Flower Seeds Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

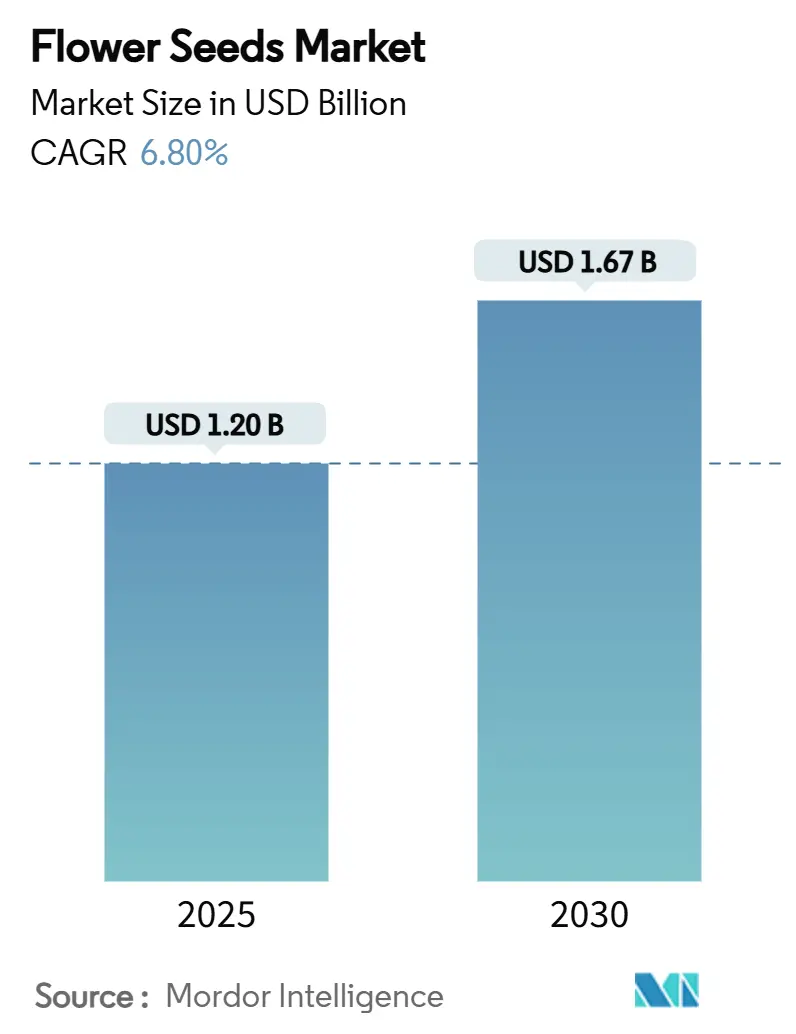

| Market Size (2025) | USD 1.20 Billion |

| Market Size (2030) | USD 1.67 Billion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

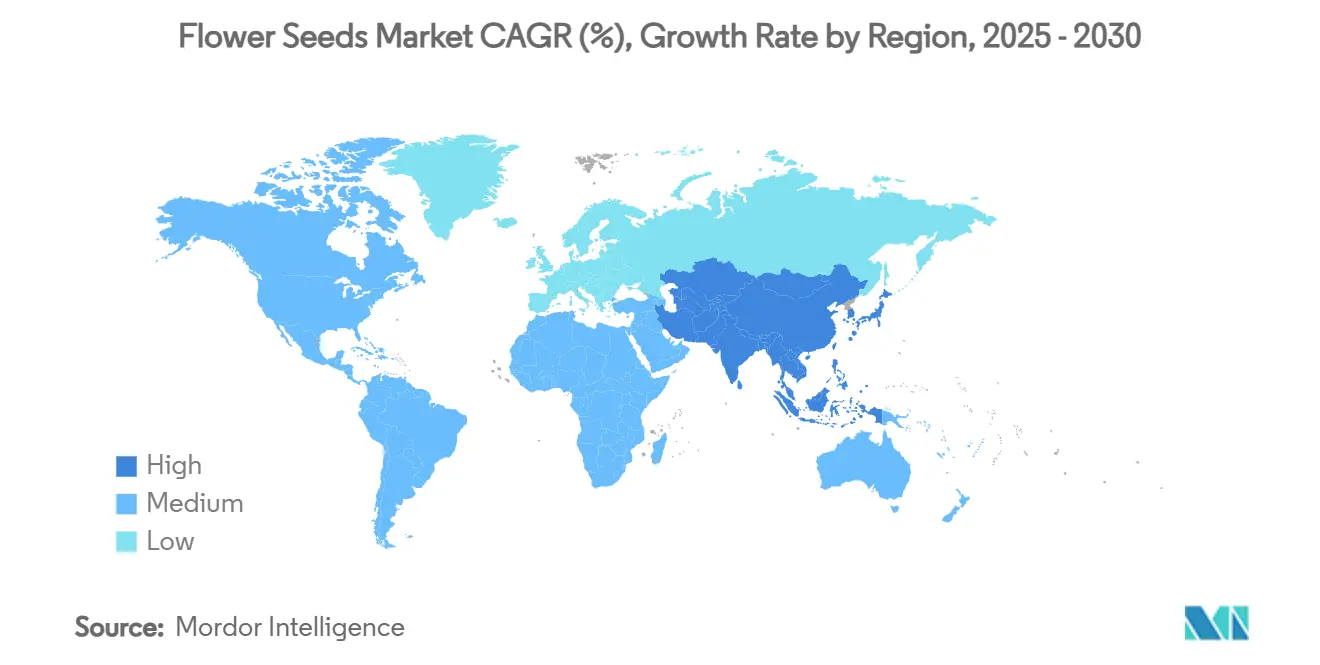

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flower Seeds Market Analysis by Mordor Intelligence

The global flower seeds market attained a market size of USD 1.20 billion in 2025 and is estimated to advance to USD 1.67 billion by 2030, reflecting a CAGR of 6.8% over the forecast period. Macroeconomic recovery, climate-smart landscaping policies, and the digitalization of retail are steering steady value creation across producer and consumer economies. Asia-Pacific provides the fastest-growing demand pool, while Europe retains the largest regional foothold due to mature distribution systems and robust pollinator support programs. Product differentiation is intensifying as breeders combine molecular tools with traditional crossing to extend blooming duration, improve drought tolerance, and create novel color lines. On the commercial side, greenhouse operators are pursuing energy-efficient lighting and climate control to counter volatile utility costs, while residential consumers shift toward compact cultivars suitable for limited urban spaces. Online platforms that curate subscription boxes and provide agronomic guidance are scaling quickly, capturing new entrants to hobby gardening and reshaping customer acquisition economics across the flower seeds market.

Key Report Takeaways

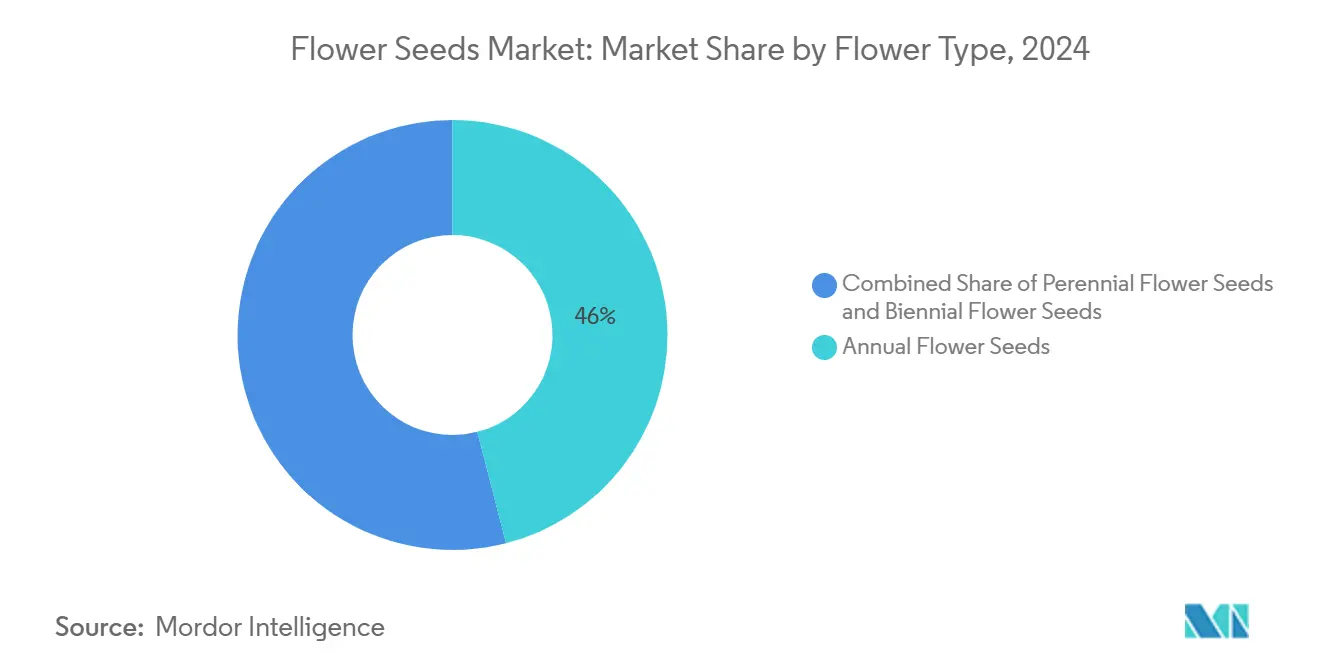

- By flower type, annual varieties led with 46% flower seeds market share in 2024, whereas perennial varieties are forecast to expand at a 7.5% CAGR through 2030.

- By seed type, open-pollinated products accounted for 57% of the flower seeds market size in 2024, and hybrid offerings are projected to grow at a 7.0% CAGR through 2030.

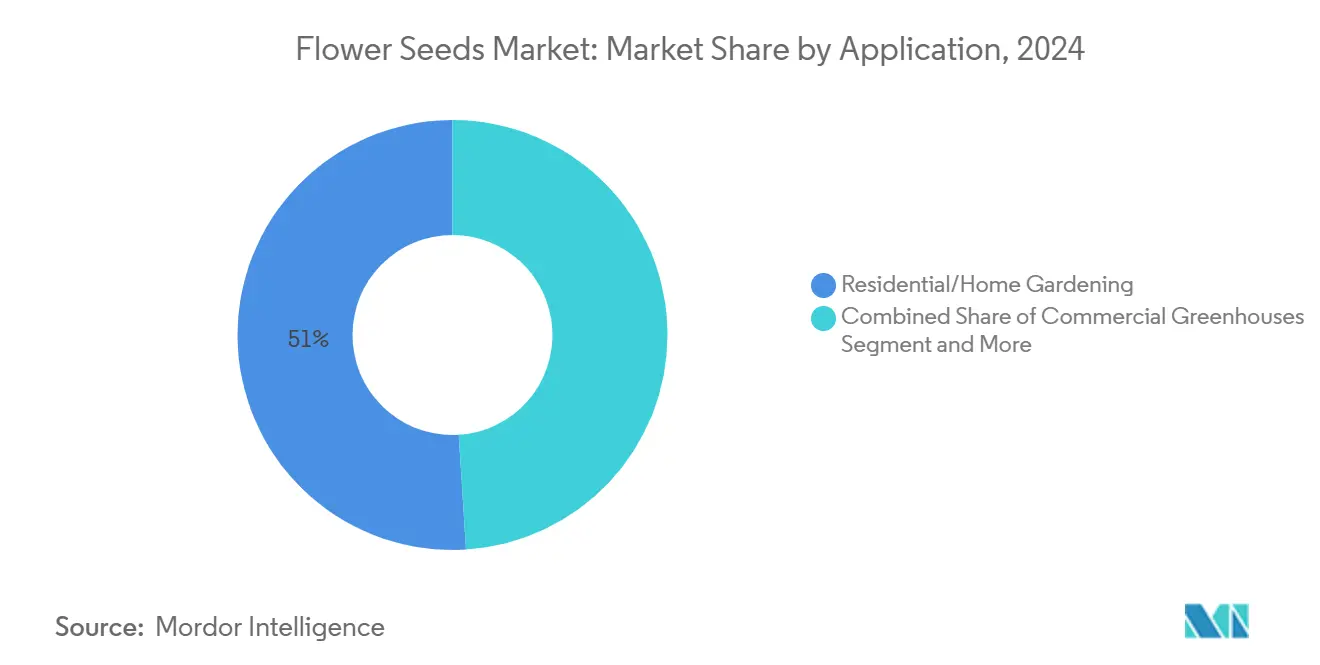

- By application, the residential segment accounted for 51% of 2024 revenue, while commercial greenhouses represented the fastest trajectory, with a 7.7% CAGR through 2030.

- By distribution channel, offline retail retained a 61% revenue share in 2024, while online retail is advancing at a 9.2% CAGR through 2030.

- By geography, Europe captured 32% of the 2024 value, and Asia-Pacific is on track to post a 7.9% CAGR up to 2030.

- Ball Horticultural Company and Syngenta Group together commanded 26% combined market share in 2024, underscoring a moderately concentrated competitive field.

Global Flower Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate-resilient ornamental landscaping demand | +1.2% | North America and Europe, growing uptake in Asia-Pacific | Medium term (2-4 years) |

| Rising disposable income driving gardening as a hobby | +1.5% | Asia-Pacific core and spill-over into emerging African markets | Long term (≥ 4 years) |

| Growth of urban rooftop and vertical gardens | +0.8% | Global megacities led by Asia-Pacific | Medium term (2-4 years) |

| Expansion of online seed subscription models | +0.6% | North America and Europe with rapid rollout in Asia-Pacific | Short term (≤ 2 years) |

| Hybrid seed innovation for extended blooming | +0.9% | Concentrated in developed markets and adoption is spreading worldwide | Long term (≥ 4 years) |

| Government pollinator-support programs boosting flower plots | +0.7% | North America and Europe, nascent programs in the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Climate-Resilient Ornamental Landscaping Demand

Municipal authorities and corporate estate managers increasingly specify drought-tolerant flowering mixes to address water-scarcity mandates. Species such as butterfly weed and blue vervain are being blended into public-space seed mixes to boost ecosystem services while curbing irrigation budgets[1]Natural Resources Conservation Service, “Pollinator Habitat Establishment,” usda.gov. Procurement frameworks that award credits for pollinator-friendly plantings reinforce recurring orders, allowing suppliers to expand native seed lines at scale. Research into nature-based solutions also portrays flowering strips as effective stormwater mitigators, a finding that elevates their role in urban infrastructure investment planning.

Rising Disposable Income Driving Gardening as a Hobby

Inflation-adjusted wage gains across China, India, and Indonesia have lifted discretionary spending, turning home gardening into an affordable lifestyle upgrade. Social media-driven aesthetics, particularly balcony makeovers, amplify demand for visually impactful hybrid marigolds and zinnias. Government conservation programs such as the New England Pollinator Partnership provide liability protection for participating gardeners, further incentivizing private flower plots[2]Natural Resources Conservation Service, “Pollinator Habitat Establishment,” usda.gov. Higher spending power also translates into a willingness to purchase value-added seed coatings that improve germination.

Expansion of Online Seed Subscription Models

Direct-to-consumer portals capture beginner gardeners by bundling seasonal assortments with how-to guides. Integrated data analytics provide region-specific cultivar recommendations, driving repeat purchase rates above traditional retail averages. With freight costs normalizing to pre-pandemic levels, e-commerce platforms have regained gross-margin leverage, allowing competitive price promotions that offline stores struggle to match.

Hybrid Seed Innovation for Extended Blooming

Breeders apply MiMe (mitosis instead of meiosis) technology to generate genetically identical hybrids that retain vigor across propagation cycles, thus lowering production costs while sustaining trait expression. In 2024, studies on Torenia fournieri demonstrated successful betalain biosynthesis, which widens the ornamental color spectrum. Intellectual-property protection around such breakthroughs increases barriers to entry for smaller competitors but creates premium SKU opportunities for established firms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in commercial greenhouse energy costs | -0.8% | Europe and cold-climate North America | Short term (≤ 2 years) |

| Intellectual-property disputes on proprietary cultivars | -0.4% | North America, Europe, and Japan | Medium term (2-4 years) |

| Increasing preference for low-maintenance hardscapes | -0.6% | North America and Europe, budding in urban Asia | Long term (≥ 4 years) |

| Biosecurity regulations restricting seed trade | -0.5% | European Union, United States, and New Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Commercial Greenhouse Energy Costs

Natural gas price volatility has significantly increased operating costs for greenhouse growers in Denmark, the Netherlands, and other northern European regions, where controlled-environment cultivation is critical for seed production. Higher heating demands during extended winters have led growers to reduce or delay the expansion of their greenhouse capacity. While LED retrofits can lower long-term energy consumption, the high initial investment, often financed at higher interest rates, places financial pressure on smaller seed producers, reducing profit margins and limiting operational flexibility.

Intellectual-Property Disputes on Proprietary Cultivars

As breeders increasingly patent novel traits, cross-licensing disputes have become more frequent, particularly when hybrid performance relies on gene-edited characteristics. These legal conflicts consume substantial time and resources, diverting R&D budgets toward litigation instead of innovation. The resulting delays in commercial releases erode first-mover advantages in a market where seasonal timing is crucial. Smaller seed firms, often lacking dedicated intellectual property teams, are especially vulnerable and frequently adopt white-label or contract production models to mitigate legal risks. While this approach enables them to remain operational, it restricts their ability to establish brand recognition and fully capitalize on their proprietary germplasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flower Type: Annual Versus Perennial Dynamics

Annual seeds delivered 46% of 2024 revenue within the flower seeds market, benefiting from fast cultivation cycles that align with beginner gardener preferences and promotional retail calendars. In contrast, perennial seeds exhibited the strongest growth trajectory with a 7.5% CAGR, reflecting consumer appetite for low-maintenance gardens that offer multi-year aesthetics. Biennial offerings remain a niche for experienced enthusiasts seeking dual-season bloom performance.

Perennials also intersect with sustainability mandates because their deep root systems improve soil structure and carbon sequestration, making them a favored component of municipal planting tenders. Conversely, annuals retain an edge in the gift-flower channel due to their vibrant color palette and compatibility with container formats.

By Seed Type: Open-Pollinated Stability Against Hybrid Acceleration

Open-pollinated seeds accounted for 57% of the 2024 flower seeds market size, upheld by heritage gardeners who value seed-saving traditions and genetic diversity. The hybrid segment, however, is expanding at a 7.0% CAGR to 2030, propelled by demonstrated yield advantages, disease resistance, and prolonged bloom windows. MiMe-enabled propagation promises to lower the cost of producing uniform hybrid lines, signaling potential margin enhancement for vertically integrated producers.

Certified organic growers often rely on open-pollinated seed to meet regulatory thresholds for genetic diversity, yet rising pest pressure is nudging some operators toward hybrid varieties coated with biofungicides. Intellectual-property protections around cutting-edge genetics grant incumbents premium pricing power, though they simultaneously raise stewardship obligations under international treaties. Suppliers able to balance open-pollinated breadth with hybrid depth are better positioned to capture wallet share across the fragmented customer spectrum of the flower seeds market.

By Application: Residential Leadership and Commercial Greenhouse Momentum

Residential gardening accounted for 51% of the market share in 2024 turnover, reflecting a pandemic-era surge in home beautification that has transitioned into a steady leisure pursuit. The commercial greenhouse segment, while smaller, is on pace for a 7.7% CAGR through 2030 as retailers demand year-round supply consistency and ornamental quality. Public parks and institutional plantings contribute a stable baseline demand anchored by policy targets for biodiversity corridors.

Application trends also highlight the growing role of landscaping projects in residential complexes, hotels, and corporate campuses, where demand for diverse flower varieties is rising to enhance aesthetic appeal and environmental value. Educational institutions and botanical gardens are incorporating the use of flower seeds into their sustainability programs, promoting awareness of native and pollinator-friendly species. Meanwhile, urban greening initiatives, such as roadside plantings and rooftop gardens, are expanding the scope of flower seed application beyond traditional home or greenhouse settings, reinforcing the market’s long-term relevance across both private and public spaces.

By Distribution Channel: Offline Resilience Amid Digital Surges

Offline retail retained 61% revenue share in 2024, underpinned by entrenched consumer habits and the tactile nature of seed selection at garden centers. However, online retail is expanding at a 9.2% CAGR, reshaping the path-to-purchase with doorstep delivery and algorithm-driven personalization. Wholesale and bulk procurement channels remain indispensable for landscapers and municipal clients that buy in volume, yet even these professional segments are beginning to experiment with web-based ordering portals.

Channel dynamics also reflect the growing importance of specialty nurseries and cooperative outlets, which cater to niche preferences such as organic, heirloom, or native flower seeds. Supermarkets and home improvement chains are increasingly dedicating shelf space to branded seed packets, enhancing visibility among casual buyers. At the same time, hybrid retail models such as click-and-collect services are bridging the gap between traditional and digital channels, offering convenience while retaining the reassurance of physical inspection. These evolving formats are strengthening the market’s ability to reach both hobbyist gardeners and institutional buyers.

Geography Analysis

Europe commanded a 32% share of the global flower seed market in 2024, supported by its longstanding horticultural tradition and favorable policy frameworks, such as subsidies for establishing nectar-rich flowers along farmland margins. The regional market is projected to grow at a CAGR of 4.9% through 2030, driven by replacement demand for climate-resilient cultivars amid overall market saturation. While the region’s revised phytosanitary regulations introduce stricter compliance requirements, they are projected to enhance consumer confidence in seed quality over time. [3]Source: European Commission, “Plant Health Law 2025 Guidance,” ec.europa.eu

Asia-Pacific is projected to register the highest CAGR of 7.9% by 2030. This growth is fueled by accelerating urbanization and an expanding middle class that is increasingly embracing gardening as a cost-effective leisure activity. The region also benefits from flexible labor availability and relatively relaxed regulatory environments, enabling quicker product rollouts, particularly through e-commerce platforms that bypass traditional retail constraints.

North America grows at a steady rate, supported by the United States Department of Agriculture (USDA’s) Specialty Crop Block Grant Program and private-sector investment in controlled-environment agriculture. The collective momentum keeps the flower seeds market on a globally diversified trajectory. North America balances a robust consumer gardening culture with significant institutional demand. Federal grants channeled through state agriculture departments support floriculture research on pest management and sustainable growth media, indirectly benefiting seed suppliers.

Competitive Landscape

The flower seed market displays moderate concentration with the top five suppliers controlling a significant revenue share, leaving meaningful whitespace for niche specialists. Ball Horticultural Company holds a prominent position, supported by production hubs across Costa Rica, Guatemala, and Chile that supply 8,000 greenhouse growers and 17,000 garden centers across North America. Syngenta Group maintains a strong presence and has recently refocused its strategy on core ornamental genetics following the divestment of its FarMore vegetable seed treatment platform to Gowan SeedTech.

Japanese incumbents Sakata Seed Corporation and TAKII & CO.,LTD. utilize their proximity to Asia-Pacific growth markets and leverage their standing breeding pedigrees to reinforce regional dominance. German family-owned Benary exports 90% of its output to more than 120 countries, thereby solidifying its presence in the premium bedding plant segment. Strategic priorities across leaders include the vertical integration of supply chains, the deployment of genetic editing, and the acceleration of direct-to-consumer initiatives.

Acquisition appetite is intensifying, mainstream ag-inputs players eye ornamental seeds as a diversification route in response to slowing row-crop demand. The expansion of the agricultural biologicals sector further supports this approach, as adjacent biocontrol solutions enhance the value offered to ornamental growers seeking alternatives to conventional pesticides. Market entrants focusing on climate-resilient and ppollinator-friendlycultivars can still differentiate ithemselves n this competitive landscape, provided they aachievereliable distribution or digital reach.

Flower Seeds Industry Leaders

Ball Horticultural Company (PanAmerican Seed)

Sakata Seed Corporation

Ernst Benary Samenzucht GmbH

Syngenta Group

TAKII & CO.,LTD.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Syngenta Group launched the Penny Pro Viola series at IPM Essen. The Viola cornuta "Penny Pro" series features robust plants with strong branching characteristics and requires reduced plant growth regulator (PGR) usage. The series, developed through advanced phenotyping techniques, is optimized for spring and autumn growing seasons.

- October 2024: Ball Seed released its 2025-2026 cut-flower catalog. The new two-year catalog features an expanded selection of seed varieties, including snapdragons and zinnias. The company provides additional support through its ColorLink service and on-demand resources to enhance production efficiency.

- October 2024: Syngenta Group announced the iCandy Begonia series, featuring five double-flowered varieties with rooted cuttings now available through United States brokers. The full launch is projected in 2026, reflecting Syngenta Group's continued investment in ornamental genetics amid growing demand for differentiated offerings in the flower seed market.

- May 2024: Syngenta Group established a technical sales team by appointing regional managers across India, with offices in Delhi, Uttarakhand, and Pune. The team conducts grower trials and provides support for pot and bedding seed to increase local market penetration.

Global Flower Seeds Market Report Scope

| Annual Flower Seeds |

| Perennial Flower Seeds |

| Biennial Flower Seeds |

| Open-Pollinated |

| Hybrid |

| Commercial Greenhouses |

| Residential/Home Gardening |

| Public Parks and Institutions |

| Offline Retail (Garden Centers, DIY Stores) |

| Online Retail |

| Wholesale/Bulk |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia and New Zealand | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Flower Type | Annual Flower Seeds | |

| Perennial Flower Seeds | ||

| Biennial Flower Seeds | ||

| By Seed Type | Open-Pollinated | |

| Hybrid | ||

| By Application | Commercial Greenhouses | |

| Residential/Home Gardening | ||

| Public Parks and Institutions | ||

| By Distribution Channel | Offline Retail (Garden Centers, DIY Stores) | |

| Online Retail | ||

| Wholesale/Bulk | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia and New Zealand | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the flower seeds market?

The flower seeds market is valued at USD 1.20 billion in 2025.

How fast will the flower seeds market grow through 2030?

It is forecast to post a 6.8% CAGR, reaching USD 1.67 billion by 2030.

Which region is expanding quickest?

Asia-Pacific is projected to lead growth with an 7.9% CAGR through 2030.

Which product segment dominates the flower seeds market share?

Annual flower seeds held 46% of revenue in 2024, making them the leading segment.

What channel is gaining traction for seed distribution?

Online retail is advancing rapidly at a 9.2% CAGR due to subscription-based and data-driven offerings.

Page last updated on: