Watermelon Seeds Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

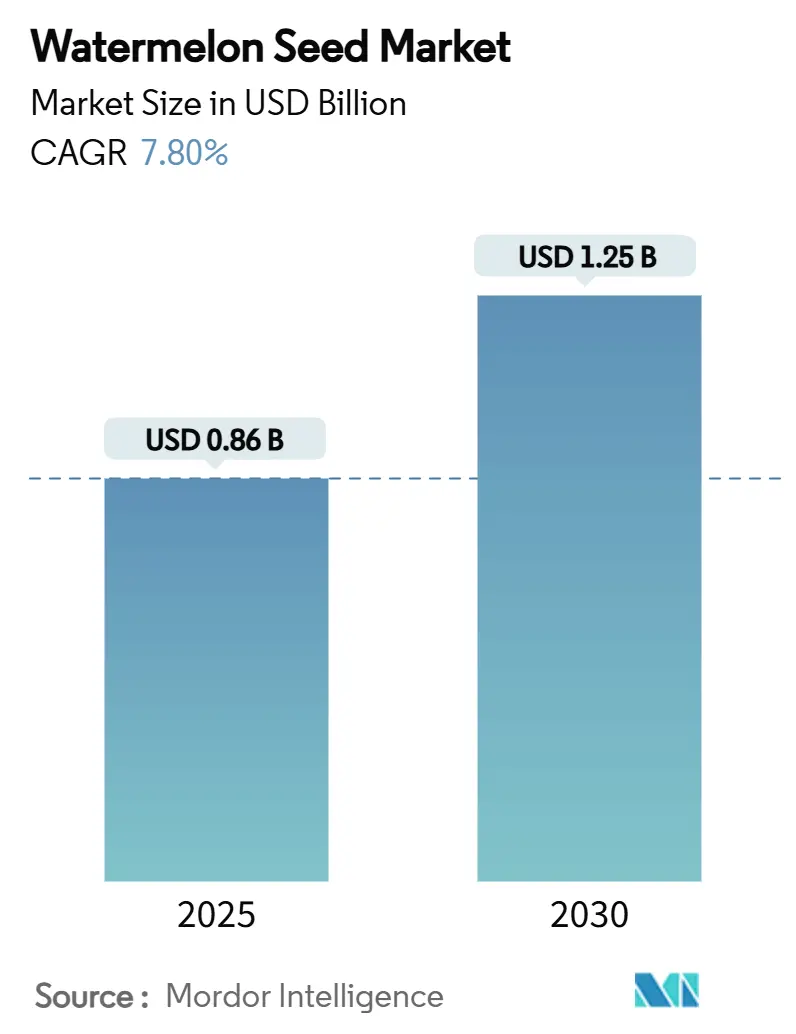

| Market Size (2025) | USD 0.86 Billion |

| Market Size (2030) | USD 1.25 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

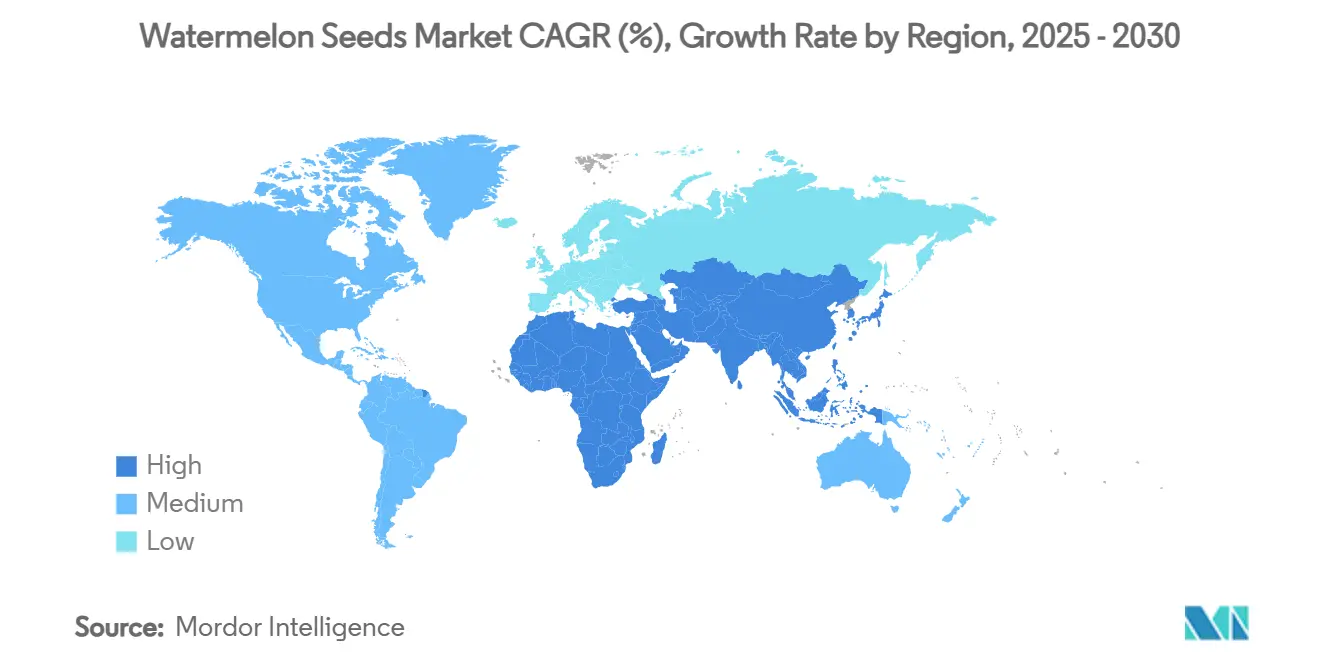

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

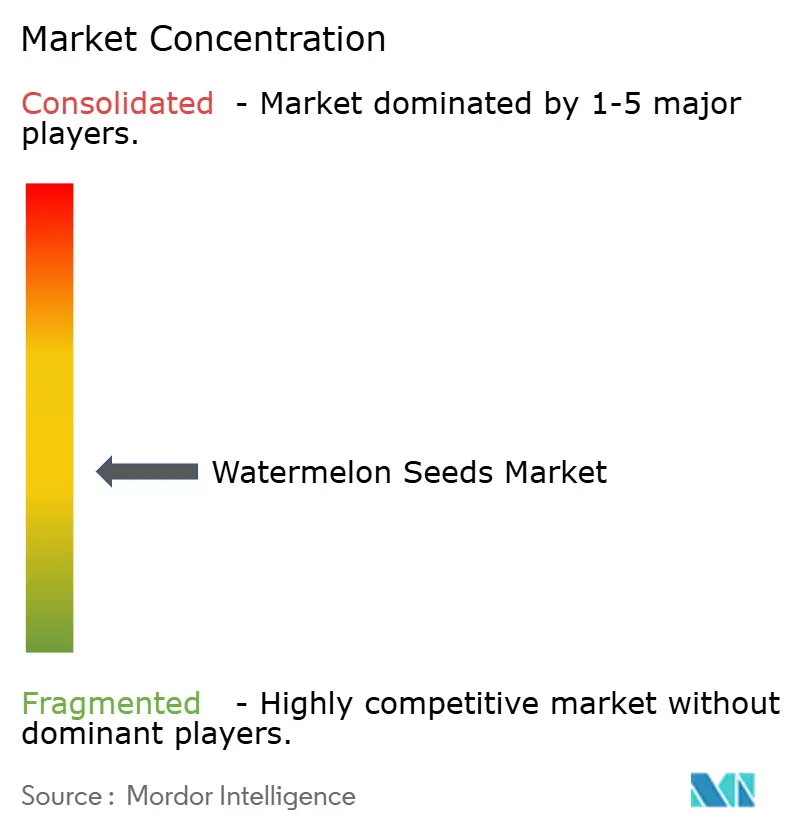

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Watermelon Seeds Market Analysis by Mordor Intelligence

The watermelon seeds market size reached USD 0.86 billion in 2025 and is anticipated to grow to USD 1.25 billion by 2030, at a CAGR of 7.8%. The market growth is driven by the transition from open-pollinated to hybrid varieties, increasing demand for seedless watermelons, and the development of climate-resilient varieties. Commercial growers are adopting F1 hybrids that increase yields by 20-30%, while retailers benefit from improved product uniformity and longer shelf life. The adoption of seed treatments is increasing due to stricter phytosanitary regulations, which enhance germination rates and facilitate international trade. The market exhibits moderate competition, with the top five companies accounting for nearly half of the revenue, enabling specialized breeders focusing on mini watermelons or protected cultivation to maintain a market presence. Additionally, government subsidies for certified seeds and traceability programs in Africa and South Asia are increasing seed adoption rates, contributing to market growth.

Key Report Takeaways

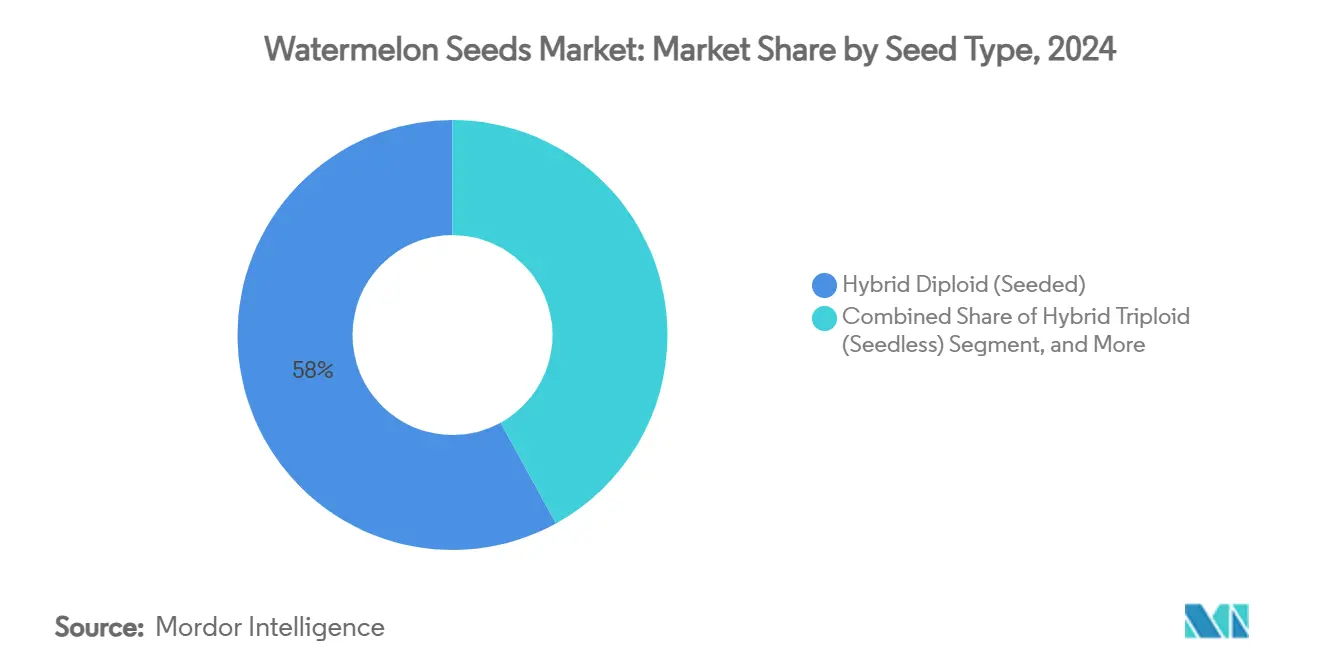

- By seed type, hybrid diploid seeds held 58% watermelon seeds market share in 2024, whereas hybrid triploid seeds are forecast to grow at a 12.1% CAGR through 2030.

- By treatment, untreated seeds accounted for 56% of the watermelon seeds market size in 2024, while film-coated and pelleted seeds are expanding at a 10.2% CAGR.

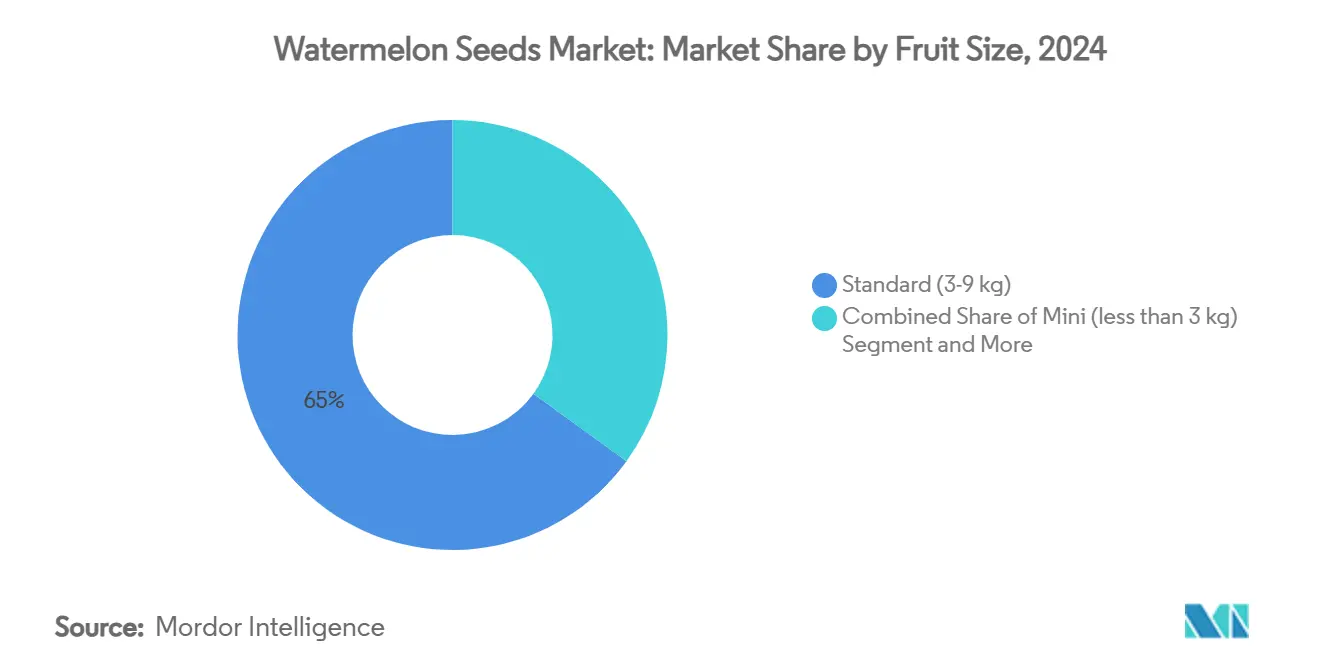

- By fruit-size class, standard fruit led with 65% share in 2024, and mini fruit is projected to advance at a 9.1% CAGR between 2025 and 2030.

- By end user, open-field cultivation owned a 72% revenue share in 2024, and protected cultivation represented the fastest growth at a 10.7% CAGR.

- By geography, Asia-Pacific controlled 41% of the watermelon seeds market in 2024, and Africa is projected to register a 10.5% CAGR, the highest globally.

- Major Players, including Syngenta Group, BASF SE, Bayer AG, UPL Limited, and Sakata Seed Corporation, collectively held a majority of the market share in 2024.

Global Watermelon Seeds Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid global shift from open-pollinated to high-value F1 hybrids | +2.1% | Global, with strongest adoption in North America and Europe | Medium term (2-4 years) |

| Accelerating adoption of triploid (Seedless) cultivars in premium retail channels | +1.8% | North America, Europe, and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Climate-resilient, drought-tolerant germplasm demanded by growers | +1.4% | Africa, Middle East, and drought-prone regions globally | Long term (≥ 4 years) |

| Integration of marker-assisted and genomic selection shortening breeding cycles | +1.2% | Global, led by major seed companies in developed markets | Medium term (2-4 years) |

| Emerging small/mini watermelon formats requiring new pollenizer ratios | +0.9% | North America, Europe, and premium Asian markets | Short term (≤ 2 years) |

| Expanded government subsidies for certified seed quality and traceability schemes | +0.7% | Developing markets in Africa, Asia-Pacific, and South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Global Shift from Open-pollinated to High-value F1 Hybrids

Growers are adopting F1 hybrids that produce uniform fruits and offer enhanced disease resistance, despite hybrid seeds costing four to five times more than farm-saved seeds. The uniform maturity of these hybrids facilitates mechanical harvesting, while their resistance to Fusarium wilt races 2 and 3 reduces fungicide costs. Genomic breeding programs have shortened variety development cycles from 8-10 years to approximately five years, enabling faster development of hybrids adapted to changing climate conditions and retail requirements. This transition improves supply chain reliability by enabling producers to better plan harvest schedules and market availability. F1 hybrids help growers meet quality standards and maintain yields while satisfying consumer preferences for consistent taste and appearance.

Accelerating Adoption of Triploid (Seedless) Cultivars in Premium Retail Channels

Seedless (triploid) watermelons sell at a 15-25% premium in supermarkets and constitute over 80% of U.S. production. Through improved tetraploid parent lines, breeders have increased laboratory germination rates to 90-99%. The convenience of seedless fruit appeals to retailers, leading growers to dedicate 20-33% of their fields to pollenizer rows for successful fruit set. Integrated breeding companies with proprietary tetraploid lines maintain strong profit margins due to the technical complexity of triploid seed production. Large-scale farms now routinely implement precision planting and pollination mapping to ensure consistent yields. The growing consumer demand for convenient, uniform fruit drives the adoption of seedless varieties in emerging markets.

Climate-resilient, Drought-tolerant Germplasm Demanded By Growers

African watermelon landraces possess deep root systems and high citrulline content that protect against oxidative stress, allowing breeders to incorporate drought tolerance traits. The adoption of drought-tolerant varieties increases as irrigation costs rise and water allocation regulations become stricter. The combination of rootstock grafting and precise fertigation methods in semi-arid regions reduces water consumption by 30% while maintaining yields, encouraging farmers to invest in drought-resistant hybrid varieties. These genetic traits demonstrate effectiveness during irregular rainfall patterns, improving fruit set reliability during stress conditions. Field trials across multiple locations in North Africa and southern India are confirming the performance of these varieties in both saline and low-input environments, increasing their global market potential.

Integration of Marker-assisted and Genomic Selection Shortening Breeding Cycles

High-throughput Single Nucleotide Polymorphism (SNP) arrays and machine learning models now enable the screening of thousands of seedlings for complex traits without the need for field plots. Commercial programs combine DNA fingerprinting with hyperspectral imaging to verify inbred purity and predict fruit quality, shrinking breeding cycles by 30–40%. Early releases with stacked Fusarium and Green Mottle Mosaic Virus (GMMV) resistance demonstrate the speed advantage, signaling a step change in competitive dynamics. Integrating environmental data with genotype performance enables predictive breeding tailored to regional stress profiles. This precision accelerates the development of cultivars with combined resilience, shelf life, and flavor attributes, aligning genetics with market trends.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and lower germination rates of triploid seeds | -1.6% | Global, particularly in price-sensitive developing markets | Short term (≤ 2 years) |

| Strict phytosanitary regulations limiting cross-border seed trade | -1.2% | Global trade corridors, especially Asia-Pacific to other regions | Medium term (2-4 years) |

| Intellectual-property disputes over patented hybrid lines | -0.8% | North America, Europe, and major seed company jurisdictions | Long term (≥ 4 years) |

| Increasing disease pressure (BFB, CGMMV) raising seed-treatment costs | -1.1% | Global, with highest impact in intensive production regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Lower Germination Rates of Triploid Seeds

Triploid seeds often retail at three to five times the cost of diploid seed, and field germination can dip below 85%, forcing growers to oversow. Priming and film-coating lift emergence but add cost. Price-sensitive growers in Africa and parts of Asia restrict acreage, slowing the overall watermelon seeds market growth. The thicker seed coat and lower seedling vigor of triploids demand greenhouse transplanting, further increasing labor and infrastructure costs. Breeders are exploring embryo rescue and oxygen-enhanced germination protocols to improve viability under direct-seeding conditions.

Strict Phytosanitary Regulations Limiting Cross-border Seed Trade

Strict phytosanitary regulations requiring PCR certificates for bacterial fruit blotch and Green Mottle Mosaic Virus (GMMV) increase customs clearance times and raise landed seed costs by 10-15%. Small-scale breeders struggle to meet compliance requirements, which restrict their export capabilities and delay their market entry. These regulations have a particularly significant impact on emerging markets due to the limited availability of diagnostic facilities and certification accessibility. The increasing frequency of disease outbreaks has prompted seed companies to establish internal pathogen testing facilities and disease-free seed production zones to maintain uninterrupted trade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Seed Type: Triploid Seedless Momentum Reshapes Demand

Hybrid diploid seeds captured a 58% share in the watermelon seeds market size in 2024 and underpin both fruit production and pollenizer demand. Still, triploid seed sales are rising at 12.1% CAGR, the highest of any segment in the watermelon seeds market. Consumers reward seedless fruit with shelf premiums, prompting distributors to push triploid options deeper into mainstream retail. Conversely, open-pollinated lines are shrinking as cost gaps narrow and uniformity gains from hybrids outweigh savings.

Triploid expansion relies on improved germination and cost management. Seed companies deploy proprietary tetraploid parental stocks and tighter production protocols to raise pure seed yields and stabilize pricing. Film-coated variants integrating fungicide and micronutrient packages lift field emergence, mitigating historical grower hesitancy. The U.S. Department of Agriculture (USDA) cultivar evaluations, such as the North Carolina Standard Triploid Watermelon Cultivar Trials, highlight how coated seeds with fungicide and micronutrient packages consistently outperform untreated variants in stand establishment and disease resistance[1]Source: U.S. Department of Agriculture, “North Carolina Standard Triploid Watermelon Cultivar Evaluation,” usda.gov.

By Treatment: Film Coating Gains Traction Across Value Chains

The untreated product still commands 56% revenue in the watermelon seeds market share in 2024, especially in informal trade channels where unit cost matters most. Yet film-coated and pelleted seeds are advancing at 10.2% CAGR, buoyed by large corporate farms and integrated supply chains that prioritize stand establishment and disease control. Coatings embed systemic fungicides, beneficial bacteria, or micronutrient blends that lift emergence by 5-10% points in challenging soils. On triploid lines, premium coatings can recoup their cost through stronger stands and reduced reseeding.

Innovation centers on water-soluble biodegradable polymers and bio-based binders that comply with evolving residue limits. Producers such as Lucent BioSciences deliver nutrient-infused coatings that release zinc and iron during germination, supporting early vigor. In export-heavy Asia-Pacific hubs, test reports showing pathogen-free status and labeled coating contents facilitate customs clearance, making coated seed the default for cross-border shipments.

By Fruit-Size Class: Mini Fruit Attracts Premium Consumers

Standard fruit (3-9 kg) generated 65% of 2024 revenue, reflecting its dominance in wholesale and roadside markets. Large fruit (more than 9 kg) remains important for catering and mass gatherings, though its broader growth is flat. Mini watermelons, weighing under 3 kg, are the clear outlier with 9.1% CAGR. Urban shoppers favor small formats that fit refrigerator shelves and curb waste. Retailers allocate branded clamshells and two-packs that spotlight seedless minis, fuelling trade-up spending. Early-maturing mini lines also reduce field exposure to rainfall, cutting split risk and fungicide sprays.

Breeding focuses on sugar concentration above 11 Brix and a crisp texture, traits that are often diluted in small fruit. Programs use genomic markers linked to soluble solids and rind firmness to maintain eating quality. Mini types also facilitate protected-cultivation rotations, and their shorter vine length and uniform set mesh well with greenhouse spacing.

By End User: Protected Cultivation Underpins Intensification

Open-field farms still buy 72% of seed volume, yet protected-cultivation operators record 10.7% CAGR. Greenhouse and high-tunnel systems control temperature and humidity, enabling transplant dates in cool seasons, faster cycles, and off-season retail slots that command premiums. Triploid seedless lines particularly benefit from stable environments that improve stand establishment. Many growers graft seedlings onto disease-resistant rootstocks, extending crop longevity and raising yields per unit area.

As LED lighting and precise fertigation slash production risk, seed companies create greenhouse-tailored cultivars with compact vines and adaptable pollination needs. In Spain, transplanting data show 20-30% shorter seedling phases under LED arrays. Such savings offset higher seed costs. This convergence of technology and genetics keeps protected cultivation the fastest-growing buyer group in the watermelon seeds market.

Geography Analysis

Asia-Pacific led with 41% revenue in 2024, anchored by China’s 60.5% share of global fruit output. Hybrid adoption rises across Southeast Asia as retailers standardize sizing and sweetness[2]Source: Philippine News Agency, “Unlimited Free Watermelons, but Leave the Seeds,” pna.gov.ph. India’s private seed sector invests in fusarium-resistant lines suited for long-haul trucking, while Japan’s protected-culture niche commands ultra-high seed prices justified by premium retail tags.

Africa represents the fastest climbing region at 10.5% CAGR through 2030. Governments subsidize certified hybrid seeds, and regional trade corridors into the Gulf states lift demand. Nigeria’s gross margin of Naira 253,850 (USD 279) per hectare underscores attractive returns compared to staples, encouraging household growers to scale acreage. Local seed multipliers partner with multinational breeders to produce foundation seeds, lowering landed cost and improving availability. Watermelon thrives in arid and semi-arid regions, making it a strategic crop in areas with limited water access, where coated seeds with embedded micronutrients and disease resistance can significantly improve stand establishment and yield[3]Source: Food and Agriculture Organization, “Watermelon Crop Information,” fao.org.

North America and Europe reflect mature penetration of triploid seedless varieties, yet value growth persists via mini categories, organic certification, and extended shelf life targets. High food-service demand across the United States sustains diploid pollenizer sales even as seedless varieties occupy consumer shelves. South America delivers moderate gains as Brazil and Mexico integrate protected tunnels that temper rainfall variability. The Middle East leverages arid-zone protected culture and desalinated water supplies, underpinning steady hybrid uptake.

Competitive Landscape

The watermelon seeds market shows moderate fragmentation, with the top five companies accounting for nearly half of the revenue. Syngenta Group maintains a significant market share through its strong triploid and mini watermelon portfolios, strategic marketing in Asia, and collaboration between breeders and growers. BASF SE and Bayer AG maintain their positions through extensive dealer networks and genomics-based pipeline development. East-West Seed has established itself as a primary supplier in tropical Asia by focusing on hybrid seeds for smallholder farmers and implementing community agronomy programs.

Companies invest substantial portions of their revenue in technological advancements, including marker-assisted selection, DNA purity testing, and AI-aided phenotyping. Strategic partnerships demonstrate this technological emphasis, such as Corteva and Pairwise's USD 25 million joint venture in September 2024 to develop gene-edited traits for climate resilience. Portfolio restructuring also reflects this focus, as evidenced by Syngenta's divestment of the FarMore vegetable seed treatment line to Gowan SeedTech to concentrate resources on genomics research.

Specialized companies succeed by focusing on mini watermelons or developing region-specific disease-resistant varieties. Enza Zaden's watermelon division has scheduled three new product launches by 2028, targeting the growing demand for snack-sized, seedless varieties. The protection of parental lines remains essential, with Patent Trial and Appeal Board decisions highlighting both the legal challenges of genetic uncertainty and the importance of precise genotypic documentation.

Watermelon Seeds Industry Leaders

Syngenta Group

Bayer AG

BASF SE

UPL Limited

Sakata Seed Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bayer AG launched two watermelon varieties, such as Lunalinda, a seedless variety suitable for export markets, and SVWT3052, a micro-seed pollinator characterized by synchronized flowering and firm texture. These varieties enhance triploid production capabilities and serve fresh-cut market requirements, demonstrating Bayer's focus on varietal development and agricultural solutions.

- February 2025: Ferry-Morse launched Triple Crown Hybrid Organic watermelon seeds, which produce high yields of seedless watermelons. The seeds, developed for home gardeners and small-scale farmers, feature strong germination rates and robust plant growth, making them suitable for summer cultivation and market sales.

- January 2025: Syngenta Group's vegetable seeds domain and Apricus Seeds established a global licensing agreement that provides Syngenta with exclusive access to Apricus' watermelon germplasm and breeding pipeline. This collaboration enhances Syngenta's cucurbit portfolio and advances seed genetics development for global agricultural producers.

- August 2024: BASF's Nunhems expanded its distribution network by partnering with TS&L Seed Company to supply watermelon seeds in California, Arizona, and Nevada. This partnership improves access to Nunhems genetics and incorporates grower feedback into product development, enhancing the development and regional adoption of watermelon varieties.

Global Watermelon Seeds Market Report Scope

Watermelon Seeds are planting materials used to grow watermelon plants, developed to deliver specific traits such as fruit size, yield, disease resistance, and seedlessness.

The Watermelon Seeds Market Report is segmented by seed type (Open-Pollinated, Hybrid Diploid (Seeded), Hybrid Triploid (Seedless)), by treatment (Untreated, Film-Coated/Pelleted), by fruit-size class (Mini (less than 3 kg), Standard (3–9 kg), Large (more than 9 kg)), by end user (Open-Field, Protected-Cultivation), and by geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Open-Pollinated |

| Hybrid Diploid (Seeded) |

| Hybrid Triploid (Seedless) |

| Untreated |

| Film-Coated/Pelleted |

| Mini (less than 3 kg) |

| Standard (3-9 kg) |

| Large (more than 9 kg) |

| Open-Field |

| Protected-Cultivation |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Spain |

| Italy | |

| Greece | |

| France | |

| Germany | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Seed Type | Open-Pollinated | |

| Hybrid Diploid (Seeded) | ||

| Hybrid Triploid (Seedless) | ||

| By Treatment | Untreated | |

| Film-Coated/Pelleted | ||

| By Fruit-Size Class | Mini (less than 3 kg) | |

| Standard (3-9 kg) | ||

| Large (more than 9 kg) | ||

| By End User | Open-Field | |

| Protected-Cultivation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Spain | |

| Italy | ||

| Greece | ||

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the watermelon seeds market?

The watermelon seeds market size reached USD 0.86 billion in 2025 and is projected to expand to USD 1.25 billion by 2030.

Which region shows the fastest growth for watermelon seed demand?

Africa leads growth with a projected 10.5% CAGR through 2030 as certified hybrid adoption accelerates.

Why are triploid seedless varieties gaining traction?

Triploid seeds enable seedless fruit that commands 15-25% retail premiums, driving a 12.1% CAGR for this segment.

Which end-user group is expanding fastest?

Protected-cultivation growers are increasing seed purchases at 10.7% CAGR due to year-round production and premium mini varieties.

Page last updated on: