Luxury Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.66 Billion |

| Market Size (2031) | USD 24.17 Billion |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Packaging Market Analysis by Mordor Intelligence

The luxury packaging market size is projected to be USD 18.91 billion in 2025, USD 19.66 billion in 2026, and reach USD 24.17 billion by 2031, growing at a CAGR of 4.22% from 2026 to 2031. The steady headline growth conceals a deeper pivot in which premium brands now treat packaging as a revenue generator, not merely a protective shell. E-commerce sales of luxury goods overtook department-store volumes in 2025, turning the at-home unboxing event into a primary brand touchpoint. Europe remains the anchor geography, yet rising affluence in Asia-Pacific cities such as Chengdu and Bengaluru reshapes global design priorities toward ornate finishes and gifting suitability. Paper-based substrates advance fastest because retailers and regulators link fiber content with corporate emission targets, while intelligent closures carrying RFID or NFC chips become a compliance prerequisite as the European Union phases in product-passport rules.

Key Report Takeaways

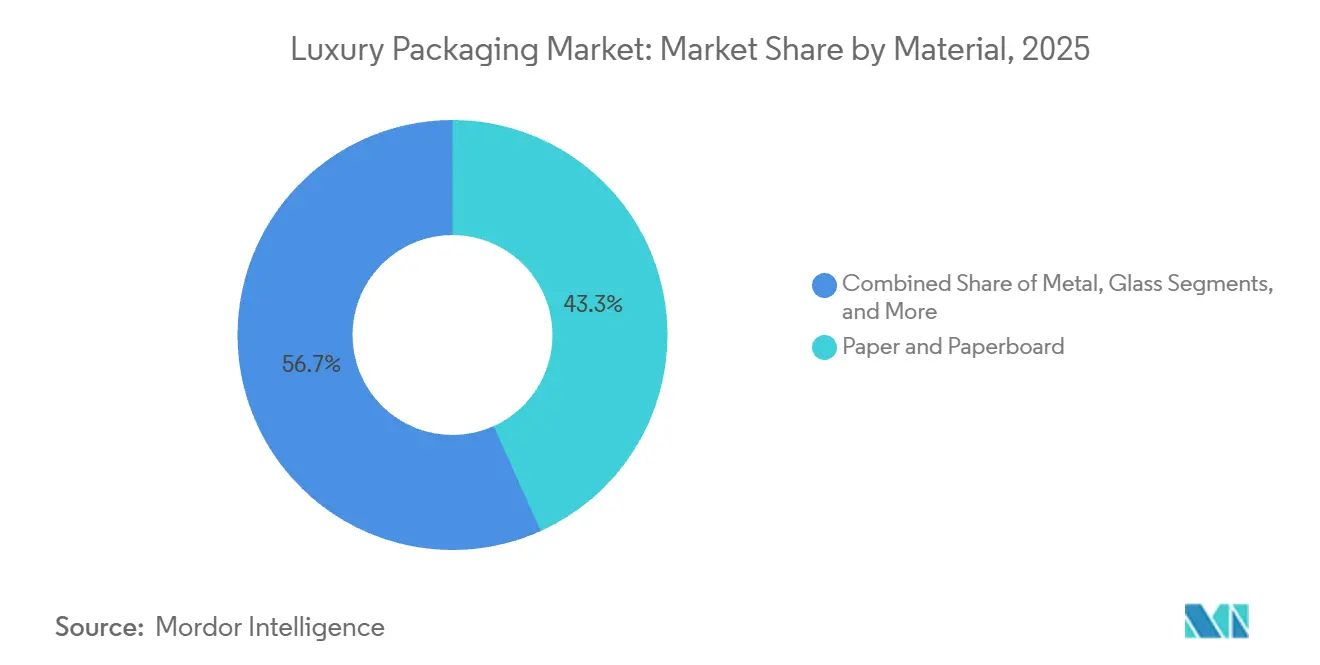

- By material, paper and paperboard led with 43.26% of the luxury packaging market share in 2025, whereas metalized grades delivered the highest 5.32% CAGR outlook toward 2031.

- By packaging format, the folding cartons and rigid boxes segment commanded a 41.19% share of the luxury packaging market size in 2025 and is projected to expand at a 5.62% CAGR through 2031.

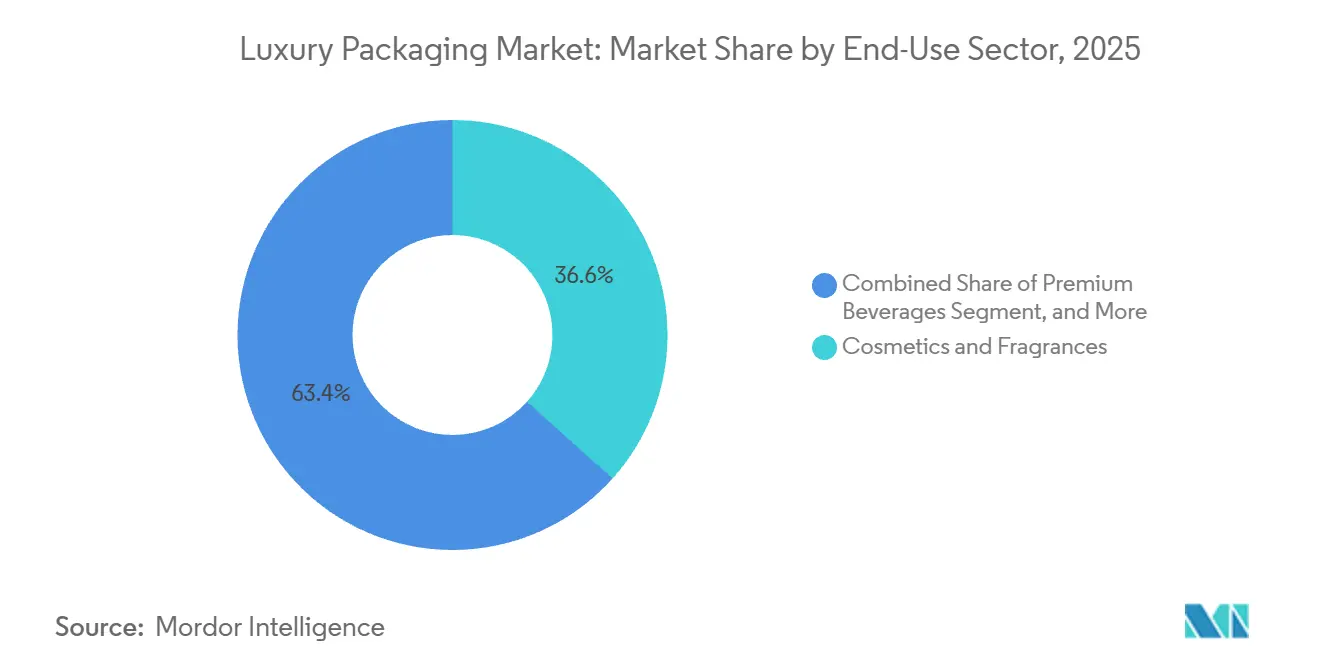

- By end-use sector, cosmetics and fragrances held 36.63% of the market share in 2025, while premium beverages recorded the fastest CAGR of 6.21% to 2031.

- By functionality, conventional luxury packaging accounted for 67.89% of the market share in 2025, though the smart and connected luxury packaging segment is poised to grow at a 5.81% CAGR through 2031.

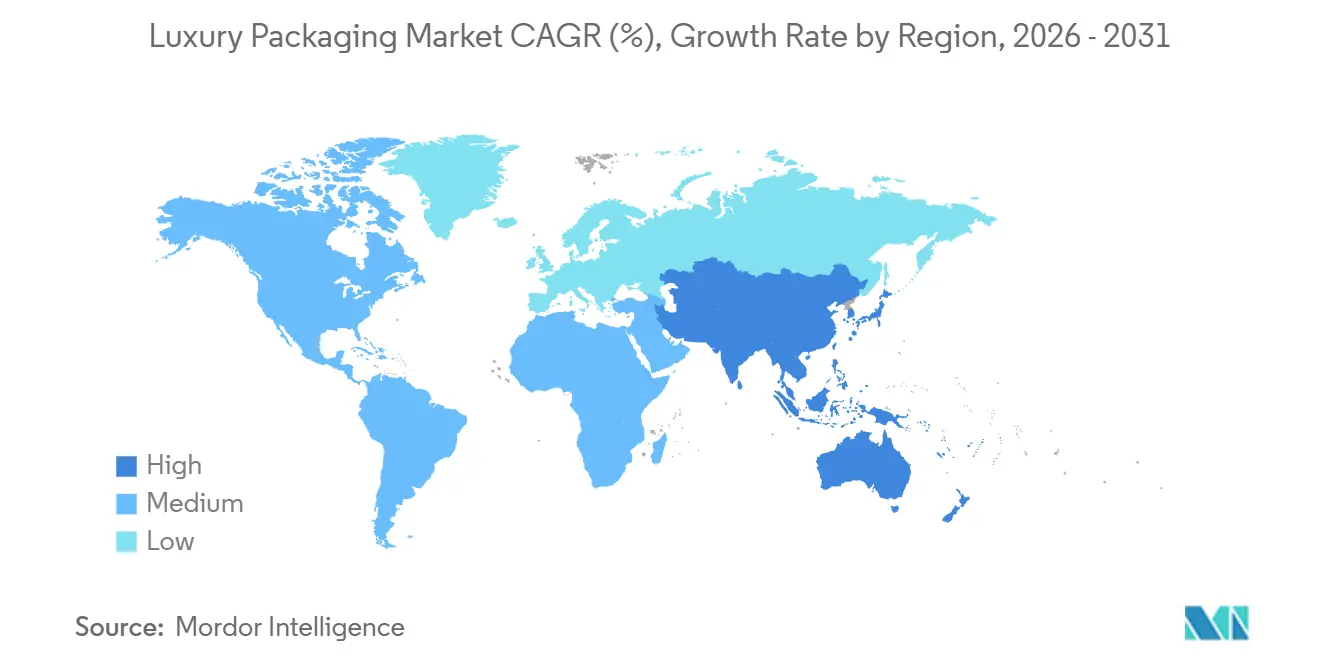

- By geography, Europe captured the largest 38.62% of the market share in 2025, yet Asia-Pacific is forecast to register a 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Luxury Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-Driven Demand for Premium Unboxing | +1.2% | Global, strongest in North America, Europe, Asia-Pacific tier-one cities | Short term (≤ 2 years) |

| Sustainability and Shift to Bio-based Materials | +0.9% | Europe and North America leading, Asia-Pacific following | Medium term (2-4 years) |

| Rising Disposable Income in Emerging Markets | +0.8% | Asia-Pacific core plus Middle East gifting hubs | Medium term (2-4 years) |

| Smart Authentication Packaging (NFC/RFID) | +0.6% | Early adoption in Europe and North America, global scalability | Long term (≥ 4 years) |

| Travel-Retail Premiumisation Boom | +0.4% | Hub airports in Middle East, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Artist-Brand Limited-Edition Collaborations | +0.3% | North America, Europe, select Asia-Pacific metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Demand for Premium Unboxing

Online luxury sales already account for nearly one-third of category revenue, pulling packaging into the spotlight as the digital sales associate. Social-media feeds amplify every tactile cue, so converters now engineer magnetic closures that click audibly and inserts that stage a multi-step reveal. Spirits houses deploy double sleeves that slow the opening sequence, extending dwell time on user-generated videos and reinforcing perceived exclusivity. High customer-acquisition costs in direct-to-consumer channels justify spending an incremental USD 1-2 per unit on presentation features because repeat-purchase intent rises when the unboxing moment delights. Brand teams consequently prioritize rigid-box specifications over flexible pouches since dimensional stability photographs better and withstands parcel handling without creasing.

Sustainability and Shift to Bio-Based Materials

The European Union Packaging and Packaging Waste Regulation obliges converters to deliver ever-higher recycled content thresholds, accelerating the transition from polyethylene liners to water-based barrier coatings that are compatible with curbside collection.[1]European Commission, “Packaging and Packaging Waste Regulation,” ec.europa.eu Paperboard mills in Italy and Germany commissioned new dispersion-coat lines in 2025, allowing chocolate and skincare brands to retain moisture and oxygen barriers while removing plastic. Chanel disclosed that switching to FSC-certified fiber and soy-based inks raised its unit packaging cost by 14% but also improved sell-through among environmentally minded customers in Scandinavia. Although some heritage maisons worry about matte aesthetics, converters continue to refine gloss additives derived from algae and corn starch that mimic the sheen of virgin plastic without compromising recyclability.

Rising Disposable Income in Emerging Markets

Disposable income rose 6.8% in China during 2025, with the fastest gains in inland cities that prize ornate presentation during gifting festivals. India added 11.2% more ultra-high-net-worth individuals in the same year, elevating demand for bespoke rigid boxes wrapped in fabric or leatherette. Unlike minimalism-oriented Western consumers, these buyers infer value from heavier substrates and metallic foils, prompting global brands to maintain dual stock-keeping-unit strategies. Converters located near Shenzhen and Mumbai report order volumes for multi-layered constructions increasing 18-20% year on year despite higher freight surcharges. The divergence forces multinational supply chains to hold parallel inventory sets, increasing working capital requirements but unlocking incremental revenue that offsets the complexity.

Smart Authentication Packaging (NFC/RFID)

Counterfeit luxury goods eroded roughly USD 98 billion in branded sales during 2024, making digital traceability a board-level priority. Diageo embedded NFC tags inside closures of its Johnnie Walker Blue Label, allowing owners to tap a smartphone and verify source data stored on a blockchain ledger.[2]Diageo plc, “Annual Report 2025,” diageo.com Early adopters capture consumer-engagement metrics when the tap event also unlocks tasting notes or refill-ordering portals. Unit cost for encrypted tags fell to a USD 0.40-1.20 band during 2025, and learning curves across semiconductor fabs signal further declines. The European Union Digital Product Passport program, starting in 2026, will mandate such traceability for multiple categories, effectively pushing smart-tag adoption from an optional premium to a legal requirement across luxury cosmetics and spirits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Premium Substrates and Finishes | -0.7% | Global, acute in Europe manufacturing corridors | Short term (≤ 2 years) |

| Regulatory Pressure on Single-Use Materials | -0.5% | Europe and North America first movers, Asia-Pacific next wave | Medium term (2-4 years) |

| Reluctance to Package Heavy or Bulky Items | -0.3% | Global e-commerce operations | Medium term (2-4 years) |

| Counterfeit-Proof Tech Complexity and Cost | -0.2% | Higher impact in emerging markets with limited infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Premium Substrates and Finishes

Natural-gas price shocks lifted production costs for metalized paperboard by 16% and embossed glass by 14% in 2025, squeezing margins for mid-tier fragrance lines.[3]Ardagh Group, “Annual Report and Accounts 2025,” ardaghgroup.com Specialty finishes such as hot-foil stamping add USD 2,000-8,000 in plate fees per stock-keeping unit, deterring small-batch seasonal launches. Brands responded by trimming assortment breadth, a move that moderates novelty but preserves gross margin. Integrated converters that own both substrate and finishing assets can shield clients from multi-vendor mark-ups, enabling them to increase contract pricing by 8-12% without losing business. While material inflation has cooled slightly since Q4-2025, premium substrates remain vulnerable to energy swings, keeping cost discipline at the top of brand agendas.

Regulatory Pressure on Single-Use Materials

France banned plastic inserts in cosmetic boxes during 2025, and Germany raised producer-responsibility fees 22% for non-recyclable components, penalizing classic nested constructions. The United Kingdom plastic-packaging levy, applied at GBP 210.82 per metric ton on formats with less than 30% recycled content, added GBP 18 million in aggregate costs across the British luxury sector last year. Brands that shifted to mono-material paperboard avoided most fees and won positive coverage in Scandinavian media, a region where eco-labels strongly influence purchase decisions. Because the European rule set remains fragmented, global converters must navigate multiple certificate regimes, raising compliance overhead yet also rewarding early movers that can document closed-loop design credentials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Paper And Paperboard Extend Leadership

Paper and paperboard secured 43.26% of luxury packaging market share in 2025 and are on track for a 5.32% CAGR through 2031. This forward momentum reflects corporate commitments to eliminate virgin plastic by 2030 coupled with consumer appreciation for tactile substrates that feel environmentally responsible. The luxury packaging market size allocated to glass hovered near 23% because prestige fragrance houses prize inertness and heft, but thin-wall light-weighting initiatives limit future acceleration. Metal, primarily food-grade aluminum for spirits tins and aerosol cans, accounts for roughly one-fifth of the revenue pool, helped by its infinite-recyclability narrative that resonates in North American regulatory filings. Plastics remain indispensable in squeezable tubes and transparent jars despite reputational risk, though bio-sourced cellulose films commercialized in 2025 promise compostability within 90 days. Niche materials such as wood and fabric serve ultra-premium watch boxes where unit prices exceed USD 50, a small yet stable segment insulated from commodity cost swings.

Converters increasingly apply barrier coatings made from corn-starch derivatives that deliver oxygen-transmission rates below 1 cc/m²/day, opening paperboard to chocolate and skincare again. Foldable pulp inserts replace polystyrene vac-forms, enabling mono-material recyclability without sacrificing product fixation. European mills running biomass-fired boilers further cut embedded carbon, a metric that luxury conglomerates now score in supplier audits. The rapid iteration cycle of paper substrate improvements contrasts with the longer asset refresh timelines in glass or metal, giving fiber-based producers a structural innovation advantage through the forecast window.

By Packaging Format: Rigid Box Architecture Drives Value Perception

Folding cartons and rigid boxes represented 41.19% of the luxury packaging market in 2025 and carry a 5.62% CAGR outlook. Their modular architecture ships flat, reducing logistics cost by up to 40%, yet assembles into high-impact structures once filled. Magnetic closures and hidden ribbon pulls communicate craftsmanship that supports 25-35% retail-price premiums versus flexible alternatives. Pouch formats held close to 19% share, favored in duty-free channels where weight savings matter most, but constrained by inconsistent recycling streams outside Europe. Tubes and jars, roughly 17% share, remain the workhorse of prestige skincare because they control dosage and resist leakage, helping brands meet shelf-life guarantees.

Bottle and vial suppliers introduced reinforced-base designs that shave 18% off gram weight while retaining 100 ml capacity, responding to transport-emission targets without compromising break resistance. Secondary elements such as slip sleeves and bellybands serve tamper evidence and marketing copy, yet brands increasingly print QR codes instead of product inserts, collapsing material layers. Converters offering end-to-end design, print, and assembly win share because they shorten launch lead times from 16 weeks to under 10 days, a speed advantage critical when TikTok trends can fade in a month.

By End-Use Sector: Cosmetics Anchor, Beverages Surge

Cosmetics and fragrances absorbed 36.63% of the market share in 2025, a dominance fueled by continual product refresh cycles and a cost-of-goods structure that tolerates packaging accounting for 15-20% of the final retail price. The luxury packaging market for premium beverages is smaller in volume but posts the fastest 6.21% CAGR, as aged whiskies and limited-batch gins position packaging as a collectible artifact. Pernod Ricard disclosed a 19% increase in presentation-case expenditure for its flagship cognac line in 2025, evidence that elaborate packaging serves as a gifting trigger. Watches and jewelry maintain a mid-teens share, requiring anti-tarnish linings and lockable clasps, which push unit-packaging costs well above category averages.

Fashion accessories significantly contribute to fiber demand, with items like handbag dust bags, and reinforced shoe boxes playing a key role. Confectionery packaging, particularly for seasonal assortments, often utilizes rigid trays to maintain product quality and separation. Electronics and home décor represent a fragmented segment, characterized by varying order sizes and design requirements, highlighting the importance of digital printing for small production runs without high setup costs.

By Functionality: Smart Solutions Gain Ground

Conventional substrates still hold 67.89% of the market share in 2025 because visual and tactile cues alone once signaled authenticity. Yet counterfeit rings now replicate embossing and foil stamping cheaply, prompting brands to embed electronics that cannot be faked by eyesight. Smart and connected variants occupied 32.11% last year and will gain steadily at a 5.81% CAGR as NFC chip prices drop and as regulators standardize data-sharing protocols. LVMH reported that 22% of its fragrance packaging carried an NFC element by end-2025, up from single-digits in 2023, underscoring accelerating scale. Hybrid designs keep antennas invisible by printing conductive ink within traditional graphics, avoiding compromises in shelf aesthetics.

Cost sensitivity remains the drag on universal adoption. However, technology vendors now offer subscription analytics platforms bundled with tag hardware, letting brands offset upfront expenditure through consumer-insight dashboards. As blockchain-backed authenticity becomes a resale prerequisite, even mid-tier labels will have little choice but to upgrade conventional cartons or risk marketplace exclusion.

Geography Analysis

Europe accounted for 38.62% of luxury packaging market in 2025, supported by clusters of heritage cosmetic houses in Paris, fashion ateliers in Milan, and Scotch distilleries in Scotland. The region’s mid-single-digit growth reflects regulatory friction and consumer maturity, yet proximity to brand headquarters confers design-collaboration advantages that overseas suppliers struggle to match. France and Italy together generated over 60% of regional volume, with many houses sourcing paperboard from mills within a 500-km radius to satisfy Scope 3 emission audits.

Asia-Pacific is projected to have the fastest 6.08% CAGR through 2031. Rising affluence in tier-two Chinese cities and across India’s tech corridors enlarges the customer base that regards ornate boxes as integral to the gift, not just its container. Converter capacity in Guangdong and Zhejiang operates near full utilization, incentivizing Crown Holdings to purchase a premium glass plant in the region during 2026, thereby localizing supply for spirits brands. E-commerce penetration accelerates the adoption of robust, rigid formats that can survive parcel networks without deformation, favoring thicker boards and multiple sleeves.

North America is expected to grow steadily, driven by direct-to-consumer channels where unboxing serves as the first physical interaction with a brand. Consumers in the United States increasingly favor refillable or mono-material packaging, making suppliers with relevant certifications more appealing for premium contracts. The Middle East benefits from travel-retail and gifting traditions, while South America and Africa face challenges due to infrastructure limitations that hinder the adoption of advanced technologies like smart tags.

Competitive Landscape

The market is moderately fragmented. Ardagh Group, Owens-Illinois, and Crown Holdings defend glass and metal niches through long-term agreements with beverage and fragrance multinationals, leveraging scale to hedge raw-material volatility. Paperboard leaders such as Smurfit WestRock and James Cropper compete on sustainability credentials, offering fiber validated for chain-of-custody and barrier properties that meet upcoming European thresholds.

White-space opportunities center on smart-packaging integration, where electronics knowledge is scarce among legacy converters. Technology firms partner with substrate makers to deliver turnkey NFC or RFID solutions, capturing margin that once flowed solely to printers. Digital-printing players like GPA Global threaten traditional offset volumes by supporting 500-unit limited editions without plate costs, enabling influencer collaborations that demand rapid design turnovers. Patent activity highlights a pivot toward bio-barrier coatings and mono-material construction, with Fedrigoni’s cellulose-acetate film winning European Patent Office approval for compostability within 12 weeks.

Supply-chain resilience now trumps absolute capacity. Brands require secondary sources across at least two continents to mitigate logistics disruption, prompting global converters to acquire regional players. Cost, speed, and environmental proof points combine into a three-legged competitive bar that incumbents must clear to retain share during the forecast window.

Luxury Packaging Industry Leaders

GPA Global Holdings B.V.

Delta Global Source (UK) Limited

Keenpac (Bunzl UK Limited)

McLaren Packaging Ltd.

Fedrigoni S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Smurfit WestRock committed EUR 120 million (USD 135.6 million) to expand Italian luxury paperboard output with water-based coating lines targeting cosmetics and confectionery.

- January 2026: Crown Holdings acquired a specialty glass plant in Guangdong, China for USD 78 million to serve Asia-Pacific premium spirits demand.

- December 2025: LVMH disclosed that recycled content reached 35% across its cosmetics and fragrance packaging, pledging 50% by 2028.

- November 2025: Diageo rolled out blockchain-enabled NFC closures for Johnnie Walker Blue Label, logging 1.2 million consumer taps in the first month.

Global Luxury Packaging Market Report Scope

Luxury packaging refers to high-end packaging solutions designed to elevate product perception and create a premium brand image. It involves the use of high-quality materials, intricate designs, and sophisticated finishes to appeal to discerning consumers and often incorporates elements such as embossing, debossing, foil stamping, and unique shapes.

The Luxury Packaging Market Report is Segmented by Material (Paper and Paperboard, Glass, Metal, Plastics, and Other Materials), Packaging Format (Folding Cartons and Rigid Boxes, Flexible Pouches and Bags, Tubes and Jars, Bottles and Vials, and Other Packaging Formats), End-Use Sector (Cosmetics and Fragrances, Confectionery and Gourmet Food, Watches and Jewellery, Premium Beverages, Fashion and Accessories, and Other End-Use Sectors), Functionality (Conventional Luxury Packaging, and Smart/Connected Luxury Packaging), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Paper and Paperboard |

| Glass |

| Metal |

| Plastics |

| Other Materials |

| Folding Cartons and Rigid Boxes |

| Flexible Pouches and Bags |

| Tubes and Jars |

| Bottles and Vials |

| Other Packaging Formats |

| Cosmetics and Fragrances |

| Confectionery and Gourmet Food |

| Watches and Jewellery |

| Premium Beverages |

| Fashion and Accessories |

| Other End-Use Sectors |

| Conventional Luxury Packaging |

| Smart / Connected Luxury Packaging |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material | Paper and Paperboard | ||

| Glass | |||

| Metal | |||

| Plastics | |||

| Other Materials | |||

| By Packaging Format | Folding Cartons and Rigid Boxes | ||

| Flexible Pouches and Bags | |||

| Tubes and Jars | |||

| Bottles and Vials | |||

| Other Packaging Formats | |||

| By End-Use Sector | Cosmetics and Fragrances | ||

| Confectionery and Gourmet Food | |||

| Watches and Jewellery | |||

| Premium Beverages | |||

| Fashion and Accessories | |||

| Other End-Use Sectors | |||

| By Functionality | Conventional Luxury Packaging | ||

| Smart / Connected Luxury Packaging | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global demand for premium paperboard growing?

Paper and paperboard capture 43.26% of luxury packaging market share in 2025 and are forecast to advance at a 5.32% CAGR through 2031 as brands replace plastic liners with recyclable fiber-based barriers.

Which packaging format delivers the highest value perception to online shoppers?

Rigid boxes with magnetic closures dominate because their dimensional stability withstands parcel networks and their layered opening sequence generates shareable social-media content.

Why are spirits producers investing in smart closures?

Embedded NFC tags authenticate provenance, enable blockchain traceability demanded by regulators, and create post-purchase engagement that boosts brand loyalty.

What regulatory change will most influence material choice by 2030?

The European Union Packaging and Packaging Waste Regulation sets escalating recycled-content thresholds and design-for-disassembly rules that favor mono-material, fibre-rich constructions.

Page last updated on: