Market Overview

| Study Period | 2020 - 2031 |

|---|---|

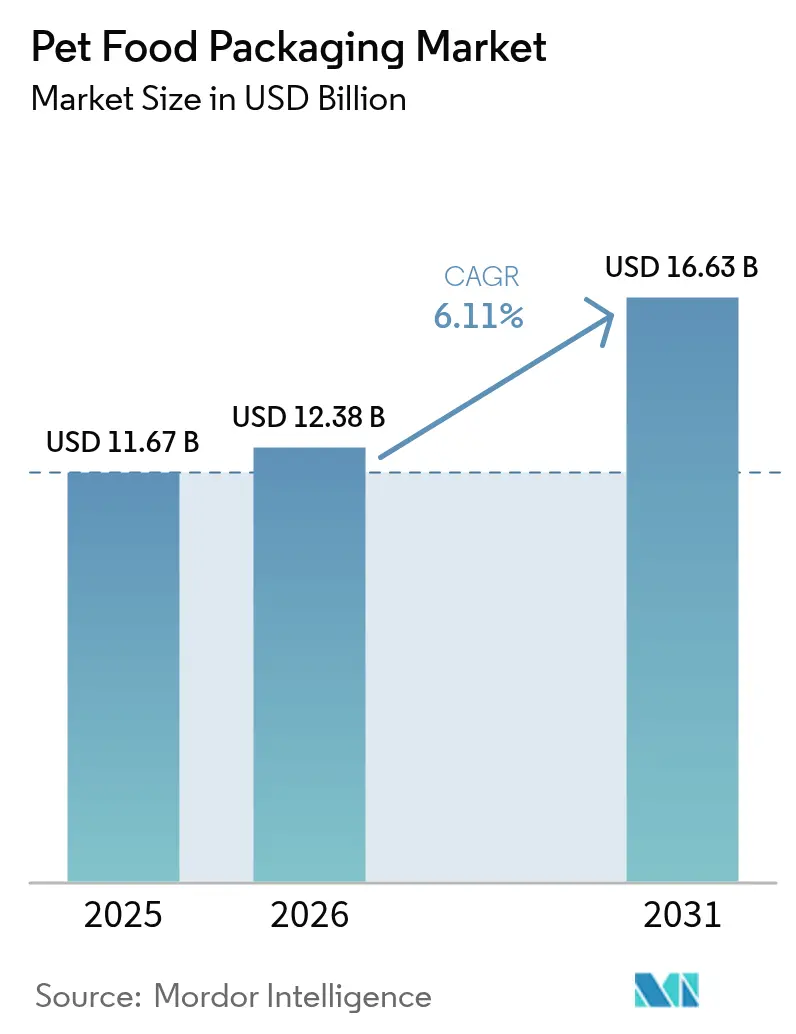

| Market Size (2026) | USD 12.38 Billion |

| Market Size (2031) | USD 16.63 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pet Food Packaging Market Analysis by Mordor Intelligence

pet food packaging market size in 2026 is estimated at USD 12.38 billion, growing from 2025 value of USD 11.67 billion with 2031 projections showing USD 16.63 billion, growing at 6.11% CAGR over 2026-2031. Growing regulatory pressure in Europe and the United States, rapid premiumization of wet formats, and disruptive material science innovations together create a steady demand pipeline for solutions that balance barrier protection with recyclability. North America remains the largest consuming region, supported by strong e-commerce penetration and early adoption of mono-material flexibles, while Asia-Pacific records the fastest regional growth as urban pet ownership rises in China. Brand owners’ 2025 sustainability pledges, rising raw-material volatility, and the FDA’s phase-out of 35 PFAS food-contact approvals reinforce the need for converters to shift away from conventional multi-layer plastics toward recyclable paper, mono-PE, and bio-composite alternatives. Competitive intensity stays moderate as large integrated players capitalize on scale, but nimble specialists gain share by offering PFAS-free barriers, smart-packaging features, and design-for-recycling services that major brand owners increasingly require.

Key Report Takeaways

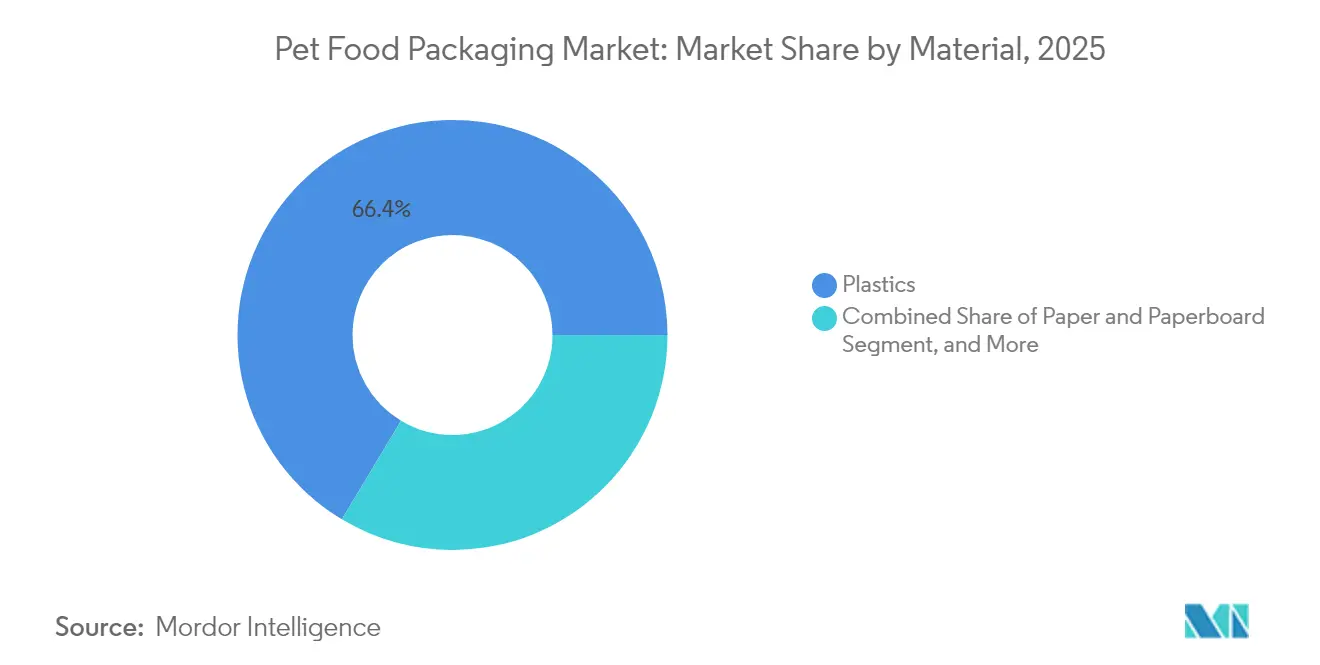

- By material, plastics retained 66.40% of the pet food packaging market share in 2025, while biobased and composite alternatives are poised for a 10.2% CAGR through 2031.

- By product type, pouches held 42.30% revenue share of the pet food packaging market in 2025; smart formats and other emerging solutions are forecast to rise at a 9.3% CAGR to 2031.

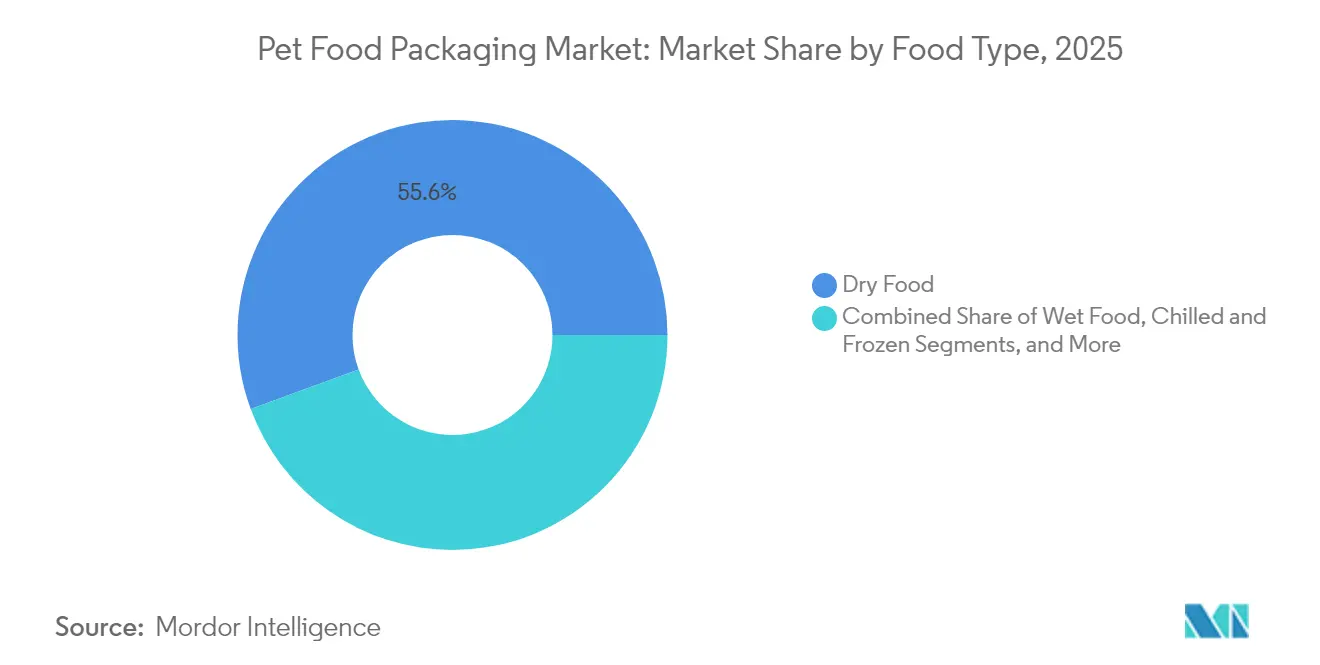

- By food type, dry formulations accounted for 55.60% share of the pet food packaging market size in 2025; wet foods are projected to grow at an 8.6% CAGR between 2026-2031.

- By pet type, dog food commanded 46.50% of the pet food packaging market in 2025, whereas cat food is expected to expand at an 7.9% CAGR through 2031.

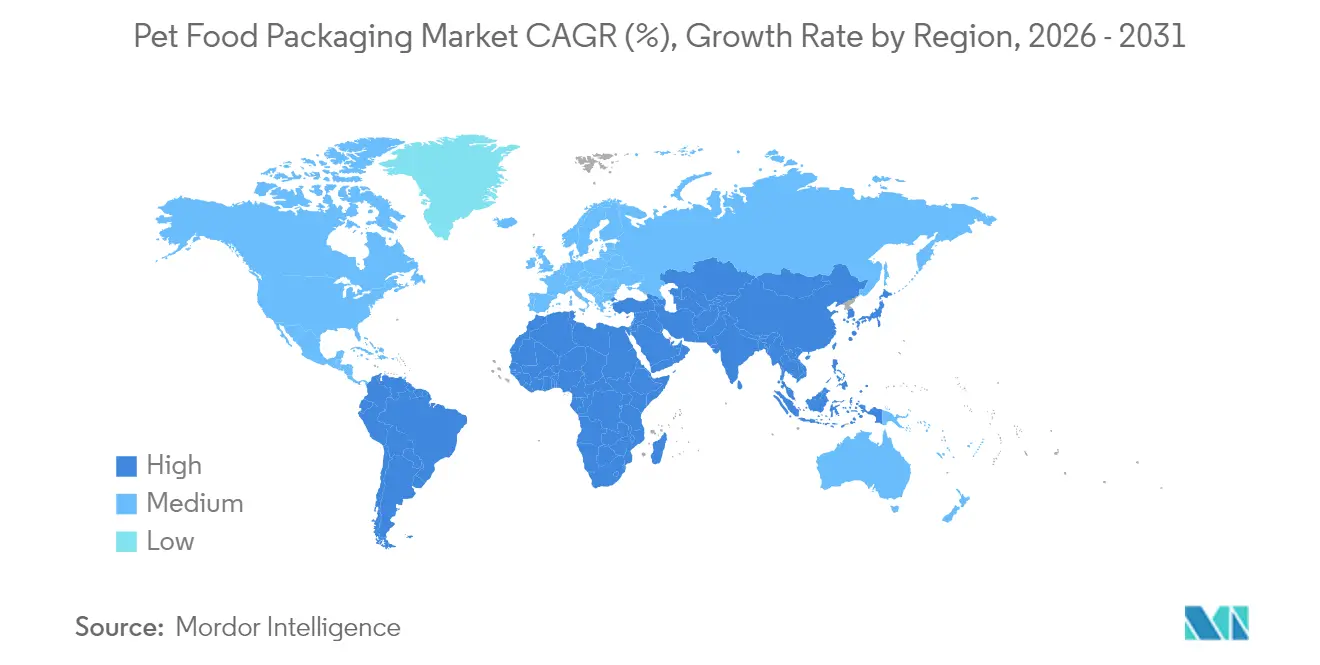

- By region, North America led with 33.70% of the pet food packaging market share in 2025; Asia-Pacific is set to post a 7.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pet Food Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Demand for Recyclable Mono-Material Pouches Post-Europe SUP Directive | +1.2% | Europe, spill-over to North America | Medium term (2-4 years) |

| Premiumization of Wet Dog Food Driving High-Barrier Retort Pouch Adoption in North America | +0.9% | North America, expanding to APAC | Short term (≤ 2 years) |

| Urban Pet Ownership Boom in China Fueling Small-Pack Formats with Reclosable Zippers | +0.8% | APAC core, particularly China | Long term (≥ 4 years) |

| E-commerce Growth for Specialty Diets Accelerating Lightweight Flexible Packaging in the US | +0.7% | North America, expanding globally | Medium term (2-4 years) |

| Brand Owner 2025 Sustainability Pledges Catalyzing Paper-Based Bag Investments in Europe | +0.6% | Europe, with global influence | Short term (≤ 2 years) |

| EU Regulation 2024/354 on Mineral-Oil Migration Spurring Functional Barrier Laminates | +0.5% | Europe, regulatory spill-over globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for recyclable mono-material pouches post-SUP Directive

European Single-Use Plastics rules compel brand owners to abandon complex laminates, prompting converters to commercialize mono-PE structures that equal traditional barrier performance yet meet recyclability targets.[1]European Commission, “Directive (EU) 2019/904 on Single-Use Plastics,” europa.euSiegwerk’s CIRKIT coatings now enable grease, oil, and oxygen protection inside mono-PE, while Longdapac’s 100% recyclable high-barrier pouches for North American brands confirm regulatory ripple effects beyond Europe.

Premiumization of wet dog food driving retort pouch adoption

North American consumers pay 30-50% premiums for chef-style wet formats, spurring investments in Amcor’s AmLite HeatFlex recycle-ready pouches that preserve nutrients during thermal sterilization. Inline seal-inspection systems such as Special Dog Company’s 100% coverage model safeguard quality, and NaturPak Pet’s 50 million-carton annual capacity illustrates scalability requirements for premium growth.

Urban pet ownership boom in China fueling small formats

China’s pet economy exceeded USD 41.8 billion in 2024, with 57% of food bought online, pushing demand for compact, zipper-reclosable pouches that fit smaller apartments and withstand parcel delivery stresses. U.S. pet-food exports of USD 296.6 million in 2024 also accelerate packaging upgrades that convey origin, freshness, and portion control.

E-commerce growth for specialty diets accelerating flexibles

In the United States, online sales growth and shipping-cost sensitivity steer brands toward 20-30% lighter flexible formats that still withstand automated handling. Amcor’s ISTA-certified labs ensure packages survive the e-commerce journey, while direct-to-consumer startups leverage digital printing for on-pack personalization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PET and Aluminum Prices Squeezing Converter Margins for Wet-Food Cans | -0.8% | Global, particularly Europe and North America | Short term (≤ 2 years) |

| US PFAS Bans in Food-Contact Boards Forcing Costly Reformulations | -0.6% | North America, regulatory spill-over globally | Medium term (2-4 years) |

| EVOH Barrier Resin Shortages Limiting Stand-Up Pouch Capacity in APAC | -0.5% | APAC core, supply chain impacts globally | Short term (≤ 2 years) |

| Limited Curb-Side Recyclability of Retort Structures Discouraging Retailers | -0.4% | Global, particularly Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile PET and aluminum prices squeezing converter margins

Anti-dumping measures and logistics disruptions pushed European PET above EUR 1,130 t in early 2025, while global aluminum demand for cans topped USD 59 billion, compressing converter profits and hastening interest in recycled content or alternative substrates.

U.S. PFAS bans triggering costly reformulations

The FDA’s withdrawal of 35 PFAS food-contact clearances by January 2025 forces board-and-paper suppliers to adopt new barriers, with compliance documentation and line retrofits disproportionately burdening small converters.[2]FDA, “35 PFAS Food-Contact Notifications No Longer Effective,” fda.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: plastics dominance amid bio-based acceleration

Plastics supplied 66.40% of 2025 revenues, making the material segment the economic backbone of the pet food packaging market. Yet brand commitments and EU rules spur a 10.2% CAGR for bio-based and composite formats. Polyethylene thrives in mono-material designs, whereas PET’s volatility drives interest in chemically recycled and rPET blends. Paperboard progresses as Packaging-and-Waste Regulation deadlines approach, while lignin-bionanocomposites showcase antioxidant capabilities for future high-barrier adoption. The pet food packaging market size attached to paper and board is projected to expand at a mid-teens pace through 2031, supported by Billerud’s plan to supply 300 kilotons of cartonboard annually.

Second-generation bio-composites use agricultural waste streams to cut carbon intensity without compromising machinability, offering converters a hedge against fossil feedstock risk. Amcor’s Indiana recycled-PE agreement with NOVA Chemicals underpins a North American circular platform, ensuring resin availability for mono-PE pouches. Meanwhile, aluminum’s high recycling rate cushions cost headwinds, keeping cans relevant for retort wet food even as converters investigate PFAS-free epoxy replacements.

By Product Type: pouches leadership challenged by innovation

Pouches captured 42.30% 2025 share owing to convenience, shelf appeal, and e-commerce compatibility. Retort variants underpin wet-food premiumization, while stand-up formats benefit from zipper-reseal trends among urban consumers. The other-product-types bucket, expanding at 9.3% CAGR, covers smart labels, portion-controlled dispensers, and paper-based cups that meld fiber strength with barrier coatings. Amcor’s 80%-recyclable AmFiber Performance Paper proves the viability of paper for moisture-sensitive applications without sacrificing branding surface.

Graphics quality, handling efficiency, and pack-to-product ratios keep pouches favorable, yet retailer take-back pilots for curbside recycling remain limited. Smart-packaging prototypes embed freshness sensors and color-change inks, but mass uptake awaits cost parity. Bags still dominate large-volume dry food, though single-serve trends could gradually migrate volume into flexibles. Metal cans hold niche loyalty for heritage wet lines despite aluminum volatility, supported by robust recycling infrastructure.

By Food Type: dry-food stability versus wet-food dynamism

Dry kibble commanded 55.60% revenue in 2025 and remains the volume anchor of the pet food packaging market. Its scale reinforces demand for cost-efficient flexibles and bags that preserve freshness and oil stability. The segment embraces mono-PE with EVOH or plasma coatings to satisfy recyclability mandates while protecting against moisture ingress.

Wet food, growing at 8.6% CAGR, is reshaping converter portfolios. Shoppers equate stew-like textures with human-grade meals, propelling adoption of retort pouches, aluminum trays, and shelf-stable cartons that deliver premium cues. Cold-chain chilled products incrementally emerge, requiring high-barrier films capable of seal integrity at sub-zero temperatures. Treats and functional snacks rely on high-definition graphics and window features to showcase product form and reinforce transparency claims.

By Pet Type: dog-food foundation with cat-food momentum

Dog products commanded 46.50% 2025 share, favoring bulk-size packaging optimized for pantry storage. Large-bag offerings depend on PE films with anti-grease coatings, while wet dog sub-segments gravitate toward retort pouches for higher-margin single-serve lines. Cat items register an 7.9% CAGR to 2031 as smaller-pack, portion-controlled, and multi-variety packs align with feline eating behavior and rising cat ownership in high-density cities. Other species-birds, fish, reptiles-represent niche but fast-growing spaces for specialized oxygen-barrier sachets and dosing closures.

Geography Analysis

North America controlled 33.70% of 2025 sales, reflecting established ownership rates and the region’s early pivot to recycle-ready pouches. High producer-price inflation since 2021 elevates packaging optimization on cost and carbon, driving uptake of lightweight flexibles seasoned for e-commerce shocks. The FDA’s PFAS phase-out accelerates paper-and-polymer barrier R&D, while California and Maine mandates create a patchwork that favors suppliers with lab-validated compliance toolkits.

Asia-Pacific is the fastest-growing region at 7.3% CAGR, led by China’s USD 41.8 billion pet economy and digital-first purchasing habits. Local converters grapple with EVOH resin shortages that cap pouch capacity, prompting R&D into silicon-oxide and plasma-coated mono-PE as substitute barriers. Tier-2 cities show domestic brands advancing localized graphics and QR code traceability to court rising middle-income pet owners.

Europe’s growth remains steady, anchored by robust regulation that forces recyclability and recycled-content integration. The Packaging-and-Packaging-Waste Regulation sets firm 2030 targets, spurring investment in paper-based bag lines and new grease-proof coatings. Single-Use Plastics requirements bring forward design-for-recycling guidelines that displace legacy multilayer structures in dry food. Cross-industry alliances such as Saica–Mondelez transfers know-how to pet food, widening supply of paper flexibles.

Competitive Landscape

The pet food packaging market features moderate fragmented. Global multi-sleeve players such as Amcor, Mondi, and ProAmpac command scale, proprietary coatings, and multi-regional plant networks that attract multinational brand contracts. Strategic roadmaps emphasize PFAS-free barriers, mono-material architectures, and validated e-commerce durability tests. Innovation portfolios now include paper-based high-barrier laminates, advanced seal-inspection AI, and recycled-resin integration.

M&A activity intensifies. Toppan’s USD 1.8 billion purchase of Sonoco’s flexible unit bolsters retort-pouch know-how, while General Mills’ USD 1.45 billion buy of Whitebridge Pet Brands signals downstream vertical integration that influences packaging specifications. Patent landscapes in lignin-bionanocomposites and active-oxygen scavengers confer defensive moats to early movers. Regional specialists flourish by servicing mid-size pet-food producers seeking fast design iterations and label-ready small batch runs.

Supply risks from raw-material price spikes incentivize converters to tether resin sourcing to recycled streams and long-term metal contracts. ESG investors scrutinize greenhouse-gas footprints, prompting public targets such as ProAmpac’s Science-Based Net-Zero pledge, which ramps up adoption of low-carbon substrates and closed-loop partnerships with U.S. material recovery facilities.

Pet Food Packaging Industry Leaders

American Packaging Corporation

ProAmpac LLC

Constantia Flexibles Group GmbH

Amcor Group GmbH

Crown Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: JBT Corporation closed its acquisition of Marel, adding Wenger equipment capabilities that integrate processing and pet food packaging lines.

- December 2024: Toppan Holdings agreed to acquire Sonoco’s Thermoformed & Flexible Packaging unit for USD 1.8 billion, expanding high-barrier pouch capacity.

- November 2024: General Mills purchased Whitebridge Pet Brands for USD 1.45 billion, deepening wet-food portfolio breadth.

- October 2024: ProAmpac committed to SBTi-aligned net-zero targets and received an EcoVadis sustainability medal.

Global Pet Food Packaging Market Report Scope

Pet food packaging ensures products remain fresh, durable, and contamination-free. As pet owners grow increasingly concerned about their pets' nutritional intake, there has been a surge in the production of diverse pet foods. This, in turn, amplifies the demand for innovative materials in pet food packaging. The study meticulously monitors fundamental demand-side dynamics, leveraging a comprehensive set of base indicators, including pet food demand and local production trends.

The pet food packaging market is segmented by material (paper and paperboard, metal, and plastic), product type (pouches, folding cartons, metal cans, bags, and other product types), type of food (dry food, wet food, and chilled and frozen food), animal (dog food, cat food, and other animal), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for the above-mentioned segments.

By Material

| Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Other Plastics | |

| Paper and Paperboard | |

| Metal | |

| Biobased and Compostie Materials |

By Product Type

| Pouches |

| Bags |

| Metal Cans |

| Other Product Types |

By Type of Food

| Dry Food |

| Wet Food |

| Chilled and Frozen |

| Treats and Snacks |

By Pet Type

| Dog Food |

| Cat Food |

| Other Pet Food |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Material | Plastic | Polyethylene (PE) | |

| Polypropylene (PP) | |||

| Polyethylene Terephthalate (PET) | |||

| Other Plastics | |||

| Paper and Paperboard | |||

| Metal | |||

| Biobased and Compostie Materials | |||

| By Product Type | Pouches | ||

| Bags | |||

| Metal Cans | |||

| Other Product Types | |||

| By Type of Food | Dry Food | ||

| Wet Food | |||

| Chilled and Frozen | |||

| Treats and Snacks | |||

| By Pet Type | Dog Food | ||

| Cat Food | |||

| Other Pet Food | |||

| By Geography | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the pet food packaging market?

The pet food packaging market is valued at USD 12.38 billion in 2026 and is forecast to reach USD 16.63 billion by 2031.

Which region holds the largest share of pet food packaging sales?

North America accounts for 33.70% of global revenues, driven by high e-commerce penetration and early adoption of recyclable mono-material pouches.

Why are mono-material pouches gaining traction?

They meet Single-Use Plastics and recyclability mandates while providing comparable barrier protection, creating a regulatory-compliant alternative to multilayer laminates.

How fast is the Asia-Pacific market growing?

Asia-Pacific is projected to expand at a 7.3% CAGR, fueled by China’s surging urban pet ownership and dominant online retail channels.

What is the biggest challenge for converters between 2025 and 2031?

Volatile PET and aluminum prices, compounded by PFAS regulatory bans, are squeezing margins and forcing accelerated material innovation.

Which companies lead sustainable packaging innovation?

Amcor, Mondi, and ProAmpac spearhead the development of PFAS-free coatings, high-barrier paper solutions, and recycle-ready mono-PE structures.

Page last updated on: