Fillings and Toppings Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

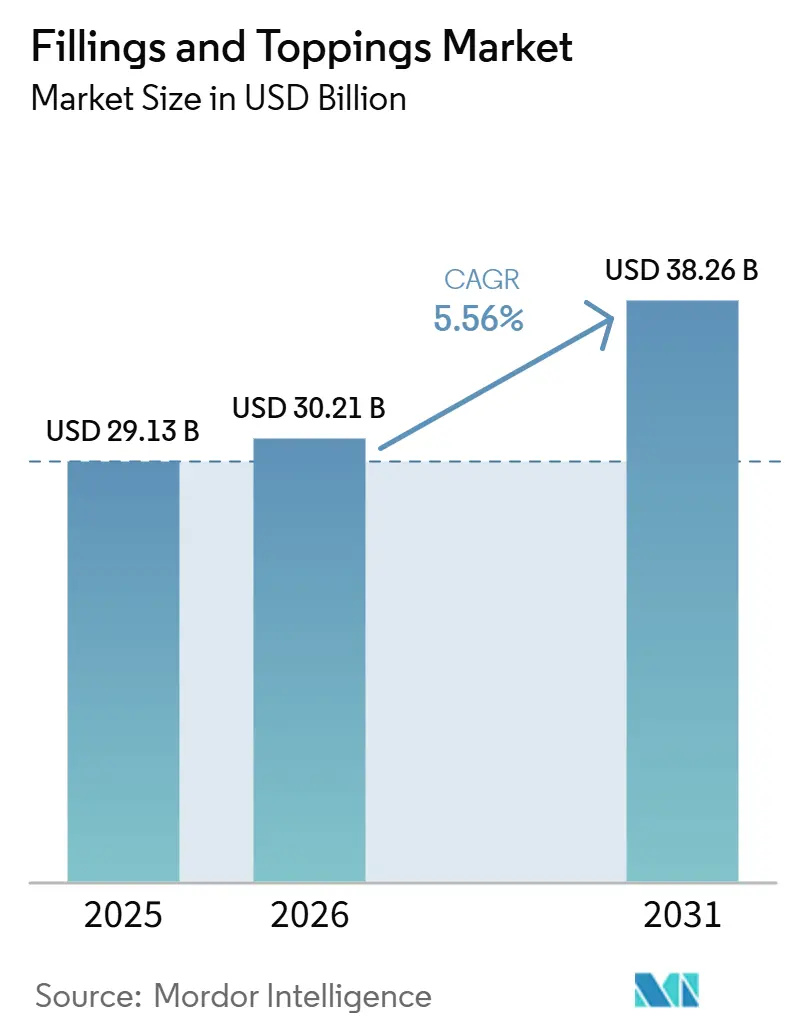

| Market Size (2026) | USD 30.21 Billion |

| Market Size (2031) | USD 38.26 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fillings and Toppings Market Analysis by Mordor Intelligence

The fillings and toppings market size is expected to increase from USD 29.13 billion in 2025 to USD 30.21 billion in 2026 and reach USD 38.26 billion by 2031, growing at a CAGR of 5.56% over 2026-2031. The fillings and toppings market is supported by steady demand from industrial bakeries, confectionery producers, and foodservice operators, where fillings and bakery toppings now shape product structure, shelf appeal, and menu differentiation rather than serving as optional add-ons. The demand base remains broad across fruit fillings, cream-based fillings, chocolate fillings, sugar toppings, chocolate toppings, cheese toppings, and whipping cream toppings, which helps the fillings and toppings market stay resilient across retail, foodservice, and industrial bakery channels. In the United States, retail baked goods sales are on track to reach USD 97.7 billion in 2026, which underlines the scale of downstream demand feeding the fillings and toppings market[1]Source: Agriculture and Agri-Food Canada, “Sector Trend Analysis – Bakery Products in the United States,” Government of Canada, agriculture.canada.ca. Competitive activity in the fillings and toppings market is centered on clean-label reformulation, flavor customization, cocoa-risk diversification, and regional expansion, while the main pressure points remain cocoa price volatility and the shift toward lower-sugar and lower-calorie product design. The result is a market where volume demand remains stable, but supplier advantage increasingly depends on technical formulation depth, customer co-development capability, and the ability to localize premium concepts across regions.

Key Report Takeaways

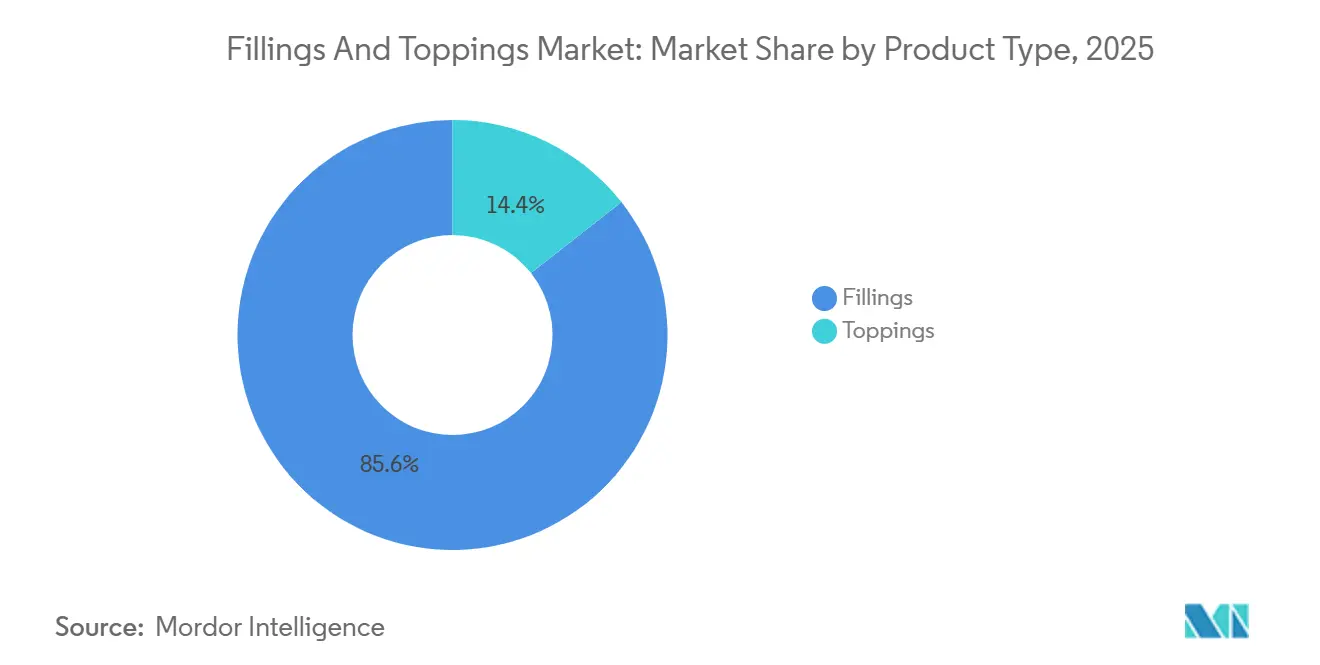

- By product category, fillings held 85.62% of the fillings and toppings market share in 2025, while toppings are forecast to expand at a 6.58% CAGR through 2031.

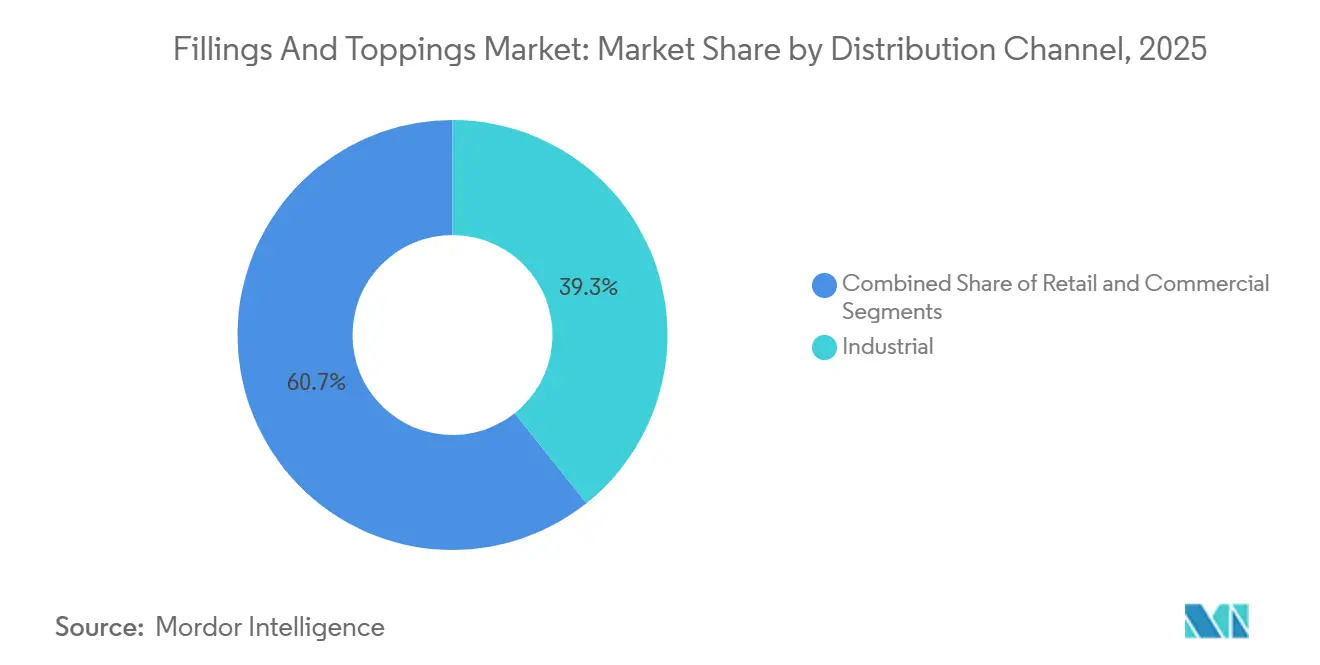

- By distribution channel, industrial held 43.23% share in 2025, while retail is projected to grow at a 7.02% CAGR through 2031.

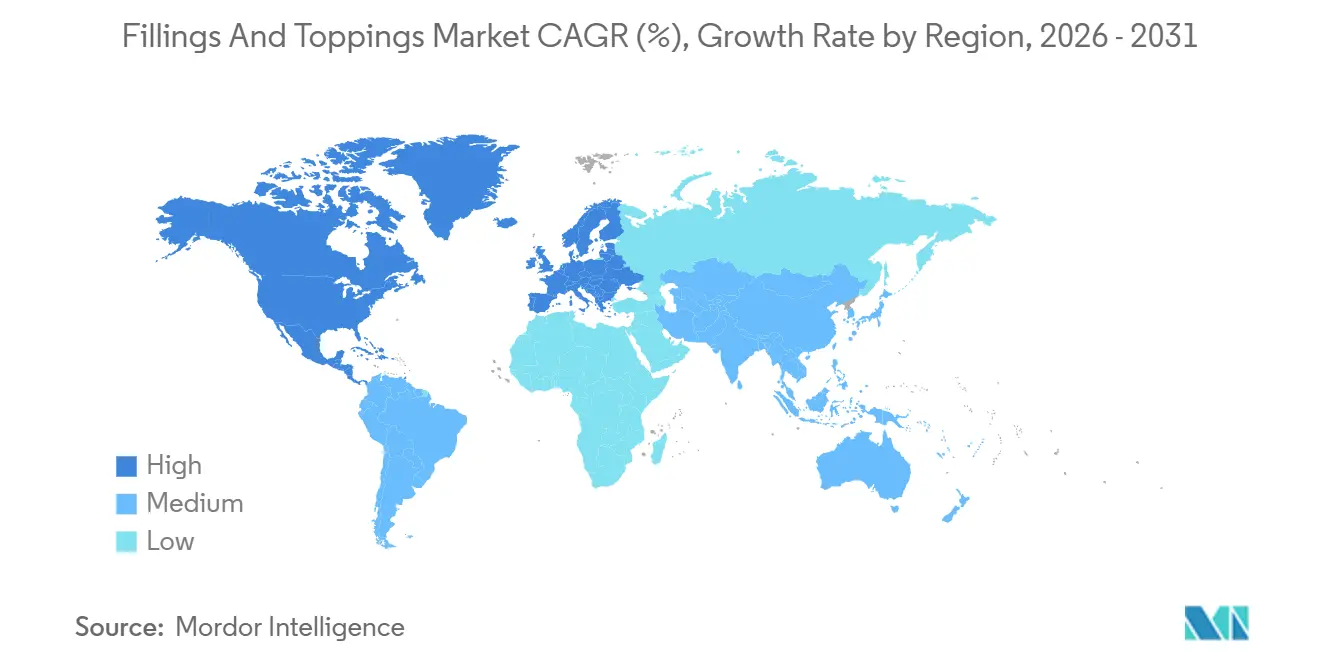

- By geography, Europe accounted for 37.31% share in 2025, while Asia-Pacific is forecast to expand at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fillings and Toppings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand of Fillings from Bakery and Confectionery Products | +1.4% | Global, concentrated in Europe and North America | Long term (≥ 4 years) |

| Increasing Consumer Preference for Premium and Indulgent Foods | +1.0% | Europe and North America, with rapid uptake in APAC | Medium term (2–4 years) |

| Innovation in Flavors and Product Customization | +0.8% | Global, fastest adoption in APAC and North America | Medium term (2–4 years) |

| Growth in Retail Packaged Bakery and Snack Products | +0.7% | Global, with concentrated impact in North America, Europe, and APAC | Short term (≤ 2 years) |

| Increasing Use of Toppings in Foodservice Industries | +0.6% | North America, APAC, and Middle East | Short term (≤ 2 years) |

| Technological Advancements in Ingredient Formulation | +0.5% | Global, concentrated R&D in Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Fillings from Bakery and Confectionery Products

The fillings and toppings market continues to benefit from the fact that fillings remain deeply embedded across bakery and confectionery formats, including croissants, Danish pastries, biscuit sandwiches, éclairs, and layered cakes. This matters because these products depend on filling consistency, bake stability, and repeatable flavor delivery, which increases reliance on industrial ingredient suppliers as volume scales. France also recorded meaningful bakery and pâtisserie growth in 2025, with viennoiserie and individual pastry categories acting as major revenue contributors, which supports strong pull for premium fruit and cream fillings. As bakery chains adjust production footprints to manage labor costs, in-house preparation becomes less attractive and standardized sourced fillings become more important, which strengthens procurement power for large suppliers in the fillings and toppings market. That pattern supports durable revenue visibility for companies that can provide flavor-customized and process-stable systems at scale.

Increasing Consumer Preference for Premium and Indulgent Foods

The fillings and toppings market is also supported by resilient consumer demand for indulgent bakery products, even while household food budgets remain under pressure. Puratos reported that 65% of British consumers still treat themselves and their families despite budget constraints, and 60% actively seek products that balance health with sensory enjoyment, especially in chocolate and cocoa-based bakery formats. This keeps premium fillings and toppings relevant because they help brands justify higher shelf prices through sensory appeal rather than simple volume. Texture has become a stronger purchase signal within the fillings and toppings market, with Puratos stating that 67% of consumers seek novelty through unexpected mouthfeel, while 75% of Gen Z and 80% of Millennials say texture shapes snack cravings. As a result, gooey centers, mousse-like fillings, and whipped toppings are being used as product-positioning tools in both retail and foodservice. This favors suppliers that can engineer complex topping and filling systems, while smaller regional producers face difficulty matching the same functional and sensory precision.

Innovation in Flavors and Product Customization

Flavor innovation has become one of the clearest routes to differentiation in the fillings and toppings market because it moves products away from commodity positioning and toward longer-term customer partnerships. In 2026, the bakery flavor direction is shifting toward sweet-spicy and fruity-spicy contrasts, botanical notes, and globally inspired formats that reflect wider consumer exposure to international cuisines. In Asia-Pacific, flavors such as matcha, yuzu, miso caramel, and tropical fruit blends are moving beyond local novelty and are now shaping development agendas for export-ready bakery concepts. Kerry Group strengthened that customization model in February 2026 through the inauguration of its Customer Co-Creation Centre in Medellín, Colombia, which is designed to develop flavors and sensory profiles tailored to Andean bakery, confectionery, and snack categories. The 2025 U.S. patent application for a freeze-thaw stable, thermoreversible gel-based pastry filling, which shows that customization now extends beyond flavor and into structural performance. In the fillings and toppings market, that creates a wider gap between suppliers with true formulation capability and those competing mainly on volume.

Technological Advancements in Ingredient Formulation

The fillings and toppings market is being reshaped by advances in emulsification, encapsulation, hydrocolloid engineering, and preservation technology. Cargill highlighted a synergistic system that combines UniPECTINE high-methoxyl pectin with SimPure functional starch for bake-stable fruit fillings, which improves gel stability, spreadability, and control over syneresis during thermal cycles. In May 2025, a European Patent Office application described a biscuit filling composition with reduced saturated fat and without palm oil, hydrogenated fats, or E-number additives, aligning formulation work with tightening European compliance expectations[2]Source: European Patent Office, “Filling for a Bakery or Chocolate Product – EP 4552502 A2,” European Patent Office, data.epo.org. Non-thermal preservation is also gaining importance, with high-pressure processing at 300-500 MPa shown to reduce yeast and mold counts in fruit fillings from 4.6 log CFU/g to below 1 log CFU/g, which offers a cleaner-label route to shelf-life control. These changes matter because the fillings and toppings market now rewards multi-component system design rather than isolated ingredient substitution. Suppliers with stronger technical platforms therefore gain a clearer capability moat over manufacturers still relying on older formulation approaches.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward healthier and low-calorie foods | -1.4% | Global, most pronounced in Europe and North America | Long term (≥ 4 years) |

| Limited shelf life of fruit and dairy-based products | -0.8% | Global, with heightened challenge in APAC and emerging markets with limited cold-chain infrastructure | Medium term (2–4 years) |

| Competition from in-house formulations | -0.6% | North America and Europe (large industrial bakeries) | Short term (≤ 2 years) |

| Stringent food safety and labeling regulations | -0.3% | Europe (EFSA-driven under EC 1333/2008), North America (FDA), with tightening across APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Healthier and Low-Calorie Foods

The fillings and toppings market faces its strongest structural restraint from the shift toward healthier and lower-calorie food choices. The market links this shift not only to broader health awareness, but also to the growing use of GLP-1 medications, which are changing appetite behavior and pushing bakery consumption toward smaller portions, higher protein content, and lower-calorie formats. That directly pressures conventional cream and chocolate filling volumes, while at the same time forcing suppliers to spend more on reformulation. A 2025 study in Molecules found that plant-based proteins such as pea, pumpkin, hemp, brown rice, and sunflower can act as partial palm fat replacers in cream fillings, but flavor masking and oxidative stability remain practical challenges during longer storage periods. In the fillings and toppings market, that means reformulation is not a simple ingredient swap, because it raises technical complexity and often weakens margins. Larger companies are better placed to absorb that R&D burden, while smaller producers are more exposed to cost pressure and customer loss.

Limited Shelf Life of Fruit and Dairy-Based Products

Limited shelf life remains a major operating restraint for the fillings and toppings market, especially in high-moisture fruit and dairy applications. The fruit fillings are vulnerable to fungal spoilage from molds such as Penicillium, Aspergillus, and Cladosporium, as well as acid-tolerant yeasts like Zygosaccharomyces bailii, which can resist weak organic acid preservatives. This becomes more difficult when sugar is reduced, because lower sugar content raises water activity and increases both microbial risk and moisture migration into surrounding dough. Dairy-based cream fillings, buttercream products, and cheese toppings add another layer of difficulty because they depend on stable cold-chain conditions, which raises logistics costs and limits distribution in emerging markets. The clean-label movement compounds the challenge by narrowing the use of established synthetic preservatives, which leaves manufacturers choosing between higher-cost natural antimicrobials and capital-intensive processes such as high-pressure processing. In the fillings and toppings market, this restraint is especially visible in Asia-Pacific and Sub-Saharan Africa, where cold-chain gaps still limit wider distribution of premium dairy-filled bakery products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fillings Scale While Toppings Capture Premium Growth

Toppings are forecast to grow at a CAGR of 6.58% through 2026-2031, which makes them the fastest-moving product category in the fillings and toppings market. Their expansion reflects stronger use in foodservice menu differentiation and in premium home-baking formats, where visual impact now carries commercial value alongside taste. Sugar toppings, chocolate and caramel toppings, whipping cream toppings, and cheese toppings each fill distinct application roles across bakery and dessert occasions. Chocolate and caramel toppings benefit most directly from premium confectionery and visually driven retail bakery products, while whipping cream and cheese toppings are gaining momentum in café, brunch, and dessert-led formats. The social media has strengthened this demand pattern, because glazes, layered finishes, and visually striking toppings now function as product marketing tools as much as ingredients.

Fillings held 85.62% of the fillings and toppings market share in 2025, which shows how central they remain across the broadest range of bakery formats. Fruit fillings continue to benefit from a health-adjacent position that supports demand in premium retail bakery and functional-snacking concepts. Cream-based fillings remain important in large-volume industrial products such as cream-filled cookies and pastries, while chocolate fillings serve both premium confectionery and mass-market biscuit lines. A 2025 study in Applied Sciences on apple cream filling formulations for the pastry sector shows how much technical work still goes into viscosity control, texture stability, and sensory balance in premium fruit-cream formats. The cocoa price volatility is putting more direct cost pressure on chocolate fillings than on fruit or cream alternatives, which is quietly encouraging some industrial buyers to shift toward fruit and cream-based systems as part of cost management.

By Distribution Channel: Industrial Anchors Volume as Retail Outpaces on Growth

Retail is projected to expand at a 7.02% CAGR through 2026-2031, making it the fastest-growing route to market in the fillings and toppings market. This growth is tied to sustained home-baking engagement and to wider availability of premium finishing ingredients across supermarkets, convenience channels, and online retail stores. Online retail is particularly useful in countries where physical specialty food retail remains limited, because it broadens access to niche toppings and premium filling products without needing dense store networks. Puratos reported in 2025 that searches for "mini desserts near me" rose 400% and online conversations around mini tartlets increased 1,500% in the second quarter of 2025, which points to stronger interest in portion-controlled and premium-filled bakery formats. That shift supports retail demand for more specialized ingredient purchases and creates better shelf space prospects for premium packaged toppings and fillings.

Industrial accounted for 43.23% of the fillings and toppings market size in 2025, reflecting its role as the main procurement channel for large-scale bakery and confectionery manufacturers. Buyers in this channel prioritize bake stability, viscosity consistency, product documentation, and long-run production reliability, which tends to strengthen supplier lock-in. That procurement structure supports steady volumes for the fillings and toppings market, but it also slows reaction time to new flavor cycles compared with retail and foodservice channels. Foodservice sits between those two models, because it has meaningful upside from menu innovation while still requiring operational simplicity and ready-to-use systems. In the United States, the National Restaurant Association projects foodservice sales at USD 1.55 trillion in 2026, which supports incremental demand for toppings and fillings across café chains, casual dining outlets, and delivery-oriented kitchens[3]Source: National Restaurant Association, “2026 State of the Restaurant Industry,” National Restaurant Association, restaurant.org.

Geography Analysis

Europe held 37.31% of the fillings and toppings market share in 2025, which made it the largest regional market. The region benefits from Germany's scale in industrial bakery and from France's strong pastry and pâtisserie culture, both of which support steady demand for standardized fillings and premium finishing systems. Germany's bakery clusters support high-volume procurement of bake-stable fillings and topping systems, while clean-label preferences are pushing demand toward natural fruit fillings and plant-based cream alternatives. Italy, the Netherlands, Spain, Poland, Sweden, and the Benelux markets add further demand in artisanal and premium retail bakery, where ingredient quality and flavor provenance help support pricing power. European compliance also shapes the fillings and toppings market through Regulation EC No 1333/2008 and EFSA's food additive re-evaluation program, both of which are steering reformulation choices across the region.

Asia-Pacific is forecast to grow at a CAGR of 6.65% through 2026-2031, making it the fastest-growing regional segment in the fillings and toppings market. China, India, Japan, South Korea, Vietnam, Indonesia, Thailand, and Singapore are at different stages of bakery development, but each is seeing stronger demand from urban consumers and from wider exposure to Western-style café and bakery formats. In China, premium bakery chains are lifting demand for chocolate and fruit filling systems, while local flavor preferences such as matcha, taro, and black sesame are shaping more frequent development cycles. In India, organized retail expansion in 2024 added more shelf space for premium packaged bakery ingredients, while front-of-pack nutrition labeling requirements from FSSAI are pushing formulation priorities toward reduced-sugar and clean-label variants. Japan and South Korea remain early adopters of high-design topping systems and flavor-forward filled pastries, which gives the broader Asia-Pacific fillings and toppings market a premium innovation template that suppliers can adapt elsewhere.

North America remains the second-largest geography in the fillings and toppings market, led by the United States through its large food processing base, commercial bakery sector, and extensive foodservice network. Canada continues to support premium bakery growth, while Mexico's urban middle class is widening demand for both retail and foodservice-focused filling products. South America is led by Brazil and Argentina, where established bakery and confectionery traditions sustain baseline demand for filled and topped products. The Middle East and Africa remain smaller today, but investment in modern retail and quick-service restaurant chains across Gulf Cooperation Council markets is creating new demand for industrial and consumer-facing topping and filling solutions. Turkey also plays an important regional role through pastry culture and flour supply connectivity, which supports wider ingredient trade across the corridor.

Competitive Landscape

The fillings and toppings market is moderately consolidated, with Barry Callebaut, Cargill, Puratos, Kerry Group, and AGRANA operating with the broadest product reach and geographic coverage, while Zentis, Andros, Frujo, Bakels, Skjodt-Barrett, and Pecan Deluxe hold more focused positions by niche or region. Competition in the fillings and toppings market is centered on four priorities, which are reducing cocoa exposure, strengthening clean-label reformulation, building co-development capabilities, and expanding selectively in Asia-Pacific and Latin America. The same competitive direction can be seen in patent-backed formulation work, including the 2025 European Patent Office application for a reduced-saturated-fat filling free from palm oil, hydrogenated fats, and E-number additives. In the fillings and toppings market, that kind of R&D matters because regulatory compliance and consumer label expectations are now shaping development cycles much faster than before.

A clear opportunity area in the fillings and toppings market lies in regionally specific flavor systems for Asia-Pacific, where demand for localization runs deeper than what many global platform suppliers can currently deliver at scale. Another open space lies in shelf-stable, clean-label, dairy-free fillings for Western consumers who still want indulgent bakery experiences with a better-for-you profile. Smaller and mid-tier players such as Frujo a.s. and Skjodt-Barrett Foods are trying to compete through private-label agility and quicker reformulation cycles rather than global breadth. That gives them some room in accounts where speed and customization matter more than scale. The market still favors larger platforms in technically demanding categories, but faster-moving specialists can remain relevant where product adaptation cycles are short.

Kerry Group's February 2026 opening of its Medellín co-creation center shows another path, where suppliers deepen customer collaboration rather than simply add capacity. Barry Callebaut's partnership with NotCo's Giuseppe platform, which points to AI-assisted formulation as a practical tool for faster concept testing and shorter development cycles. Taken together, these moves suggest that the fillings and toppings market is not competing only on ingredient cost, but also on formulation speed, compliance readiness, and the ability to translate local taste signals into scalable commercial products.

Fillings and Toppings Industry Leaders

Barry Callebaut AG

Cargill Inc.

Puratos Group

Dawn Food Products Inc.

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ZYtaste expanded its bakery ingredient portfolio with the launch of a new range of baking fillings and sauces designed for commercial bakeries and food manufacturers. The new products offer enhanced bake stability, improved texture, rich flavor profiles, and extended shelf life, making them suitable for applications such as cakes, pastries, doughnuts, croissants, and other baked goods. T

- July 2025: Dawn Foods UK and Ireland expanded its Delifruit range by introducing five new ready-to-use fruit filling varieties: Pineapple, Mango, Forest Fruits, Apple & Cinnamon, and Blueberry. The new fillings were developed with high fruit content and enhanced bake, freeze-thaw, and cut stability to support a wide range of bakery applications.

- June 2025: Puratos and AMF jointly opened a cutting-edge pilot bakery at Puratos USA headquarters in Pennsauken, NJ. This facility accelerates innovation by allowing customers to collaborate on product development, optimize recipes, test ingredients, including toppings and fillings, and train bakery teams using advanced automation and sensory research tools.

Global Fillings and Toppings Market Report Scope

| Toppings | Sugar Toppings |

| Chocolate and Caramel Toppings | |

| Cheese | |

| Whipping Cream Toppings | |

| Others | |

| Fillings | Fruit Fillings |

| Cream-based Fillings | |

| Chocolate Fillings | |

| Others |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Stores | |

| Foodservice | |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Category | Toppings | Sugar Toppings |

| Chocolate and Caramel Toppings | ||

| Cheese | ||

| Whipping Cream Toppings | ||

| Others | ||

| Fillings | Fruit Fillings | |

| Cream-based Fillings | ||

| Chocolate Fillings | ||

| Others | ||

| Distribution Channels | Retail | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Stores | ||

| Foodservice | ||

| Industrial | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of fillings and toppings by 2031?

The fillings and toppings market is expected to reach USD 38.26 billion by 2031 from USD 30.21 billion in 2026, with a CAGR of 5.56% over 2026-2031.

Which product category holds the largest share?

Fillings led the product mix with 85.62% share in 2025, reflecting their broad use across pastries, cookies, cakes, and confectionery items.

Which route to market is growing the fastest?

Retail is the fastest-growing channel, with a projected CAGR of 7.02% through 2031, supported by home-baking activity and wider availability of premium packaged ingredients.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific is forecast to expand at a 6.65% CAGR through 2031 because urban bakery culture, café expansion, and demand for localized flavors are increasing across major markets.

Page last updated on: