Spectacles Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

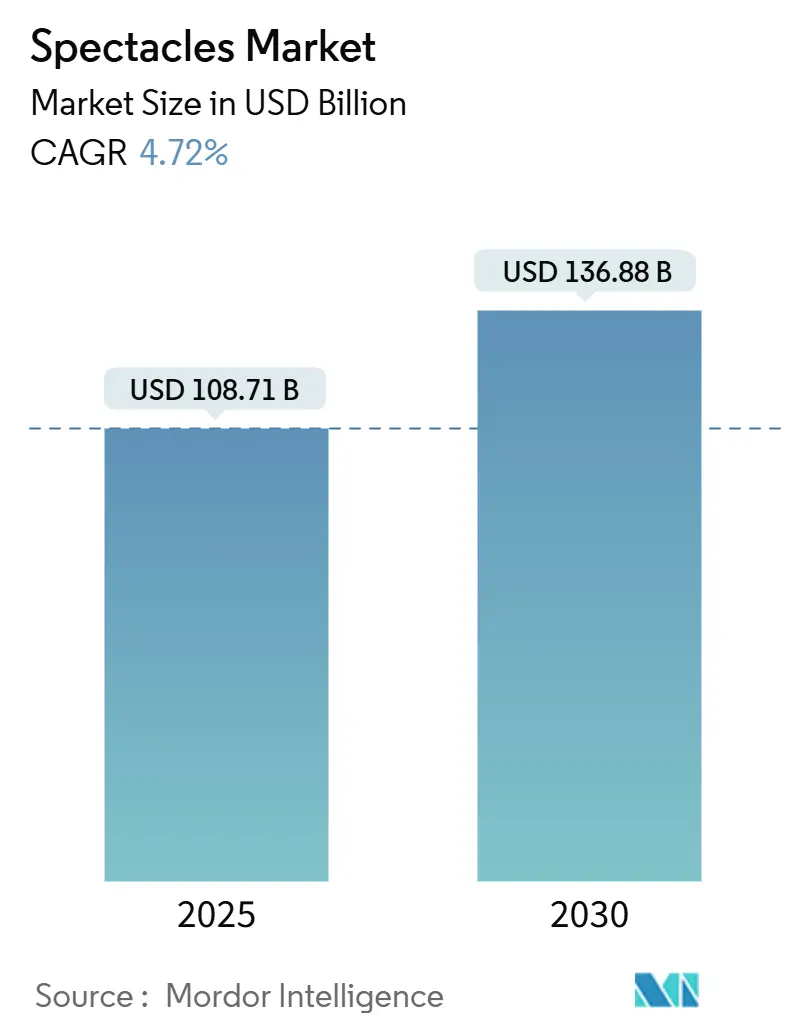

| Market Size (2025) | USD 108.71 Billion |

| Market Size (2030) | USD 136.88 Billion |

| Growth Rate (2025 - 2030) | 4.72% CAGR |

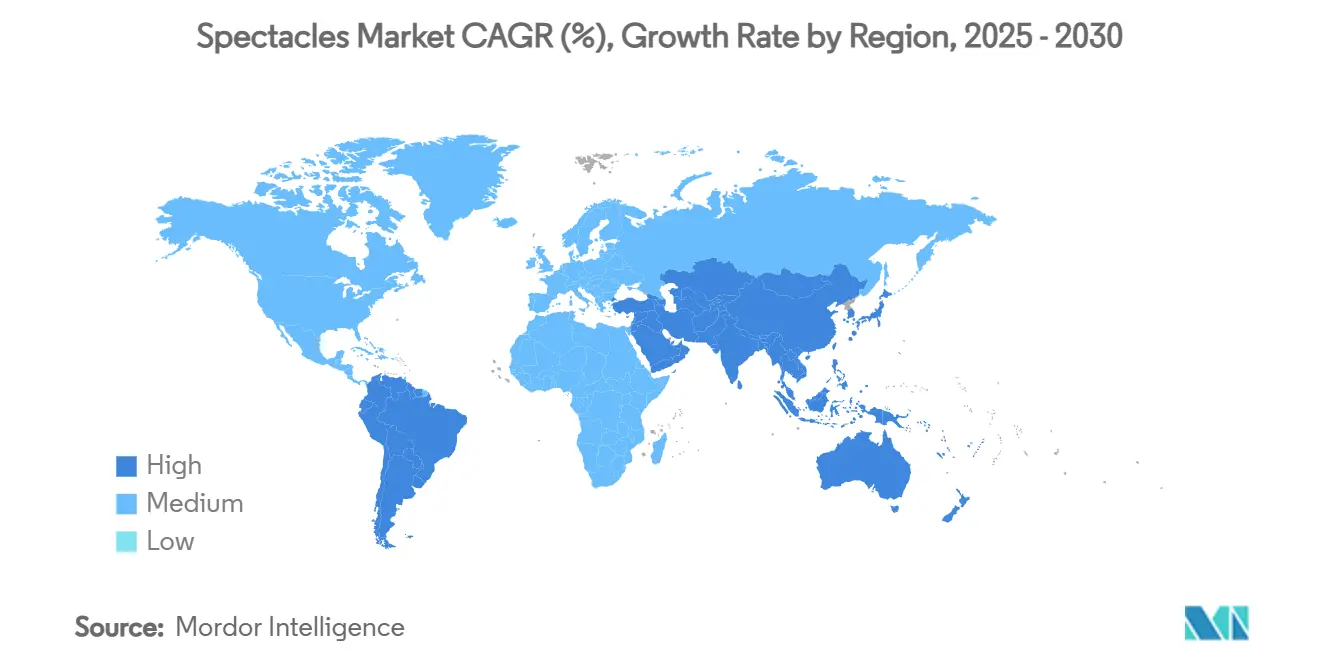

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

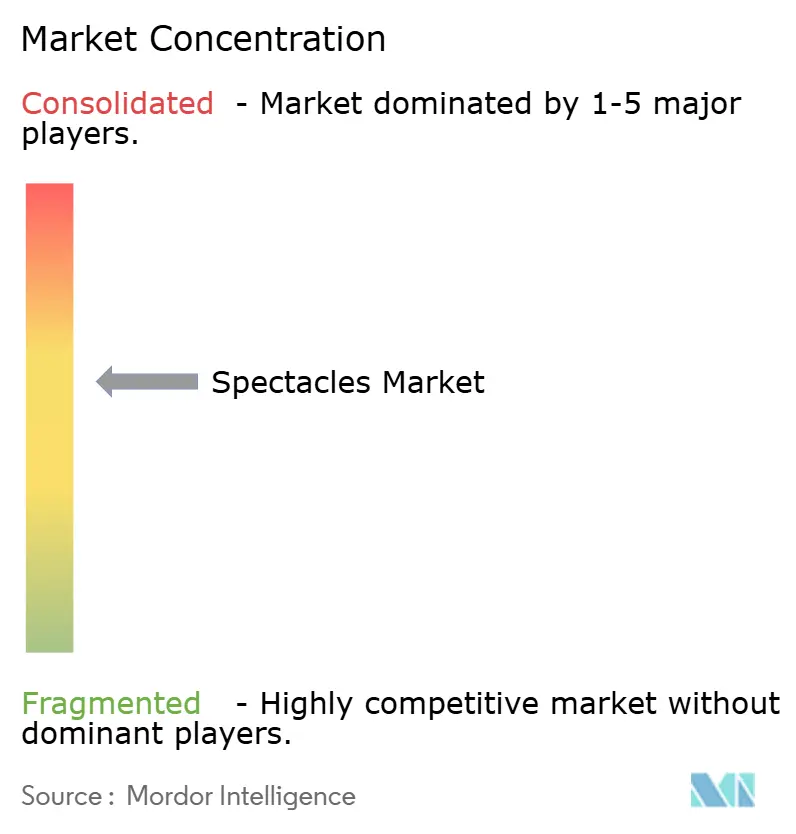

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spectacles Market Analysis by Mordor Intelligence

The global spectacles market size is valued at USD 108.71 billion in 2025 and is forecast to reach USD 136.88 billion by 2030, expanding at a 4.72% CAGR over 2025-2030. The eyewear market is evolving, shifting from merely correcting vision to becoming a platform where fashion, technology, and vision care seamlessly blend. This transformation is driven by demographic shifts, notably an aging population and increased screen time, which is accelerating myopia, especially among the youth. The aging population is contributing to a higher prevalence of presbyopia, while prolonged exposure to digital screens is exacerbating vision issues in younger demographics, creating a broad spectrum of demand for eyewear solutions. Innovations in freeform optics, lightweight alloys, and augmented reality are enabling brands to enhance their premium offerings and shorten production timelines.

Furthermore, the rise of digital distribution and virtual try-on technologies is tapping into previously unreachable customer segments. Virtual try-on software, in particular, is enhancing the online shopping experience by allowing customers to visualize products before purchase, thereby reducing return rates and increasing customer satisfaction. This evolution compels established players to juggle between engaging customers across channels and managing supply chain risks. This sets the stage for a dynamic spectacles market, projected to evolve significantly by 2030.

Key Report Takeaways

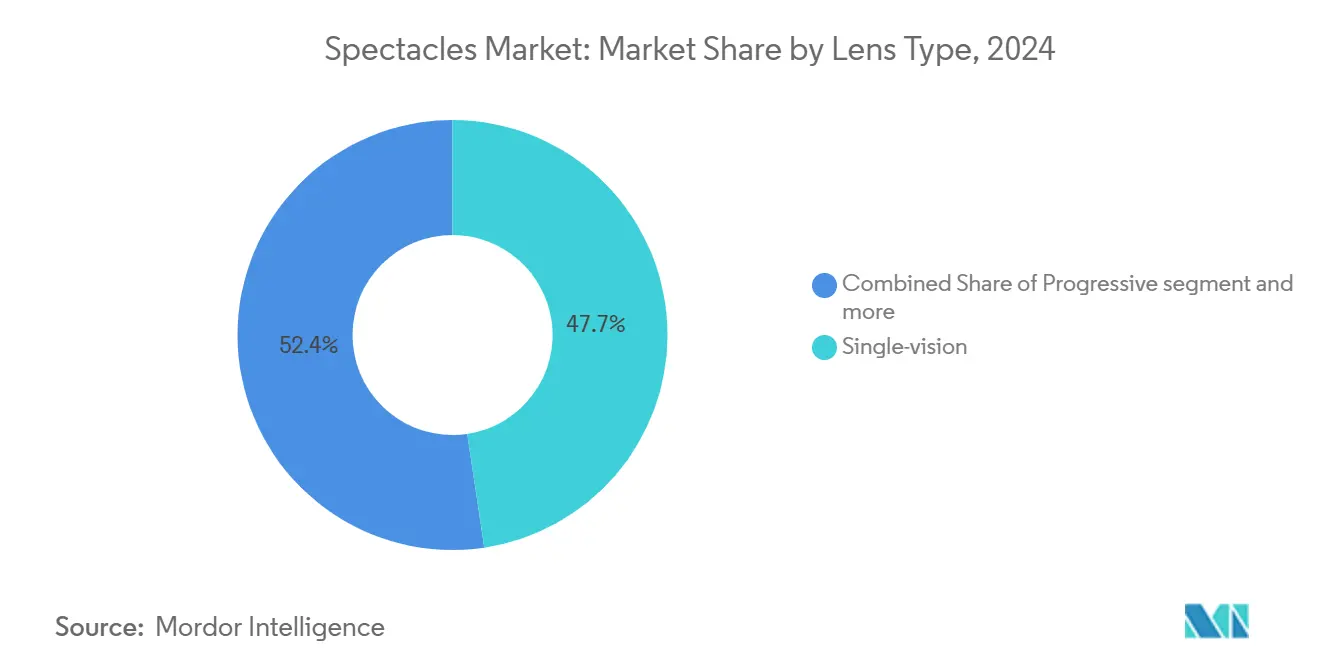

- By lens type, single-vision lenses led with 47.65% of the 2024 spectacles market share, and progressive lenses are projected to post the fastest 5.87% CAGR to 2030 across all regions.

- By end user, adults commanded 87.43% of demand in 2024, whereas the kids category is poised for a 5.42% CAGR through 2030, driven by rising myopia prevalence in the Asia-Pacific.

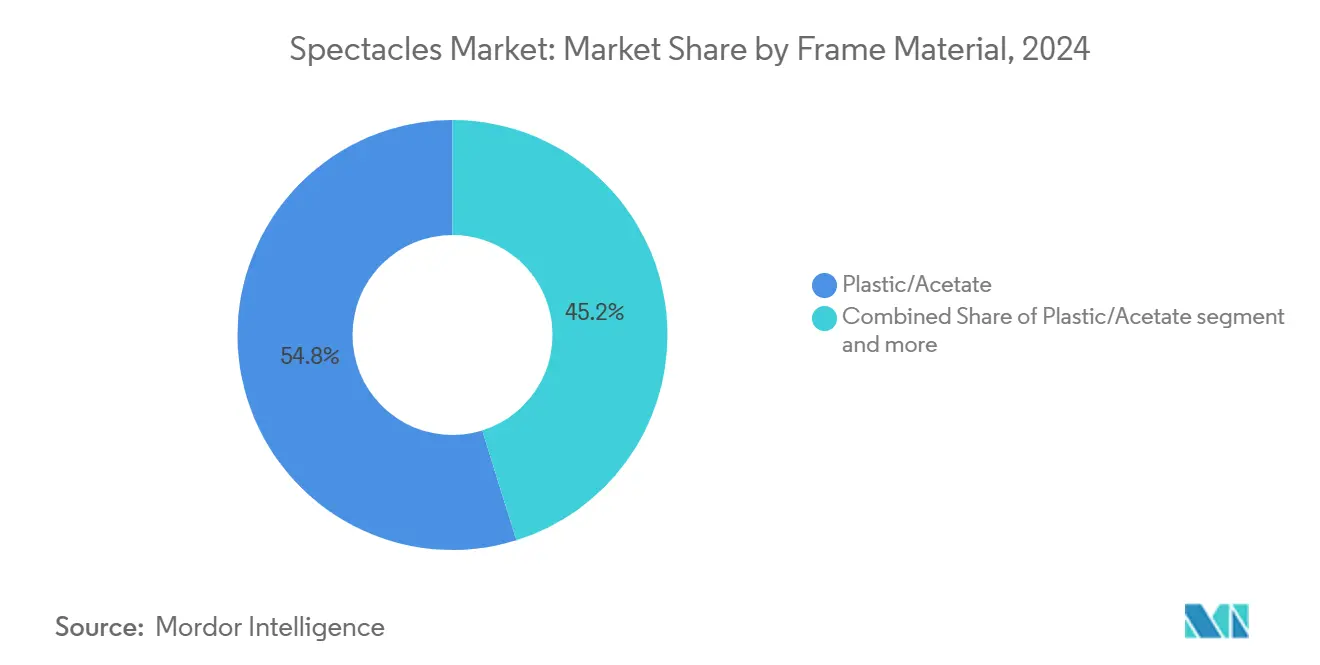

- By frame material, plastic/acetate captured 54.82% revenue in 2024, but metal frames are expected to expand at a 5.16% CAGR, reflecting premiumization trends in North America and Europe.

- By distribution channel, offline retail accounted for 87.61% of 2024 revenue; however, online sales are on track for a 5.27% CAGR to 2030, aided by virtual try-on adoption worldwide.

- By geography, North America retained 34.24% share of the spectacles market in 2024, while Asia-Pacific is forecast to deliver the quickest 5.38% CAGR during 2025-2030.

Market Trends and Insights

Drivers Impact Analysis of Spectacles Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing-population driven presbyopia surge | +1.2% | Global, Higher in North America and Europe | Long term (≥ 4 years) |

| Screen-time induced myopia among Gen-Z | +0.9% | Global, strongest in Asia-Pacific cities | Medium term (2-4 years) |

| Growth of low-cost fast-fashion frames | +0.7% | Global, led by emerging markets | Short term (≤ 2 years) |

| Vision-insurance expansion in emerging markets | +0.6% | Asia-Pacific core, Latin America spill-over | Long term (≥ 4 years) |

| AI-enabled personalised refraction kiosks | +0.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rise of blue-light filtering as workplace safety mandate | +0.3% | Global, regulatory focus in EU and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing-population driven presbyopia surge

By 2050, the population aged 65 and older is set to double, putting 2 billion individuals at risk of presbyopia. This surge is fueling a growing demand for premium progressive lenses, which offer seamless near-vision correction and cater to the aging population's need for functional and aesthetic solutions. According to the American Foundation for the Blind, 15.2% of adults aged 75 and older already face significant sight loss, highlighting the urgent need for advanced optical solutions to improve quality of life. In developed markets, there's a swift adoption of progressive lenses, with consumers favoring discreet, line-free designs that maintain a professional appearance while addressing vision challenges. The WHO's SPECS 2030 initiative, targeting a 40% improvement in coverage, underscores policy backing aimed at enhancing access to optical care, even in resource-limited areas[1]Source: World Health Organisation,"Launch of the WHO SPECS 2030 initiative, including the inaugural meeting of the Global SPECS Network", www.who.int. This initiative also emphasizes the importance of equitable distribution of vision correction solutions globally. Given these trends, the spectacle market is poised to become the primary avenue for managing presbyopia in the coming decade, driven by innovation, policy support, and increasing consumer awareness.

Screen-time induced myopia among gen-z

Gen Z's average weekly screen time has hit a staggering 96 hours, pushing the global prevalence of myopia towards the 50% mark. This surge in screen time has intensified the demand for specialized single-vision and myopia-management lenses. Studies from the UK indicate that from 2020 to 2022, children's screen time surged by 52%. This uptick correlates with accelerated axial elongation of the eye and an increase in diopter prescriptions, as highlighted in a 2024 report. Myopia, a condition where distant objects appear blurry, is becoming a significant public health concern due to its association with prolonged screen exposure[2]Source: National Center for Biotechnology Information,"The association between screen time exposure and myopia in children and adolescents: a meta-analysis", pmc.ncbi.nlm.nih.gov. Furthermore, data from the workplace reveal that 54% of Gen Z employees link their deteriorating vision to prolonged digital tasks. This trend underscores the need for workplace interventions and awareness campaigns to mitigate the impact of excessive screen use on eye health. In response to this growing concern, there's been a notable surge in innovations such as blue-light filtering, anti-reflective coatings, and ergonomic lens designs. These advancements aim to alleviate eye strain while maintaining style and affordability. Blue-light filtering technology, for instance, helps reduce the harmful effects of prolonged exposure to digital screens, while anti-reflective coatings enhance visual clarity and comfort. Ergonomic lens designs are tailored to meet the specific needs of individuals, ensuring optimal performance during extended screen use. On the regulatory front, there's a burgeoning interest in establishing screen safety standards. This could pave the way for protective spectacles to become mandatory in tech-centric workplaces, ensuring that employees are equipped with the necessary tools to safeguard their vision in increasingly digital environments.

Vision-insurance expansion in emerging markets

Recognizing the productivity boosts tied to corrected vision, governments are increasingly integrating eye care into universal health frameworks to address widespread vision issues. Medicare Advantage has announced enhanced eyewear reimbursements for 2025, aligning with similar updates from Medicaid, which aim to improve access to vision correction services. In India, the government’s ambitious "eyeglasses for all" initiative targets 550 million untreated vision cases, with the potential to increase worker productivity by 21.7% upon successful implementation. This initiative underscores the significant economic and social benefits of prioritizing vision health on a national scale. In Kenya, non-profit pilot programs demonstrate that micro-financed spectacles can effectively reach low-income consumers while maintaining sustainable profit margins, offering a replicable model for other developing economies. Additionally, the expansion of insurance coverage is transforming spectacles from discretionary goods into reimbursable medical devices. This shift is driving substantial growth in the spectacles market, particularly in price-sensitive regions, by making vision correction more accessible and affordable for underserved populations.

Rise of blue-light filtering as workplace safety mandate

With up to 97% of device users experiencing digital eye strain, employers and regulators are increasingly viewing blue-light filtration as essential health protection rather than a mere upgrade. Digital eye strain, often caused by prolonged exposure to screens, leads to symptoms such as headaches, blurred vision, and discomfort, which can significantly impact workplace productivity. In response to studies linking eye strain to productivity losses, vision plans have begun reimbursing coated lenses to mitigate these effects. Although some research questions the therapeutic benefits of blue-light filtration, the policy momentum remains strong; for instance, European authorities have classified extended screen time as an occupational hazard, mandating preventive eyewear to safeguard workers' health. These compliance regulations have spurred demand for coated lenses, which come with a higher average selling price, thereby benefiting the spectacles market, especially through corporate procurement channels. This trend highlights the growing recognition of eye health as a critical component of occupational safety and productivity enhancement.

Restraints Impact Analysis of Spectacles Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unregulated online sales of sub-par lenses | -0.8% | Global, concentrated in price-sensitive markets | Short term (≤ 2 years) |

| Rebound in corrective eye-surgery uptake | -0.6% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Supply-chain fragility in acetate and rare-earth coatings | -0.5% | Global, manufacture centred in China | Long term (≥ 4 years) |

| Counterfeit luxury frames eroding brand value | -0.4% | Global, strongest in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Unregulated online sales of sub-par lenses

Bypassing prescription verification, e-commerce platforms are selling lenses, which erodes consumer trust and poses significant vision risks. This practice allows consumers to purchase lenses without proper oversight, increasing the likelihood of incorrect prescriptions and potential eye health complications. Meanwhile, cut-price suppliers, taking advantage of scant regulatory oversight, are putting pressure on legitimate retailers who shoulder compliance costs associated with adhering to regulations. These suppliers often prioritize cost-cutting over quality, leading to a dilution in product standards. This dilution not only tarnishes brand reputations but also nudges customers towards surgical alternatives, which are perceived as more permanent and reliable solutions for vision correction. While education campaigns and stricter rules on digital platforms seek to stem this tide by raising awareness and enforcing compliance, persistent loopholes in the regulatory framework continue to challenge the mid-term growth rate of the spectacles market, as reflected in its compound annual growth rate (CAGR).

Rebound in corrective eye-surgery uptake

As consumers increasingly turn to permanent vision correction solutions, the demand for traditional spectacles faces a challenge from the recovery of LASIK and refractive surgeries, which had been deferred during the pandemic. Despite a 50% decline in LASIK procedures since 2007, the annual procedures for refractive cataract surgery have surged to 350,000, highlighting a growing acceptance of surgical alternatives among certain demographics. This shift reflects advancements in surgical technologies and increased awareness of the benefits of refractive surgeries, such as improved vision quality and reduced dependency on corrective eyewear. To cater to the rising demand for outpatient ophthalmic procedures, ambulatory surgical centers are ramping up their capacity. This expansion not only enhances accessibility but also curtails costs, which had previously tilted in favor of spectacles. Additionally, the convenience of outpatient settings and shorter recovery times contribute to the growing preference for surgical options. Yet, challenges remain: surgical complications, such as dry eye or glare, and age-related vision changes ensure that a segment of the post-surgical population still relies on spectacles, tempering the long-term shift away from them. Furthermore, the high upfront costs of surgeries and limited insurance coverage in some regions continue to act as barriers for certain consumer groups, sustaining the demand for traditional spectacles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Spectacles Market Segment Analysis

By Lens Type:

Progressive Innovation Drives Premium ShiftIn 2024, single-vision lenses command a dominant 47.65% share of the market. This leadership position is largely attributed to a rising myopia epidemic, particularly among the youth in the Asia-Pacific. Here, heightened screen time has led to a surge in prescription eyewear adoption. The segment's cost-effectiveness and straightforward nature make it particularly appealing to first-time eyewear users and those sensitive to pricing. Moreover, enhanced manufacturing efficiencies enable producers to uphold profit margins, even amidst fierce pricing battles with online retailers and fast-fashion eyewear brands. The robust volume sales of single-vision lenses further solidify their market stability. In essence, single-vision lenses continue to be a go-to choice, offering practical and budget-friendly solutions to a broad audience.

On the other hand, progressive lenses are on a rapid ascent, boasting a projected CAGR of 5.87% through 2030. This surge is driven by a consumer shift towards premium offerings that ensure smooth vision correction, sidestepping the visible lines of traditional bifocals. As older consumers make the transition to progressive lenses, the demand for bifocals wanes, thanks to the superior aesthetics and functionality of progressives. Innovations like freeform surfacing and digital lens design have not only shortened adaptation periods but also enhanced peripheral vision clarity. This has led to consumers being more willing to invest in these premium innovations. Thus, the progressive lens segment adeptly leverages both an aging consumer base and state-of-the-art technology, propelling its robust market growth.

By End User:

Pediatric Acceleration Alters Long-Run Demand CurveIn 2024, adults dominated the spectacles market, accounting for 87.43% of total revenue. Yet, as regions like North America and Europe near saturation, growth in this adult segment is decelerating. To counteract stagnant population growth and maintain steady adult unit sales, brands are innovating. They're not just updating fashion trends but also introducing smart glasses and enhancing safety eyewear for workplaces. A pivotal strategy is premium upselling, with features like blue-light filter lenses, augmented reality (AR)-ready frames, and subscription-based replacement programs boosting customer lifetime value. These tactics are essential for sustaining revenue in a fiercely competitive landscape. While the adult segment remains dominant, its reliance on innovation and added-value features underscores the challenges of a maturing market.

On the other hand, the pediatric segment is witnessing the fastest growth, expanding at an annual rate of 5.42%. This surge is driven by an earlier onset of myopia in children and parents' increasing willingness to invest in premium lenses that slow its progression. In the Asia-Pacific, supportive policies, such as government-subsidized school vision screenings, further boost prescription uptake. In response, manufacturers are crafting durable frames using hypoallergenic materials and flexible spring hinges. These innovations not only minimize breakage and returns but also enhance profitability, even at lower price points. Projections suggest that today's pediatric wearers will transition to progressive lenses by 2035, fueling compounded revenue growth. Moreover, this tech-savvy group is primed to embrace smart eyewear, presenting brands with a golden opportunity to foster early loyalty and tap into future growth.

By Frame Material:

Metal Reinvention Spurs Premium RepositioningIn 2024, plastic and acetate frames dominated the market, clinching 54.82% of total sales. Their allure stems from cost-effective production, a spectrum of vibrant colors, and a strong foothold in the fast-fashion arena. Thanks to injection molding technology, retailers can swiftly align new collections with the ever-evolving seasonal fashion trends. Addressing rising sustainability concerns, the industry has innovated bio-acetate materials, curbing the dependence on petroleum-based plastics and easing consumer apprehensions. These advancements empower brands to harmonize style, affordability, and ecological mindfulness. In essence, the versatility of plastic and acetate frames, coupled with their resonance with both fashion-forward and budget-conscious consumers, cements their market dominance.

Metal frames are on an upward trajectory, boasting a 5.16% CAGR, thanks to innovations in alloy blends like beta titanium. These blends offer a harmonious mix of lightweight comfort and robust strength. The superior tensile strength of metal frames facilitates ultra-thin temples, reducing contact pressure. This feature resonates well in professional settings that favor a minimalist aesthetic. The premium image of metal frames not only commands higher profit margins but also sees consumers opting for metal frames with progressive lenses or specialty coatings, boosting the average transaction value. Furthermore, hybrid designs merging acetate fronts with metal temples broaden their appeal and provide a buffer against raw material price swings. Eco-aware consumers are drawn to new recycling initiatives for aluminum and stainless steel, crafting a sustainability narrative that justifies the premium price tag. Yet, the dependence on rare-earth PVD coatings for scratch resistance and bespoke finishes poses supply chain challenges, underscoring the urgent need for diversified sourcing to safeguard the metal frame market's growth.

By Distribution Channel:

Omnichannel Redefines Customer JourneyIn 2024, offline optical stores dominated the global spectacles market, capturing a substantial 87.61% share of the revenue. This stronghold is largely due to the value consumers place on professional fitting services and the allure of immediate, in-person purchases. These traditional retailers adeptly cater to customer needs, like personalized adjustments and instant product access, which are challenging to replicate in the online realm. Legacy chains bolster this offline advantage by introducing appointment-based digital kiosks, which not only streamline the sales process but also elevate the overall customer experience. Moreover, the trend of omnichannel bundles, where customers make online purchases but seek in-store adjustments, is gaining traction, particularly in urban locales. Despite shifting consumer preferences, offline stores continue to be pivotal revenue-generating hubs.

On the other hand, online retail is emerging as the fastest-growing segment, boasting a compound annual growth rate of around 5.27%. This surge can be attributed to innovations like augmented reality (AR) try-on technology, remote pupillary distance measurements, and efficient e-prescription verifications, all of which significantly enhance the online shopping journey. To further bridge the divide between digital ease and physical service, pure-play e-tailers are rolling out micro-showrooms for product adjustments and lens exchanges. The COVID-19 pandemic acted as a catalyst, propelling e-commerce adoption and instilling lasting online shopping habits. This shift is bolstered by improved return logistics and regulatory assurances in the US and Europe regarding prescription validity. Meanwhile, emerging markets are sidestepping traditional infrastructures, harnessing smartphone-centric and social commerce platforms to drive impulse purchases among a burgeoning consumer base. In this evolving landscape, success hinges on agility in digital technologies, adept data analytics, and a focus on efficient last-mile delivery.

Geography Analysis

North America Spectacles Market

In 2024, North America secured a 34.24% share of the global spectacles market, buoyed by robust vision insurance and a penchant for discretionary spending. The region shows a pronounced tilt towards premium progressive and smart eyewear. Notably, the AI glasses pipeline from Google and Warby Parker underscores North America's innovative edge, positioning the region as a leader in technological advancements within the spectacles market. However, with a sluggish population growth and an uptick in surgeries, unit expansion faces challenges. This shift nudges brands to explore service-based revenues, like subscription lens replacements, which offer recurring income streams and foster customer loyalty.

APAC Spectacles Market

Asia-Pacific, riding on urban myopia trends, a burgeoning middle class, and proactive national screening, boasts the highest CAGR at 5.38%. In 2023, China led the charge with frame exports worth USD 3.31 billion, reflecting its dominance in global manufacturing. Meanwhile, India's Lenskart, eyeing a USD 10 billion IPO, stands as a testament to home-grown prowess and the region's entrepreneurial spirit. Here, a volume-driven approach offsets lower average selling prices (ASPs), pushing firms towards localised manufacturing and distribution strategies to cater to diverse consumer needs and improve operational efficiency.

EMEA Spectacles Market

Europe finds itself straddling maturity and growth. Italy, with its luxury focus, exports frames worth USD 1.64 billion, yet simultaneously imports premium collections to cater to its fashion-forward clientele[3]Source: The Observatory of Economic Complexity,"Exporters of Eyewear Frames in 2023", oec.world. The recent Operation Dolce Vita seizure highlights Europe's stringent counterfeit policing, bolstering protections for genuine brands and ensuring market integrity. In the Middle East and Africa, while the spectacles market remains in its infancy, there's a promising horizon. As infrastructure developments enhance optical coverage, early movers eye the demographic advantages, particularly the region's young and growing population. Yet, challenges loom: currency fluctuations and supply chain disruptions hinder swift expansions, requiring companies to adopt adaptive strategies to navigate these hurdles effectively.

Competitive Landscape

The spectacles market exhibits moderate consolidation. EssilorLuxottica is on a vertical consolidation spree, snapping up frame makers, lens labs, and even ophthalmic clinics, crafting a comprehensive ecosystem that's tough for competitors to match. This strategy allows the company to control the entire value chain, from manufacturing to retail, ensuring quality and cost efficiency. Meanwhile, direct-to-consumer brands like Warby Parker and Lenskart are shaking up the status quo. With nimble supply chains and savvy data-driven merchandising, they're enticing customers with unbeatable prices and convenience. These brands leverage technology to predict consumer preferences and optimize inventory, further enhancing their competitive edge. Partnerships are reshaping the competitive landscape: Google is backing Warby Parker's AI glasses, Meta has teamed up with Ray-Ban, and VSP Vision's acquisition of Eyemart Express bolsters its rural outreach, enabling better access to underserved markets.

Investor valuations are now swayed by intellectual-property assets in waveguide optics, biometric sensing, and cloud-based prescription management. A notable 35% spike in patent filings from 2023 to 2025 highlights the industry's pivot towards augmented-reality display integration and digital convergence. These advancements are expected to redefine user experiences, blending traditional eyewear functionality with cutting-edge technology.

Mid-cap companies are carving out their niches, focusing on areas like children's myopia management, eco-friendly materials, and ergonomic sports frames, all while harnessing online communities to build brand loyalty. By addressing specific consumer needs and emphasizing sustainability, these firms are creating strong differentiation in the market. As traditional optics, consumer electronics, and health-tech converge, the spectacles industry is witnessing a surge in competitive energy, driving innovation and expanding the scope of offerings.

Spectacles Industry Leaders

-

EssilorLuxottica SA

-

Hoya Corporation

-

Safilo Group S.p.A.

-

Fielmann AG

-

Marchon Eyewear Inc.

- *Disclaimer: Major Players sorted in no particular order

Spectacles Market Companies Covered in this Report

- EssilorLuxottica SA

- Hoya Corporation

- Safilo Group S.p.A.

- Marchon Eyewear Inc. (VSP Vision)

- Fielmann AG

- Shamir Optical Industry

- Marcolin S.p.A.

- Carl Zeiss AG

- The Cooper Companies (CooperVision Inc.)

- Warby Parker Inc.

- Zenni Optical Inc.

- Oliver Peoples

- Charmant Group

- De Rigo Spa

- Specsavers Optical Group

- Alcon Vision LLC

- Harvey & Lewis Optical

- Lenskart Solutions Pvt Ltd

- Oakley Inc.

- Silhoutte International Schmeid AG

Recent Industry Developments in Spectacles Market

- June 2025: in collaboration with Meta and EssilorLuxottica, Prada unveiled its inaugural AI-integrated smart glasses. These glasses feature a sleek design with lightweight acetate frames and sculpted metal temples, combining advanced technology with high-end fashion to cater to tech-savvy consumers.

- June 2025: Lenskart introduced its latest offering, the Smart Glasses Phonic, equipped with Bluetooth connectivity, AI assistant access, and other advanced features. These glasses, reportedly co-developed with Qualcomm, aim to enhance user convenience by integrating cutting-edge technology into everyday eyewear.

- May 2025: EssilorLuxottica bolstered its presence by acquiring Optegra, integrating over 70 hospitals and diagnostics across the UK, Czech Republic, Poland, Slovakia, and the Netherlands. This acquisition expands its med-tech portfolio, offering services such as cataract treatment, lens exchange, and AI-driven eye care, thereby strengthening its position in the integrated eye care market.

- May 2025: Warby Parker joined forces with Google to collaboratively design AI-enhanced smart glasses. Google invested approximately USD 150 million in the project, utilizing multimodal AI and Android XR technology to develop innovative eyewear solutions that blend functionality with style.

Global Spectacles Market Report Scope

Segmentation Overview

| Single-vision |

| Bifocal |

| Progressive |

| Adults |

| Kids |

| Metal |

| Plastic/Acetate |

| Combination and Others |

| Offline Retail Stores |

| Online Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Lens Type (Value) | Single-vision | |

| Bifocal | ||

| Progressive | ||

| By End User | Adults | |

| Kids | ||

| By Frame Material (Value) | Metal | |

| Plastic/Acetate | ||

| Combination and Others | ||

| By Distribution Channel | Offline Retail Stores | |

| Online Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the spectacles market in 2025?

The spectacles market size stands at USD 108.71 billion in 2025 with a 4.72% CAGR projected to 2030.

Which lens type is growing fastest worldwide?

Progressive lenses lead growth with a 5.87% CAGR as consumers favor seamless multi-focal correction.

Why is Asia Pacific a key growth region for spectacles?

High urban myopia rates, rising disposable incomes, and rapid digital adoption combine to deliver a 5.38% CAGR through 2030.

How are online channels affecting eyewear sales?

Online retail posts a 5.27% CAGR by leveraging virtual try-on and simplified prescription verification while offline retains volume leadership.

Page last updated on: