Bake Stable Pastry Filling Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

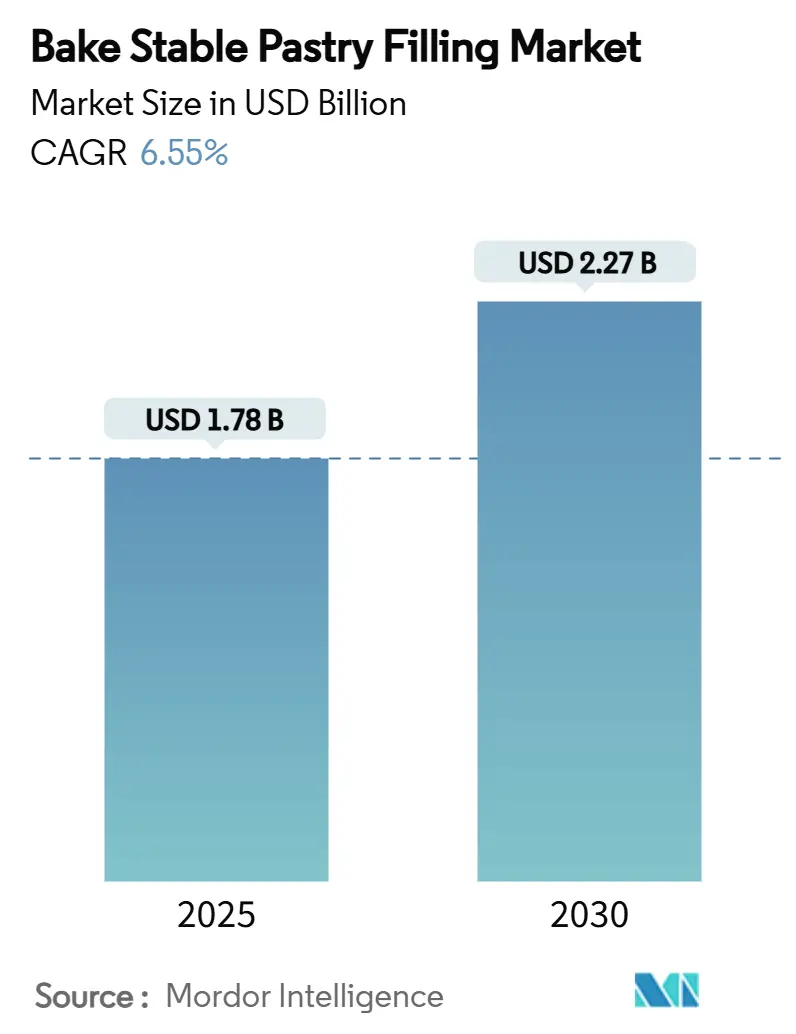

| Market Size (2025) | USD 1.78 Billion |

| Market Size (2030) | USD 2.27 Billion |

| Growth Rate (2025 - 2030) | 6.55% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bake Stable Pastry Filling Market Analysis by Mordor Intelligence

The bake stable pastry filling market size stood at USD 1.78 billion in 2025 and is forecast to reach USD 2.27 billion by 2030, registering a 6.55% CAGR. This steady climb reflects the accelerated adoption of automation in industrial bakeries, rising demand for frozen and thaw-bake formats, and ongoing clean-label reformulation efforts that favor heat-resistant fillings. Strengthening low-water-activity hydrocolloid systems enables producers to extend shelf life without synthetic preservatives, while single-dose piping technologies reduce production cycles and mitigate food-safety risks. Europe remains the largest regional consumer, supported by stringent labeling rules and established artisanal traditions now scaling industrially. At the same time, the Middle East and Africa advance quickly on the back of urbanization and international chain expansion, creating white-space opportunities for suppliers able to handle long logistical routes.

Key Report Takeaways

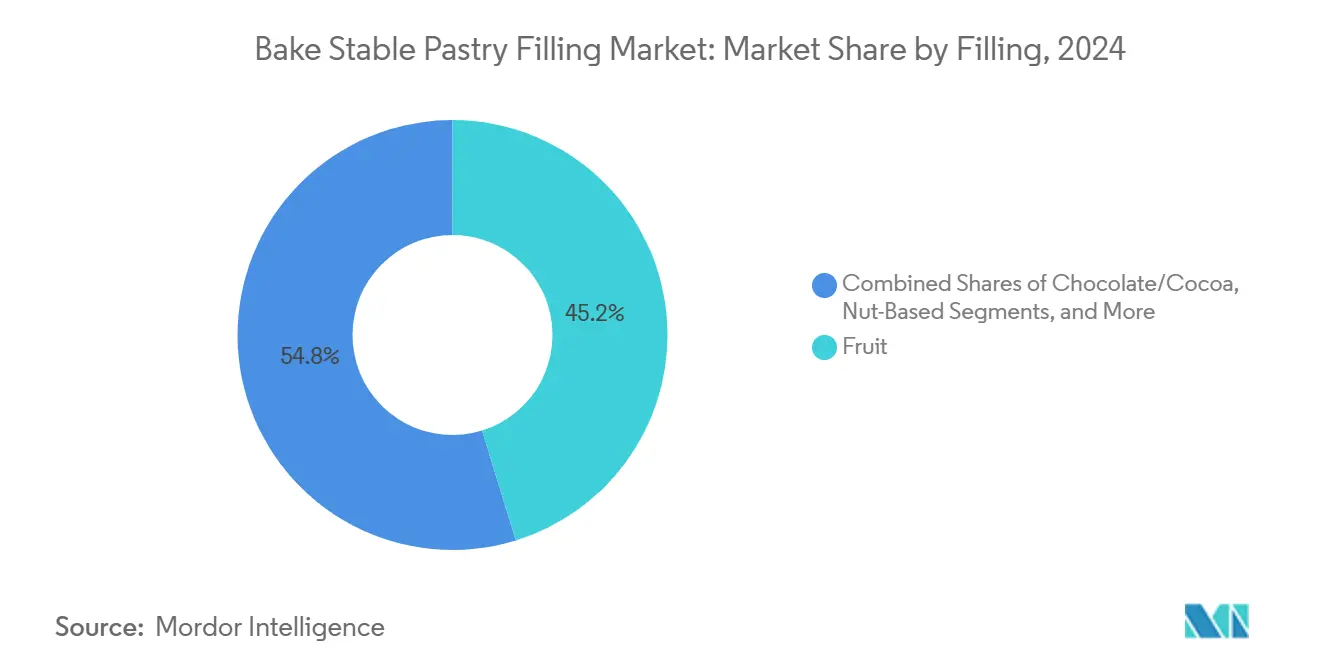

- By filling type, fruit captured 45.23% of the bake stable pastry filling market share in 2024, whereas chocolate/cocoa is projected to expand at a 6.88% CAGR through 2030.

- By form, smooth/pureed held 48.67% share of the bake stable pastry filling market in 2024, while chunky/particulate records the highest projected CAGR at 7.20% to 2030.

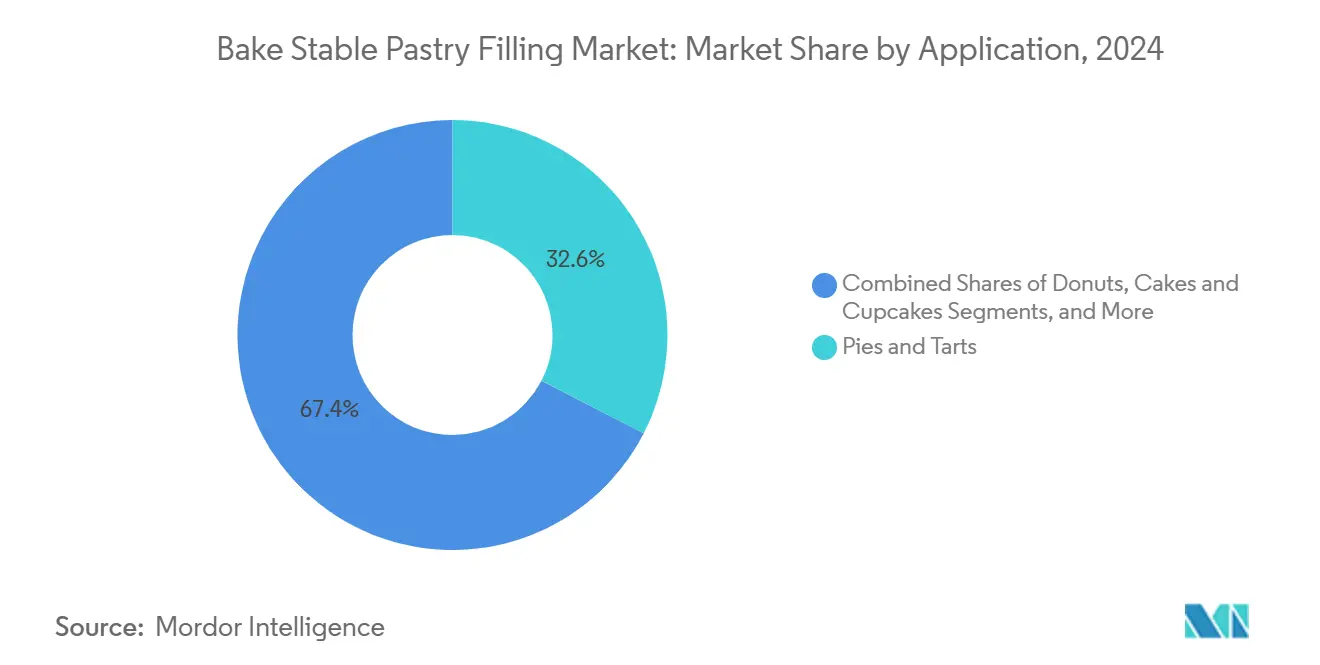

- By application, pies and tarts accounted for a 32.56% share of the bake stable pastry filling market size in 2024, and Danish & croissants are advancing at a 7.50% CAGR through 2030.

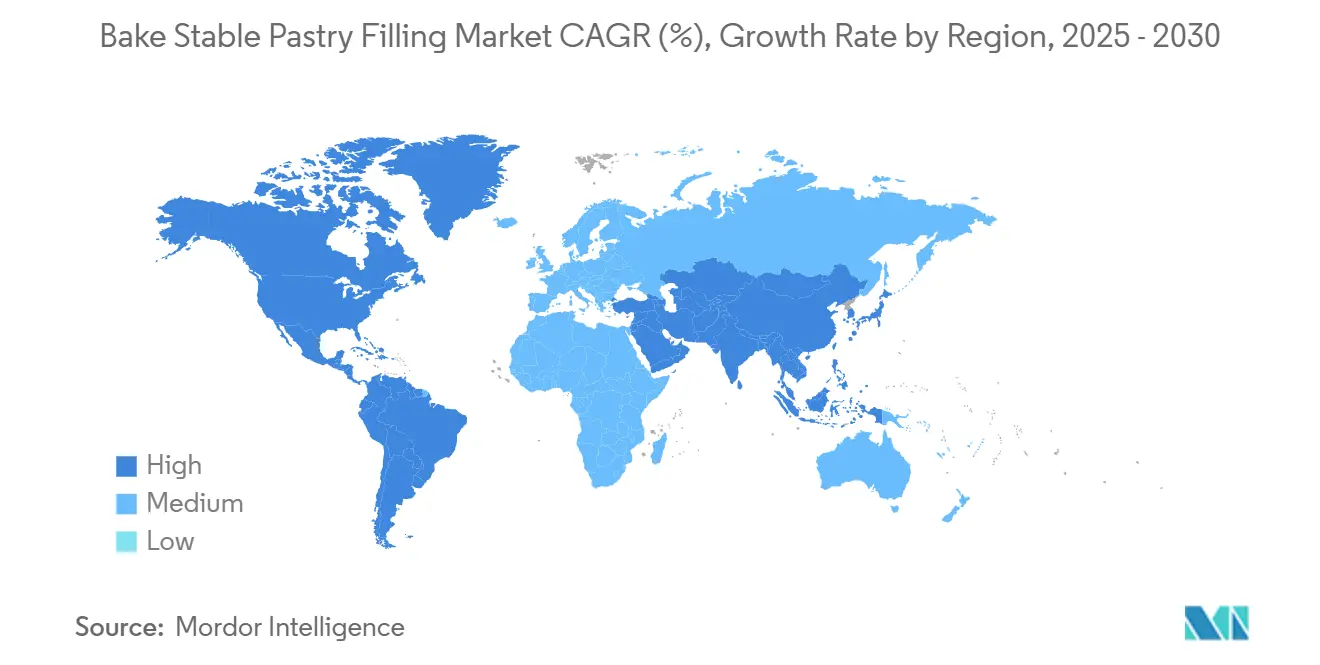

- By geography, Europe led with 35.89% of the bake stable pastry filling market share in 2024; the Middle East and Africa are forecast to expand at a 7.45% CAGR through 2030.

Global Bake Stable Pastry Filling Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for convenience-ready bakery ingredients | +1.2% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| Rapid growth of frozen & thaw-bake channels | +1.1% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Trend Toward Clean Label & Natural Ingredients | +0.9% | Europe & North America core, expanding to APAC | Long term (≥ 4 years) |

| Expansion of Frozen and Pre-baked Bakery Sectors | +0.8% | Global, with Increasing Demand in North America | Medium term (2-4 years) |

| Advanced low-water-activity hydrocolloid systems | +0.7% | North America & EU, with technology transfer to emerging markets | Long term (≥ 4 years) |

| Single-dose industrial piping solutions | +0.6% | Global, with increasing expansion of Industrial bakeries globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Demand for Convenience-Ready Bakery Ingredients

Commercial baking operations are experiencing fundamental changes due to labor shortages and efficiency requirements, leading to increased adoption of pre-formulated solutions. Industrial bakeries now focus on ingredients that reduce preparation time while maintaining consistent quality across production batches. The Indonesian bakery market demonstrates this shift, with annual growth exceeding 10% and ingredient imports accounting for 70% of the market, indicating a clear preference for standardized, ready-to-use formulations. In 2023, 53% of baking companies increased their capital investments, with spending reaching 14.1% of revenue, according to Baking Business. Bake-stable pastry fillings have emerged as a key beneficiary of this trend, as they eliminate refrigerated storage requirements and complex preparation processes while ensuring consistent performance across various baking applications.

Rapid Growth of Frozen & Thaw-Bake Channels

The frozen and thaw-bake distribution channels are experiencing rapid growth in bake-stable pastry fillings, primarily due to quick-service restaurant expansion and retail bakery automation. These channels extend product shelf life from days to months while preserving taste and texture characteristics during final preparation. The technology helps bakeries reduce waste, manage inventory efficiently, and maintain consistent quality across locations. Frozen bakery products utilize five production technologies, including pre-fermented, par-baked, and fully baked formats, each requiring specific filling formulations that maintain stability during freeze-thaw cycles. This growth increases demand for freeze-thaw stable fillings, advancing developments in hydrocolloid systems and moisture management technologies that preserve texture throughout the cold chain.

Trend Toward Clean Label and Natural Ingredients

Consumer demand for clean labels is reshaping bake-stable pastry filling formulations, as buyers closely examine ingredient lists and seek transparency in food production. This shift requires manufacturers to replace synthetic preservatives and stabilizers with natural alternatives, creating both opportunities and technical challenges in product development. Natural preservatives derived from herbs demonstrate significant effectiveness in reducing rancidity in low-moisture bakery products. Specifically, hop, chamomile, and nettle extracts reduce peroxide values while enhancing nutritional profiles through their inherent antioxidant properties. However, manufacturers face multiple challenges in this transition, including achieving comparable functionality to synthetic ingredients, ensuring consistent product quality, maintaining shelf stability, and managing production costs while remaining competitive in the market. The integration of these natural alternatives also requires careful consideration of their impact on taste, texture, and overall product performance.

Expansion of Frozen and Pre-baked Bakery Sectors

The frozen and pre-baked bakery market generates consistent demand for bake stable pastry fillings, as these enable efficient mass production and distribution of partially prepared products. This market growth aligns with retail strategies that combine fresh-baked offerings with operational efficiency and cost management. Pre-baked items need fillings that maintain quality through multiple processing stages, including initial baking, freezing, storage, and reheating. These fillings must retain their texture, flavor, and structural integrity throughout the entire production and consumption cycle. The market shows significant expansion in emerging economies, where the rise of modern retail formats and evolving consumer preferences increases the demand for convenient bakery products. This growth is further supported by urbanization, rising disposable incomes, and the increasing adoption of Western-style bakery products in these regions.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevace | Impact Timeline |

|---|---|---|---|

| Volatility in fruit raw-material prices | -0.8% | Global, with acute impact in import-dependent regions | Short term (≤ 2 years) |

| Stringent global food-safety shelf-life rules | -0.5% | Europe & North America, expanding to emerging markets | Long term (≥ 4 years) |

| Limited clean-label preservative options | -0.4% | Europe & North America core, spreading globally | Medium term (2-4 years) |

| Hydrocolloid supply bottlenecks (LBG/guar) | -0.3% | Global, with regional supply concentration risks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Fruit Raw-Material Prices

Fruit raw-material price volatility creates significant margin pressure for stable pastry filling manufacturers, particularly those specializing in fruit-based variants that command 45.23% market share. Agricultural commodity prices face upward pressure from fertilizer cost increases, climate variability, and geopolitical disruptions affecting global supply chains. The OECD-FAO[1]OECD-FAO, “Agricultural Outlook 2023-2032,” oecd-ilibrary.orgAgricultural Outlook projects a 1.3% annual increase in global food consumption, with rising input costs translating to higher commodity prices that directly impact filling manufacturers' cost structures. Fruit preparation specialists like AGRANA, which holds approximately 40% global market share in fruit preparations, must navigate these price fluctuations while maintaining competitive positioning. Price volatility particularly affects manufacturers serving price-sensitive market segments, forcing difficult decisions between margin compression and market share preservation. The challenge intensifies for companies committed to sustainable sourcing practices, as premium fruit ingredients command higher prices while facing the same underlying commodity pressures.

Stringent Global Food-Safety Shelf-Life Rules

Stringent global food-safety shelf-life regulations impose substantial compliance costs and technical challenges on bake stable pastry filling manufacturers. Regulatory frameworks like the FDA's[2]Food and Drug Administration, "Food Safety Modernization Act (FSMA)", www.fda.gov Food Safety Modernization Act (FSMA) require extensive validation studies and documentation to demonstrate product safety throughout declared shelf life periods. The European Union's Regulation (EC) 2073/2005 on microbiological criteria for foodstuffs establishes specific requirements for ready-to-eat products, including pastry fillings, that must remain safe throughout their shelf life, according to the Food Standards Scotland[3]Food Standards Scotland, “Shelf-life guidance,” www.foodstandards.gov.scot. Compliance requires sophisticated testing protocols, including accelerated shelf-life studies, predictive microbiology modeling, and continuous monitoring systems that add significant operational costs. The regulatory burden disproportionately affects smaller manufacturers who lack the resources for extensive validation studies, potentially consolidating market share toward larger players with established regulatory expertise. Water activity (Aw) and pH measurements become critical control points, requiring specialized equipment and trained personnel to ensure consistent compliance across production batches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filling Type: Fruit Fillings Lead Market Share as Chocolate Innovations Drive Growth

Fruit fillings dominated the market with a 45.23% share in 2024, supported by established consumer preferences and robust supply chain networks. Chocolate/cocoa fillings are projected to grow at 6.88% CAGR through 2030, driven by premium product demand and innovative cocoa alternatives. The significant increase in cocoa prices, which rose 400% between 2023 and 2024, has led to the development of wheat-based cocoa substitutes capable of replacing up to 25% of conventional cocoa while retaining taste characteristics. The declining costs of vanilla have positively impacted custard and cream fillings, potentially increasing their market presence after previous price-driven substitutions.

Nut-based fillings are gaining traction due to increasing health awareness, while savory and meat & cheese fillings expand into breakfast and snack categories. Specialty fillings, including unique fruit blends and functional ingredients, cater to premium market segments where product differentiation yields higher margins. The industry continues to adapt to consumer preferences for distinctive flavors and healthier options, with manufacturers developing plant-based alternatives and reduced-sugar options. AGRANA's development of customized fruit preparations exemplifies the necessity of specialized solutions across filling applications.

By Form: Smooth Textures Lead Despite Chunky Growth

The smooth/pureed form segment holds 48.67% market share in 2024, due to its versatile applications and consistent manufacturing processes that ensure uniform quality across production batches. The chunky/particulate fillings segment is growing at 7.20% CAGR through 2030, driven by consumer preferences for authentic textures and premium positioning. Suspension-stabilized forms combine texture variety with the processing benefits of smooth formulations through hydrocolloid systems. Form selection is crucial in frozen and thaw-bake applications, where texture stability during temperature changes determines product performance.

Manufacturing requirements influence form selection, as smooth fillings work efficiently with automated piping systems, while chunky variants need specialized equipment to maintain particle integrity. Applications determine texture preferences - pie and tart fillings typically use chunky forms for visual appeal, while cake and cupcake applications use smooth formulations for even distribution. Allulose shows potential in improving product freshness across all forms, with studies showing better moisture retention and reduced starch retrogradation that extends shelf life. The form segmentation demonstrates the industry's advancement in texture control, where hydrocolloid technology helps manufacturers achieve specific mouthfeel properties while meeting thermal stability requirements.

By Application: Traditional Pies and Tarts Lead, While Danish Croissants Surge

Pies and tarts hold the dominant market position with a 32.56% share in 2024, due to their established consumer base and the effectiveness of bake stable fillings in high-temperature, extended baking processes. Danish pastries and croissants show the highest growth rate at 7.50% CAGR through 2030, supported by the expansion of artisanal bakeries and premium breakfast offerings. This growth aligns with evolving breakfast preferences and the increase in specialty coffee establishments offering premium pastries. Cakes and cupcakes maintain steady demand, while donut applications grow through quick-service breakfast outlets and round-the-clock convenience stores.

The cookies and biscuits segment requires specific formulations that address low moisture content needs and extended shelf life requirements. Specialty pastries and ethnic baked goods offer market differentiation opportunities through distinct flavors and traditional authenticity. Each application requires precise thermal profile matching, with baking processes needing specific filling formulations for optimal results. CSM Ingredients has developed specialized reduced-fat emulsions for laminated products, demonstrating the technical requirements for various applications. The growth in Danish pastries and croissants aligns with clean label preferences, as consumers associate these items with artisanal quality and natural ingredients.

Geography Analysis

Europe maintains its position as the dominant regional market with 35.89% share in 2024, driven by sophisticated regulatory frameworks that favor clean label solutions and established artisanal bakery traditions transitioning to industrial-scale operations. Germany, France, and the United Kingdom represent the largest individual markets, where established bakery chains and specialty retailers create sustained demand for consistent, high-quality filling solutions. The Netherlands and Spain serve as processing and distribution hubs for broader European markets. While European growth through 2030 will moderate as markets mature, the region's emphasis on sustainability and clean label innovation supports long-term value creation. The European Union's Deforestation Regulation (EUDR) influences cocoa-based filling formulations, driving innovation in alternative ingredients and sustainable sourcing practices.

The Middle East and Africa region demonstrates the fastest growth rate at 7.45% CAGR through 2030, driven by rapid urbanization, expanding middle-class populations, and improved infrastructure supporting modern retail formats. The United Arab Emirates functions as a regional hub for international bakery chains and ingredient suppliers, while South Africa provides access to sub-Saharan markets with increasing consumer purchasing power. The region benefits from young demographics, evolving dietary patterns, and the expansion of shopping malls and quick-service restaurants. Investments in cold chain infrastructure and food safety systems create opportunities for bake-stable pastry fillings that maintain quality in challenging distribution conditions.

North America's market emphasizes convenience and health-conscious formulations, creating demand for clean label solutions and functional ingredients. The region's frozen food distribution networks require products with enhanced freeze-thaw stability. In Asia-Pacific, Japan and Australia prioritize premium quality and innovation, while China and India focus on accessibility and value positioning. Indonesia's bakery market, growing at 10% annually with 70% imported ingredients, demonstrates the region's expansion potential. South America's growth centers on Brazil and Argentina, where urban development and retail modernization drive demand for international bakery concepts and ingredients.

Competitive Landscape

The bake stable pastry filling market maintains moderate concentration, reflecting balanced dynamics between multinational ingredient suppliers and specialized filling manufacturers. Market leadership is distributed among companies with specific competitive strengths: Puratos Group utilizes its global presence and sustainability programs, Dawn Foods focuses on innovation and customer service, while AGRANA Beteiligungs-AG controls approximately 40% of the global fruit preparations market share.

The market structure reflects the technical requirements of bake-stable formulations, where expertise in thermal stability, moisture management, and clean-label compliance creates entry barriers for smaller manufacturers. This consolidation trend indicates that clean label compliance and sustainability now significantly influence market position. Growth opportunities remain in emerging markets, where specific local taste preferences and regulations create demand for specialized formulations not yet developed by global manufacturers.

Companies differentiate themselves through technology investments in automation, single-dose piping systems, and preservation methods to improve operational efficiency while maintaining product standards. The market maintains balanced competition due to required technical expertise, importance of customer relationships, and diverse application needs that prevent market dominance by any single company across all segments and regions.

Bake Stable Pastry Filling Industry Leaders

-

Puratos Group

-

Dawn Foods

-

AGRANA Beteiligungs-AG

-

CSM Ingredients

-

Bakels Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Cargill expanded its coatings and fillings plant in Deventer, Netherlands, increasing production capacity by 60% to meet rising demand from European bakery, confectionery, and food manufacturers.

- June 2023: British Bakels launched a new range of fruit fillings—Strawberry, Dark Cherry, Wild Blueberry, and Lemon Creamy—under its Ta-Da! Home Baking Line, expanding its offerings to include vegan, bake-stable, and freeze-thaw stable fillings for home bakers.

- February 2023: Dawn Foods launched its Delifruit Xtra range of fruit fillings, which contain 80% fruit and have 30% less sugar and calories compared to the market average. The new fillings, available in strawberry, blueberry, cherry, and mango & passionfruit flavors, are bake-, freeze-, and cut-stable, as well as suitable for vegetarian and vegan applications.

Global Bake Stable Pastry Filling Market Report Scope

| Fruit |

| Chocolate/Cocoa |

| Custard & Cream |

| Nut-Based |

| Savory/Meat & Cheese |

| Other Specialty |

| Smooth/Pureed |

| Chunky/Particulate |

| Suspension-Stabilized |

| Pies & Tarts |

| Cakes & Cupcakes |

| Donuts |

| Danish & Croissants |

| Cookies & Biscuits |

| Other Bakery |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South America | |

| Rest of Middle East and Africa |

| By Filling Type | Fruit | |

| Chocolate/Cocoa | ||

| Custard & Cream | ||

| Nut-Based | ||

| Savory/Meat & Cheese | ||

| Other Specialty | ||

| By Form | Smooth/Pureed | |

| Chunky/Particulate | ||

| Suspension-Stabilized | ||

| By Application | Pies & Tarts | |

| Cakes & Cupcakes | ||

| Donuts | ||

| Danish & Croissants | ||

| Cookies & Biscuits | ||

| Other Bakery | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South America | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the bake stable pastry filling market and its projected growth to 2030?

The market is valued at USD 1.78 billion in 2025 and is forecast to reach USD 2.27 billion by 2030, growing at a 6.55% CAGR.

Which filling type commands the largest share within bake-stable pastries?

Fruit fillings lead with 45.23% share in 2024 due to familiar taste profiles and versatile use in pies, tarts, and Danish pastries.

Which region shows the fastest future growth for bake-stable pastry fillings?

Middle East and Africa is projected to grow at a 7.45% CAGR through 2030, driven by urbanization and quick-service chain expansion.

How are clean-label demands influencing formulation strategies?

Producers increasingly replace synthetic preservatives with natural gums, pectin, and herbal extracts to satisfy label transparency without losing heat stability.

Page last updated on: