Limb Prosthetics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

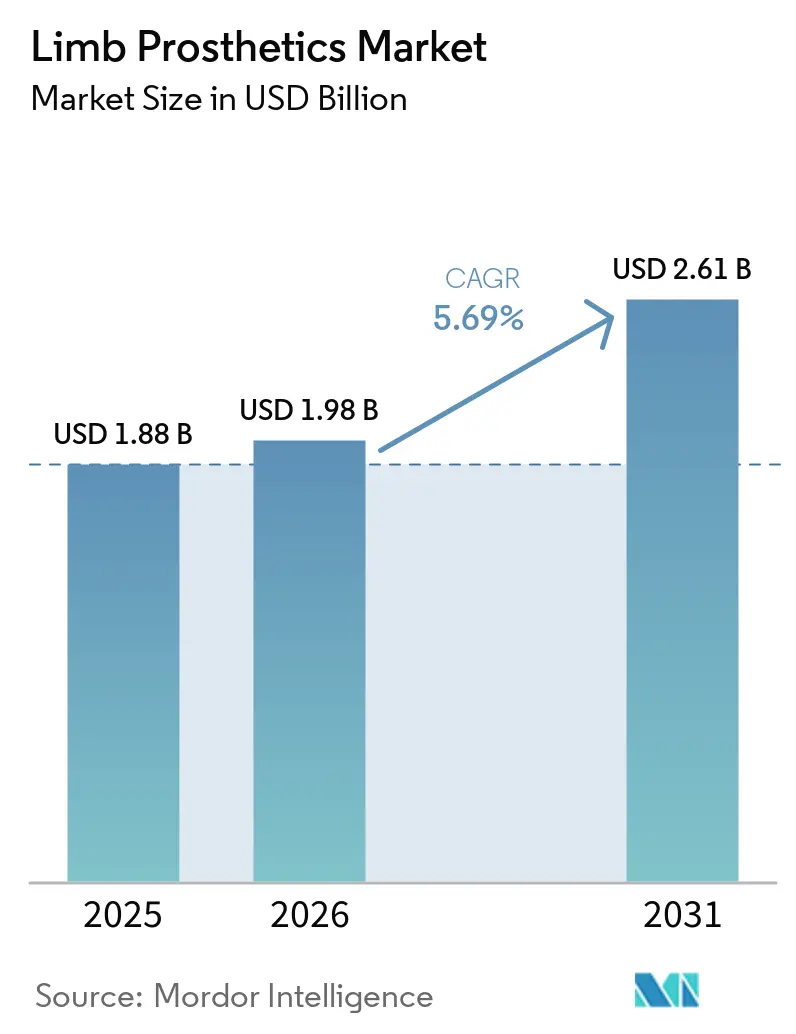

| Market Size (2026) | USD 1.98 Billion |

| Market Size (2031) | USD 2.61 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Limb Prosthetics Market Analysis by Mordor Intelligence

The Limb Prosthetics Market size is expected to increase from USD 1.88 billion in 2025 to USD 1.98 billion in 2026 and reach USD 2.61 billion by 2031, growing at a CAGR of 5.69% over 2026-2031.

Demand continues to widen because the addressable patient pool is increasing across both traumatic limb loss and chronic disease related amputations, with 2.309 million Americans living with limb loss in a 2025 study and a much larger global burden of traumatic amputation already in place. The growth path for the limb prosthetics market is also supported by the steady rise in diabetes linked lower extremity amputations, which adds recurring need for replacement devices, sockets, liners, and follow-up care over time. Near-term expansion is being shaped by broader reimbursement access, stronger veteran care pathways, and wider acceptance of advanced device categories such as microprocessor knees and digitally fabricated components. Innovation is moving from isolated premium devices toward more scalable customization, with 3D design, better fit management, and modular architectures creating openings for both large manufacturers and specialist developers. Competition remains strongest at the premium end of the limb prosthetics market, but growth opportunities are widening in outpatient care models, cost-sensitive product tiers, and regions where reimbursement is still catching up with clinical need.

Key Report Takeaways

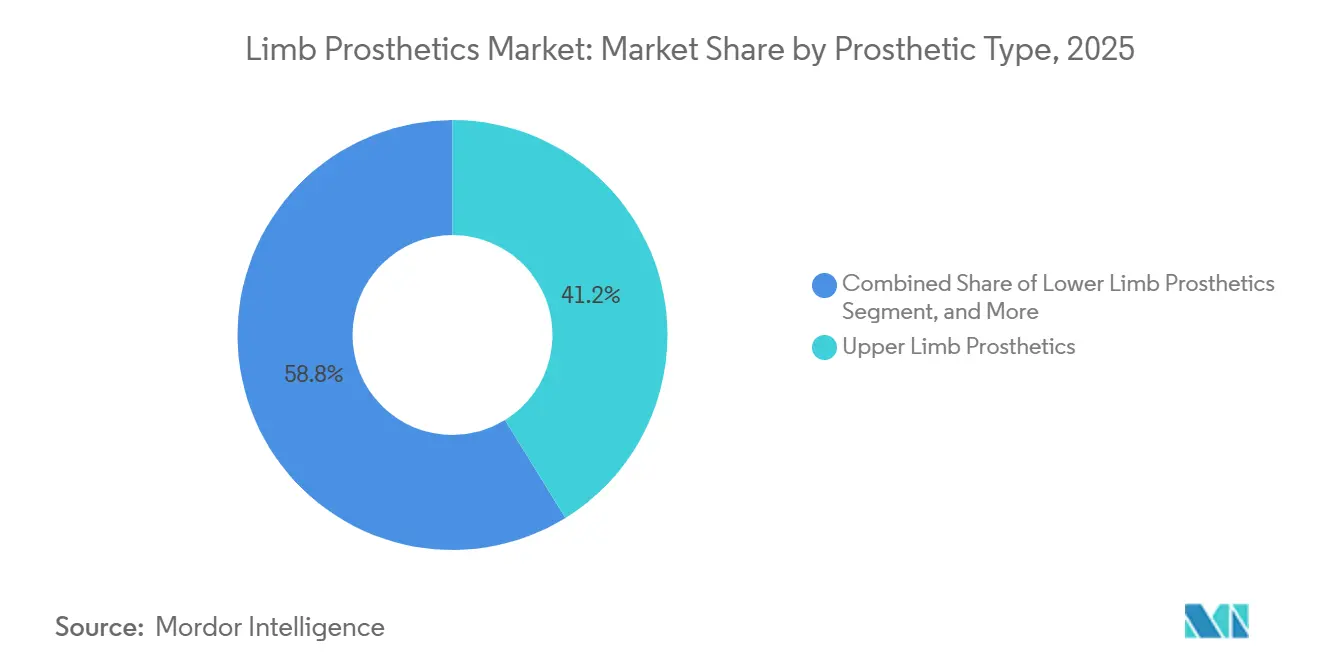

- By prosthetic type, upper limb prosthetics held 41.21% of the limb prosthetics market share in 2025, while lower limb prosthetics are projected to grow at a 7.14% CAGR through 2031.

- By material, CFRPs accounted for 37.83% share of the limb prosthetics market size in 2025, while titanium alloys are projected to expand at a 6.32% CAGR through 2031.

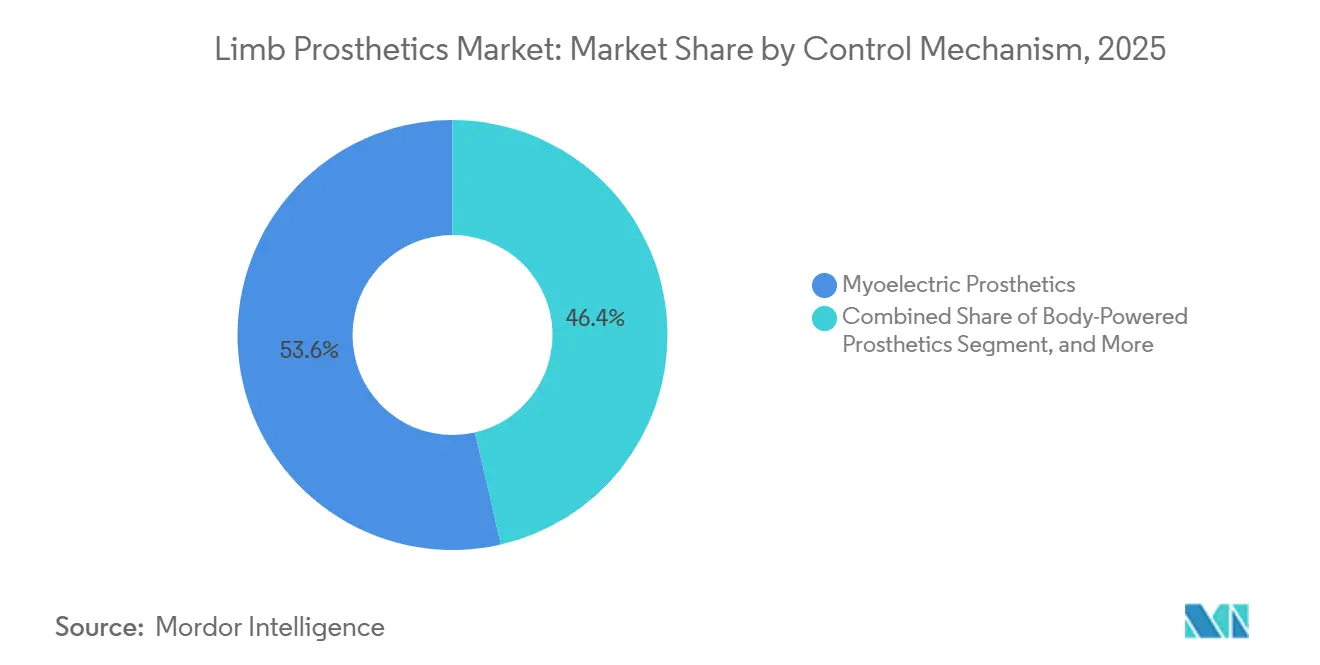

- By control mechanism, myoelectric prosthetics led with 53.64% share in 2025, while body-powered prosthetics are forecast to advance at a 7.68% CAGR through 2031.

- By component, sockets held 29.23% share of the limb prosthetics market size in 2025, while appendages are expected to record the highest CAGR at 6.03% through 2031.

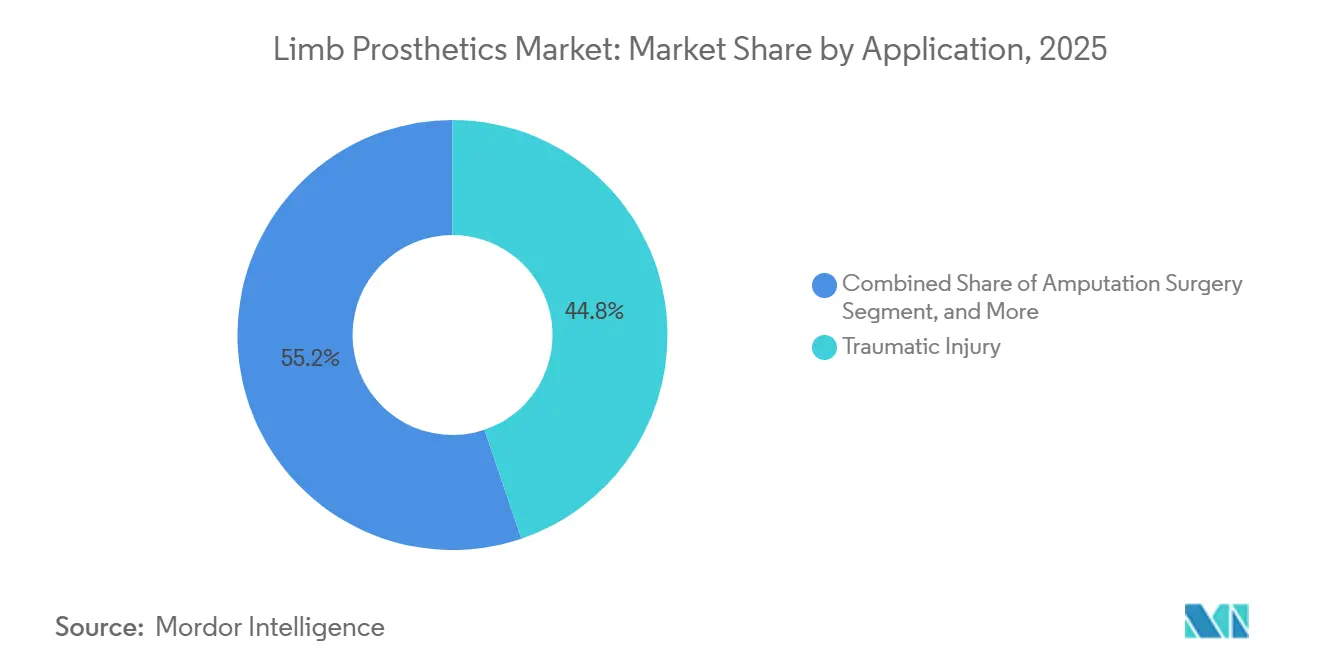

- By application, traumatic injury represented 44.83% share in 2025, while amputation surgery is set to grow at a 7.04% CAGR through 2031.

- By end user, hospitals accounted for 38.18% share in 2025, while prosthetics clinics are projected to expand at a 6.87% CAGR through 2031.

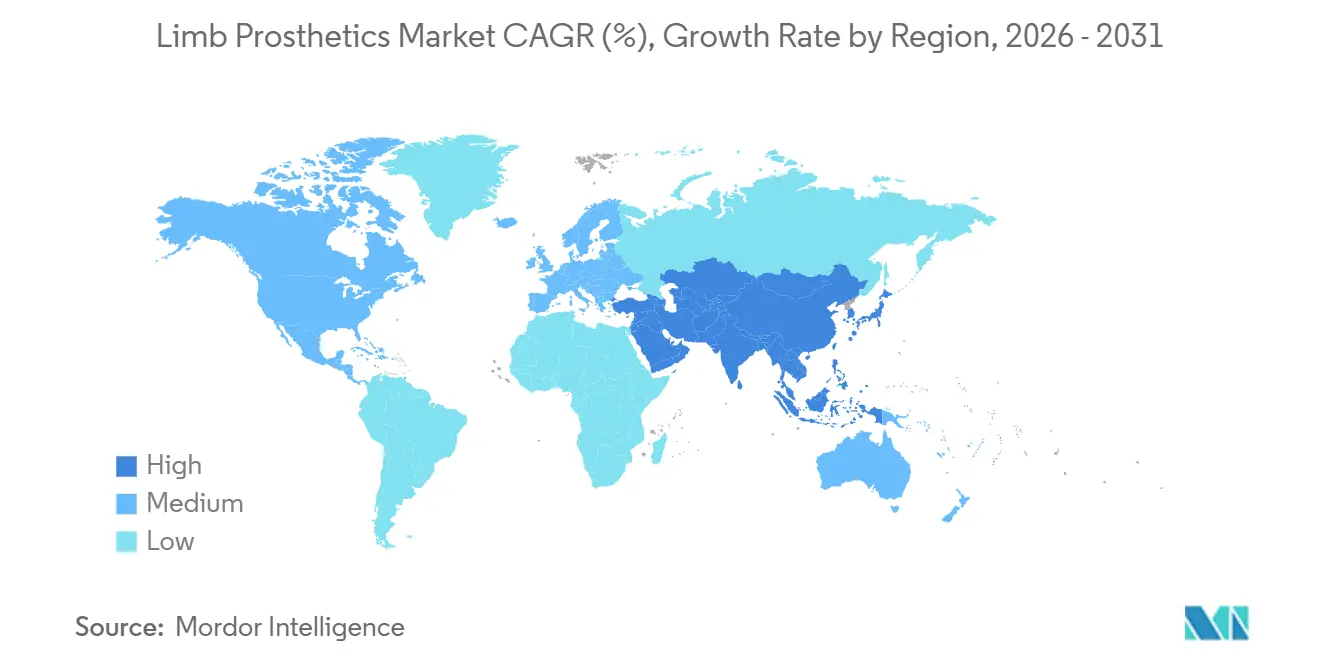

- By geography, North America held 42.23% of the limb prosthetics market share in 2025, while Asia-Pacific is projected to grow at a 7.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Limb Prosthetics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Traumatic and Disease-Linked Amputations | +1.5% | Global, with concentrated impact in South Asia, Sub-Saharan Africa, and Southern United States | Long term (≥ 4 years) |

| Advancing Microprocessor, Myoelectric, and Bionic Control Systems | +1.8% | North America and Western Europe as adoption leaders, APAC as a fast-following adopter | Medium term (2-4 years) |

| Greater Access Through Reimbursement, Subsidy, and Veteran Support Programs | +1.2% | North America, Western Europe, Ukraine, spill-over to GCC and South Korea | Short term (≤ 2 years) |

| 3D Scanning, Additive Manufacturing, and Rapid Customization at Scale | +1.0% | Global, early leadership in North America, UK, Germany, Australia | Medium term (2-4 years) |

| Pediatric Replacement Cycles and Growth Accommodating Device Demand | +0.6% | APAC core, including India and China, North America, Western Europe | Long term (≥ 4 years) |

| Expansion of Remote Fitting, Tele-Rehabilitation, and Connected Follow-Up Care | +0.5% | North America, Northern Europe, early gains in Australia and South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Traumatic and Disease-Linked Amputations

The limb prosthetics market continues to rest on a widening demand base created by trauma, vascular disease, and diabetes related limb loss. A 2025 study using National Inpatient Sample data estimated that 2.309 million Americans were living with limb loss, and it projected that this number will double by 2050 and rise by 145% by 2060. The global burden is already much larger, with 445.2 million people living with traumatic amputation in 2021 and 5.9 million years lived with disability linked to that condition. Hospital evidence in Illinois also showed a 65% rise in leg and foot amputations between 2016 and 2023, which reflects the same pressure from diabetes and peripheral artery disease seen more broadly.[1]Northwestern Medicine, “Leg and Foot Amputations Increased 65% in Illinois Hospitals Between 2016-2023,” Northwestern Now, news.northwestern.edu Diabetes related lower extremity amputations add a recurring replacement cycle to the limb prosthetics market because 1.5 million such amputations occur each year worldwide, and diabetes accounts for 50% to 70% of them.

Advancing Microprocessor, Myoelectric, and Bionic Control Systems

The limb prosthetics market is moving toward devices that improve control, stability, and functional range rather than only replacing lost anatomy. A 2026 study validated bone-anchored, neurally controlled knee prosthesis performance through intramuscular electrodes and agonist-antagonist myoneural interface surgery, which shows that neural control is moving beyond laboratory promise.[2]Rickard Brånemark et al., “Design and Evaluation of a Bone-Anchored, Neurally-Controlled Knee Prosthesis,” Journal of NeuroEngineering and Rehabilitation, link.springer.com That progress matters because it raises the performance ceiling for premium devices and supports the long-term case for broader clinical use. Ottobock also showed commercial traction in this part of the limb prosthetics market, with 2025 growth supported by microprocessor knee launches and stronger adoption in the Americas and EMEA. Coverage expansion is beginning to support demand more directly, as HCSC started covering K2 microprocessor knees across 5 U.S. states from January 1, 2026. This combination of technical validation and payer acceptance should keep advanced systems at the center of product differentiation in the limb prosthetics market.

Greater Access Through Reimbursement, Subsidy, and Veteran Support Programs

Reimbursement remains one of the clearest near-term growth levers in the limb prosthetics market because access often changes faster than underlying disease patterns. The U.S. Department of Veterans Affairs continues to provide comprehensive prosthetic care through its Amputation System of Care, which keeps eligible veterans from facing most out-of-pocket device costs.[3]U.S. Department of Veterans Affairs, “Tennessee VA Revolutionizing How Veterans with Limb Loss Receive Care,” VA News, news.va.gov The same system is also improving care delivery efficiency, since the Mobile Prosthetic and Orthotic Care program saves the VA USD 86,000 per clinician annually compared with community providers. Private payer decisions are also expanding the addressable pool, with HCSC now covering K2 microprocessor knees in Texas, Illinois, Montana, Oklahoma, and New Mexico. As reimbursement improves, manufacturers gain more confidence to fund premium research, and clinics gain more reason to expand fitting capacity for advanced prosthetic categories across the limb prosthetics market.

3D Scanning, Additive Manufacturing, and Rapid Customization at Scale

Digital production methods are shortening the path from clinical assessment to final fit across the limb prosthetics market. A 2025 review found that 3D-printed lower limb prostheses consistently improved gait biomechanics, patient satisfaction, and usability, although workflow refinement and material durability still need work.[4]Journal of Functional Biomaterials, “The Current State of 3D-Printed Prostheses Clinical Outcomes,” MDPI, mdpi.com Ottobock's iconiq liner launch in 2026 showed that additive manufacturing is moving into scaled commercial use, with variable thickness profiles designed to improve compression and address fit problems that affect nearly 68% of lower limb prosthesis users. Open Bionics adds another proof point because its FDA-cleared 3D-printed Hero FLEX arm is now available through more than 800 clinical locations across multiple countries. As these tools become part of routine practice, the limb prosthetics market should see faster customization cycles, lower iteration burden, and broader product reach without giving up functional performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Cost for Advanced Prosthetics and Consumables | -0.9% | Global, most acute in South Asia, Sub-Saharan Africa, Latin America, and rural North America | Long term (≥ 4 years) |

| Fit Failure, Socket Intolerance, and Revision Complexity | -0.6% | Global, concentrated in markets with limited certified prosthetist access for follow-up care | Medium term (2-4 years) |

| Limited Access to Certified Prosthetists in Secondary and Tertiary Cities | -0.5% | APAC, MEA, South America, and rural North America | Long term (≥ 4 years) |

| Weak Supply Chain Depth for Precision Components and Advanced Materials | -0.4% | Global, concentrated in titanium alloy machining, carbon fiber prepregs, and electronic components | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost for Advanced Prosthetics and Consumables

Affordability remains a major brake on the limb prosthetics market, especially when advanced devices are only partly covered or not covered at all. The access gap is also uneven, since U.S. public health data links higher amputation risk and poorer access conditions to low socioeconomic neighborhoods and to Black adults with diabetes. Even where primary devices are reimbursed, recurring consumables such as liners and replacement sockets still create repeated spending pressure for users. That cost burden matters because premium myoelectric, bionic, and microprocessor devices are not one-time purchases, and long-term upkeep can steer patients toward simpler alternatives. As a result, the limb prosthetics market often splits between well-insured premium users and cost-sensitive users who prioritize durability, repairability, and lower total ownership cost.

Fit Failure, Socket Intolerance, and Revision Complexity

Fit failure continues to limit device satisfaction and effective daily use in the limb prosthetics market, even when the underlying prosthetic technology is advanced. Ottobock reported that nearly 68% of lower limb prosthesis users experience problems related to their devices, with socket and liner fit issues among the leading causes. The clinical review literature also shows that digital manufacturing is improving outcomes, but it still requires better workflow precision and stronger material consistency before fit problems fall sharply across routine care. Revision work remains time-intensive for clinics because socket fabrication, residual limb changes, and repeated adjustments are difficult to standardize fully. These constraints weigh most heavily on limb prosthetics market users who do not have reliable access to certified follow-up care and who are least able to manage repeated visits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Prosthetic Type: Upper Limb Segment Anchors Premium Device Economics

Upper limb prosthetics held 41.21% share in 2025, and that leadership reflected the higher average selling prices associated with dexterity-focused systems. In the limb prosthetics market, upper limb devices often carry more premium pricing because they must replicate fine motor movement, grip variation, and cosmetic expectations in a more demanding way than many lower limb systems. This makes the category an important revenue anchor even when the clinical population is smaller than that of lower extremity users. Product development activity also remains intense in this segment, with manufacturers competing on multi-grasp control, modular wrists, lighter structures, and more natural user interaction. Open Bionics strengthened that direction in 2026 when it expanded Hero FLEX to above-elbow amputees and continued distribution through more than 800 clinical locations across the United States, the United Kingdom, Europe, Australia, and New Zealand.

Lower limb prosthetics are still expected to record the fastest growth, with the limb prosthetics market size for this subtype projected to rise at a 7.14% CAGR through 2031. That growth reflects the much larger base of lower extremity limb loss, with prior epidemiology showing that 91% of U.S. limb loss cases involve the lower extremity. Diabetes also reinforces this outlook because lower extremity amputations remain heavily tied to chronic disease progression and vascular complications. Other prosthetic types, including partial foot, partial hand, and transmetatarsal devices, remain smaller but clinically meaningful categories in the limb prosthetics industry because partial amputation care is common in diabetic foot management and requires different fitting economics. Growth in lower limb systems also supports adjacent revenue from sockets, liners, pylons, and follow-up replacements across the broader limb prosthetics market.

By Material: Titanium Alloys and Composites Compete on a New Dimension

Carbon fiber reinforced polymers held 37.83% share in 2025, which kept composites at the center of structural performance across the limb prosthetics market. Carbon composites remain deeply embedded in prosthetic feet and pylons because weight reduction and energy return are central to user comfort and functional efficiency. A 2026 study on running prosthetic feet showed that honeycomb sandwich carbon composite designs delivered a 57.4% increase in energy storage capacity versus solid reference designs while maintaining a 1.95 safety factor. That result suggests there is still room for meaningful performance gains within established composite material systems. It also helps explain why CFRPs remain critical to premium lower limb products in the limb prosthetics market.

Titanium alloys are projected to expand at a 6.32% CAGR through 2031, making them the fastest-growing material group in the limb prosthetics market. Their appeal is tied to strength-to-weight performance, corrosion resistance, and biocompatibility, all of which matter more as devices move toward long-wear, higher-load, and osseointegration-compatible designs. The same trend is supported by growing interest in bone-anchored prosthetic approaches, where interface stability becomes central to the device architecture. Polyethylene and silicone still hold important niches, with polyethylene used in cost-sensitive liners and soft socket applications, and silicone favored where skin compliance and individualized fit matter more. Material competition in the limb prosthetics industry is therefore shifting from simple cost comparison toward a broader mix of weight, durability, clinical comfort, and digital fabrication compatibility.

By Control Mechanism: Myoelectric Consolidation Meets Emerging Neural Interface Competition

Myoelectric prosthetics accounted for 53.64% share in 2025, which confirmed their position as the leading control mechanism in the limb prosthetics market. That dominance reflects years of clinical acceptance in high-income markets where powered upper limb devices and advanced control systems are more likely to be funded. Myoelectric systems also benefit from a strong installed base, more established clinician familiarity, and a clearer path into premium pricing bands. In practice, they remain the default option when users need a higher functional range without moving into experimental neural interface platforms. This keeps myoelectric products central to premium competition in the limb prosthetics market, even as their performance ceiling becomes more visible.

Body-powered prosthetics are projected to record the fastest growth at a 7.68% CAGR through 2031, which shows that simpler systems still have strong commercial relevance. Their growth is tied to durability, repair simplicity, and easier maintenance in cost-sensitive settings, conflict-affected regions, and pediatric use cases where resilience often matters more than electronics. Cable-powered systems remain present in sports and occupational use because some users still value direct mechanical feedback and lower service complexity. At the same time, neural interface approaches are beginning to shape future competition, with 2026 research demonstrating continuous neural control over a powered knee prosthesis through a bone-anchored and surgically integrated platform. The result is a limb prosthetics market where myoelectric devices still lead, but the long-term innovation frontier is already moving toward deeper human-device integration.

By Component: Appendage Innovation Concentrates Value Upstream

Sockets held 29.23% share in 2025, which made them the largest component group in the limb prosthetics market by value contribution. This position comes from the fact that the socket is the main interface between the user and the device, and it also requires repeated adjustment and replacement over time. Frequent replacement cycles give socket systems a recurring revenue profile that is structurally larger than many other single components. The commercial importance of the category is reinforced by the high rate of fit complications in lower limb users, which keeps redesign and liner replacement activity elevated.

Appendages are expected to grow the fastest, with the limb prosthetics market size for this component group advancing at a 6.03% CAGR through 2031. That reflects premium pricing in prosthetic hands, energy return feet, and ankle units that deliver visible functional differentiation and command higher unit economics. Joints remain among the most technically complex components because microprocessor knees and other powered articulations combine software, sensors, and mechanical engineering in a high-value package. Connecting modules serve a more standardized role, but they remain essential to modular product architecture and high-volume assembly. A 2026 computational study also pointed to future changes in socket production by showing that lattice-integrated transfemoral sockets can improve structural efficiency and patient-specific load distribution through additive manufacturing. Taken together, these patterns show a limb prosthetics market where value is spread between recurring interface components and premium appendages that capture innovation-led pricing.

By Application: Chronic Disease Burden Anchors Core Demand

Traumatic injury represented 44.83% share in 2025, which kept it as the largest application group in the limb prosthetics market. This reflects the large installed base created by road accidents, industrial injury, military exposure, and long-term post-trauma rehabilitation needs. The category is no longer only about acute recovery, because many users require multiple upgrades, replacements, and component changes over several years. That long replacement arc supports recurring sales and long clinical relationships for manufacturers and service providers. It also helps stabilize the limb prosthetics market when short-term procedure volumes vary across healthcare systems.

Amputation surgery is projected to grow at a 7.04% CAGR through 2031, making it the fastest-growing application in the limb prosthetics market. The main reason is the persistent rise in diabetes related lower extremity amputations, with 1.5 million lower extremity amputations performed each year worldwide, and diabetes accounting for 50% to 70% of them. Congenital limb deformity remains a smaller segment by volume, but it has high strategic importance because pediatric users require repeated replacement and upsizing through growth stages. Open Bionics has already shown how modular and adaptable systems can help extend reach in these user groups through a wide clinical distribution model. This gives the limb prosthetics market a balanced application mix of large trauma driven demand, rising chronic disease demand, and smaller but high lifetime value pediatric cohorts.

By End User: Specialty Clinics Emerge as the Growth Channel

Hospitals held 38.18% share in 2025, which kept them as the largest end-user setting in the limb prosthetics market. Their position reflects the central role of hospitals in post-amputation recovery, early rehabilitation planning, and initial fitting pathways that remain tied to surgical care. In many health systems, hospital-linked rehabilitation teams still control the first step in device selection and referral. This gives hospitals continuing influence over premium device adoption, clinical protocol standardization, and the timing of first fittings. It also explains why hospital relationships remain commercially important throughout the limb prosthetics market, even as care shifts outward.

Prosthetics clinics are projected to grow at a 6.87% CAGR through 2031, making them the fastest-growing end-user channel in the limb prosthetics market. Dedicated clinics benefit from more focused fitting workflows, digital scanning capability, and recurring follow-up visits that are harder to manage efficiently in inpatient settings. The VA's Mobile Prosthetic and Orthotic Care model provides a useful example of this efficiency shift because it saves USD 86,000 per clinician annually compared with community providers while extending access to rural users. Rehabilitation centers still matter for complex powered systems that require gait training, calibration, and longer supervised adjustment periods. The resulting channel mix shows a limb prosthetics market that is gradually moving from hospital-dominated initiation toward clinic-centered maintenance and optimization.

Geography Analysis

North America held 42.23% share in 2025, which gave it the leading regional position in the limb prosthetics market. The region benefits from strong clinical infrastructure, established reimbursement pathways, and a sizeable military and veteran patient base. The VA's Amputation System of Care continues to support comprehensive access for eligible veterans and helps reduce direct patient cost exposure for prosthetic care. Private payer policy is also moving in a supportive direction, with HCSC expanding K2 microprocessor knee coverage across 5 U.S. states from January 1, 2026. Within the region, the United States anchors most of the limb prosthetics market size, while Canada and Mexico remain more selective opportunities where advanced coverage depth still trails the U.S. benchmark.

Europe remains a structurally important part of the limb prosthetics market because its public health systems support long-term prosthetic care and because aging populations continue to raise chronic disease burden. Germany, the United Kingdom, and France remain the core markets due to stronger rehabilitation networks and more established orthotics and prosthetics infrastructure. The region also has a long history of clinical standardization and engineering depth, which supports adoption of premium lower limb and upper limb systems. At the same time, reimbursement pressure and supply dependence can create uneven access conditions across countries, which limits how evenly premium devices scale. This leaves Europe as a stable but mixed landscape in the limb prosthetics market, where strong clinical demand exists alongside tighter cost control and country level variation.

Asia-Pacific is projected to record the fastest growth at a 7.74% CAGR through 2031, and it is becoming a key expansion zone for the limb prosthetics market. Rising diabetes prevalence, broader healthcare investment, and improving prosthetic service capacity are supporting this direction across China, India, South Korea, and Australia. China and India offer the largest volume opportunity, but adoption remains stronger in body-powered and modular lower limb products than in high-end myoelectric devices. Australia and other developed pockets of the region are showing stronger premium penetration, and Ottobock's APAC business also benefited from its 2025 acquisition of Northern Prosthetics in Australia.

Competitive Landscape

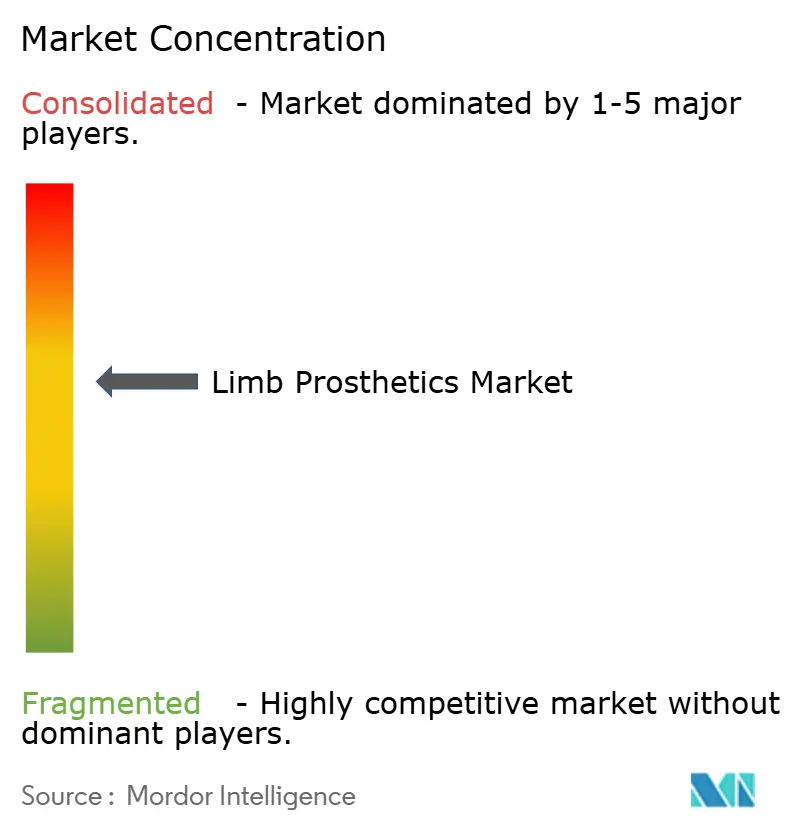

The limb prosthetics market is moderately consolidated at the premium end, where a few global medtech companies hold strong positions in myoelectric, microprocessor-controlled, and advanced bionic categories. Ottobock and Embla Medical remain the most visible large-scale players because they combine brand strength, broad portfolios, and long clinical relationships. Ottobock's 2025 core revenue reached EUR 1.6 billion (USD 1.8 billion) with 10.6% organic core growth and a 26% underlying core EBITDA margin, which points to scale advantages that smaller competitors do not easily match. The broader limb prosthetics market still remains more fragmented below this top tier, where regional providers and specialist developers compete on customization, service reach, and cost. That mix supports premium concentration without making the overall market fully consolidated.

A major competitive pattern in the limb prosthetics market is vertical integration between device manufacturing and patient care delivery. Companies that control both product supply and fitting networks are better positioned to hold referrals, manage follow-up, and capture recurring revenue from liners, sockets, and maintenance. Ottobock's 2025 performance in the Americas, where organic growth reached 14%, reflected the benefit of strong product launches and improving reimbursement support in high-value categories. The launch of the iconiq 3D-printed silicone liner in 2026 also showed how leading players are moving beyond flagship knees and feet into digitally manufactured consumables that strengthen ecosystem control. This keeps competitive pressure focused not only on breakthrough devices, but also on fit quality, service retention, and product family depth across the limb prosthetics market.

Specialist challengers are still shaping important pockets of the limb prosthetics market. Open Bionics has shown that a 3D-printed myoelectric arm can achieve regulatory approval and broad clinical distribution without requiring the same scale of legacy infrastructure as the largest incumbents. Embla Medical also broadened its strategic scope through the Fior & Gentz acquisition, which expanded its position into adjacent lower limb neuro orthotics and reinforced its wider rehabilitation platform. The remaining white space is strongest in mid-market modular systems, pediatric growth-accommodating designs, and connected follow-up models where category leadership is still less defined. This leaves the limb prosthetics market open to targeted disruption, even while premium leadership remains concentrated among a small number of established brands.

Limb Prosthetics Industry Leaders

Fillauer LLC

Integrum AB

Ottobock SE & Co. KGaA

Össur hf.

WillowWood Global LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Ottobock launched iconiq, the company's first 3D-printed silicone prosthetic liner, at OTWorld in Leipzig. The product targets fit complications affecting approximately 68% of lower-limb prosthesis users and marks Ottobock's entry into digitally manufactured consumable components at industrial scale, with global rollout underway.

- March 2026: Ottobock published its 2025 annual report, confirming full-year core revenue growth of 10.6% with underlying core EBITDA margin reaching 26.0%, supported by microprocessor knee adoption in the Americas and new product momentum in EMEA.

- February 2026: Ottobock's HCSC insurance coverage expansion for K2-level microprocessor knees took effect across Blue Cross Blue Shield plans in Texas, Illinois, Montana, Oklahoma, and New Mexico, significantly expanding the addressable patient pool for MPK devices in line with Medicare's revised Local Coverage Determination.

Global Limb Prosthetics Market Report Scope

Limb prosthetics are custom-fitted artificial devices used to replace missing upper or lower extremities (such as arms or legs). They restore mobility, functional independence, and natural appearance for individuals who have experienced amputations due to trauma, diabetes, vascular diseases, or congenital conditions.

The Limb Prosthetics Market is segmented by prosthetic type, material, control mechanism, component, application, end user, and geography. By prosthetic type, it includes Upper Limb Prosthetics, Lower Limb Prosthetics, and Other Prosthetic Types. By material, the market covers Carbon Fiber Reinforced Polymers, Titanium Alloys, Polyethylene, and Silicone. By control mechanism, prosthetics are categorized into Myoelectric Prosthetics, Body-Powered Prosthetics, and Cable-Powered Prosthetics. By component, they include Socket, Appendage, Joint, Connecting Module, and Other Prosthetic Components. By application, prosthetics are used in Amputation Surgery, Traumatic Injury, and Congenital Limb Deformity. By end user, they are adopted in Hospitals, Prosthetics Clinics, and Rehabilitation Centers.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Upper Limb Prosthetics |

| Lower Limb Prosthetics |

| Other Prosthetic Types |

| Carbon Fiber Reinforced Polymers |

| Titanium Alloys |

| Polyethylene |

| Silicone |

| Myoelectric Prosthetics |

| Body-Powered Prosthetics |

| Cable-Powered Prosthetics |

| Socket |

| Appendage |

| Joint |

| Connecting Module |

| Other Prosthetic Components |

| Amputation Surgery |

| Traumatic Injury |

| Congenital Limb Deformity |

| Hospitals |

| Prosthetics Clinics |

| Rehabilitation Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Prosthetic Type | Upper Limb Prosthetics | |

| Lower Limb Prosthetics | ||

| Other Prosthetic Types | ||

| By Material | Carbon Fiber Reinforced Polymers | |

| Titanium Alloys | ||

| Polyethylene | ||

| Silicone | ||

| By Control Mechanism | Myoelectric Prosthetics | |

| Body-Powered Prosthetics | ||

| Cable-Powered Prosthetics | ||

| By Component | Socket | |

| Appendage | ||

| Joint | ||

| Connecting Module | ||

| Other Prosthetic Components | ||

| By Application | Amputation Surgery | |

| Traumatic Injury | ||

| Congenital Limb Deformity | ||

| By End User | Hospitals | |

| Prosthetics Clinics | ||

| Rehabilitation Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the limb prosthetics space by 2031?

It is projected to reach USD 2.61 billion by 2031, rising from USD 1.98 billion in 2026 at a 5.69% CAGR over 2026-2031.

Which region leads global revenue for limb prosthetic devices?

North America led in 2025 with 42.23% share, supported by stronger reimbursement systems, veteran care programs, and advanced clinical capacity.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to post the fastest growth at a 7.74% CAGR, supported by rising diabetes prevalence and improving prosthetic care access.

Which control technology currently holds the largest share?

Myoelectric prosthetics led with 53.64% share in 2025, reflecting their long-standing position in advanced upper limb and premium device categories.

What is driving the strongest demand for lower limb systems?

Demand is being supported by the high volume of lower extremity amputations, especially those linked to diabetes, vascular disease, and long-term replacement needs.

Why are prosthetics clinics gaining importance over hospitals?

Prosthetics clinics are expected to grow at a 6.87% CAGR because they are better suited for digital scanning, fitting, adjustment, and repeat follow-up than inpatient settings.

Page last updated on: