U.S. Orthopedic Braces And Supports Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

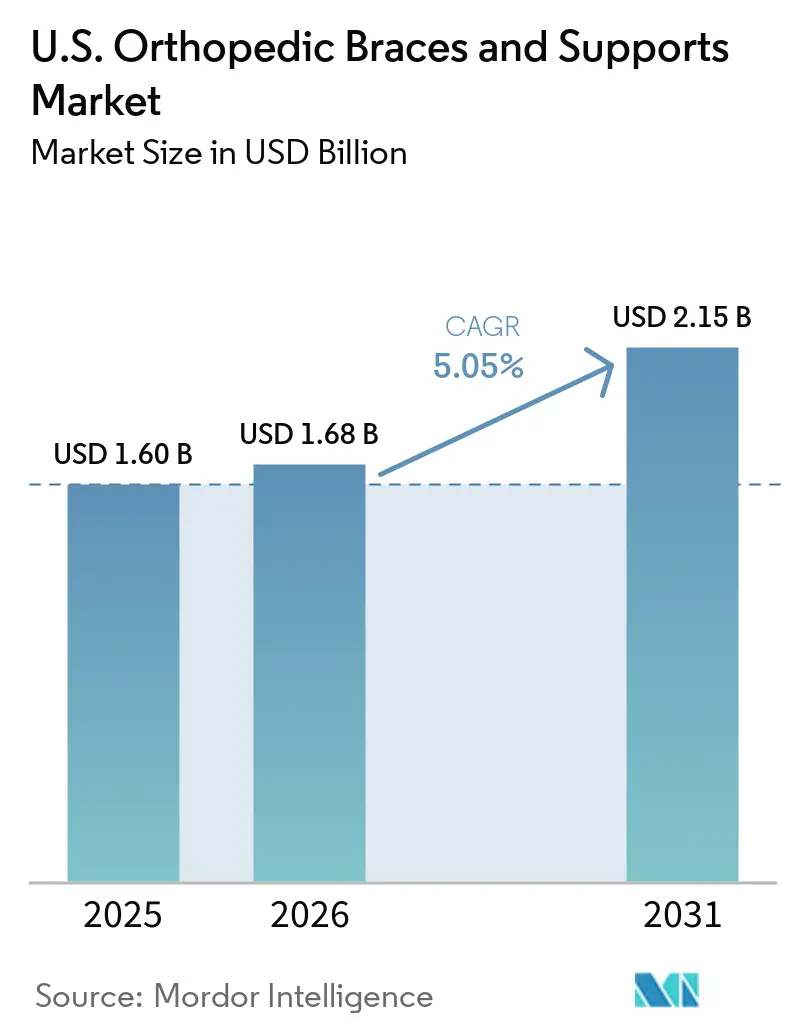

| Base Year Market Size (2025) | USD 1.60 Billion |

| Market Size (2026) | USD 1.68 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Orthopedic Braces And Supports Market Analysis by Mordor Intelligence

The U.S. Orthopedic Braces And Supports Market size is projected to expand from USD 1.60 billion in 2025 and USD 1.68 billion in 2026 to USD 2.15 billion by 2031, registering a CAGR of 5.05% between 2026 to 2031.

The growth path rests on three structural factors: a large and aging patient population with osteoarthritis, increasing musculoskeletal injuries from sports and workplaces, and the growing adoption of conservative care before surgery. In 2024, 21.3% of adults in the United States were diagnosed with arthritis, driving demand across knee, ankle, back, and upper-extremity support categories. Sports and recreational equipment injuries resulted in 4.4 million emergency department visits in 2024, a 17% increase from 2023.[1]Centers for Disease Control and Prevention, “FastStats, Arthritis,” National Center for Health Statistics, cdc.gov This rise sustained high demand for short-cycle replacement and recovery products. Ambulatory surgery centers are performing more orthopedic procedures, with same-day discharges making take-home bracing a standard recovery component.

Key Report Takeaways

- By application, ligament injury led with 39.27% share in 2025, while post-operative rehabilitation is projected to expand at a 7.53% CAGR through 2031.

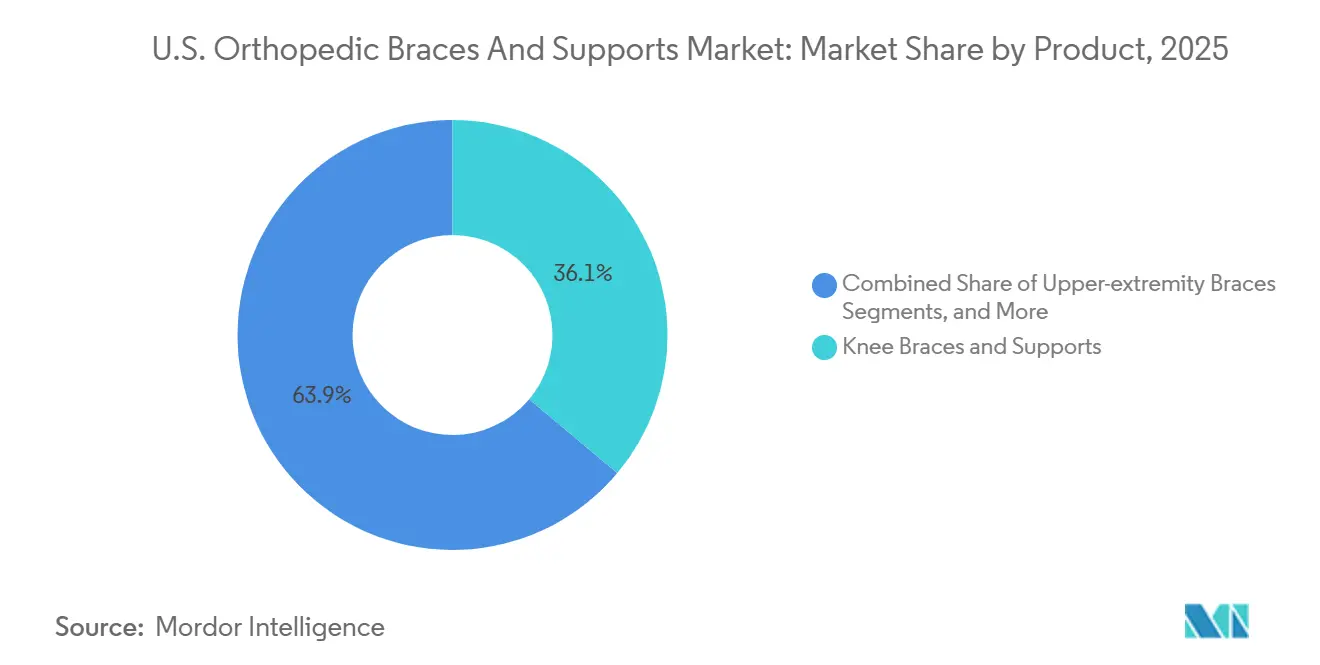

- By product, knee braces & supports accounted for 36.11% of the US orthopedic braces and supports market size in 2025, while upper-extremity braces are expected to grow at a 6.06% CAGR through 2031.

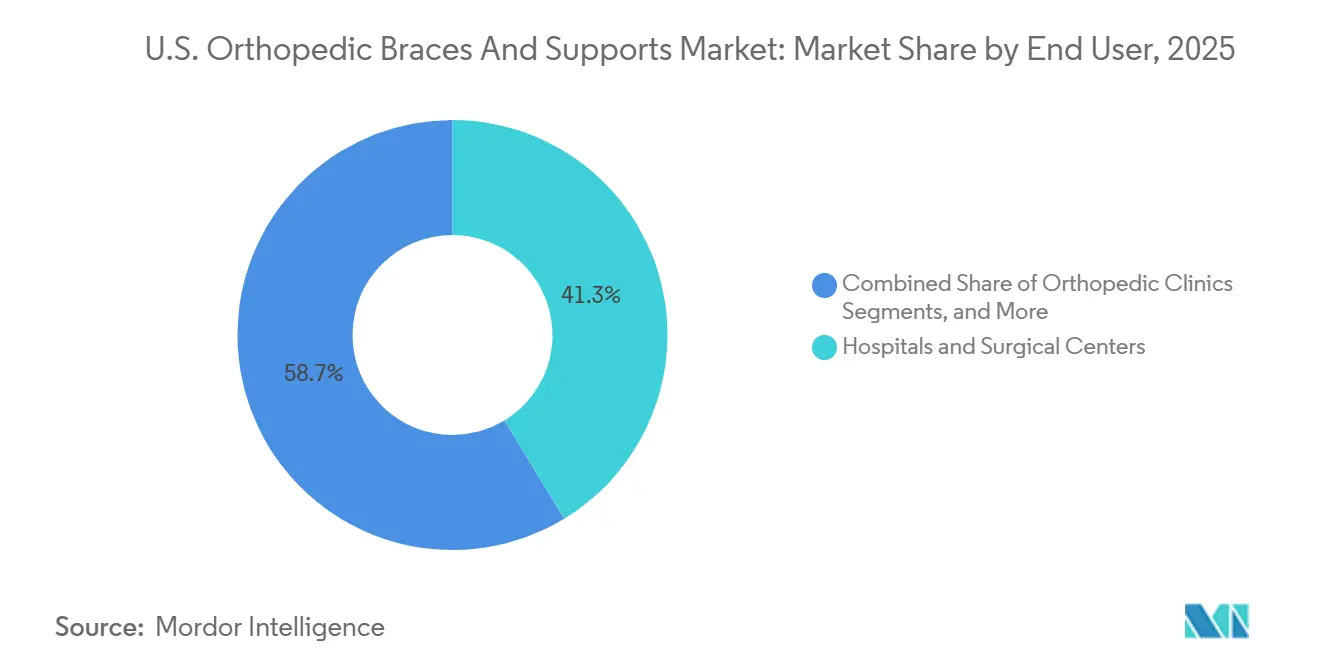

- By end user, hospitals & surgical centers held 41.32% of the US orthopedic braces and supports market share in 2025, while orthopedic clinics are expected to advance at a 5.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Orthopedic Braces And Supports Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging US population and osteoarthritis burden | +1.4% | National, with higher intensity in the Southeast and Sunbelt states | Long term (≥ 4 years) |

| High sports and musculoskeletal injury incidence | +1.0% | National, with stronger activity in the Southeast, Midwest, and West Coast | Short term (≤ 2 years) |

| Shift toward non-invasive care and post-operative rehabilitation | +0.9% | National, with stronger relevance in metropolitan areas with high ASC density | Medium term (2-4 years) |

| Product innovation in lightweight, breathable, low-profile designs | +0.6% | National | Medium term (2-4 years) |

| 2026 lower-extremity orthosis code expansion | +0.3% | National, with early gains in markets with established orthotic coding infrastructure | Short term (≤ 2 years) |

| Digital ordering, scanning, and DMEPOS workflow tools | +0.3% | National, with faster uptake in large hospital systems and orthopedic group practices | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging US Population and Osteoarthritis Burden

The United States faces a significant osteoarthritis burden among older adults, driving long-term brace usage for knee, hip, and back conditions. In 2025, osteoarthritis incidence among adults aged 55 and older was 1,973.19 per 100,000, surpassing other major markets. With 53.9% of adults aged 75 and older diagnosed with arthritis and 88% of cases in those aged 45 and above, demand for clinician-directed devices that alleviate pain and maintain mobility is rising.[2]National Safety Council, “Sports and Recreational Injuries,” Injury Facts, nsc.org As Baby Boomers age into the 75-plus bracket by 2030, the orthopedic braces and supports market will see sustained growth, particularly for unloader knee braces and hip offloading products.[3]MIAA and Datalys Center, “2024-25 High School RIO Summary Report,” High School RIO, miaa.net

High Sports and Musculoskeletal Injury Incidence

Sports participation in the United States continues to drive ligament, ankle, knee, and shoulder injuries. Emergency department visits for sports-related injuries reached 4.4 million in 2024, a 17% increase from 2023. High school programs reported 5,921 injuries during the 2024/25 academic year, with knee and ankle ligament injuries being most common. Adult recreational activities, especially among those aged 35 to 60, further contribute to demand for prescription-grade braces, ensuring steady market growth.

Shift Toward Non-Invasive Care and Post-Operative Rehabilitation

Orthopedic care in the United States is shifting toward conservative treatments, with bracing increasingly used early in care pathways. Insurers often require documented conservative treatment before approving surgeries, boosting brace adoption. Ambulatory surgery centers are driving demand for structured at-home recovery solutions due to same-day discharges. Post-operative and preventive use cases, particularly in shoulder arthroplasty, ACL reconstruction, meniscal repair, and knee replacements, are fueling demand for bracing products, supporting market growth.

2026 Lower-Extremity Orthosis Code Expansion

Reimbursement changes in 2026 enhanced the commercial viability of advanced lower-extremity orthoses. CMS introduced HCPCS code L2221 with a payment of USD 1,889.92 for microprocessor-controlled ankle-foot orthoses, providing a clear billing pathway. Additionally, CMS expanded the Required List to include 83 more HCPCS codes, increasing the need for face-to-face consultations and written orders. These changes favor larger, compliant dispensers over smaller channels, strengthening the organized dispensing segment of the market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Reimbursement gaps and patient out-of-pocket burden | -0.6% | Southeast, rural states, and Medicaid-heavy markets | Long term (≥ 4 years) |

| Commoditization pressure in soft goods and OTC channels | -0.4% | National, with stronger effect in dense retail markets | Medium term (2-4 years) |

| Tight custom-fabricated eligibility and documentation barriers | -0.3% | National, with stronger effect in non-metropolitan areas with limited O&P access | Medium term (2-4 years) |

| Non-rigid supports can fall outside medicare brace benefit category | -0.2% | National, with stronger effect in Medicare-heavy patient groups | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Gaps and Patient Out-of-Pocket Burden

Reimbursement challenges remain a significant barrier to converting clinical recommendations into product adoption. Medicare and Medicaid cover a substantial portion of patients using orthopedic braces, particularly those with osteoarthritis, chronic musculoskeletal conditions, or post-surgical recovery needs. The 2026 DMEPOS fee schedule update reflected a 2.0% increase for non-competitive-bidding orthotic items, while orthotic labor code L4205 rose by 2.7%, both trailing the rising costs faced by brace manufacturers. Co-insurance and deductibles often delay adoption for fixed-income patients, especially for premium devices like unloader knee and OA hip braces. This issue is more pronounced in dual-eligible and lower-income regions, where limited coverage and tight provider economics reduce addressable demand.

Commoditization Pressure in Soft Goods and OTC Channels

Soft braces sold through pharmacies, online platforms, and sporting goods stores continue to pressure pricing in basic support categories. These products compete with clinician-dispensed options, offering lower prices and faster availability. Branded manufacturers face challenges as most soft supports fall under FDA Class I exempt status, enabling generic competition and limiting pricing protection. This dynamic creates a divide in the United States orthopedic braces market, with premium-coded products maintaining margins while high-volume soft goods struggle to differentiate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Knee and Spine Anchor Revenue, Upper Extremity Carries the Growth Premium

Knee Braces & Supports accounted for 36.11% of the market share in 2025, making them the primary revenue driver in the United States orthopedic braces and supports market. Their broad application in osteoarthritis management, ligament injury recovery, and preventive use among active adults ensures frequent prescriptions. The segment benefits from a wide price range, from low-cost OTC sleeves to custom unloader devices exceeding USD 1,000, capturing both volume and value.

Back & Spine Braces remain a key segment due to their use in chronic lumbar pain, post-surgical stabilization, and work-related strain. Ankle & Foot Braces hold a significant position, driven by demand for sprain management and recovery from calcaneal and tibial procedures. Upper-extremity Braces are projected to grow at a 6.06% CAGR through 2031, supported by structured outpatient care for shoulder, wrist, and elbow conditions. Smith+Nephew's acquisition of Integrity Orthopaedics in January 2026 and Bauerfeind's launch of the GenuTrain P3 patella tracking brace in 2026 highlight the strategic focus on expanding product offerings.

By Application: Ligament Injury Leads Volume, Post-Operative Rehabilitation Carries the Fastest Growth

Ligament Injuries represented 39.27% of the total demand in 2025, making it the largest application segment in the United States orthopedic braces and supports market. This demand is driven by acute injuries and extended recovery cycles, particularly for ACL, MCL, and ankle ligament protocols. High school and collegiate sports continue to contribute significantly to this segment.

Post-operative Rehabilitation is forecast to grow at a 7.53% CAGR through 2031, the highest among all application segments. The growth is fueled by same-day discharges from ambulatory surgery centers, where patients require immediate bracing for recovery. Procedures like shoulder arthroplasty and total knee replacement reinforce this trend. OrthoPediatrics' launch of the TRAXIO Complete Weight System in April 2026 further expands the post-operative care landscape.

By End User: Hospital Systems Hold the Base, Orthopedic Clinics Gain Momentum

Hospitals & Surgical Centers held a 41.32% market share in 2025, maintaining their leadership in the United States orthopedic braces and supports market. Their dominance is attributed to their role in acute injury treatment, surgical recovery, and compliance with prescribing workflows. The April 2026 CMS Required List expansion further strengthened their position.

Orthopedic Clinics are expected to grow at a 5.90% CAGR through 2031, driven by the shift of routine musculoskeletal care to cost-effective outpatient settings. Clinics are enhancing integrated dispensing capabilities to streamline prescription fulfillment. Homecare Settings are expanding due to chronic osteoarthritis management and telehealth-supported prescriptions. Sports & Rehabilitation Centers, though the smallest segment, play a critical role in adopting performance-focused braces.

Geography Analysis

In the United States orthopedic braces and supports market, demand is widespread, but the Southeast experiences higher patient volumes due to elevated osteoarthritis prevalence and a dense older population. Many states in this region have older adult populations exceeding 56%, with projections reaching 60%-70%. This drives strong demand for knee, hip, and back supports among Medicare-dependent populations. However, affordability challenges for premium devices persist in lower-income and rural areas.

The Northeast and West Coast are key markets for premium orthopedic products, supported by a high density of specialists, robust commercial insurance coverage, and a significant private-pay patient base. Urban centers like Boston, New York, San Francisco, and Los Angeles lead in adopting clinician-directed protocols. The West Coast benefits from year-round outdoor activities, ensuring consistent demand for ligament and post-operative care. California stands out with its large population, growing orthopedic clinics, and expanding ambulatory surgery centers, boosting clinic-dispensed brace usage.

The Midwest and South-Central states exhibit demand driven by manual labor, worker's compensation, and repetitive strain injuries. States like Ohio, Michigan, Illinois, and Texas maintain steady use of upper-extremity and lumbar braces due to significant injury patterns in manufacturing, construction, and agriculture. Texas is notable for its large working-age population and expanding orthopedic group practices, which support clinician-directed dispensing. Rural access remains a challenge, as long travel distances to clinics hinder timely bracing prescriptions. The April 2026 documentation rules may worsen access disparities if telehealth-enabled prescribing pathways are not preserved.

Competitive Landscape

The competitive structure of the United States orthopedic braces and supports market is moderately consolidated for prescription-grade clinical products but fragmented when including OTC retail, independent DME suppliers, and O&P channels. Enovis, through DJO and DonJoy, along with Embla Medical via Össur, Ottobock, and Bauerfeind, are prominent players in clinician-directed bracing. The top 3 to 4 suppliers hold an estimated 35% to 45% combined share of clinician-directed volume, leaving room for smaller specialists and regional distributors. Portfolio breadth is critical as large suppliers aim for full anatomical coverage agreements rather than competing on single products. Account control increasingly depends on operational tools alongside brace design.

Enovis has strengthened its position by offering a comprehensive portfolio across knee, ankle, elbow, back, wrist, shoulder, and hip categories, enabling integrated selling to orthopedic practices. In January 2024, the company launched the DonJoy ROAM OA Knee Brace, targeting patients who might otherwise require custom devices, thereby expanding access in the osteoarthritis segment. Össur has focused on digital infrastructure, enhancing clinic loyalty through its EmpowerX workflow platform, which has processed nearly 4 million orders across over 4,800 billing locations, creating a competitive advantage in clinic retention.

Competition in the United States orthopedic braces and supports market is evolving through coding, specialization, and selective consolidation. The April 2026 introduction of the L2221 code clarified reimbursement for advanced ankle-foot orthoses, favoring suppliers in premium lower-extremity technology. Smith+Nephew’s January 2026 acquisition of Integrity Orthopaedics highlights the trend of orthopedic device companies moving closer to post-operative bracing due to high procedure volumes and recovery-related opportunities. Smaller companies like Becker Orthopedic, Bird & Cronin, and medi defend niche positions in custom fabrication and medical-grade support, while low-cost e-commerce brands maintain price pressure on undifferentiated soft goods.

U.S. Orthopedic Braces And Supports Industry Leaders

Breg, Inc.

Enovis Corporation

Essity Aktiebolag (publ)

Ottobock SE & Co. KGaA

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: OrthoPediatrics Corp., in partnership with Synetik Group, expanded its Specialty Bracing portfolio by introducing the TRAXIO Complete Weight System, targeting the USD 500 million U.S. pediatric orthopedic specialty bracing market.

- January 2026: Smith+Nephew acquired Integrity Orthopaedics for USD 225 million upfront, with additional performance-based payments, strengthening its position in the U.S. shoulder repair segment with the Tendon Seam rotator cuff repair system.

- January 2025: Aspen Medical Products acquired Advanced Orthopaedics, enhancing its spine-focused brace portfolio and expanding distribution across hospitals, DME, and retail channels.

- January 2025: Mueller Sports Medicine acquired the Pro Orthopedic brand, integrating its neoprene product lines and institutional relationships into its sports medicine portfolio.

U.S. Orthopedic Braces And Supports Market Report Scope

As per the scope of the report, orthopedic braces and supports are external medical devices used to stabilize, align, protect, or immobilize joints, muscles, and bones. They are non-surgical tools designed to relieve pain, prevent further injury, and aid in rehabilitation following trauma or surgery.

The U.S. orthopedic braces and supports market is segmented by product, application, end-user, and geography. By product, the market includes knee braces & supports, ankle & foot braces, back & spine braces, upper-extremity braces, hip & pelvic braces, and others. By application, the market is segmented into ligament injury, preventive care, post-operative rehabilitation, osteoarthritis, and other chronic conditions. By end-user, the market is categorized into hospitals & surgical centers, orthopedic clinics, homecare settings, and sports & rehabilitation centers. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Knee Braces & Supports |

| Ankle & Foot Braces |

| Back & Spine Braces |

| Upper-extremity Braces |

| Hip & Pelvic Braces |

| Others |

| Ligament Injury |

| Preventive Care |

| Post-operative Rehabilitation |

| Osteoarthritis |

| Other Chronic Conditions |

| Hospitals & Surgical Centers |

| Orthopedic Clinics |

| Homecare Settings |

| Sports & Rehabilitation Centers |

| By Product | Knee Braces & Supports |

| Ankle & Foot Braces | |

| Back & Spine Braces | |

| Upper-extremity Braces | |

| Hip & Pelvic Braces | |

| Others | |

| By Application | Ligament Injury |

| Preventive Care | |

| Post-operative Rehabilitation | |

| Osteoarthritis | |

| Other Chronic Conditions | |

| By End User | Hospitals & Surgical Centers |

| Orthopedic Clinics | |

| Homecare Settings | |

| Sports & Rehabilitation Centers |

Key Questions Answered in the Report

What is the current value of the US orthopedic braces and supports space in 2026

It stands at USD 1.68 billion in 2026 and is projected to reach USD 2.15 billion by 2031 at a 5.05% CAGR.

Which application area generates the highest demand in the United States

Ligament Injury led demand with a 39.27% share in 2025 because knee and ankle injuries create both acute and long-duration brace use.

Which product category is growing the fastest through 2031

Upper-extremity Braces are projected to grow at a 6.06% CAGR, supported by rising shoulder, wrist, and elbow care needs in workplace and outpatient settings.

Why are orthopedic clinics gaining importance in brace dispensing

Orthopedic Clinics are forecast to expand at a 5.90% CAGR as outpatient care shifts away from higher-cost hospital settings and more clinics add in-house DMEPOS dispensing.

What is driving stronger post-operative brace demand

Same-day discharge from ambulatory surgery centers is increasing the need for take-home braces after ACL, meniscal, shoulder, and knee procedures, which is why Post-operative Rehabilitation is set to grow at 7.53% CAGR.

Which regions show the strongest demand conditions

The Southeast has the heaviest volume tied to osteoarthritis and Medicare exposure, while the Northeast and West Coast support more premium demand because of specialist density and stronger commercial coverage.

Page last updated on: