Bromelain Products Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

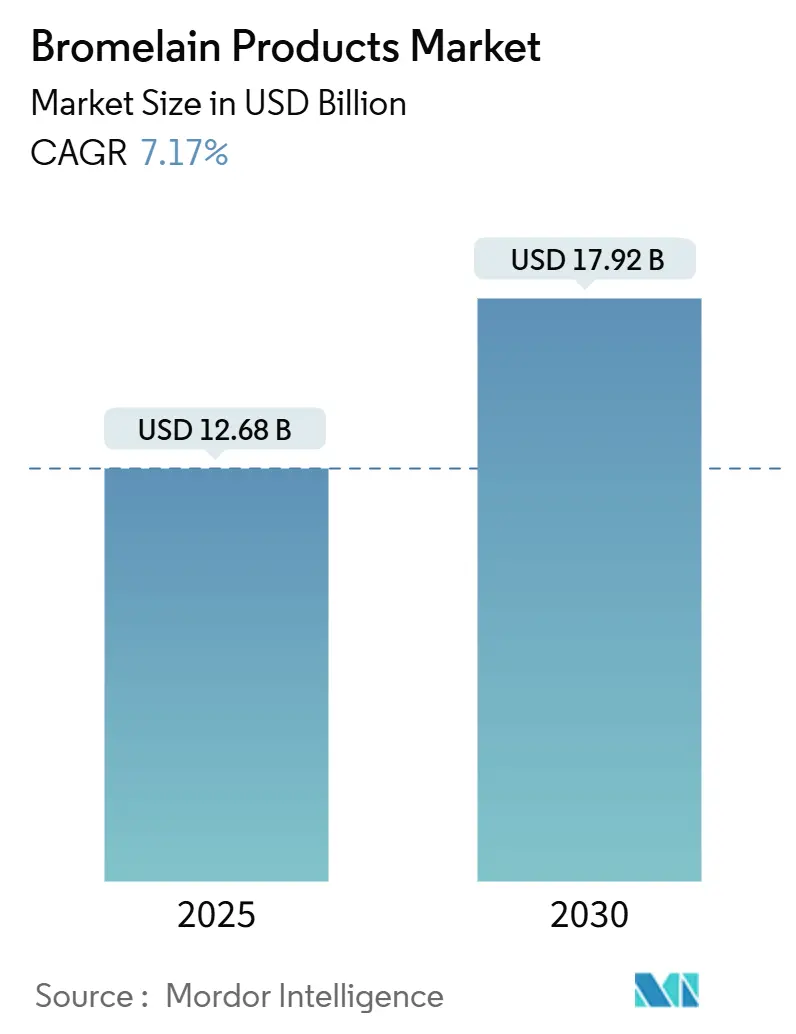

| Market Size (2025) | USD 12.68 Billion |

| Market Size (2030) | USD 17.92 Billion |

| Growth Rate (2025 - 2030) | 7.17% CAGR |

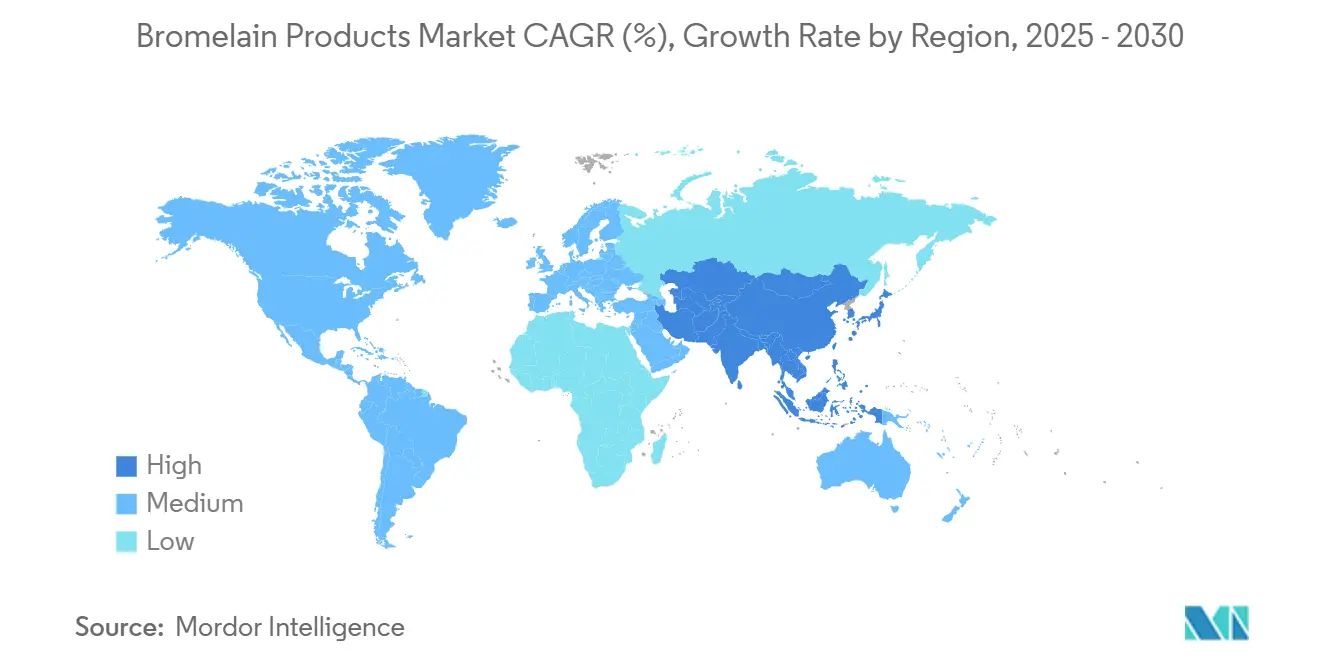

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bromelain Products Market Analysis by Mordor Intelligence

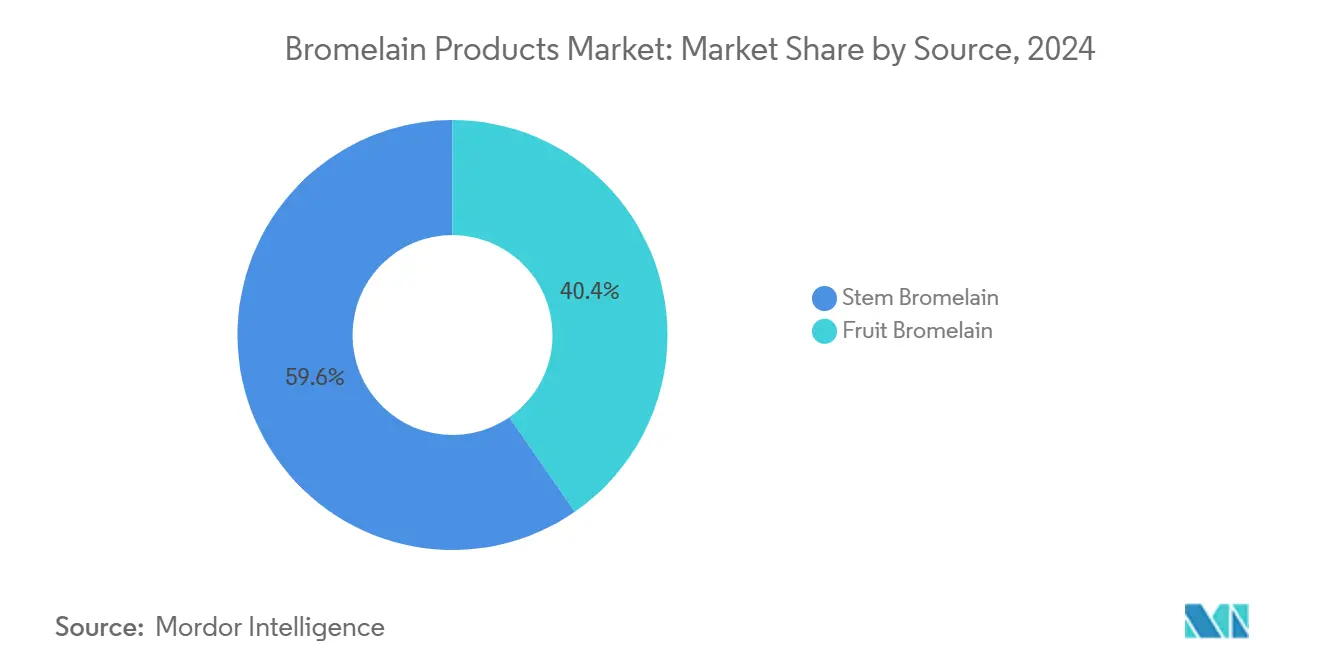

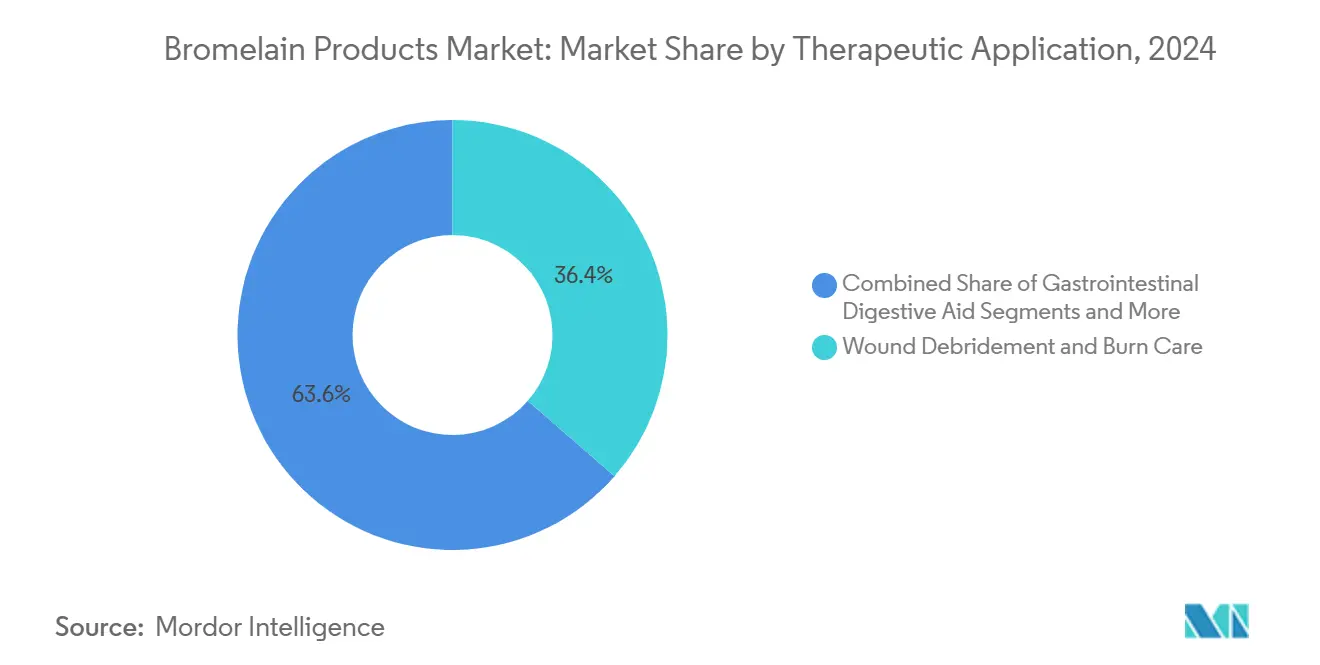

The bromelain products market size is USD 12.68 billion in 2025 and is projected to reach USD 17.92 billion by 2030, advancing at a 7.17% CAGR, confirming robust near-term expansion for the bromelain products market. Regulatory approvals, shifting clinical protocols, and heightened reimbursement clarity are steering demand away from general dietary supplements toward prescription-driven therapeutic uses. Enzymatic debridement sets the growth pace after the FDA cleared MediWound’s NexoBrid in 2023, providing clinical validation and payer confidence.[1]MediWound, “MediWound Announces FDA Approval of NexoBrid for Severe Thermal Burns,” ir.mediwound.comQuality assurance has become a strategic differentiator as independent testing found that 75% of Amazon-listed bromelain supplements failed potency claims, propelling consolidation among firms with sophisticated analytics. Stem bromelain retained 59.63% bromelain products market share in 2024 thanks to higher activity levels, while powder formats dominated with a 44.37% share, reflecting hospital demand for shelf-stable dosage forms. North America captured 39.48% of 2024 sales due to mature reimbursement systems, yet Asia-Pacific offers a stronger 9.58% growth outlook as local extraction capacity scales up.

Key Report Takeaways

- By source, stem bromelain led with 59.63% bromelain products market share in 2024; fruit bromelain is forecast to grow at a 10.83% CAGR through 2030.

- By form, powder accounted for 44.37% of the bromelain products market size in 2024, while the “others” segment is advancing at a 9.48% CAGR to 2030.

- By therapeutic application, wound debridement & burn care held 36.42% revenue share in 2024, and oncology adjuvant therapy records the fastest 10.36% CAGR through 2030.

- By distribution channel, hospital pharmacies controlled 53.75% of 2024 revenue; online channels are expanding at an 11.74% CAGR to 2030.

- North America maintained 39.48% sales in 2024, whereas Asia-Pacific posts the highest 9.58% CAGR through 2030.

Global Bromelain Products Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Chronic Wounds & Diabetic Ulcers Boosting Enzymatic Debridement Demand | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Increasing Adoption Of Natural Anti-Inflammatory Agents In OTC Health Supplements | +1.2% | Global, strongest in APAC and North America | Short term (≤ 2 years) |

| Integration Of Bromelain In Combination Therapies For Post-Operative Inflammation | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing Clinical Evidence For Mucolytic Efficacy In Respiratory Conditions | +0.9% | Global, accelerated by COVID-19 research | Short term (≤ 2 years) |

| Development Of Bromelain-Based Topical Formulations For Burn Debridement | +0.7% | North America & EU regulatory markets | Long term (≥ 4 years) |

| Emergence Of Bromac Protocol For Cytokine-Storm Attenuation In Viral Infections | +0.6% | Global, pending clinical validation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Chronic Wounds & Diabetic Ulcers Boosting Enzymatic Debridement Demand

Diabetic foot ulcers create a persistent clinical burden, and MediWound’s EscharEx achieved 63% complete debridement versus 0% for collagenase in Phase II trials during 2024, prompting Medicare to expand coverage for bromelain-based wound products.[2]Centers for Medicare & Medicaid Services, “Skin Substitute Grafts for Diabetic Foot Ulcers,” cms.govRecent studies reported 98% biofilm reduction, a key factor in chronic ulcer healing. The policy shift elevates bromelain from a salvage tool to a frontline option, widening the bromelain products market.

Increasing Adoption Of Natural Anti-Inflammatory Agents In OTC Health Supplements

Randomized trials in 2024 showed bromelain matching diclofenac for post-operative pain relief, encouraging clinicians and consumers to consider enzyme-based options. The FDA affirms GRAS status under 21 CFR 184.1024, enabling clear label claims for supplement brands.[3]U.S. Food and Drug Administration, “21 CFR 184.1024 — Bromelain,” ecfr.govHowever, independent testing uncovered potency shortfalls in three-quarters of online listings, nudging shoppers toward premium, third-party-verified products. Walmart’s 2025 listing of bromelain signals mainstream retail acceptance.

Integration Of Bromelain In Combination Therapies For Post-Operative Inflammation

A 2025 trial combining bromelain with alpha-lipoic acid cut breast-surgery complications by 40%, allowing lower steroid requirements and shorter hospital stays. European centers using bromelain-coumarin protocols for facial trauma documented significant edema reduction across 100 patients in 2024. Hospital formularies increasingly specify bromelain combinations, strengthening the bromelain products market in institutional care.

Growing Clinical Evidence For Mucolytic Efficacy In Respiratory Conditions

Phase 1b/2a studies confirmed that bromelain combined with N-acetylcysteine disrupts SARS-CoV-2 spike proteins, accelerating mucus clearance. Pediatric otitis media research in 2024 showed improved fluid drainage without antibiotics, broadening bromelain adoption in ENT practices. NCCIH now lists bromelain among recognized respiratory adjuncts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Stem Advantage Sustains but Fruit Gains

Stem bromelain accounted for 59.63% of the bromelain products market share in 2024 and retains the dominant position because hospital protocols demand the higher, more predictable enzymatic activity delivered by stem extracts. Sustainability concerns and climate-driven supply shocks, however, are pushing manufacturers to diversify; fruit bromelain is set to expand at a 10.83% CAGR through 2030, helped by waste-stream valorization that lowers raw-material costs. A growing number of processors in Thailand, Indonesia, and the Philippines are integrating stem and fruit feedstocks to hedge against El Niño-related crop losses documented in 2025 regional market updates. Pharmaceutical buyers still prefer stem material for dosage accuracy, yet formulators targeting consumer supplements view fruit bromelain as a lower-priced path to “clean label” positioning.

Circular-economy narratives strengthen fruit bromelain’s appeal because processors recover ethanol and xylitol alongside the enzyme, improving plant economics and reducing waste. Emerging oncology and respiratory developers also test fruit-sourced material to secure dual-origin supply in case stem harvest volatility escalates. Sustained investment in cold-chain logistics and ISO-certified assays is narrowing quality gaps between the two sources, but reimbursement codes remain tied to stem activity units, locking in near-term demand. Over the outlook period, blended-feedstock contracts are expected to rise, gradually diluting stem’s lead while keeping the bromelain products market focused on activity-driven specifications rather than raw-material origin.

By Form: Powder Format Dominates Clinical Supply

Powder formulations captured 44.37% of the bromelain products market size in 2024 because lyophilization locks in activity for 24 months at 2 °C–8 °C, simplifying hospital stocking and compounding. Liquids remain less than 15% of shipments due to cold-chain costs and rapid potency decay, while capsule and tablet lines serve retail buyers seeking convenience over maximal bioactivity. Topical gels, liposomes, and micro-encapsulated beads—all grouped under “others”—are advancing at a 9.48% CAGR through 2030 as innovators chase targeted delivery and controlled release.

Clinical precedent set by NexoBrid’s topical gel encourages developers to pursue wounds, dermatology, and mucosal applications that powders cannot reach. Enteric-coated microcapsules now entering pilot scale protect bromelain from gastric degradation and allow site-specific intestinal release, a capability valued in anti-inflammatory and gastrointestinal protocols. Powder’s dominance will persist in inpatient settings, yet retail and specialty channels prize differentiated formats that command higher margins per activity unit. As pharmaco-economic models reward outcomes over dosage volume, the form factor race will pivot on demonstrable clinical advantages rather than headline concentration numbers.

By Therapeutic Application: Wound Care Leads, Oncology Accelerates

Wound debridement and burn care represented 36.42% of 2024 revenue after the FDA cleared NexoBrid, solidifying enzymatic debridement as a reimbursable first-line intervention. Oncology adjuvant use is the fastest-moving niche, anticipated to grow 10.36% annually as mucin-rich tumors respond to BromAc protocols that dismantle protective barriers and improve chemotherapy penetration. Anti-inflammatory and pain management products serve the widest patient base but face price pressure from generic NSAIDs and biologics.

Respiratory and ENT adoption builds on pediatric otitis and COVID-19 mucolytic studies, while digestive-aid SKUs plateau amid intensified probiotic competition. Long-term upside centers on oncology, where hospital formularies weigh bromelain combinations against costly monoclonal antibodies. Cross-label evidence from cancer and chronic-wound trials strengthens payer confidence by showcasing enzyme versatility across tissue types. Commercial momentum will depend on Phase III data translating laboratory promise into measurable survival or recovery benefits that justify premium pricing.

By Distribution Channel: Hospitals Anchor Sales, Online Surges

Hospital pharmacies controlled 53.75% of global revenue in 2024 because reimbursement codes, dosing precision, and clinician oversight favor institutional dispensing. Retail drugstores continue to service over-the-counter demand yet concede share to e-commerce as telemedicine mainstreams electronic scripts. Online pharmacies are projected to post an 11.74% CAGR to 2030, supported by direct-to-consumer subscription models and virtual follow-ups that sidestep travel and scheduling barriers.

Potency scandals—75% of Amazon listings failed label claims in 2024—restrain mass-market momentum, prompting premium brands to display third-party certificates prominently on product pages. Prescription-based e-pharmacies exploit this credibility gap, bundling clinician consultations with controlled-temperature fulfillment. Offline chains respond by adding refrigerated enzyme sections and deploying QR code verification at shelf. Over the forecast horizon, blended models that merge hospital-grade sourcing with digital convenience are set to capture incremental share, provided quality governance keeps pace with volume growth.

Geography Analysis

North America sustained 39.48% of 2024 global sales, aided by FDA approvals, Medicare reimbursement, and early clinician adoption. High labor and compliance costs curb price competitiveness, but regulatory clarity gives exporters an edge in other regions.

Europe is sizable yet fragmented: differing member-state classifications slow product launches and complicate pan-EU trials. Nonetheless, academic hospitals there conduct pivotal combination studies that influence global guidelines.

Asia-Pacific posts a 9.58% forecast CAGR, reflecting its dominance in pineapple agriculture and rising healthcare outlays. Taiwan, Thailand, and India scale extraction capacity, using waste-stream valorization to cut costs and win ESG-minded buyers. Climate-related crop risk remains an operational challenge.

Competitive Landscape

The bromelain products industry features moderate fragmentation with consolidation pressure around GMP adherence and assay standardization. MediWound’s pharmaceutical route delivers defensible IP, price premiums, and hospital adoption. NOW Foods’ open potency testing serves both as brand protection and industry-wide quality wake-up call. Walmart’s large-scale retail entry signals commoditization on the supplement side, whereas smaller labs explore oncology, respiratory, and topical innovations.

Vertical integration spans plantation sourcing, enzyme extraction, cold-chain logistics, and in-house analytics. Firms pursuing biorefinery concepts aim to offset raw-material costs and lessen climate risk. Market concentration is a moderately fragmented landscape with escalating quality-based consolidation.

Bromelain Products Industry Leaders

Ursapharm Arzneimittel GmbH

MediWound Ltd

Vital Nutrients

Life Extension

NOW Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MediWound began the VALUE Phase III trial of EscharEx in venous leg ulcer patients across 40 sites, targeting market entry by 2027.

- October 2024: MediWound announced Phase II head-to-head study comparing EscharEx versus collagenase ointment for venous leg ulcers, scheduled to begin in 2025 with 45 patients across U.S. and European sites, supporting the Biologics License Application strategy for market entry.

Global Bromelain Products Market Report Scope

| Stem Bromelain |

| Fruit Bromelain |

| Powder |

| Liquid |

| Capsule / Tablet |

| Others |

| Wound Debridement & Burn Care |

| Anti-inflammatory & Pain Management |

| Respiratory & ENT Applications |

| Gastrointestinal Digestive Aid |

| Oncology Adjuvant Therapy |

| Others (Obesity, Cardiovascular Support) |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Stem Bromelain | |

| Fruit Bromelain | ||

| By Form | Powder | |

| Liquid | ||

| Capsule / Tablet | ||

| Others | ||

| By Therapeutic Application | Wound Debridement & Burn Care | |

| Anti-inflammatory & Pain Management | ||

| Respiratory & ENT Applications | ||

| Gastrointestinal Digestive Aid | ||

| Oncology Adjuvant Therapy | ||

| Others (Obesity, Cardiovascular Support) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the bromelain products market in 2025?

The bromelain products market size stands at USD 12.68 billion in 2025.

What is the forecast CAGR for bromelain products to 2030?

The market is expected to grow at a 7.17% CAGR between 2025 and 2030.

Which source segment holds the majority share today?

Stem bromelain controls 59.63% of revenue thanks to higher enzymatic activity.

Why are powder formulations preferred in hospital settings?

Lyophilized powders preserve enzyme activity, extend shelf life, and simplify dosing, securing 44.37% share in 2024.

What geography offers the fastest growth outlook?

Asia-Pacific shows a 9.58% CAGR forecast, driven by raw-material availability and rising healthcare spending.

Which therapeutic area is emerging quickest after wound care?

Oncology adjuvant therapy is climbing at a 10.36% CAGR as research confirms bromelain’s mucin-disrupting benefits.

Page last updated on: