Snacks, Bars and Ready-to-Eat Foods |

| Others |

| Plant-Based |

| Animal-Based |

| Adults |

| Children |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retailers |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Fortified Dairy | |

| Fortified Bakery and Cereals | ||

| Fortified Beverages | ||

| Fortified Oils and Fats | ||

| Fortified Infant Formula | ||

| Fortified Snacks, Bars and Ready-to-Eat Foods | ||

| Others | ||

| By Ingredient Source | Plant-Based | |

| Animal-Based | ||

| By End-User | Adults | |

| Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global fortified food market and its growth projection?

The global fortified food market is valued at USD 203.88 billion in 2026 and is projected to reach USD 281.04 billion by 2031, exhibiting a compound annual growth rate of 6.63% during the forecast period.

Which product segment dominates the fortified food market?

Fortified dairy products command the largest market share at 28.05% in 2025, benefiting from established consumer acceptance and regulatory frameworks that facilitate vitamin D and calcium fortification.

What is the market concentration level in the fortified food industry?

The fortified food market exhibits moderate fragmentation, indicating significant opportunities for consolidation through strategic acquisitions and partnerships.

Which region leads the fortified food market and why?

North America leads with 36.92% market share in 2025, supported by established fortification regulations, consumer health awareness, and advanced food processing infrastructure.

Page last updated on: