Seed Binders Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

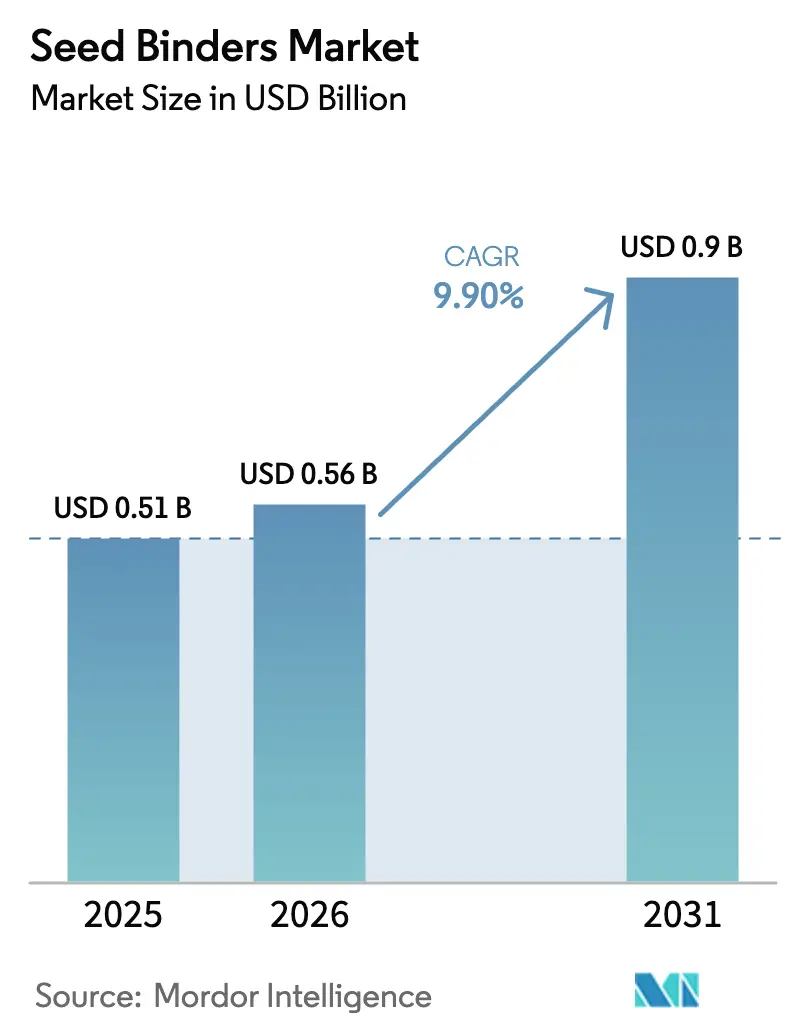

| Market Size (2026) | USD 0.56 Billion |

| Market Size (2031) | USD 0.9 Billion |

| Growth Rate (2026 - 2031) | 9.90% CAGR |

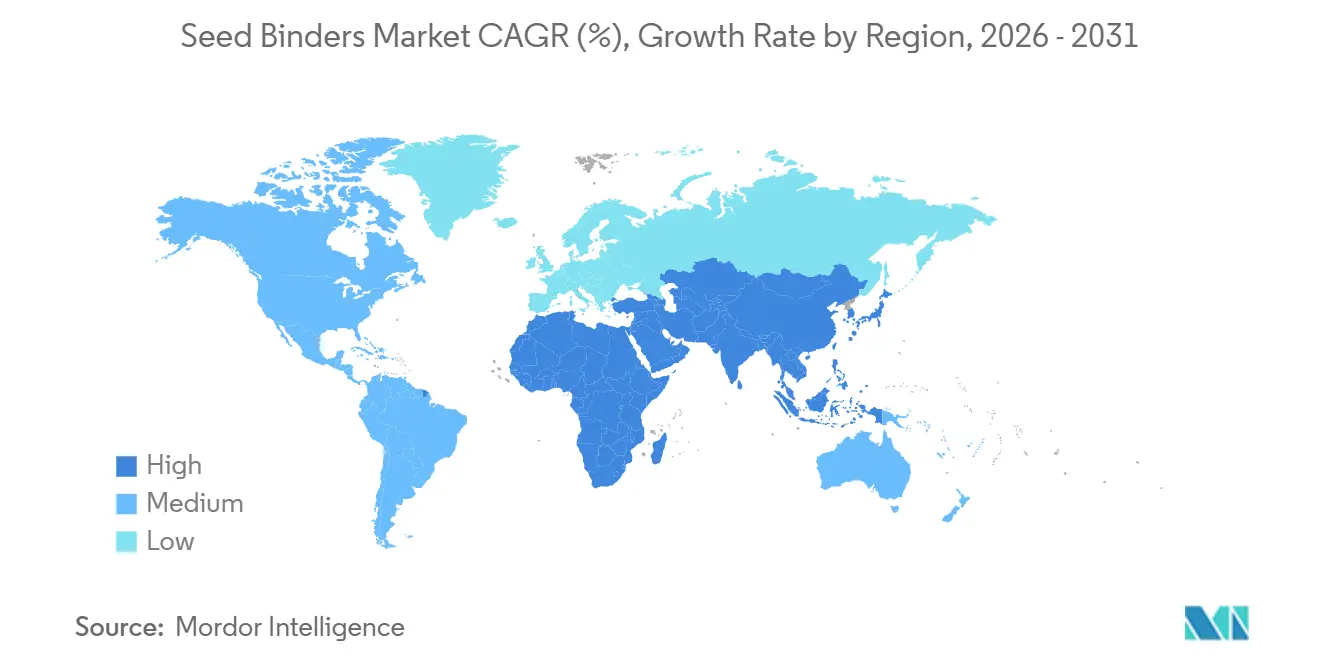

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

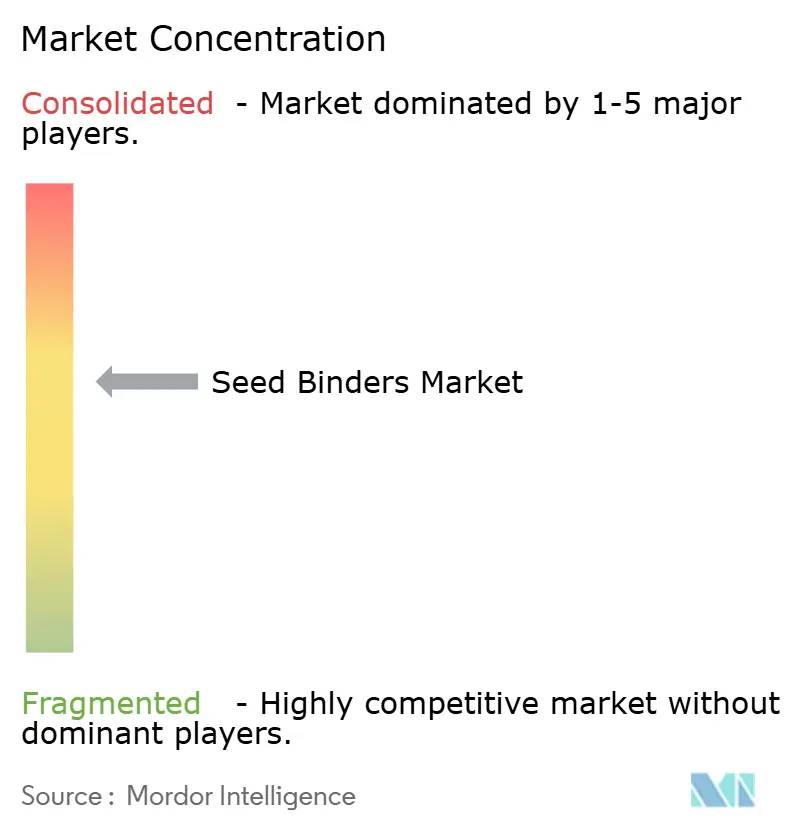

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seed Binders Market Analysis by Mordor Intelligence

The seed binders market size was valued at USD 0.51 billion in 2025 and estimated to grow from USD 0.56 billion in 2026 to reach USD 0.90 billion by 2031, at a CAGR of 9.9% during the forecast period (2026-2031). Demand acceleration comes from precision planting mandates, lower pesticide-loading allowances, and the spread of controlled-release micronutrient shells, all of which require stickier, cleaner coatings to keep inputs on the seed. Biopolymer platforms are moving faster than synthetics as growers, regulators, and investors treat carbon intensity and pollinator safety as procurement criteria rather than nice-to-have attributes. Strong early adoption in North America anchors revenue today, yet the next growth spurt is already visible in Asia-Pacific, where mechanization incentives and seed subsidies quicken the transition from raw seed to fully treated packets. Competitive intensity remains moderate because the leading five firms account for only a major share of market value in 2025, leaving headroom for regional specialists and bio-startups that can solve dust-off and adhesion problems at competitive costs.

Key Report Takeaways

- By product type, polyvinyl alcohol held 49% of the seed binders market share in 2025, while biopolymer-based binders are forecast to post a 12.11 % CAGR through 2031.

- By crop type, cereals and grains accounted for 44% of the seed binders market size in 2025, and fruits and vegetables are projected to expand at a 10.30 % CAGR between 2026 and 2031.

- By function, film coating led with a 47% share of the seed binders market in 2025, whereas encrusting is projected to grow at a 10.24% CAGR through 2031.

- By geography, North America accounted for 29.1% of the seed binders market in 2025, whereas Asia-Pacific is set to grow at a 10.2% CAGR between 2026 and 2031.

- BASF SE, Clariant AG, Incotec Group BV (Croda International plc), Bayer AG, and Michelman, Inc. together accounted for the majority share of the seed binders market size in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Seed Binders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of film-coated seeds in high-value horticulture | +1.8% | Global hubs with cluster activity in North America, Europe, and the Asia-Pacific vegetable belts | Medium term (2-4 years) |

| Precision planting driving demand for uniform seed geometry | +2.1% | North America and Europe lead, and Brazil and Argentina are scaling up | Short term (≤2 years) |

| Regulatory caps on pesticide loading per hectare | +1.5% | North America and Europe core, Asia-Pacific and the Middle East follow | Long term (≥4 years) |

| Commercial expansion of controlled-release micronutrient coatings | +1.3% | Asia-Pacific and South America are primary, and Africa is emerging | Medium term (2-4 years) |

| Patent surge in nanoparticle biopolymer binders for dust-off mitigation | +1.2% | Global, first-wave launches in North America and Europe | Long term (≥4 years) |

| Venture investment in multifunctional biological-binder platforms | +0.8% | North America and Europe venture hubs, Asia-Pacific pilots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Film-Coated Seeds in High-Value Horticulture

Protected-cultivation vegetables such as tomatoes and lettuce increasingly demand film-coated seed to secure emergence rates above 95% and extend shelf life during long shipping windows[1]Source: Food and Agriculture Organization of the United Nations, “Statistics 2025,” fao.org . The smooth coat lowers seeder clogging and anchors biological inoculants that lose viability on dusty surfaces. Greenhouse acreage expanded by around 7.2% in 2025, with China, the Netherlands, and Spain accounting for most of the additional square meters. Sustainability programs also push growers toward coatings that can carry microbial pesticides without synthetic carriers. India and Japan accelerate momentum by subsidizing greenhouse infrastructure and premium seed lines.

Precision Planting Driving Demand for Uniform Seed Geometry

Modern vacuum and air planters operate at 8 kilometers per hour yet keep singulation accuracy above 98% only when seed size and shape are tightly controlled. Pelleting binders round out irregular seeds and add enough mass to improve flight, without so much that drivetrain loads spike. Driven by a 5% increase in adoption between 2023 and 2025, nearly all North American corn and soybean operations now utilize some form of precision machinery. However, the adoption of comprehensive 'closed-loop' management systems that integrate Variable Rate Technology (VRT) and soil sensors remains the key growth area for the 2026 season.[2]Source: United States Department of Agriculture National Agricultural Statistics Service, “2025 Crop Acreage Report,” nass.usda.gov . South American growers follow, with a growing inclination towards digital agriculture solutions and precision-backed seed technology, citing yield lifts of around 3% to 5% within two harvests. Chinese maize producers deploy the same tech to counter rising rural labor costs.

Regulatory Caps on Pesticide Loading per Hectare

The U.S. Environmental Protection Agency is reviewing neonicotinoid seed treatments, with application rates for corn ranging from 0.25 mg to 1.25 mg per seed. Updated worker safety assessments were released in 2024, with final decisions on pollinator protections and application limits anticipated in 2025[3]Source: United States Environmental Protection Agency, “Pesticide Registration Notice 2024,” epa.gov. The European Food Safety Authority mirrored these ceilings in 2025 and added dust-off tests that simulate real planter exhaust velocities. Seed companies are adopting advanced binders include BASF’s Flo Rite Pro, to achieve dust-off levels of 0.2g or less per 100,000 seeds, cutting particulate loss by over 50–70% compared to traditional coatings. These solutions meet microplastic-free regulations and reduce pollinator exposure. Bioformulations offer the added benefit of lower toxicity profiles, streamlining separate pollinator-risk dossiers. India tabled a similar draft in 2025 for cotton, foreshadowing broader Asian uptake.

Commercial Expansion of Controlled-Release Micronutrient Coatings

Controlled-release fertilizers, utilizing polymer-encapsulated technology, ensure a consistent supply of Zinc, Boron, and Molybdenum. This targeted approach addresses micronutrient deficiencies in staple crops while reducing labor costs associated with repeated foliar applications. Treated hectares have shown a significant growth in 2025, with India, Brazil, and Australia supplying two-thirds of demand. Zinc deficiency alone clips yields by up to 20% in affected paddies, making the cost of a micronutrient coat easy to justify. Binder innovation must avoid premature nutrient leaching under monsoon soils. In 2025, Clariant's agricultural solutions focused on biodegradable adjuvants and seed coatings to improve plant resilience, while the industry remains centered on developing cellulose-based delivery systems to synchronize nutrient release. These advancements indicate significant commercial growth in the Seed Binders Market, as controlled-release micronutrient coatings play a crucial role in providing precise and sustainable nutrition in modern agriculture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in petrochemical raw material prices | −1.2% | Global, most acute in Asia-Pacific and Middle East importers | Short term (≤2 years) |

| Stringent residue-limit compliance is delaying product approvals | −0.9% | North America and Europe are key, Asia-Pacific and South America are widening | Long term (≥4 years) |

| Limited binder adhesion on large-seed species | −0.6% | North America, South America, and China have large row-crop zones | Medium term (2-4 years) |

| Supply-chain fragility for specialty biopolymers | −0.5% | Global chokepoints in guar gum (India) and nano-starch (Europe, North America) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Petrochemical Raw-Material Prices

In 2025, polyvinyl alcohol and specialized polyacrylates traded between USD 1,800 and USD 2,400 per metric ton, with North American spot prices reaching USD 3,000 per metric ton. Crude-linked feedstock volatility, such as Vesicular Arbuscular Mycorrhiza (VAM), led to gross margin compression of 140 to 300 basis points for major petrochemical manufacturers. Import-dependent formulators in India and Southeast Asia found hedging tools limited, so some cut production to curb cash burn. Michelman reported a 1.8-percentage-point margin hit and accelerated its switch to corn-stover polymers by year-end 2025. Smaller blenders lack the working capital to warehouse feedstock during downturns. Forward cracks are anticipated to stay volatile until new refineries arrive after 2027.

Supply-Chain Fragility for Specialty Biopolymers

The dependence on rain-fed crops in Rajasthan and Gujarat remains a significant risk factor. However, in 2025, the acreage remained steady at 3.15 million hectares. While pharmaceutical demand for high-viscosity gum is increasing, the petrochemical industry continues to drive global demand, maintaining prices at approximately USD 1,550 per metric ton. Nano-starch capacity is concentrated among fewer than five global processors, each holding proprietary enzymatic steps that limit tolling flexibility. Clariant postponed two pelleting launches by up to 9 months while awaiting nano-starch allotments in 2025. Supply tightness will persist until at least 2028, when new enzymatic reactors come online in North America. Formulators hedge by dual-sourcing but cannot entirely avoid single-feedstock exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biopolymers Gain as Synthetics Face Margin Pressure

Polyvinyl alcohol dominates, accounting for 49% of the seed binders market share in 2025, as it delivers reliable film strength for corn and soybean coatings. Biopolymer platforms are the fastest-growing segment and are projected to post a 12.11% CAGR through 2031 as regulators and buyers favor lower-carbon inputs. Together, these two segments illustrate how sustainability pressure is reshaping raw-material preference without immediately displacing legacy synthetics.

Polyvinyl acetate retains a solid foothold as the low-cost option for basic dust-control coats where adhesion demands are modest. Hybrid chemistries that merge silane-modified starches with protein blends deliver multifunctional films that combine adhesion, color, and nutrient carry. Guar gum is appealing for high-value vegetable coatings, though monsoon-driven price spikes limit its use to premium seeds. Collectively, these smaller groups diversify supplier portfolios and cushion against petrochemical volatility.

By Crop Type: Cereals Dominate, Horticulture Accelerates

Cereals and grains captured 44% of the seed binders market share in 2025 as more than 400 million hectares of corn and wheat rely on coatings for early pest defense and planter cleanliness. Fruits and vegetables are the fastest-growing segment and are projected to grow at a 10.30% CAGR to 2031, driven by greenhouse expansion and organic labels that mandate dust-free, microbe-friendly films. The contrast highlights how acreage volume secures dominance while value density drives growth pace. Growers of greenhouse tomatoes and lettuce willingly absorb higher unit costs to gain precision singulation and strong emergence.

Oilseeds and pulses maintain steady demand, as soybeans and canola require binders to grip lipid-rich coats during high-speed planting. Flowers and ornamentals remain a small but lucrative niche because pelletized seeds cut nursery labor. Forage grasses and specialty grains add incremental volume as smallholders adopt low-rate seed treatments. Each of these segments broadens the customer base and lessens exposure to swings in any single crop type.

By Function: Pelleting Surges as Mechanization Spreads

Film coating remained the top function, with 47% of the seed binders market share in 2025, by cost-effectively wrapping pesticides and pigments around large-acreage cereals. Encrusting is the fastest-growing function and is forecast to advance at a 10.24% CAGR through 2031, balancing higher payload capacity than films while avoiding the full bulk of pellets. These two roles illustrate how planter technology and regulatory dust caps dictate the next generation of coating recipes. Demand for encrusting accelerates when growers need room for micronutrients or biologicals but still want seeds to flow smoothly.

Pelleting keeps meaningful scale because it transforms irregular seeds into spheres that precision planters singulate at 98% accuracy in vegetable and flower beds. Dust-control topcoats gain traction as agencies push particulate loss below 0.5 grams per 100,000 seeds. Controlled-release shells and color identification layers offer specialized value, such as phased nutrient delivery or quick hybrid verification. Together, these functions broaden supplier menus and enable treaters to tailor solutions for diverse agronomic scenarios.

Geography Analysis

North America accounted for 34% of seed binder revenue in 2025, driven by high seed-treatment penetration and strict dust-off regulations that favor premium coatings. Asia-Pacific is the fastest-growing region and is projected to grow at a 10.2% CAGR between 2026 and 2031, as mechanization subsidies in China and seed-subsidy programs in India move growers from raw seed to fully coated seed. The United States drives most North American demand through its corn and soybean acreage, while Canada adds canola and wheat volumes. Asia-Pacific growth is anchored by China’s hybrid maize push and by expanding vegetable greenhouse acreage across Southeast Asia.

Europe follows next, shaped by the European Green Deal, which encourages biopolymer adoption, and by residue-limit laws that tighten dust-control rules. South America’s binder uptake accelerates in Brazil and Argentina, where no-till soybean and corn systems seek coatings that survive long transport from interior farms. The Middle East remains a small but strategic outlet as Saudi Arabia and Turkey expand protected horticulture under food-security mandates. Africa sees early traction in South Africa and Egypt, with donor-funded hybrid maize programs seeding future demand.

Regional momentum will continue to shift toward Asia-Pacific as planter fleets modernize and local seed firms scale biopolymer capacity. Europe will climb steadily under policy pressure that forces reformulation toward lower-carbon inputs and grower willingness to pay for sustainability labels. North America should hold value leadership, but its growth will decelerate as penetration nears saturation and as coatings become a routine cost of doing business. South America, the Middle East, and Africa offer upside optionality, expanding the total addressable market as infrastructure, credit access, and climate resilience programs unlock new hectares for treated seed.

Competitive Landscape

The top five players, including BASF SE, Clariant AG, Incotec Group BV (Croda International plc), Bayer AG, and Michelman, Inc., controlled the majority of the seed binders market share in 2025, signaling moderate concentration with room for challenger entry. Within this group, BASF SE utilizes its backward-integrated Verbund system and plans a capacity increase for 1,4-butanediol at Ludwigshafen by February 2026 to ensure a stable supply of feedstock for advanced seed-coating polymers, aligning with stricter European dust-off and microplastic regulations. Clariant AG utilized its November 2025 integration of Lucas Meyer’s phospholipid technology to gain access to plant- and fungal-derived biopolymers. This development facilitates the production of seed binders that reduce greenhouse gas intensity by 60% while ensuring compliance with the 2026 Registration, Evaluation, Authorisation, and Restriction of Chemicals (REACH) regulations. These two leaders set technical benchmarks that shape formulation targets for the wider industry.

Incotec Group BV (Croda International plc) specializes in vegetable pelleting and leverages Croda International's research funding to accelerate the development of controlled-release shells. Michelman, Inc. focuses on waterborne dust shields and used a United States Department of Agriculture loan in May 2025 to build a 5,000 metric ton corn stover polymer line in Ohio. Corteva Agriscience integrates binders with its crop-protection actives, and a January 2026 partnership with SilviBio adds starch-nano technology that halves greenhouse gas footprints compared with polyvinyl alcohol. Together, these three firms maintain high innovation pressure through frequent patent filings for nanoparticle starch films and hybrid cellulose blends.

Growth strategies now cluster around bio-based feedstock security, regional production, and co-development with seed companies. BASF, Clariant, and Incotec are installing pilot reactors in Asia-Pacific to capture double-digit demand tied to mechanization subsidies. Michelman, Inc. and Corteva Agriscience are hedging against petrochemical volatility by locking in multi-year supply contracts for agricultural residues and by validating life-cycle assessments that appeal to sustainability-driven buyers. As regulations tighten and greenhouse acreage spreads, these proactive moves are anticipated to increase manufacturing capacity and speed the market shift toward multifunctional biological binders.

Seed Binders Industry Leaders

BASF SE

Clariant AG

Incotec Group BV (Croda International plc)

Bayer AG

Michelman, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Corteva’s Board approved splitting the company into two publicly traded entities. One for crop-protection chemistry and the other for seeds. The seed-focused entity (SpinCo) will handle binder and coating platforms, while the crop-protection company (New Corteva) will retain polymer-dispersion expertise. The separation enables targeted research and development in biological seed binders and precision-coating technologies for microplastic-free solutions. Anticipated to close after regulatory approvals, the transaction aims to strengthen partnerships and grow in the seed binders market.

- March 2025: Michelman unveiled a microplastic-free seed-coating line built on bio-based wax emulsions and binders and invested in a dedicated seed laboratory to refine these sustainable formulations for crops including corn, soybeans, and sunflowers.

- October 2024: Incotec Group BV launched Disco Blue L-1523, a microplastic-free film coat designed for sunflower seeds, at the Euroseeds Congress 2024 in Copenhagen, while the blue formulation offers improved processing efficiency and high cosmetic value while meeting rising sustainability requirements.

Global Seed Binders Market Report Scope

Seed binders are coating agents used to help adhesives, polymers, or films stick uniformly to seeds, improving shape, flowability, and the retention of active ingredients during planting. The Seed Binders Market Report is Segmented by Product Type (Polyvinyl Alcohol, Polyacrylate, Biopolymer-based, Cellulose Derivatives, Others), Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others), Function (Film Coating, Pelleting, Encrusting, Dust-Control, Controlled-Release), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are in Value (USD).

| Polyvinyl Alcohol |

| Polyacrylate |

| Polyvinyl Acetate |

| Biopolymer-based |

| Acrylic Latex |

| Cellulose Derivatives |

| Guar-Gum Binders |

| Others |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Flowers and Ornamentals |

| Other Crops |

| Film Coating |

| Pelleting |

| Encrusting |

| Dust-Control Coatings |

| Controlled-Release Shells |

| Color-Enhancement Layers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Polyvinyl Alcohol | |

| Polyacrylate | ||

| Polyvinyl Acetate | ||

| Biopolymer-based | ||

| Acrylic Latex | ||

| Cellulose Derivatives | ||

| Guar-Gum Binders | ||

| Others | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Flowers and Ornamentals | ||

| Other Crops | ||

| By Function | Film Coating | |

| Pelleting | ||

| Encrusting | ||

| Dust-Control Coatings | ||

| Controlled-Release Shells | ||

| Color-Enhancement Layers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How big will the seed binders market be by 2031?

It is forecast to reach USD 1.55 billion, expanding at an 8.7% CAGR from 2026 to 2031.

Which function is growing fastest within seed coatings?

Pelleting is projected to climb at an 11.2% CAGR through 2031 due to precision planting in high-value vegetables.

Why are biopolymer binders gaining momentum?

They reduce dust-off, cut fossil carbon, and help meet new pesticide-loading caps, driving a 10.8% CAGR through 2031.

Which region is set to add the most incremental demand?

Asia-Pacific will see the quickest rise at a 10.2% CAGR through 2031, led by China and India.

How concentrated is supplier power today?

The top five companies control majority of revenue, leaving scope for startups and regional specialists.

Page last updated on: