Femoral Head Prostheses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.41 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

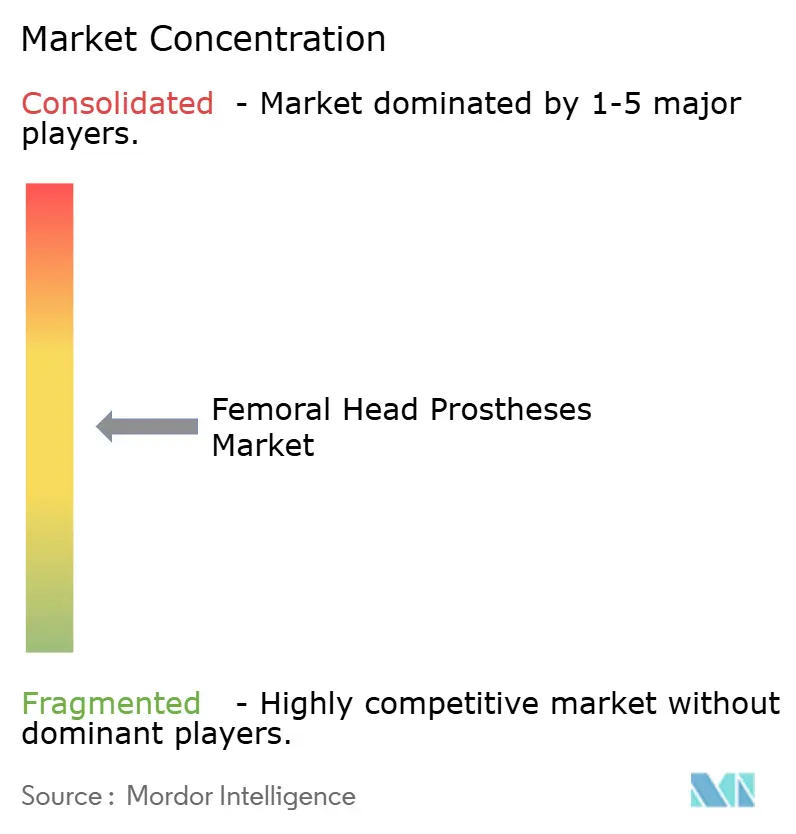

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Femoral Head Prostheses Market Analysis by Mordor Intelligence

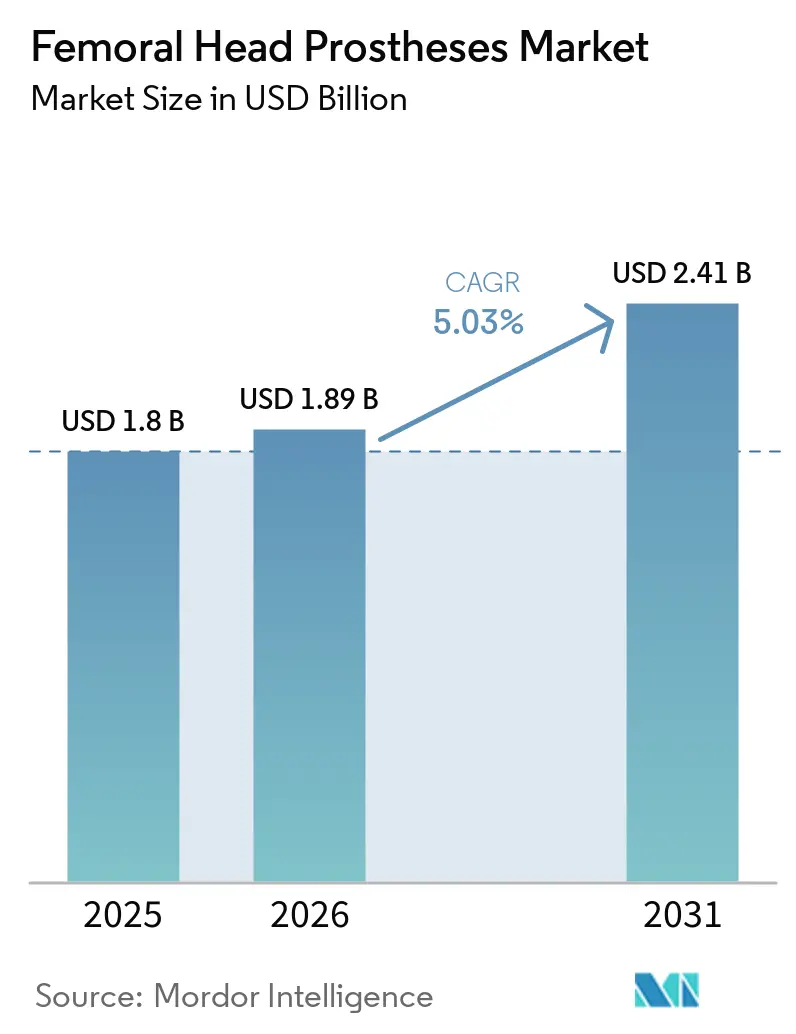

The Femoral Head Prostheses Market size is expected to increase from USD 1.8 billion in 2025 to USD 1.89 billion in 2026 and reach USD 2.41 billion by 2031, growing at a CAGR of 5.03% over 2026-2031.

The rising incidence of hip fractures among older adults continues to drive demand, with a global age-standardized incidence rate of 930.73 per 100,000 in 2021. Projections estimate 16.8 million cases by 2036, with 75% of this increase attributed to population aging.[1]Chuwei Tian, Liu Shi et al., “Global, Regional, and National Burden of Hip Fractures Attributable to Falls in Older Adults,” Frontiers in Public Health, frontiersin.org. Procedure trends favor arthroplasty over conservative care. An Italian review of over 1.12 million femoral neck fracture records showed Total Hip Arthroplasty (THA) usage rising from 13.3% to 24.3%, partial hip arthroplasty increasing from 40.0% to 44.5%, and conservative treatment declining from 27.5% to 14.6% between 2001 and 2023.[2]M. Bortolin et al., “Incidence Rates and Treatment of the Transcervical Fracture of the Neck of Femur in Italy, Trends Between 2001 and 2023,” Journal of Orthopaedics and Traumatology, link.springer.com.

Key Report Takeaways

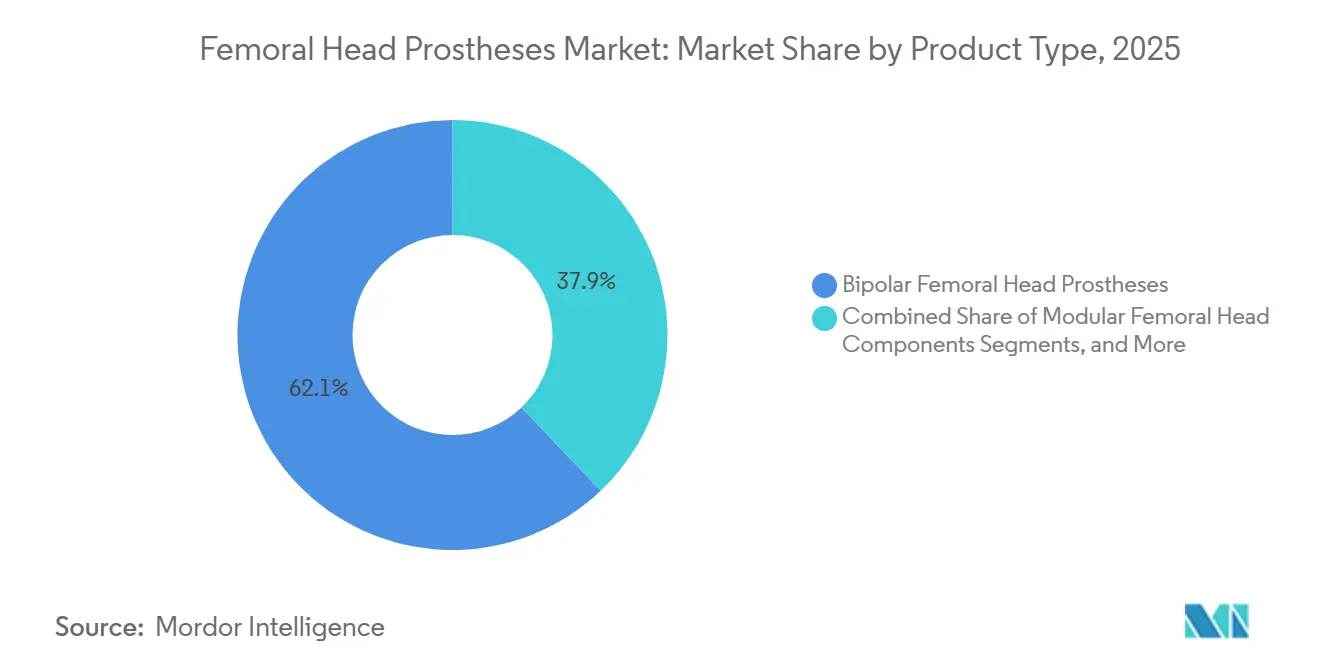

- By product type, bipolar femoral head prostheses held 62.10% of revenue in 2025, while modular femoral head components are projected to grow at 6.90% CAGR through 2031.

- By material, cobalt-chromium alloy accounted for 48.85% of revenue in 2025, while ceramic is forecasted to expand at 7.20% CAGR through 2031.

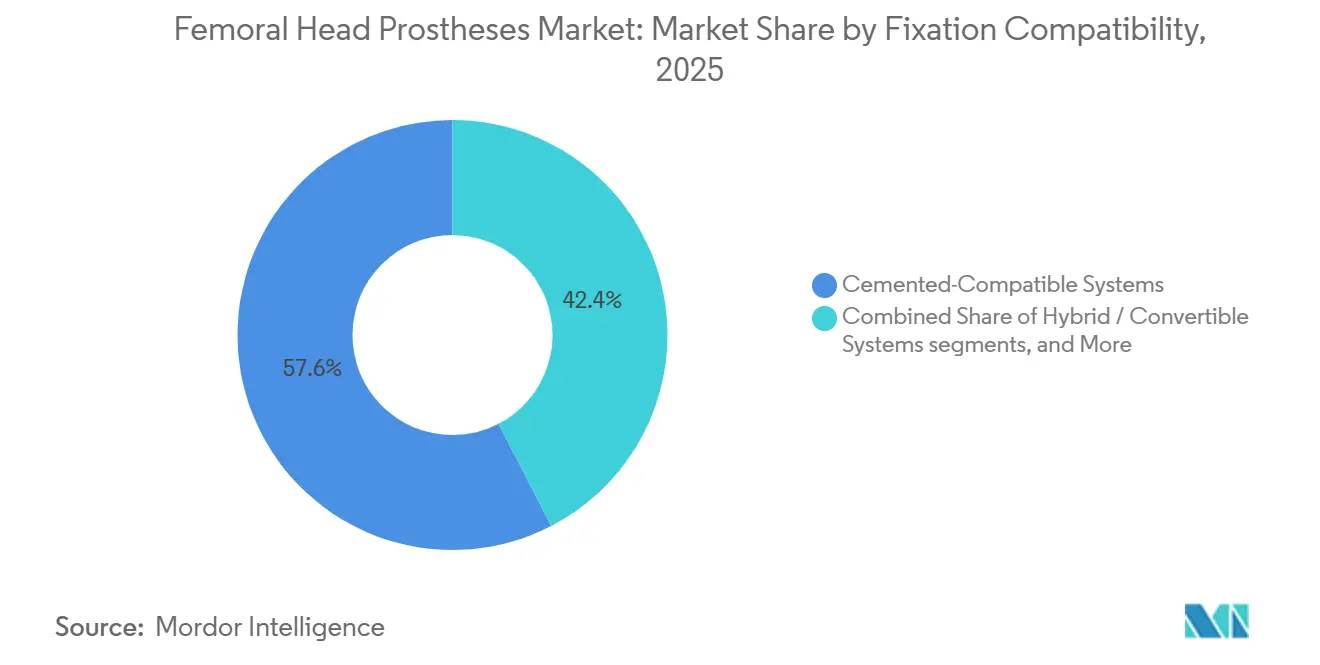

- By fixation compatibility, cemented-compatible systems captured 57.60% of revenue in 2025, while cementless-compatible systems are projected to grow at 6.40% CAGR through 2031.

- By procedure type, total hip arthroplasty represented 54.10% of revenue in 2025, while hemiarthroplasty for displaced femoral neck fracture is forecasted to advance at 6.60% CAGR through 2031.

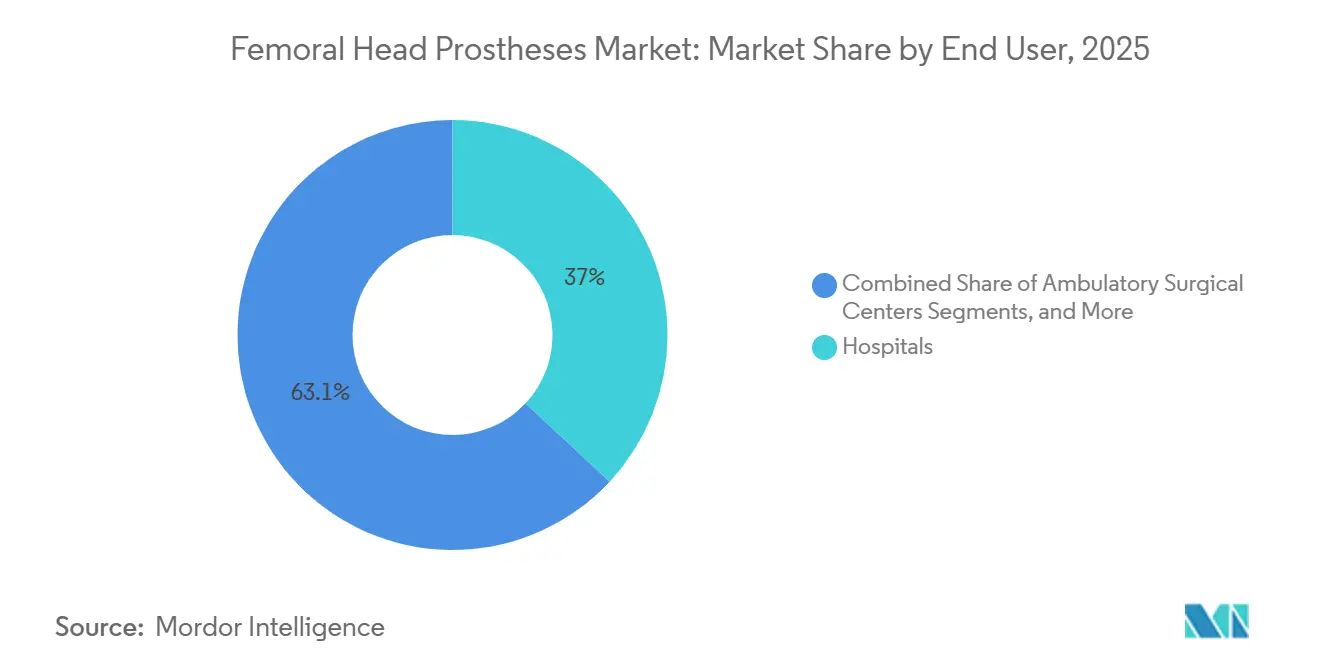

- By end user, hospitals contributed 36.95% of revenue in 2025, while ambulatory surgical centers are projected to grow at 7.50% CAGR through 2031.

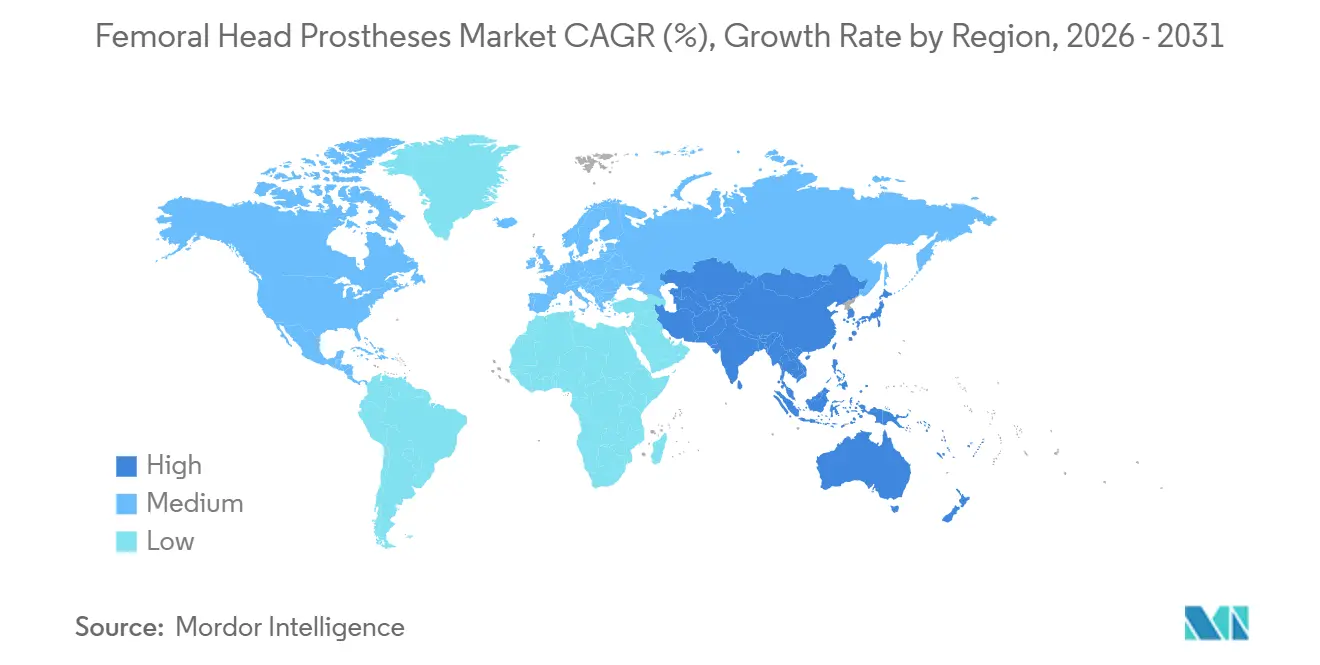

- By geography, North America commanded 41.95% of revenue in 2025, while Asia-Pacific is expected to expand at 8.30% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Femoral Head Prostheses Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising displaced femoral neck fracture burden in aging population | +1.5% | Global, concentrated in North America, Western Europe, and East Asia | Long term (≥ 4 years) |

| Arthroplasty preference over fixation for unstable fractures | +1.0% | North America and Europe, with spillover to core Asia-Pacific markets | Medium term (2-4 years) |

| Cemented stem adoption in osteoporotic fracture care | +0.8% | Global, particularly Europe and Japan | Medium term (2-4 years) |

| Faster-recovery surgical workflows and muscle-sparing approaches | +0.7% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Registry-led shift toward validated stem and head platforms | +0.5% | North America, Europe, and Australia | Medium term (2-4 years) |

| SKU renewal from MDR recertification favoring scaled suppliers | +0.4% | Europe primarily, with spillover to CE Mark-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Displaced Femoral Neck Fracture Burden In Aging Population

The femoral head prostheses market continues to find strong support from the aging global population, as the incidence of fractures rises steadily despite funding fluctuations. A 2025 analysis highlighted a global age-standardized prevalence rate of 1,834.14 per 100,000 in 2024, reflecting a 14.2% increase from 1990 levels. The study projected 16.8 million global hip fracture cases by 2036, driven by population aging and growth. In the United States, hip fractures currently affect over 250,000 individuals annually, with projections reaching 500,000 by 2050, ensuring consistent demand for fracture-related implants. T

Arthroplasty Preference Over Fixation For Unstable Fractures

The femoral head prostheses market benefits from a clear shift toward arthroplasty for unstable fractures. A 2025 review of 20 systematic studies involving 29,980 patients showed that Total Hip Arthroplasty (THA) reduced revision risk by 33% and improved early functionality compared to hemiarthroplasty, despite a 20-minute longer surgery.[3]“Total Hip Arthroplasty Versus Hemiarthroplasty for Displaced Femoral Neck Fracture, An Overview of Systematic Reviews,” Journal of Orthopaedic Surgery and Research, link.springer.com. Hemiarthroplasty remains relevant for older patients with limited mobility due to shorter operation times and reduced anesthesia exposure. Bipolar implants are increasingly used in patients over 75 with higher frailty and comorbidities. In 2023, partial arthroplasty accounted for 44.5% of femoral neck fracture treatments in Italy, reflecting a selective role for hemiarthroplasty within the market.

Cemented Stem Adoption In Osteoporotic Fracture Care

Cemented fixation remains critical in the femoral head prostheses market, as osteoporotic bones often lack the stability required for press-fit solutions. A 2024 study in northeast China reported that femoral neck fractures constituted 62.9% of hip fractures in males, while only 4.7% to 8.6% of patients had received anti-osteoporotic treatment prior to the fracture.[4]W. Lozano et al., “A Real-World Analysis of 1,823 Hospitalized Osteoporotic Fractures in Northeast China,” Frontiers in Endocrinology, frontiersin.org. This treatment gap sustains unplanned fracture volumes, driving demand for fixation methods that ensure immediate stability. Cemented systems support early weight-bearing, crucial for elderly patients at higher risk of complications from delayed mobilization. Advanced polyethylene combinations are increasingly used to manage wear and taper damage without significantly raising costs. As registry use expands in mature health systems, fixation choices are expected to align more closely with patient profiles favoring cemented implants.

Faster-Recovery Surgical Workflows And Muscle-Sparing Approaches

Efforts to enhance efficiency in hospitals and outpatient centers are reshaping the femoral head prostheses market, with a focus on faster recovery pathways, shorter stays, and reduced tray burdens. Muscle-sparing approaches, such as anterior methods, emphasize compact instrumentation, shorter stem options, and designs suited for constrained surgical fields. R&D is increasingly focused on modular systems that allow surgeons to adjust offset, length, and fit without expanding instrument footprints.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Total hip arthroplasty and dual-mobility substitution in fitter elderly | -0.8% | North America and Western Europe | Medium term (2-4 years) |

| Tender-driven pricing pressure and bundled trauma episode economics | -0.6% | Europe and China | Short term (≤ 2 years) |

| MDR recertification cost and portfolio rationalization | -0.5% | Europe primarily, with spillover to CE Mark-dependent markets | Short term (≤ 2 years) |

| Medico-legal overhang on taper and head-related failures | -0.3% | North America, the United Kingdom, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Total Hip Arthroplasty And Dual-Mobility Substitution In Fitter Elderly

Healthier elderly patients are increasingly choosing Total Hip Arthroplasty (THA) and dual-mobility constructs, driving demand in the femoral head prostheses market. A 2025 systematic review and meta-analysis highlighted that dual-mobility THA demonstrated superior functional outcomes and fewer long-term complications compared to bipolar hemiarthroplasty in select geriatric femoral neck fracture cases. This trend is most evident among active patients aged 60 to 79, who are cognitively intact and prioritize minimizing revision risks over their extended lifespan. Surgeons are now more proactive in addressing the acetabulum in these patients to mitigate potential cartilage wear or future conversion challenges.

Tender-Driven Pricing Pressure And Bundled Trauma Episode Economics

The femoral head prostheses market faces pricing constraints due to tender-driven structures and bundled trauma economics, which limit hospital spending on standardized implants. In Europe, regional procurement favors suppliers with broad certified portfolios, creating challenges for smaller companies with limited product ranges. Similarly, in China, volume-based purchasing reduces unit prices, restricting premium positioning opportunities in high-volume trauma care. Advanced materials like ceramic and oxidized zirconium face budget approval challenges, as their clinical benefits are weighed against the combined costs of implants, surgery, and rehabilitation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bipolar Dominance Persists As Modularity Gains Clinical Ground

In 2025, bipolar femoral head prostheses held 62.10% of the market share, maintaining their leadership in displaced femoral neck fracture care. Their clinical advantages, including shorter procedures and reduced acetabular wear, make them ideal for elderly patients. Unipolar and endocephalic devices remain relevant in cost-sensitive markets, while modular components, projected to grow at 6.90% CAGR through 2031, gain traction for their intraoperative flexibility and ability to address revision complexities.

By Material: Ceramic Adoption Accelerates On Registry-Validated Outcomes

Cobalt-chromium alloy accounted for 48.85% of the market share by material in 2025, driven by its cost-effectiveness and surgeon familiarity. Stainless steel continues to decline in favor of materials with better long-term performance. Ceramic, forecasted to grow at 7.20% CAGR through 2031, is gaining popularity for its lower wear and revision risks, particularly among younger, active patients. The market is shifting towards proven materials with validated outcomes and consistent manufacturing standards.

By Fixation Compatibility: Cemented Systems Lead While Cementless Gains In Younger Cohorts

Cemented-compatible systems dominated with 57.60% of the market share in 2025, reflecting their reliability in osteoporotic elderly patients and suitability for acute trauma care. Cementless systems, projected to grow at 6.40% CAGR through 2031, are increasingly preferred for younger patients with better bone quality. Hybrid and convertible systems are gaining attention for their adaptability in intraoperative fixation strategies and future reconstructive needs.

By Procedure Type: Fracture-Driven Hemiarthroplasty Sustains Core Volume

Total hip arthroplasty (THA) represented 54.10% of the market share by procedure type in 2025, driven by its role in elective reconstructions. Hemiarthroplasty, forecasted to grow at 6.60% CAGR through 2031, is expanding due to the aging trauma population and rising fracture incidence. Revision procedures and hemi-to-total conversions are gaining relevance as earlier implants age, emphasizing the importance of modularity and material durability in complex cases.

By End User: Hospitals Anchor Volume While ASCs Drive Faster Growth

Hospitals accounted for 36.95% of the market revenue in 2025, reflecting their role in managing complex hip fractures and elderly trauma care. Specialty orthopedic centers focus on elective THA and revisions, while ambulatory surgical centers (ASCs), projected to grow at 7.50% CAGR through 2031, are driving growth by shifting select arthroplasty cases to cost-effective outpatient settings. ASCs prioritize efficient instrumentation and components compatible with minimally invasive techniques.

Geography Analysis

In 2025, North America held a 41.95% share of the femoral head prostheses market, driven by premium implant demand and clinical adoption. The United States led this trend due to a high incidence of hip fractures, established arthroplasty reimbursements, and rapid surgeon adoption of validated implants. Age-adjusted mortality from femoral neck fractures in the United States declined from 39.6 per 100,000 in 2002 to 22.4 per 100,000 in 2023. Improved outcomes have increased the focus on revision management, material choice, and survivorship. Canada and Mexico contributed smaller shares, with Mexico benefiting from medical tourism by price-sensitive United States patients.

Asia-Pacific is projected to grow at a CAGR of 8.30% through 2031, making it the fastest-growing region in the femoral head prostheses market. Aging populations in China, Japan, and South Korea, along with expanding surgical capacity in India and Southeast Asia, are driving growth. The region’s unmet needs mean even modest improvements in diagnosis, trauma referrals, and operating capacity can significantly boost procedure volumes. In China, stricter implant classifications are improving supplier quality but may delay market entry for new players.

Europe remains a key market for femoral head prostheses, supported by mature arthroplasty pathways, widespread cemented fracture care, and strong registry systems. Western Europe favors validated implant platforms, while Eastern Europe offers growth potential in cost-sensitive cemented trauma procedures. In South America, Brazil dominates the market, with suppliers focusing on price-conscious demand through scaled distribution. The Middle East and Africa contribute a smaller share, but GCC investments in specialized orthopedic centers are creating opportunities for high-value cases.

Competitive Landscape

Leading players such as Zimmer Biomet, Stryker, Johnson & Johnson MedTech, and Smith & Nephew dominate the femoral head prostheses market by leveraging their scale, distribution networks, and strong surgeon relationships. Competition now extends beyond implants, as hospitals and surgeons prioritize evidence support, material options, instrument efficiency, and procedural compatibility. Companies with extensive clinical data and a broad installed base maintain market share more effectively, while opportunities for differentiation remain in materials, minimally invasive techniques, and outpatient-friendly configurations. This dynamic ensures the market remains competitive for both large-cap and specialized players.

Zimmer Biomet expanded its orthopedic platform in October 2025 by acquiring Monogram Technologies, integrating AI-driven semi-autonomous robotics to strengthen joint reconstruction workflows. In September 2025, the company received Japan PMDA approval for its iodine-treated total hip replacement system, showcasing its focus on innovative implant designs for market access and premium positioning. Stryker launched the Trident II Acetabular System in India in April 2026, combining premium implant placement with robotic-arm-assisted surgery to tap into a high-growth emerging market. These strategic initiatives highlight the emphasis on ecosystem development, regional expansion, and differentiated product offerings over basic implant demand.

Femoral Head Prostheses Industry Leaders

B. Braun Melsungen AG

Johnson & Johnson MedTech (DePuy Synthes)

Stryker Corporation

Smith & Nephew plc

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Stryker launched the Trident II Acetabular System in India to address growing hip replacement demand driven by an aging population and rising osteoarthritis cases. The system featured robotic-arm-assisted placement and advanced bearing materials, aligning with Stryker's strategy to integrate premium implants with its Mako robotics in emerging markets.

- October 2025: Zimmer Biomet completed the acquisition of Monogram Technologies, an AI-driven orthopedic robotics company. Monogram's FDA-cleared semi-autonomous TKA system was planned for commercialization with Zimmer Biomet implants by early 2027, enhancing the company's robotics portfolio beyond the ROSA platform.

Global Femoral Head Prostheses Market Report Scope

As per the scope of the report, a femoral head prostheses is an artificial, spherical implant used to replace the natural "ball" of the hip joint. It is a critical component in partial (hemiarthroplasty) or total hip replacement surgeries, designed to articulate smoothly within the hip socket or a synthetic liner to restore movement and relieve pain.

The femoral head prostheses market is segmented by product type, material, fixation compatibility, procedure type, end-user, and geography. By product type, the market includes bipolar femoral head prostheses, unipolar/endocephalic femoral head prostheses, and modular femoral head components. By material, the market is segmented into cobalt-chromium alloy, stainless steel, ceramic, oxidized zirconium, and advanced bearing surfaces. By fixation compatibility, the market is categorized into cemented-compatible systems, cementless-compatible systems, and hybrid/convertible systems. By procedure type, the market is segmented into hemiarthroplasty for displaced femoral neck fracture, hemiarthroplasty for femoral head necrosis, total hip arthroplasty, revision hip arthroplasty, and hemi-to-total conversion. By end-user, the market is segmented into hospitals, ambulatory surgical centers, and specialty orthopedic centers. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Bipolar Femoral Head Prostheses |

| Unipolar / Endocephalic Femoral Head Prostheses |

| Modular Femoral Head Components |

| Cobalt-Chromium Alloy |

| Stainless Steel |

| Ceramic |

| Oxidized Zirconium and Advanced Bearing Surfaces |

| Cemented-Compatible Systems |

| Cementless-Compatible Systems |

| Hybrid / Convertible Systems |

| Hemiarthroplasty for Displaced Femoral Neck Fracture |

| Hemiarthroplasty for Femoral Head Necrosis |

| Total Hip Arthroplasty |

| Revision Hip Arthroplasty and Hemi-to-Total Conversion |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopedic Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Bipolar Femoral Head Prostheses | |

| Unipolar / Endocephalic Femoral Head Prostheses | ||

| Modular Femoral Head Components | ||

| By Material | Cobalt-Chromium Alloy | |

| Stainless Steel | ||

| Ceramic | ||

| Oxidized Zirconium and Advanced Bearing Surfaces | ||

| By Fixation Compatibility | Cemented-Compatible Systems | |

| Cementless-Compatible Systems | ||

| Hybrid / Convertible Systems | ||

| By Procedure Type | Hemiarthroplasty for Displaced Femoral Neck Fracture | |

| Hemiarthroplasty for Femoral Head Necrosis | ||

| Total Hip Arthroplasty | ||

| Revision Hip Arthroplasty and Hemi-to-Total Conversion | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopedic Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the femoral head prostheses market by 2031?

The femoral head prostheses market is projected to reach USD 1.89 billion by 2031 from USD 1.80 billion in 2026, at a CAGR of 5.03% over 2026-2031.

Why do bipolar femoral head prostheses still lead demand?

Bipolar products held 62.10% of 2025 revenue because they fit displaced femoral neck fracture care well, especially in elderly patients who benefit from shorter surgery and lower acetabular wear.

Which material category is growing fastest through 2031?

Ceramic is the fastest-growing material segment, with a projected 7.20% CAGR through 2031, supported by the shift toward lower wear and stronger long-term performance in younger or more active patients.

Why do cemented systems remain the largest fixation category?

Cemented-compatible systems held 57.60% of 2025 revenue because they provide reliable fixation in osteoporotic bone and support earlier weight-bearing in elderly fracture patients.

Which region leads revenue and which region grows fastest?

North America led with 41.95% of 2025 revenue, while Asia-Pacific is expected to record the fastest growth at 8.30% CAGR through 2031.

How are outpatient settings changing product strategy?

Ambulatory surgical centers are projected to grow at 7.50% CAGR through 2031, pushing suppliers to prioritize compact trays, efficient instrumentation, and components suited to minimally invasive workflows.

Page last updated on: