Thyroid Eye Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

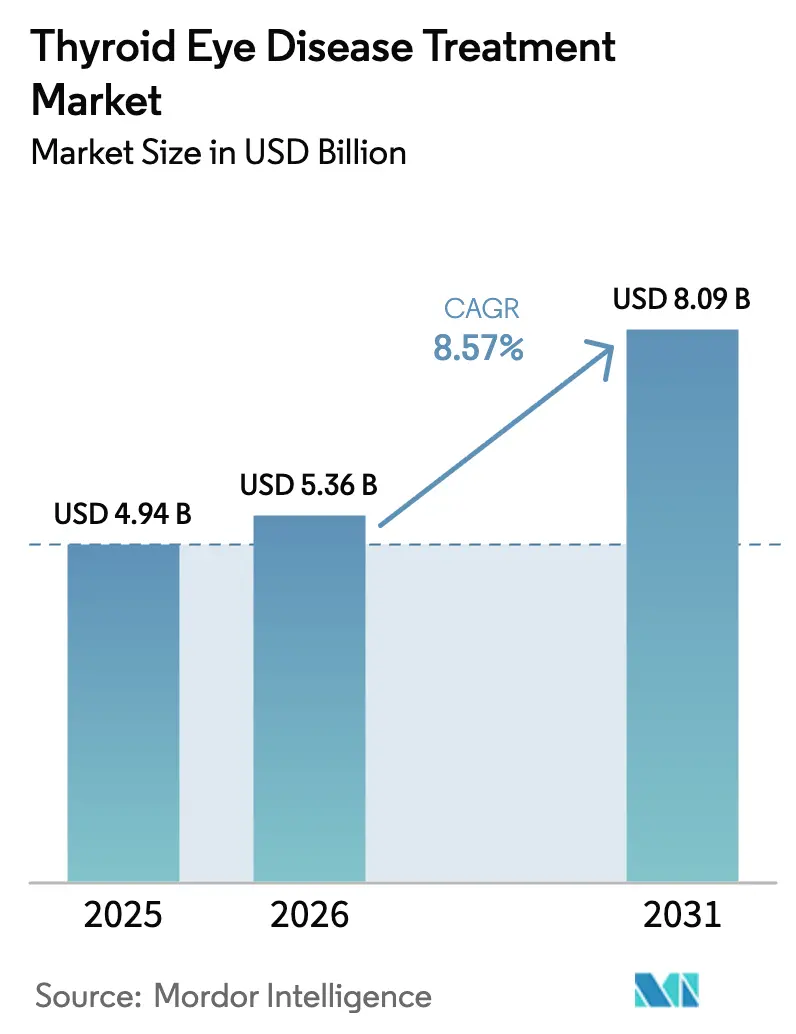

| Market Size (2026) | USD 5.36 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 8.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thyroid Eye Disease Treatment Market Analysis by Mordor Intelligence

Thyroid eye disease treatment market size in 2026 is estimated at USD 5.36 billion, growing from 2025 value of USD 4.94 billion with 2031 projections showing USD 8.09 billion, growing at 8.57% CAGR over 2026-2031. Clinical validation of insulin-like growth factor-1 receptor (IGF-1R) inhibition, rising global screening initiatives, and streamlined orphan-drug pathways are transforming a once treatment-scarce arena into a competitive landscape. Investor confidence has strengthened after landmark transactions such as Amgen’s acquisition of Horizon Therapeutics, while late-stage biologics with more convenient dosing schedules promise to expand patient access. Parallel progress in telemedicine, multidisciplinary clinic networks, and international regulatory harmonization is repositioning the thyroid eye disease treatment market for sustained double-digit growth in underserved regions[1]European Medicines Agency, “Tepezza: CHMP Opinion,” ema.europa.eu.

Key Report Takeaways

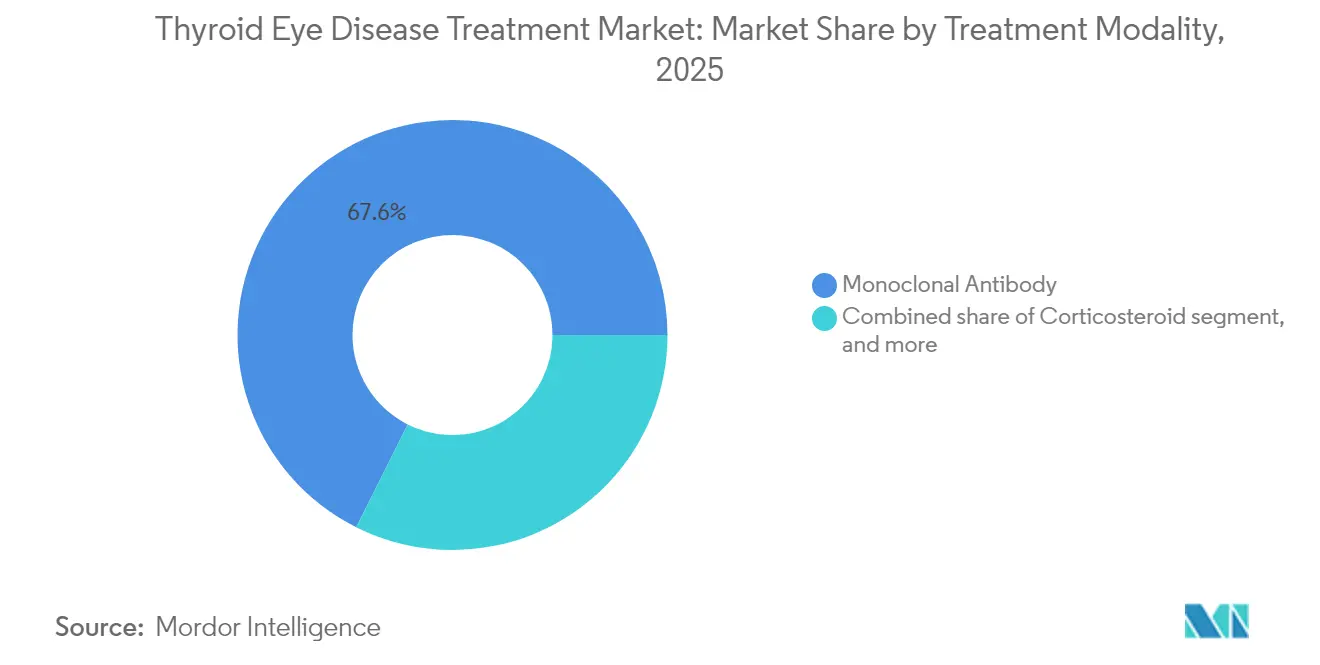

- By treatment modality, monoclonal antibodies led with 67.61% revenue share in 2025; subcutaneous and oral pipeline candidates are forecast to record the highest CAGR at 11.54% through 2031.

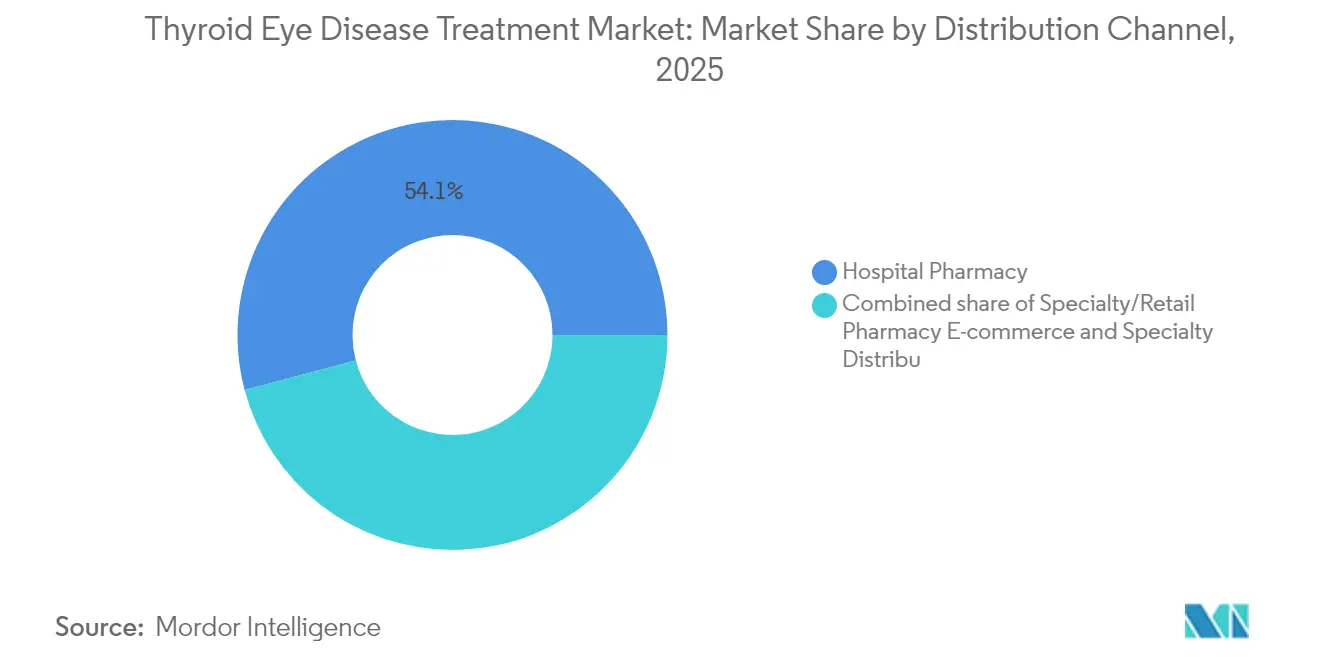

- By distribution channel, hospital pharmacies held 54.12% of the thyroid eye disease treatment market share in 2025, while e-commerce and specialty distributors are projected to expand at a 12.31% CAGR through 2031.

- By end user, tertiary-care hospitals commanded 48.92% share of the thyroid eye disease treatment market size in 2025, and specialty endocrine / ophthalmology clinics are advancing at an 11.08% CAGR to 2031.

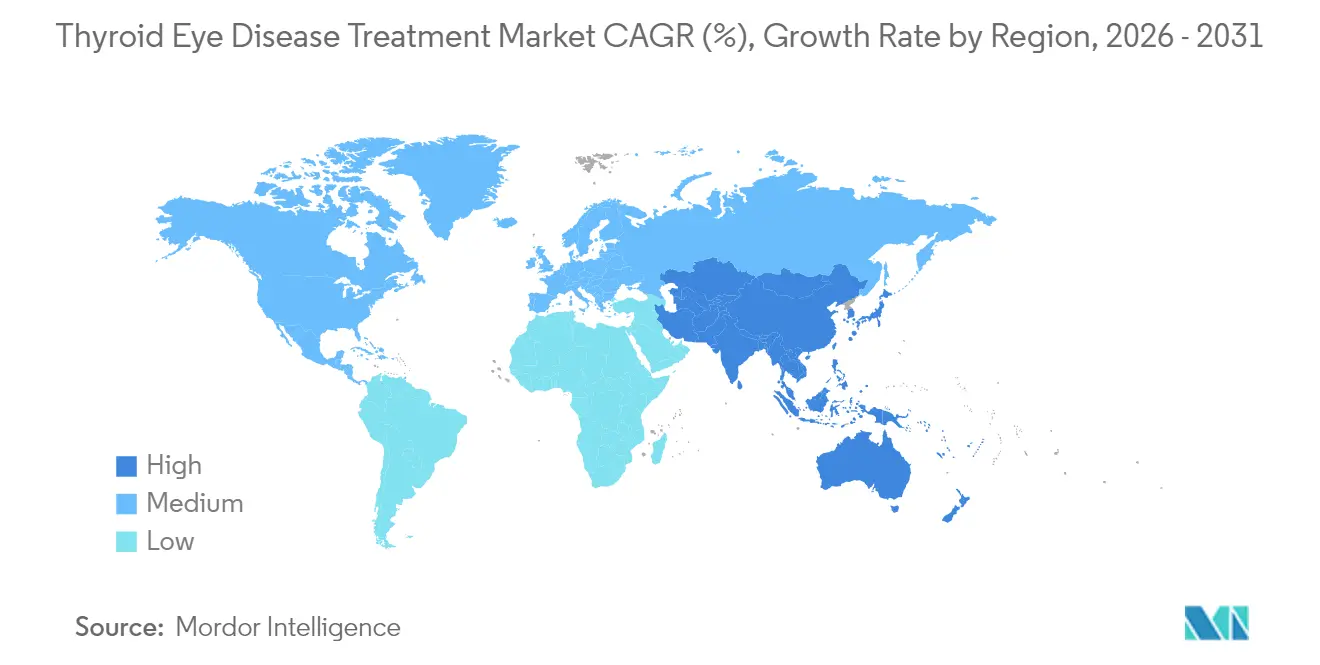

- By geography, North America accounted for 46.25% share in 2025; Asia-Pacific is set to grow the fastest at 10.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thyroid Eye Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Prevalence of Autoimmune Thyroid Disorders | 1.80% | Global, with higher concentration in North America & Europe | Long term (≥ 4 years) |

| Growing Awareness & Screening Programs for Thyroid Dysfunction | 1.50% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expansion Of Specialty Ophthalmology & Endocrinology Infrastructure | 1.20% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Favorable Orphan-Drug Incentives and Reimbursement Pathways | 2.10% | Global, with early gains in US, EU regulatory zones | Short term (≤ 2 years) |

| Advances In Biologic & Targeted Immunotherapy Platforms | 1.90% | Global | Long term (≥ 4 years) |

| Increasing Healthcare Expenditure on Vision-Saving Therapies | 1.40% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Prevalence of Autoimmune Thyroid Disorders

Thyroid eye disease (TED) accompanies 25–50% of Graves’ disease cases and now affects roughly 1 million people in the United States alone. Urban lifestyle stressors, smoking, and iodine intake shifts are intensifying autoimmune thyroid dysfunction rates, especially in high-income economies. Broader recognition of Hashimoto-linked eye involvement enlarges the treatable patient base and reinforces the growth outlook for the thyroid eye disease treatment market. Demographic aging in developed regions further lifts prevalence, aligning with health-system capacity to manage chronic immune-mediated conditions.

Growing Awareness & Screening Programs for Thyroid Dysfunction

Inter-society clinical guidelines between endocrinology and ophthalmology bodies have shortened average time-to-diagnosis from 18-24 months to roughly 6–12 months in specialized centers[2]American Academy of Ophthalmology, “Economic Impact of Early TED Treatment,” aao.org. Artificial-intelligence decision support embedded in primary care boosts early recognition of orbital changes, and tele-ophthalmology platforms extend specialist reach into rural areas. Earlier detection channels more patients into the active phase when biologic intervention yields maximal visual benefit, reinforcing uptake across the thyroid eye disease treatment market.

Favorable Orphan-Drug Incentives and Reimbursement Pathways

Breakthrough therapy and orphan-drug designations compress review timelines and confer up to seven years of exclusivity in major markets. Clear clinical end-points such as proptosis response simplify health-technology assessments, easing reimbursement hurdles. The resulting predictability underpins pipeline funding and supports accelerated launch strategies that expand the thyroid eye disease treatment market.

Advances in Biologic & Targeted Immunotherapy Platforms

Subcutaneous IGF-1R inhibitors like VRDN-003 offer 4–8 week dosing intervals versus the 3-week intravenous standard, boosting adherence and lowering infusion-center traffic[3]Viridian Therapeutics, “VRDN-003 and Veligrotug Clinical Updates,” viridiantherapeutics.com. Parallel research in IL-6 blockade, FcRn antagonists, and B-cell depletion widens mechanistic diversity, setting the stage for personalized combination regimens that may augment clinical response and durably modify disease.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Treatment Costs and Payer Budget-Impact Concerns | -1.60% | Global, with acute impact in price-sensitive markets | Short term (≤ 2 years) |

| Limited Availability Of TED-Trained Specialists | -1.10% | APAC, MEA, selective EU markets | Medium term (2-4 years) |

| Safety & Tolerability Challenges with Systemic Biologics | -0.80% | Global | Long term (≥ 4 years) |

| Regulatory Uncertainty Around Off-Label & Emerging Therapies | -0.70% | Global, with regional variation in approval timelines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs and Payer Budget-Impact Concerns

An average full-course biologic cost of USD 386,424 per patient, disclosed in company price filings, strains payer budgets. Prior-authorization processes extend beyond thirty days in many US plans, delaying therapy during the critical active disease window. In emerging economies, limited rare-disease budgets force tough resource allocation choices that restrict uptake and temper near-term expansion of the thyroid eye disease treatment market.

Limited Availability of TED-Trained Specialists

A survey by the American Society of Ophthalmic Plastic and Reconstructive Surgery found that fewer than 60% of TED patients are managed by a subspecialist. Urban clustering of expertise forces rural patients to travel long distances, adding indirect costs and contributing to under-treatment. Building human capital through fellowships and tele-mentoring is essential to unlock the next growth wave.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Modality: Biologics Sustain Segment Dominance

Monoclonal antibodies captured 67.61% of the thyroid eye disease treatment market share in 2025, underpinned by teprotumumab’s 83% proptosis responder rate documented in pivotal trials. Intravenous delivery and hospital-based monitoring supported robust adoption despite logistical complexity. Small-molecule immunosuppressants and orbital radiation retained niche roles for maintenance or refractory cases but collectively accounted for less than one-fifth of revenue.

Pipeline momentum centers on subcutaneous IGF-1R inhibitors and oral agents such as linsitinib, which achieved a 52% proptosis response in Phase 2b/3 testing. Subcutaneous formulations promise at-home administration every 4–8 weeks, a shift likely to redistribute value toward outpatient settings. As these candidates secure approval, they are expected to lift the segment CAGR above the overall market pace, deepening penetration among patients deterred by infusion burdens and reinforcing growth across the thyroid eye disease treatment market.

By Distribution Channel: Digital Pathways Disrupt Conventional Supply

Hospital pharmacies held 54.12 % of 2025 revenue because infusion-requiring biologics depend on institution-based cold-chain storage and specialist oversight. This dominance is projected to erode gradually as subcutaneous and oral therapies reach market, allowing prescriptions to migrate into community and home settings. Specialty distributors and e-commerce platforms are forecast to post a 12.31 % CAGR, benefiting from direct-to-patient fulfillment models, insurance navigation support, and adherence monitoring apps that strengthen retention.

Rising adoption of tele-ophthalmology consultations through networks such as Medii shortens diagnostic lag and aligns with home-delivery logistics. These parallel trends broaden access in remote regions, lower facility fees, and tighten supply-chain transparency, attracting manufacturers eager to secure consistent margins while expanding the reach of the thyroid eye disease treatment market.

By End User: Specialist Clinics Accelerate Patient-Centric Care

Tertiary-care hospitals generated 48.92% of 2025 revenue by offering comprehensive diagnostic imaging, infusion capabilities, and surgical backup. They also host clinical trials that refine treatment algorithms and facilitate early access programs. However, patient throughput is limited by scheduling bottlenecks and high overhead.

Specialty endocrine and ophthalmology clinics are predicted to grow at an 11.08% CAGR, empowered by streamlined care pathways and lower capital intensity. Purpose-built infusion suites, coupled with emerging subcutaneous options, enable higher visit volumes and shorter chair times, enhancing economic viability. As these clinics expand regionally, they underpin decentralization of care, boosting convenience for patients and reinforcing the long-term expansion of the thyroid eye disease treatment market.

Geography Analysis

North America maintained a 46.25% revenue share in 2025, reflecting early FDA approval of teprotumumab and widespread insurance coverage. Integrated academic networks supply real-world evidence that steadily increases physician comfort with biologics. The thyroid eye disease treatment market size for North America is projected to reach USD 3.73 billion by 2031, supported by continuous pipeline launches and an aging population.

Europe entered a new growth phase when the European Medicines Agency backed teprotumumab approval in April 2025, initiating country-level pricing negotiations. National health-technology assessments scrutinize cost-effectiveness but tend to green-light therapies that prevent vision loss. Robust research infrastructure facilitates post-marketing surveillance, critical for uptake under outcome-based reimbursement schemes. As local centers emulate US specialty-clinic models, regional penetration should accelerate, especially in Germany, France, and the Nordics.

Asia-Pacific is on track for the fastest regional CAGR of 10.22% through 2031, propelled by rapidly modernizing healthcare systems and increasing endocrinology capacity. Japan already covers teprotumumab under its national insurance, while partnerships such as Amgen-Medii equip clinicians with teleconsultation tools for remote TED management. China and India remain cost-sensitive but are piloting orphan-drug funds that could unlock broader access. Rising autoimmune-disease incidence linked to urban stress and lifestyle change adds further momentum, positioning the thyroid eye disease treatment market for significant scale-up in the region.

Competitive Landscape

The thyroid eye disease treatment industry remains moderately concentrated. Amgen’s control of teprotumumab following its USD 27.8 billion Horizon Therapeutics acquisition established a clear market leader with extensive commercial infrastructure. Yet competitive pressure is intensifying as five Phase 3 programs approach submission. Viridian Therapeutics secured Breakthrough Therapy designation for veligrotug after delivering 70% proptosis response in active TED and 56% in chronic disease, signaling a credible rival entry point.

Innovation is coalescing around three strategic levers. First, differentiated formulations such as long-acting subcutaneous injections promise superior patient convenience. Second, alternative mechanisms including FcRn inhibition aim to broaden the responder pool. Third, companies are bundling therapeutics with digital-health services to streamline care coordination. Early examples include AI-driven symptom trackers integrated into specialty-pharmacy workflows that flag non-adherence proactively.

Competition is also expanding geographically. Domestic biotechs in Japan and China are advancing IGF-1R and IL-6 candidates, leveraging regional clinical-trial networks for rapid enrollment. Multinational firms increasingly partner with local distributors to navigate complex reimbursement systems while securing data exclusivity. These dynamics suggest that the thyroid eye disease treatment market will remain innovation-driven, with share shifts dictated by demonstrable gains in efficacy, convenience, and affordability.

Thyroid Eye Disease Treatment Industry Leaders

F. Hoffmann-La Roche Ltd

Amgen Inc.

Novartis AG

Viridian Therapeutics Inc.

Immunovant Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Viridian Therapeutics received FDA Breakthrough Therapy designation for veligrotug after 70% proptosis response in active disease and 56% in chronic cases.

- April 2025: The European Medicines Agency recommended marketing authorization for Tepezza (teprotumumab) for adults with moderate-to-severe thyroid eye disease.

- February 2025: Viridian Therapeutics launched global Phase 3 trials (REVEAL-1 and REVEAL-2) for VRDN-003, a subcutaneous anti-IGF-1R therapy dosed every 4–8 weeks.

- January 2025: Sling Therapeutics announced positive Phase 2b/3 LIDS results for oral linsitinib, showing 52% proptosis responders at 150 mg BID.

- December 2024: Viridian Therapeutics reported that the Phase 3 THRIVE-2 trial of veligrotug in chronic TED met all endpoints with 56% proptosis and diplopia response rates.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the thyroid eye disease (TED) treatment market as all prescription-grade pharmacologic therapies, biologics, systemic or locally delivered immunosuppressants, corticosteroids, small-molecule IGF-1R inhibitors, and adjunct orbital radiation administered for active or chronic TED episodes worldwide.

Scope exclusion: purely cosmetic orbital decompression surgery and over-the-counter lubricants are not tracked.

Segmentation Overview

- By Treatment Modality

- Monoclonal Antibody

- Small-Molecule Immunosuppressant (Mycophenolate, Sirolimus)

- Corticosteroid (IV, Oral, Local Injection)

- Orbital Radiation Therapy

- Other Treatment Modalities

- By Distribution Channel

- Hospital Pharmacy

- Specialty/Retail Pharmacy

- E-commerce & Specialty Distributors

- By End User

- Tertiary-Care Hospitals

- Specialty Endocrine/Ophthalmology Clinics

- Ambulatory Surgery Centers

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed endocrinologists, oculoplastic surgeons, payers, and specialty-pharmacy managers across North America, Europe, and Asia-Pacific. These discussions clarified real-world dosing adherence, emerging subcutaneous biologic pricing, and country-level reimbursement triggers, allowing us to reconcile desk findings and fine-tune adoption ramps.

Desk Research

We began by mapping the patient and therapy universe through freely accessible tier-1 datasets such as WHO Global Health Estimates, National Eye Institute epidemiology briefs, Eurostat hospital discharge files, and customs trade codes for monoclonal antibody imports. Clinical-trial portals, peer-reviewed journals, and association white papers (e.g., American Thyroid Association) helped us size treated-case pools and typical dosing schedules. Company 10-Ks, D&B Hoovers financials, FDA/EMA approval dockets, and Dow Jones Factiva news feeds then grounded average selling prices, launch timelines, and regional uptake curves. These references illustrate the range of inputs; many additional public and paid sources fed the model.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-cohort build was applied. Diagnosed TED cases, treatment eligibility ratios, and therapy penetration rates produced volume pools, which were valued with region-specific ASP lines. Supplier roll-ups and sampled hospital charge data provided a bottom-up cross-check before values were locked. Key variables include biologic course completion rates, biologic-to-steroid switching trends, average vial strength, currency shifts, and regulatory approval cadence. Multivariate regression, validated by expert consensus, projects each driver to 2030; scenario testing covers pricing resets and second-to-market launches.

Data Validation & Update Cycle

Outputs pass variance checks against independent hospital billing panels and import data, followed by a two-level analyst review. Reports refresh annually, and interim updates are triggered by material events such as new biologic approvals.

Why Mordor's Thyroid Eye Disease Treatment Baseline Stands Firm

Published estimates differ because firms vary study geographies, include only biologics, or freeze assumptions for years. Mordor's disciplined scope alignment, dual-path modeling, and yearly refresh make our baseline dependable for budget planning.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.94 B (2025) | Mordor Intelligence | - |

| USD 2.26 B (2024) | Regional Consultancy A | Focuses on 7 major markets, omits radiation therapy revenue |

| USD 2.71 B (2025) | Global Consultancy B | Counts biologics only; excludes hospital-billed steroids |

| USD 0.17 B (2025) | Industry Journal C | Models mild TED medication segment alone, conservative ASPs |

In short, while other publishers narrow definitions or rely on single-source price decks, Mordor's balanced, transparent build, anchored in broad treatment modalities and refreshed inputs, offers decision-makers the most reliable TED market view today.

Key Questions Answered in the Report

What is the current size of the thyroid eye disease treatment market?

The thyroid eye disease treatment market size is USD 5.36 billion in 2026 and is forecast to reach USD 8.09 billion by 2031.

Which treatment modality leads the market today?

Monoclonal antibodies dominate with 67.61% revenue share in 2025, primarily due to teprotumumab’s strong clinical performance.

Why is Asia-Pacific expected to grow the fastest?

Healthcare modernization, expanding endocrinology capacity, and increased autoimmune-disease awareness drive a 10.22% CAGR in Asia-Pacific through 2031.

How are new delivery formats changing patient care?

Subcutaneous IGF-1R inhibitors and oral small-molecule therapies reduce reliance on hospital infusions, improving convenience and broadening access.

What factors could restrain near-term growth?

High drug prices, limited specialist availability, and payer budget pressures may slow uptake, especially in cost-sensitive regions.

Who are the key emerging competitors?

Viridian Therapeutics, Immunovant, and Sling Therapeutics are advancing late-stage programs that could challenge Amgen’s leadership over the next five years.

Page last updated on: