Eye Health Supplement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 4.23 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

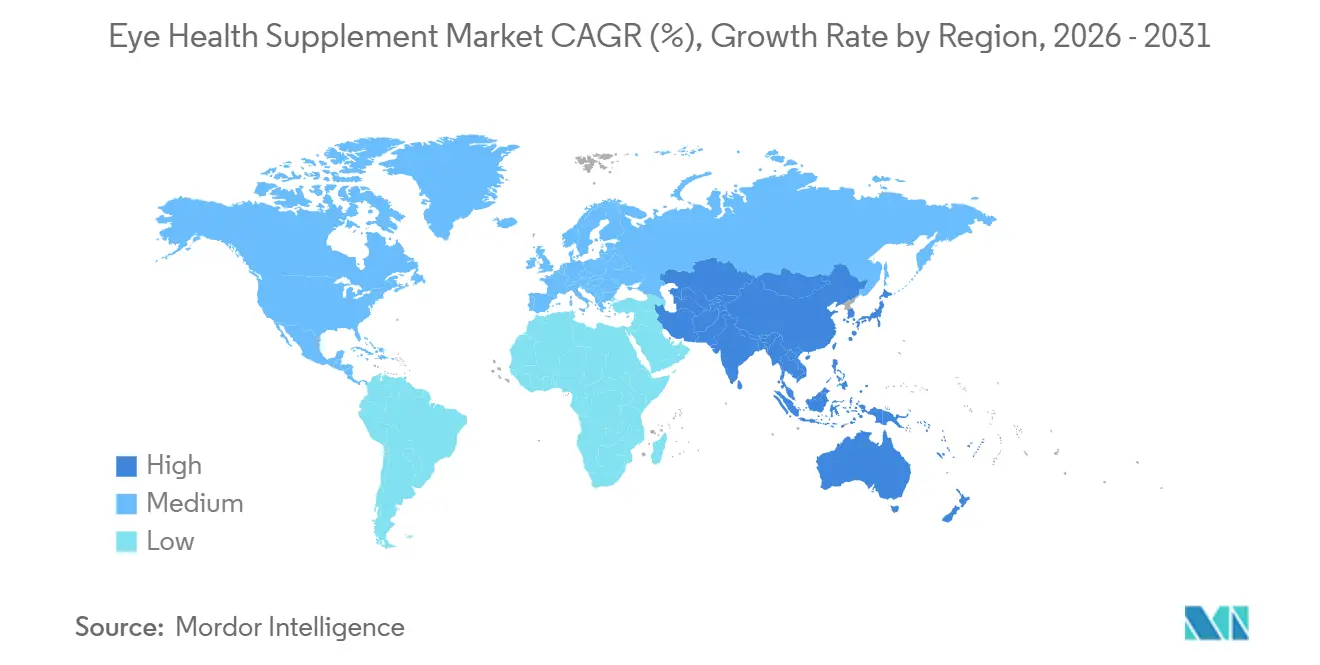

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

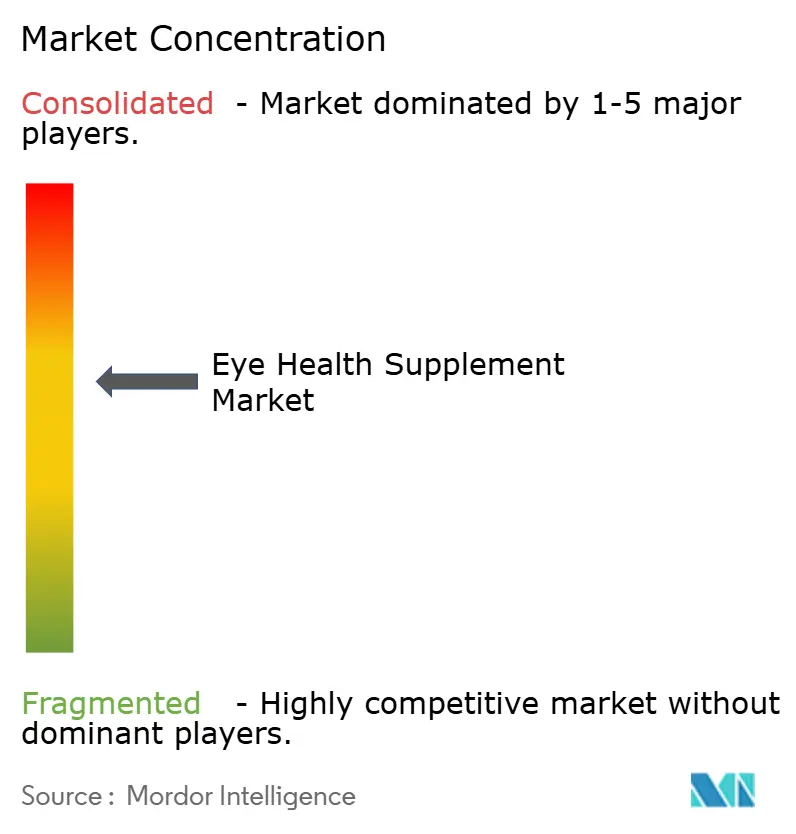

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eye Health Supplement Market Analysis by Mordor Intelligence

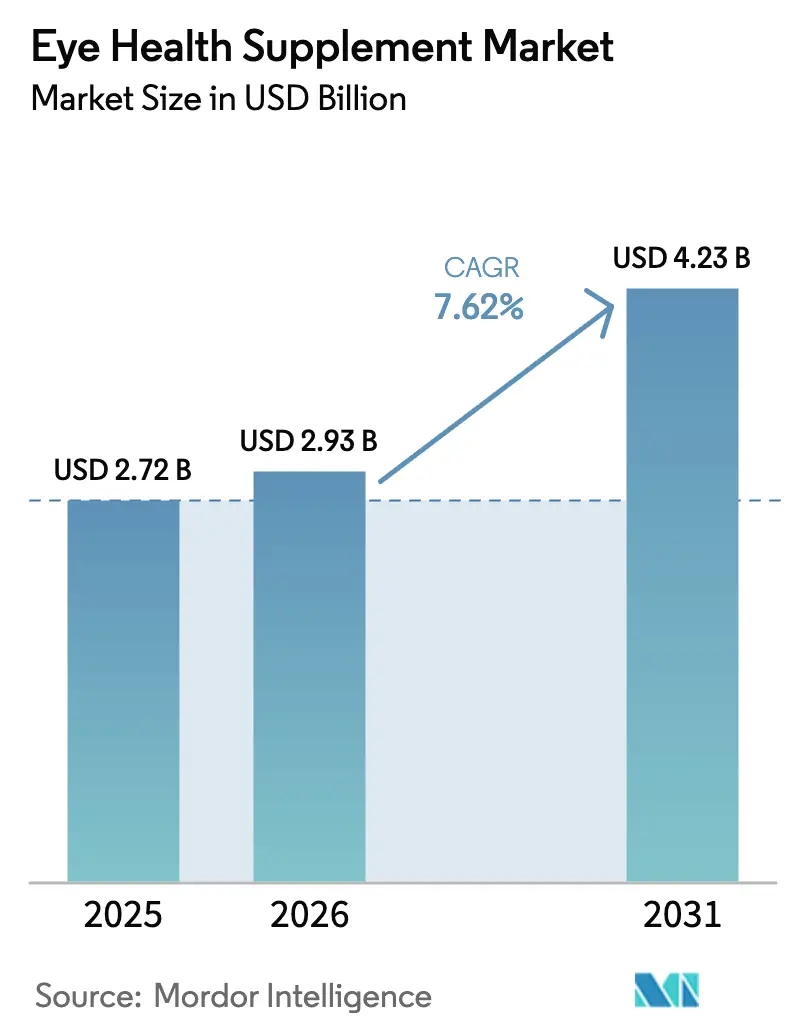

The Eye Health Supplement Market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.93 billion in 2026 to reach USD 4.23 billion by 2031, at a CAGR of 7.62% during the forecast period (2026-2031).

Ingredient innovation, led by carotenoids combined with omega-3 fatty acids, is widening the consumer base by demonstrating an 18% reduction in geographic atrophy progression among age-related macular degeneration (AMD) patients over 24 months. Gummy and chew formats are pulling new users toward preventative routines after pectin encapsulation raised carotenoid bioavailability to 87% of softgels while removing gelatin allergens. Direct-to-consumer (DTC) subscription channels are lowering acquisition costs by 34% and locking purchasers into 90-day refill cycles, a pattern that is redistributing category profits toward agile online brands. Supply shocks in Peruvian anchovy fisheries have tightened marine-sourced DHA and EPA availability, but cost-parity micro-algae alternatives now permit mass-market price points without mercury risk.

Key Report Takeaways

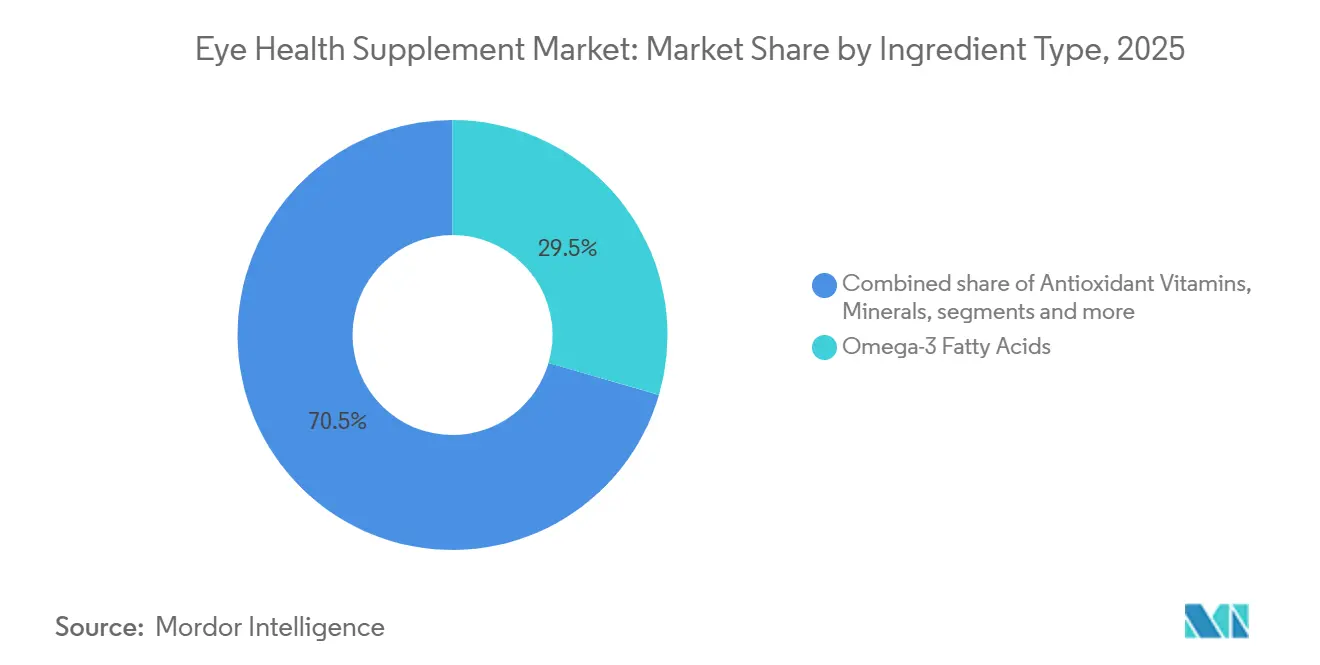

- By ingredient type, omega-3 fatty acids led with 29.55% of the eye health supplement market share in 2025, while carotenoids are projected to expand at a 9.85% CAGR through 2031.

- By form, softgel capsules held 45.53% of the eye health supplement market size in 2025, whereas gummies and chews are advancing at a 10.75% CAGR during the forecast period.

- By indication, AMD commanded 39.15% revenue in 2025, yet myopia progression is forecast to grow at 10.82% CAGR.

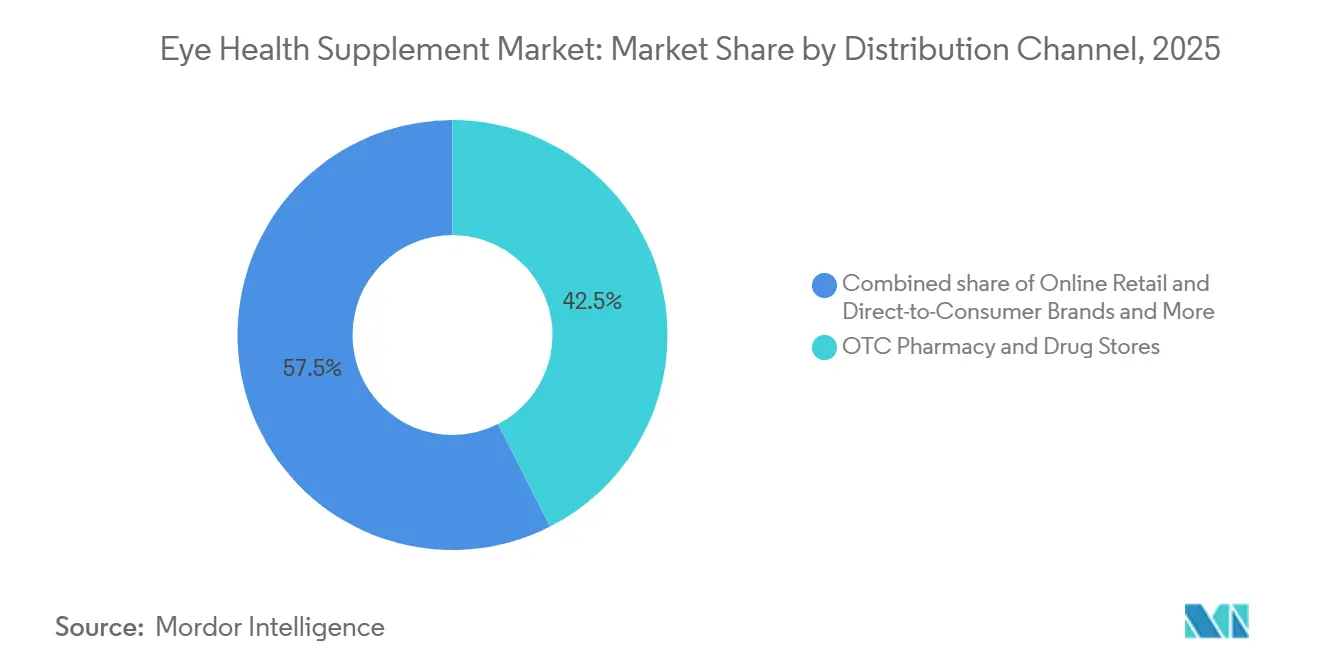

- By distribution channel, pharmacy and drug stores accounted for 42.52% revenue in 2025, while online retail and DTC brands are expected to grow at 12.12% CAGR through 2031.

- By age group, adults comprised 60.54% of the eye health supplement market size in 2025, whereas the pediatric segment is set to record a 9.32% CAGR over 2026-2031.

- By geography, North America captured 36.62% revenue in 2025, yet Asia-Pacific is poised for the fastest 8.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Eye Health Supplement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of ocular diseases linked to metabolic syndrome | +1.8% | Global, with concentration in South Asia and Middle East | Long term (≥ 4 years) |

| Adoption of preventative-health mindset among Gen Z & Millennials | +1.3% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Surge in self-directed eye-care via e-commerce nutraceuticals | +1.6% | Global, led by North America and China | Short term (≤ 2 years) |

| Clinical validation of carotenoid + omega-3 synergistic formulations | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| Micro-algae DHA/EPA cost breakthroughs enabling mass-market pricing | +0.9% | Global, early adoption in North America and Europe | Long term (≥ 4 years) |

| Patent expiries spurring fortified eye-vitamin line extensions | +0.8% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Ocular Diseases Linked to Metabolic Syndrome

Diabetic retinopathy incidence tracks hemoglobin A1c levels above 7.5%, a threshold exceeded by 58% of diagnosed diabetics in the United States in 2024[1]Centers for Disease Control and Prevention, “National Diabetes Statistics Report, 2024,” cdc.gov. India’s urban prevalence reached 17.6%, translating to 14.2 million affected individuals who often lack access to laser treatment, leaving supplementation as an interim measure. Combination products blending omega-3s and coenzyme Q10 grew 34% in 2024-2025 because metabolic syndrome comorbidities intensify retinal oxidative stress. The American Diabetes Association’s 2025 care standards call for yearly retinal screening at diagnosis, indirectly endorsing early supplement uptake. Supplement demand therefore escalates in tier-2 cities where ophthalmologist density remains below one per 100,000 residents, filling a glaring care gap.

Adoption of Preventative-Health Mindset Among Gen Z and Millennials

Consumers aged 25–40 made up 41% of purchases in 2025 as daily screen exposure averaged 11 hours during remote work. Ingredient transparency matters; 68% will pay a 25% premium for NSF-verified labels[2]Council for Responsible Nutrition, “2024 Consumer Survey on Dietary Supplements,” crnusa.org. Social media amplified demand—TikTok eye-health hashtags amassed 2.3 billion views in 2024, and influencer content drove 29% of first-time buys. Gummies captured 18% of this cohort’s spending against 9% for baby boomers, demonstrating taste preferences that shape product formats. Early lutein and zeaxanthin adoption before symptom onset differentiates this demographic from older groups that initiate supplementation only after diagnosis.

Surge in Self-Directed Eye-Care via E-Commerce Nutraceuticals

DTC brands cut customer acquisition costs to USD 18 in 2025 by targeting precise search queries, down from USD 27 in 2023. Subscription models triple lifetime value relative to single-purchase buyers while permitting 15% price discounts that still protect 38% gross margins. Amazon sales expanded 31% in 2024, with private-label products using AREDS2 profiles priced at half of branded equivalents. Tele-optometry portals convert 14% of virtual exams into supplement sales by pairing personal recommendations with one-click checkout. Regulatory gray zones around structure-function claims on e-commerce listings let 63% of top sellers suggest disease benefits without FDA pre-approval, accelerating online channel growth.

Clinical Validation of Carotenoid + Omega-3 Synergistic Formulations

The 10-year AREDS2 follow-up showed that adding 1 gram of EPA/DHA to 10 mg lutein and 2 mg zeaxanthin cut progression to advanced AMD by 26%. Co-encapsulation raised combined bioavailability by 34% while protecting against oxidation during shelf storage. EFSA confirmed a vision-maintenance claim for lutein and zeaxanthin in 2024, allowing targeted messaging across EU markets. Yet 41% of 2025 commercial SKUs contained subtherapeutic carotenoid doses below 6 mg, undercutting real-world effectiveness. Brands that align with validated ratios differentiate on efficacy as well as trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scientific controversy over supplement efficacy & lack of reimbursement | -0.9% | Global, particularly impacting North America and Europe | Medium term (2-4 years) |

| Price volatility of key marine-sourced omega-3 inputs | -0.7% | Global, supply concentrated in Peru and Norway | Short term (≤ 2 years) |

| Counterfeit & adulterated products eroding consumer trust | -0.6% | Global, acute in Asia-Pacific and online channels | Medium term (2-4 years) |

| Stringent cross-border novel-food rules for high-dose carotenoids | -0.5% | Europe, Asia-Pacific (China, India), with spillover to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scientific Controversy Over Supplement Efficacy and Lack of Reimbursement

A 2024 Cochrane review of 19 trials reported no significant benefit from lutein or zeaxanthin against cataract progression, reducing clinician endorsement. Medicare Part D continued to exclude eye supplements from formularies in 2025, classifying them as wellness products. Out-of-pocket costs deterred 34% of AMD patients from starting supplementation, according to an American Academy of Ophthalmology survey. Ophthalmologists cite permissive FDA structure-function rules as misleading because products can claim eye support without pre-market efficacy proof. Without payer backing, pharmaceutical firms avoid prescription-grade pathways, limiting innovation beyond over-the-counter formulas.

Price Volatility of Marine-Sourced Omega-3 Inputs

Peruvian anchovy landings fell 29% in 2024 after El Niño disrupted spawning, raising crude fish-oil prices to USD 2,850 per ton in Q3 2024. Norwegian herring and mackerel increases met only 62% of pharmaceutical-grade demand, sustaining tight supply. Brands depending solely on anchovy oil saw cost of goods sold jump 19% year-over-year, forcing dosage cuts that risk consumer backlash. Futures for 2026 delivery at USD 2,950 per ton suggest persistent strain as climate models predict continued El Niño through mid-2027. Formulators blending algal DHA partially insulated margins, yet the restraint still trims growth projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type Carotenoids Extend Growth Runway

Omega-3 fatty acids commanded 29.55% revenue in 2025, but carotenoids are forecast to deliver the fastest 9.85% CAGR because rising macular pigment scores link directly with 0.12 logMAR visual-acuity gains in early AMD cases. High-purity lutein pricing—USD 180 per kilogram in 2025—helps private labels compete while still funding quality testing. Antioxidant vitamins face falling margins as commoditized ascorbic acid prices declined 14% since 2023. Minerals such as zinc and copper keep stable volume but reformulate into chelated formats after 22% of users reported gastrointestinal discomfort at standard zinc dosages.

Botanical and polyphenol innovation is advancing category differentiation. Bilberry extract at 25% anthocyanins improved night-vision adaptation by 18% among Italian military pilots. Astaxanthin attracted mainstream attention in 2025, with 12 mg daily reducing accommodative decline by 0.8 diopters among presbyopic adults. Multi-ingredient blends accounted for 68% of 2024 launches, as brands layer carotenoids, omega-3s, and botanicals to command premiums. The United States Pharmacopeia’s 2024 monographs for lutein and zeaxanthin raised compliance costs but also enabled trust-building label claims.

By Form Gummies Challenge Capsule Leadership

Softgel capsules retained 45.53% revenue in 2025 by safeguarding shelf life up to 36 months. Yet gummies and chews posted a 10.75% CAGR due to pectin matrices that mask fishy aftertaste while delivering 87% bioequivalence to softgels. The format appeals to dysphagia patients and children, with pediatric gummies capturing 31% of under-12 spending in 2025.

Tablets are retreating as slow disintegration undermines lipophilic payloads, although effervescents are gaining traction in Europe for faster dissolution. Powders attract fitness consumers seeking custom blends, while liquids represent a premium niche at under 5% share but 40% higher price points. Capsule makers have introduced chewable softgels, though broad acceptance remains untested.

By Indication Myopia Progression Creates Pediatric Upside

AMD maintained 39.15% of 2025 revenue, reflecting 196 million global cases. Myopia progression, however, is projected to record a 10.82% CAGR as China’s pediatric prevalence reached 71.6% in 2024. Parental willingness to pay sustains comparable pricing even though myopia formulas use lower lutein doses than AMD products.

Cataract-oriented SKUs remain flat after a 2024 Cochrane review questioned efficacy. Dry-eye products doubled omega-3 dosage to 2 grams daily to address meibomian dysfunction that now affects 344 million adults. Diabetic-retinopathy blends use alpha-lipoic acid plus resveratrol, a format still under-represented at 9% of category sales despite 31% reductions in oxidative-stress markers in trials.

By Distribution Channel DTC Subscriptions Reshape Economics

Pharmacy and drug stores held 42.52% share in 2025, but year-on-year growth is slowing as younger shoppers shift online. DTC and other e-commerce outlets are set to rise 12.12% annually by using algorithmic targeting that converts searches such as “dry eye relief” into sales within 48 hours. Subscriptions lift repeat rates and justify discounted bundles, strengthening gross margins.

Clinic-dispensed SKUs command price premiums due to perceived professional endorsement, yet overall clinic channels remain a minority. Amazon’s private labels mirrored AREDS2 ratios at half the legacy brand price, forcing incumbents toward differentiated line extensions. Pharmacy chains are now responding with loyalty discount programs that pair supplements with prescription pick-ups.

By Age Group Pediatric Momentum Builds Alongside Senior Core

Adults represented 60.54% revenue in 2025 because AMD risk peaks in the 65-plus cohort, yet pediatric users will post a 9.32% CAGR amid the myopia epidemic. Gummies account for 73% of under-12 purchases due to taste and chewability, overcoming softgel compliance problems.

Geriatric loyalty is high once vision improvement is perceived; generic AREDS2 options gained traction after Medicare non-coverage pushed price-sensitive seniors toward lower-cost SKUs. Working-age adults now adopt preventative regimens tied to digital eye-strain awareness campaigns, expanding beyond symptom-driven usage.

Geography Analysis

North America captured 36.62% of 2025 revenue on the back of established clinician recommendations and high per-capita spending, yet penetration among diagnosed AMD patients already stands at 67%, slowing organic growth. Private-label SKUs and generic AREDS2 formulas appeal to cost-conscious seniors, while younger buyers migrate to DTC subscriptions that combine eye supplements with wellness bundles.

Asia-Pacific is projected to expand at an 8.72% CAGR through 2031 as China’s myopia crisis drives pediatric uptake and India’s diabetic retinopathy prevalence surges. Japan’s super-aged population allocates USD 47 per capita annually, second only to the United States, creating steady baseline demand[3]Statistics Bureau of Japan, “Population Estimates 2024,” stat.go.jp. South Korea’s 2024 school-based screening program now subsidizes lutein products, trimming retail prices by 40% and accelerating adoption.

Europe and other mature markets grow modestly under strict novel-food regulations that delayed high-dose astaxanthin until 2024. Middle East demand clusters in Gulf nations where diabetes prevalence exceeds 20%, supporting premium SKUs sold through private hospitals. South American consumption is rising in Brazil and Argentina as smartphone use raises digital-eye-strain awareness, while Africa remains nascent due to low public-sector access and limited ophthalmology capacity.

Competitive Landscape

The eye health supplement market remained fragmented in 2025, with the top five players holding a combined share indicative of moderate concentration as AREDS2 patent expiries permitted 47 new entrants to launch copycat blends priced 40% lower. Leaders such as Bausch + Lomb, BASF Nutrition & Health, and Kemin Industries sustain gross margins above 55% through vertical integration that spans carotenoid extraction to finished-product encapsulation. Contract manufacturers in India and China now achieve 92% purity lutein at USD 180 per kilogram, trimming incumbents’ cost advantage.

DTC insurgents like Performance Lab and Nuzena devote about 18% of revenue to targeted digital ads, capturing niches such as “floaters relief” that legacy brands overlook. White-space innovation is clustering around diabetic-retinopathy combinations of alpha-lipoic acid and resveratrol, yet only a handful of brands have moved beyond pilots despite clinical proof of a 31% oxidative-stress reduction. Technology adoption differentiates quality leaders: OmniActive introduced spectroscopy-based carotenoid verification in 2024, cutting batch rejections to 0.8% and enabling premium positioning.

Blockchain traceability emerged in 2025, with ZeaVision linking marigold harvests to finished goods on IBM Food Trust, slashing counterfeit incidents by 67%. Consolidation is accelerating; seven acquisitions totaling USD 890 million occurred in 2024-2025 as private equity firms aggregate regional brands to scale e-commerce infrastructure. Meanwhile, capacity expansions such as DSM-Firmenich’s 40% boost in South Carolina signal confidence in algal DHA’s mainstream adoption.

Eye Health Supplement Industry Leaders

Vitabiotics Ltd

Bausch Health Inc. ( Bausch & Lomb Incorporated)

Kemin Industries Inc.

ZeaVision (EyePromise)

Amway (Nutrilite)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Optivell released a vision-support formula positioned for digital lifestyles.

- January 2026: OCuSOFT introduced Retaine Omega Forté, a purified omega-3 product aimed at dry-eye sufferers.

- December 2025: Jubileye Health debuted Dry Eye & Glare Defense, a clean-label supplement for ocular comfort.

Global Eye Health Supplement Market Report Scope

As per the scope of the report, eye health supplements are ocular nutraceuticals, which include vitamins, proteins, fatty acids, and others that help in improving eye health and providing better vision. These supplements play a crucial role in vision by maintaining a clear cornea, protecting the eye from damage caused by free radicals, and reducing inflammation in the eyes.

The segmentation for the eye health supplements market is categorized by ingredient type, form, indication, distribution channel, age group, and geography. By ingredient type, the market includes carotenoids, antioxidant vitamins, omega-3 fatty acids, minerals, botanicals & polyphenols, and multi-ingredient blends. By form, it is segmented into softgel capsules, tablets, gummies & chews, powders & sachets, and liquid drops & shots. By indication, the market covers age-related macular degeneration (AMD), cataract, dry eye syndrome, diabetic retinopathy, glaucoma & ocular hypertension, myopia progression, and others. By distribution channel, it is divided into OTC pharmacy & drug stores, online retail & direct-to-consumer brands, and other distribution channels. By age group, the segmentation includes pediatric, adults, and geriatric. By geography, the market is analyzed across North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Carotenoids |

| Antioxidant Vitamins |

| Omega-3 Fatty Acids |

| Minerals |

| Botanicals & Polyphenols |

| Multi-ingredient Blends |

| Softgel Capsules |

| Tablets |

| Gummies & Chews |

| Powders & Sachets |

| Liquid Drops & Shots |

| Age-Related Macular Degeneration (AMD) |

| Cataract |

| Dry Eye Syndrome |

| Diabetic Retinopathy |

| Glaucoma & Ocular Hypertension |

| Myopia Progression |

| Others |

| OTC Pharmacy & Drug Stores |

| Online Retail & Direct-to-Consumer Brands |

| Other Disctribution Channels |

| Pediatric |

| Adults |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Ingredient Type | Carotenoids | |

| Antioxidant Vitamins | ||

| Omega-3 Fatty Acids | ||

| Minerals | ||

| Botanicals & Polyphenols | ||

| Multi-ingredient Blends | ||

| By Form | Softgel Capsules | |

| Tablets | ||

| Gummies & Chews | ||

| Powders & Sachets | ||

| Liquid Drops & Shots | ||

| By Indication | Age-Related Macular Degeneration (AMD) | |

| Cataract | ||

| Dry Eye Syndrome | ||

| Diabetic Retinopathy | ||

| Glaucoma & Ocular Hypertension | ||

| Myopia Progression | ||

| Others | ||

| By Distribution Channel | OTC Pharmacy & Drug Stores | |

| Online Retail & Direct-to-Consumer Brands | ||

| Other Disctribution Channels | ||

| By Age Group | Pediatric | |

| Adults | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the eye health supplements market be by 2031?

It is forecast to reach USD 4.23 billion by 2031, advancing at a 7.62% CAGR from 2026 to 2031.

Which ingredient segment is growing fastest within eye health supplements?

Carotenoids, led by lutein and zeaxanthin, are projected to post a 9.85% CAGR through 2031 due to strong clinical support for AMD and myopia prevention.

Why are gummies gaining popularity in vision-support products?

Pectin-based gummies now deliver 87% of softgel carotenoid bioavailability, eliminate gelatin allergens, and appeal to children and adults who dislike swallowing capsules.

What is driving online sales of eye health supplements?

Subscription-based DTC models lower acquisition costs, lock in 90-day refills, and exploit targeted search ads that convert symptom-related queries into immediate purchases.

Which region is expected to see the highest growth?

Asia-Pacific, propelled by China's pediatric myopia wave and expanding diabetic populations, is set to record an 8.72% CAGR to 2031.

Page last updated on: