Eyeliner Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

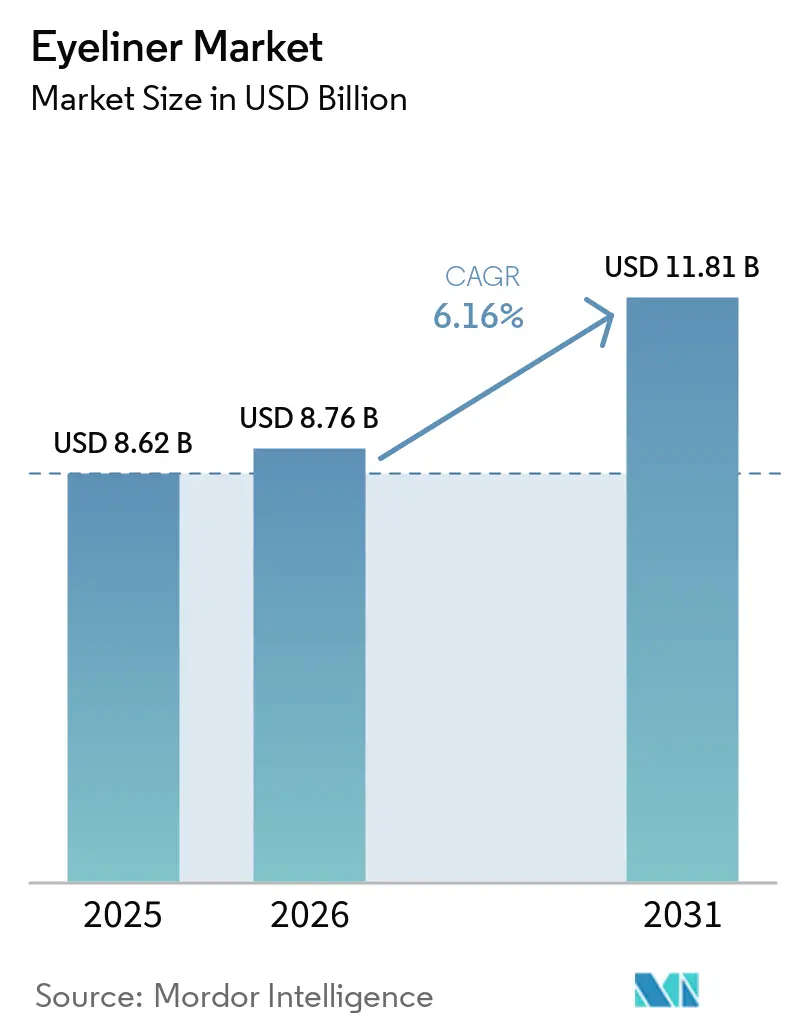

| Market Size (2026) | USD 8.76 Billion |

| Market Size (2031) | USD 11.81 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eyeliner Market Analysis by Mordor Intelligence

The eyeliner market size is expected to be USD 8.62 billion in 2025, USD 8.76 billion in 2026, and reach USD 11.81 billion by 2031, growing at a CAGR of 6.16% from 2026 to 2031. Premium-grade waterproof liquid finishes built on bio-based polyurethane and trimethylsiloxysiloxane polymers now deliver 24–48-hour wear, turning “long-wear” from a premium promise into a baseline expectation across price tiers. Asia-Pacific contributed 35.40% of 2025 revenue on the back of humid-climate demand, while the Middle East and Africa registered the fastest growth at 7.82% CAGR because of halal-certified launches and 94.3% social-media penetration that amplifies influencer discovery. Online retail is outpacing store-based channels at 8.01% CAGR as quick-commerce in India and live-streaming in China translate tutorials into same-day purchases. Counterfeits still distort price signals, but recent U.S. regulatory crackdowns and the April 2025 closure of the de minimis loophole have begun to curb gray-market inflows[1]Source: “FY 2023 Intellectual Property Rights Seizures,” U.S. Customs and Border Protection, cbp.gov .

Key Report Takeaways

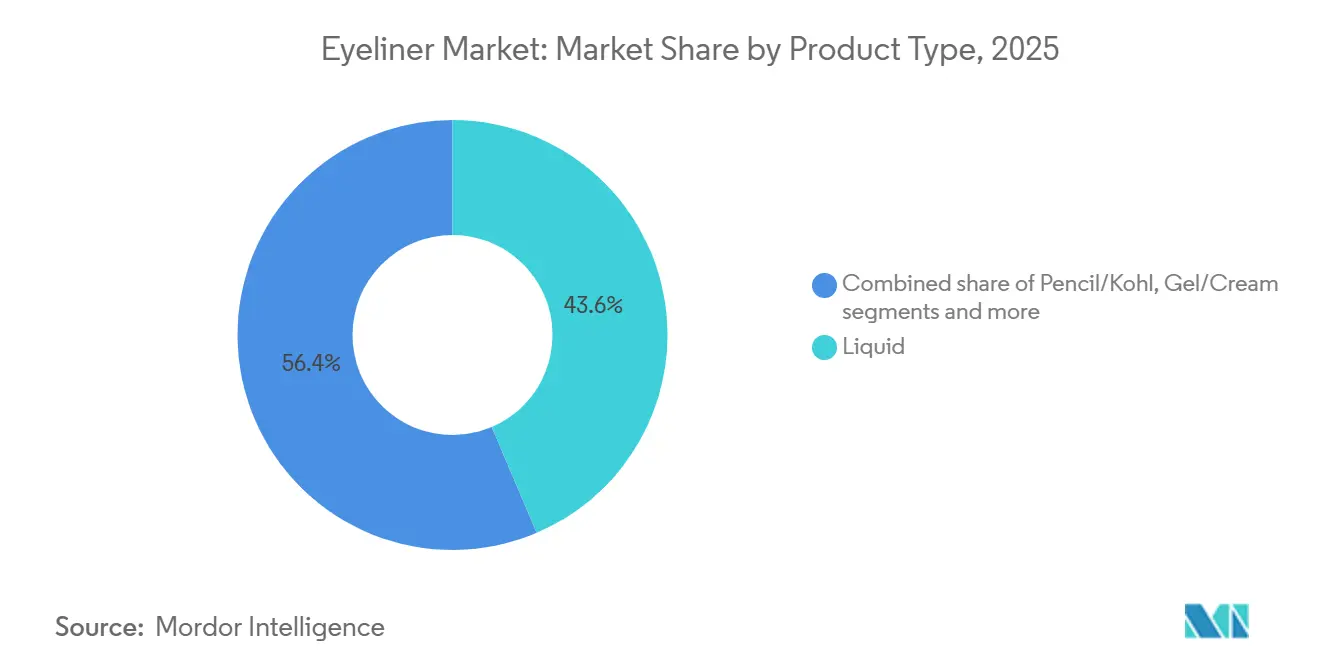

- By product type, liquid formats led with 43.59% of 2025 revenue, while gel and cream variants are projected to expand at a 7.08% CAGR through 2031.

- By formulation, regular finishes held 61.69% of the 2025 share, but waterproof lines are advancing at a 7.97% CAGR.

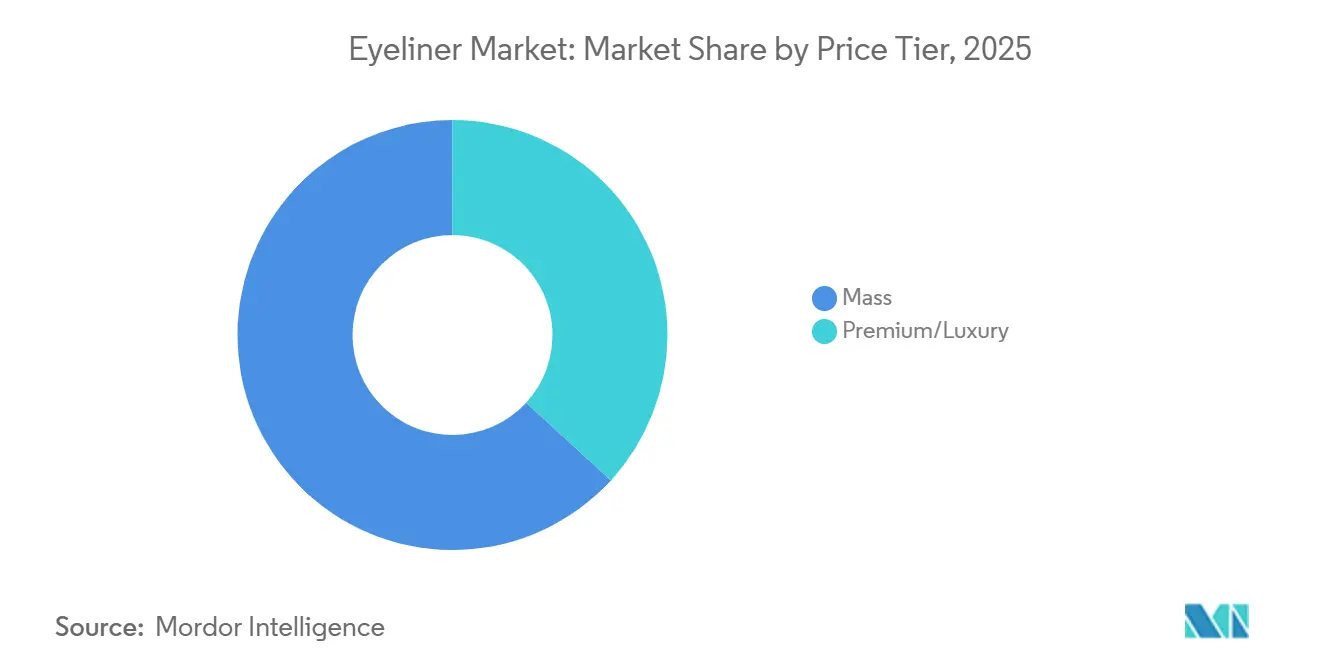

- By price range, the mass tier dominated with 63.18% 2025 share, whereas premium and luxury are forecast to grow at 7.17% CAGR.

- By distribution channel, health and beauty stores accounted for a 35.72% eyeliner market share in 2025, yet online retail is the fastest mover at 8.01% CAGR.

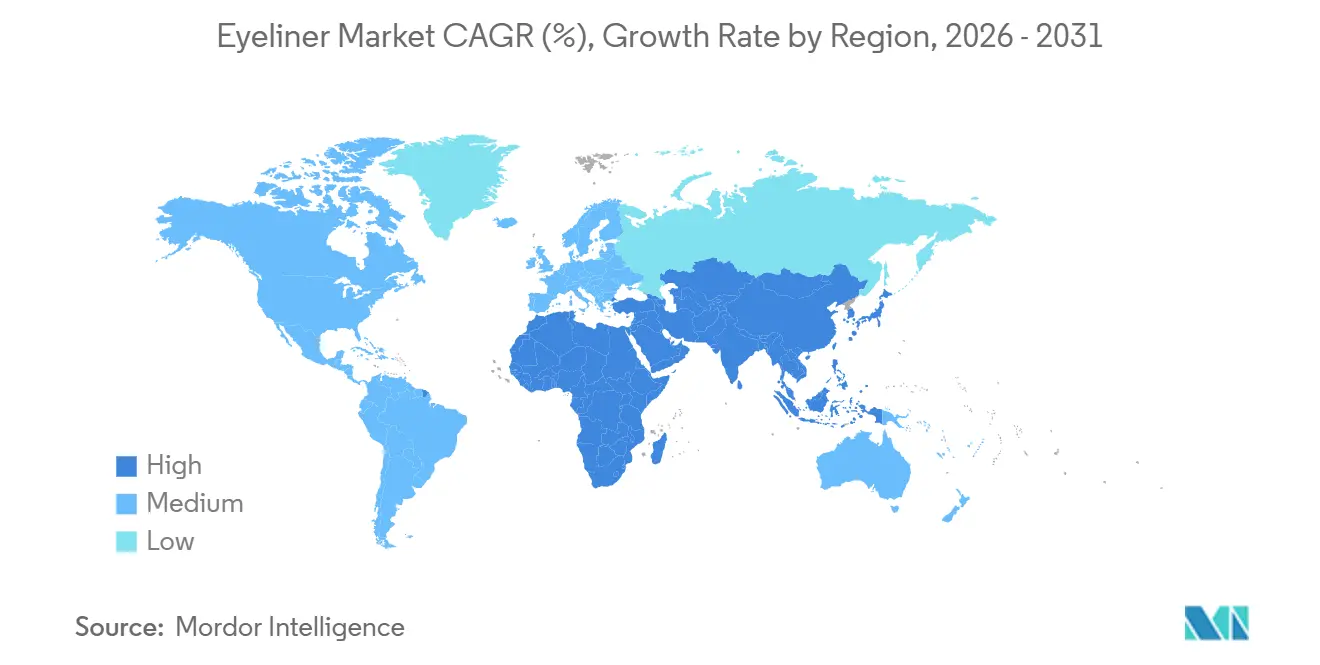

- By geography, Asia-Pacific accounted for 35.40% of global sales in 2025, while the Middle East and Africa region is expected to grow at the highest CAGR of 7.82% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Eyeliner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social-media–fuelled tutorial and influencer impact | +1.2% | Global, with a concentration in Asia-Pacific (TikTok Shop), North America, and Europe | Short term (≤ 2 years) |

| Demand for long-lasting, waterproof, and smudge-proof formulations | +1.5% | Global, particularly Asia-Pacific (humid climates), the Middle East (high temperatures) | Medium term (2-4 years) |

| Rise of clean, vegan, and cruelty-free cosmetics | +0.9% | North America, Europe (regulatory push), China (consumer preference) | Medium term (2-4 years) |

| Expansion of e-commerce and DTC beauty brands | +1.3% | Asia-Pacific (China, India, quick commerce), North America (omnichannel), Europe | Short term (≤ 2 years) |

| Packaging innovation and sustainability initiatives | +0.7% | Europe (EPR mandates), North America, Asia-Pacific premium segments | Long term (≥ 4 years) |

| Micro-precision tips enabling graphic looks | +0.8% | Asia-Pacific (K-beauty, J-beauty trends), North America (social media adoption) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of Clean, Vegan, and Cruelty-Free Cosmetics

Sephora's "Clean at Sephora" initiative, certifying 156 brands against a restricted-ingredient list, has become a key gatekeeper for shelf placement, driving reformulation of eyeliners to exclude parabens, phthalates, and synthetic fragrances. Leaping Bunny and PETA cruelty-free certifications are now essential for entry into European and North American prestige channels. In China, 72% of consumers prefer natural-ingredient cosmetics, including eyeliners, despite challenges in achieving pigmentation and waterproof performance without synthetic polymers. The EU's May 2026 ban on 15 CMR chemicals, including azo dyes and preservatives, has tightened reformulation timelines and raised research and development costs for brands without toxicology expertise. L'Oréal's 4,000 research and development scientists and 725 patents filed in 2025 highlight the investment needed to maintain clean formulations without compromising performance. Vegan, cruelty-free eyeliner growth is supported by India's Ayurvedic cosmetics trend, appealing to traditional and Gen Z consumers. In the Middle East and Southeast Asia, halal cosmetics demand has grown, with Saudi Arabia's streamlined SFDA registration process in January 2025 reducing approval timelines to under six months, enabling faster halal-certified eyeliner launches[2]Source: “Halal Cosmetics Registration Guide,” Saudi Food and Drug Authority, sfda.gov.sa.

Expansion of E-Commerce and DTC Beauty Brands

By 2030, India's beauty and personal care e-commerce is expected to account for a significant share of total spending, with quick and value-commerce models driving nearly 50% of online transactions. Nykaa's Q4 FY2026 net revenue growth in the high-20% range highlights how curated assortments, virtual try-on tools, and same-day delivery foster loyalty. In China, Tmall and JD.com dominate 60% of digital beauty sales, while live-streaming generates CNY 20 billion in gross merchandise value. Brands leveraging live-demo formats and flash-sale strategies excel during events like Double 11 and 618. e.l.f. Beauty's entry into 1,600 Rossmann stores in Germany and its rise to the number-four brand in the UK demonstrate how DTC-native brands optimize assortments using digital insights, achieving 38% year-over-year revenue growth in Q3 FY2026. L'Oréal's e-commerce penetration exceeding 30% of total sales by 2025, supported by 8,000 digital experts, showcases its ability to manage omnichannel inventory, personalized recommendations, and augmented-reality try-ons. By 2030, over 150 Indian beauty brands are projected to surpass INR 100 crore (around USD 12 million) in annual revenue, collectively capturing 25% of beauty spending, with eyeliner brands benefiting from unique formulations and platform-specific strategies.

Packaging Innovation and Sustainability Initiatives

Albéa's Endless Kiss refillable stick, launched in November 2025, features a mono-material polypropylene design that eliminates mixed-plastic components, enabling recycling in standard PP streams. This reduces per-unit material costs by 12% and warehousing lead times by five days while maintaining premium aesthetics through precision injection molding. Morrama's Maya Packaging, used by brands like Wild, employs paper-pulp refills made from bamboo and bagasse with a 5% PET lining, cutting plastic use by 98% compared to single-use eyeliner pens and allowing cartridge replacement without discarding applicators. The EU's Packaging and Packaging Waste Regulation (PPWR) and Extended Producer Responsibility (EPR) mandates are driving adoption of refillable and mono-material formats, with recycled-content targets and carbon-disclosure requirements penalizing virgin-plastic reliance[3]Source: “Packaging and Packaging Waste Regulation Factsheet,” European Commission, ec.europa.eu. Refill models can reduce packaging material use by 30% in prestige cosmetics, with lighter cartridges lowering freight emissions and improving pallet efficiency, offsetting upfront investment in durable outer shells. Glass and aluminum are resurging as premium materials due to their recyclability and luxury appeal, attracting consumers willing to pay for sustainability. QR codes and NFC tags on packaging link to environmental data and recycling instructions, turning compliance into brand storytelling. Faca Packaging's PET refill systems demonstrate that circular design can maintain aesthetics, with frosted and tinted PET and custom neck finishes meeting prestige eyeliner packaging standards while preparing brands for stricter regulations.

Micro-Precision Tips Enabling Graphic Looks

ILM Cosmetics launched its 0.01 mm Ultra Thin Eyeliner in April 2026, advancing felt-tip precision for seamless single-stroke application, supporting K-beauty's Idol Blur and J-beauty's translucent layering techniques. Japanese brands like CANMAKE dominate the precision segment with 0.01–0.1 mm tips, catering to natural looks that prioritize eye enlargement, securing a 35.40% share in the Asia-Pacific market. Schwan Cosmetics' Meta-Ink PrimeLiner, introduced in 2026, features a micro-precision applicator and a quick-dry formula that sets in under 10 seconds, addressing smudging risks in intricate designs popular on TikTok. UNICOS' V-Flash stamp eyeliner, launched in February 2026, automates winged-liner application with a dual-ended stamp-and-pen design, reducing application time to under one minute. Asteri Beauty's Calligraphy Eyeliner, released in 2026, offers a flexible brush tip for variable line widths, appealing to makeup artists and social media enthusiasts. Mirenesse's 4D stamp liner, also launched in 2026, includes interchangeable stamp shapes and a refillable pen base, combining precision with sustainability. These innovations lower the skill barrier, expanding the eyeliner market to occasional users and increasing purchase frequency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and low-quality products | -0.8% | Global, with concentration in Asia-Pacific (cross-border e-commerce), North America (online marketplaces) | Short term (≤ 2 years) |

| Stringent regulatory standards | -0.6% | Europe (CMR bans, PPWR), North America (MoCRA), Middle East (halal certification) | Medium term (2-4 years) |

| Substitution by semi-permanent tattooing | -0.3% | North America, Europe (cosmetic tattoo salons), Asia-Pacific urban centers | Long term (≥ 4 years) |

| Product safety and health concerns | -0.5% | Global, particularly among contact-lens wearers and sensitive-eye consumers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Low-Quality Products

In FY2023, counterfeit cosmetics made up 31% of U.S. Customs and Border Protection's (CBP) intercepted goods. A June 2024 seizure worth USD 575,000 highlighted the scale of gray-market operations undermining legitimate brands and risking consumer safety with unregulated ingredients. The April 2025 closure of the de minimis import loophole, which allowed duty-free shipments under USD 800, reduced low-value counterfeit eyeliner imports but did not eliminate domestic distribution via online marketplaces. MoCRA's facility registration mandate increased active listings from 35,102 pre-2024 to 589,762 by January 2025, creating a traceable supply chain that raises compliance costs for small brands while challenging counterfeit operators. In India, counterfeit eyeliners remain prevalent due to low prices, high turnover, and consumer preference for unbranded products. Brands are adopting QR codes, holographic seals, and blockchain-verified supply chains to protect equity and safety, though these measures add 2–4% to costs and require consumer education. Counterfeit vegan and cruelty-free claims erode trust in clean beauty, prompting brands to seek third-party certifications like Leaping Bunny and EcoCert, which involve audit fees but ensure differentiation.

Stringent Regulatory Standards

In May 2026, the European Union banned 15 CMR chemicals, requiring eyeliner reformulations to exclude prohibited azo dyes, preservatives, and fragrance compounds. This increased research and development costs, especially for brands without in-house toxicology teams. MoCRA's adverse-event reporting and facility registration mandates have added compliance burdens, disproportionately affecting smaller brands, while large players like L'Oréal leverage extensive research and development resources to manage costs. Saudi Arabia's SFDA streamlined halal-certified cosmetics registration in January 2025, cutting approval times to under six months but adding USD 5,000–15,000 per SKU in certification costs, challenging indie brands. India's proposed New Cosmetics Bill aims to enforce stricter ingredient disclosures, stability testing, and post-market surveillance, raising entry costs but reducing counterfeits. ISO 22716 certification, though voluntary, is becoming essential for exports to Europe and North America, with costs ranging from USD 10,000 to USD 50,000. EU fragrance allergen labeling rules, requiring disclosure of 26 substances, have driven eyeliner reformulations and label complexity, though rising demand for fragrance-free products has mitigated the impact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Dominance Drives Innovation

Liquid eyeliners hold a dominant 43.59% market share in 2025, as consumers prioritize precise application and intense color payoff in eye makeup. The gel/cream segment shows the highest growth rate at 7.08% CAGR (2026-2031), attributed to formulations that merge liquid precision with pencil blendability. This trend aligns with the industry's focus on products offering both performance and convenience. Pencil/kohl formats retain consistent demand due to their accessibility, particularly among beginners, while felt-tip pens gain popularity by combining pencil ease with liquid accuracy.

Powder and cake eyeliners serve a specific market segment, mainly professional makeup artists and users who prefer adjustable color intensity. Manufacturers are developing products that integrate multiple format benefits, driven by advances in applicator technology. Social media trends featuring detailed eyeliner styles reinforce liquid eyeliners' market position. Felt-tip pens show strong performance in Asian markets influenced by K-beauty trends, while gel and cream formulations expand globally as consumers seek products balancing immediate results with long-wearing comfort and skin compatibility.

By Formulation: Waterproof Innovation Accelerates

Regular formulations maintain a 61.69% market share in 2025, dominating the market due to their versatility and simple removal process that appeals to everyday consumers. Waterproof/sweat-proof variants are growing at 7.97% CAGR (2026-2031), driven by increasing demand for products that suit active lifestyles and varying weather conditions. Recent advances in polymer chemistry have enabled the development of long-lasting waterproof products that remain easy to apply and remove. This shift in growth patterns indicates a market transition toward specialized products that address specific consumer needs.

Increased consumer awareness about formulation benefits has created distinct market segments, with regular formulations serving daily and special occasion needs, while waterproof variants target sports activities, humid environments, and extended wear requirements. The emergence of "tubing" mascaras and eyeliners, which create flexible films, represents a new category offering waterproof benefits with simplified removal. The introduction of improved micellar water and oil-based cleansers has addressed traditional waterproof makeup removal challenges, supporting the growth of the waterproof segment. This market segmentation aligns with the beauty industry's move toward targeted solutions, enabling companies to implement premium pricing and distinct brand positioning.

By Price Tier: Premium Growth Outpaces Mass Market

The mass segment holds a 63.18% market share in 2025, demonstrating the segment's wide accessibility and appeal across various economic demographics. The premium/luxury segment shows strong growth potential with an 8.09% CAGR (2026-2031), as consumers increasingly choose higher-quality formulations and innovative packaging despite premium pricing. This shift aligns with broader beauty industry trends where consumers, especially younger demographics, prioritize product effectiveness and brand values, viewing beauty purchases as investments rather than discretionary spending.

Premium segment growth stems from advancements in sustainable packaging, clean formulations, and improved applicator technology that deliver measurable performance benefits. Mass market brands have adapted by introducing "masstige" products that combine premium features with accessible pricing. The luxury segment strengthens its position through exclusive retail partnerships and limited edition releases that generate consumer interest through perceived scarcity. E-commerce channels have increased access to premium brands while enabling direct-to-consumer models that deliver luxury quality at competitive prices by reducing retail markups. These price tier developments reflect increased consumer knowledge and their readiness to invest in products that offer clear value through performance, ethical practices, or enhanced user experience.

By Distribution Channel: Digital Transformation Accelerates

Health and beauty stores hold a 35.72%% market share in 2025, serving as primary destinations for product discovery and testing before purchase. Online retail stores demonstrate the highest growth rate at 8.01% CAGR (2026-2031), driven by the digital transformation in beauty retail and evolving consumer shopping patterns that emerged during the pandemic. This expansion is enhanced by virtual try-on features, AI-powered recommendations, and integrated omnichannel experiences.

Supermarkets/hypermarkets function as convenient points for replenishing established brands and daily-use products, while specialty beauty retailers differentiate themselves through curated product selections and professional consultation services. In the omnichannel space, retailers like Sephora report that 70% of customers who browse their websites make in-store purchases within 24 hours, generating 3.9 times higher return on ad spend. Online retail platforms are addressing the traditional limitation of physical product testing through augmented reality and artificial intelligence technologies.

Geography Analysis

Asia-Pacific holds 35.40% market share in 2025, supported by its large population base, increasing disposable incomes, and cultural emphasis on eye makeup, particularly influenced by K-beauty trends. The region's manufacturing capabilities and product innovations focus on precision application and long-wearing formulations. China's position as a major consumer market and manufacturing center creates cost efficiencies and enables rapid product development. High digital adoption and social media usage in the region accelerate trend adoption and product discovery.

The Middle East and Africa region demonstrates the highest growth rate at 7.82% CAGR (2026-2031). This growth stems from economic development, urbanization, and increasing female workforce participation. Social reforms have enhanced women's financial independence and spending power on beauty products. The United Arab Emirates' beauty retail market is expanding through digital channels. Regional regulatory developments include the UAE's Emirates Conformity Assessment Scheme (ECAS) and Emirates Quality Mark (EQM) certification requirements, while Saudi Arabia has implemented comprehensive cosmetic ingredient regulations.

Europe maintains its market position through strict cosmetic safety regulations and consumer demand for premium, ethically-sourced products. The EU's Regulation (EC) No 1223/2009 implements comprehensive safety requirements, including nanomaterial authorization and responsible person designation. European consumers show willingness to pay premium prices for products meeting safety and environmental standards. The region combines traditional beauty retail with e-commerce platforms, offering integrated shopping experiences. Moreover, North America and South America maintain consistent growth through established retail networks and increasing digital beauty technology adoption. North American consumers lead premium product consumption, while South American markets present growth opportunities through expanding middle-class populations and increasing beauty awareness.

Competitive Landscape

The eyeliner market exhibits moderate concentration, indicating balanced competition between established multinational corporations and emerging direct-to-consumer brands that are leveraging digital channels and innovative formulations to gain market share. Strategic patterns center on omnichannel excellence, with leading players investing heavily in technology integration to create seamless customer experiences across digital and physical touchpoints.

The competitive dynamics are being reshaped by the integration of artificial intelligence and augmented reality, as demonstrated by The Estée Lauder Companies' partnership with Microsoft to establish an AI innovation lab that develops tools for trend identification, product development, and customer experience enhancement. Companies are pursuing vertical integration strategies to control supply chains and ensure quality consistency, while simultaneously forming strategic partnerships to access specialized technologies and emerging market distribution networks.

White-space opportunities are emerging in the intersection of clean beauty and high-performance formulations, where companies that can deliver waterproof, long-wearing products using sustainable ingredients and packaging gain competitive advantages. Emerging disruptors are focusing on direct-to-consumer models that eliminate traditional retail markups while offering personalized product recommendations through AI-powered platforms and virtual try-on technologies.

Eyeliner Industry Leaders

L'Oréal S.A.

The Estée Lauder Companies Inc

Coty Inc.

Shiseido Company, Limited

LVMH Moët Hennessy Louis Vuitton SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ILM Cosmetics launched its 0.01 mm Ultra Thin Eyeliner, featuring a micro-precision felt-tip applicator that enables single-stroke application of intricate graphic designs and K-beauty Idol Blur techniques without dragging or skipping.

- March 2026: L'Oréal completed the acquisition of Kering Beauté, securing 50-year exclusive licenses to create, develop, and distribute fragrance and beauty products for Bottega Veneta and Balenciaga, with rights to enter a 50-year exclusive license for Gucci after Coty's existing license expires; the acquisition includes House of Creed and strengthens L'Oréal Luxe's portfolio in the prestige beauty segment.

- February 2026: UNICOS introduced the V-Flash stamp eyeliner, a dual-ended stamp-and-pen design that automates winged-liner application and reduces application time from five minutes to under one minute, democratizing graphic looks for consumers lacking steady-hand skills.

Global Eyeliner Market Report Scope

Eyeliner is a cosmetic product used to define and accentuate the appearance of the eyes. The global eyeliner market is segmented by product type, formulation, price range, distribution channel, and geography. By product, the market is segmented into liquid, pencil/kohl, gel/cream, felt-tip pen, and powder/cake. By formulation, the market is segmented into regular and waterproof/sweat-proof. By price range, the market is segmented into mass and premium/luxury. By distribution channel, the market is segmented into health and beauty stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Liquid |

| Pencil/Kohl |

| Gel/Cream |

| Felt-tip Pen |

| Powder/Cake |

| Regular |

| Waterproof/Sweat-Proof |

| Mass |

| Premium/Luxury |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Liquid | |

| Pencil/Kohl | ||

| Gel/Cream | ||

| Felt-tip Pen | ||

| Powder/Cake | ||

| Formulation | Regular | |

| Waterproof/Sweat-Proof | ||

| Price Range | Mass | |

| Premium/Luxury | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the eyeliner market and how fast is it growing?

The eyeliner market size is USD 8.76 billion in 2026 and is projected to expand to USD 11.81 billion by 2031 at a 6.16% CAGR.

Which product type holds the largest share?

Liquid eyeliners lead with 43.59% of global revenue in 2025, favored for intense pigmentation and precise application.

Which region offers the highest growth potential for brands?

The Middle East and Africa promises the fastest 7.82% CAGR through 2031, driven by rising disposable incomes and expanding female workforce participation.

Why are waterproof eyeliners gaining traction?

Waterproof/Sweat-proof formulations meet active lifestyle needs and are forecast to grow 7.97% annually, outpacing regular variants.

Page last updated on: