Orthodontic Headgear Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 4.27% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Orthodontic Headgear Market Analysis by Mordor Intelligence

The Orthodontic Headgear Market size is expected to grow from USD 1.75 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 2.25 billion by 2031 at 4.27% CAGR over 2026-2031.

Growth remains steady because malocclusion continues to affect a large untreated patient base, and the World Health Organization still lists it as the third most prevalent oral health condition after dental caries and periodontal disease. A 2025 epidemiological study in children aged 10 to 12 reported Class II division 2 malocclusion in 20.8%, Class II division 1 in 15.8%, and deep bite in 22.6%, which supports sustained clinical need for orthopedic correction during growth years. The orthodontic headgear market also retains relevance in higher-severity skeletal cases because treatment plans that require vertical control still favor extraoral force mechanics over purely cosmetic alignment approaches. Competitive behavior is changing as larger dental companies link appliances to digital scanning, remote monitoring, and training ecosystems, while smaller manufacturers compete through customization, speed, and lower price points. At the same time, substitution pressure from mandibular advancement aligners in milder Class II cases and lower production costs from 3D-printed parts are shifting where value is created across the orthodontic headgear market.

Key Report Takeaways

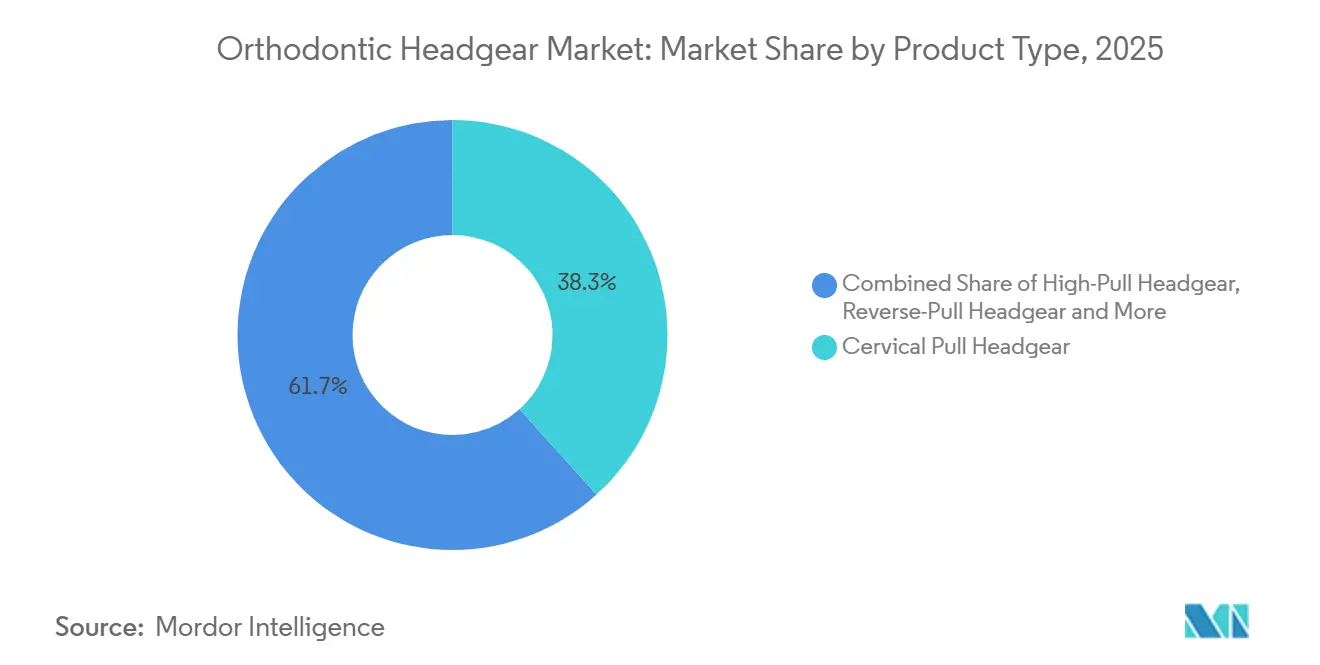

- By product type, Cervical Pull Headgear held 38.31% of the orthodontic headgear market size in 2025, while High-Pull Headgear is forecast to grow at 6.38% CAGR through 2031.

- By material type, Stainless Steel held 67.24% share in 2025, while Plastic is projected to expand at 6.52% CAGR through 2031.

- By application, Overbite Treatment accounted for 42.52% of the orthodontic headgear market size in 2025, while Malocclusion Correction is expected to advance at 5.25% CAGR through 2031.

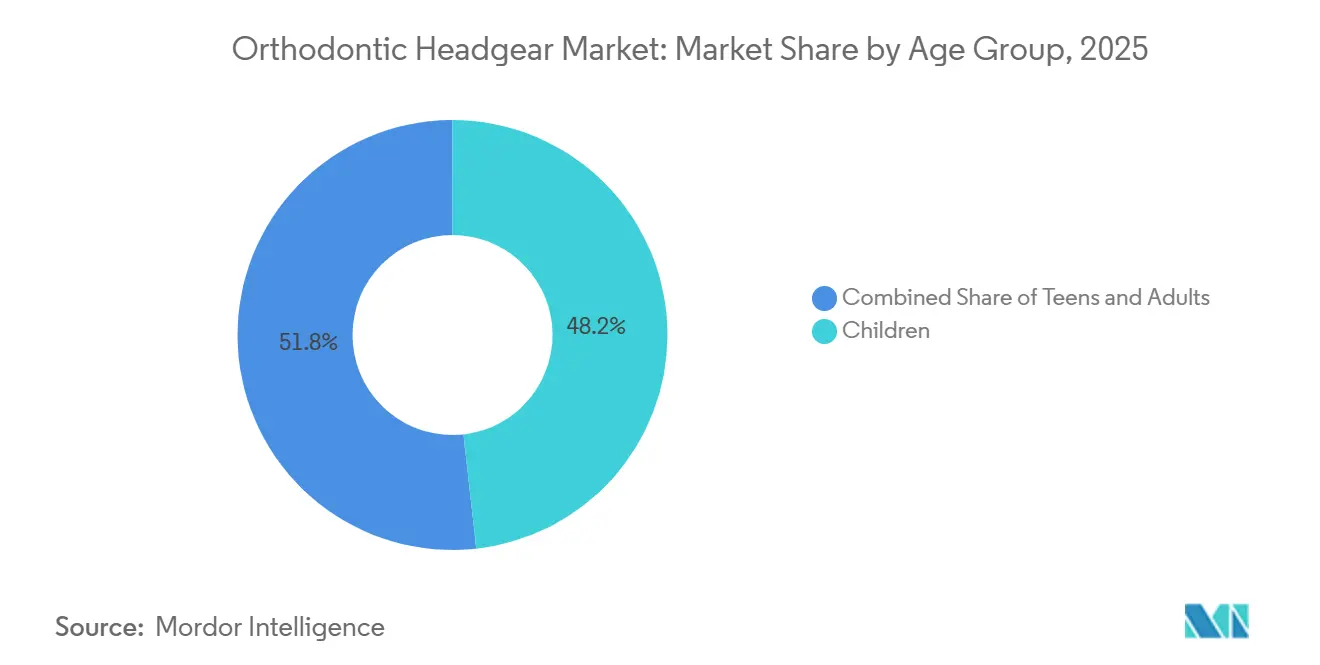

- By age group, Children aged 5 to 12 held 48.24% share in 2025, while Teens are expected to record the fastest growth at 6.52% CAGR through 2031.

- By end user, Dental Clinics held 53.56% of the orthodontic headgear market share in 2025, while Hospitals are projected to grow at 5.85% CAGR through 2031.

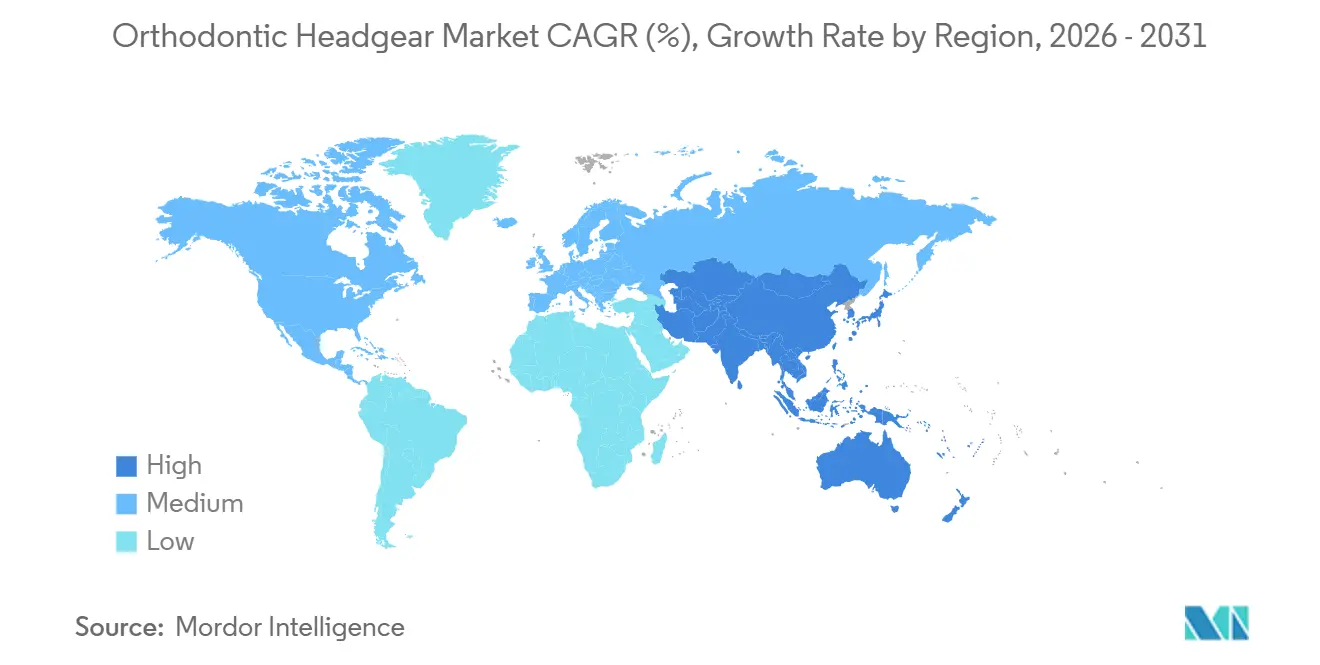

- By geography, North America held 38.22% of the orthodontic headgear market share in 2025, while Asia-Pacific is forecast to expand at 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Orthodontic Headgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Malocclusion Burden and Earlier Orthodontic Intervention | +1.2% | Global, with concentrated impact in North America, Europe, and APAC core | Medium term (2-4 years) |

| Expanding Pediatric and Adolescent Orthodontic Treatment Adoption | +0.9% | Global, early gains in US, Germany, South Korea, Australia | Medium term (2-4 years) |

| Improved Customization Through Digital Scanning and 3D Printing | +0.8% | North America and EU primary, spill-over to APAC | Short term (≤ 2 years) |

| Smart Compliance Tracking and Wear-Time Monitoring | +0.5% | North America, EU, South Korea | Short term (≤ 2 years) |

| Dental Infrastructure Expansion in Secondary Cities | +0.6% | APAC core, spill-over to MEA and South America | Long term (≥ 4 years) |

| Rising Demand for Lower-Cost Functional Alternatives to Complex Surgery | +0.4% | Global, concentrated in cost-sensitive emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Malocclusion Burden and Earlier Orthodontic Intervention

The orthodontic headgear market is supported by a treatment shift toward the mixed dentition stage, where skeletal correction still responds well to orthopedic force. Malocclusion remains a broad clinical burden, and the World Health Organization continues to rank it as the third most prevalent oral condition worldwide[1]World Health Organization, “Oral Health,” WHO Fact Sheet, who.int. The orthodontic headgear market also benefits from the continued size of the Class II treatment pool, because company data released in 2025 still described Class II cases as a large portion of global malocclusions. A 2025 schoolchild study found oral habits tied to skeletal discrepancy in 28.4% of the sample, alongside notable rates of deep bite and Class II patterns, which reinforces the value of screening early rather than waiting for later adolescence. When treatment is delayed past the main growth window, clinicians lose some orthopedic leverage, so earlier diagnosis helps maintain a stable case flow for headgear-based treatment. This keeps demand durable even as newer appliance types expand, because timing still matters as much as appliance preference in many pediatric cases.

Expanding Pediatric and Adolescent Orthodontic Treatment Adoption

The orthodontic headgear market is also gaining from broader acceptance of orthodontic treatment in children and teens, especially where parents now treat early correction as part of routine dental care. This demand signal appears durable because the need is tied to growth biology rather than short-term discretionary fashion. The largest benefit is visible in treatment settings that manage growing patients through standardized protocols, since headgear remains a practical first-line orthopedic option when cost and skeletal control both matter. The orthodontic headgear market also stands to gain as more adolescent patients enter organized clinic systems in cities beyond major urban centers, where treatment pathways are becoming more structured and more affordable. This effect is stronger in households that are willing to fund correction but remain price sensitive, because headgear often sits below premium aligner pricing while still addressing orthopedic needs. As a result, pediatric and adolescent uptake widens the patient funnel for headgear even where aligners are growing in parallel.

Improved Customization Through Digital Scanning and 3D Printing

The orthodontic headgear market is being reshaped by digital scanning and additive manufacturing, which are reducing the dependence on centralized production and long lead times. A 2025 paper described a fully functional 3D-printed J-hook headgear that used openly available STL files and standard desktop slicing software, showing that clinics and smaller manufacturers can produce usable components much faster than before[2]S. Graf et al., “Three-Dimensional Printed J-Hook Headgear: Bridging Traditional and Contemporary Orthodontic Practices,” AJO-DO Clinical Companion, sciencedirect.com. This matters because digital fabrication lets suppliers respond to patient-specific fit needs without carrying the same level of finished inventory. The orthodontic headgear market is also moving toward more digital workflow integration at the practice level, where scanners, treatment planning, and appliance output are increasingly linked in one process. That direction became clearer in May 2026 when Medit established a Global Orthodontic Business Division after acquiring Progressive Orthodontics to deepen digital orthodontic workflow adoption. Traditional suppliers will face pressure if they cannot fit into these connected workflows, because clinicians increasingly value compatibility as much as the appliance itself.

Smart Compliance Tracking and Wear-Time Monitoring

The orthodontic headgear market continues to face a basic usage problem, and that has pushed compliance tracking from a niche idea into a meaningful product differentiator. A 2024 case-control study found that patients wore headgear for a mean of 6.7 hours per day against a prescribed 13 hours, which translated into 46.15% compliance. The same study showed that simply telling patients they were being monitored did not deliver a statistically meaningful increase in wear time, so passive reminders alone appear insufficient. The orthodontic headgear market therefore has room for products that combine force sensing, temperature tracking, and digital feedback in a way that helps orthodontists intervene before treatment quality drops. Recent patent activity also points in that direction, with multi-signal monitoring concepts describing the use of temperature, capacitance, impedance, and pressure-force inputs to determine appliance wear status. As these tools become easier to use inside daily practice software, smart headgear could command a premium even in a category that otherwise faces pricing pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clear Aligner Substitution in Mild to Moderate Class II Cases | -1.5% | North America, Europe, Australia, Japan, premium markets first | Short term (≤ 2 years) |

| Wear-Time Compliance and Social Visibility Friction | -0.8% | Global, especially pronounced in adolescent-heavy markets | Medium term (2-4 years) |

| Regulatory and Biocompatibility Burden for Small Manufacturers | -0.5% | EU, North America, APAC regulatory variance | Medium term (2-4 years) |

| Limited Clinical Preference in Adult Aesthetic-Oriented Cases | -0.4% | North America, Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clear Aligner Substitution in Mild to Moderate Class II Cases

The orthodontic headgear market is under real substitution pressure in milder Class II cases, especially in premium private-pay settings where aesthetics have a strong influence on choice. The most direct example came in July 2025, when Align Technology launched an Invisalign system with mandibular advancement and solid occlusal blocks for growing Class II patients in APAC. A 2025 systematic review reported that mandibular advancement aligner systems achieved comparable correction to conventional orthopedic appliances on several treatment measures, while also showing strong patient preference. That said, the orthodontic headgear market still holds firmer ground in cases with vertical excess, mixed dentition limitations, and tighter budgets, where clear aligners do not solve every clinical or economic issue. The substitution effect is therefore uneven rather than universal, with the mild-to-moderate end most exposed first. This shifts the case mix of headgear more than it removes the category altogether.

Wear-Time Compliance and Social Visibility Friction

The orthodontic headgear market also remains constrained by a behavior issue that product design alone has not resolved. Objective monitoring showed that 85% of wear happened at night and that older children wore the appliance less than younger children, which points to self-consciousness during school and social hours as a meaningful barrier. This problem matters commercially because poor wear time extends treatment, weakens satisfaction, and can lower referral momentum for clinics that rely on predictable outcomes. The orthodontic headgear market is especially exposed in early adolescence, where orthodontic prevalence rises but social sensitivity also becomes stronger. Manufacturers have tried smaller profiles, more aesthetic parts, and softer contact materials, yet the basic visibility issue remains. The most credible response is still better data-driven oversight, but until that becomes common, compliance friction will continue to limit full category uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cervical Pull Leads, High-Pull Accelerates on Vertical Indications

Cervical Pull Headgear held 38.31% share in 2025, which kept it as the leading product type in the orthodontic headgear market. Its lead reflects a simple clinical and economic fit, because it remains the default choice for Class II molar distalization in many pediatric cases. Clinicians continue to favor it when they need a familiar appliance that is straightforward to prescribe, easy to adjust, and less expensive than more customized alternatives. That cost accessibility matters because the orthodontic headgear market still serves many families and clinics that balance treatment effectiveness with affordability. Cervical pull designs also benefit from the scale of the Class II treatment pool, which keeps baseline demand stable even when premium aligner options expand.

High-Pull Headgear is the fastest-growing product segment, with a CAGR of 6.38% over 2026 to 2031, because vertical control is becoming a more visible treatment priority in complex cases. That growth reflects its usefulness in open-bite tendencies and in patients who present with both skeletal discrepancy and vertical growth excess. Reverse-Pull Headgear, or facemask designs, remains a narrower but clinically distinct sub-segment that serves Class III correction during maxillary protraction in younger patients. The orthodontic headgear industry still depends on this type because skeletal Class III correction in growing children remains far less substitutable than mild Class II treatment. Product innovation is also entering this category through digitally fabricated J-hook concepts, which suggests that even mature product groups are moving toward hybrid digital and traditional production models.

By Material Type: Stainless Steel Entrenched, Plastic Gains on Fabrication Flexibility

Stainless Steel held 67.24% share in 2025, which made it the dominant material base across the orthodontic headgear market. Its position remains strong because high-load extraoral mechanics still require structural integrity, fatigue resistance, and stable force delivery over time. These properties are difficult to replace when appliances need to generate sustained orthopedic forces through outer bow and inner bow configurations. For that reason, metal remains central in the orthodontic headgear market even as external components evolve toward lighter designs. Stainless steel also fits established clinical workflows, which reduces the switching incentive for practices that already manage a large volume of traditional headgear cases.

Plastic is the fastest-growing material segment, with a CAGR of 6.52% through 2031, as digital fabrication makes lighter and more patient-friendly non-metal components easier to produce. Its momentum is tied to visible parts such as head caps, chin cups, and adjustment elements, where comfort and aesthetics matter more than peak load-bearing performance. Silicone, nylon, and rubber continue to play supporting roles in pads, straps, and elastic elements, especially where patient comfort influences daily wear. Over time, the orthodontic headgear market is likely to split more clearly between metal for core force delivery and polymers for fit, comfort, and customization. This shift helps smaller fabricators enter selected niches, but it also compresses price premiums in commoditized components as desktop printing becomes more accessible.

By Application: Overbite Treatment Dominates, Malocclusion Correction Expands on Case Complexity

Overbite Treatment accounted for 42.52% share in 2025, which made it the leading application across the orthodontic headgear market size. That position reflects the common incidence of deep bite and the continued need for controlled vertical expression in growing patients. A 2025 child study reported deep bite in 22.6% of the sample, which supports the sizable treatment pool tied to this indication[3]M. E. Toprak et al., “Prevalence of Orthodontic Malocclusion in Children Aged 10–12: An Epidemiological Study,” BMC Oral Health, link.springer.com. High-pull and cervical pull configurations remain especially relevant here because they combine dental correction with orthopedic control in ways that aligners do not fully replicate in severe vertical cases. As a result, overbite management gives the orthodontic headgear market a durable clinical base even while substitution grows in more cosmetic treatment paths.

Malocclusion Correction is the fastest-growing application, with a CAGR of 5.25% over 2026 to 2031, because more patients present with combined skeletal and dental issues rather than a single isolated problem. This broader category includes Class II and other skeletal management cases where headgear is used as part of a phased treatment sequence instead of a standalone appliance. Underbite Treatment and Crossbite Treatment remain more specialized, but they preserve an important share of demand because early interceptive care still values extraoral mechanics in selected younger patients. The orthodontic headgear market also benefits when practices focus on moderate-to-severe case types, since that is where appliance substitution is weakest and clinical necessity is strongest.

By Age Group: Children Hold the Base, Teens Post the Fastest Growth

Children held 48.24% share in 2025, making them the largest age group in the orthodontic headgear market. This result is consistent with the biological window in which active bone growth allows orthopedic force to influence skeletal development rather than only tooth position. Early intervention protocols continue to support treatment during mixed dentition, especially when clinicians aim to modify growth instead of waiting for later fixed-appliance correction. The orthodontic headgear market size therefore remains closely linked to pediatric case identification, referral timing, and parental willingness to treat before adolescence. Younger patients also face less social resistance than older ones, which supports better acceptance when clinicians recommend extraoral wear.

Teens are the fastest-growing age segment, with a CAGR of 6.52% through 2031, as awareness and access continue to improve. Growth in this cohort reflects expanding diagnosis and stronger parental engagement, but it also comes with a split in treatment behavior. Some teens in premium settings prefer aligners because appearance matters more in daily school life, while others remain suitable for headgear because of growth stage, severity, or budget. The orthodontic headgear market still benefits from this group when treatment needs extend beyond cosmetic alignment and when mixed dentition or skeletal correction remains part of the plan. Adults represent a smaller opportunity set because aesthetic concerns are stronger, which keeps headgear use more limited despite broader awareness of functional orthodontic care.

By End User: Dental Clinics Anchor Procurement, Hospitals Rise with Institutional Care

Dental Clinics commanded 53.56% share in 2025, which gave them the leading position in orthodontic headgear market share by end user. This outcome reflects the outpatient nature of most headgear prescribing, fitting, adjustment, and follow-up work. Independent clinics and small-group practices remain well suited to this category because they can manage frequent chair-side checks without the cost structure of a hospital setting. The orthodontic headgear market also aligns with clinic procurement because many prescriptions are still made in routine orthodontic pathways rather than in complex inpatient environments. That model is especially visible in mature regions where referral networks and private-pay treatment are already established.

Hospitals are the fastest-growing end-user segment, with a CAGR of 5.85% over 2026 to 2031, as pediatric dental and craniofacial services expand inside larger institutional settings. Growth in this channel reflects the gradual build-out of specialist care capacity rather than a shift away from clinics. Orthodontic Centers are also becoming more visible where organized dental groups want standardized treatment pathways and higher patient throughput. The orthodontic headgear market industry therefore spans both traditional clinic settings and larger institutional channels, but clinics are likely to remain the purchasing anchor because continuity of follow-up is still central to successful use.

Geography Analysis

North America held 38.22% share in 2025, which made it the largest regional base in the orthodontic headgear market size. The region benefits from a mature private-pay orthodontic structure, strong referral links between general dentists and specialists, and clinician familiarity with early orthopedic intervention. The United States remains the core demand center because extraoral mechanics are well understood in pediatric orthodontic practice and because families often enter treatment earlier than in many emerging regions. Canada and Mexico add smaller volumes, but they also widen the regional base through urban treatment demand and specialist care availability. This makes North America a stable revenue anchor for the orthodontic headgear market even as faster growth shifts elsewhere.

Asia-Pacific is projected to expand at a CAGR of 6.65% through 2031, which makes it the fastest-growing geography in the orthodontic headgear market. Growth is being led by China, India, South Korea, and Australia, though the pattern is not uniform across the region. South Korea and Australia show stronger digital maturity, while India, Southeast Asia, and inland Chinese cities depend more on clinic network expansion and better specialist reach. The region also benefits from rising middle-class spending on pediatric dental aesthetics and from broader access to orthodontic consultation outside the largest metro areas. Align Technology’s 2025 APAC launch of an Invisalign system with mandibular advancement also confirms that major companies see growing Class II treatment demand in the region, even though that product competes with headgear in part of the addressable pool.

Europe remains a mature but active region for the orthodontic headgear market, with Germany, the United Kingdom, and France continuing to set the tone for product quality and specialist practice standards. Larger, better-documented suppliers tend to be favored in this region because procurement expectations are more demanding and clinicians place greater weight on material reliability and regulatory readiness. South America and the Middle East and Africa are earlier-stage opportunity areas, where urban dental demand and expanding care infrastructure are gradually broadening the patient base for growth-oriented orthodontic treatment. This leaves the orthodontic headgear market with a balanced geographic profile, where North America provides scale, Asia-Pacific provides speed, and Europe and emerging regions provide selective replacement and expansion demand.

Competitive Landscape

The orthodontic headgear market is moderately fragmented, with global dental groups and specialist orthodontic manufacturers competing side by side. The leading multinational names include Dentsply Sirona, Ormco Corporation, and Henry Schein, while specialist suppliers such as American Orthodontics, G&H Orthodontics, Rocky Mountain Orthodontics, and Dentaurum GmbH remain important in product-specific niches. This mix keeps pricing, product breadth, and distribution relationships central to competition. The orthodontic headgear market also shows a clear split between companies that sell broad digital treatment ecosystems and companies that compete through targeted appliance expertise. As a result, differentiation is now built as much around workflow fit and service reach as around the appliance catalog itself.

A notable competitive pattern is the effort to connect orthodontic products with software and remote monitoring. In April 2025, Ormco and DentalMonitoring announced a partnership that linked Ormco cases with AI-powered remote monitoring support and a fee discount structure, which strengthened the value of ecosystem-based selling. In May 2026, Medit deepened the same digital direction by establishing a Global Orthodontic Business Division and acquiring Progressive Orthodontics to combine scanning hardware, AI-driven dental software, and practitioner education. Align Technology also sharpened competition in the growth-patient segment with its 2025 APAC launch of mandibular advancement aligners for Class II correction, which directly challenges part of the traditional headgear case base. These moves show that competition in the orthodontic headgear market is increasingly about owning the treatment workflow rather than only shipping a physical device.

White-space remains in smart-sensor-integrated headgear, because no supplier in the supplied material appears to have scaled a full commercial product that combines wear verification, force tracking, and app-based feedback in one unified assembly. That leaves room for a first mover to create a premium tier within the orthodontic headgear market, especially if it can prove better compliance and better case efficiency. At the same time, lower-cost manufacturers, including Asian suppliers, can pressure standard product categories through customization and faster fabrication in adjustable external components. The result is a competitive environment that is active and evolving, but still far from consolidated around a single dominant player.

Orthodontic Headgear Industry Leaders

Dentsply Sirona

Henry Schein, Inc.

Solventum Corporation

Ormco Corporation (Envista Holdings Corporation)

American Orthodontics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Medit Corp. established its Global Orthodontic Business Division and completed the acquisition of Progressive Orthodontics (Aliso Viejo, California). The division integrates Medit's 3D scanning hardware and AI-driven dental software platforms with a globally recognized practitioner training network, accelerating digital orthodontic workflow adoption across the Medit Orthodontic Suite and Medit Aligners product lines.

- January 2026: Smartee Denti-Technology released its 2025 annual review, reporting 100,000 GS mandibular repositioning cases, the launch of a 100,000-square-meter intelligent manufacturing campus in Shanghai, and a strategic partnership with the Straumann Group. The facility operates fully automated production lines with modular capacity and supports both internal product lines and third-party manufacturing.

Global Orthodontic Headgear Market Report Scope

As per the scope of the report, orthodontic headgear is a device used in orthodontics to help correct bite and jaw alignment issues. It consists of an external apparatus with straps and appliances that attach to braces or teeth, applying gentle pressure to guide the growth of the jaws and teeth into proper position.

The orthodontic headgear market is segmented by product type, material type, application, age group, end user, and geography. By product type, the market includes cervical pull headgear, high-pull headgear, reverse-pull headgear, and facemask headgear. By material type, it is categorized into stainless steel, plastic, rubber, silicone, and nylon. By application, the market covers malocclusion correction, overbite treatment, underbite treatment, and crossbite treatment. By age group, it is segmented into children, teens, and adults. By end user, the market includes dental clinics, hospitals, orthodontic centers, and other end users. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Cervical Pull Headgear |

| High-Pull Headgear |

| Reverse-Pull Headgear |

| Facemask Headgear |

| Stainless Steel |

| Plastic |

| Rubber |

| Silicone |

| Nylon |

| Malocclusion Correction |

| Overbite Treatment |

| Underbite Treatment |

| Crossbite Treatment |

| Children |

| Teens |

| Adults |

| Dental Clinics |

| Hospitals |

| Orthodontic Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Cervical Pull Headgear | |

| High-Pull Headgear | ||

| Reverse-Pull Headgear | ||

| Facemask Headgear | ||

| By Material Type | Stainless Steel | |

| Plastic | ||

| Rubber | ||

| Silicone | ||

| Nylon | ||

| By Application | Malocclusion Correction | |

| Overbite Treatment | ||

| Underbite Treatment | ||

| Crossbite Treatment | ||

| By Age Group | Children | |

| Teens | ||

| Adults | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Orthodontic Centers | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the outlook for orthodontic headgear through 2031?

The category is projected to rise from USD 1.82 billion in 2026 to USD 2.25 billion by 2031 at a 4.27% CAGR, supported by ongoing malocclusion treatment needs and continued use in growth-related skeletal correction.

Which product type currently leads demand?

Cervical Pull Headgear led in 2025 with a 38.31% share because it remains widely used for Class II correction and offers a lower-cost, familiar treatment option.

Why does headgear still matter when clear aligners are expanding?

Headgear remains important in moderate-to-severe skeletal cases, especially when vertical control is essential and when clinicians need orthopedic force during active growth.

Which region is growing the fastest?

Asia-Pacific is projected to post the highest regional CAGR at 6.65% through 2031, supported by rising clinic density, broader access, and higher spending on pediatric orthodontic care.

Which patient group drives the largest treatment volume?

Children aged 5 to 12 held the largest share at 48.24% in 2025 because this age window is best suited for growth modification and early interceptive treatment.

What are the main limits on wider adoption?

The biggest constraints are clear aligner substitution in milder Class II cases and weak wear-time compliance, especially among adolescents who are more sensitive to visibility in daily life.

Page last updated on: